DOJ To Declassify ‘The Backbone’ Of Mueller Investigation With Monthly Document Dumps

The Department of Justice will release to the public approximately 500 pages of FBI ‘302’ witness interview forms per month, according to CNN – which sued the DOJ along with co-plaintiff BuzzFeed News under the Freedom of Information Act (FOIA).

The documents, known as 302s, memorialize interviews conducted by the office and form the backbone of much of the Mueller report. –CNN

The government has until November 1 to product the first tranche of documents, according to a fuling by federal Judge Reggie B. Walton in Washington DC.

The Mueller investigation initially sought to determine whether the Trump campaign ‘colluded’ with the Russian government during the 2016 US election, along with whether President Trump attempted to obstruct the FBI’s efforts. In his report, released April 18, Mueller’s team was unable to establish any conspiracy, while declining to render an opinion on ten instances of potential obstruction. Ultimately, Attorney General William Barr and Deputy Attorney General Rod Rosenstein determined that obstruction had not occurred.

According to DOJ attorney Courtney Enlow at a Tuesday morning hearing, a total of 800 302 forms were generated during the Mueller probe, potentially numbering around 44,000 pages – which are now subject to a release rate of 500 per week.

Enlow said the FBI had already begun to process the records but said a host of potential exemptions that had to be considered before their release, including national security implications, certain privileges, and exposure to ongoing prosecutions and investigations.

“We have been going through 302s line by line,” Enlow said. “It’s a very intensive process.“

The future production schedule for the remaining interview forms, as well as other records requested by the news outlets, is a matter of contention. –CNN

Judge Walton criticized the incredibly slow declassification, only for the Enlow to respond that the pace was ‘routine’ for the FBI.

Walton will also rule on a request by next month for the release of an unredacted version of the Mueller report, when another status hearing has been scheduled in the cases.

The releases of genetically-modified organisms (GMOs) into the natural environment is having a catastrophic and irreversible impact on our planet. A company known as Oxitec, based out of the United Kingdom, which had announced plans to release genetically-engineered, or transgenic, mosquitoes into the wild.

Oxitec’s stated goal was to eradicate native mosquito populations carrying potentially deadly diseases like Zika by infiltrating their ranks with transgenic impostors. These impostor mosquitoes, we were told, do not have the ability to reproduce, and thus pose no risk of causing long-term changes to the natural ecosystem, according to a report by Natural News.

What could possibly go wrong?

However, it appears that Oxitec was wrong about their GMO mosquitoes. As revealed in a new study, which was published in the esteemed journal Nature,Oxitec’s transgenic mosquitoes are not only able to reproduce, but their presence within native mosquito populations is actually causing super-mosquitoes to spawn. The world will have to face an onslaught of super-mosquitoes that are more resilient than the ones that previously existed in nature.

“To summarize the findings of the study, this mad science GMO experiment managed to create a super mutant population of mosquitoes that now carry genes that are potentially tied to enhanced insecticide resistance, making them harder to kill than ever before,” MikeAdams wrote for Natural News.

“The experiment utterly failed to achieve its promised outcome of wiping out mosquitoes, too.”

Failure is an understatement. Since the goal was a decrease in the mosquito populations that carry infectious diseases, this quote from the conclusion of the study bears mentioning:

The results of our tests of the infectivity of one strain each of the dengue and Zika viruses in females of the OX513A strain and the Jacobina natural population (before releases) indicate no significant differences (Fig. 3). –Nature

The mosquitoes are still carrying infectious diseases at the same rate as before the GMO mosquitoes were released. The study states that this whole plan broke down because the natural female mosquitoes prefer to mate with male mosquitoes that were known to be fertile, and not the infertile GMO mosquitoes released by Oxitec.

Judge Rules Harvard Can Keep Discriminating Against Asians Using ‘Race-Conscious Admissions’

A federal judge has decided in favor of Harvard University, ruling that the college can continue using Obama-era “race-conscious” affirmative action policies designed “to promote diverse educational settings,” according to NPR.

Federal District Court Judge Allison D. Burroughs issued her decision Tuesday, saying, “Harvard’s admission program passes constitutional muster,” and that “ensuring diversity at Harvard relies, in part, on race conscious admissions.“

The plaintiff, advocacy group Students for Fair Admissions, accused Harvard of discriminating against Asian-American applicants. It argued the school considers race too much, forcing Asian-Americans to meet a higher bar to get in. –NPR

The plaintiffs, Students For Fair Admissions (SFFA), are likely to appeal the case which may make it all the way to the Supreme Court. They have alleged that based on their analysis, Asian-American applicants receive Harvard’s lowest subjective personal rating scores, while consistently achieving the highest academic and extracurricular ratings of any other racial group. The personal rating is in part based on teacher recommendations, personal essays and admissions interviews, according to Harvard.

Last August, the Department of Justice lent its support to SFFA – concluding that Harvard’s use of a “personal rating” system violates the law, and that the college failed to demonstrate how its use of the system is narrowly tailored to suit a competing interest.

“Harvard acknowledges that it voluntarily uses race as a factor in deciding whether to offer certain young adults admission to, and the substantial educational benefits of, its elite institution,” reads the DOJ brief. “Harvard seeks to justify this use of race to award educational opportunities as necessary to its pursuit of the ‘educational benefits of diversity.’ But Harvard has failed to carry its demanding burden to show that its use of race does not inflict unlawful racial discrimination on Asian Americans.”

Over the summer, the DOJ and Department of Education began jointly directing schools to adopt race-neutral admissions standards – reversing the Obama-era guidance encouraging the use of race to promote diversity.

Never mind all that – for now. Harvard successfully argued that the lawsuit should be tossed because the case was founded on “invective, mischaracterizations and in some cases outright misrepresentations,” adding that the judge should rule in their favor since the lawsuit is nothing but a “litigation vehicle” to advance the ideological objectives of the plaintiffs’ group, led by Edward Blum.

As the exodus gathers momentum, all the reasons people clung so rabidly to urban meccas decay.

If there is any trend that’s viewed as permanent, it’s the enduring attraction of coastal urban meccas: despite the insane rents and housing costs, that’s where the jobs, the opportunities and the desirable urban culture are.

Nice, but like many other things the status quo considers permanent, this could reverse very quickly, and all those pricey urban meccas could become crime-ridden ghost towns. How could such a reversal occur?

1. Those in the top 10% who can leave reach an inflection point and decide to leave. The top 1% who live in enclaves filled with politicians, celebrities and the uber-wealthy see no reason to leave, as the police make sure no human feces land on their doorstep.

It’s everyone who lives outside these protected enclaves, in neighborhoods exposed to exasperating (and increasingly dangerous) decay who will reach a point where the “urban lifestyle” is no longer worth the sacrifices and costs.

It might be needles and human feces on the sidewalk, it might be petty crime such as your mail being stolen for the umpteenth time, it might be soul-crushing commutes that finally do crush your soul, or in Berkeley, California, it might be getting a $300 ticket for not bringing your bicycle to a complete stop at every empty intersection on a city bikeway. (I’ve personally witnessed motorcycle officers nailing dozens of bicyclists with these $300 tickets.)

It might be something that shreds the flimsy facade of safety and security complacent urban dwellers have taken for granted, something that acts as the last grain of sand on the growing pile of reasons to get the heck out that triggers the decision.

Not everyone can move, but many in the top tier can, and will. Living in a decaying situation is not a necessity for these lucky few, it’s an option.

2. Those who have to leave when they lose their job. A funny thing happens in all economies, even those with central banks: credit-cycle / business-cycle recessions are inevitable, regardless of how many times financial pundits say, “the Fed has our back” and “don’t fight the Fed.”

As I’ve noted here numerous times, a great many small businesses in these pricey urban meccas are one tiny step from closing: one more rent increase, one more bad month, one more regulatory burden, one more health issue and they’re gone. They will move to greener pastures for the same reason as everyone else–they can’t afford to live in urban meccas.

Once enough of the top 10% leave (by choice or because they can no longer afford it), the food/beverage service industry implodes. Wait staff and bartending have been a major source of jobs in these urban meccas, and when hundreds of struggling establishments fold due to a 10% decline in their sales, thousands of these employees will lose their jobs and the prospects of getting hired elsewhere decline with every new closure.

The vast majority of these service employees are renters, paying sky-high rents that unemployment can’t cover. They will hang on for a few months and then cash in their chips and move to more affordable climes.

3. Once the stock market returns to historic norms, the gargantuan capital gains that supported local tax revenues and spending dry up. WeWork is the canary in the coal mine; from a $50 billion IPO to insolvency in six weeks.

Once tax revenues plummet (no more IPOs, hundreds of restaurants closing, etc.), cities and counties will have to trim their workforces to maintain their ballooning pension payments for retirees. This will leave fewer police and social workers available to deal with everyone with little motivation (or option) to leave: thieves, those getting public services and the homeless.

4. Housing prices and rents are sticky: sellers and landlords won’t believe the good times have ended, and so they will keep home prices and rents at nosebleed valuations even as vacancies soar and the market is flooded with listings.

Neighborhoods that had fewer than 100 homes for sale will suddenly have 500 and then 1,000, as sellers realize the boom has ended and they want out–but only at top-of-the-bubble prices.

Ironically, this stubborn attachment to boom-era prices for homes and rents accelerates the exodus. As incomes decline, costs remain sky-high, so the only option left is to move away, the sooner the better.

By the time sellers grudgingly reduce prices, it’s too late: the market has soured. The Kubler-Ross dynamic is in full display, as sellers go through the stages of denial, anger, bargaining and acceptance: they grudgingly drop the price of the $1.2 million bungalow or flat to $1.15 million, then after much anger and anguish, to $1.1 million, but the market has imploded while they processed a reversal they didn’t think possible: now sales have dried up, and prices are sub-$800,000 while they ponder dropping their asking price to $995,000.

Vacant apartments pile up, as the number of laid-off and downsized employees who can still afford high rents collapses. (Recall that tens of thousands of recent arrivals in urban meccas rely heavily on tips for their income, and as service and gig-economy business dries up, so do their tips.)

5. As the exodus gathers momentum, all the reasons people clung so rabidly to urban meccas decay: venues and cafes close, street life fades, job opportunities dry up, and yet prices for everything remain high: transport, rent, taxes, employees, etc.

Friends move away, favorite places close suddenly, streets that were safe now seem foreboding, and all the friction, crime, grime and dysfunction that was once tolerable becomes intolerable.

6. In response to deteriorating city and county finances, local government jacks up fees, tickets, permits and taxes, accelerating the exodus. How many $300 tickets, fees and penalties does it take to break the resolve to stick it out?

7. Those on the cusp cave in and abandon the mecca. Once those who had the option to leave have left, and those who can no longer afford to stay leave, the decay causes those on the cusp of bailing out to abandon ship.

Renters move out in the middle of the night, homeowners who have watched their equity vanish as prices went into freefall jingle-mail the keys to the house to the lender and small businesses that had clung on, hoping for a turn-around close their doors.

8. Each of these dynamics reinforce the others. Soaring taxes, decaying services, declining business, rising insecurity and stubbornly high costs all feed on each other.

And that’s how pricey urban meccas turn into ghost towns inhabited by those who can’t leave and those living on public services, i.e. those too poor to support the enormously costly infrastructure of public spending in the urban mecca.

The lifestyle you ordered is not just out of stock, the supplier closed down.

VC Veterans Host Emergency Meeting Of Unicorns As IPO ‘Bubble’ Implodes

Recently, we have uncovered evidence that the proverbial tide is going out and also determined who is swimming naked.

SoftBank Vision Fund is one of those without a bathing suit, caught in a bind over several of its investments that are imploding, WeWork and Uber are to name a few.

Last week the Peloton IPO collapsed, turned out to be one of the worst opening trades for a unicorn IPO since 2008.

Now top venture capitalists, who are primarily based on the West Coast, are hosting an emergency meeting on Tuesday, invited more than 100 startups that will be advised not to IPO in the year ahead but rather use direct listings, considering numerous IPO failures seen this year.

Benchmark Capital partner Bill Gurley, one of the organizers of Tuesday’s meeting, told Reuters that two dozen venture capital firms would be advising more than 100 startups on how to go public in 2020.

Gurley said technology startups would need a more reliable alternative to the traditional IPO underwritten by investment banks, especially since what has happened to the latest IPO disasters: Peloton, Uber, and Lyft.

He warned of investment banks, like Goldman Sachs and JPMorgan, who have been “fleecing” companies by intentionally underpricing shares on IPO day. The ability to underprice then pop the new issuance enables the investment bank’s clients to make a quick gain.

Reuters notes that “underpriced IPOs provide the company less capital and diminish valuations for early investors such as venture capital backers, and any investors or employee stockholders who sell in the offering do not realize full value for their stakes.”

David Golden, a retired JP Morgan banker who is now managing partner at Revolution Ventures, said price action on IPO day doesn’t determine the whole story.

“If in the first few days of trading it doubles because there’s all this retail sentiment … and then it trickles down over the next two, three months, maybe even four months, then they probably priced the deal right,” said Golden.

Golden said direct listings could be the right solution for technology startups that don’t need to raise capital.

Venture capitalist sources told Reuters that Airbnb Inc is likely slated for a direct listing in 2H20.

Gurley said investment banks popping the stock on the first day is a market failure: “Giving away five hundred million dollars in one day – it’s really hard to justify.”

And here’s Gurley in 2016 when he spoke with CNBC’s Carl Quintanilla and Jon Fortt at the Code Conference about the “culling of the Silicon Valley herd,” his prediction of a bust cycle in Silicon Valley was likely three years too early.

With the IPO market bust underway, venture capitalists are now resorting to direct listings to dump worthless unicorns onto unsuspecting retail.

Regarding that classic dangerous journey, you have heard me describe it many times but, at the risk of boring you, I will repeat it. I believe that we are on a classic journey that we haven’t seen in our lifetimes but has happened many times before, most recently in the late 1930s.

It is being driven by the same big forces that drove the dynamics in the late 1930s. In particular, now, like in the late 1930s and unlike any period since, these three big forces are converging.

They are:

The largest wealth and political gaps since the late 1930s exist, which is leading to the emergence of and conflicts between populists of the left and populists of the right. If history and logic are to be our guides, it seems reasonable to worry that the gaps between the rich and the poor and the populists of the left and the populists of the right will become more war-like and that the consequences of their fighting could undermine the efficient operation of the economy as well as the efficient running of government. History has shown, logic suggests, and what seems to be happening is that the greater conflict leads to a) the reduced respect for both law and the art of compromise by our political leaders, and b) the increased testing of relative powers and the increased use of “emergency powers” to gain and use more power than these acts were intended for. It is likely that the upcoming US elections will be the greatest ideological clash that we have seen in our lifetimes, approaching the extreme fascist-communist clashes of the 1930s. It is likely that after the election there will be many more conflicts, tax law changes, and wealth redistributions that will have big implications for markets and economies.

There is limited ability of the world’s reserve currency central banks to stimulate the economy in the event of an economic downturn. When I imagine what the next economic downturn will be like with the social and political polarity that now exists, I expect it will be socially and politically ugly and that some form of “Monetary Policy 3” (see this May 2019 article) will have to happen or the economic depression won’t be rectified. To implement MP3-type monetary policy will require very large fiscal spending and large budget deficits that will have to be funded by a) substantially increased taxes on companies and the rich, and b) the printing of money by central banks and the buying of the debts that are coming from the deficits. Typically, this has led to capital flight as investors seek to escape these things, which has quite often led to capital controls that are intended to keep capital in the country and the currency so that it can more easily be taxed and/or devalued. So, naturally, I can’t help but wonder whether this extraordinary (i.e., nothing like this has happened in my lifetime) deviation from convention to restrict capital flows to China could be followed by these other steps when/if the circumstances that I’m describing unfold.

There is a rising power (China) challenging the existing world power (the US), which will probably lead to more conflicts between them about many different issues. History has shown that this situation has led to the increased risk of wars that typically come in four forms: trade wars, capital wars, technology wars, and geopolitical wars. As far as the trade wars go, you can see them for yourself (so I won’t delve into them) and probably have yourself drawn comparisons with the Smoot-Hawley Tariffs in 1930 and with various tariffs in several countries during the 1930s. Regarding the capital and currency wars, the ability of the US president to unilaterally cut off capital flows to China and also freeze payments on the debts owed to China and also use sanctions to inhibit non-American financial transactions with China must be considered as possibilities. That’s why the proposed step of limiting American portfolio investments in China makes me both think about the implications of this step and wonder if it is an inching toward bigger moves.

For perspective about what can be done and how it would be done, one can look at the US freezing of Japanese assets and embargoing of oil to Japan in the late 1930s to early ‘40s; they show how the use of special emergency powers gives the president the ability to do these things. Emergency powers today are most accessible to the president under the International Emergency Economic Powers Act of 1977 (IEEPA). It empowers the president to unilaterally impose capital and FX controls, freeze assets and/or payments on assets (coupons), and force asset divestures to “deal with any unusual and extraordinary threat” from outside the US to “the national security…economy of the United States.” Just the realization that these moves can be used has important implications for capital flows. For example, how would you feel if you were an adversarial foreign investor holding US bonds given this situation, given where US bond interest rates are and the impending deficits and monetizations of them? Of course, China dumping US bonds would have its own terrible consequences too. In any case, from not having to worry about such things in the past, now all market participants need to worry about them.

Regarding the technology war, we have seen the tip of the spear with Huawei, and we (Bridgewater) have given you an extensive look at the moves we can imagine could be done by both sides, so I won’t embellish more on them. As far as the geopolitical war is concerned, it’s a war of influence that is being fought in the classic Chinese way of quietly gaining strength and showing that strength to one’s opponent so that they realize that it is better to retreat than to fight. That is certainly happening in Asia and, to a lesser extent, in other parts of the world.

Countries are increasingly having to choose whether they are aligned with the US or China. When presented with this choice, they typically answer it based on both economic and military calculations. Almost without exception, they say that the economics favors being aligned with China because China is more important to them economically (because China is bigger in trade and bigger in capital inflows) and that the military support favors the US if the US is willing to use it to support them, which is highly doubtful.

At the same time, China’s own military capabilities (including cyber) are rising relative to the US’s, especially in Asia. As a result, China is for the most part quietly winning the geopolitical war, particular in Asia. As for what is likely to happen next, the big thing is the 2020 elections because that will determine who the players are; until then, actions and agreements are more for theater to play to the crowd than the real deal. After the elections, the real picture will emerge. Longer term, barring any big shocks, time is on China’s side as it is improving at a faster rate than the US, and the big question is whether the world will:

a) peacefully evolve toward two different spheres of influence, with China the dominant force in the East and the US the dominant force in West, or

b) have more painful wars of their various types.

Under each of these three broad categories of influences, I have imagined a detailed sequence of events for how these dynamics will progress, based on how sequences of events have classically played out in the past and how it is logical they will play out nowadays. I do this so I can compare how events transpire relative to expectations. If they’re largely the same, I assume the sequence will continue as imagined, and if they’re different, I abandon my theory and recalibrate.

To me, last week’s developments seemed like the most recent logical steps in this classic dangerous journey that is analogous with that which occurred in the 1935-45 period.

Four Appendices

What follows are four appendices.

Appendix 1 provides a more detailed account of what actually happened, what can happen, and how it can happen pertaining to threats to curtail capital flows to China.

Appendix 2 recounts the path to war in the late 1930s via excerpts from my book “Principles for Navigating Big Debt Crises” (available in pdf form here for free).

Appendix 3 recounts various times monetary policies didn’t work because there was “pushing on a string” and provides the various Monetary Policy 3-type fiscal/monetary coordinations that occurred in the past.

Appendix 4 provides the legal basis for capital controls and capturing the assets of foreign entities.

Appendix 1: A More Precise Account of What Happened, Why, and What Is Likely to Happen

To be precise, two narrow measures are being examined by the administration.

The first narrow step under consideration by the White House is whether to support/push for Senator Marco Rubio’s Equitable Act legislation. The Equitable Act outlines a process for the delisting of a Chinese firm from US stock exchanges if it doesn’t fully comply with US accounting and oversight regulations, e.g., audit requirements. Senator Rubio notes that China’s government has long been reluctant to allow overseas regulators to inspect local accounting firms—including member firms of the Big Four international accounting networks—citing national security concerns, and that a 2013 agreement allowing US regulators to request audit working papers in China has not been effectively implemented. Resultantly, in December 2018, the SEC and the Public Company Accounting Oversight Board (PCAOB) flagged the difficulties US regulators faced in inspecting the audit work and practices of auditing firms in China that examine US-listed Chinese companies.

The second narrow measure under discussion is a potential ban (or restriction) precluding the Federal Retirement Thrift Investment Board from including the MSCI All Country World ex-US Index in the ~$50 billion Federal Employees Retirement Fund (FERF, the government’s main retirement savings fund) in 2020. Senator Rubio and other members of Congress who support such a ban argue that retirement assets of federal government employees, including members of the US Armed Forces, will be exposed to “severe and undisclosed material risks” associated with many of the Chinese companies listed on this MSCI index.

Why Are These Things Happening?

The motivations and objectives driving these discussions appear varied: from wanting to enforce US accounting and oversight regulations in order to engender reciprocity (Senator Rubio’s Equitable Act bill), to curtailing access to US capital by certain Chinese firms implicated by national security concerns (restricting FERF’s planned MSCI offering), and ultimately to decoupling US and China capital markets so as to undermine China’s rise. There are officials (Peter Navarro) who seek to limit China’s access to US capital, as they think such access strengthens the Communist Party in China—an economic rival and rising geostrategic competitor with different values antithetical from the US/West. Recently, Steve Bannon characterized the goal this way: “The Frankenstein monster that we have to destroy is created by the West. It’s created by our capital.” There are other officials trying to circumscribe these measures and keep them separated from trade negotiations so as not to inflame tensions, sink markets, and weaken the real economy. Some officials, on the other hand, reportedly see these measures as giving the US increased leverage in the trade negotiations with China at a critical juncture. All these US officials appear to share concerns about US capital enabling Chinese firms when the lines of demarcation between state-owned and private firms are further eroding. They are concerned with the unusual influence the Chinese government has over private firms, including placing restrictions on the release of financial information of Chinese firms. And, importantly, they want to counter industrial policies such as President Xi’s new “military-civil fusion” directed at enhancing cooperation between China’s technology firms and the military and Made in China 2025.

These discussions, in turn, are taking place days before Vice Premier Liu He’s expected visit to Washington for high stakes talks on October 10-11. These talks importantly will play out in the shadow of scheduled US tariff increases, a potential Xi-Trump meeting, and the pending expiration of Huawei licenses. In particular, i) on October 15 tariffs are scheduled to increase to 30% from 25% on $200 billion in imports from China; ii) there is a scheduled meeting on November 16-17 between Xi and Trump at the APEC Summit; iii) on November 19 Huawei’s general temporary license is due to expire, and iv) on December 15 tariffs are scheduled to be imposed on $160 billion of the most politically sensitive Chinese imports (consumer products of high value to US consumers with no readily available substitutes (~87% sourced from China)).

Appendix 2: The 1930s Path to War (Excerpted from Part 2 of “Principles for Navigating Big Debt Crises,” Which Was about the 1930 – 1941 Period)

While the purpose of this chapter has been to examine the debt and economic circumstances in the United States during the 1930s, the linkages between economic conditions and political conditions, both within the United States and between the United States and other countries—most importantly Germany and Japan—cannot be ignored because economics and geopolitics were very intertwined at the time. Most importantly, Germany and Japan had internal conflicts between the haves (the Right) and the have-nots (the Left), which led to more populist, autocratic, nationalistic, and militaristic leaders who were given special autocratic powers by their democracies to bring order to their badly managed economies. They also faced external economic and military conflicts arising as these countries became rival economic and military powers to existing world powers.

To help to convey the picture in the 1930s, I will quickly run though the geopolitical highlights of what happened from 1930 until the official start of the war in Europe in 1939 and the bombing of Pearl Harbor in 1941. While 1939 and 1941 are known as the official start of the wars in Europe and the Pacific, the wars really started about 10 years before that, as economic conflicts that were at first limited progressively grew into World War II. As Germany and Japan became more expansionist economic and military powers, they increasingly competed with the UK, US, and France for both resources and influence over territories. That eventually led to the war, which culminated in it being clear which country (the United States) had the power to dictate the new world order. This has led to a period of peace under that world order and will continue until the same process happens again.

More precisely:

In 1930, the Smoot-Hawley Tariff began a trade war.

In 1931, Japan’s resources were inadequate, and its rural poverty became severe, so it invaded Manchuria, China to obtain natural resources. The US wanted to keep China free from Japanese control and was competing for natural resources—especially oil, rubber, and tin—from Southeast Asia, while at the same time Japan and the US had significant trade with each other.

In 1931, the depression in Japan was so severe that it drove Japan off the gold standard, leading to both the floating of the yen (which depreciated greatly) and big fiscal and monetary expansions that led to Japan being the first country to experience a recovery and strong growth (which lasted until 1937).

In 1932, there was a lot of internal conflict in Japan, which led to a failed coup and a massive upsurge in right-wing nationalism and militarism. During the period from 1931 to 1937, the military took over control of the government and increased its top-down command of the economy.

In 1933, Hitler came to power in Germany as a populist promising to exercise control over the bad economy, to bring order to the political chaos of the democracy of the time, and to fight the communists. Within just two months of being named chancellor, he was able to take total authoritarian control; using the excuse of national security, he got the Reichstag to pass the Enabling Act, which gave him virtually unlimited powers (in part by locking up political opponents and also by convincing some moderates that it was necessary). He promptly refused to make reparations payments, stepped out of the League of Nations, and took control of the media. To create a strong economy and attempt to bring prosperity to the people, he created a top-down command economy. For instance, Hitler was involved with setting up Volkswagen to build a more affordable car and directed the building of the national German Autobahn (highway system). He believed that Germany’s potential was limited by its geographic boundaries, that it didn’t have adequate raw materials to feed the industrial military complex, and that German people should be ethnically united.

At the same time, Japan became increasingly strong with its top-down command economy, building a military-industrial complex, with the military intended to protect its bases in East Asia and northern China and to expand its controls over other territories.

Germany also got stronger by building its military-industrial complex and looking to expand and claim adjacent lands.

In 1934, there was severe famine in parts of Japan, causing even more political turbulence and reinforcing the right-wing, militaristic, and nationalistic movement. Because the free market wasn’t working for the people, that led to the strengthening of the command economy.

In 1936, Germany took back the Rhineland militarily, and in 1938, it annexed Austria.

In 1936, Japan signed a pact with Germany.

In 1936–37, the Fed tightened, which caused the fragile economy to weaken, and other major economies weakened with it.

In 1937, Japan’s occupation of China spread, and the second Sino-Japanese War began. The Japanese took over Shanghai and Nanking, killing an estimated 200,000 Chinese civilians and disarmed combatants in the capture of Nanking alone. The United States provided China’s Chiang Kai-shek government with fighter planes and pilots to fight the Japanese, thus putting a toe in the war.

In 1939, Germany invaded Poland, and World War II in Europe officially began.

In 1940, Germany captured Denmark, Norway, the Netherlands, Belgium, Luxembourg, and France.

During this time, most companies in Germany and Japan remained publicly owned, but their production was controlled by their respective governments in support of the war.

In 1940, Henry Stimson became the US Secretary of War. He increasingly used aggressive economic sanctions against Japan, culminating in the Export Control Act of July 2, 1940. In October, he ramped up the embargo, restricting “all iron and steel to destinations other than Britain and nations of the Western Hemisphere.”

Beginning in September 1940, to obtain more resources and take advantage of the European preoccupation with the war on their continent, Japan invaded several colonies in Southeast Asia, starting with French Indochina. In 1941, Japan extended its reach by seizing oil reserves in the Dutch East Indies to add the “Southern Resource Zone” to its “Greater East Asia Co-Prosperity Sphere.” The “Southern Resource Zone” was a collection of mostly European colonies in Southeast Asia, whose conquest would afford Japan access to key natural resources (most importantly oil, rubber, and rice). The latter, the “Greater East Asia Co-Prosperity Sphere,” was a bloc of Asian countries controlled by Japan, not (as they previously were) the Western powers.

Japan then occupied a naval base near the Philippine capital, Manila. This threatened an attack on the Philippines, which was at the time an American protectorate.

In 1941, to aid the Allies without fully entering the war, the United States began its Lend-Lease policy. Under this policy, the United States sent oil, food, and weaponry to the Allied Nations for free. This aid totaled over $650 billion in today’s dollars. The Lend-Lease policy, although not an outright declaration of war, ended the United States’s neutrality.

In the summer of 1941, US President Roosevelt ordered the freezing of all Japanese assets in the United States and embargoed all oil and gas exports to Japan. Japan calculated that it would be out of oil in two years.

In December 1941, Japan attacked Pearl Harbor and British and Dutch colonies in Asia. While it didn’t have a plan to win the war, it wanted to destroy the Pacific Fleet that threatened Japan. Japan supposedly also believed that the US would be weakened both by fighting a war in two fronts (Europe and Asia) and by its political system; Japan thought that totalitarianism and the command military industrial complex approaches of their country and Germany were superior to the individualistic/capitalist approach of the United States.

These events led to the “war economy” conditions, explained at the end of Part 1.

Appendix 3: Past Needs for and Ways of Executing Monetary Policy 3

Monetary Policy 3 puts money more directly into the hands of spenders instead of investors/savers and incentivizes them to spend it. Because wealthy people have fewer incentives to spend the incremental money and credit they get compared to less wealthy people, when the wealth gap is large and the economy is weak, directing spending opportunities at less wealthy people is more productive. Logic and history show us that there is a continuum of actions to stimulate spending that have varying degrees of control to them. At one end are coordinated fiscal and monetary actions, in which fiscal policy makers provide stimulus directly through government spending or indirectly by providing incentives for nongovernment entities to spend. At the other end, the central bank can provide “helicopter money” by sending cash directly to citizens without coordination with fiscal policy makers. Typically, though not always, there is a coordination of monetary policy and fiscal policy in a way that creates incentives for people to spend on goods and services. Central banks can also exert influence through macroprudential policies that help to shape things in ways that are similar to how fiscal policies might. For simplicity, I have organized that continuum and provided references to specific prior cases of each below.

Fiscal/Monetary Coordination can take three basic forms:

Increase in debt-financed fiscal spending, paired with QE that buys most of the new issuance (e.g., Japan in the 1930s, US during WWII, US and UK in the 2000s).

Increase in debt-financed fiscal spending, where the Treasury isn’t on the hook for the debt, because:

a) The spending is paired with QE where the central bank retires the debt or commits to rolling the debt forever,

b) The central bank promises to print money to cover debt payments (e.g., Germany in the 1930s), or

c) Where the central bank directly lends to entities other than the government that will use it for stimulus projects (e.g., lending to development banks in China in 2008).

Directly giving newly printed money to the government to spend, not bothering to go through issuing debt. Past cases have included printing fiat currency (e.g., Imperial China, the American Revolution, the US Civil War, Germany in the 1930s, UK during WWI) or debasing hard currency (Ancient Rome, Imperial China, 16th-century England).

Printing money and doing direct cash transfers to households (i.e., helicopter money). When we refer to “helicopter money,” we mean directing money into the hands of spenders of money to get them to spend (e.g., the US veterans’ bonus during the Great Depression, Imperial China).

How that money is directed could take different forms—the basic variants are a) to either direct the same amounts to everyone, or to aim for some degree of helping one or more groups over others (e.g., to the poorer more than to the rich), and b) to provide this money either as one-offs or over time (perhaps as a universal basic income). These variants could be paired with an incentive to spend it—like the money disappearing if not spent within a year.

The money could be directed to specific investment accounts (like retirement, education, or accounts earmarked for small business investments) to target it toward socially desirable spending/investment.

One potential way to craft the policy is to distribute returns/holdings from QE to households instead of to the government.

Big debt write-down accompanied by big money creation (the “year of Jubilee”). (e.g., Ancient Rome, the Great Depression, Iceland).

While I won’t offer opinions on each of these, I will say that the most effective approaches involve fiscal/monetary coordination, because that ensures that both the providing and the spending of money will occur. If central banks just give people money (helicopter money), that’s typically less adequate than giving them that money with incentives to spend it. However, sometimes it is difficult for those who set monetary policy to coordinate with those who set fiscal policy, in which case other approaches are used.

Also, keep in mind that sometimes the policies don’t fall exactly into these categories, as they have elements of more than one of them. For example, if the government gives a tax break, that’s probably not helicopter money, but it depends on how it’s financed. The government can also spend money directly without a loan financed by the central bank—that is helicopter money through fiscal channels.

While central banks influence the costs and availabilities of credit for the economy as whole, they also have powers to influence the costs and availabilities of credit for targeted parts of the financial system through their regulatory authorities. These policies, which are called macroprudential policies, are especially important when it’s desirable to differentiate entities—e.g., when it is desirable to restrict credit to an overly indebted area while simultaneously stimulating the rest of the economy, or when it’s desirable to provide credit to some targeted entities but not provide it broadly. Macroprudential policies take numerous forms that are valuable in different ways in all seven stages of the big debt cycle. Because explaining them here would require too much of a digression, they are explained in some depth in the appendix of my book “Principles for Navigating Big Debt Crises.” If you want to dig deeper, please review that appendix.

Appendix 4: The Legal Authorities of the President to Curtail Capital Flows

The president has broad, powerful, and mostly unilateral authority to regulate commerce (trade and finance) with foreign countries, under the executive’s emergency powers—codified in statute and reaffirmed by courts (courts have shown great deference to the president’s judgment in matters of foreign and national security). Key among them and one that President Trump has tapped and will likely tap for any meaningful curtailment of capital flows (e.g., foreign exchange controls) is the International Emergency Economic Powers Act (IEEPA) of 1977. §1701 of IEEPA empowers the president to declare a national emergency to “deal with any unusual and extraordinary threat, which has its source…outside the United States, to the national security, foreign policy, or economy of the United States.” IEEPA gives the president discretion to “investigate,” “block,” “regulate,” “compel,” or “prohibit,” the “importation,” “transfer,” or “acquisition” of “property in which any foreign country or a national thereof has any interest.” §1702(a)(1)(B) of IEEPA empowers the president to act with respect to any person “subject to the jurisdiction of the United States.”

In the 42 years since its enactment, presidents have declared 54 national emergencies under IEEPA, 29 of which are ongoing. Presidents have tapped IEEPA to restrict a wide range of international transactions while expanding both the rationale for emergencies and targets of the restrictions, e.g., at first, targets were foreign governments, and later IEEPA was used to target individuals and non-state actors (terror groups). History (judicial precedent and congressional inaction) suggests that Trump could wield IEEPA with great force/impact, e.g., delisting Chinese companies on US stock exchanges, blocking all US-based transactions or freezing the US assets of any foreign firm or person, imposing currency controls or restricting FX purchases for certain or all foreign nationals, forcing divestment of US assets, blocking SWIFT payments system for foreign firms, and prohibiting US firms from outsourcing to China. President Trump cited IEEPA as the legal authority enabling his “order” that American companies “immediately start looking for an alternative to China.” Barring a successful court challenge, the only check on Trump’s IEEPA authority is Congress, which has yet to attempt to invalidate a national emergency. The political bar for congressional action is high—under IEEPA, Congress can invalidate a state of emergency via a joint resolution. The Supreme Court, however, has held that a joint resolution will not suffice. Congress must pass legislation to that effect, e.g., amend IEEPA to circumscribe the president’s emergency powers. Trump could then veto the legislation. And overriding a veto requires a two-thirds supermajority in both chambers.

Historical Precedent

There is much precedent for the president’s use of emergency powers before IEEPA. Before IEEPA’s enactment in 1977, the president’s emergency powers—enabling broad regulation of commerce (trade and financial)—were anchored in the Trading with the Enemy Act (TWEA) of 1917. It was enacted after the US entered World War I. Section 5 of TWEA delegates to the president broad wartime powers to regulate all forms of international commerce and financial flows and to freeze or seize any foreign assets during a time of war. While the 1917 Act required a declaration of war, it was subsequently amended in 1933 to allow the president to declare a national emergency during peacetime. The declaration empowers the president with broad powers over both domestic and international transactions (the amendment came about due to the Great Depression, and President Roosevelt invoked Section 5(b) of the amended TWEA to declare a national emergency and order a bank holiday). Specifically, the 1933 amendment gave the president the authority to: “investigate, regulate, or prohibit…by means of licenses or otherwise any transactions in foreign exchange, transfers of credit between or payments by banking institutions…and export, hoarding, melting, or earmarking of gold or silver coin or bullion or currency by any person within the United States or any place subject to the jurisdiction thereof.” For example, with the objective of denying Germany access to Danish and Norwegian assets in the US, President Roosevelt issued Executive Order 8389, based on the authority vested in him by the TWEA Act as amended in 1933, to freeze all financial transactions involving (and assets of) Danes and Norwegians. In June 1941, President Roosevelt extended the freezing of assets to all of continental Europe under Executive Order 8785, backstopped by the TWEA.

Oil Prices Rebound After Ugly Day On Big Surprise Crude Draw

Oil prices tumbled back below pre-Saudi-attack levels today, near 2-month lows, as a global growth scare was sparked by disappointing PMIs around the world spooking the global energy demand bounceback narrative. WTI almost tested $52 handle intraday.

“Demand fears are overriding supply fears,” Phil Flynn, senior market analyst at Price Futures Group Inc., said by telephone.

API

Crude -5.92mm (+2.25mm exp)

Cushing +373k

Gasoline +2.133mm

Distillates -1.741mm

After the previous week’s surprise crude build, traders expected another notable rise in stocks, but were surprised when API reported a large 5.92mm draw.

Ahead of the print, WTI was trading well below the pre-Saudi attack levels…

WTI hovered around $53.70 into the API print and kneejerked back above $54 after the surprise draw…

“In view of subdued global economic prospects and rising U.S. oil production, any concerns” about oil supply tightening have evaporated, said Carsten Fritsch, an analyst at Commerzbank AG in Frankfurt.

The major premise for tactics is the development of operations that will maintain a constant pressure upon the opposition

– Saul Alinsky, “Rules for Radicals”

Accuse your enemy of what you are doing, as you are doing it to create confusion.

– Marxist maxim

Who controls the past controls the future. Who controls the present controls the past.

– George Orwell, “1984”

I’m just a normal guy who started a blog three years ago, so I won’t claim to be officially credentialed for political commentary. I’m not a boots-on-the-ground reporter or even a writer, per se, although I was published nationally before my blogging career; just primarily pursuant to business and technical concerns. Regardless, given our times, I feel I’d be remiss for not sharing my personal observations – even if that is all I have: observations. Hence, the blog.

In past articles, such as “Breakfast Club: Dining with Friends”, and “The Persistence of Their Delusion is Despicable”, and “The Rants of the Libtards Ring Hollow then Echo”, I’ve written about my conversations with friends who are politically liberal; or, at least, more liberal than I. This past weekend, another such conversation began during breakfast with a snide remark about the “deep state impeaching Trump”. Of course, my democratic and Republican in Name Only (RINO) friends don’t believe in the deep state. But they do believe everything written in The New York Times and The Washington Post and that yours truly is an extreme right-wing, tinfoil-hat adorned, conspiracy theorist.

As I passionately decimated their arguments, they kept saying “let me speak…, let me speak” right up to the point a thirty-something young lady dining at an adjacent table with her husband and young children jumped to my defense and yelled at my friends: “You are the ones who keep interrupting HIM!”

I had to laugh at that, because at that point I was discussing how San Fran Nan (Pelosi) may have inconsolably angered the silent majority with her latest impeachment gambit derived from “Operation Ukraine”. And, this, just as the “Socialist Clown Show” plays nationwide during the Democratic Presidential Primaries.

I said:

“The Democrats have nothing. Absolutely nothing real to offer.”

The RINO kept trying to pin me down on the transcript of Trump’s July 25, 2019 phone call with Ukrainian President Volodymyr Zelensky with questions like:

“Did Trump, at first, financially hold up what Zelensky desired?”

“Did Trump request a favor from a foreign power that could be used against his U.S. political opponent, Joe Biden?”

“Was an agreement made?”

The main thrust being, according to the RINO, that these violated the U.S. Constitution, which the Democrat at our table claimed Pelosi was trying to protect.

Beyond the risibility of Pelosi’s concern for the Constitution, I refused to accept their premise that Trump was acting solely to benefit his 2020 election chances. He was, instead, I argued, on a mission to discover the origins of the now-debunked Russiagate Operation as well as rooting out the Obama Administration’s corrupt past involvement in Ukrainian affairs.

And this really goes to the heart of the American divide on Operation Ukraine.

For those on the Political Left, who view Trump as a self-seeking traitor, this latest effort is merely the continuation of Operation Russiagate.

For Trump supporters, however, the transcript of Trump’s phone call revealed a seemingly earnest effort to fulfill his 2016 campaign promises of draining the swamp and making America great again.

The American rift is, indeed, very real and the breach is growing wider. In fact, it now appears to be a matter of survival for those on both sides of the political aisle and Trump’s mere single mention of the word “CrowdStrike” to the Ukrainian President is akin to the first shot being fired at Fort Sumter during the beginning of America’s first civil war. For those unaware, CrowdStrike is the cybersecurity firm located dead center within the U.S. Intelligence Agencies’ Russiagate Operation which has maliciously undermined Donald Trump’s presidency for the last three years. The phony Russian “golden shower” dossier and unsubstantiated reports from the Democratic National Committee (DNC) contractor, CrowdStrike, represent what one might call razor thin or hanging by a thread “proof” of Russia’s alleged hacking of the U.S. 2016 Presidential Election.

Yet, exactly like Russiagate, the psychological defense mechanisms of Projection and Displacement are being utilized in this latest initiative, with the whistleblower in Operation Ukraine being the new “dirty dossier” of Operation Russiagate’s former glory days.

Furthermore, there is no doubt that Operation Ukraine’s Whistleblower’s Complaint was quite carefully crafted with the vague legal objective of forcing Attorney William Barr to recuse himself from any ongoing investigations; or perhaps only from those inquiries regarding the involvement of U.S. intelligence officials colluding with foreign nations toward the goal of overturning a U.S. Presidential Election. Or, it could be said that Operation Ukraine, at the very least, is meant to simultaneously defang Attorney General Barr both legally and in the eyes of the American public prior to any forthcoming Russiagate disclosures by Inspector General Michael Horowitz and U.S. Attorney John Durham.

In any event, like Russiagate’s dirty dossier, the carefully constructed CIA Whistleblower’s Complaint within Operation Ukraine is evidence of collusion and, in fact, meets the threshold for the text-book definition of “conspiracy”.

Still, most Americans remain fooled.

At a get together in a church on Sunday, I listened to an elderly gentleman and “youngish” female boomer lament the “toxicity” in Washington D.C. Although no specific names were mentioned, it seemed to me they both blamed Trump – the woman in particular because she commented on how “diversity was a good thing” because, after all, her son-in-law worked at a plant that employed many people from India. Nice people. Good people.

Of course, so many Americans, including my breakfast friends, believe unity is obtained through diversity. Yet, at the same time, they eschew ideological diversity in favor of psychologicalconformity; even taken to the extremes whereupon melanin and genitalia supercede disparate thoughts and perspectives.

Just as many people today seek salvation through their tiny houses and smart cars, the Unity via Diversity crowd are self-justified by their virtue signaling. It really is like a religion. But a new religion that makes national borders immoral, parochial, and out of style.

And this is why Trump is considered to be a selfish pig by those who currently desire a new president. Trump is a divider; a xenophobic racist. He builds walls instead of bridges.

Indeed, this last weekend was a reminder regarding the logic of the mob, as well as the difference between propaganda and conspiracy. Most people don’twant to believe in conspiracy. Or, dare I say: “critical thinking”. It’s just another reason why the intelligence of the American Body Politic should never be overestimated.

For many years now, Joe Biden’s maleficence in Ukraine has been known by anyone with a computer, an internet connection, and a modicum of curiosity; including, yours truly, a genuine nobody who wrote about it near 2.5 years ago in a piece entitled “Dogs of War: Fight to the Death”. That article was posted just hours before the nation of Syria was bombed by Trump for the first time and my main point, now, is this: If I (and others) knew about these events so many years ago, then that should remove anydoubt in anyone’s mind as to the continuing complicity of the Orwellian Media in these odious international affairs (then and now):

In November of 2013 when, Ukraine’s President Viktor Yanukovych abandoned an agreement on closer trade ties with the European Union and, instead, sought closer co-operation with Russia, it began a series of events which then transitioned into the natural gas wars of 2014, and the Ukrainian coup in February, 2014 during the winter Olympics of that year.

This all, in turn, caused Russia to make the decision to annex Crimea in March 2014. Then, Russia signed a $400 billion “Holy Grail” gas deal with China in May and this gave the Petrodollar a nice kick in the nuts.

In June of that year, Ukraine, at the behest of the Western globalists, refused to pay its gas bill to Moscow’s Gazprom, so Russia cut off their gas. Soon after that MH17 was shot out of the sky and Joe Biden’s son’s company began preparing to drill for shale gas in eastern Ukraine.

The “memory hole” in George Orwell’s 1984 was a chute connected to an incinerator and served as the mechanism by which the Ministry of Truth would abolish historical archives. With Operation Ukraine, today’s Ministry of Truth needed to accomplish two primary goals: First, to magnify Trump’s guilt while, secondly, whitewashing former Vice President Joe Biden (and son’s) previous “involvement” in Ukraine.

And this is exactly what has happened. Trump has, once again, been slandered as guilty by the Orwellian Media just as Biden & Son were concurrently vindicated via articles such as these:

All of these headlines emerge on hundreds of millions of cell phones and devices, as the spin machines ceaselessly cycle. At the time of this writing, stories are being generated about how Adam Schiff (D-CA), the ranking member of the U.S. House Intelligence Committee, plans to hold President Trump “accountable”:

“The president used that opportunity to try to coerce that leader to manufacture dirt on his opponent and interfere in our election,” Schiff told ABC News Chief Anchor George Stephanopoulos, referring to Ukraine’s president, Volodymyr Zelenskiy.

“I can’t imagine a series of facts more damning than that.”

But, paradoxically, in 2018, Schiff was caught red-handed colluding with a foreign-power in order to undermine the President of the United States. The fact the congressman was pranked by Russian comedians is beside the point. Schiff clearly cooperated with whom he perceived as foreign assets. Why is this not considered relevant by the Orwellian Media? Obviously, some questions answer themselves.

Orwell’s memory-hole works overtime in America today, as propaganda reigns. These are, in fact, a double-whammy. A one-two punch.

And most people don’t stand a chance.

Even if desktop reporters and internet sleuths wanted to discover the truth today, they would find it quite difficult. One reason, in the example of Operation Ukraine, is because search engines answering queries for “Biden’s Son” or “Hunter Biden” favor the online encyclopedia, Wikipedia, which states the following about the gas company, “Bursima Holdings”, that previously employed Hunter Biden:

There is no evidence that Hunter Biden was ever under investigation by the government of Ukraine, or that Vice President Biden sought the removal of [prosecutor Viktor] Shokin to protect Hunter Biden or Burisma Holdings.

Now, if you research the online link-attribution listed at the end of that Wikipedia statement, you will see articles sourced to a think-tank identified as The Annenberg Public Policy Center as well as other Orwellian Media outlets. The Annenberg Public Policy Center is subsidized by the University of Pennsylvania, and the Annenberg Foundation, with an office in Washington DC – and describes FactCheck.org as one of its “most notable initiatives”.

Fair and balanced? Probably not.

Furthermore, it is interesting that on Wikipedia’s “Hunter Biden/Bursima Holdings” section, the online encyclopedia very conveniently posts a “more information” link to their “Trump–Ukraine controversy” page – which has been growing every day, even now to the point of addressing various “conspiracy theories”. These conspiracies include speculations regarding the leftist mogul George Soros, the CIA “whistleblower”, and the DNC cyber-security contractor Crowdstrike. Accordingly, it appears very determined digital fingers are pointed at Donald Trump and Rudy Giuliani as well as “right-wing discussion forums on the Internet” engaging in “disorganized speculation, racism and misogyny”; all the while very cautiously minimizing the Ukrainian shenanigans of the Biden boys. Of course, the page is rife with many additional citations from The Washington Post and The New York Times as well.

No matter where one stands today in regards to American politics, one thing is very clear: We are in the midst of a narrative war.

On September 27, 2019 Fox News host Tucker Carlson discussed Operation Ukraine in a direct way. But if one searches Google or YouTube, it appears they have scrubbed it from their internet pages. Here is the episode linked on another site, but if you search “Tucker Carlson tonight 9/27/19” you will see many disconnected clips all shortened to between 1 to 42 seconds; even if Tucker’s 9/27/18 full show (on the Kavanaugh affair!), past episodes, and tonight’s episode, all remain available on YouTube in their entirety.

It is possible the entire Operation Ukraine, also known as Russiagate Part Deux, could be the result of panic on behalf of The Establishment? Could this be because Team Trump is about to go on offense? Is Trump playing for real this time? Or, will the president just tweet away while the nation burns?

Projection and hypocrisy are, indeed, the standard modi operandi of both deep state operatives and wild-eyed collectivists. But one wonders how much of the silent majority actually understands what is happening now. Some recent polls showing Trump hovering around 50% could be indicating sympathy for the ever-harassed president among the great unwashed; even as CNBC has reported support for Trump’s impeachment inquiry rising.

One also wonders if these new Operation Ukraine allegations against Trump could be just another scene from the ongoing, never-ending, reality TV series that has, once again, been taken off “pause”.

Regardless, the plot thickens as things are just beginning to really heat up.

In January 2019, Nancy Pelosi’s strategic new rules for the 116th Congress created “her own mini DOJ inside the legislative branch” in order to ease congressional impeachment efforts against President Trump. But also interesting, was how fast Senate Majority Leader Mitch McConnell fast-tracked Senate Minority Leader Chuck Schumer’s resolution to hand the CIA Whistleblower’s complaint to congressional intelligence committees:

One of the most pressing questions of the hectic Tuesday involved why Senate Majority Leader Mitch McConnell chose to counter his block-everything legacy and fast-track the resolution. (McConnell chose to “hotline” the motion, meaning he bypassed normal Senate procedures to move Schumer’s request to a vote without floor debate.)

It has also been reported that the U.S. Intelligence community “eliminated a requirement that whistleblowers must provide first-hand knowledge of alleged wrongdoings” just weeks after Trump’s July 25, 2019 “Crowdstrike” phone call to the Ukrainian President. Although, Wikipedia, and The Washington Post, and the Office of the Inspector General of the Intelligence Community has since labeled the alleged form change as a fake news conspiracy theory. This is because Operation Ukraine’s CIA Whistleblower used a “new form” utilized since May 24, 2018 that did “not require whistleblowers to possess first-hand information in order to file a complaint or information with respect to an urgent concern” and that the CIA Whistleblower also claimed to possess “both first-hand and other information”.

Seems legit, right?

Nevertheless, is it possible Operation Ukraine is a trap? Obviously, but for whom? Because if impeachment efforts fail, then the optics will be very bad for the Deep State and the Democrats – which could, very likely, result in Trump winning the 2020 Presidential Election.

Or it could all just be another Red vs. Blue cage fight as the exit doors are locked before the arena burns.

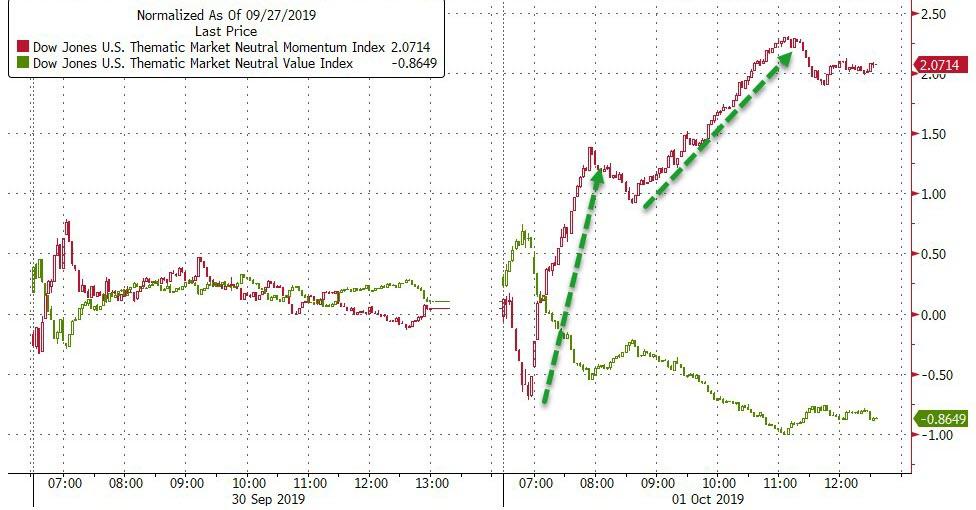

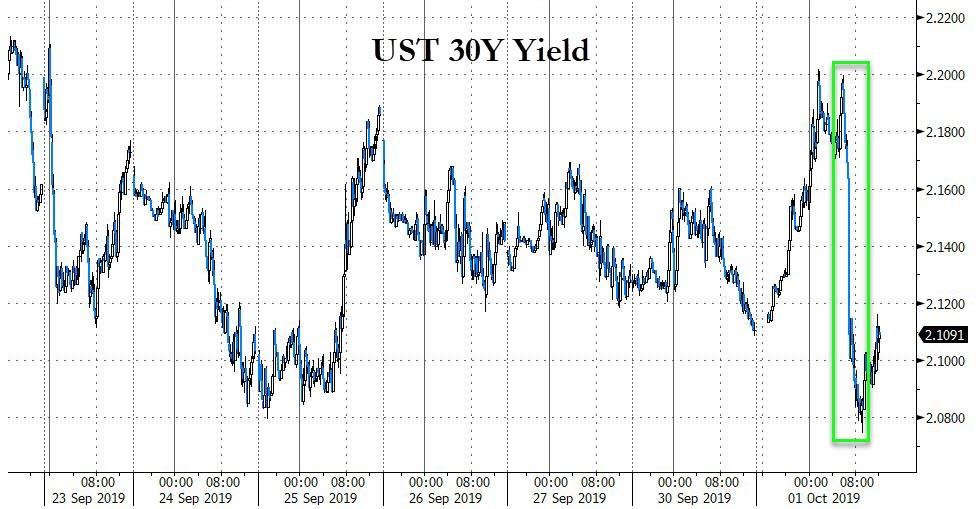

Global Growth Scare Sparks Safe-Haven Surge, Slam Stocks

“Everything was awesome” overnight – China was closed, futures drifted higher, hope remained, impeachment headlines had calmed down… and then the growth scare started in Asia with South Korean CPI deflated for the first time ever, then European PMIs plunged… But markets held in (hey, The Fed’s got our bank, right) as it’s just a fleshwound…

…and then US Manufacturing ISM survey missed by a mile, dropping to its biggest contraction since 2009 – and all hell broke loose.

Instantly, stocks and the dollar were dumped and safe haven flows sent gold higher and bond yields lower…

Source: Bloomberg

The moves today were quite shocking: Dow futures dropped 500 points from their overnight highs, 30Y Yields crashed 13bps from overnight highs, the dollar tumbled 0.6% intraday, and gold spiked $30. Additionally, rate-cut odds for October jumped higher to 60%…

Source: Bloomberg

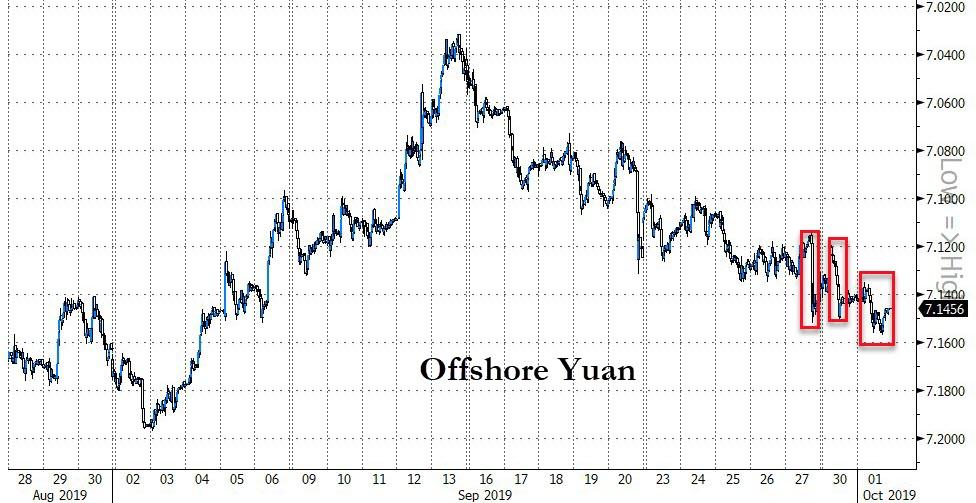

Chinese markets were closed last night (and all week) due to Golden Week celebrations but China ADRs in the US traded down

Source: Bloomberg

European stocks tumbled today…

Source: Bloomberg

US stocks were all red today led by Trannies and Small Caps…

Futures show the stable drift higher overnight that was abruptly ended by the ISM Manufacturing data…

S&P filled the gap from 9/5

Led by selling in cyclicals…

Source: Bloomberg

And momentum was very bid today…

Source: Bloomberg

VIX surged back above 18 once again…

All the major US indices tested or broke key technical levels today… (NOTE – The Dow was strongest until the last minute and it tumbled back to the 50DMA)

Treasury yields tumbled intraday, all now lower on the week…

Source: Bloomberg

30Y Yields collapsed 13bps from overnight highs…

Source: Bloomberg

JGBs spooked global bond yields overnight, but that was entirely erased by Treasuries…

Source: Bloomberg

The dollar surged overnight to fresh highs, then cratered after the ISM data…

Source: Bloomberg

Cable whipped around on backstop headlines today (and its 50DMA)

Source: Bloomberg

With China closed, offshore yuan continued to drift lower…

Source: Bloomberg

Cryptos managed to hold on to gains since last week’s carnage…

Source: Bloomberg

Commodities were mixed with PMs bid today as crude tumbled…

Source: Bloomberg

WTI broke below the pre-Saudi attack levels, retested them, then plunged to almost a $52 handle…

Gold rebounded from yesterday’s losses but remains red on the week…

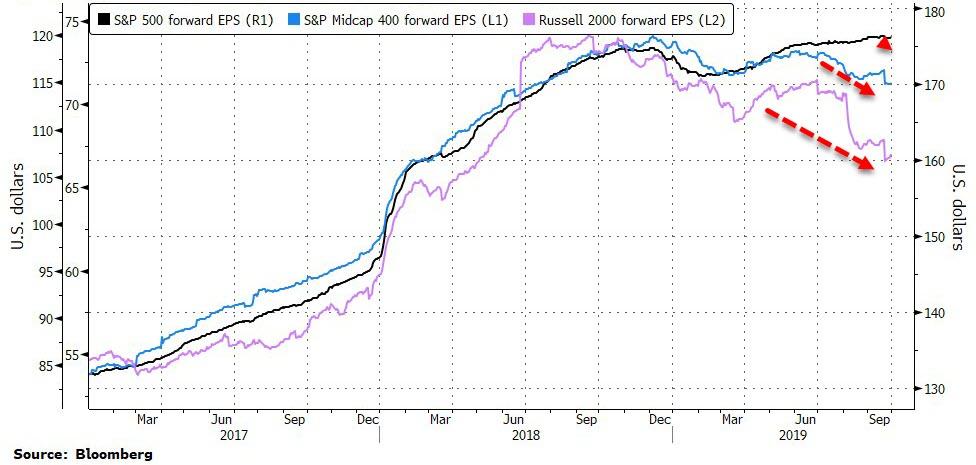

Finally, lower earnings estimates for the largest U.S. companies may only be a matter of time, according to Mike Wilson, Morgan Stanley’s chief U.S. equity strategist.

Source: Bloomberg

And the September “use it or lose it” surge in macro data… is over

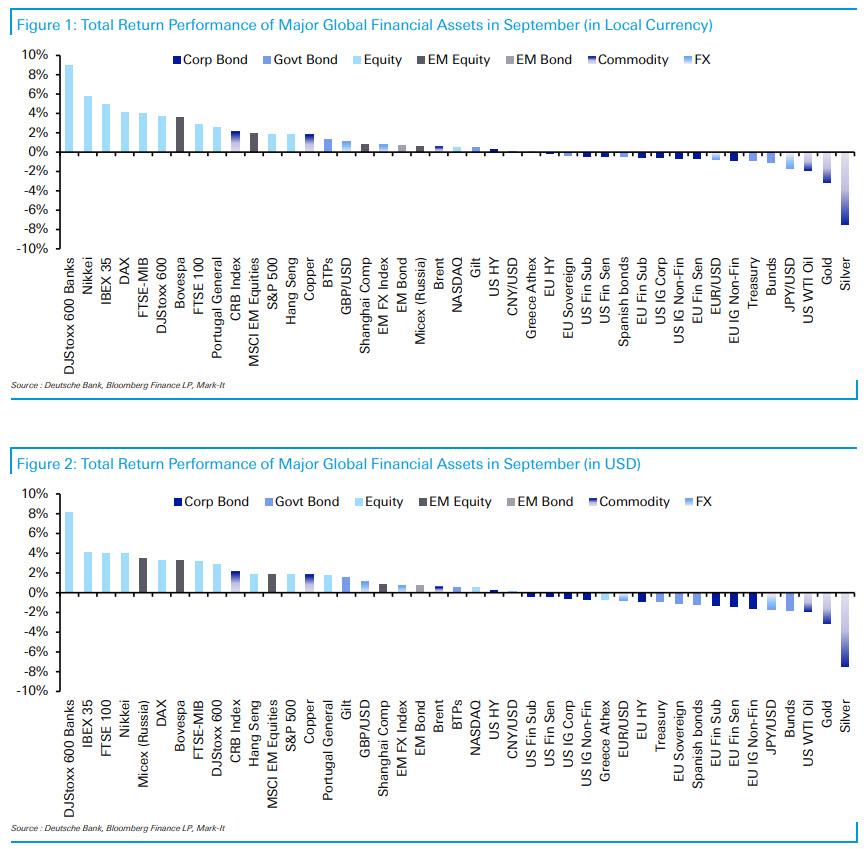

These Were The Best And Worst Performing Assets In September, Q3 And YTD

As we enter the final quarter of an eventful 2019 so far, the month of September was a partial reversal of the fairly extreme price action that we saw in August, according to Deutsche Bank’s Craig Nicol. The big winners last month were equity markets while the bottom of the table was dominated by fixed income and precious metals. When it was all said and done, excluding currencies 23 out of the 38 assets in Deutsche Bank’s sample ended with a positive total return in local currency terms while 22 did so in dollar adjusted terms.

Looking across the main winners in equity markets last month, topping the table were European Banks which returned +9.0% in local currency terms and +8.1% in dollar adjusted terms. That was the best performance for the sector since March 2017. The small sell-off in rates clearly helped, however the reality is that last month’s performance only really recouped the prior two months’ worth of losses before that. That being said the sector did have to contend with some disappointment around the ECB meeting outcome. Meanwhile, the general trend across equities was Europe outperforming the US. Indeed the STOXX 600 (+3.7%), DAX (+4.1%), IBEX (+4.9%), and FTSE MIB (+4.0%) all outperformed the S&P 500 (+1.9%) and more notably the NASDAQ (+0.5%) where a combination of sector rotation and trade war and impeachment tensions appear to have weighed more, according to DB. In Asia the Nikkei (+5.7%) outperformed the Hang Seng (+1.9%) and Shanghai Comp (+0.8%) while EM equities returned +1.9%.

As for the laggards last month, Gold (-3.2%) and more notably Silver (-7.5%) dipped following a few months of strong performance, although Q3 returns were still strong. As for sovereign bond markets, Bunds and Treasuries returned -1.1% and -0.9% respectively however we did see positive returns for BTPs (+1.3%) and EM bonds (+0.7%). As for what that meant for credit, returns were slightly negative with the exception of US HY which returned +0.3%. EUR HY was down -0.1% while the higher duration impact saw US non-fin IG and EUR non-fin IG return -0.7% and -0.9% respectively.

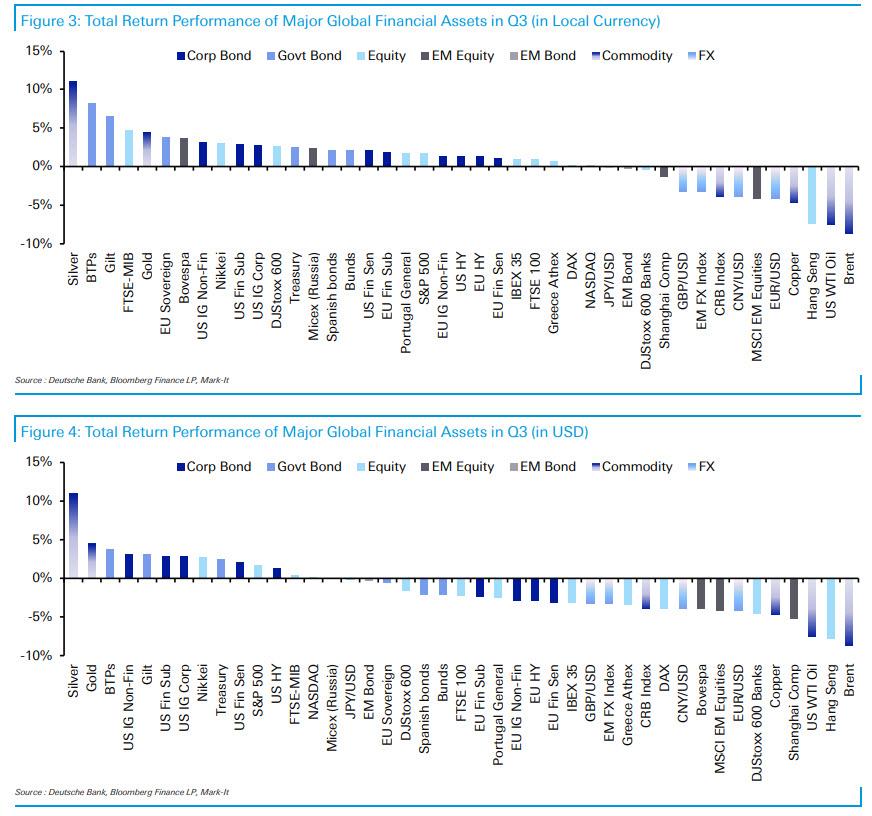

In terms of what that meant for Q3, despite the turmoil of August, there were still 29 of 38 assets in the constituent universe that finished with a positive total return although only 14 did so in dollar adjusted terms owing to the stronger greenback. In local currency terms, the top 3 spots went to Silver (+11.0%), BTPs (+8.3%) and Gilts (+6.5%). Equity markets were fairly mixed with decent gains for the FTSE MIB (+4.8%) and Nikkei (+3.0%), a more muted gain for the S&P 500 (+1.7%), little change for European Banks (-0.5%) and a notable underperformance for the Hang Seng (-7.5%) following the protests in Hong Kong. In terms of sovereign bonds, the big rally in August meant Treasuries and Bunds finished with returns of +2.5% and +2.1% respectively while in credit returns were also positive, with US outperforming EUR and IG outperforming HY.

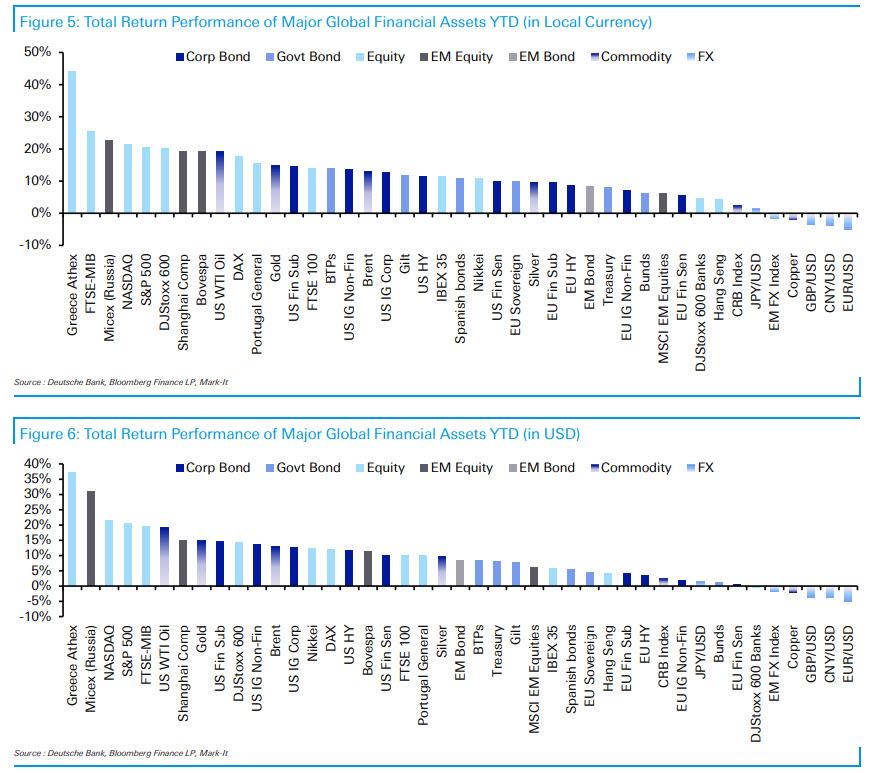

August meant Treasuries and Bunds finished with returns of +2.5% and +2.1% respectively while in credit returns were also positive, with US outperforming EUR and IG outperforming HY. Finally, the picture YTD remains very strong with 37 out of the 38 assets still delivering a positive total return in local currency terms and 36 in dollar adjusted terms. Copper (-2.0%) still occupies last spot with the Greek Athex (+44.2%), FTSE MIB (+25.6%) and Russia’s MICEX (+22.8%) holding the top 3 spots. DM equities broadly are up 10-20% while sovereign bond markets are led by BTPs (+14.1%) with Treasuries and Bunds returning +8.0% and +6.4% respectively. Finally credit markets are up between 10-15% in the US and 5-10% in EUR.