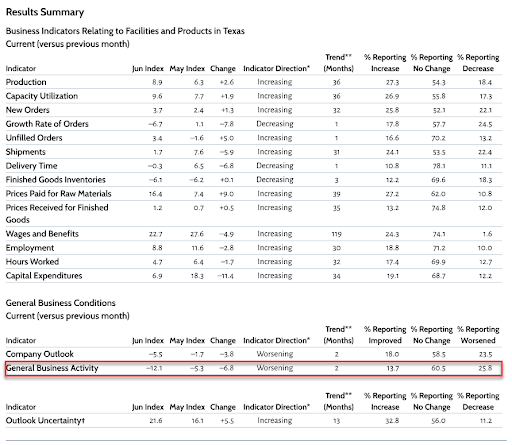

‘Soft’ survey data in June has collapsed. On the heels of the plunge in Empire Fed Manufacturing and Philly Fed, Dallas Fed Manufacturing survey just crashed from -5.3 to -12.1 (worse than the weakest analyst estimate) and lowest since June 2016.

Worse still ‘hope’ has plunged into the negative…

Respondents are not happy:

“I don’t care what the indicators say—things are slowing down in energy and manufacturing. Construction is still strong(ish). But, customers are shopping every nickel, quoting and requoting; no one wants inventory. Steel prices are dropping like a rock due to lack of demand and overcapacity. It is rough waters right now, for the last 60–90 days.”

“China tariffs are a big drain on profits, so we are covering with a general price increase July 1. Future improvements are expected due to new product introductions.”

“We cannot explain it, but we have gotten stupid slow, with incoming orders lagging way behind last year to date. At this rate, this will be the lowest year in over 15 years. All of our customers are complaining about being slow. Perhaps the economy is not in as good a condition—with all the uncertainty coming from Washington, D.C., people are afraid to pull the trigger on projects. Then adding on to our issues, San Antonio is about to implement mandatory paid sick time for hourly workers, adding even more pressure on profits, as we predict there will be widespread abuses of this. Most likely, this will result in a reduction in the workforce to cover the cost.”

“We need all the Democrats and all the Republicans to get on board with efforts to improve trading agreements and open foreign markets to U.S. business. Foreign governments won’t cooperate if we are divided and they think political change will allow them to keep taking advantage of our country’s historically bad trade deals. This political gridlock is hurting American business interests, and the tariffs and fear of increasing tariffs are not good. It is time we get fair trade, and we need everybody working together for the good of the country.”

We note that margin pressure is reasserting itself (Prices paid for raw materials 16.4 from 7.4, Prices received for finished goods 1.2 from 0.7)

Finally there is one silver lining:

“Military apparel orders appear to be strong for the next 12 months. “

As always, war is a racket.

via ZeroHedge News http://bit.ly/2ZHtcz4 Tyler Durden

InPart I, we discussed the problems with the “savings” side of the equation as it relates to building wealth.

It is always interesting reading article comments as they are generally full of excuses why saving money and building wealth can’t be done. The general thesis is that as long as you have social security (which is threatening payout cuts over the next decade) and/or a pension (which only applies to 15% of the country currently,) then you don’t need to save as much.

Personally, I don’t want my retirement based on things which are a) underfunded 2) subject to government-mandated changes, and 3) out of my control. In other words, when planning for an uncertain future, it is always optimal to hope for the best but plan for the worst.

However, the premise of the article was to clear up the disconnect between the cost of living today and 30-years into the future, as well as the amount of money needed to be financially independent for the entire lifespan after retirement.

Yes, we can all get by on less, in theory. But an examination of retirement savings statistics and the cost of healthcare in retirement (primarily due to poor healthcare habits earlier in life) doesn’t necessarily support those comments that saving less and being primarily dependent on Social Security is optimal.

The Investing Problem

While “Part One” focused on the amount savings required to sustain whatever level of lifestyle you choose in the future, we also need to discuss the issue of the investing side of the equation.

Let’s start with a comment made on Part-One of this series:

“If you want to play it safe just buy a no-load, low fee, index fund and index into it regularly. Pay yourself first. Let the power of compounding do its magic.”

See, it’s so easy. Just buy and index fund, dollar cost average into it, and “bingo,” you have got it made.

“More than half of Americans who were adults amid the Great Recession said they endured some type of negative financial impact, Bankrate found. And half of those people say they’re doing worse now than before the crisis.”

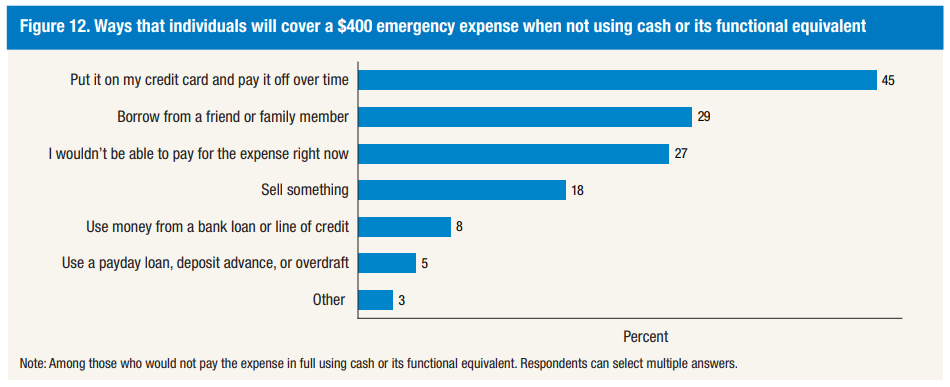

“According to a brand new survey from Bankrate.com, just 37% of Americans have enough savings to pay for a $500 or $1,000 emergency. The other 63% would have to resort to measures like cutting back spending in other areas (23%), charging to a credit card (15%) or borrowing funds from friends and family (15%) in order to meet the cost of the unexpected event.”

As I stated in the previous article, I am all for any program and process which encourages people to save and invest for their retirement. My hope is that we can clear up some of the “misconceptions” to improve the chances that retirement years are not spent collecting food stamps and shopping at the local “Goodwill” store,

Let’s start by clearing up the numerous erroneous comments on the previous article with respect to returns and investing.

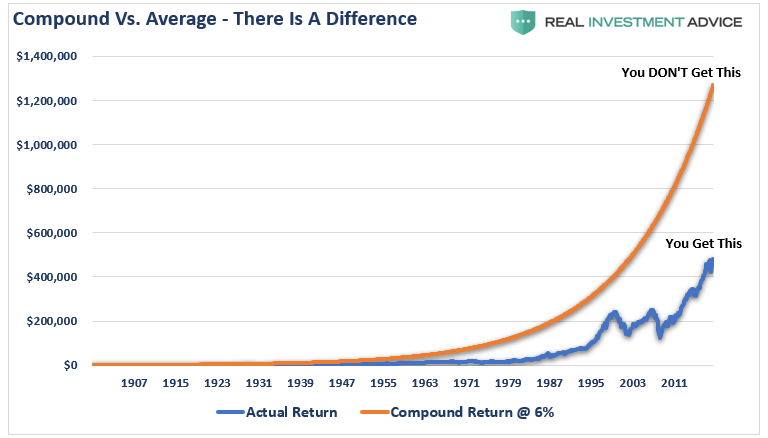

Compound & Average Are Not The Same Thing

” Markets have returned roughly 10% per year of compounded growth, INCLUDING the down years.”

What the commenter is confused about is, as stated previously, is that markets have variable rates of returns. Historically, over the last 120 years, the market has AVERAGED roughly 10% annually. (6% from capital appreciation which is equivalent to the long-term economic growth rate, and 4% from dividends. Today, economic growth is averaging 2%ish since 2000 and dividends are 2% so do the math for future return expectations. 2+2=4%. (Since 2000, average growth has been just a bit more than 5% and the next bear market will roll that average back to 4%)

The chart below shows the difference in nominal values of $1000 invested on an actual basis versus a compounded rate of return of 6% (For the example we are using capital appreciation only.)

Mathematically, both of those lines equate to a 6% return.

The top line is what investors THINK they will get (compound returns.) The bottom line is what they ACTUALLY get

The difference is when losses applied to invested dollars. The periods of time spent making up previous losses is not the same as growing money.(Bonds, which mature at face value and have a fixed coupon, have had the same return as stocks since the turn of the century.)

This “math problem” is the reason there is a pension fund crisis in the U.S. The massively underfunded pension system was caused by depending on 7%-annual returns in order to reduce saving rates.

Variable Rates Of Return Change The Game

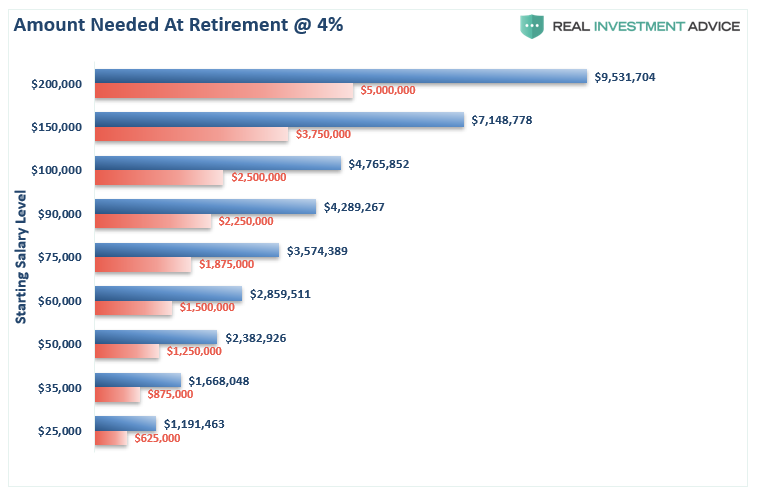

In Part 1, we laid out a simple example of various current incomes adjusted for inflation 30-years into the future. I am presenting the chart again so the subsequent charts have context.

Now, let’s look at the impact of variable rates of returns on outcomes.

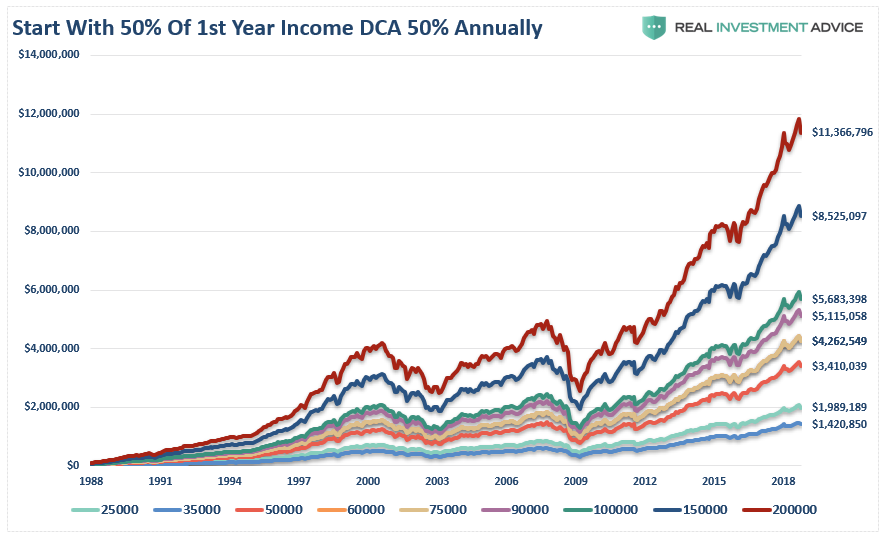

Let’s assume someone starts a super aggressive program of saving 50% of their income annually in 1988. (This was at the beginning of one of the greatest bull market booms in history giving them every advantage of front loaded returns and they get the benefit of the last 10-year long bull market.) Since our young saver has to have a job from which to earn income to save and invest, we assume he begins his journey at the age of 25.

The chart below starts with an initial investment of 50% of the various income levels shown above with 50% annual savings into the S&P 500 index. The entire portfolio is on a total return basis and adjusted for inflation.

Wow, they certainly saved a lot of money, and they met the amount need to completely replace their inflation-adjusted living standards for the rest of their lives.

Unfortunately, our young saver didn’t actually retire all that early.

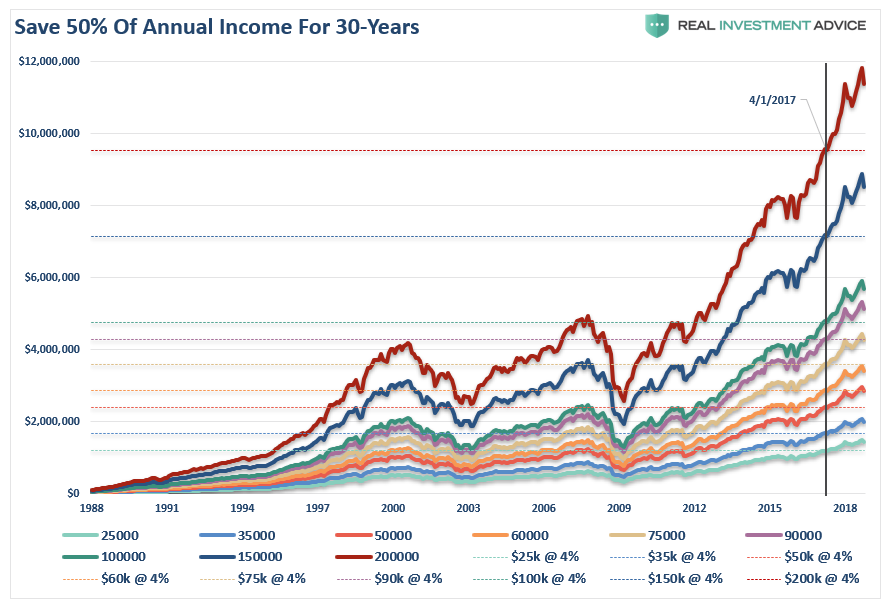

Despite the idea that by saving 50% of one’s income and dollar-cost averaging into index funds, it still took until April of 2017 to reach the retirement goal. Yes, our your saver did retire early at the age of 54, and it only took 29-years of saving and investing 50% of their salary to get there.

Given the realities of simply maintaining a rising standard of living, the ability for many to save 50% of their income is likely unrealistic. If it wasn’t then we would not have statistics like this:

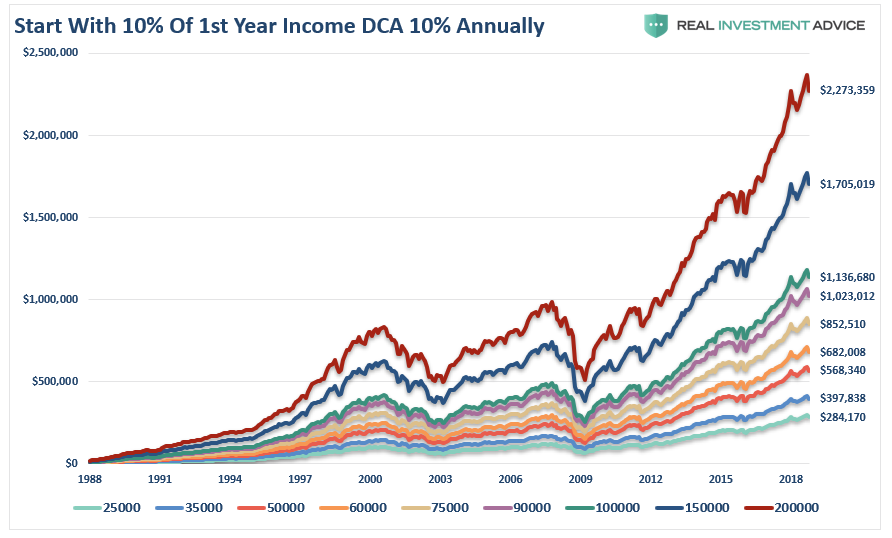

Instead, the next chart shows the same data but starting with 10% of our young saver’s income and adding 10% annually. (Which is the “Magic Number” for success)

Okay, it’s not so “Magic.”

There are two important things to note in the charts above.

The first is that saving 10% annually leaves individuals far short of their retirement needs. The second is that despite two massive bull market advances, it was the lost 13-year period from 2000 to 2013 which left individuals far short of their retirement goals.

What the majority of investors misunderstand when throwing around numbers like 6% average returns, 10% compound returns, etc., is that losses matter, and they matter a lot.

Here are the TWO most important lessons:

Getting back to even is not the same as making money.

The time lost in reaching your financial goals can not be recovered.

It should be relatively obvious the last decade of a massive, liquidity driven advance will eventually suffer much the same fate as every other massive bull market advance in history. This isn’t a message of “doom,” but rather the simple reality that every bull market advance must be followed by a reversion to remove the excesses built up during the previous cycle.

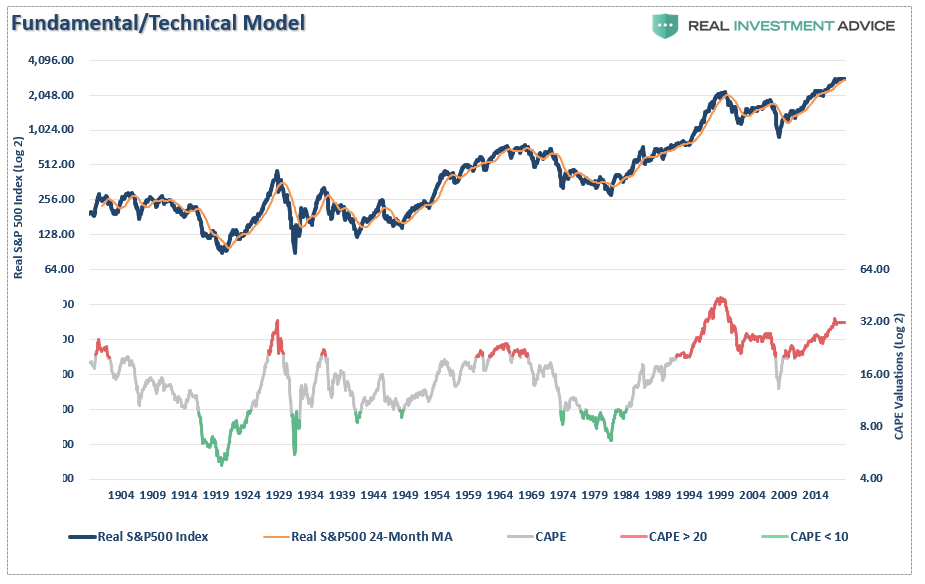

The chart below tells a simple story. When valuations are elevated (red), forward returns have been low and market corrections have been exceptionally deep. When valuations are cheap (green), investors have been handsomely rewarded for taking on investment risk.

With valuations currently on par with those on the eve of the Great Depression and only bettered by the late 1990’s tech boom, it should not be surprising that many are ringing alarm bells about potentially low rates of return in the future. It is not just CAPE, but a host of other measures including price/sales, Tobin’s Q, and Equity-Q are sending the same message.

The problem with fundamental measures, as shown with CAPE, is that they can remain elevated for years before a correction, or a “mean reverting” event, occurs. It is during these long periods where valuation indicators “appear” to be “wrong” that investors dismiss them and chase market returns instead.

Such has always, without exception, had an unhappy ending.

Things You Can Do To Succeed

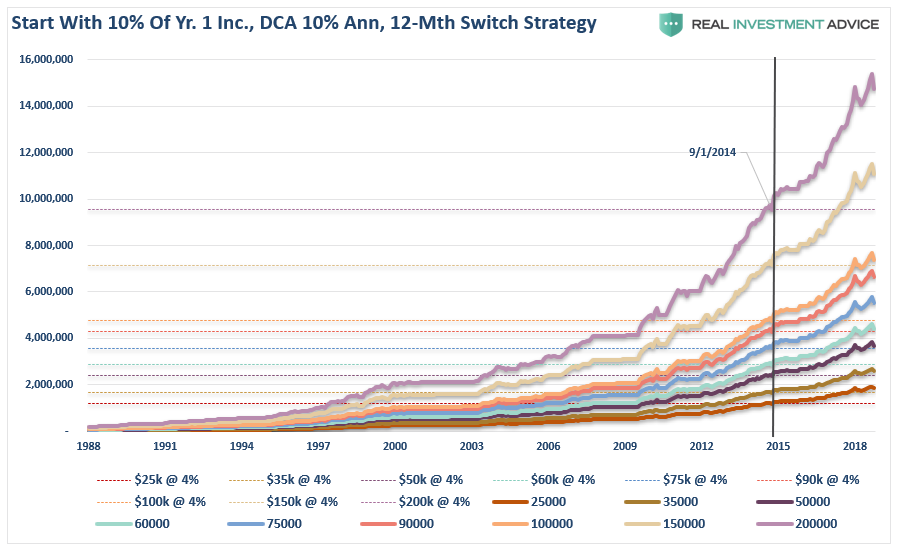

There are many ways to approach managing portfolio risk and avoiding more major “mean reverting”events. While we don’t recommend or suggest that you try to “time the market” by being “all in” or “all out,” it is critical to avoid major market losses during the accumulation phase. As an example, the chart below shows how using a simple 12-month moving average to avoid major drawdowns can impact long-term returns. We used the same 10% savings rate as above, dollar cost averaged into an S&P 500 index on a monthly basis, and moved to cash when the 12-month moving average is breached.

By avoiding the drawdowns, our young saver not only succeeded in reaching their goals but did so 31-months sooner than our example of saving 50% annually. It doesn’t matter what methodology you use to minimize risk, the end result will be same if you can successfully navigate the full-cycles of the market.

You Can Do This

Last week, we laid out some suggestions on what you can do to build savings. This week will add the suggestions for the investing side of the equation.

It’s all about “cash flow.” – you can’t save if you don’t have positive cash flow.

Budget – it’s a four-letter word for most Americans, but you can’t have positive cash flow without it.

Get off social media – one of the biggest impacts to over spending is “social media” and “keeping up with the Jones’.” If advertisers were getting your money from social media they wouldn’t advertise there.

Get out of debt and stay that way. No, you do not need a credit card to build credit.

If you can’t pay cash for it, you can’t afford it. Do I really need to explain that?

Expectations for future returns should be downwardly adjusted. (You aren’t going to make 6% annually)

The potential for front-loaded returns going forward is unlikely.

Control investment behaviors and emotions that detract from portfolio returns is critical.

Future inflation expectations must be carefully considered.

Account for “variable rates of returns” in your plan rather than “average” or “compound.”

Understand risk and control drawdowns in portfolios during market declines.

Save money regularly, invest when reward outweighs the risk.Cash is always an alternative.

Lastly, remember that “time” is your most valuable commodity and is the only thing we can’t get more of.

via ZeroHedge News http://bit.ly/2RuyfjA Tyler Durden

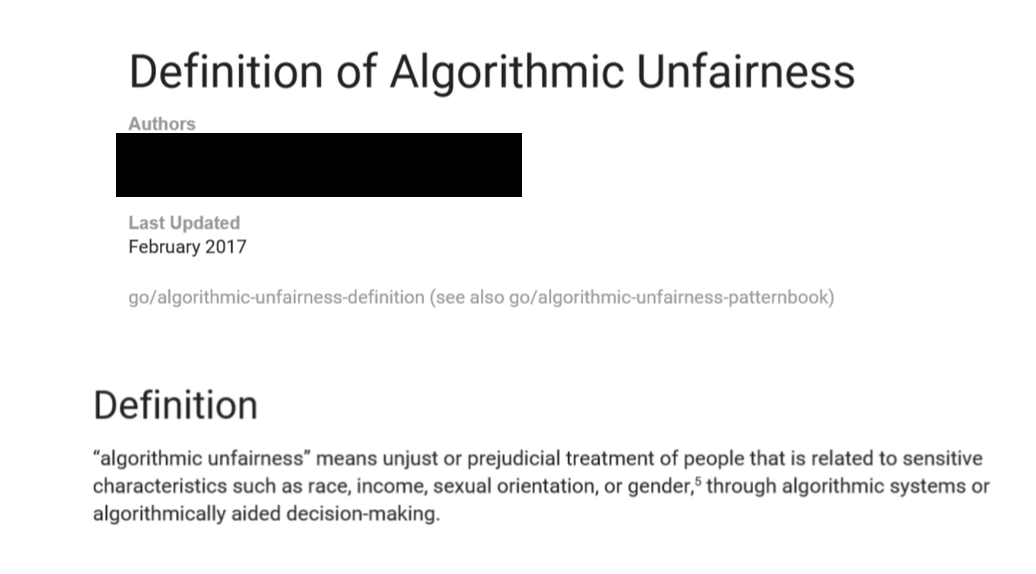

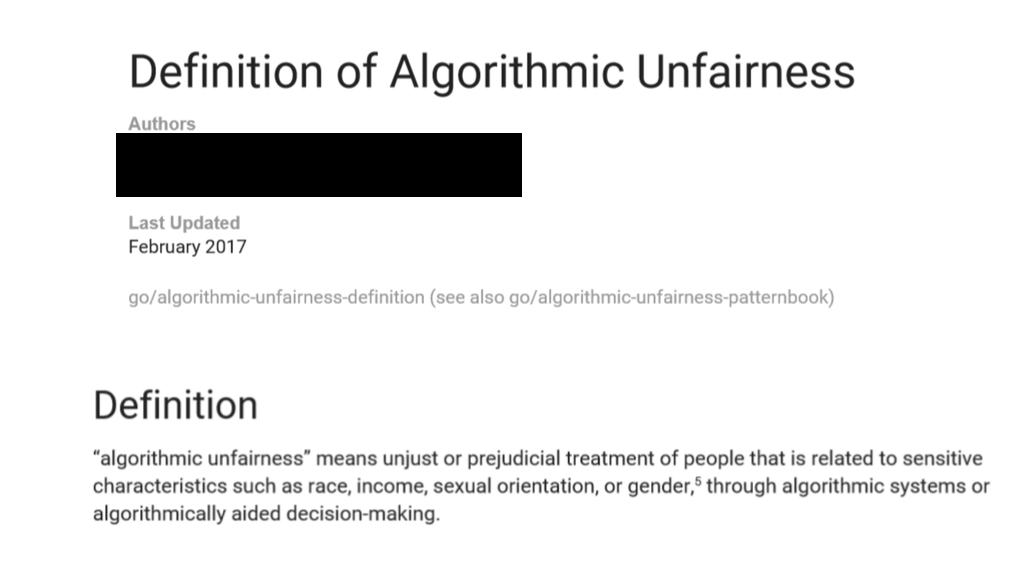

A new undercover exposé by Project Veritas reveals that the company is programming its machine learning algorithms in order to avoid the “next Trump situation.”

“We all got screwed over in 2016, again it wasn’t just us, it was, the people got screwed over, the news media got screwed over, like, everybody got screwed over so we’re rapidly been like, what happened there and how do we prevent it from happening again,” said longtime Google employee and head of “Responsible Innovation,” Jen Gennai.

“We’re also training our algorithms, like, if 2016 happened again, would we have, would the outcome be different?” she added.

Gennai says that Elizabeth Warren’s proposal to break up Google is ‘very misguided,’ because “all these smaller companies who don’t have the same resources that we do will be charged with preventing the next Trump situation, it’s like a small company cannot do that.”

Meanwhile, a Google insider who came forward to Veritas confirmed what they filmed Gennai admitting; that the company is using “Machine Learning Fairness” as just one of several political tools used to promote their political agenda by combating “algorithmic unfairness.”

Via Project Veritas

Of course, as Gennai puts it: “We have gotten accusations of around fairness is that we’re unfair to conservatives because we’re choosing what we find as credible news sources and those sources don’t necessarily overlap with conservative sources …“

As an aside, Project Veritas’s James O’Keefe tweeted on Monday that Reddit has suspended their account.

Reddit SUSPENDED @Project_Veritas account. We discovered this as we tried to post a link to today’s Google insider story. You can see the full report on our website: https://t.co/8DWus8E4ia

By the summer of 1936, Europe was in a state of perpetual crisis. Hitler’s rise to power, German invasion of the Rhineland, Spanish Civil War, Fascist Coup attempt in France, etc. World War was just a few years away.

25-year old Scotsman with a proper Scottish name– Fitzroy MacLean, who was in the His Majesty’s Foreign Service, was on his way from Paris to his new post in Moscow, where he would spend the next few years of his life traveling around the Soviet Union… and specifically Eurasia.

No Westerner had been to the region for decades.

He wrote his memoirs of the trip in a great book called Eastern Approaches. It’s a must read for any travel lover. To give you a flavor of the book, Maclean describes a night he spent in a dingy basement room at an inn where the floor above him was a restaurant:

At a point which must have been just above my bed a team of six solidly built Armenians were executing, with immense gusto, a Cossack dance, kicking out their legs to the front and sides and springing in the air, to the accompaniment of a full-sized band and of frenzied shouting and hand-clapping from all present. There was no hope of sleep. I ordered a bottle of vodka and decided to make a night of it.

Maclean writes very fondly of Almaty, then the capital city of the Soviet republic of Uzbekistan

Alma Ata must be one of the pleasantest provincial towns in the Soviet Union. . .

In Kazakh its new name means ‘Father of Apples’, an appellation which it fully merits, for the apples grown there are the finest in size and flavour that I have ever eaten. The central part of the town consists of wide avenues of poplars at right angles to one another.

In some respects, very little has changed. Almaty is still very much a provincial town– quiet, picturesque with tree-lined streets and bazaars.

It’s no longer the capital– that distinction is in a city formerly known as Akmolinsk, which became Akmola, and was then renamed Astana in the 1990s, and renamed again to Nursultan a few months ago.

Almaty is more quaint and traditional than Astana/Nursultan. It’s incredibly cheap.

Gasoline is about 40c per liter, less than $1.50 per gallon.

Kazakhstan’s economy is a one-trick pony. But it’s a great trick… one that has created a lot of wealth.

70% of exports are energy. #1 producer of uranium, with roughly 40% of the world’s supply. Top producer of coal, oil, and gas.

Limited population… smaller than metropolitan Paris, but larger than all of Western Europe combined.

So this has had a hugely beneficial impact that has actually trickled down and created a robust middle class.

You can see a lot of wealth. Nice houses, nice apartments, nice cars. Incredible infrastructure– highways better than what I’ve driven on in North America and Europe.

Despite that economic success and robust growth, this is definitely not a place for a casual entrepreneur. Large scale energy or agricultural project, sure.

What’s really compelling is for people who are location-independent… who can take their work with them and roam from place to place. Tens of millions of people, more and more every day.

Kazakhstan ticks the boxes… sufficient Internet speed (minor censoring that’s easy to get around with VPNs), incredibly cheap.

Good lifestyle– plenty of nightlife, plush shopping malls and restaurants.

Remote, but easy to get to. Air Astana flies to plenty of gateway cities like Bangkok, Hong Kong, Beijing, Dubai, Moscow, etc. plus other major airlines fly to/from Frankfurt, Istanbul.

But there are lots of cheap places with decent Internet.

What’s really exceptional about this place is the outdoors… it’s Disneyland for nature lovers.

20 minutes in one direction and you’re in the Tien Shan: Mountains of Heaven. Ski resorts, hiking, cable car rides, pristine alpine lakes.

20 minutes in the other direction and you’re in the vast open plains… the legendary steppe grasslands of central Eurasia that extend all the way to Mongolia.

I spent some time here en route to Uzbekistan for our Total Access trip. Wild horses across the infinite openness. Some of the most scenic vistas I’ve ever seen traveling across 120+ countries on all seven continents.

And no one else around. You feel like you’re on your own planet. No endless nuisance of rules and signs telling you what to do, where to go, etc. Just beauty and freedom.

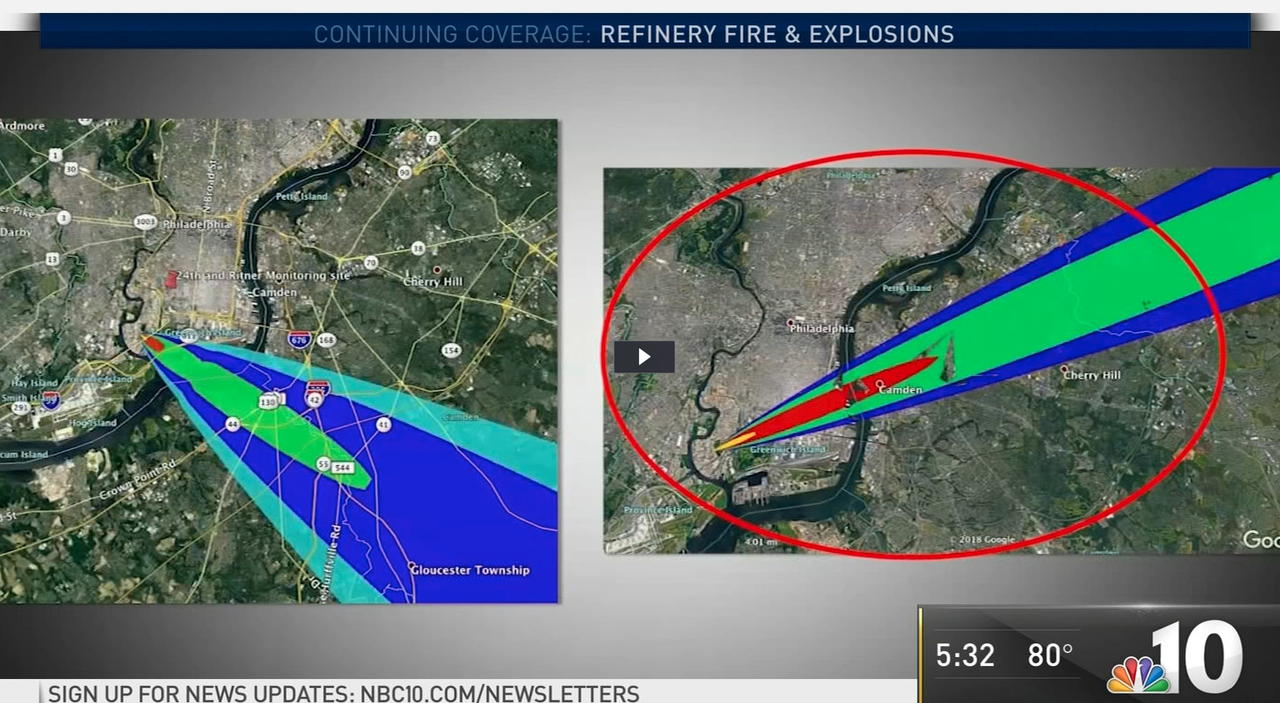

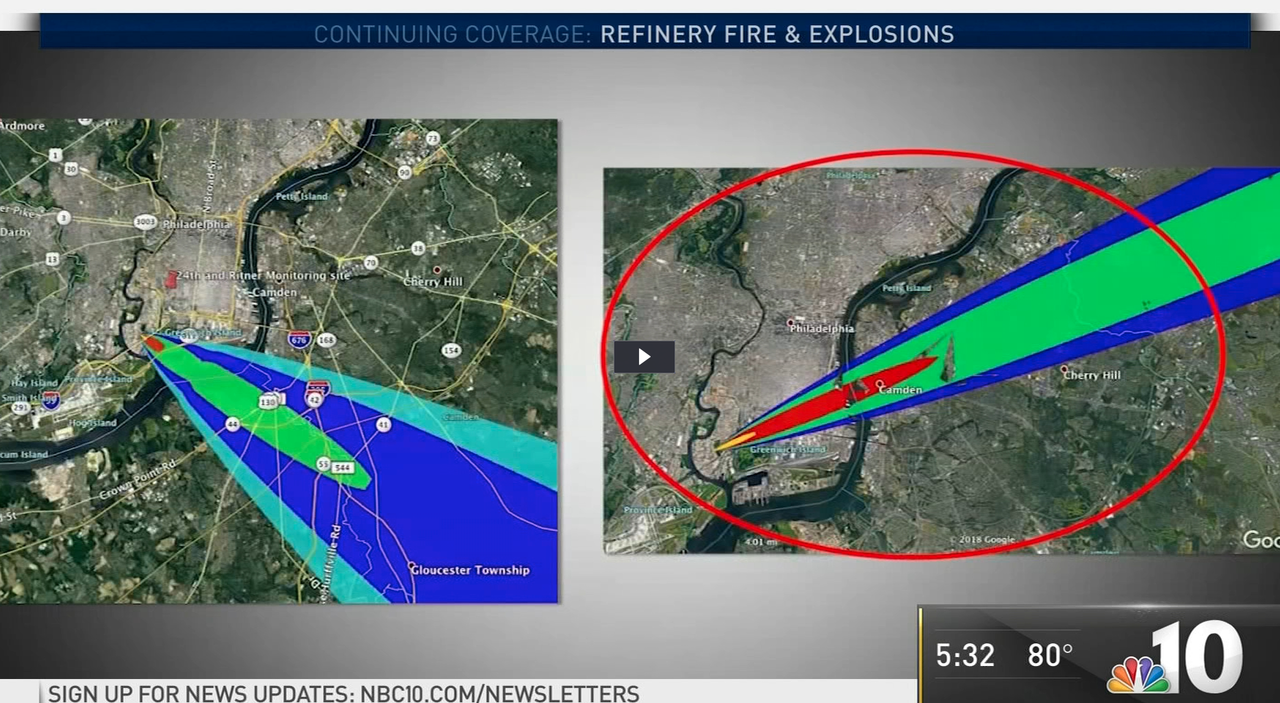

Following the explosion and subsequent inferno at Philadelphia Energy Solutions’ oil refinery last week, its alkylation unit has been “completely destroyed”. After fire tore through the east coast’s largest refinery, workers are now getting a chance to finally assess some damage that will hamper the normal production of fuel going forward.

According to Reuters, the refinery could remain shut down for an extended period of time even though NBC Philadelphia reported on Sunday that the blaze had finally been extinguished and air quality testing in the area was taking place. Philadelphia Deputy Fire Commissioner Craig Murphy said that the cause of the fire remained unclear on Friday, but reports did say that “the gas valve that had been fueling the blaze was shut off and the tank involved in the explosion was isolated”.

Following the plume from the explosion – NBC Philadelphia

So far, air quality testing has not found anything unsafe, according to officials.

After a leak in an alkylation unit, an explosion sent the complex ablaze, forcing the Girard Point section of the refinery to shut down. The Point Breeze section had already been under repair due to a fire earlier this month. Due to the fact that it is a chemical fire, officials said last week that it could burn for a lengthy amount of time.

— hood’s favorite vegan (@1nicetownbean) June 21, 2019

Four staff members are reported to have suffered minor injuries as a result of the explosion. Mayor Jim Kenney said: “My initial reaction was ‘Damn, this is bad. It was a frightening scene. I’m thankful that no one got killed or seriously injured.”

“We will see what the federal and state authorities say, if that’s what is called for that’s what we will do,” Kenney continued.

Neighbors are protesting the refinery, with one telling NBC: “I have witnessed it for years, blowing up. This is bad, people. Enough is enough.”

Recall, our last article on the refinery fire pointed out that gasoline futures spiked the day of the incident.

The Philadelphia refinery is “the largest such plant on the U.S. East Coast and the main supplier to the local gasoline market.”

Gasoline demand nationwide was already at a record last week, nearing 10 million barrels per day.

via ZeroHedge News http://bit.ly/31SI13C Tyler Durden

Following statements on Meet the PressSunday where he said “I was against going into the Middle East,” and lamenting that “we’ve spent 7 trillion dollars” there, Trump continued his theme of drawing down in the region on Twitter, saying Monday morning it’s time for China and others to protect their own ships in the Persian Gulf.

“China gets 91% of its Oil from the Straight, Japan 62%, & many other countries likewise.” Trump tweeted, making the common mistake of spelling the word “strait” wrong.

“So why are we protecting the shipping lanes for other countries (many years) for zero compensation,” he questioned. “All of these countries should be protecting their own ships on what has always been a dangerous journey.”

….a dangerous journey. We don’t even need to be there in that the U.S. has just become (by far) the largest producer of Energy anywhere in the world! The U.S. request for Iran is very simple – No Nuclear Weapons and No Further Sponsoring of Terror!

“We don’t even need to be there in that the U.S. has just become (by far) the largest producer of Energy anywhere in the world! The U.S. request for Iran is very simple – No Nuclear Weapons and No Further Sponsoring of Terror!” he concluded.

There was no immediate reaction in oil price in response to Trump’s signaling the US could be no longer willing to protect international shipping following the June 13 tanker attack incident in the Gulf of Oman, and following last week’s dramatic events which almost witnessed the US and Iran go to war.

Indeed according to 2018 figures some 62% of Japan’s oil does get imported via the Strait of Hormuz; however, China’s imports are more diverse (Trump claimed 91% comes through the strait), given its diverse network of oil imports, notably also a pipeline from Russia.

via ZeroHedge News http://bit.ly/2N9cveC Tyler Durden

It’s hard to tell whose bluff was called last week, but the end result is that almost every systemically important central bank did more than blink. They caved.

The question is, did they do so to keep the fun alive?

Because they know something that they are loathe to tell us?

Or have they finally and totally given up faith in their government counterparts?

It surely isn’t because they have suddenly realized, en masse, that inflation, as they choose to measure it, hasn’t reached the arbitrary 2% target.

Whatever the reason, and despite equity markets and related risk assets having a field day, there isn’t a great deal to celebrate.

There should be no comfort taken that a Fed president argued for a 50 basis point rate cut and wasn’t laughed out of the room.

That 10-year Treasury yields are back down to current levels is a clear sign that the battle is being lost. It’s a shame that it would probably take an oil shock that would adversely affect consumer lifestyles to perk up the spirits of central bankers who think it’s fun to contemplate how far below zero rates can go without doing any harm.

Efforts are being made to lower market expectations for the outcome of trade talks at the G-20 meeting. That’s a shame. Rate cuts are worse than an inadequate substitute for real progress. At this point, they are positively harmful. As are currency wars. And they put the burden of responsibility to act on the wrong people.

Continuing to respond to all difficulties through fiddling with short-term interest rates exposes the defining characteristic of our economic times: that financial conditions being kept at elevated levels is the primary way policy-makers validate their understanding of how well they are doing. Is there any other way of understanding who they think of as their constituency?

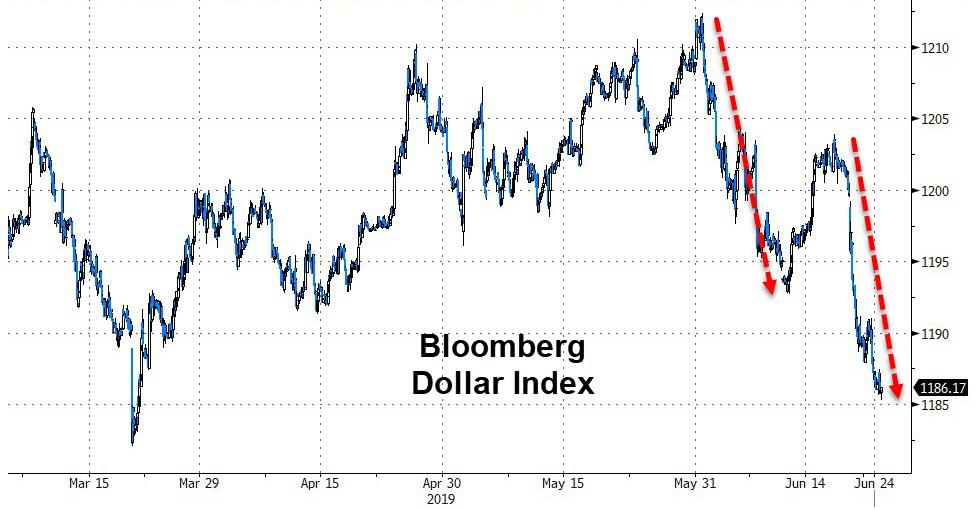

The dollar is trading horribly. And that’s a crying shame.

Last week’s CFTC data showed an out-sized rotation out of the U.S. currency and into the euro and yen. That helps no one.

One of the most-cited reasons is that the Fed has room to out-cut the other central banks. That’s pathetic.

Nevertheless, with the break below support at the 200-day moving average that had previously contained this year’s sell-offs in the Dollar Index, the next technical target is 95.75.

Through there and this thing will look ugly. It shouldn’t give way easily. But, if it does, it could prompt responses from competing central banks that would further solidify the beliefs of those who reasonably posit that there is no escape from the policy regimes that we were sold as easily reversed.

via ZeroHedge News http://bit.ly/2RFN5nz Tyler Durden

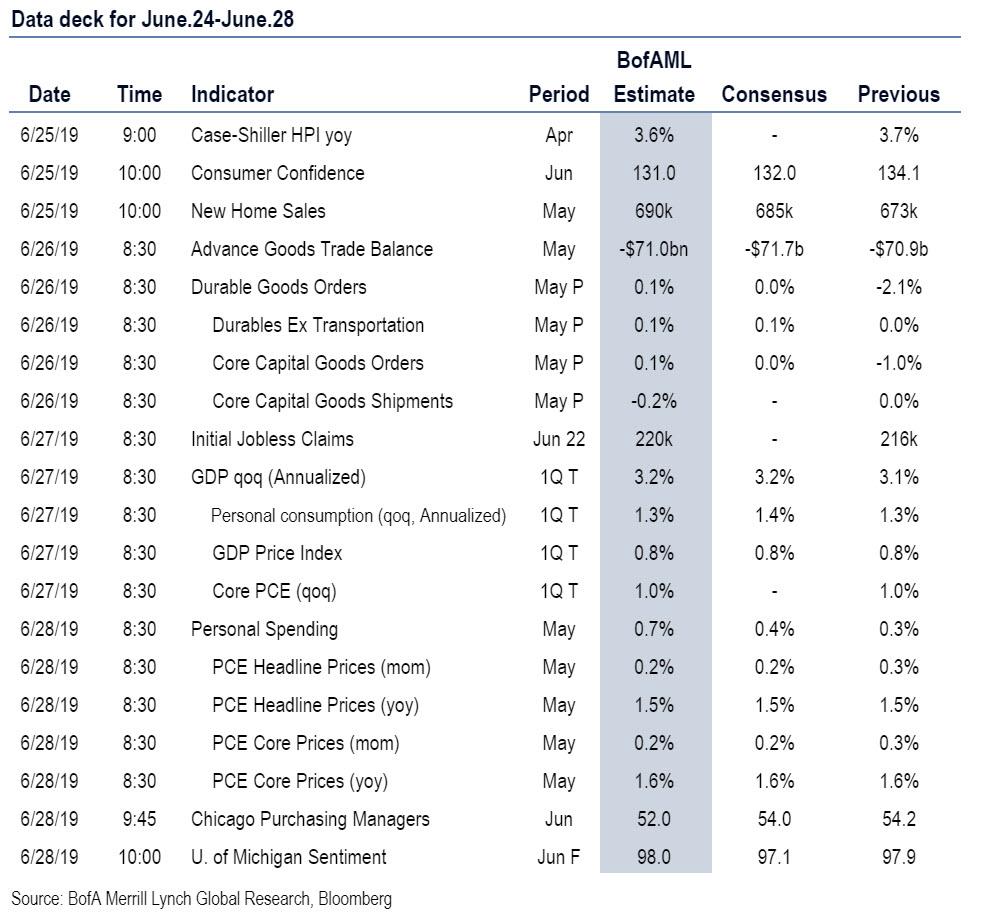

Now that the Fed’s capitulation is complete and “Powell has thrown in the towel”, bending the knee to Trump, the event baton passes from central banks to politicians this week with the big highlight being the G-20 summit and a potential meeting between President’s Trump and Xi. Prior to that, DB’s Craig Nicol writes that there is still the possibility of a confrontational speech on China by Vice President Pence. Meanwhile, data highlights include PCE inflation in the US and preliminary June CPI reports in Europe. We’ll also get plenty of survey data in the US. Fed Chair Powell will speak and part two of the Fed’s stress tests results will be released.

Touching on those in more detail, the G-20 summit in Osaka next week will take place on Friday and Saturday. Expectations are that Trump and Xi will meet on the sidelines of the summit to continue trade negotiations that had seemingly broken down last month. Rhetoric in recent days from both sides has signaled an openness to resume discussions and consensus expects a talk but no deal driven by the intuition that both sides would still like to avoid an economically fatal escalation in tensions, and given that both heads of state would be personally invested in this meeting. The main thing to watch in this case is how short the fuse is on a final deal; i.e. if and for how long the next round of US tariffs are put on hold. In any case, the meeting should provide some direction for markets on where the trade war is heading next.

Prior to this, on Monday US Vice President Pence is tentatively scheduled to give a speech on China. This is the speech which was initially scheduled for the anniversary of the Tiananmen Square massacre, which President Trump delayed to avoid potentially raising tensions with Beijing ahead of a potential meeting with Xi at the G-20. Therefore, it remains to be seen if the speech will still go ahead for the same reason. Bloomberg have reported that there are staff-level disputes over the actual content of the speech with some advocating for a delay. However the same story also suggests that Trump supports Pence in delivering it.

As for data, we’ll have to wait for Friday for the main event with the May PCE inflation report in the US. The consensus is for a +0.2% mom reading for the core PCE which would leave the year-on-year rate at +1.6% and therefore below the Fed’s target. We will also get preliminary June CPI readings due in Europe including data for Germany and Spain on Thursday, and France, Italy and the Euro Area on Friday. The IFO survey in Germany on Monday is also worth a watch.

Other data worth flagging in the US includes the preliminary May durable and capital goods orders data on Wednesday and the third and final revision of Q1 GDP on Thursday. The current expectation is for growth to be lifted one-tenth to +3.2%. Also worth flagging are the various regional Fed surveys. We’ve got June surveys due from the Dallas Fed on Monday, Richmond Fed on Tuesday, Kansas Fed on Thursday and then the Chicago PMI on Friday. A reminder that two of the June surveys that we got this week – the empire manufacturing and Philly Fed business outlook – were mixed. The June consumer confidence reading is also due on Tuesday and final revisions to the June University of Michigan consumer sentiment on Friday.

As for Fedspeak, Powell is due to speak on Tuesday evening in New York to a council on foreign relations. On the same day we’re also due to hear from Williams, Bostic, Barkin and Bullard at separate events. Harker also speaks this weekend on Sunday.

Over at the ECB we’re due to hear from Nowotny on Thursday while the BoE’s Carney and colleagues testify on the May inflation report on Wednesday. Also worth flagging at the Fed will be Thursday’s results from part two of its annual bank stress tests. This will confirm which banks have sufficient capital to increase dividends and share buybacks. The results from part last Friday showed that, surprise, all banks passed.

As for other things to watch out for next week, this weekend leaders from the Association of South Asian Nations meet for their annual summit. On Tuesday President Trump’s Middle East advisers are due to hold an economic development summit in Bahrain. On Wednesday NATO defence ministers are due to meet in Brussels for two days of talks. Also on Wednesday, twenty contenders for the Democratic presidential nomination are due to debate over two nights including Senator Elizabeth Warren and front runner Joe Biden. Finally, on Thursday the Mexico central bank rate decisions is due.

Courtesy of Deutsche Bank, here are the key events broken down by day:

Monday: Data releases include the June IFO survey in Germany as well as the May Chicago Fed survey for May and Dallas Fed survey for June in the US. Elsewhere, US Vice President Pence is tentatively scheduled to give a speech on China.

Tuesday: Overnight, the BoJ minutes will be released while data in Europe includes June confidence indicators in France and June CBI survey data in the UK. In the US we’ll get the April FHFA house price index, April S&P CoreLogic house price index, June Richmond Fed survey, May new home sales and June consumer confidence. The Fed’s Powell, Williams, Bostic, Barkin and Bullard are all due to speak.

Wednesday: Data in Europe includes July consumer confidence in Germany while in the US we’re due to get the preliminary May durable and capital goods orders data, May advance goods trade balance and May wholesale inventories. The BoE’s Carney, Cunliffe, Tenreyro and Saunders are due to testify before the Parliament’s Treasury Committee on the May inflation report. Meanwhile, NATO defence ministers will meet in Brussels for two days of discussions, while the contenders for the US Democratic presidential nomination will start two days of debates.

Thursday: Overnight, May retail sales data in Japan is due to be released along with May industrial profits in China. In Europe we get preliminary June CPI readings in Germany and Spain while in the US the third reading of Q1 GDP is due along with the latest weekly jobless claims reading, May pending home sales and June Kansas Fed survey. The ECB’s Nowotny is also due to speak, while part two of the Fed’s stress test results will be released.

Friday: The G-20 meeting in Osaka will begin, continuing into the weekend with the expectation that President’s Trump and Xi will meet on the sidelines. The data highlight is the May PCE inflation report in the US. Prior to that we’ll get May industrial production and employment data in Japan, preliminary June CPI in France, Italy and for the Euro Area, and final Q1 GDP revisions for the UK. In the US we’ll also get the May personal spending and income data, June MNI Chicago PMI and final June revisions for the University of Michigan consumer sentiment survey.

Finally, focusing on just the US, Goldman writes that “the key economic data release this week is the core PCE report on Friday. There are several scheduled speaking engagements from Fed officials this week, including from Chair Powell on Tuesday. The G20 Summit will take place on Friday and Saturday, June 28-29 in Osaka, Japan.”

Monday, June 24

There are no scheduled major economic data releases.

Tuesday, June 25

08:45 AM New York Fed President Williams (FOMC voter) speaks: Federal Reserve Bank of New York President John Williams will give opening remarks at the OPEN Finance Forum in New York. Prepared text is expected; audience Q&A is not expected.

09:00 AM FHFA house price index, April (consensus +0.2%, last +0.1%)

09:00 AM S&P/Case-Shiller 20-city home price index, April (GS +0.2%, consensus +0.1%, last +0.1%): We estimate the S&P/Case-Shiller 20-city home price index increased by 0.2% in April, following a 0.1% increase in March. Our forecast largely reflects the appreciation in other home prices indices such as the CoreLogic house price index in April.

10:00 AM Conference Board consumer confidence, June (GS 132.1, consensus 131.0, last 134.1): We estimate that the Conference Board consumer confidence index declined by 2.0pt to 132.1 in June, reflecting a drag to confidence from negative employment headlines.

10:00 AM Richmond Fed manufacturing index, June (consensus +4, last +5)

10:00 AM New home sales, May (GS +1.4%, consensus +1.8%, last -6.9%): We estimate that May new home sales rebounded by a modest +1.4% in May from a 6.9% decline in April. Single family permits declined in the two prior months, and mortgage applications were somewhat weak.

12:00 PM Atlanta Fed President Bostic (FOMC non-voter) speaks: Federal Reserve Bank of Atlanta President Raphael Bostic will speak on a panel on housing issues in Atlanta.

01:00 PM Fed Chair Powell (FOMC voter) speaks: Federal Reserve Chair Jerome Powell will give a speech on monetary policy and the economic outlook at the Council on Foreign Relations in New York. Prepared text and audience Q&A are expected.

03:30 PM Richmond Fed President Barkin (FOMC non-voter): Federal Reserve Bank of Richmond President Barkin will participate in a moderated discussion on the outlook for US-Canada business relationship.

06:30 PM St. Louis Fed President Bullard (FOMC voter) speaks: St Louis Fed President James Bullard will give welcoming remarks at a lecture at the St. Louis Fed.

Wednesday, June 26

8:30 AM Durable goods orders, May preliminary (GS -4.0%, consensus flat, last -2.1%); Durable goods orders ex-transportation, May preliminary (GS flat, consensus +0.1%, last flat); Core capital goods orders, May preliminary (GS +0.1%, consensus +0.1%, last -1.0%); Core capital goods shipments, May preliminary (GS -0.3%, consensus +0.1%, last flat): We expect durable goods orders retrenched by 4.0% further in May, mostly reflecting a further decline in commercial aircraft orders. We estimate core capital goods orders edged up by 0.1% and core capital goods shipments declined by 0.3%, as global manufacturing trends remain soft.

08:30 AM Advance goods trade balance, May (GS -$70.9bn, consensus -$71.4bn, last -$72.1bn): We estimate that the goods trade declined slightly to $70.9bn in May, following a decline in inbound container traffic.

08:30 AM Wholesale inventories, May (last +0.8%): Retail inventories, May (last +0.5%)

Thursday, June 27

08:30 AM GDP (final), Q1 (GS +2.9%, consensus +3.2%, last +3.1%); Personal consumption, Q1 (GS +0.9%, consensus +1.0%, last +1.3%): We expect a two-tenths downward revision in the final estimate of Q1 GDP to +2.9%, mainly reflecting an expected downward revision to consumer spending, partially offset by an upward revision to state and local government spending.

08:30 AM Initial jobless claims, week ended June 22 (GS 220k, consensus 218k, last 216k); Continuing jobless claims, week ended June 15 (last 1,662k): We estimate jobless claims increased by 4k to 220k in the week ended June 22, after decreasing by 6k in the prior week. There are no auto plant shutdowns this week.

10:00 AM Pending home sales, May (GS +1.5%, consensus +1.0%, last -1.5%): We estimate that pending home sales rose by 1.5% in May based on regional home sales data, following a 1.5% decline in April. We have found pending home sales to be a useful leading indicator of existing home sales with a one- to two-month lag.

Friday, June 28

08:30 AM Personal income, May (GS +0.4%, consensus +0.3%, last +0.5%); Personal spending, May (GS +0.6%, consensus +0.5%, last +0.3%); PCE price index, May (GS +0.15%, consensus +0.2%, last +0.31%); Core PCE price index, May (GS +0.18%, consensus +0.2%, last +0.25%); PCE price index (yoy), May (GS +1.45%, consensus +1.5%, last +1.51%); Core PCE price index (yoy), May (GS +1.54%, consensus +1.6%, last +1.57%): Based on details in the PPI, CPI, and import price reports, we forecast that the core PCE price index rose 0.18% month-over-month in May, or 1.54% from a year ago. Additionally, we expect that the headline PCE price index increased 0.15% in May, or 1.45% from a year earlier. We expect a 0.4% increase in personal income in May and a 0.6% increase in personal spending.

09:45 AM Chicago PMI, June (GS 53.0, consensus 53.8, last 54.2): We estimate that the Chicago PMI declined by 1.2pt in June, following a 1.6pt increase in May. Previous regional surveys have been weaker, but the Chicago survey timing suggests some scope to outperform.

10:00 AM University of Michigan consumer sentiment, June final (GS 97.5, consensus 97.9, last 97.9): We expect the University of Michigan consumer sentiment index to edge down by 0.4pt to 97.5 in the final estimate for June. The resolution of the trade and immigration dispute with Mexico concluded after the preliminary reading, but we expect a possible drag from negative employment-related headlines. The report’s measure of 5- to 10-year inflation expectations dropped by four tenths to 2.2% in the preliminary report for June.

Source: Deutsche Bank, Goldman, BofA

via ZeroHedge News http://bit.ly/2WVDE4g Tyler Durden

Two “eurofighter” jets belonging to the German air force have crashed over the Müritz region in Mecklenburg-Vorpommern, according to Die Welt.

Video of the crash can be seen below:

The circumstances surrounding the accident, and the fate of the pilots, remains unclear. The two machines were said to have touched in the air around 2 pm local time, before crashing to the earth. Firefighters and rescue workers have hurried to the crash site.

via ZeroHedge News http://bit.ly/2WXIf61 Tyler Durden

Having confirmed his view over the weekend that he has the power to demote Fed Chair Jay Powell, President Trump has taken to Twitter this morning to explain his thoughts as to how the central bank – more specifically Powell – has hurt the economy and market (and implicitly his election chances).

Trump started by claiming that the “Federal Reserve that doesn’t know what it is doing” citing the following as why they are clueless: “raised rates far to fast (very low inflation, other parts of world slowing, lowering & easing) & did large scale tightening, $50 Billion/month” but noting that despite all that “we are on course to have one of the best Months of June in U.S. history.” This will be the best June since 1995 if these gains hold until the G-20.

Despite a Federal Reserve that doesn’t know what it is doing – raised rates far to fast (very low inflation, other parts of world slowing, lowering & easing) & did large scale tightening, $50 Billion/month, we are on course to have one of the best Months of June in U.S. history..

And then he forecasts what could have been if “the Fed had gotten it right”… “Thousands of points higher on the Dow, and GDP in the 4’s or even 5’s.”

Trump then gets personal: “Now they stick, like a stubborn child, when we need rates cuts, & easing, to make up for what other countries are doing against us. Blew it!”

….Think of what it could have been if the Fed had gotten it right. Thousands of points higher on the Dow, and GDP in the 4’s or even 5’s. Now they stick, like a stubborn child, when we need rates cuts, & easing, to make up for what other countries are doing against us. Blew it!

With stocks at record highs and market expectations for Fed dovishness at record highs, Trump is right on one thing, if Powell doesn’t do as the market wants, there will be carnage.

via ZeroHedge News http://bit.ly/2Y8GbcM Tyler Durden

{kind=link}

{kind=link}