Just as The S&P was heading towards its best 7-day win-streak since 2003, a long-weekend of reflection on reality ruined the party – not helped by Wal-Mart’s biggest earnings-driven gap-down in years. (Nasdaq failed to hold green)

Futures show the utter idiocy of yesterday’s trading (the plunge at the cash open – that didn’t happen)…

The Dow fell back below 25k this afternoon, having failed to hold its 61.8% Fib retracement and testing back to the 50% level…

The S&P fell back below its 50DMA…

Small Caps are back in the red (with Trannies) for 2018…

Ugly day for the FANG stocks..

VIX pushed back above 20…

And for those looking to pin the blame on Wal-Mart, note that The Dow really did not react to WMT’s moves (and by the close WMT was just 70 of The Dow’s 300-plus point drop…

Treasury yields were all higher from Friday but the last hour of the day, as stocks were slammed, saw bonds bid and the mid- to long-end rally notably…

For the first time since President Trump signed it into law late last year, the Republican tax-reform plan has more supporters than opponents, according to the New York Times.

The law’s increasing popularity, which is likely tied to the fact that workers are beginning to see the withholding savings materialize in their paychecks, is also buoying Republicans’ chances during the upcoming 2018 midterm elections, which were previously expected to be a rout for the party, which controls both houses of Congress – but holds only a one-vote majority in the Senate. It also follows a multimillion-dollar effort to convince consumers of the law’s benefits.

And, in another sentence we bet you never thought you’d read in the New York Times, the paper admits that the law’s growing popularity is eroding the Democrats’ lead in election polling for 2018. Dozens of Republican lawmakers opted to announce their retirement last year instead of face a difficult reelection campaign, but at least a few of them – including Tennessee Sen. Bob Corker – are reportedly reconsidering that decision.

While most of the law’s newfound supporting is coming from Republicans, the tax bill is winning over more Democrats than many of Trump’s other, more controversial, policies. Support for the law remains low among Democrats, but it has doubled in the past month. Democrats’ approval of the tax bill is twice as high as their approval of Trump.

Overall, 51% of Americans approve of the law, while 46% disapprove. By comparison, approval was 37% in December.

Democratic support, meanwhile, has grown from 8% in December to 19% when the poll was taken.

Even Democratic strategists are beginning to worry about the implications of this troubling trend…

“It’s less of a sure bet than it was in December,” he said. “This isn’t a problem yet for Democrats, but the movement isn’t a positive one.” According to the Times,Dems have done little to counteract the Republican messaging on tax reform…

Unsurprisingly, the Times blames the bump in polling on – what else? – Americans overestimating the benefits they will receive from the tax law.

Just under one in five respondents expect to see either a raise or a bonus thanks to the law’s business tax cuts. Early returns from public companies indicate that’s an overshot. Just Capital, a nonprofit research organization analyzed the 90 largest public companies that have announced how they will spend the combined $45 billion in savings they stand to receive from the tax bill this year.

It found that those companies planned to pass 6% of those savings directly on to workers, with more than half of that spending in one-time bonuses.

“That doesn’t really track to how the public thinks the companies should be spending the money,” said Martin Whittaker, Just Capital’s chief executive.

Only one in three respondents expects to see a tax cut from the law.

…

Close to half of Americans now expect some direct benefit from the law, either a tax cut or a salary increase or a bonus. Support for the law is far stronger among that group, with more than three-quarters of Americans approving of the law..

Sarah Huckabee Sanders lauded the polling results in a tweet.

Other than Nancy Pelosi and her Democratic allies, who could be against lower taxes, higher wages, and a booming economy? https://t.co/ZGmZxjwGkj

And she’s not the only one: Rep. Kevin Cramer of North Dakota cited Sen. Heidi Heitkamp’s vote against the law as one of his reasons for running against her when he announced his candidacy.

However, unsurprisingly, The Daily Caller reports that, after weeks of dismissing the Republican tax plan as one that only benefits the wealthy — and giving time to pundits who predicted far more apocalyptic consequences, MSNBC and CNN have given zero coverage to a survey showing a majority of Americans approving of the bill.

According to tv clipping service Grabien, which logs transcripts from all network shows over the last year, not a single individual on CNN or MSNBC mentioned the public’s dramatic turnaround in support for the tax bill that saves average American families thousands of dollars annually after The Daily Caller News Foundation conducted a search for “New York Times” and “Tax Reform.”

A search on both CNN and MSNBC’s website for any story showing the tax bill’s popularity also curiously revealed no coverage either.

Which further indicates the left-leaning media’s ignorance of real America; as according to the latest University of Michigan survey on consumer sentiment, released last week, government policies were cited in January and early February by the largest percentage of American households in a half century as a reason for optimism. Some 35% of respondents said as much, an indication that the Trump tax plan is resonating.

Optimism about government policy direction’s implications for business conditions climbed during Trump’s first year, dwarfing levels seen during the prior administration…

“Share buybacks are like a giant synthetic short-volatility position.“

Bloomberg explains the logic: Companies over the past decade or so have significantly increased buybacks to the point where they are now collectively the largest single buyer of stocks. Some have called the market self-cannibalizing. Equity shrink is the nicer way to say that.

As Matt Maley, a strategist at Miller Tabak & Co, told Bloomberg,

“The corporate buying — they were basically the only buyers last week,’’

And for now that is true, but

“Whenever we have forced selling take place, the buyers disappear and the sellers have to sell no matter what. And corporate buybacks are not going to be enough.”

The problem is – what happens next, as debt costs spike, it will become harder for C-level execs, no matter how desperate to juice their compensation-dependent stock prices, to justify the balance sheet leverage to buyback shares in a market whose Fed Put appears to have been removed…

But, just like XIV’s termination event “could never happen,” there are numerous factors that leave that irrational corporate buyback-er as anything but a sure thing. Just ask GE (as it loaded up massively in 2016 to ‘defend’ its share price, only to see it collapse)…

Vineer Bhansali, the chief investment officer of LongTail Alpha, who has warned about the volatility bubble, told Bloomberg that buybacks can suppress volatility for the right reasons. When companies produce more cash than they can productively reinvest in their businesses, they buy back stock, lifting prices and curbing volatility.

The problem, as has increasingly been the case, comes when companies fund buybacks by taking on more debt rather than with the cash generated by their operations.

That’s when repurchases become part of the leveraged low-volatility trade that can unwind disastrously when interest rates rise.

And as we first pointed out over two years ago, all net debt issuance in the 21st century has been used to pay for stock buybacks…

Which may be an imminent issue as the total cost of funding debt for buybacks is soaring…

The $171 billion in YTD stock buyback announcements is the most ever for this early in the year. In fact, it is more than double the prior 10 year average of $77 billion in YTD buyback announcements.

Incidentally, the record burst of stock buybacks was arguably the key driver behind last week’s miraculous stock rebound.

“It acts as a floor, you have a natural buyer in there,” Birinyi’s Jeff Rubin told CNBC. “At the end of the third quarter, companies had dry powder of over $800 billion,” he said. Fourth quarter actual purchases are not yet available.

But, as Bloomberg concludes, those pointing the finger at buybacks say continued corporate stock purchases — which, unlike some of those volatility funds, survived the brief market downturn — will make the next one far worse.

On the morning of May 18, 1927 in Bath Township, Michigan, a 55-year old municipal worker named Andrew Kehoe used a timed detonator to set off a bomb he had planted at the local school.

Kehoe was Treasurer of the School Board, so he had unfettered access to the school.

According to friends and neighbors, he was having personal issues with his wife (who he had murdered days prior) and extreme financial difficulties. He was also severely disgruntled about having lost a local election the previous autumn.

Whatever his reasons, Kehoe took out his rage on the 38 schoolchildren he killed that day.

It remains the deadliest attack on a school in US history.

Sadly, it wasn’t the first– there were numerous reports of school shootings throughout the 1800s and before.

And as we all know too well, it wouldn’t be the last.

Last week’s shooting in Florida is another tragic stain in the pages of US history. And it’s completely understandable that emotions are running high now.

People are demanding action. They want their government to “do something.”

The problem, of course, is what we’ve been talking about so far this year in our daily conversations: emotional decisions tend to be bad decisions– and that includes public policy.

We keep hearing the phrase “Common Sense Gun Laws,” for example.

And that certainly sounds reasonable. Who could possibly be against common sense?

[As an aside, I do wonder why “common sense” is only reserved for the gun control debate. Why doesn’t anyone demand common sense airport security? Or a common sense federal budget?]

But it’s never quite so simple.

Many of these “common sense” solutions are emotional reactions.

As an example, the Florida shooter in last week’s tragedy is only 19 years old. So now one of the proposals being tossed around is to have a minimum age limit to be able to purchase a firearm.

I suppose if the shooter happened to have been 70 years old, people would be talking about having a maximum age limit instead.

Yet neither of these “common sense solutions” really solves the problem.

A big part of this is because no one really knows what’s causing the problem to begin with.

We know that there are far too many people committing acts of violence in schools and other public places.

And, sure, a lot of the time they use firearms. But we’re also seeing murderous rampages with cement trucks, U-Hauls, and everyday appliances like pressure cookers.

Any of these can be turned into a weapon of mass destruction.

But the debate only focuses on firearms.

One side presupposes that more regulations and fewer guns will make everyone safer.

The other side of the debate, of course, argues that more guns and fewer regulations will make everyone safer.

The reality is that there’s no clear evidence that either side is correct.

Australia is often held up as an example of a nation that passed strict gun laws (including confiscation) in 1996 following several mass shootings.

And yes, gun violence dropped precipitously. Australia now has one of the lowest murder rates in the world.

But contrast that with Serbia, for example, which is the #2 country in the world in terms of guns per capita (the US is #1).

Serbia has a strong gun culture and fairly liberal laws. Yet its gun violence rate is incredibly low, on par with Australia’s.

There are plenty of examples in the world of places that passed strict gun laws, and violence decreased (Colombia).

Others where violence INCREASED after passing strict gun laws (Venezuela, Chicago).

Other examples of places which have LOW levels of gun violence, yet liberal laws (Serbia). And still others with LOW levels of gun violence and fairly strict laws (Chile).

The point is that you can look at the data 10,000 different ways and never really find a clear correlation. So there HAS to be something else going on.

Is it cultural? Perhaps.

Japan, for example, has extremely strict firearms laws. You can’t even own a sword without special permission.

And Japan, of course, has very limited gun violence. But this is not a violent culture to begin with.

You probably recall back in 2011 after the devastating earthquake and tsunami, Japanese people sat quietly outside of their collapsed homes and waited for authorities. No looting. No pillaging.

Contrast that with the city of Philadelphia earlier this month, where people were out rioting, looting, and setting property on fire… simply because their football team won the Super Bowl.

Perhaps there’s something about the US that has people so tightly wound they dive into violence at the first opportunity.

Maybe it’s all the medication people take. Or the crap in their food. Who knows. But it’s worth exploring the actual SOURCE of the problem rather than treating a symptom.

The larger issue, though, is that this “common sense” mantra is tied exclusively to LAWS.

Guess what? There are already laws, rules, regulations, and procedures on the books. They’re not working.

In the November 2017 mass shooting in Sutherland Springs, Texas, the shooter was able to purchase weapons because the Air Force erroneously failed to record his military court-martial.

And with the Florida shooting, the FBI had the suspect on a silver platter and did nothing.

It’s clear that the laws on the books aren’t being properly implemented. Yet the solution people want is MORE LAWS.

How about better execution? How about applying that all-important “common sense” to the way laws are carried out?

This is conspicuously missing from the debate.

There’s almost no conversation about what’s actually CAUSING the violence.

Instead, people are focused on a manifestation of that problem (guns) and demanding more laws to control that symptom even though the existing laws are being pitifully executed.

This is a pretty horrendous way to solve a problem.

[We discuss this more in today’s podcast, along with plenty of other extremely uncomfortable realities. Listen in here.]

Long Blockchain has been delisted from the Nasdaq and the “just add blockchain”-effect appears to be softening – but the white hot ICO market rages on.

As we reported yesterday, Telegram, which is about to open its token sale to the public, is hoping to raise a total of $1.8 billion total from its ICO after raising nearly half that sum from private-placement “VIP” investors.

And with so much money to be made hocking the dozens of coins that continue to be launched every month, perhaps it’s unsurprising that Facebook is doing a less-than-perfect job of filtering out all the crypto-related advertising (almost all of which is paid for and allocated through an automated system that is prone to lapses, as we learned during one memorable incident last year), which the company denounced last month.

Case in point: Earlier today, Ryan Mac, a tech reporter at Buzzfeed News, pointed out the following (extremely eye-catching) advertisement, which he claimed to have seen on Facebook (both it’s traditional and mobile sites) and Facebook-owned Instagram.

The advertisement is soliciting buyers for an ICO called “Datecoin”.

The advertisement describes Datecoin as “the world’s first dating service that uses neural networks and artificial intelligent [sic] algorithms based on working business model with clear buyback on blockchain…”

…or whatever the fuck that means…

Facebook is doing an amazing job blocking crypto advertis…

Meanwhile, a Youtube video entitled “What is DateCoin?” features five men discussing how DateCoin leverages AI and neural networking…except their discussion is entirely in Russian.

yo i’m totally gonna trust the company in the video that features 5 dudes only speaking in Russian with subtitles about employing neural networks on the blockchain for dating https://t.co/QXWuYKYJDj

What would you rather do? Spend an afternoon deciphering this nonsense diagram? Or lustily gaze upon a model who bears a suspicious resemblance to American actress Angelina Jolie.

look at a diagram of our nonsense tech, OR GET DISTRACTED BY RUSSIAN ANGELINA JOLIE pic.twitter.com/Hch5jGBAUR

Finally, as Mac points out, Facebook’s new transparency-in-advertising features reveal that the ad is targeted at people in the US aged 15-60 who are interested in bitcoin…

The ad was targeted at people who liked bitcoin, and are age 16 to 50 in the United States, which is a pretty wide range. Also saw the ad on Instagram and Facebook mobile web. pic.twitter.com/UN6ooJzzFq

A quick visit to the DateCoin website shows that the company claims to have raised more than 2,200 ETH (roughly $2 million at this afternoon’s prices) already during its private sale…the tokens will be offered to the public beginning in March…

So, with all of this in mind, is DateCoin “the next bitcoin”? Or just another trash ICO?

The Russian government has again denied U.S. allegations that it interfered in the 2016 U.S. election, saying it “does not” meddle in the “internal affairs” of other countries.

The statement was the Kremlin’s first official response following last Friday’s indictment of 13 Russian nationals and three Russian organizations by Special Counsel Robert Mueller.

The indictment focuses on Russian nationals, although according to statements coming out of Washington, the accusations are against the Russian state, Kremlin and the Russian government. But “there are no indications that the Russian state could be involved in this, there arent any and there cant be any,” said Kremlin spokesman Dmitry Peskov in a conference call with reporters.

Dmitry Peskov

“Russia did not meddle, does not have the habit of meddling in the internal affairs of other countries, and is not doing so now“, he said.

A January 2017 report by U.S. intelligence agencies concluded that Russian President Vladimir Putin ordered an influence campaign in 2016 aimed at preventing presidential candidate Hillary Clinton.

“We further assess Putin and the Russian Government developed a clear preference for President-elect Trump. We have high confidence in these judgments,” the report claimed.

Mueller’s report, however, claims that the Russian cyber-offensive began in 2014, two years before U.S. intelligence claims the campaign began. The report also claimed that wealthy Russian businessman Evgeny Prigozhin – known as “Putin’s chef,” was the man behind a “troll farm” that used various social media platforms to meddle in the 2016 election – primarily Facebook and Twitter.

Hours after Mueller’s indictment, Facebook VP of Ads, Rob Goldman, tweeted out a stream of “uncleared” thoughts on the incident, including one which was picked up and retweeted by President Trump which reads “The majority of advertising purchased by Russians on Facebook occurred after the election”

The Fake News Media never fails. Hard to ignore this fact from the Vice President of Facebook Ads, Rob Goldman! https://t.co/XGC7ynZwYJ

Goldman went on to say that he had “seen all of the Russian ads and I can say very definitively that swaying the election was *NOT* the main goal.”

Most of the coverage of Russian meddling involves their attempt to effect the outcome of the 2016 US election. I have seen all of the Russian ads and I can say very definitively that swaying the election was *NOT* the main goal.

The main goal of the Russian propaganda and misinformation effort is to divide America by using our institutions, like free speech and social media, against us. It has stoked fear and hatred amongst Americans. It is working incredibly well. We are quite divided as a nation.

After what must have been an awkward weekend for Rob, Facebook’s VP of Global Public Policy issued a Sunday night statement saying Nothing we found contradicts the Special Counsels indictments. Any suggestion otherwise is wrong.

According to Wired magazine, Goldman issued an internal apology at Facebook that read: I wanted to apologize for having tweeted my own view about Russian interference without having it reviewed by anyone internally. The tweets were my own personal view and not Facebooks. I conveyed my view poorly. The Special Counsel has far more information about what happened [than] I doso seeming to contradict his statements was a serious mistake on my part. (more here)

We’re sure Rob will pre-clear his thoughts in the future.

Just wait until it hits the doctoring, lawyering, and accounting class.

To take an example, COIN (contract intelligence) interprets commercial loan agreements that previously consumed 360,000 hours of lawyers’ time per year. ROSS intelligence is another example, combining a simple, Google-like search system to find up-to-date cases, law and extensive advice in seconds, by quickly sifting through databases of legal history. — marketMogul

Karl and Friedrich wrote about it over 150 years ago:

On disruptive labor destroying technology (AI and the robots are coming):

Constant revolutionizing of production, uninterrupted disturbance of all social conditions, everlasting uncertainty and agitation distinguish the bourgeois epoch from all earlier ones. – Marx and Engels

On free-trade and globalism (protectionism on the rise):

The need of a constantly expanding market for its products chases the bourgeoisie over the whole surface of the globe. It must nestle everywhere, settle everywhere, establish connexions everywhere. – Marx and Engels

Then there are the political leanings of the millennials:

Millennials opt for socialism over capitalism

Given the choice, most Americans would opt for a capitalist country. However, one third would prefer to live in a socialist nation. Millennials are the leading force behind this preference with more than four in ten opting for socialism. – YouGov

Absolutely stunning. More than 50 percent of American millennials prefer to live in a socialist or communist country. Can you blame them?

Debt is a happiness killer. None of us can be truly happy if we’re saddled with debt.

…At the present time, the average American household with student debt owes about $49,000. Graduates in their twenties spend more than $350 per month, on average, on student loan payments and interest. Since the average “entry-level” job was worth about $50,000 a year in 2016 for new graduates, “truly average” college grads in America can expect to see their earnings garnished by between eight and 10% for roughly ten to twelve years after they graduate. — Forbes

Remember Bernie?

Therein lies the spectre that will haunt the investor class over what is sure to be a tumultuous next decade.

Of course, we are not predicting America is on the verge of a communist revolution.

Nordic Capitalism Cometh

We do believe, however, if things continue as they are, and there is not a major political and economic reset, the move to Nordic capitalism, or Nordic socialism — call it what you will — is a done deal in the United States.

Time To Wake Up

Look at the rising political power of the high school students over the past week, now revolting over the country’s revolting gun laws. It feels like a watershed moment to us, and they smell it, a chance to change the culture. They and their older brothers and sisters are the future.

Moreover, what do you think their reaction will be when they have the epiphany the baby boomers have screwed most of them economically?

One should always be cognizant that an increase in the relative price of assets (prices to income), and housing, in particular, is generally a transfer of wealth from the younger generations to the older generations.

The $112 trillion question is what generation will take the hit? Will it be the baby boomers as their asset prices mean revert to income or the younger generations who are forced to pay up for the overvalued assets? Or will a leveling of the playing field take place through the political system?

Our recommendation to the one percenters and the comfortably numb retired baby boomers, who have bequeathed to and saddled the younger generations with massive pension and public sector debt liabilities?

One day after the February 5 volocaust, the first real casualty of the record VIX surge emerged, when the Chicago-based vol-selling fund, LJM Partners, unpleasantly surprised its investors that it was down more than 50% in one day, a loss which has since ballooned to roughly 80%.

Since then, however, while many hedge funds emerged exhibiting material losses, none had what appeared to be a terminal wound.

Until today, because while until now it had managed to sneak through the cracks, in its latest monthly update, the so-called 1.2 Fund reported a number that no hedge fund would ever want to show to its LPs: after nearly 10 years of stable, if modest, growth, the fund which “invests in short and long option strategies on the S&P 500 futures index” reported an apocalyptic -60.11% collapse for the month of February, the direct result of the February 5 VIXplosion.

And this is how you go from being up 91% since inception to -24%. And yes, the annualized volatility cell is intentionally left blank.

The only thing that diffuses the otherwise tragic situation – for 1.2 Fund investors that is – is the sheer comedy that effuses from the Fund’s “strategy” page, highlights ours:

The strategy of The 1.2 Fund is to invest in short and long option strategies on the S&P 500 futures index, employing an active management to market exposure and risk. The fund mainly trades front month expiry and aims to hold a balanced exposure to upside and downside market movements. The fund further employs the use of futures and can buy outright puts and put and call spreads to act as insurance to minimise the potential draw down from extreme market movements to both the downside and upside.

The 1.2 Fund aims to achieve steady monthly returns based on a low volatility model; the choice of the monthly target is flexible and depends on market conditions and the level of volatility as indicated by the Vix. The flexibility of the strategy allows the managers to liquidate the portfolio and/or remain flat also during the expiry whenever the market conditions dictate it as the priority of the managers is always to minimise risk versus returns.

The strategy is dynamic and evolves throughout the expiry as market conditions change. The managers aim to minimise market exposure and seek to generate profit via market movements. The strategy implemented by the investment managers creates returns by exploiting volatility and by the natural time decay process exhibited by options every month. The portfolio is constantly monitored in real time and modelled under differing market conditions in order to determine if positions need to be adjusted.

We aim to achieve return via a disciplined, staged process, combining top down macro analysis of the global economy with technical analysis and strict risk management designed to help protect the fund against any unexpected downside or upside risk.

Of course, it all worked… until it didn’t. Oh, and for those wondering why the fund is called 1.2, here is the answer:

The fund generates returns via option positions on the S&P 500 Futures Index. Exposure to the index is gained through a range of structures utilising both long and short positions seeking to achieve a monthly return of 1.2% net of fees.

To be sure, The 1.2 Fund sure sounds better than The -60% Fund.

In our portfolio management practice, we focus on weekly and monthly data to smooth out daily volatility. Since we are longer-term investors, our focus remains on being invested during rising (bullish) trends and more heavily weighted to fixed income and cash during declining (bearish) trends. Therefore, the only data that really matters to us is where the market closes at the end of each week.

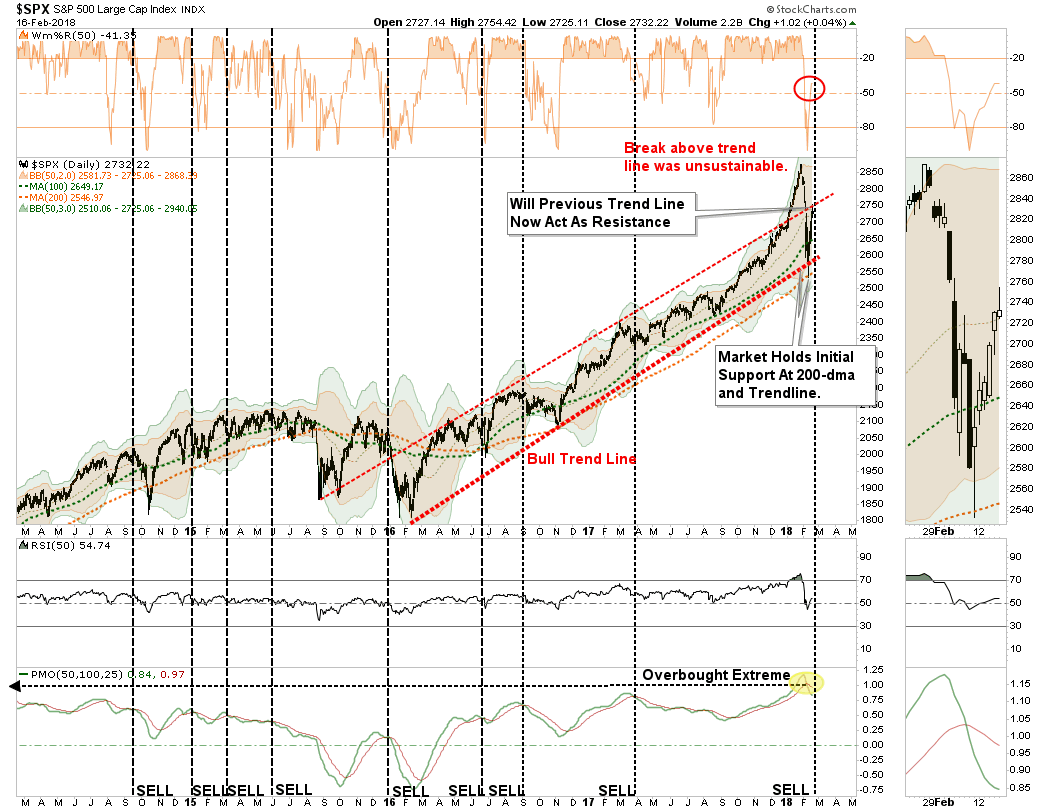

“While the immediate consensus is the ‘bear market of 2018’ is now over, there are several important points about the chart below that should be considered.

Despite the correction, the market did hold support at the 200-dma

The bullish trend line, which goes back to the beginning of 2016, has also not been violated.

However, the upper red “trendline” may provide some overhead resistance temporarily and is worth watching closely.

While the market did get oversold on a short-term basis, which suggested a bounce was likely, the longer-term overbought condition, and subsequent ‘sell signal’ remain intact.

The bottom line is that while there was much ‘angst’ in the markets last week, the market has not violated any important trend lines that would suggest the current sell-off is anything more than just an ordinary ‘garden variety’ correction.”

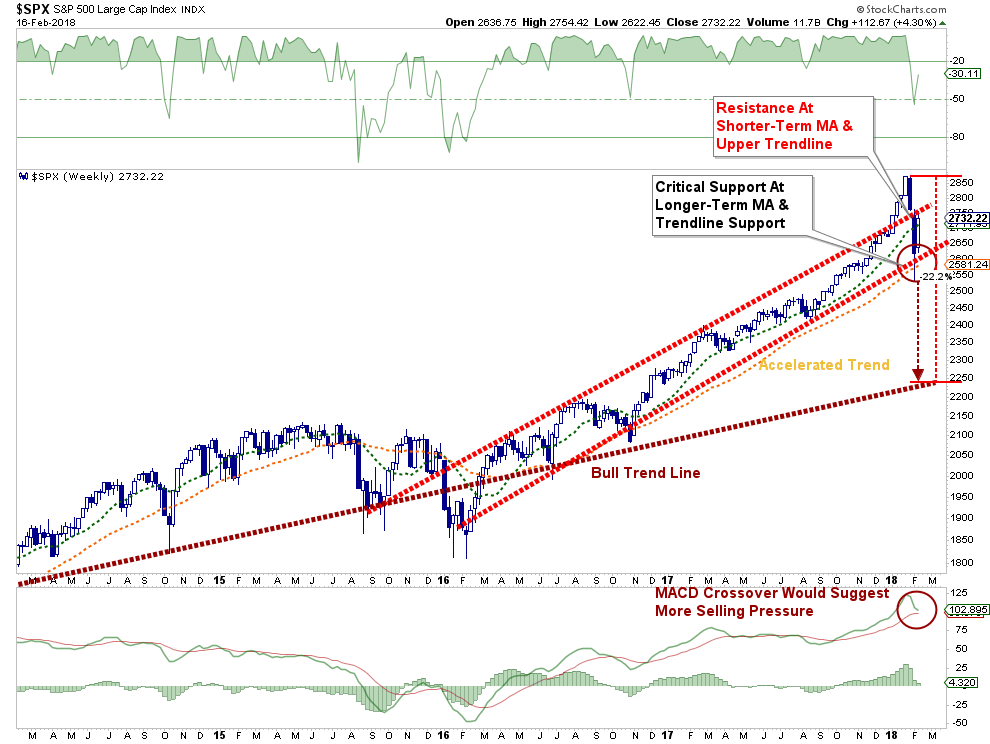

This morning, the market opened back below the 50-dma.

While this is concerning, and keeps our short-hedge in place for now, it is where we finish this trading week that will determine out next positioning changes. The chart below is a weekly view of the S&P 500 index. With much of the volatility stripped away, the important levels for the close of trading on Friday become more evident.

In order for us to fully remove hedges, the market must close above the 50-dma on Friday.

As noted, there is tremendous resistance from the upper trendline of the bullish trend channel that began at the beginning of 2016. We currently expect the market to remain confined to the currently rising bullish trend channel, but there are risks to that view which keeps us cautious.

A failure at resistance which leads to a retracement back to recent lows and the 200-dma is very likely. Here is what we are looking for if that happens.

If the market holds support at the 200-dma and completes a successful retest, we will begin removing hedges and adding to equity exposure.

The retracement to the 200-dma will trigger the MACD sell-signal which is already at historically high levels. That “sell signal” will put additional downward pressure on the market.

As long as the market holds at the rising bullish trend and 200-dma, the bullish backdrop remains intact keeping portfolios weighted towards equity exposure.

However, if the market breaks below those “critical support” levels, as noted above, the risk of a deeper correction rises. Such a break will lead to increased hedging and a reduction of equity risk in our portfolio models.

A break of that critical support will likely lead to a retest of the longer-term bullish trend around 2250 which would be a 22% decline from recent highs and an “official bear market.”

A break below 2250 will likely coincide with the onset of the next recession and is an entirely different portfolio management strategy.

While I have laid out the risks, the bullish trend remains intact. While we are currently hedged, we remain primarily long-biased in our portfolios.

However, don’t completely dismiss the “bearish” case either.

The Bear Still Cometh

Back the newsletter:

“The good news, for those who remain ever bullishly inclined, is on a long-term, monthly basis, the bull market remains intact for now. Unfortunately, despite the rather harrowing correction, little was done to relieve any of the underlying pressures.

Valuations still remain elevated

Bearishness and volatility, despite the recent spike, remain at historically low levels, and;

Investors simply could not jump “back” into the markets fast enough.

These are not signs of a real, lasting bottom, which long-term investors should aggressively buy into.”

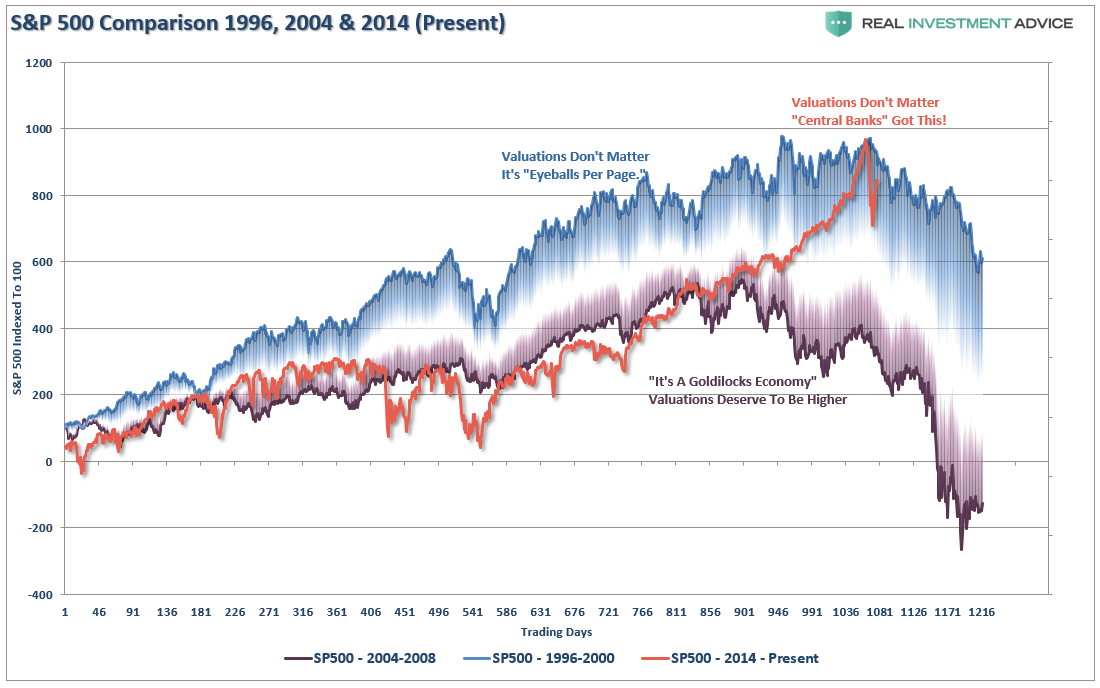

In that missive, I laid out two charts of the 2000 and 2007 market topping processes. In both previous cases, the first 10% correction was a precursor to a bear market. The chart below shows this a little differently by comparing the both previous bull markets to the current bull run. As you can see, the recent correction, which followed an accelerated advance, is behaving in much the same fashion as seen previously.

Does this mean we are the cusp of the next great “bear market?”

Simply looking at prices without context can be misleading. While markets are driven in the short-term by momentum, or better termed “psychology,”it is the long-term underlying fundamentals which ultimately determine a market’s fate.

Not surprisingly, given the surge in monetary liquidity by the Federal Reserve, combined with the underlying sluggishness of economic growth, investors are once again betting on a “this time is different” scenario as market valuations, on many measures, are at, or near, historically high levels.

But, again, just weak economic growth, or high valuations, or rising prices does not necessarily immediately result in a substantial mean-reverting event.

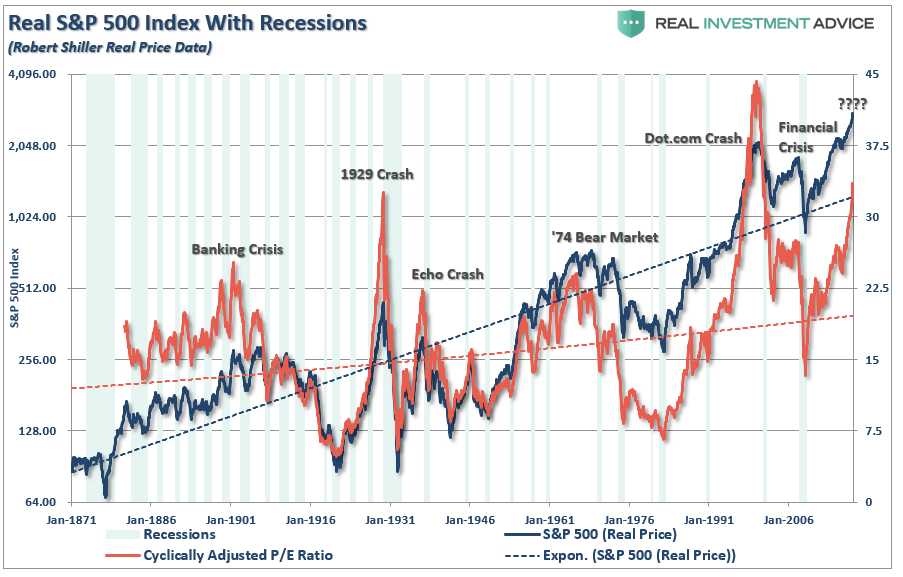

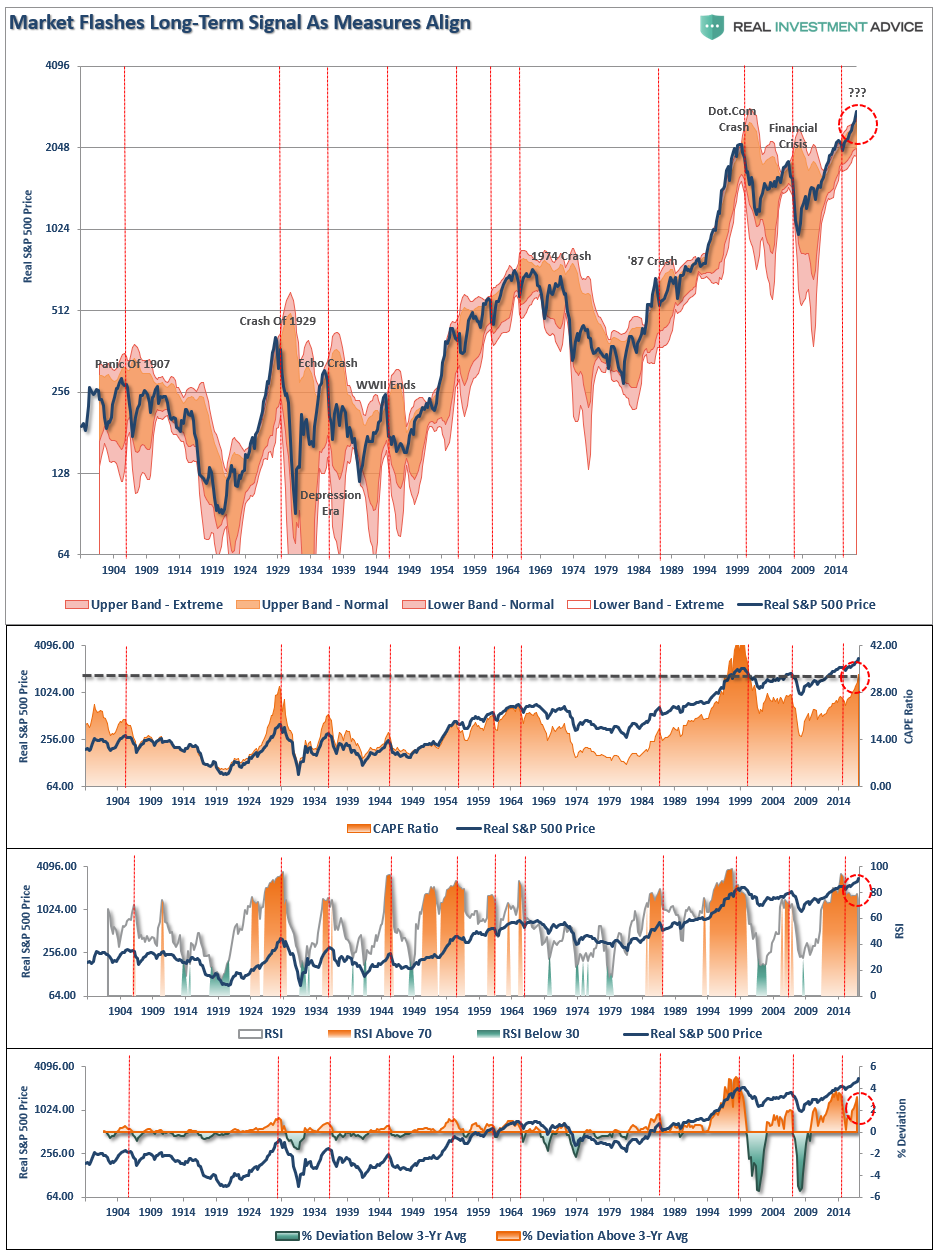

Major mean reverting events are generally tied to the combination of more major extremes in long-term measures of price deviations, economic growth, and valuations. Using quarterly data we can calculate several long-term measures for the S&P 500:

The 12-period (3-year) Relative Strength Index (RSI),

Bollinger Bands (2 and 3 standard deviations of the 3-year average),

CAPE Ratio, and;

The percentage deviation above and below the 3-year moving average.

The vertical RED lines denote points where all measures have aligned

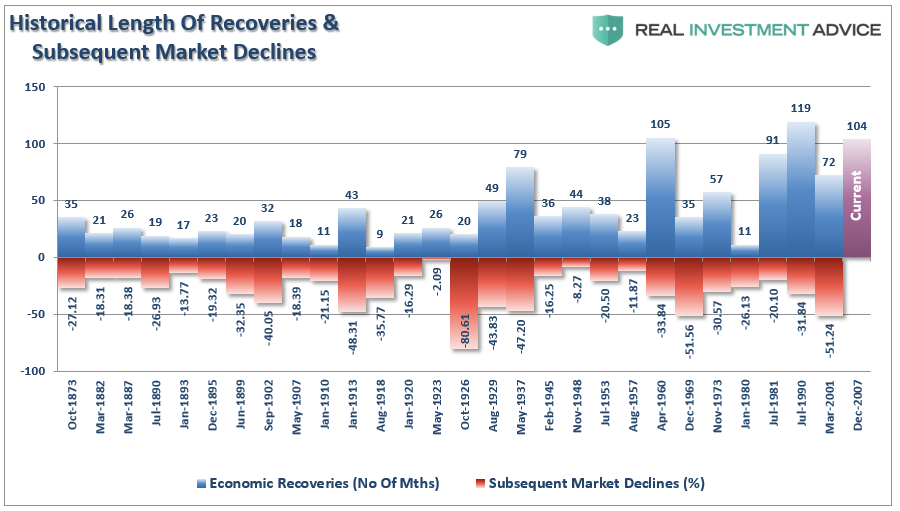

On virtually every measure price and valuation, the markets are grossly extended. However, it is when these measures coincide with the onset of an economic recession that “mean reverting” events tend to occur. The table below looks at the S&P 500 going back to 1873, based on Robert Shiller’s data, to detail economic recessions and bear markets.

In April, the current economic expansion will become the second longest in U.S. history. However, that period of expansion will also be the slowest, based on annualized economic growth rates, as well.

Could the current economic expansion become the longest in U.S. history?

Absolutely.

Over the next several weeks, or even months, the markets can certainly extend the current deviations from long-term means even further. But such is the nature of every bull market peak, and bubble, throughout history as the seeming impervious advance lures the last of the stock market “holdouts” back into the markets.

The correction over the last couple of weeks did little to correct these major extensions OR significantly change investor’s mental state from “greed” to “fear.”

As discussed above, the bullish trend remains clearly intact for now, but all “bull markets” end….always.

Do not be mistaken, the next “bear market” is coming.

Of that, there is absolute certainty.

As the charts clearly show, “prices are bound by the laws of physics.” While prices can certainly seem to defy the law of gravity in the short-term, the subsequent reversion from extremes has repeatedly led to catastrophic losses for investors who disregard the risk.

There are substantial reasons to be pessimistic about the markets longer-term. Economic growth, excessive monetary interventions, earnings, valuations, etc. all suggest that future returns will be substantially lower than those seen over the last eight years. Bullish exuberance has erased the memories of the last two major bear markets and replaced it with “hope” that somehow “this time will be different.”

Maybe it will be.

Probably, it won’t be.

The Reason To Focus On Risk

Our job as investors is to navigate the waters within which we currently sail, not the waters we think we will sail in later. Greater returns are generated from the management of “risks” rather than the attempt to create returns by chasing markets. That philosophy was well defined by Robert Rubin, former Secretary of the Treasury, when he said;

“As I think back over the years, I have been guided by four principles for decision making. First, the only certainty is that there is no certainty. Second, every decision, as a consequence, is a matter of weighing probabilities. Third, despite uncertainty, we must decide and we must act. And lastly, we need to judge decisions not only on the results, but on how they were made.

Most people are in denial about uncertainty. They assume they’re lucky, and that the unpredictable can be reliably forecast. This keeps business brisk for palm readers, psychics, and stockbrokers, but it’s a terrible way to deal with uncertainty. If there are no absolutes, then all decisions become matters of judging the probability of different outcomes, and the costs and benefits of each. Then, on that basis, you can make a good decision.”

It should be obvious that an honest assessment of uncertainty leads to better decisions, but the benefits of Rubin’s approach, and mine, goes beyond that. For starters, although it may seem contradictory, embracing uncertainty reduces risk while denial increases it. Another benefit of acknowledged uncertainty is it keeps you honest.

“A healthy respect for uncertainty and focus on probability drives you never to be satisfied with your conclusions. It keeps you moving forward to seek out more information, to question conventional thinking and to continually refine your judgments and understanding that difference between certainty and likelihood can make all the difference.”

We must be able to recognize, and be responsive to, changes in underlying market dynamics if they change for the worse and be aware of the risks that are inherent in portfolio allocation models. The reality is that we can’t control outcomes. The most we can do is influence the probability of certain outcomes which is why the day to day management of risks and investing based on probabilities, rather than possibilities, is important not only to capital preservation but to investment success over time.

In a day of record debt issuance, moments ago the US Treasury sold not only $55bn in 4 week bills at a yield of 1.38% (higher than the 6 month average of 1.348%) at a bid to cover that tumbled from the 6MMA of 3.12 to just 2.48, the lowest since July 2008, suggesting that demand for 1 month US paper was not exactly stellar…

… but also $28 billion in 2Year notes, the day’s first coupon issuance.

Unlike the 4-Week auction, which saw surprisingly poor interest judging by the plunge in the BTC,the 2Y auction was average at worst, pricing at 2.255%, stopping through the When Issued 2.256% by 0.1 basis point. This was the highest 2Y yield since August 2008, one month before the Lehman bankruptcy. As a reminder, the auction size on today’s auction was increased from $26bn – where it was since January 2015 – to $28bn.

Yet while the headlines were good, the internals were not: just like the 4 Week, the Bid to Cover tumbled from 3.222 to 2.722. This was modestly below the average 6 month BTC of 2.83.

Another indication of poor reception is that Indirects took down just 36.3% of the auction, well below the 58.3% last month, and in line with the 46.4% 6 auction average. Directs were awarded 13.4%, fractionally below January’s 15.9%, and the 6 month average of 15.5%. This left Dealers with 40.3%, slighly above the 38.1% 6 auction average.

Overall, two mediocre auction which however was still impressive in light of the record amount of debt sold today, and likely an indication that yields at current levels are neither too high, nor too low to absorb at least the near-term mountain in upcoming issuance.