Authored by Peter Earle via The American Institute for Economic Research,

The past year has been one full of superlatives: from the most votes ever cast in a presidential election to the worst unemployment claims the United States has ever seen. There have been unbelievable highs, such as the record-breaking increase in new businesses launching, and there have been crushing lows, like the largest surge in poverty in US history. Perhaps no field highlights those highs and lows better than the financial sector.

The volatile financial landscape has become an indispensable component of ongoing pandemic coverage. Much like 2020 as a whole, events in global financial markets over the past year have ranged from shocking to devastating to mind-boggling. The sheer concentration of so many unlikely events taking place in the span of a year can, at least partially, be explained by economic logic, but that answer alone would paint an incomplete picture. Widespread fear and panic stemming from the ongoing Covid-19 pandemic and government-imposed lockdowns and business closures have played massive roles in rattling the financial sector.

In looking back at the extremes of 2020––in rough chronological order, as some starting dates are estimated and many of the phenomena described persisted for days or weeks after emerging––the following events in global financial markets helped make this year one for the books.

-

US Treasury Yield Curve Inversions – February 14, 2020

The significance of an inverted Treasury curve can be debated, but in any event, short-term rates on government bonds exceeding long-term rates are an uncommon event and are typically indicative of increasing pessimism about economic prospects in the near- and medium-term.

The US Treasury yield curve inverted almost exactly one year prior to the Covid-19 panic and spent a good portion of fall 2019 inverted. But in February 2020, both one- and three-month Treasury bills inverted. Investors concerned about the severity of the virus and, more importantly, policy responses to the growing pandemic fled risk instruments (stocks, bonds, etc.) for the safety of short-term Treasuries, in which the principal is guaranteed by the United States government. When growing doubt (or, indeed, utter panic) leads to a rush into short-term government-issued securities, the prices of those instruments are pushed up and the yield (interest) down, creating the inversion.

Although inversion of yield curves sometimes concerns the outlook for the issuing nation, the broad-based inversion that began on roughly February 14th, 2020 had less to do with the US than global economic prospects as a whole. On that day, the one- and two-month Treasury bill yields rose to 1.60% with the ten-year note at 1.59%. This should be viewed as the first sign of the Covid-19 financial panic to come.

-

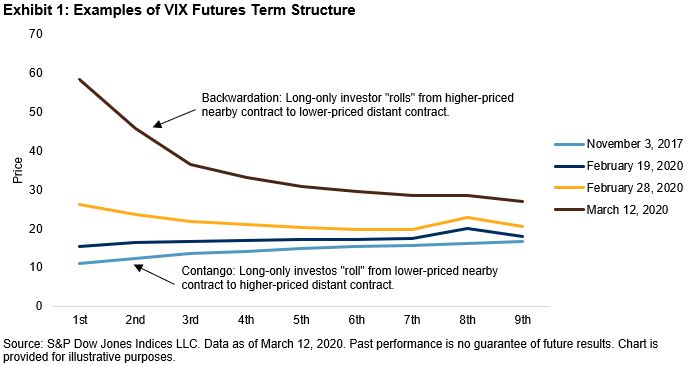

VIX Futures in Backwardation – February 27, 2020

The VIX is the Chicago Board Options Exchange’s Volatility Index. Using exchange-traded option prices, it tracks the level of “fear” (anticipation of downside) in the market regarding equity prices. It’s a somewhat esoteric financial market instrument upon which futures––market-traded contracts to buy or sell financial instruments at specified prices in the future––are traded, and the prices at which they trade imply expectations of future volatility.

Typically, when a number of futures contracts specifying a particular financial instrument over a series of dates are trading, they trade in a condition called “contango.” In contango, progressively longer-dated futures trade at progressively higher prices. The term structure slopes upward. That makes sense for a few reasons: A longer time to expiry means more risk, more uncertainty, and higher time value of money (greater opportunity cost).

On exceedingly rare occasions, the term structure slopes downward in price over time: Thus the price today, usually a bit lower than the price a month from now, which is a bit lower than the price two months from now, is inverted. The opposite of contango is backwardation, with the present priced higher than contract dates further out in time.

This is what happened in the VIX futures contracts:

VIX started the year at 13.78 and its term structure was in the classic contango … When the coronavirus outbreak hit China, the VIX spot [current market] was slightly elevated to 17.97 on Fed 3 out of concerns of supply chain disruptions and a global economic slowdown, but the VIX term structure was nearly flat … Then the sell-off began on February 20. From February 21 to 28 the VIX term structure quickly evolved to contango to backwardation. But the increases were relatively small and mostly in the front end showing that investors believe that the episode would turn out to be no more than a temporary hiccup. Entering March, major [equity] indices had their fastest downfalls in history. VIX shot up to 81 on March 16. Its term structure exhibited severe backwardation and all futures prices moved up across the time horizon. The message it was delivering: the stock market could be all over the place in the near term, and even 6 months out (180 days), the range of movement for the S&P 500 would be as wide as +/- 32% annualized.

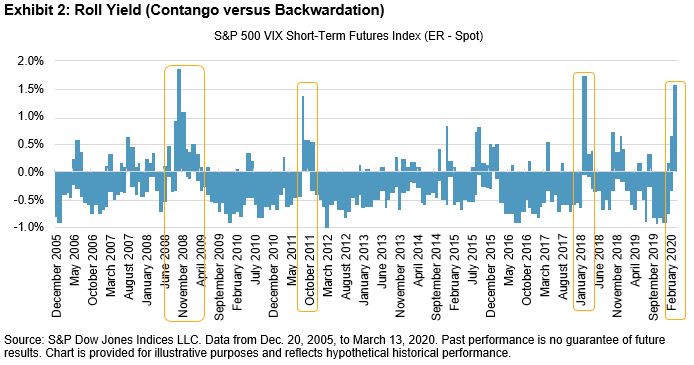

This, though, does not give an impression of exactly how unlikely such an event is. One way of defining a significant episode of backwardation is to calculate the roll yield, the positive or negative return generated by shifting from a short-term to a longer-term futures contract. It is rarely positive, and even then it is scarcely greater than 1%. Since 2005, there have only been four such occurrences: During the 2008 financial crisis when Lehman and a number of other firms were collapsing; in 2011 when the US government lost its AAA credit rating; in February of 2018; and in March-April 2020.

-

Seizing up of the US Treasury Market – March 11, 2020

An extremely complex series of interactions occurred throughout February and into early March 2020 and led to never-before-seen duress in the cash markets for US Treasuries. In short, to ensure their access to financing––often referred to as seeking more “balance sheet”––many firms took large positions in US Treasury bonds, hedging them with Treasury futures contracts. Some did this purposely, to capture small disparities in what is called a basis trade. Others did so only to put money to work in a low-risk way, such that they might be able to borrow funds more easily should opportunities arise.

Treasury bonds, of course, are limited in supply, and newly-issued Treasuries (“on the run”) are far more liquid than similar bonds which were not recently issued (“off the run”). As certain firms began to enter into basis trades using less liquid Treasuries for the cash leg, the futures hedge became less effective, resulting in paper (unrealized) losses. As certain market participants sought to exit that trade, they began buying back the bond futures and selling the bonds aggressively, causing a plummet in Treasury prices––in some cases, on already illiquid issues.

Treasury dealers, firms that stand ready to buy and sell a wide variety of US government bonds and agency issues, began to “get full:” they typically attempt to maintain a balanced book, adjusting prices to regulate the flow, but the torrent of bond sales (largely concentrated in certain popular maturities, such as the 10-year Treasury bond) led them to begin to lower their bids or, in some cases, exit the market. Bond sales were made at incrementally lower prices with paper losses mounting for firms unwilling or unable to liquidate their positions.

Banks and investors have said that trading conditions in Treasuries, the world’s biggest and deepest debt market, have deteriorated markedly this week as the coronavirus outbreak has ignited severe ructions. The market became “overwhelmed by liquidity concerns” during a chaotic day on Wednesday, Bank of America analysts said … A bond portfolio manager at a large asset manager said the situation had not improved on Thursday as volatility continued to grip the market. “We’re not trading,” he said.

It is rare, indeed, to see as broad and deep a market as Treasury securities, even across a small handful of maturities, driven to panic selling. And this is approximately when the Federal Reserve initiated its Treasury purchase program, which sought to assure sellers that they would get a price for their bonds and encouraged them not to sell.

A standard analogy features a burning theater, which symbolizes bond prices collapsing, with moviegoers––owners of bonds––all attempting to flee through a single door. As they attempt to squeeze through, the fire worsens and injuries/deaths mount. In terms of the Fed’s Treasury liquidity facility, the analogy would see the Fed break six or eight more “doors” in the theater, not only giving moviegoers ready exit, but possibly reason not to flee.

-

The First Stock Market Crash in 33 Years – March 16, 2020

There have been many drops in the market over the last few decades, but there hasn’t been a crash since 1987, despite frequent misuse of the term and breathless reporting of notable, but statistically routine, declines. The most widely-accepted definition of a stock market crash is a drop of 10% or more in one day, and on March 16, 2020, equity markets crashed: The Dow Jones Industrial Average declined just short of 13% (2,997 points) with both the S&P 500 and NASDAQ Composite down 12%. That capped off the longest and most severe equity market losing streak since October 1929, with a four-day market decline of over 26% (approximately 6,400 Dow points).

The drop on that Monday came amid increasingly pessimistic predictions for the economic impact of the policy choices that government officials were considering to address the pandemic. But on that day, selling accelerated and triggered a trading halt when, during a press conference, President Donald Trump commented that the worsening pandemic could linger until August. And with that, the outlook for corporate earnings nosedived, followed by equity valuations and prices. (I wrote about the Crash of 2020 at that time.)

-

Corporate Bond ETF Prices Below NAV – March 17, 2020

Exchange traded funds (ETFs) are basically tradeable portfolios of financial assets. They can be diversified to provide investors with exposure to specific instruments, market sectors, capitalizations, and so on. In addition to the market price, ETFs have a net asset value (NAV) associated with them, which is essentially the pro rata portion of the underlying instruments of each share. The difference between the ETF price and the NAV should be very close in most cases, but they sometimes trade at a spread owing to stale prices (certain securities do not trade frequently), time differences (for example, a Japanese stock in a US fund is not actively trading at 11am EST), and so on.

During March 2020, a handful of corporate bond ETFs came to trade with massive spreads between their prices (which had also fallen, of course) and their NAVs. In the case of LQD and HYD––two ETFs which trade investment grade and high yield (“junk”) bonds, respectively––the spreads implied that many, if not a majority, of bonds in each were highly distressed and likely to experience defaults.

Several factors were at work: First, to be sure, investor redemptions in ETFs and selling in the underlying corporate bonds sent prices plummeting and led to increasing illiquidity as fixed income dealers became more reticent to step forward and buy. With illiquidity comes wider spreads and less firm prices. And with political talk of lockdowns in the air, the prospect of certain bonds becoming impaired––the issuing companies having trouble paying required interest to bondholders and other creditors––heightened as well.

And it is worth mentioning that unlike in equity markets, bond investors are generally less likely to “buy the dip” when prices fall. One estimate holds that only 20% of corporate bonds trade daily under normal conditions, and thus, after being sharply discounted owing to the economic uncertainties surrounding the policy reaction to the pandemic, the market froze up. That chill represents tens of thousands of traders, dealers, and other market participants waiting for more information in order to price near-term risk. As noted on Bloomberg,

It might seem like perfectly good bonds are trading at fire-sale prices. In time, that will likely turn out to be the correct assessment. But in the middle of a maelstrom of selling, the likes of which has never been seen before, no security is safe, not when there’s virtually no buyers to speak of. And if more retail investors decide they want out of the storm, as they have in the past, the vicious cycle has only begun.

Adding to this historic dislocation in pricing, though, is that in early April 2020 the Federal Reserve began purchasing high-yield bonds––an even more unprecedented development than the dislocation between ETF and NAV prices which in part triggered the intervention.

Most of those ETFs and the bonds stuffed into them recovered over subsequent months, but it was by all accounts the worst drop in corporate bonds in modern history: far worse than anything seen during 2008, after 9/11, and so on.

Tied to both the seizing up of US Treasury markets and the collapse of corporate bond prices: As those markets became less liquid, with spreads widening and bids disappearing, other credit markets––commercial paper and revolving credit facilities, for instance––began seeing a withdrawal of market participants as well. Yields on municipal bonds––instruments critical to county and state financing––skyrocketed. As in many previous financial crises, a wide range of asset, security, and derivative markets devolved into a breaknight flight toward cash.

-

Breakdown in the Historical Gold-Silver Ratio – March 18, 2020

There is a case to be made that the price-ratio of gold-to-silver is the oldest financial time series on record. And although the ratio of silver to gold in the Earth’s crust is approximately 18:1, silver and gold in modern financial markets have traditionally traded at a ratio of around 60:1. That ratio fluctuates owing to both supply and demand (ornamental and industrial) and sentiment, but over time tends to revert to the 60:1 level.

In the first week of April 2020, the ratio hit an all-time high (by some accounts, a 5,000 year high).

We have data for this series going back a long, long time – during Pharaoh Menes’ time (circa 3100 BCE) for example the ratio was 2.5x, whereas in King Hammurabi’s day (circa 1750 BCE) it was 6x. The legendary Greek king Croesus (circa 560 BCE), who supposedly invented gold and silver coins, was more of a gold bug – he used a 13.33x ratio. Emperor Constantine I (280-337 CE) was less so at 10.5x. We have more frequent data starting from 1687 that confirms it: yesterday the gold/silver ratio was the highest ever. The ratio peaked at 123.78x. During Asian trading today it dropped back to around 116-117, but once London came in it went shooting back up to the 120-121 range. For reference, on Friday it averaged 101.74, and during all of 2019 it averaged 86.04. This is an amazingly swift change in this price. (The previous high before this month was in 1940, when it averaged 99.76 for the year.)

The reasons for the massive disconnection include sudden scarcity of physical silver (being more affordable for hedgers than gold) and the notorious difficulty of trading/hedging silver in futures markets. The silver futures contract is legendarily volatile––it is nicknamed “white lightning”––owing to low liquidity, wide spreads, and an uncommonly large 5,000-ounce contract size.

-

Historical Gold Spot-Future Spreads – March 24, 2020

Traditionally, spot prices (the price of a commodity today or delivered immediately) and futures prices (the price of a commodity delivered at a future date) trade at fairly close prices. For example, at present an ounce of gold is trading at $1,877 in spot markets, and the nearest-to-expire gold futures contract is trading at $1,882––a $5 “spread.” But between late March and mid-April 2020, the spread between gold’s spot and gold futures prices disengaged to an extent never before seen.

In late March, gold futures traded over $80 above the spot price. The incredible gap was reflective of the sudden rush to acquire gold as a hedge against economic uncertainty and, specific to the nature of the pandemic and travel/cargo restrictions, difficulty in procuring and transporting physical gold between major gold-trading hubs (New York, London, Switzerland, and Hong Kong) and other locations.

A factor contributing to the difficulties in the US Treasury markets was in effect here as well: Traders and brokers were working from home, without the multi-trunk phones (“turrets”) and technology they are accustomed to. As reported:

Ole Hansen, head of commodity trading at Saxo Bank, pointed out that a lockdown is occurring in two biggest gold hubs in the world – New York and London – so many traders are working from home. This has caused a breakdown in the marketplace, he said … “We don’t have enough hands to handle all the demand,” he said. “There is plenty of gold in the market, but it’s not in the right places. Nobody can deliver the gold because we are forced to stay at home.”

-

Negative US Treasury Bill Rates – March 25, 2020

Not only did the US Treasury yield curve see an inversion, but the aforementioned rush into short-term, nominally risk-free government bills caused their yields to turn negative. In other words––and this is a bit oversimplified, as short-term instruments are issued in zero-coupon form (meaning interest is not paid on them, but rather the bills are issued at a discount and mature at their full face value)––investors were willing to “pay” the government $1.00, knowing they would receive only $0.99 or so back one to three months later, but a guaranteed $0.99 from the collector of taxes and owner of the printing presses.

Yields on both the 1-month and 3-month Treasury bills dipped below zero Wednesday, a week and a half after the Federal Reserve cuts its benchmark rate to near zero and as investors have flocked to the safety of fixed income amid general market turmoil … both bills briefly flashed red and yields fell to minus-0.002% each. The readings Wednesday were well below those. The one-month traded at minus-0.053% while the three-month was at minus-0.033% around 2:35 p.m. ET.

This, too, is a sign of complete market capitulation rarely seen outside of the most severe market conditions, such as in the days leading up to and just after the bankruptcy of Lehman Brothers in 2008.

-

WTI May Futures Settle at Negative Prices – April 20, 2020

One of the oddest moments in financial markets occurred on April 20, 2020, when the price of the West Texas Intermediate May crude oil contract fell well below zero to settle at -$37.63 per barrel. The combination of a sudden, tremendous drop in demand for oil (owing to lockdowns, a historic drop in tourism, event cancellations, and the like) occurred as production disagreements between Russia and Saudi Arabia resulted in a number of OPEC member nations flooding the world with oil.

With an unprecedented supply of oil being unleashed in a global economy with precipitously falling demand for oil (visible in other petroleum-based products as well), storage facilities filled quickly. So much oil was being held that––and this is what negative futures prices imply––traders were paying counterparties to take their oil, a phenomenon now known as “peak storage.”

I spoke at length about this particular phenomenon on Gary Baumgarten’s show on April 29, 2020.

-

Bitcoin’s Historic Moonshot – November 30, 2020 (ongoing)

From starting the year fluctuating between $7,000 and $10,000 to hitting a low of just over $4,900 in March of 2020––strongly indicating that at least some market participants dumped their holdings during the most chaotic period of the panic––Bitcoin has since vaulted to all-time highs. As of this writing it stands at $29,488, a rise of over 250% this year. Whether that has to do with the halvening (which I wrote about in January), growing recognition of its resilience, or some other factor is difficult to say.

The Upshot

Uncertainty about the policy response to Covid-19 initiated the cascade of financial market extremes, but expansionary monetary policy was a profound accelerant as lockdowns took hold. The US government spent roughly $7 trillion in 2020, with the Fed having committed between $3 and $4 trillion to programs intended to keep markets functioning.

It also lowered the Fed Funds rate to zero, gave forward guidance indicating that it would keep rates low until inflation materially exceeded the 2% level, opened international swap lines, reopened some 2008 Financial Crisis programs, and embarked upon a Main Street Lending Program reminiscent of Great Depression-era policies. On the fiscal side, the US budget deficit was approximately $865 billion in June 2020 alone––an amount exceeding the entire debt incurred by the United States government between 1776 and 1980.

Beyond representing curiosities and the awesome distorting power of central bank largesse, each of the aforementioned extremes demonstrates that however well-designed a particular market is, and however carefully a regulatory oversight structure may be crafted, the sometimes-unpredictable nature of human action can and does lead to unintended consequences. And when, on those rare occasions, confusion and fear reach an apex, unforeseen events do not only occur, they cluster together.

Many options traders have the words abyssus abyssum invocat emblazoned on a notebook, a monitor, or some other nearby fixture––I certainly did––reminding that every so often “hell calls hell.” One misstep or fluke event makes another more likely, at times resulting in a full-on cascade before calm prevails.

There is a tendency to view financial markets as either superfluous casinos of no real economic significance or, conversely, as invaluable social instruments for distilling disparate views. This year’s clusters of remarkably unusual events feed the first view, but the second is far closer to the truth than the first.

A year like 2020 educates another generation of traders and corporate managers, contributes to more robust market and exchange designs, and draws in innovators and risk-takers seeking to capitalize on the next crisis opportunity. Whatever 2021 has in store, it is unlikely to replicate financial market conditions witnessed throughout 2020.

{kind=link}

{kind=link}