China Slaps Sanctions, Travel Restrictions On US Officials As Feud Over Hong Kong Intensifies Tyler Durden

Thu, 12/10/2020 – 07:37

Considering all that has happened in the year since the first coronavirus cases were discovered, one might expect China and the CPC to be somewhat more contrite. But although President Xi has promised to dole out billions of doses of China-developed vaccines throughout the developed world, Beijing has rattled its rivals in the West by putting its foot down and pushing back against American efforts to curb China’s growing geopolitical rivals.

On Thursday, China warned that it would retaliate against the US by slapping new sanctions on American officials and place travel restrictions on diplomats, following the announcement of sanctions on 14 members of China’s NPC, the massive legislative body that functions as China’s “Congress” (it’s merely a rubber-stamp legislature, to be sure).

SCMP claimed these tit-for-tat restrictions are the result of President Trump trying to preserve his “tough on China”, and box VP Joe Biden into preserving the approach, something Biden has promised to do, at least, at first. Biden has even reportedly brought in Mayor Pete Buttigieg to handle the whole situation and maintain the tough stance.

China is aiming to sanction powerful Americans including lawmakers, NGO personnel and their families, Foreign Ministry spokeswoman Hua Chunying told a regular news briefing Thursday in Beijing.

China added that the sanctions would only “strengthen its resolve” to crush Hong Kong’ democratic freedoms – Beijing’s primary goal in all of this.

While Trump’s rhetoric and actions certainly seem aggressive, Washington has been careful not to cross an important red line: Beijing has warned that it would never tolerate sanctions on members of China’s seven-member standing committee, otherwise known as the Politburo, which is the group of the 7 most powerful government officials in all of China.

via ZeroHedge News https://ift.tt/2K8JWg8 Tyler Durden

President-elect Joe Biden’s campaign is the first in history to raise $1 billion from donors, adding yet another broken record to the 2020 cycle that set a new benchmark for political fundraising.

Biden wielded a massive financial advantage over President Donald Trump during the final months of the 2020 campaign. Biden heavily outspent Trump on the airwaves in key swing states he ultimately won by narrow margins. He also had superior backing from big-money super PACs and “dark money” groups.

Chandan Khanna/AFP via Getty Images

The Biden campaign netted nearly $107 million from Oct. 15 to Nov. 23, according to Federal Election Commission filings released Thursday, pushing its total past the billion-dollar mark.

Overall, the 2020 election cycle is by far the most expensive ever. OpenSecrets estimated that the election will cost roughly $14 billion — twice as expensive as the 2016 contest — and the total could rise further with big spending in the Georgia Senate runoffs.

Biden secured 306 electoral votes with narrow victories in Georgia, Arizona, Wisconsin and Pennsylvania. But Trump has not conceded. He continues to push unfounded claims of voter fraud and a “rigged election” while keeping up his campaign’s fundraising efforts long after the election was called for Biden.

Trump’s campaign netted $178 million from Oct. 15 to Nov. 23, according to FEC filings. That’s significantly more than Trump raised during even the months leading up to Election Day. The campaign has sent out hundreds of misleading fundraising emails to its large list of supporters accusing Democrats of trying to “steal” the election and asking for money to fund its legal challenges. According to post-election filings, the campaign spent about $9 million on recount efforts, with the vast majority of its money on advertising and fundraising fees.

Trump’s campaign reported bringing in $774 million in net contributions, the second-most raised by a presidential candidate. That’s in addition to hundreds of millions Trump raised for the Republican National Committee and leftover cash Trump’s joint fundraising committees did not transfer to the main campaign.

The Biden campaign’s $1 billion fundraising haul is unprecedented. Former New York City MayorMichael Bloomberg’s unsuccessful presidential campaign spent $1.1 billion, but that money came from Bloomberg himself, not from individual donors. Former President Barack Obama raised $745 million for his 2008 campaign and slightly less for his 2012 run.

Both Biden and Trump stressed the 2020 contest was the “most important election ever” and they made that urgency clear in their flurries of online fundraising appeals. The candidates spent record sums on online ads mostly aimed at converting supporters’ rage into campaign donations. Campaigns invested heavily in online fundraising with the pandemic shutting down in-person events. Democratic fundraising firm ActBlue facilitated $4.8 billion in online donations in the 2020 cycle, and Republicans’ rival firm WinRed helped Republicans make gains with small donors.

Through mid-November, Trump raised an estimated 49 percent of his money from small donors giving $200 or less, an astoundingly high figure for a presidential candidate. Biden brought in an estimated 38 percent of his campaign cash from bite-sized donors. The president-elect received far more support from donors in the financial sector, as well as lawyers and educators.

Trump broke boundaries when he began raising money for his reelection campaign shortly after his inauguration. Now Trump is raising money for a potential 2024 bid while still in office. Trump’s new leadership PAC, Save America, raised roughly $569,000 in a matter of weeks. The PAC could be used to lay the groundwork for a Trump 2024 run by spending on consulting and polling. Or the PAC could pay for Trump’s travels or funnel more money to Trump-owned properties under fewer restrictions than a campaign committee.

Researcher Doug Weber contributed to this report.

via ZeroHedge News https://ift.tt/2VWuzdd Tyler Durden

ECB Preview: Here Comes Another €500 Billion In QE Tyler Durden

Thu, 12/10/2020 – 05:45

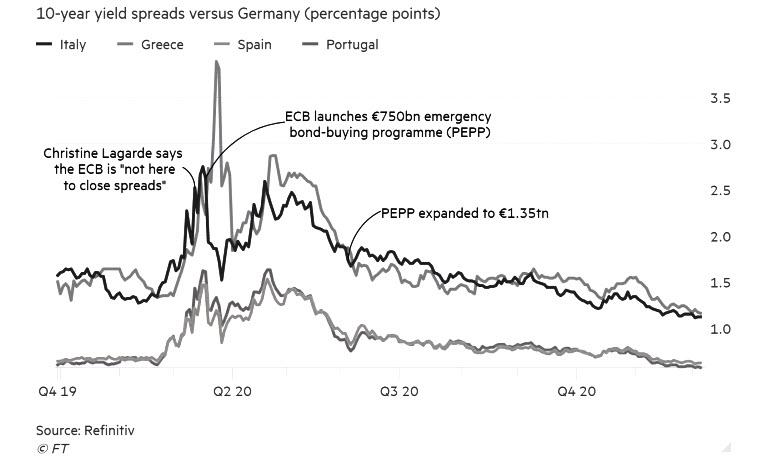

Last March, the ECB’s then-brand new boss Christine Lagarde sparked a mini crisis when quipped that it was not the job of the European Central Bank to narrow the gap in borrowing costs between the eurozone’s stronger and weaker members. The resulting bond selloff and market mess prompted the ECB’s chief economist Philip Lane to secretly call some of the largest asset managers to calm them that Lagarde had no idea what she was talking about and to stop selling.

Nine months on, investors have gone all-in on bets that the ECB boss has changed her mind, and is here “to close spreads” after all.

Ahead of the central bank’s next policy meeting, the FT notes that spreads in the eurozone’s periphery have been squeezed by relentless demand for riskier bonds. The buying helped push Portugal’s 10-year yield below zero for the first time. Spain is not far behind, and Italy — the last big eurozone market to offer a significant positive yield over a decade — has seen its spread closing in on its lowest since the region’s debt crisis a decade ago.

With the ECB expected to expand its €1.35tn emergency asset purchase program by (at least) another €500bn, investors are increasingly relaxed about holding peripheral bonds despite the explosion in debt levels driven by the pandemic.

Are they right? Courtesy of NewSquawk, here is a breakdown of what to expect:

ECB policy announcement due Thursday 10th December; rate decision at 12:45GMT/07:45EST, press conference 13:30GMT/08:30EST

PEPP and TLTRO set to be tweaked, rates, PSPP and tiering expected to be left untouched

The upcoming release will also be accompanied by the latest round of staff economic projections

OVERVIEW: After telegraphing in October that further stimulus would be unveiled at the upcoming meeting, the consensus looks for a €500bln addition to the PEPP programme and 6-month extension until December 2021 (a longer extension has been speculated by some), while a majority of economists expect no change to its PSPP. Elsewhere, market participants expect policymakers to tweak the parameters of the Bank’s TLTROs. Rates are set to be left unchanged, whilst an adjustment to the tiering multiplier is not expected this time around. Accompanying economic projections are set to see a downgrade to the near-term inflation outlook, but greater focus could be placed on the initial 2023 forecast. For growth, any near-term optimism on vaccines could be tempered by how the ECB addresses the yet to-be passed recovery fund and disappointing Q4 2020 outturn.

PRIOR MEETING: As expected, policymakers opted to stand pat on policy settings, with rates and bond-buying operations held at current levels. The main takeaway from the initial announcement was the introduction of a new paragraph in the statement noting that risks to the economic outlook were “clearly tilted to the downside” and the new round of Eurosystem staff macroeconomic projections in December “will allow a thorough reassessment of the economic outlook and the balance of risks.” Additionally, “on the basis of this updated assessment, the Governing Council will recalibrate its instruments, as appropriate, to respond to the unfolding situation.” In terms of the policy measures set to be unveiled in the final meeting of 2020, President Lagarde did not delve into specifics. Despite policymakers acknowledging the bleak outlook for the region, the ECB chief stated that no discussion was held on unveiling measures at the October meeting with policymakers wanting to gather further evidence on the economic impact of the second wave of COVID across the Eurozone.

RECENT DATA: Q3 Eurozone GDP was confirmed as showing a 12.5% Q/Q expansion from Q2 with the Y/Y figure printing a 4.3% contraction. On the inflation front, the Y/Y flash CPI print for November remained at -0.3%, with core CPI holding steady at 0.4%. Survey data has highlighted the differing fortunes of the services and manufacturing sectors with the EZ-wide Markit PMI report showing the former in contractionary territory and the latter in expansionary, the broader composite reading fell to 45.1 in November from 50.0 in October. Markit noted, that while the EZ economy has slipped back into a downturn, the decline is of a far smaller magnitude than seen in the spring. The unemployment rate in the Eurozone for October came in at 8.3%, with the figure obscured by regional employment support schemes.

RECENT COMMUNICATIONS: Beyond the clear signposting at the October meeting by Christine Lagarde that stimulus is set to be unveiled in December, the ECB President has reaffirmed that all options are on the table. That said, Lagarde (Nov 11th) talked up the efficacy of PEPP and TLTROs throughout the pandemic, suggesting that they will “likely remain the main tools for adjustment”. Additionally, the central banker emphasised that “what matters is not only the level of financing conditions but the duration of policy support, too”, suggesting that any expansion to the PEPP could also be met with an extension from the current endpoint of end-June 2021. Chief Economist Lane – who many view as the thought-leader at the ECB –has echoed Lagarde’s views on the efficacy of PEPP and TLTROs, whilst also noting that it is essential that the macroeconomic recovery is not derailed by a premature steepening of the yield curve. Germany’s Schnabel, one of the more vocal members of the Governing Council, recently remarked that the ECB is not obliged to do what the market expects it to, before going on to state that a 12-month extension to PEPP is one option being considered, and that the ECB could also look at a longer duration or more favorable rate for TLTROs. Elsewhere, on vaccines, Ireland’s Makhlouf says the ECB will have to evaluate the emergence of the COVID-19 vaccine, suggesting that no firm view on the matter is currently held by the Governing Council at this stage; however, Vice President de Guindos noted that vaccine developments will be taken into account at the meeting. On the prospects for a further dive into negative territory for the deposit rate, Spain’s de Cos refused to rule out a rate reduction, but acknowledged that rates were close to the lower bound, Austria’s Holzmann has stated that such a move would not have an effect. In terms of lesser talked about measures the Bank could take, outgoing Hawk Mersch recently pushed-back on the prospect of the ECB expanding its purchase remit to include “fallen angels”

RATES: From a rates perspective, consensus looks for the Bank to stand pat on the deposit, main refi and marginal lending rates of -0.5%, 0.0% and 0.25% respectively. A recent research piece from the Bank noted that the reversal rate for the deposit rate stands around -1%, suggesting there is around 50bps of space until further rate reductions could become counterproductive. That said, whilst all options are said to be on the table (and it might help stem some of the recent EUR appreciation), commentary from central bank officials has done little to suggest that rate tweaks are on the cards. Additionally, when faced with the option of lowering the deposit rate in March as the crisis was unfolding, policymakers refrained from doing so. As a guide: markets currently assign a 13.5% chance of a 10bps cut to the deposit rate at the upcoming meeting and around a 55% probability by the end of next year.

BALANCE SHEET: With the balance sheet seen as the preferred easing tool for the Governing Council, focus remains on any adjustments to its bond-buying operations. Its PEPP currently has an envelope of EUR 1.35trl and is set to run at least until the end of June 2021, whilst its regular Asset Purchase Programme (of which the Public Sector Purchase Programme is a component) runs at a monthly pace of EUR 20bln together with the purchases under the additional EUR 120bln temporary envelope until the end of 2020. A Reuters survey of economists stated that expectations are for a EUR 500bln addition to the PEPP programme and 6-month extension until December 2021. UBS also expects the ECB to extend its commitment to reinvesting the principal of maturing securities purchased under PEPP by another year, from currently end-2022 to end-2023. Note, 33 of 44 surveyed do not think that the ECB will expand the PSPP, according to the survey. Going back to PEPP, expectations have continued to gather steam since the October meeting, and it remains to be seen if policymakers could trigger a “dovish surprise” on this front. Policymakers could opt to increase the PEPP by more than EUR 500bln, however, in recent weeks policymakers have placed greater emphasis on reassuring markets about the duration of its support. Accordingly, ECB’s Schnabel has touted the possibility of a 12-month (consensus looks for 6-month) extension to PEPP. Additionally, the prospect of including “fallen angels” into its Corporate Sector Purchase Programme (CSPP) lingers around the bank, however, this idea recently received pushback from outgoing hawk Mersch.

TLTROs: Given recent rhetoric from policymakers on the efficacy of Targeted longer-term refinancing operations (TLTROs), a tweaking of its current operations has also formed part of the consensus ahead of the meeting. As it stands, the facility has just two auctions left (10th December, and 18th March 2021) with current borrowing conditions running with a rate of -0.5% for three years or as low as -1% for banks that reach certain lending requirements. The Reuters survey found that 37 of the 48 economists surveyed expect the ECB to change the terms of its TLTROs, however, there are differing views on how this will be carried out. SocGen highlights four potential ways in which the ECB could act on this front, 1) it could go for a longer maturity, or signal continuous TLTROs, 2) it could lower the threshold for the best available rate, 3) lower the best interest rate below -1%, and 4) include new loan types such as mortgage lending. SocGen themselves predict “largely unchanged conditions” with “around five quarterly operations until March 2022, for corporate lending only, 3-year loans at -1% at best, lending threshold for best rate at 0%”.

TIERING: Another option for the ECB could be an adjustment to the existing tiering multiplier of six (exempt from negative interest rates) amid rising levels of excess liquidity. However, a complicating factor is that a large part of the recent increase in excess liquidity is attributed to the ECB’s TLTRO-III facility. Therefore, an increase in the tiering multiplier could undermine policymaker’s efforts to get banks to lend to the corporate sector. One option, UBS says, would be for the ECB to exempt funds from TLTRO-III, in which case it could raise the tiering multiplier to nine from six in order to keep banks’ deposit costs constant. However, UBS suggests that even this could prove to be too generous given the lending incentives in the TLTRO scheme that already reduce net deposit costs. As such, the Swiss bank looks for no adjustment on this front in December. Additionally, SGH Macro notes that an increase in the multiplier would be unlikely to occur unless met with an accompanying deposit rate cut.

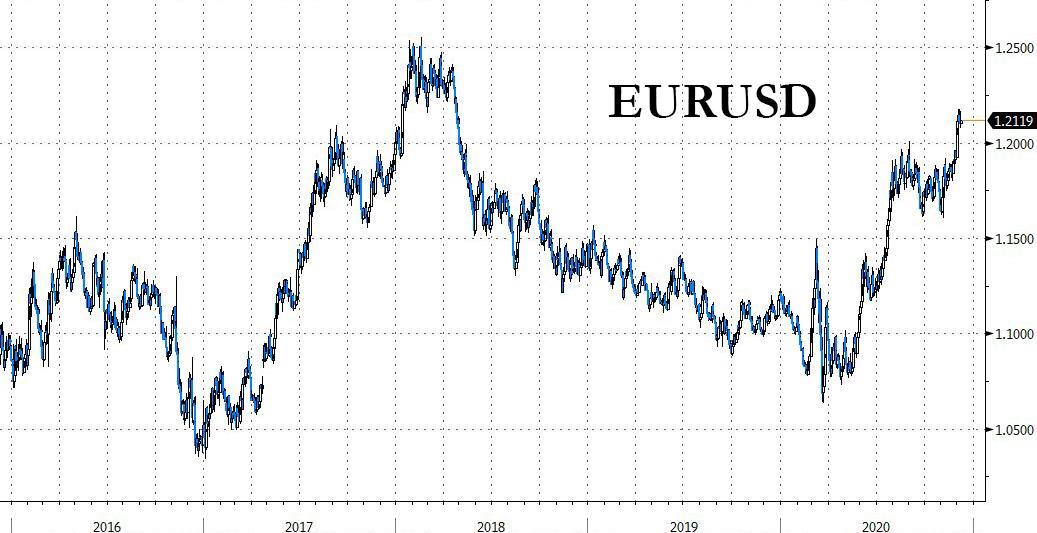

EUR: The recent appreciation of the EUR which has seen EUR/USD breach 1.20 and trade at levels not seen since 2018, has raised questions as to whether or not the ECB will attempt to talk down the currency. Note, at the September meeting after EUR/USD breached 1.20, President Lagarde noted that “the ECB does not target an FX level but will continue to monitor developments, including the EUR”. Morgan Stanley, however, suggests that we are not at levels that will concern policymakers given that the move in EUR/USD is more of a by-product of USD weakness, rather than EUR strength. In fact, the trade-weighted Euro is “a little weaker than in the summer,” the bank notes. As such, the EUR may prove to not be a major feature of the upcoming meeting.

ECONOMIC PROJECTIONS: Please see below for the September Staff Economic Projections: Inflation: 2020 +0.3% (unch), 2021 +1.0% (prev. 0.8%), 2022 +1.3% (unch) GDP: 2020 -8.0% (prev. -8.7%), 2021 +5.0% (prev. +5.0%), 2022 +3.2% (prev. +3.3%) This time around, from a growth perspective, despite a potentially disappointing Q4 outturn, better than expected growth in Q3 should see the ECB revise its 2020 estimate upwards to -7.2% from -8.0%, according to UBS. For 2021, despite the positive COVID vaccine updates, the fallout from Q4 2020 should prompt just a modest upgrade of its forecast to 5.0% from 5.5%, albeit this is largely dependent on how the ECB factors in the (yet-to-be passed) recovery fund. For 2022 and 2023, the Swiss bank pencils in growth of 3.9% and 1.9% respectively. On the inflation front, UBS expects the 2020 reading to be revised lower to 0.2% given softer prints in recent months relative to ECB expectations, whilst the better growth environment should offset any drag from softer oil prices in 2021 and 2022, leaving them unchanged at 1.0% and 1.3%. Of potentially greater interest will be the initial 2023 estimate, which UBS expects to remain below the pre-COVID inflation trend of 1.6% and therefore warrant additional stimulus.

STRATEGIC REVIEW: One issue lingering at the Bank is its ongoing strategic review. The review has been delayed by the pandemic with its findings now not due to be released until September 2021. However, on the 30th September, President Lagarde delivered a speech in which she highlighted some preliminary considerations for the review. Lagarde noted that the ECB would be considering whether to depart from its current inflation target of “below, but close to 2%” and move towards a more “symmetric” target that would tolerate overshooting the 2% threshold. Ahead of the October meeting, Morgan Stanley suggested that accelerating the release of the outcome of the review could amount to another policy option for the Bank. However, MS noted that given the current H2 2021 timeframe, it seems implausible that the findings could be released in the near-term, particularly given reports of differing views on the Governing Council, which will make fostering consensus a more difficult task.

* * *

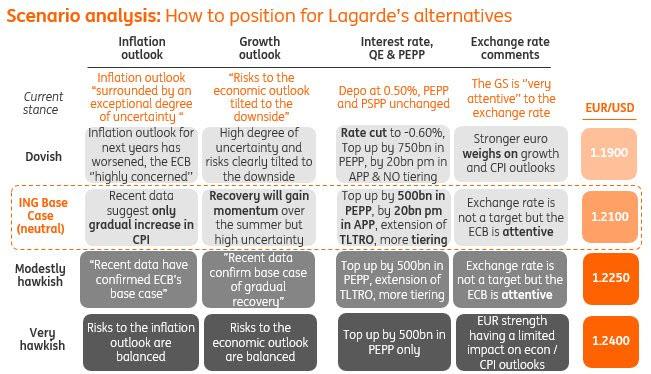

Finally, here is the traditional scenario matrix analysis from ING Economics, which as usual should be rather useful for FX traders hoping to gauge how to trade the Euro based on what Lagarde unveils tomorrow.

via ZeroHedge News https://ift.tt/3lZqLmn Tyler Durden

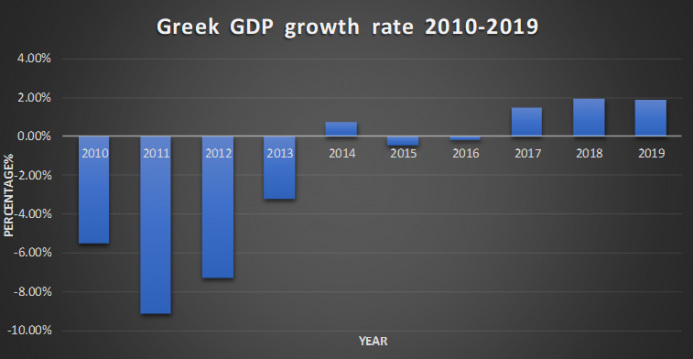

The Greek economy shrunk by a record 14 percent in the second quarter of 2020 while at the same time government efforts to ‘’cure’’ the economy have set the country on the road to cross the 200 percent debt-to-GDP ratioas the IMF forecasts. In the meantime, government budget deficits have reached new heights (around 7 percent).

The Government’s Response to the Recession

The Greek government tried to combat the economic downturn with a loose fiscal and monetary policy (through the European Central Bank). The initial aim was to support pretty much everyone from the public and private sector for the bad months of the covid-19 lockdown and hope for economic recovery when the summer arrived, with the tourist industry saving the day. It soon became evident, however, that this was wishful thinking. People from the tourist industry admitted that it could take years for the industry to recover its past numbers. The situation looked even worse once people realized how dependent the whole economy is on tourism: it accounts for 20 percent of GDP and provides 22 percent of all employment in Greece. Furthermore, the Greek government’s solutions, like those of most of the other governments in Europe, were primarily demand-side policies.

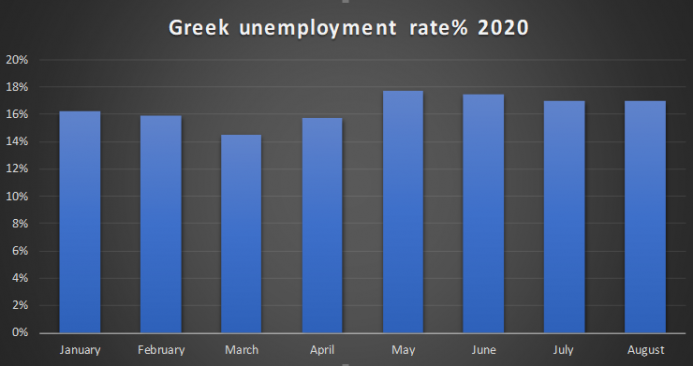

As I predicted in one of my past articles, these measures could only provide short-run relief, only postponing the pain until later. The unemployment rate saw a 1.2 percent increase from March to April, of 1.3 percent from April to May, and it saw a minor decrease during the summer tourist period. The Organisation for Economic Co-operation and Development (OECD) has estimated that the unemployment rate will reach roughly 20 percent by the end of the year.

Source: Trading Economics.

In the meantime, that the GDP saw a 14 percent contraction in the second quarter means that the Greek economy will need years to reach its precorona numbers, especially considering its anemic growth rate over the last decade.

Source: International Monetary Fund, World Economic Outlook: The Great Lockdown (Washington, DC: International Monetary Fund, April 2020).

What Went Wrong?

The ECB’s balance sheet had a massive increase from 39 percent of the GDP to 54 percent during the summer. In comparison the Fed’s balance sheet is around 32 percent of GDP. The injections of liquidity via the ECB have effectively zombified a considerable number of companies in the EU, with corporate debts reaching new highs. In the case of Greece, the government has exploited its new, EU-sanctioned fiscal leeway, which has allowed it to perpetuate structural problems in its economy along with large deficits. During the tourist season, the costs were so high that a considerable segment of the tourist industry decided to not even work this summer since they would lose less money this way.

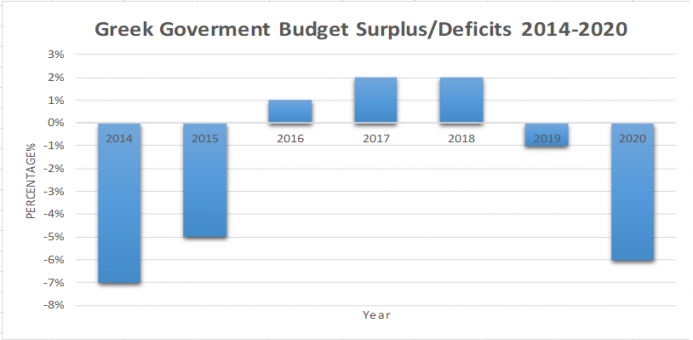

Government intervention made things even worse by failing to address the biggest problem in the economy, which is its inflexible labor laws. Rather than partially liberalizing the laws, the state made them even more restrictive and inflexible. For this reason, businessmen have failed to adjust to the corona crisis shock. Making hiring more expensive and riskier is a recipe for disaster, especially in a fragile economy that lacks savings and investments like Greece. While the spending didn’t manage to stimulate the economy, we can’t say that it had an immediate negative effect short term at least, since it was mostly financed by the European Union. On the other hand, cheap credit and loans were made possible by the ECB and by putting political pressure on banks, thus prolonging another major structural problem of the overall economy: lack of savings and more debt. The budget deficits are also a matter that needs to be addressed, since it has reached new highs, making the 2010s a lost decade for the whole economy, since the whole point of ‘’European austerity’’ was to make the debt more sustainable.

Source: Trading Economics

As the Greek minister of finance admitted the tax cuts that were made during the last few months won’t be permanent, since the new target is for Greece to have the biggest fall in debt-to-GDP in the eurozone. The state secretary of finance also talked recently about a possible new austerity program similar to that of the previous decade. On the surface, budget surpluses are a good thing and much needed, but it is important to ask these surpluses will become a reality. The tax cuts won’t be permanent, so it seems that Greeks will soon be undertaking the same failed strategy that they tried for a decade and was promoted by European officials in Brussels—high tax rates to increase government revenues but very minimal cuts in public expenditures. But the problem wasn’t the tax cuts but government spending and deficits. Deficits have a greater crowding-out effect on the private sector than just spending. At the end of the day, these deficits will have to be paid by future generations. Potential tax increases in the future would be an even bigger disaster for the private sector. The cure is worse than the disease.

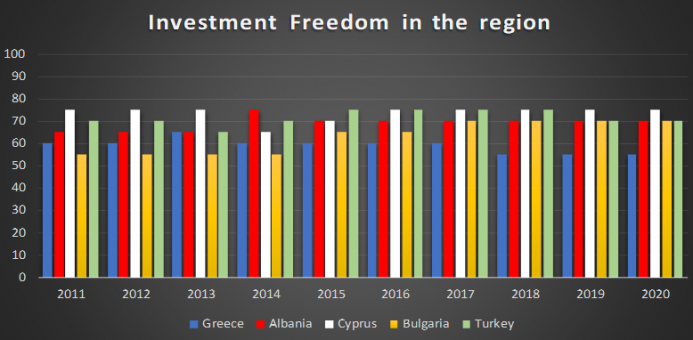

The center-right government that came into power in July of 2019 has failed to liberalize the economy and make market-oriented reforms, and the pandemic has made things even worse. It hasn’t made any major tax cuts that would be permanent and could have a big impact on alleviating some of the pressure on the private sector. Deregulation was also a major issue: the Greek economy was and still is in desperate need of foreign investment; however, investment freedom hasn’t seen a significant increase, and major investments and infrastructure programs are way behind schedule. Bureaucratic obstacles extend even to the judiciary branch, making it inefficient and slow, with corruption widespread.

Source: Heritage Foundation, Index of Economic Freedom, 2020.

The Heritage Foundation’s Index of Economic Freedom can give us some useful insight on state economic freedom in Greece.

The following graph compares investment freedom in Greece with countries that compete for investment in the same region.

Source: Heritage Foundation, Index of Economic Freedom, 2020.

Conclusion

People need to understand that when you have an economy with weak productivity that’s highly indebted, shutting down the economy two times in one year has repercussions that will be here to stay for years depending on the recovery policies. The economy needs major structural reforms. Labor laws need to be liberalized. Budget surpluses are indeed the correct goal, especially now, to avoid another debt crisis, but the surpluses need to come from cuts made in the public sector. Tax cuts need to become permanent and even bigger for the economy to grow and expand. Last but not least, making foreign and domestic investments easier, less expensive, and minimizing the potential risk is a matter of utmost urgency, since Greece is being outcompeted by neighboring countries.

Greece needs to take advantage of its potential. A business-friendly environment with a liberalized market is the way to go. It can minimize the negative effects of the corona crisis and solidify a slow but strong recovery that will make the country more productive and give it prospects of getting out economic trouble and becoming an economic powerhouse in the region.

via ZeroHedge News https://ift.tt/3741UcU Tyler Durden

Macron Under Fire For Suppressing Footage Of Red-Carpet Treatment For Dictator Sisi Tyler Durden

Thu, 12/10/2020 – 04:15

Controversy over France’s military arms sales to Egypt kicked off this week after President Emmanuel Macron said he’ll pursue future sales of French arms to Gen. Abdel Fattah el-Sisi regardless of widespread human rights abuses.

“I will not condition matters of defense and economic cooperation on these disagreements (over human rights),”Macron said Monday after the two held talks in the Elysee Palace. “It is more effective to have a policy of demanding dialogue than a boycott which would only reduce the effectiveness of one our partners in the fight against terrorism,” he added.

Things got awkward, however when during the joint presser Sisi referenced recent controversy over caricatures of Muhammad, stressing that “it’s very important that when we’re expressing our opinion, that we don’t, for the sake of human values, violate religious values.”

Via AFP

“The rank of religious values is much higher than human values… They are holy and above all other values,” he added.

Macron pushed back afterward: “We consider human values are superior to everything else. That’s what was brought by the philosophy of the Enlightment and the foundation of the universalism of human rights.” The French president further emphasized that this meant French secular values allowed for publishing or displaying what others would consider blasphemy.

Various humanitarian organizations lashed out at Macron’s explicitly saying he remains unconcerned by Sisi’s well documented history of harsh repression and even in some instances torture of political dissidents, as well as the jailing of journalists. France24 news reports:

Human rights clearly “comes second” to French President Emmanuel Macron when he invites his Egyptian counterpart to France for a state visit.

So says Human Rights Watch’s Katia Roux, hitting out at the French leader, despite Macron saying he spoke frankly and openly to Abdel Fattah al-Sisi about human rights during the visit. Roux says economic and strategic interests clearly come first, despite thousands of activists being jailed in Egypt amid a vast crackdown on civil society under Sisi’s leadership.

The controversy has continued this week after a French broadcaster has charged that the French presidency’s office is trying to hide footage of Macron rolling out the red carpet for Sisi, and laying out a lavish banquet and feast, also in which Macron awarded the Egyptian dictator the prestigious grands-croix de la Légion d’honneur medal.

Wow, Macron has actually tried to hide the fact that he awarded the highest French state medal to Egyptian dictator Sisi.

French broadcaster: “ we had to go to the website of an authoritarian regime to find out what is happening at the Elysee Palace.” pic.twitter.com/4sulRRAZRW

But Macron is still being blasted in European media and among human rights organizations for his two-faced hypocrisy given he often lectures other countries on maintaining a high human rights standard.

Turkey is especially angered over the whole spectacle and is calling it out given Macron and Erdogan have lately been in fierce disagreement on a range of issues from Armenia, to Libya to the issue of Turkish Mediterranean gas exploration and drilling.

via ZeroHedge News https://ift.tt/3qGHL49 Tyler Durden

Euro Turns From Foe To Friend In Everything Rally Tyler Durden

Thu, 12/10/2020 – 03:30

By Michael Msiak and Vassilis Karamanis

This time around, the revenge of the euro is proving no threat to Europe’s ferocious stock rebound, as the likes of Goldman Sachs Group Inc. project more gains in the region’s everything rally.

Even as the currency climbs above $1.20 to the dollar – a level that has spurred European Central Bank verbal intervention in the past — the Euro Stoxx 50 is fast retracing pandemic losses. It’s down less than 6% for the year.

A strong exchange rate typically hits exporters that have an outsize weighting in the benchmark. Now, cyclical companies are on a tear thanks to the global economic recovery and rising animal spirits. Domestic names look ready to join the party. The last time that stocks and the euro rose in concert for an extended period of time was between July 2012 and May 2014.

“A stronger euro is not necessarily a negative for European stocks,” Goldman Sachs strategist Sharon Bell said in a note last week, pointing to the positive correlation between shares and the single currency over the past two months. Economic growth matters more for earnings than foreign-exchange rates for now, she added.

The common currency is heading for its best year since 2017, buoyed by a revival in reflation trades on higher growth and vaccine bets. Positioning, chart patterns and options gauges suggest the euro is poised to extend its advance in 2021. Goldman economists, for example, expect it to appreciate toward $1.25 as the region’s consumption and investment cycle rebounds.

European cyclicals that are tracking moves in the exchange rate have the potential to outperform anew while domestic companies also have catch-up potential, according to the U.S. bank.

The pain threshold? A Bloomberg survey in August signaled that a rapid move toward $1.30 could cause problems for stock benchmarks. Of course, the flip side of the stronger euro is a weakening dollar that’s loosening international financial conditions and greasing the wheels of commerce.

“A weak dollar is directly linked to boosting global trade,” says Jefferies strategist Sean Darby. “This is not just emerging market economies, but Europe too, which have a high percentage of trade as a percentage of GDP,” he added.

One risk for euro bulls comes from the ECB, which may imminently seek to temper the appreciation trend.

“At their Dec. 10 meeting, the ECB Council will likely expand and extend – possibly to 2023 – the PEPP operations, and repeat their unhappiness with the strong euro,” says Stephen Jen, CEO and Co-CIO of Eurizon Slj Capital.

Still, with institutional investors adding to their long positioning in recent months, plenty of traders are girding for more currency gains as optimism returns – helping bullish stock sentiment along the way.

via ZeroHedge News https://ift.tt/2LdiVIT Tyler Durden

Merkel Touts Germany’s COVID Response Hasn’t Been “Dictatorship-Style” Like Other Countries Tyler Durden

Thu, 12/10/2020 – 02:45

Chancellor Angela Merkel is raising eyebrows across Europe for a veiled yet blistering critique of how other countries have handled coronavirus lockdowns and restrictions. It came in the context of urging Germans to take distancing measures seriously over the holidays and while justifying a new lockdown, which has included school closures.

On Wednesday while addressing Germany’s parliament in Berlin she touted that she’s led a sensible, balanced and “flexible” response while avoiding the extreme of “dictatorship”-style restrictions as in other countries.

“Our political action is different from what they do in countries that are more like a dictatorship,” Merkel told the parliament. She described that the appropriate answer from federal and local governments is not blanket bans on activities but policies that emphasize “the responsible behavior of each individual.”

Via AP

Many German citizens might disagree, however, given rolling protests in major cities since last month provincial governments were given formal approval to enact a second wave of shutdowns, including of restaurants, cultural sites and entertainment and leisure venues such as sports complexes.

Berlin called the measures a “lockdown lite” given it wasn’t done according to a ‘one size fits all’ policy. Authorities have blamed ‘extremists’ for holding large maskless demonstrations protesting the new shutdowns after cases recently spiked ahead of winter.

Germany has still faired better than other countries, despite its over 1.2 million cases including 20,000 deaths from COVID-19. Merkel in her Wednesday remarks said this number remains “too high”.

Police stand between anti-lockdown protesters and counter-demonstrators in #Bremen, Germany. Police break up banned Bremen lockdown protest. An anti-lockdown group in Bremen had filed an urgent court appeal in … pic.twitter.com/j9DrnMlHwk

Though she didn’t name countries she deems to have led a “dictatorial” response to fighting coronavirus, there’s lately been multiple viral videos showing harsh police crackdowns related to violating social distancing measures out of places like the UK, Australia, and Israel.

Merkel further reportedly indicated that the majority of the population would not have access to a coronavirus vaccine until much later in 2021.

via ZeroHedge News https://ift.tt/370Ig18 Tyler Durden

Last month the trial began in Belgium of Assadolah Assadi and three other Iranians accused of planning a bomb attack in Paris in 2018. Since 2015 Assadi had been the most senior officer of Iran’s Ministry of Intelligence and Security in Europe, at the time operating under diplomatic cover at the Iranian embassy in Vienna. He is the first Iranian government official to be tried by an EU country for terrorist offences, despite numerous attack attempts on EU soil ordered by Tehran.

State supported terrorism is not just an act in itself but also an instrument of national power and coercion. Together, these plots were a malevolent message and clear threat to Europe that unfortunately have been received and acted upon as intended in London, Berlin, Paris and Brussels.

Assadi’s failed plot was reportedly ordered by Iranian President Hassan Rouhani and approved by Supreme Leader Ali Khamenei. His target was a rally for the National Council of Resistance of Iran, with 80,000 supporters present and attended by former Canadian Prime Minister Stephen Harper, President Trump’s lawyer Rudy Giuliani and several British and European members of parliament. The explosives, allegedly brought into Europe from Iran by Assadi on a commercial flight, were TATP, the same type as was used to kill 22 and wound 800 in a jihadist attack at the Manchester Arena, UK, in 2017 and the London 7/7 bombings that killed 52 and wounded 700 in 2005. The message was clear. In March Assadi, who has refused to attend his own trial claiming diplomatic immunity, threatened retaliation if he is convicted. The Iranian government has also warned of a “proportionate response” against countries involved in the trial.

Assadi’s bombing was prevented by European security authorities using intelligence provided by Israel. Mossad previously passed intelligence to the British security agency MI5 that enabled them to disrupt another Iranian-directed bomb plot in 2015. Terrorists linked to the Iranian proxy Hizballah had stockpiled three metric tons of ammonium nitrate in North London — the same explosive material that caused such devastation in Beirut earlier this year. The quantity in London was greater than the ammonium nitrate that killed 168 people, injured 680 and damaged hundreds of buildings in the 1995 Oklahoma City bombings.

The same year as the London attempt, another Hizballah bomb plot was uncovered in Cyprus, also an EU member, this time involving 8.2 metric tons of ammonium nitrate, and again revealed to Cypriot authorities by Mossad. There had also been an attempt in Thailand in 2012 and, two years after the London plot was uncovered, indications of a similar plan in New York. The same year as the Thailand plot, Hizballah murdered five Israeli tourists and a driver when they bombed a bus at Burgas in Bulgaria, another EU member state.

Iranian-organized terrorist attack plans were uncovered in Germany in 2017 and Denmark in 2018, both EU members, and also in 2018 in Albania, a formal candidate for accession to the EU. Two Dutch citizens of Iranian origin were assassinated in the Netherlands, another EU state, on orders from Tehran in 2015 and 2017.

The attacks in EU countries since 2015 have all occurred during the time when Britain, France, Germany and the EU were actively involved in the JCPOA, the Iranian nuclear deal with the P5+1. European reactions have been predictably limited, with many suspecting that the weak response was due to a desire to avoid endangering the JCPOA. Until exposed in 2019 by a Daily Telegraph investigation into Hizballah terrorist activity in Europe, British authorities kept the 2015 London bomb plot secret, apparently due to pressure from the Obama administration to suppress details, to avoid compromising the nuclear deal.

Despite, or maybe because of, such terrorist outrages against them, the EU states played along with Iran, refusing to follow the US in disavowing the nuclear deal, in part a response to Iranian regional aggression and sponsorship of international terrorism. Rather than joining President Trump’s “maximum pressure” campaign to modify Iran’s behaviour, the Europeans supported Tehran and undermined the US, even seeking to subvert American economic sanctions by setting up a financial instrument, INSTEX, to allow continued trade with Iran. European governments also failed to oppose lifting UN conventional weapons sanctions against Iran this year and refused to support US snapback sanctions following Iran’s flagrant breaches of the nuclear deal.

Last year, the EU reluctantly imposed token financial sanctions on a section of the Iranian Ministry of Intelligence and Security and two officials after the terrorist plots in Paris and Denmark in 2018. Undermining their own actions and kowtowing to Tehran even while announcing these limited measures, EU officials made a point of emphasising their enduring support for the JCPOA and intent to continue trading with Iran. Since then EU leaders have vociferously protested the elimination of Qasem Soleimani, mastermind of Iran’s terrorist operations directed at them, and Mohsen Fakhrizadeh, nuclear scientist and Soleimani’s fellow general in the Islamic Revolutionary Guard Corps, a proscribed terrorist organization responsible for facilitating attacks in Europe.

Britain, Germany and especially France had severe reservations about the JCPOA during negotiations with Iran, especially over the sunset clauses that allowed expiry of provisions limiting Tehran’s access to nuclear material and advanced technology, and in reality paving a path to the bomb. They were railroaded into accepting the flawed deal, however, by President Obama’s determination to secure his legacy despite Iranian intransigence. Their failure to follow Washington out of the deal was due to misguided loyalty to Obama, contempt for President Trump and a desire to appease Iran, rather than genuine strategic calculation.

Now they find themselves locked into what they know is a phoney and highly dangerous nuclear agreement that simply consigns confrontation with a nuclear-armed Iran to future generations. Presumptive President-elect Biden and his prospective administration officials have made clear their intent to return to the deal, and Iran is desperate that they do so in order to relieve the existential pressure on its economy from current US sanctions and to clear the way for its nuclear breakout. Of course Tehran’s enthusiasm to resurrect the deal will be carefully disguised as the opposite while they push for even more favourable terms than last time.

Freed from their self-defeating scorn of Trump, there will soon be an opportunity for European governments finally to act in their own best interests, and those of their children, by persuading Biden only to accept a deal with Tehran that genuinely constrains the ayatollahs’ nuclear ambitions and curbs their regional aggression. First, however, they must confront their own fears of Iran.

Iran launched the numerous potentially devastating terrorist plots in Europe, at a critical stage for the nuclear deal and the survival of the Iranian regime, as a message directed at London, Paris, Berlin and Brussels. The targets were Iranian opposition figures. It was convenient to murder them to deter other dissidents and to warn Europe against harbouring or supporting them. But it wasn’t necessary, in particular given any risk of potential backlash from Europe. The leadership would not have done so had they in fact feared damaging retaliation.

The Iranian leadership ordered these attacks to show their supposed strength and directly to warn the Europeans of the dangers of defiance. They look at Europeans, as well as Americans, with contempt, as weak and decadent, lacking the courage or resolve to stick up for their own interests, as people they can trifle with, as they have done repeatedly in the past. President Trump gave them pause for thought, especially when he ordered the death of Qasem Soleimani, second in importance only to the Supreme Leader himself. They have higher hopes of Biden, whom they expect to be more supine.

We can be sure the Supreme Leader has rejoiced at the results of his message: cowering in Europe, with only weak and token response, accompanied by a desperate, pleading assurance that the targets of his aggression are still his friends. If ever there was a lesson that appeasement fails and strength succeeds, surely this is it. European governments must now show their own strength or face continued Iranian coercion — coercion that will be witnessed by malign actors around the world from Moscow to Beijing to Pyongyang, with obvious implications. That strategic imperative aside, can the Europeans really afford to allow such an egregiously hostile and manipulative regime as Tehran to acquire nuclear weapons?

* * *

Colonel Richard Kemp is a former British Army Commander. He was also head of the international terrorism team in the U.K. Cabinet Office and is now a writer and speaker on international and military affairs.

via ZeroHedge News https://ift.tt/2KeaZGI Tyler Durden

The United States is mired in a succession crisis. There is much loose talk about another civil war erupting between supporters of President-elect Joe Biden and President Donald Trump. As this occurs, America’s enemies act boldly against U.S. interests. Each precious moment wasted on deciding which septuagenarian won the White House in November is another moment that the Chinese Communist Party continues its long march to global dominance.

China’s dominance will not come at first in the form of military conquest. Beijing is very much a 21st century power, and its program for displacing the United States will look far different from what the Soviet Union tried during the Cold War. Chinese dominance will be brought on by superior trade, industrial, and technological development practices.

Beijing recently signed a revolutionary free trade alliance with several Asian powers—including Australia—meant to increase China’s influence over the Indo-Pacific and diminish Washington’s hard-won influence there. China announced it had achieved quantum supremacy—a lodestar for whichever country or company seeks to pioneer quantum computing. Many technologists, like Scott Amyx, have previously argued that quantum computing could be as disruptive to the world economy as the cotton gin or automobile were. Whoever dominates this new industry will write humanity’s future.

And then there’s the new space race between the United States and China. Private launch companies, including SpaceX, have revolutionized America’s overall space sector. But the lack of political vision or leadership means that real gains for America in space will be slowly realized, if ever. President Trump was the only American leader in decades who seemed to understand the promises and challenges of space. Yet, the rest of the government never fully embraced Trump’s robust space program. Now, it may be too late.

NASA’s Artemis Program, which is supposed to return Americans to the moon, is adrift, stuck in what Hollywood types might call “development hell.” Petty politics, budgetary constraints, and bureaucratic inertia have prevented this essential program from lifting off in a timely way. Judging from the profile of the individuals that President-elect Biden chose for his NASA transition team, it looks as though the Artemis program will be reduced even more in importance.

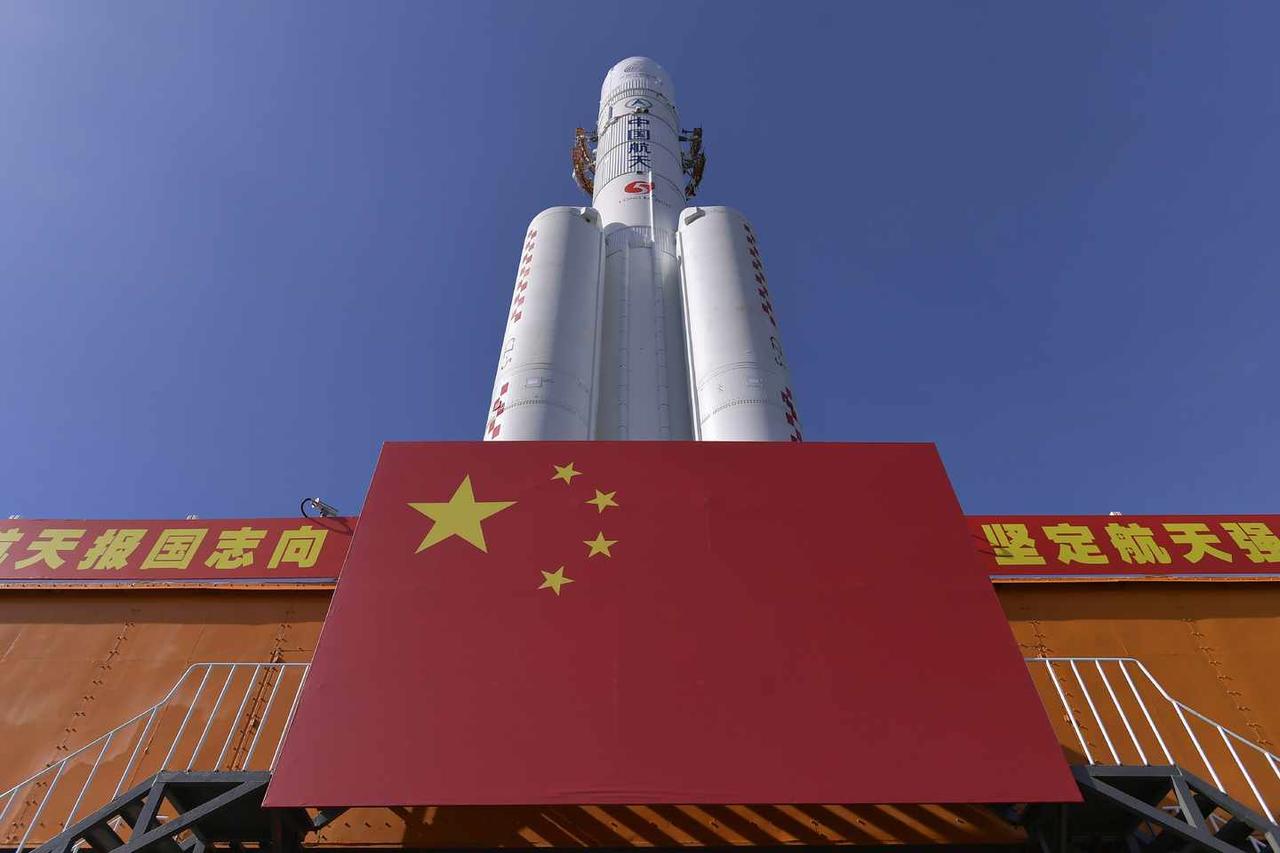

Meanwhile, the Chinese have not only landed a rover on the dark side of the moon, but they have now successfully retrieved lunar rocks—the first time in decades that this has been done. China’s leadership does not intend to stop with unmanned missions to the moon. The recent Chang’e-5 mission (launch rocket pictured above) was merely the proof that China has achieved the same capabilities as the Americans.

Now, China will outpace America. Two years ago, Ye Peijian, the head of China’s lunar mission, declared that China’s leaders viewed the moon as they do the South China Sea, with Mars being analogous to Huangyan Island. Meanwhile, NASA is reduced to begging for money to create new spacesuits for its lunar mission.

Compare these events today to the Cold War. In the Cold War between the United States and the Soviet Union, the competition between the two superpowers was visceral and the stakes were existential. There was no area of human life where the conflict did not play out … and where the combatants did not fight with everything they had to win.

When the Soviet Union beat the Americans by getting humanity’s first satellite in orbit—Sputnik—most Americans and their leaders rightly panicked. By the time the USSR placed the first human in orbit, America’s leaders knew that they could not simply shrug and lazily say, “We’ll get there eventually, too.”

This lackadaisical attitude that yesteryear’s Americans quickly overcame, however, is precisely how the Americans have responded to China’s impressive gains over the last few years. Denialism will not preserve America’s superpower status. Decisive political action will. America’s leaders, however, are still bickering with each other over petty partisan politics. Xi Jinping and China’s leaders laugh and march on.

Had it not been for the virile leadership of John F. Kennedy and his declaration at Rice University in 1962 that the United States would send the first humans to the moon by the end of that decade, the Soviets would have defeated the Americans in the moon race as well. Had that occurred, history for the rest of the Cold War would have played out differently. The spin-off technology that the Apollo program provided the United States might never have been realized in America. Instead, those impressive gains would gone to the USSR … and the inevitable implosion of the Soviet Union might have not happened.

Between China’s breakthrough in quantum supremacy and its successful lunar missions—as well as its clearly defined strategy for achieving dominance in both the high-tech sector and in space—the American leaders have ignored multiple Sputnik moments. China now has momentum in this new cold war. America’s political instability is only exacerbating these frightening trends.

What’s needed now is a bipartisan commitment to investing in the technology and capabilities that will allow for the United States to leapfrog the Chinese in critical areas, including quantum computing. American leaders must also ensure that the United States remains the dominant space power by permanently placing astronauts on the moon and Mars, and by deploying defensive space weapons above the Earth.

As an investor from China once told me, “When the donkey and elephant make war upon each other, few in your country benefit.” The bitter partisan divide in America today is a strategic liability. This division will affect the trade, economic, technology, and space policies of this country—at a time when consistency and bipartisan leadership is needed in all these areas. Until we recognize China’s threat and rally as one nation, America’s surrender to China in the new cold war is assured.

via ZeroHedge News https://ift.tt/3709jtB Tyler Durden

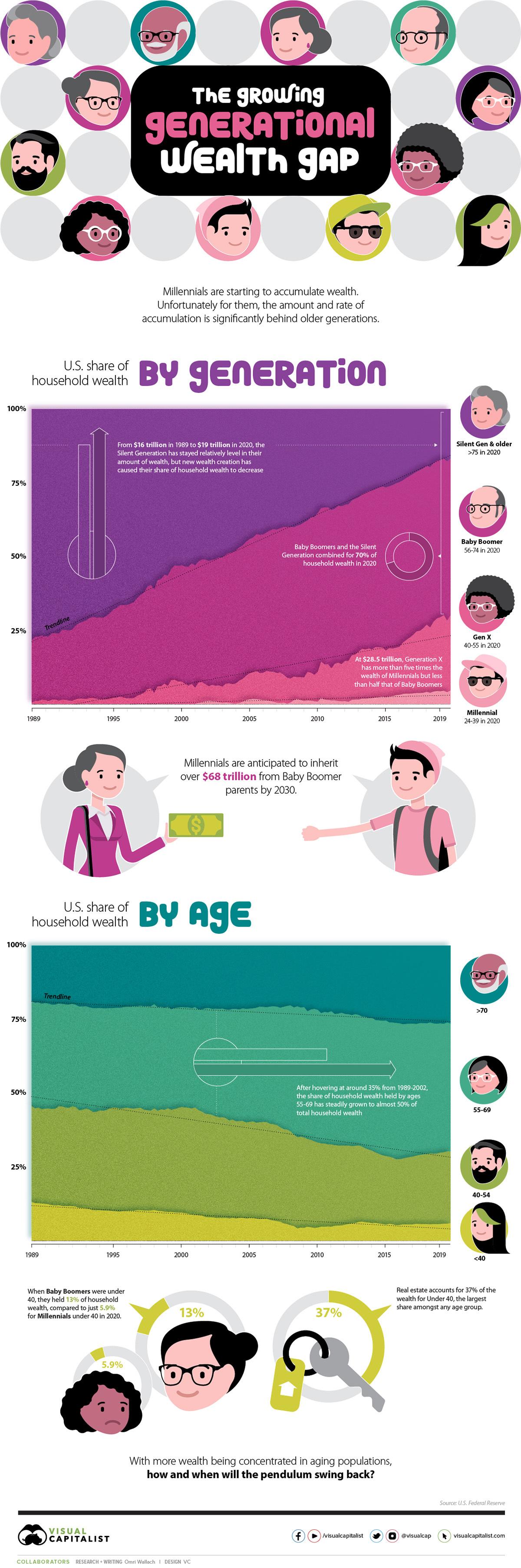

In the U.S., household wealth has traditionally seen a relatively even distribution across different age groups. However, over the last 30 years, the U.S. Federal Reserve shows that older generations have been amassing wealth at a far greater rate than their younger cohorts.

As the visual above shows, the older have been getting richer, and the younger have been starting further back than ever before.

By Generation: Baby Boomers Benefit & Millennials Lag

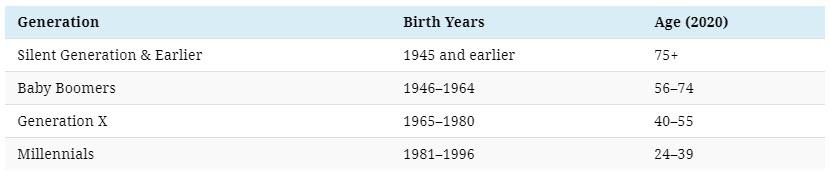

To examine the proportion of wealth each generation holds, it’s important to clearly define each age group. Though personal definitions might differ, the U.S. Federal Reserve uses a clear metric:

Relative to younger generations growing up, the Silent Generation and Greatest Generation before them have seen a decreasing share of household wealth over the last 30 years.

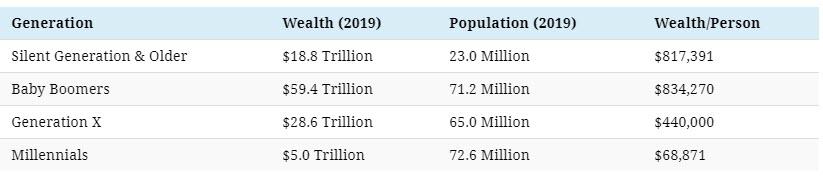

However, the numerical levels have been relatively stable. For these combined generations, total wealth has gone from $16 trillion in 1989 to $19 trillion in 2019, with a peak of $27 trillion in 2007. Considering this cohort has understandably shrunk over time—from an estimated 47 million to 23 million in 2019—their individual shares of wealth have actually increased.

Immediately following are the Baby Boomers, who held more than half of U.S. household wealth towards the end of 2020. At $59 trillion, the generation holds more than ten times the amount held by a comparative number of Millennials.

With $29 trillion held in 2019, Generation X has also been gaining in wealth over the last 30 years. It’s good enough for five times the wealth of Millennials, though at just $440k/person, they’ve fallen far behind Baby Boomers in rate of growth.

Finally, trying to catch up to their older cohorts are Millennials, who held the least amount of household wealth ($5 trillion) for the greatest population (73 million) in 2019, an average of just under $69k/person.

For a direct comparison, it took Generation X nine years to climb from their start of 0.4% of household wealth in 1989 to above 5%, while Millennials still haven’t crossed that threshold. But it’s not all doom and gloom for Millennials. Their rate of growth is starting to rise, with the generation’s level of wealth climbing from $3 trillion in 2016 to $5 trillion in 2019.

By Age: A Growing Share for 55+

Though the generational picture is stark, the difference in U.S. household wealth by age makes the picture of shifting wealth even clearer.

Until 2001, the shares of household wealth held by different age groups were relatively stable. People aged 40-54 and 55-69 held around 35% each of household wealth, retirees aged 70+ hovered around 20%, and younger people aged under 40 held around 10%.

Since that time, however, the shift in wealth to older generations is clear. The 70+ age group has seen their share of wealth increase to 26%, while the share held by ages 55-69 has grown from 35% to almost half.

But not all ages are seeing an increasing slice of wealth. The 40-54 age group saw its share drop sharply from 36% to 22% between 2001 and 2016 before starting to recover towards the end of the decade, while the youngest cohort now hover around just 5%.

Breaking down that wealth by components is even more eye-opening. The 39 and under age group holds 37.9% of their assets in real estate, the largest share amongst any age group (and concentrated in the hands of fewer people) while older age groups have their wealth spread out across real estate, equities, and pensions.

But the difference is as much in assets as it is in opportunity. In 1989, Baby Boomers and Generation X under 40 accounted for 13% of household wealth, compared to just 5.9% for Millennials and Generation Z under 40 in 2020.

Will the Tide Turn for Generation Z?

As new and accumulated wealth has been built up in older generations, it’s a matter of time before the pendulum starts to swing the other way.

The Millennials age group are expected to inherit$68 trillion by 2030 from Baby Boomer parents. Of course, that payout isn’t going to be even across the board, with wealthier families retaining the bulk of wealth and the majority of Millennials laden with debt.

And with Generation Z (born 1997-2012) starting to come of age, the uneven playing field is making it hard to begin accumulating wealth in the first place.

Since it is in the best interest of societies to have wealthy generations that can drive economic growth, potential solutions are being examined all over the political sphere. They include different taxation schemes, changing estate laws, and potentially cancelling student debt.

Whatever ends up happening, it’s important to track how the distribution of wealth changes over the coming decade, and begin accumulating your personal wealth as best as you can.

via ZeroHedge News https://ift.tt/33YGUSK Tyler Durden

{kind=link}

{kind=link}

{kind=link}