Tesla Shares Slip Despite Company Reporting Record Deliveries In Q3 Tyler Durden

Fri, 10/02/2020 – 09:50

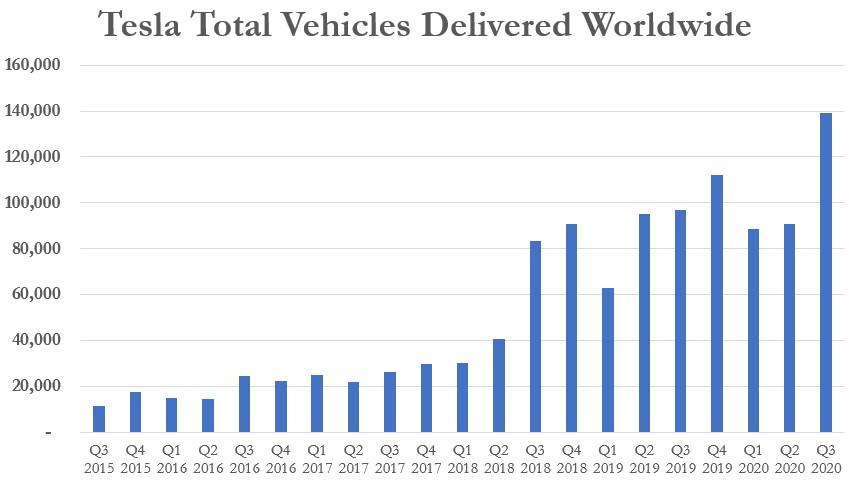

Tesla shares are volatile after moving slightly lower Friday morning as the company reported 139,000 vehicles delivered and 145,036 vehicles produced in the third quarter. The number marks a new all time delivery record for the automaker, beating out its previous record of 112,000 vehicles.

Production is up 50.8% year over year and deliveries were up 43.6% year over year. The numbers also mark what appears to be a return to normalcy after production was impacted during Q2 as a result of the coronavirus pandemic.

Analysts were expecting 137,000 vehicles delivered just days after the quarterly e-mail leak that Tesla is now becoming famous for suggested that the company could have a record quarter.

…while deliveries of Model 3 – which has been coupled with the Model Y since the beginning of 2020, carried most of the weight.

The idea of grouping its models together continues to confuse analysts and seems completely unnecessary, but for obfuscation purposes. As a reminder, major car companies like GM and Ford with many multiples more models than Tesla has, usually break out their sales on a per model basis.

Tesla has also not broken out its delivery and production numbers by region, which seems relevant now that the company is producing vehicles both in the United States and China.

Additionally, as one skeptic pointed out, the company is going to find it difficult to make its guidance for 500,000 vehicles produced for the year:

Hey, so to hit Fraud-Boy’s 500,000-car 2020 guidance, $TSLA only has to sell around 183,000 cars this quarter, lol.

So, instead, we have to go with photographs that are being produced on social media, like this one from Serramonte, California. These vehicles are all “delivered”, are we right?:

By popular demand, a Serramonte Update…well, it would be an “update” if anything had changed much. But this is not the case…more white Model Ys coming in steady. Customers are picking up cars, but obviously at way below replacement rate. $tslaQ$TSLA#SGFreportpic.twitter.com/T0524oSVAZ

Someone just emailed me a snapshot of the “unlimited Tesla demand” at its Mount Kisco, NY location. He says he’s been observing it for a long time, and it’s the most “demand” he’s ever seen there.$TSLApic.twitter.com/dEiYF9tl5J

California’s Governor Gavin Newsom, who is Nancy Pelosi’s nephew, is once again moving the goalposts in order to keep his state shut down, imposing irrelevant criteria to delay recovery. He has become an economic troll. With his state accounting for almost 15% of the national GDP, hobbling his state’s economy, even as counties are already starting to meet the criteria he set for relaxation of restrictions, depresses national output and employment statistics and thereby contributes to defeating President Trump.

Newsom, who is becoming known to Californians as Newssolini, is really stretching to find excuses to keep businesses closed and Californians unemployed and reverting to race-pandering. Jennifer Van Laar of RedState writes:

Now that more counties are set to move out of the most restrictive tier, Newsom’s changed the game again and has added an “equity requirement” counties must also meet before they can move down a tier.

From the California Department of Public Health website:

For a county with a population of greater than 106,000, the county must:

Equity Metric. Ensure that the test positivity rates in its most disadvantaged neighborhoods, as defined as being in the lowest quartile of the Healthy Places Index census tracts, do not significantly lag behind its overall county test positivity rate, as described in detail below.

Targeted Investments. Submit a plan that (1) defines its disproportionately impacted populations, (2) specifies the percent of its COVID-19 cases in these populations, and (3) shows that it plans to invest Epidemiology and Laboratory Capacity for Prevention and Control of Emerging Infectious Diseases (Strategy 5: Use Laboratory Data to Enhance Investigation, Response, and Prevention) grant funds at least at that percentage to interrupt disease transmission in these populations. The targeted investments can include spending on augmenting testing, disease investigation, contact tracing, isolation/quarantine support, and education and outreach efforts for workers. Effective for the October 13th tier assignment, this plan must be submitted before a county may progress to a less restrictive tier. Due to data limitations in small populations, the equity metric described above cannot be reliably applied to smaller counties, as described below.

With Democrats enjoying absolute dominance of the state Legislature, Newsom’s unilateral dictates will not be challenged by the lawmaking branch of the state government. And, with the state’s media at least as dominated by leftists as the national media, few voices will be heard by the public, who have been passively accepting economic strangulation in the name of safety, and now in the name of racial grievances.

There are real victims of this high-handed maneuver: businesses like restaurants that have been barely keeping their noses above water will go bankrupt and close permanently, and their employees will be jobless. I am an investor in a restaurant that was thriving until COVID, and despite the valiant efforts of its manager to stay alive, this may be the death blow.

* * *

Update:There are signs of revolution against Covid restrictions if you venture beyond the populous coastal enclaves. Michael Lewis writes at Bloomberg:

[Matt] Pontes is now the county executive officer of Shasta County in Northern California and goes to work in thin socks, but another crisis has found him.

“You cannot get closer to total disobedience of any kind of law,” he said, referring to the local response to Covid-19 strictures. “What’s happening up here is full-on anarchy.”

Then he listed for me a few of the things that had happened recently: The county sheriff had announced that he wouldn’t enforce the state’s pandemic restrictions on social gatherings and businesses. People who had never before attended county board meetings were accusing local officials of treason.

The county’s health officer, who had the unhappy job of imposing the state’s Covid rules on the citizens of Shasta County, was now receiving so many threats that Pontes had brought in a new threat-assessment team; he’d also ordered the bushes cut back away from her house, installed a security system and floodlights, and ordered police patrols of her neighborhood.

“She still doesn’t feel safe out there,” he said. “At all.”

via ZeroHedge News https://ift.tt/36Ediwj Tyler Durden

Chinese State Media Gloats That Trump Has “Paid The Price” & US Image Suffered Tyler Durden

Fri, 10/02/2020 – 09:10

Perhaps as expected, certain Chinese state media mouthpieces have appeared gleeful and gloating upon the unprecedented news that President Trump and the First Lady have tested positive for COVID-19.

The editor-in-chief of the Chinese Community Party run Global Times, Hu Xijin, said in first reaction that the president and Melania “have paid the price” and further that it is sure to have a “negative impact” on his image and that of the United States.

The editor of the Global Times, China’s hawkish state-owned tabloid, with a little schadenfreude this morning: https://t.co/WcbVpLZR9V

The Global Times editor has long trolled the US over its handling of the coronavirus pandemic while simultaneously touting China’s rapid and rigorous planned response which kept its numbers low compared to the population.

Yet the US administration has long attacked leaders in Beijing for early on downplaying it to the world, and not just that but outright lying about it when the seriousness of the novel virus and airborne spread became evident to Chinese health officials late last year into early 2020.

Thus what Trump repeatedly calls the “Chinese virus” (even in the debate) or in other instances “Wuhan virus” was entirely containable if Chinese communist authorities hadn’t deceived the world during the earliest weeks and months, according to the administration.

So likely, the White House would point out that indeed it’s Trump and much of the world that has “paid the price” for Beijing’s ineptitude and deceit in not locking down borders earlier than it did.

via ZeroHedge News https://ift.tt/36qMSxN Tyler Durden

Joe Biden Wishes President & First Lady A “Speedy Recovery” Tyler Durden

Fri, 10/02/2020 – 09:01

After Joe Biden and his top aides acquiesced to Democrats urging him to campaign more aggressively by deciding to restart in-person canvassing, President Trump – Biden’s top political rival – has tested positive. And in his first remarks on Trump’s infection, Biden and his wife Jill Biden, the former second lady,

Jill and I send our thoughts to President Trump and First Lady Melania Trump for a swift recovery. We will continue to pray for the health and safety of the president and his family.

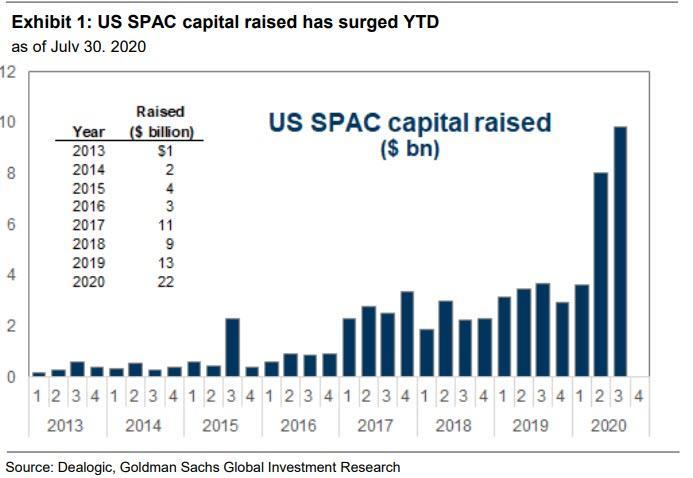

2020 has undoubtedly been the year of the special purpose acquisition company, or SPAC.

According to SPAC Insider, more than 115 initial public offerings for SPACs have brought in almost $44 billion in proceeds, which is more than the last five years combined.

Despite the popularity of SPACs so far this year, there hasn’t been an exchange-traded fund, or ETF, dedicated to SPAC investing. That all changed yesterday when the Defiance NextGen SPAC Derived ETF, which is the first ETF to track blank check companies, made its debut on the New York Stock Exchange yesterday under the ticker SPAK.

“Picking the winners of individual SPACs can be very difficult, however the ETF structure allows investors to access the most liquid SPAC IPOs in a diversified basket,” Defiance ETFs said. “SPAK allows both financial advisors and retail investors to participate in an IPO private equity style of investing, which until now was only available to large financial institutions.”

The ETF has 29 holdings which are rebalanced quarterly and has an expense ratio of 0.45%. An 80% weighting is given to IPO companies derived from SPACs while 20% is allocated to common stock of newly listed SPACs.

The ETF’s largest holding is DraftKings, which accounts for nearly 20% of the fund’s assets. The other stocks rounding out the top five holdings—which account for just over half of the ETF’s assets, are Clarivate Plc, Vertiv Holdings Co., Open Lending Corporation and Broadmark Realty Capital Inc.

Co-founder Joshua Harris of asset manager Apollo Global Management, which itself is looking to raise funds through an initial public offering for a new blank-check company, says SPACs are here to stay.

“The SPAC part of the IPO market is a part of the market that’s here to stay,” Harris said. “There’s a real need for quick, confidential capital and price certainty and for sponsorship in the markets. And most of the SPACs that have been done have been more emerging growth SPACs, less cash flow more growth. And what we see is the opportunity for sponsorship.”

With SPAC deals seemingly taking companies public on a daily basis as of late, time will tell if the launch of a dedicated SPAC ETF marked a sign of a top in the latest craze to hit Wall Street or a generational buying opportunity.

via ZeroHedge News https://ift.tt/3ilv4q5 Tyler Durden

2020 has undoubtedly been the year of the special purpose acquisition company, or SPAC.

According to SPAC Insider, more than 115 initial public offerings for SPACs have brought in almost $44 billion in proceeds, which is more than the last five years combined.

Despite the popularity of SPACs so far this year, there hasn’t been an exchange-traded fund, or ETF, dedicated to SPAC investing. That all changed yesterday when the Defiance NextGen SPAC Derived ETF, which is the first ETF to track blank check companies, made its debut on the New York Stock Exchange yesterday under the ticker SPAK.

“Picking the winners of individual SPACs can be very difficult, however the ETF structure allows investors to access the most liquid SPAC IPOs in a diversified basket,” Defiance ETFs said. “SPAK allows both financial advisors and retail investors to participate in an IPO private equity style of investing, which until now was only available to large financial institutions.”

The ETF has 29 holdings which are rebalanced quarterly and has an expense ratio of 0.45%. An 80% weighting is given to IPO companies derived from SPACs while 20% is allocated to common stock of newly listed SPACs.

The ETF’s largest holding is DraftKings, which accounts for nearly 20% of the fund’s assets. The other stocks rounding out the top five holdings—which account for just over half of the ETF’s assets, are Clarivate Plc, Vertiv Holdings Co., Open Lending Corporation and Broadmark Realty Capital Inc.

Co-founder Joshua Harris of asset manager Apollo Global Management, which itself is looking to raise funds through an initial public offering for a new blank-check company, says SPACs are here to stay.

“The SPAC part of the IPO market is a part of the market that’s here to stay,” Harris said. “There’s a real need for quick, confidential capital and price certainty and for sponsorship in the markets. And most of the SPACs that have been done have been more emerging growth SPACs, less cash flow more growth. And what we see is the opportunity for sponsorship.”

With SPAC deals seemingly taking companies public on a daily basis as of late, time will tell if the launch of a dedicated SPAC ETF marked a sign of a top in the latest craze to hit Wall Street or a generational buying opportunity.

via ZeroHedge News https://ift.tt/3ilv4q5 Tyler Durden

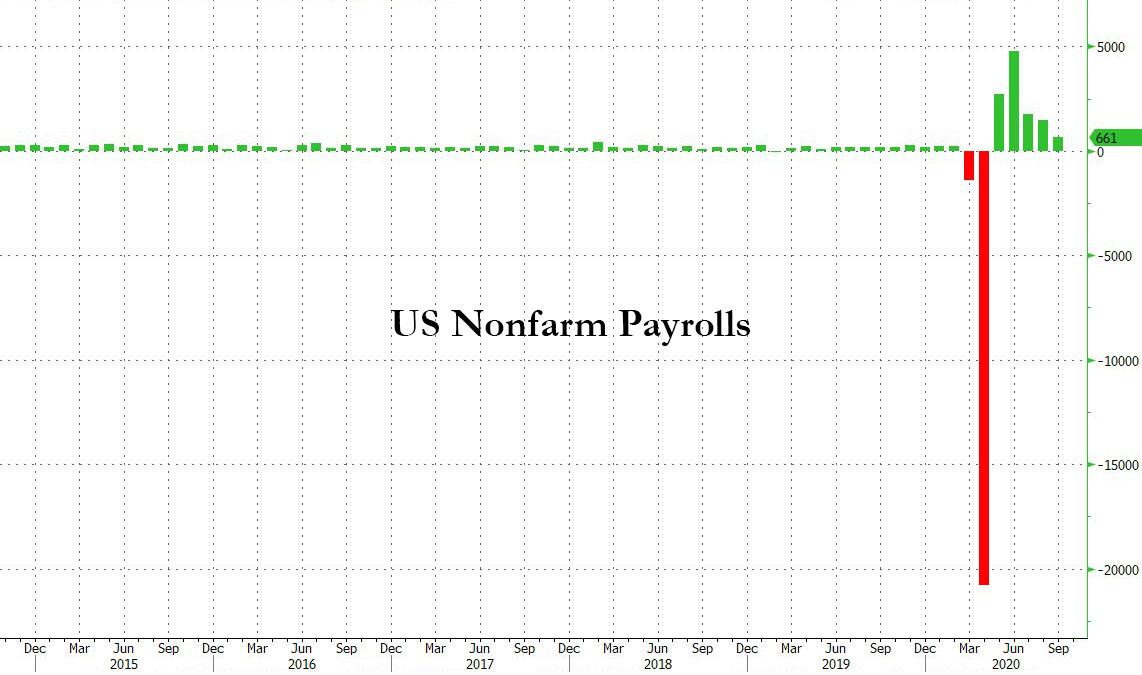

US Unemployment Rate Unexpectedly Plunges Below 8% As 661K Jobs Added Tyler Durden

Fri, 10/02/2020 – 08:36

In a repeat of last month when the monthly payrolls came in as expected but the unemployment rate dropped far more than expected, moments ago the BLS report that in September a total of 661K jobs were added, below the 868K expected, and less than half the 1.489MM in August…

… but offsetting this disappointment was the plunge in the unemployment rate which tumbled by a whopping 50bps from 8.4% to 7.9%, with rates for both blacks and Hispanic plunging as well.

Developing

via ZeroHedge News https://ift.tt/3n8DXXD Tyler Durden

Infections, Retentions, Creations, And Tensions. In That Order Tyler Durden

Fri, 10/02/2020 – 08:27

By Michael Every of Rabobank

Infections, retentions, creations, and tensions. In that order.

Here comes the first October surprise. US President Trump and the First Lady have both tested positive for Covid-19 after one his advisors, Hope Hicks, tested positive for Covid-19 and has also started showing symptoms. She travelled on Air Force One with him to Minnesota last week, and was additionally seen maskless near another presidential advisor. He tweeted:

“Tonight, @FLOTUS and I tested positive for COVID-19. We will begin our quarantine and recovery process immediately. We will get through this TOGETHER!”

To say this could potentially be a *big* deal is an understatement. Not much more can be said here at this stage, other than to do what one always does when **anyone** catches Covid – wish them a rapid and full recovery. However, one cannot help but note that Trump is very much in the age and weight category that place him in the higher risk groups, health-wise, and the market and public talk will now be of little else.

Up goes the USD as risk off? It seems that the kneejerk reaction was first to sell USD a little instead, at least until markets can work out exactly how this potentially plays out. Stock futures are certainly going down at time of writing, however. Risk is off there.

Obviously now eclipsed, but in the UK a Scottish Nationalist MP –a political party who have made a name for themselves as good stewards of public health– also started to show virus symptoms….and so decided to get on the train all the way to London; go to the House of Commons and mix with members of Parliament; and then, after a positive test result, to go all the way back to Scotland by train again. As we all know, PM Johnson has already had Covid-19 and ended up on a ventilator after boasting he had been shaking the hands of virus patients. Hopefully there won’t be any repeat for other MPs (or train passengers) now.

Apart from infections, the focus today is going to be very much on employment: both job retentions and job creations.

In the UK as one benchmark there was a report yesterday that 1 in 3 firms are preparing to fire workers imminently. Today we see the Telegraph saying unemployment is expected to reach as high as 4 million in a labour force of around 34 million. That is an entire army of people –actually the equivalent of the US and Russian and Chinese and Indian armies– all needing to be retrained as builders at once. Yet there are also reports the UK was recently looking into copying a Trump policy and building a wall around itself – on the water. This fantastical feat of engineering was apparently being considered as a way to keep the number of illegal asylum seekers arriving by boat over The Channel down. (“Welcome to day one of your builder training course everyone. Please pick up the scuba gear to your left and follow me into the pool.”) There were already some high fevers running in Westminster even before Covid re-entered the building. Does GBP float?

In the US, it will be the last monthly payrolls report before the election, if you can believe it. This will naturally be the figure that Trump will be still be able to Tweet about today, one hopes. The consensus is 875K, which would help close the gap of jobs lost to the Covid shutdown. Risks may be slightly the upside based on the ADP report this week. However, initial claims yesterday made clear yet again that we are far from back to normal. Will it move markets? Maybe not that much given the focus is now more on infection and stimulus.

Indeed, we are also not likely to get back to normal if we don’t see less tension in Washington. Markets have gyrated recently on headlines saying Mnuchin and Pelosi were close, then far, then close to a compromise stimulus deal. Well, the House Democrats just passed their own USD2.2 trillion package, which will of course be rejected by the Republican-held US Senate, so the same old games continue as everyone from the NFIB small business survey to the FOMC cries out for more stimulus, and now. The public reaction at some point may well start to echo that after the recent presidential debate: everyone loses in the most important respects even if a technical win can be claimed by both sides in others. Up went the USD – until that Trump news, which again potentially changes everything.

Meanwhile, there will be tensions in DC on another front. That is on the back of a claim from the head of a House antitrust panel that certain household-name Big Tech firms –who basically are the US economy as far as some markets are concerned– abuse their power as gatekeepers of the internet. There is apparently going to be a recommendation that legislation be passed to rein these giants in. You thought Big Tech was already involved in this election, even if they are not a topic of conversation? Well now they are trillions-of-USD deep involved.

And on another kind of tensions, the EU actually managed to agree something on joint foreign policy, which could be a headline in itself given how rare this achievement is. Targeted sanctions are now going to be put in place on Belarus, and apparently part of the quid-pro-quo of that is that the door remains open to sanctions on Turkey too if it continues to ruffle the feathers of Greece and Cyprus – which will not soothe tensions with Ankara.

Anyway, everything now takes a backseat to the latest incredible twist in this US election campaign.

via ZeroHedge News https://ift.tt/2Gs7kmX Tyler Durden

Mike Pence, Wife Test Negative For COVID-19 Tyler Durden

Fri, 10/02/2020 – 08:01

In what will undoubtedly be taken as good news by the market, Vice President Mike Pence’s office just confirmed that both the VP and the second lady, Karen Pence have tested negative for COVID-19.

Of course, there have been instances where people who have contracted the virus don’t test positive for several days, and both will likely continue to be tested in the coming days, since the incubation period is up to 14 days, with a median of about 4 to 5 days.

The White House just added that it will keep staffers for the president and the vice president separate in the coming days.

via ZeroHedge News https://ift.tt/2GrduUy Tyler Durden

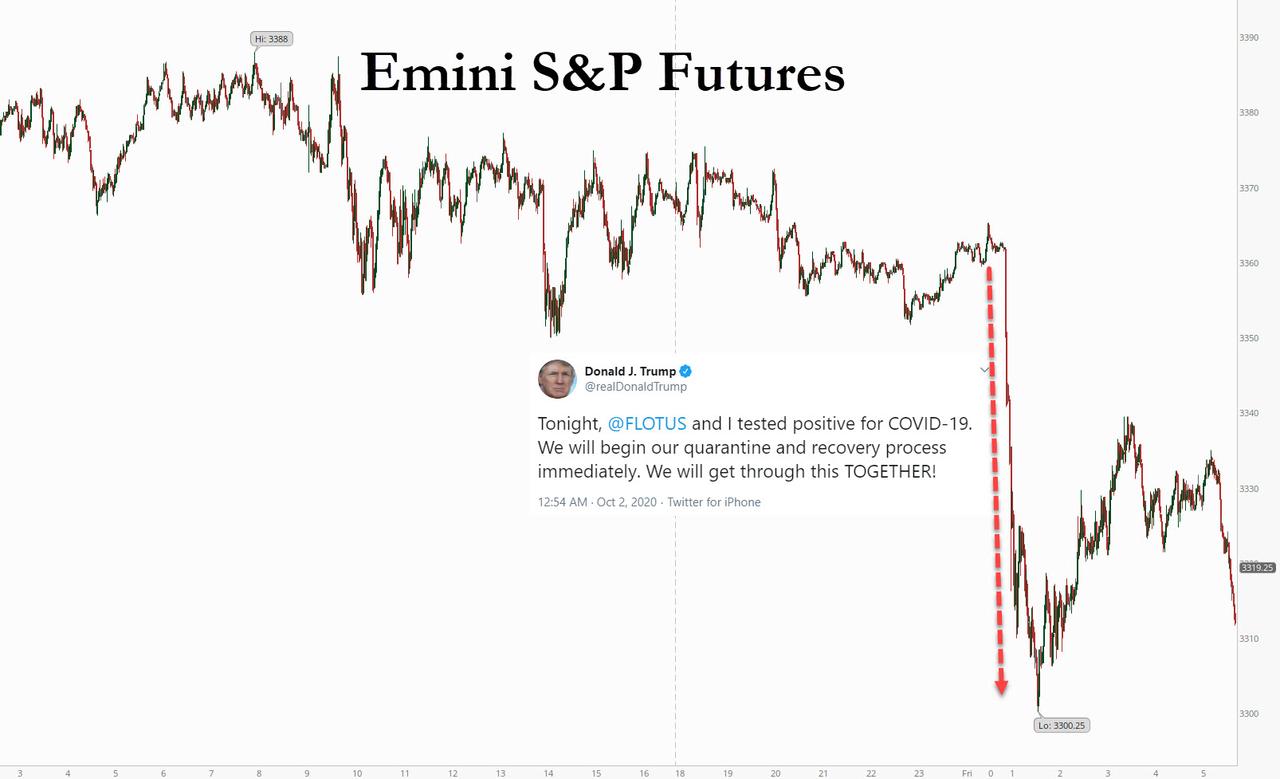

“October Shock”: Markets Tumble After Trump Tests Positive For Covid Tyler Durden

Fri, 10/02/2020 – 07:51

After going to bed expecting today’s jobs report to be the highlight of the day, shocked traders woke up this morning to the real October surprise: news tweeted by Donald Trump himself at 12:54am ET that he and the first lady had tested positive for covid after Hope Hicks, a senior advisor who recently traveled with the president, tested positive.

Tonight, @FLOTUS and I tested positive for COVID-19. We will begin our quarantine and recovery process immediately. We will get through this TOGETHER!

The result was an immediate flush in US equity futures and global markets which saw the Emini tumble to exactly 3,300 before rebounding modestly into the European open.

AS they sold risk assets, investors rush to safe assets such as gold, U.S. Treasuries and the Japanese yen. European shares also opened sharply lower, although they recovered some losses in early London trading after the initial overnight move. The STOXX 600 was down 0.6% as of 730am ET. The MSCI world equity index was down 0.2%.

“We’re just a month to the election so this news does throw the election campaign into a disarray for the Republican Party,” said Jingyi Pan, market strategist at IG Asia. “Even though Joe Biden is seen as the friendlier choice for Asia and a Trump absence could in some way or another keep that status quo of a Biden lead, generally, a contested election would generate uncertainties across the world and would not bode well for Asia equities as well.”

After Trump said he had coronavirus, online gambling site Betfair suspended betting on the outcome of the U.S. election. Betfair’s odds had previously shown Democratic challenger Joe Biden’s probability of winning at 60% on Wednesday after the first U.S. presidential debate.

Even before news of Trump’s infection, markets had been more bearish after Washington failed to reach an agreement on a fiscal stimulus package to help the U.S. economy recover from the impact of coronavirus. Late on Thursday, the House passed the Democratic stimulus plan which Republicans oppose, after Speaker Pelosi announce no bipartisan deal was achieved last night

The question now is what happens next as Trump’s exposure could cause a new wave of market volatility with investors braced for the presidential election in November. How long the risk-averse moves will last depends on the extent of the infection within the White House, said Francois Savary, chief investment officer at Swiss wealth manager Prime Partners.

“We may have to wait until the end of the weekend for more clarity on the situation,” he said. “The reaction has been a bit excessive with U.S. stock futures. It doesn’t mean the U.S. administration is not able to function. It will weigh on the market today and early next week but will not induce a long-lasting correction if the infection is contained to Trump,” he added.

Following the news, the U.S. dollar index rose and the safe-haven yen made its biggest jump in more than a month, reaching 104.95. Versus a basked of currencies, the dollar was up 0.1% on the day at 93.820. The Australian dollar, which serves as a liquid proxy for risk, was down 0.5%. The euro was down 0.3% against the dollar, at $1.1721.

In rates, Treasuries remained higher led by long end after fading from session lows. Yields are still inside Wednesday’s ranges ahead of September jobs report at 8:30am ET. Yields were lower by less than 2bp at long end of the curve, with 2s10s, 5s30s spreads flatter less than 1bp; 10-year is down 1.6bp at 0.661%, outperforming little-changed bunds and gilts, after shedding as much as 2.6bp. Yields rebounded from session lows as stock futures pared declines; S&P E-minis have trimmed a 2% drop on Trump health news to about 1.4%. Germany’s benchmark 10-year bond was down around 2 basis points at -0.545%.

In commodities, oil fell, with Brent down 3.3% at $39.57 a barrel to the lowest level since June, having fallen overnight and stabilized somewhat as European markets opened. Gold rose, up 0.1% at $1,906.26 per ounce. “Depending on how this situation evolves over the weekend, notably if more members of the U.S. government’s senior leadership are diagnosed positive, gold could be set for an extended rally,” said Jeffrey Halley, a senior market analyst at OANDA.

Elsewhere, in geopolitics, EU leaders reached an agreement regarding Belarus and Turkey in which they will impose sanctions on Belarus for violence and its election, although President Lukashenko was not included in the sanctions, while it warned that Turkey could face sanctions if it continues with its gas exploration in Cypriot waters. European Council President Michel said the next 2 weeks will be crucial with Turkey and the summit deal opened a path for dialogue but also showed firmness, while they will return to the Turkey question at the December summit. Furthermore, German Chancellor Merkel said EU leaders agreed they want constructive relations with Turkey and hope for negotiating dynamic with the country

Looking ahead, the last round of monthly U.S. unemployment data before the elections is due at 0830 (see preview here), although analysts say this has been relegated to secondary importance. We also get Factory Orders, Uni. of Michigan (F), Fed’s Harker, European Council Special Meeting. Trump’s illness prompted the White House to cancel political events on Friday, including a rally planned outside Orlando, Florida. Campaign and fundraising trips planned for the coming days — including visits to key battlegrounds including Wisconsin, Pennsylvania and Nevada — are expected to be scrapped.

Market Snapshot

S&P 500 futures down 1.2% to 3,327.75

STOXX Europe 600 down 0.4% to 360.49

MXAP down 0.3% to 169.91

MXAPJ down 0.2% to 558.19

Nikkei down 0.7% to 23,029.90

Topix down 1% to 1,609.22

Hang Seng Index up 0.8% to 23,459.05

Shanghai Composite down 0.2% to 3,218.05

Sensex up 1.7% to 38,697.05

Australia S&P/ASX 200 down 1.4% to 5,791.50

Kospi up 0.9% to 2,327.89

Brent Futures down 3% to $39.71/bbl

Gold spot up 0.2% to $1,909.27

U.S. Dollar Index up 0.06% to 93.77

German 10Y yield fell 0.5 bps to -0.541%

Euro down 0.2% to $1.1721

Brent Futures down 3% to $39.71/bbl

Italian 10Y yield fell 4.4 bps to 0.618%

Spanish 10Y yield fell 0.2 bps to 0.23%

Top Overnight News

Trump’s illness prompted the White House to cancel political events on Friday, including a rally planned outside Orlando, Florida. Campaign and fundraising trips planned for the coming days — including visits to key battlegrounds including Wisconsin, Pennsylvania and Nevada — are expected to be scrapped.

Four months of European Commission consultations with insurance companies, academics and others ends Friday, aimed at agreeing by next year what really counts as “green” in projects funded by such debt

A quick look across global markets courtesy of NewsSquawk

Asian equity markets traded lower and the E-mini S&P is showing substantial losses after US President Trump tested positive for COVID-19. ASX 200 (-1.4%) reversed yesterday’s strength in which energy and mining-related sectors led the downside following weakness across the commodities complex and as a lacklustre financials sector also contributed to the losses for the index. Nikkei 225 (-0.7 %) was initially buoyed at the open as it played catch-up on return from yesterday’s surprise trading halt in Tokyo due to hardware issues, which Japan’s FSA is reportedly to consider a punishment for. This subsequently weighed on Japan Exchange Group shares and Fujitsu was also pressured given that the Co. is the hardware provider for the market operator, while most the gains in the benchmark index were gradually pared alongside a broad tentative tone and with a lack of participants due to closures in China, Hong Kong, Taiwan, South Korea and India. Finally, 10yr JGBs were rangebound amid the mixed risk tone and with price action stuck near the 152.00 focal point, while a tepid Rinban announcement by the BoJ which were present in the market for JPY 570bln, also ensured the lackadaisical price action for government bonds.

Top Asian News

Malaysia Airlines in Urgent Restructuring as Pandemic Worsens

Australia’s Central Bank Is ‘Dysfunctional,’ Ex- Researcher Says

European cash indices briefly trimmed earlier losses (Euro stoxx 50 -0.9%) which were triggered by US President Trump announcing his positive COVID-19 test, in turn sparking risk aversion across markets. Since then, cash and futures have been attempting to lift off lows, with some Brexit optimism potentially providing support as the news of a videoconference between the European Commission President and the UK PM was received well by participants, alongside the Pound, whilst the two sides will continue with negotiations in the run up to the EU Summit mid-month. That being said, EU diplomats are still downbeat over a Brexit breakthrough whilst a UK minister highlighted that very significant issues need to be resolved. Nonetheless, the attempted recovery was fleeting, Europe trades mostly lower with the exception of Spanish and Austrian stocks, with the former supported by ACS (+18%) after Vinci (+2.6%) submitted a bid to acquire the Co’s industrial division. Sectors meanwhile opened lower across the board, but thereafter gained some composure; albeit, Energy remains the laggard whilst Telecoms tops the charts with follow-through from yesterday’s French 5G auction – which raised EUR 2.8bln, as Iliad (+4.0%), Orange (+2%) and Bouygues (+1.3%) prop up the sector. The sectoral breakdown paints a similar picture with Travel & Leisure still under pressure amid the implications of the COVID-19 resurgence on the sector. In terms of individual movers, Lagardere (-0.2%) trades with modest losses despite Vivendi (+0.6%) upping its shareholding of the Co. to 26.7% from 21.2%. Ryanair (-2.2%) meanwhile sees losses amid source reports that the Co. is mulling purchasing Boeing 737Max aircrafts for ~EUR 16bln, whilst traffic September traffic numbers fell -64% YY and the Co. was operating at around 53% of normal September schedule.

Top European News

ECB Takes Major Step Toward Introducing a Digital Euro

ACS in Talks to Sell Industrial Unit to Vinci for $6.1 Billion

German Regulator Limits Staff Trading After Wirecard Scandal

BlackRock Sees Board Governance at VW Going in Reverse

In FX, the Yen is in demand on safe-haven grounds after an initial Greenback rally on news of US President Trump catching the coronavirus saw the DXY knee-jerk just over 94.000, with Usd/Jpy subsequently retreating from around 105.66 to test bids/support below 105.00 and the index hovering just above a 93.709 low. Conversely, the Aussie has borne the brunt of risk aversion, as Aud/Usd reverses from the high 0.7100 region through 0.7150, with little consolation from retail sales not dropping quite as much as expected in August. Ahead, NFP would ordinarily command headline status on the first Friday of a new month, but the data now looks somewhat inconsequential in light of the aforementioned events in Washington.

GBP – More wild swings for Sterling, partly in line with broad sentiment, but again due to Brexit developments in the main and independently of other external or domestic factors. Cable is firmly back over 1.2900 and Eur/Gbp circa 0.9060 compared to 0.9100+ at one stage following reports that UK PM Johnson and European Commission President von der Leyen will hold a video call on Saturday to assess the situation on trade talks after this week’s formal round of discussions, and the former will push for the 2 sides to enter the tunnel stage of negotiations even though EU chief of Brexit matters, Barnier, is unsure the time is right.

CAD/NZD/EUR/CHF – All still softer against their US counterpart, with the Loonie pivoting 1.3300, Kiwi midway between 0.6654-16 parameters, Euro holding above 1.1700 within a 1.1697-1.1750 range and Franc straddling 0.9200. Aside from keeping a White House vigil in the run up to monthly US jobs data, Eur/Usd looks well flanked by decent option expiries given 1.3 bn at 1.1700, 2 bn at 1.1750 and 1.7 bn at 1.1800, if recent peaks in the headline pair are breached. For the record, very little reaction to softer than forecast prelim Eurozone inflation as the individual national reports indicated a downside skew to consensus.

SCANDI/EM – The Norwegian Crown may be deriving some traction from a lower than anticipated September jobless rate to compensate for weak oil prices and the impending strike action, but Eur/Nok is not down as much in percentage terms as Eur/Sek, albeit back under the psychological 11.0000 level in similar vein to the latter that has crossed 10.50000 to the downside. Elsewhere, EM currencies are broadly softer vs the Usd, but especially the Rub amidst ongoing diplomatic and geopolitical tensions, on top of Brent losing grip of the Usd 40/brl handle

In commodities, WTI and Brent futures remain pressured, albeit volatility has somewhat cooled down in recent trade, with the initial downside sparked by the risk aversion experienced following President Trump’s positive test. Newsflow which sent WTI Nov and Brent Dec to lows of USD 37.22/bbl (vs. high 38.65/bbl) and USD 39.40/bbl respectively (vs. high 40.77/bbl). Again, crude-specific news flow has been light and we are awaiting the NFP data for some impetus; alongside any further developments around Trump’s COVID-19 diagnosis. Looking ahead, next week seems fairly quiet in terms of crude-specific events, although the OPEC World Oil Outlook on the 8th could garner some attention with regards to its medium-term forecasts, but there is a possibly the release will get sideline if the report is consistent with the July release – as was the case last year. Spot gold meanwhile was bid early-doors on safe-haven inflow, which took the yellow metal to a high of USD 1917/oz, whilst spot silver briefly topped USD 24/oz before both precious metals waned off highs. In terms of base metals, LME copper fell to the lowest in seven weeks due to USD upside and sentiment effect from US President Trump. Meanwhile, aluminium prices fell amid talks of US aluminium exemptions for producers in UAE and Bahrain.

US Event Calendar

8:30am: Change in Nonfarm Payrolls, est. 875,000, prior 1.37m; Change in Private Payrolls, est. 875,000, prior 1.03m

Unemployment Rate, est. 8.2%, prior 8.4%

Average Hourly Earnings MoM, est. 0.2%, prior 0.4%; Average Hourly Earnings YoY, est. 4.8%, prior 4.7%

Average Weekly Hours All Employees, est. 34.6, prior 34.6

Labor Force Participation Rate, est. 61.9%, prior 61.7%; Underemployment Rate, prior 14.2%

10am: U. of Mich. Sentiment, est. 79, prior 78.9; Current Conditions, prior 87.5; Expectations, prior 73.3

10am: Factory Orders, est. 0.9%, prior 6.4%; Factory Orders Ex Trans, est. 1.1%, prior 2.1%

10am: Durable Goods Orders, est. 0.4%, prior 0.4%; Durables Ex Transportation, est. 0.4%, prior 0.4%

10am: Cap Goods Orders Nondef Ex Air, est. 1.7%, prior 1.8%; Cap Goods Ship Nondef Ex Air, prior 1.5%

DB’s Jim Reid concludes the overnight wrap

I’m not sure if it’s just me but I seem to have fought off more “Daddy longlegs” in the last few weeks than I can remember in my entire life. It could be local to me but they are everywhere. The twins are very amusing as they have only just discovered Daddy longlegs and think they are the funniest thing in the world. They also ask where Mummy shortlegs are? They then laugh at their own jokes. I’ve taught them well.

The US political spider’s web continued to dominate the narrative yesterday. Notwithstanding this, markets got off to a steady but solid start to Q4. By the close, the S&P 500 was up +0.53% and at a two-week high, though the index fell back somewhat from its opening gains following a report that Speaker Pelosi had told her deputies that she was sceptical a stimulus agreement would be reached. Markets seem to be caught between the crossfire of volatile stimulus news and a steady increase in the probability of a Biden victory in recent days according to respected modellers. Indeed FiveThirtyEight’s model ticked up to an 80% probability of a Biden win for the first time yesterday. Although Trump has traditionally been seen as good for stocks, the uncertainty of a close election, and a possible contested one at that, has been a dampener of late. If markets got more and more convinced of a Democrat clean sweep then this a) reduces uncertainty and b) potentially paves the way for a bigger fiscal stimulus after January. So Biden positive news can outweigh short-term negative news on stimulus.

Indeed, US fiscal stimulus discussions again dominated headlines yesterday. Pelosi said that the two parties are still a ways apart on the total size of stimulus and the means in which it is apportioned. It is likely that the latter is the larger sticking point as the White House has offered $1.6 trillion, well above $1 trillion figures many Senate Republicans were already uncomfortable with. The Democrats’ most recent offer of $2.2 trillion – down from their original $3.5 trillion bill – passed late last night although Senate Republicans are expected to reject it. Pelosi said that she would continue talks with Mnuchin while the passed bill will act as public account for what here caucus was pushing for. The S&P 500 dropped half a per cent yesterday when the intention to vote was announced as it signaled the talks had likely not closed the gap. Lawmakers in both chambers are expected to recess ahead of the elections next week but can be called back to take part in a vote if anything were to get done.

Staying on the US, the main story developing overnight is that President Trump is to quarantine after his aide Hope Hicks tested positive for the coronavirus. The President tweeted that “The First Lady and I are waiting for our test results. In the meantime, we will begin our quarantine process!” In terms of the market reaction, S&P 500 futures fell after the news was released, and are currently down -0.29%, while the dollar index has moved higher and is up +0.22%. Meanwhile in Asia, amidst a number of public holidays, the Nikkei (+0.25%), is trading slightly higher, in spite of Japan’s unemployment rate in August rising to a 3-year high of 3.0%.

In advance of that, equity markets generally moved higher on both sides of the Atlantic yesterday amidst the stimulus discussions and increased probabilities of a more definitive election outcome, particularly large cap tech stocks once again as the NASDAQ gained +1.42%, while the S&P 500 was ‘only’ up +0.53% with the STOXX 600 up +0.20%. The biggest drivers of the S&P and the NASDAQ were those mega-cap tech stocks such as Netflix (+5.50%) and Amazon (+2.30%). On the gap between US and European equity markets, our CoTD yesterday showed that although the gap has been widening over the last decade, if you strip out just 10 mega-cap growth stocks from the S&P 500 then the Stoxx 600 has only been slightly behind the “S&P 490” since the end of 2014. See the evidence here.

Back to markets, andthe energy sector lagged behind yesterday as a result of the major declines in oil prices. Both Brent crude (-3.24%) and WTI (-3.73%) suffered significant losses thanks to concerns about oversupply. Copper, another industrial commodity, had its worst performance (-5.51%) since March as poor global demand weighed on the metal. Precious metals on the other hand rose with gold rising +1.07% and silver gaining +2.40%. Sovereign bonds rallied for the most part as well, with yields on 10yr treasuries (-0.6bps) and bunds (-1.4bps) both falling. Italian debt was the real outperformer though, with 10yr yields down -4.5bps and at a 1-year low, while the country’s 30-year yield fell a further -3.2bps to an all-time low. The dollar fell (-0.19%) for the fifth time in the last six sessions, though Wednesday’s was nearly unchanged.

In terms of the coronavirus, there was further negative news from Western Europe, as Italy reported another 2,548 cases, which was the country’s highest daily total since April 24 albeit with higher testing now. This has prompted Prime Minister Conte to seek an extension of his emergency powers until the end of January. Meanwhile in the UK, another 6,914 cases were reported, which sent the 7-day average up to 6,260. However we should note that the 7-day rolling average as seen in the table below is “only” slightly higher than it was a week ago. A similar story for most of the second wave candidates. Regardless officials noted that London may be at a “tipping point” while further restrictions were announced for parts of northern England, including Liverpool, where it will be illegal to meet with other households indoors. More restrictions may be coming to France as well where the Health Minister said they “may have no choice” but to close bars and restaurants again in Paris, saying the city is on “maximum alert”. And over in the US, New York reported the most new virus cases since May. New York City’s positivity rate on first time tests continued to climb, but remained below the 3% threshold that would close schools. Elsewhere in the US, two Wisconsin mayors have asked President Trump to cancel large rallies in the state which currently has one of the highest daily cases per capita in the US.

Today, attention will turn to the US jobs report, which also has added political significance as the last jobs report before Election Day on November 3rd. In terms of what to expect, our US economists think that nonfarm payrolls will grow by another +800k in September (consensus +875k), which should be enough to lower the unemployment rate to 8.2% from 8.4%. Remember however, that even if this were realised, nonfarm payrolls would still be over 10m beneath their peak back in February, so there’s still a long way to go before we get back to pre-Covid levels of employment.

Ahead of that later, the weekly initial jobless claims data for the week through September 26th showed a reduction to 837k, the lowest since the pandemic began. The continuing claims number for the week through September 19th also fell to a post-pandemic low of 11.767m, and the insured unemployment rate fell to 8.1%. The other main data highlight came from the manufacturing PMIs, though these were fairly unexciting, and saw little movement compared to the flash readings. The Euro Area PMI came in at 53.7, exactly in line with the flash reading, the German number was revised down slightly to 56.4 (vs. flash 56.6), and the French number was revised up slightly to 51.2 (vs. flash 50.9). Over in the US, the ISM manufacturing index came in at 55.4 (vs. 56.5 expected), which was a modest pull back from its 56.0 reading in August.

Elsewhere, it was a volatile day for the pound sterling as a raft of Brexit news came through that saw sentiment switch dramatically as the day went on. In the morning, the European Commission President Ursula von der Leyen announced the beginning of infringement proceedings against the UK on account of the parts of the UK’s internal market bill that violate the Withdrawal Agreement. The EU had previously given the UK until the end of September to remove the relevant provisions from the bill, but with that deadline passing they announced they would be sending a “letter of formal notice” to the UK, which the UK has until the end of October to respond to. Sterling fell to an intraday low of -0.77% in response, though in reality, this is arguably somewhat second order to the ongoing trade negotiations, particularly with the bill having not yet become law and facing serious obstacles in the UK House of Lords. Notably the end-month deadline for the UK to respond is also after Prime Minister Johnson’s self-imposed deadline of October 15 to reach a free-trade deal, so by that point we could be in a very different world depending on how things progress.

Not long after midday however, a tweet from the well-connected FT’s Sebastian Payne sent sterling up to an intraday high of +0.45%, after he said that “Officials with knowledge of the talks say a landing zone on state aid has been identified”. This optimism didn’t last for long though, with sterling falling back again as another headline came through saying that the reports suggesting the two sides were entering the final stage were too optimistic, with differences still remaining on the long-standing sticking points of state aid and fisheries. The 9th round of the negotiations wraps up today in Brussels, with a meeting between the two chief negotiators, so worth keeping an eye out to see if we get any statements from either side of any progress that might have taken place.

To the day ahead now, and as mentioned the US jobs report later is likely to be the main highlight. Otherwise, we’ll get the flash estimate of Euro Area CPI in September, and from the US there’s also the final University of Michigan sentiment reading for September and factory orders for August. From central banks, we’ll hear from ECB Vice President de Guindos, along with the ECB’s Holzmann and Hernandez de Cos, while from the Fed we’ll hear from Harker and Kashkari.

via ZeroHedge News https://ift.tt/3inL37g Tyler Durden