Democratic Mayor Sylvester Turner has signed off on a new study that will see city employees visit randomly selected homes in Houston to collect blood samples for COVID-19 antibody testing.

The study is being conducted by the Houston Health Department in collaboration with the Centers for Disease Control (CDC). Household members will be asked to answer a survey and give a blood sample. For some households, all members of the household will be asked to participate.

Authorities say the tests are necessary to develop a deeper insight into how COVID-19 spreads through the community and how many people were previously infected with the virus.

The Mayor said the program would be voluntary, but urged citizens to take part.

“If we knock on your door, I strongly encourage you and your loved ones to participate in this important survey,”said Turner.

“The data you provide by participating will help inform strategies to mitigate the effects of COVID-19.”

In some other countries, such as New Zealand, people who refuse to take a COVID-19 test have been forcibly removed to quarantine facilities by health authorities.

In a previous interview, Turner had suggested that people who refused to take a coronavirus test were “irresponsible.”

Last month Turner also announced that police will begin issuing citations against people not wearing masks, hitting them with a fine of $250 dollars.

* * *

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. I need you to sign up for my free newsletter here. Also, I urgently need your financial support here.

via ZeroHedge News https://ift.tt/33Dfild Tyler Durden

Amazon Takes On Malls With Virtual “Luxury Stores” Tyler Durden

Wed, 09/16/2020 – 13:30

During the early days of the coronavirus outbreak, department stores tumbled into bankruptcy – like dominoes. After Fitch downgraded 9 retailers in one day, including Macy’s, Nordstrom and JC Penney, department stores filed for bankruptcy protection, or scrambled to secure birdge financing, delaying the inevitable liquidation reckoning.

Now, Amazon has just handed investors betting against both American malls and the department stores that were once reliable drivers of foot traffic a huge favor: the company on Tuesday unveiled a new virtual “luxury brand-focused” store along with a new brand partnership with fashion house Oscar de la Renta.

The new subsection of its mobile app called “Luxury Stores” will begin with items from designer Oscar de la Renta, known for the brand’s work on couture award-season dresses. The app will include advanced features like a 360-degree viewing option for “virtual” try-ons.

Only certain Amazon Prime members will be allowed to shop in the Luxury store – at least initially. Invites will be extended to more customers over time, the company said.

That’s ironic: Amazon, which grew into a juggernaut with a focus on ubiquity, is now giving exclusivity a try.

KeyBanc analyst Edward Yruma said he was surprised by the partnership with Oscar de la Renta; he would have expected Amazon to partner with a bigger brand, or a “collection” of smaller brands. On CNBC, after the news hit, there was speculation about Tiffany selling out to Amazon.

“Oscar’s apparel presence in the traditional wholesale channel has waned over recent years,” with the brand “increasingly reliant on its jewelry and fragrance offering,” Yruma said.

But there’s little doubt that Amazon will find opportunity in the luxury goods space, as the decline of department stores has left “significant share in luxury apparel retailing” up for grabs.

Pretty soon, Jeff Bezos is going find new ways to extract value from $425 mud jeans.

via ZeroHedge News https://ift.tt/3kmkrVt Tyler Durden

An official who worked on special counsel Robert Mueller’s Russia investigation wrote in a recently released email that he or she was in possession of an iPhone belonging to Lisa Page three days after the former FBI lawyer’s last day on the job and at a time when the device was thought to have been lost.

Lisa Page, former legal counsel to former FBI Director Andrew McCabe, arrives on Capitol Hill in Washington on July 13, 2018. (Andrew Caballero-Reynolds/AFP via Getty Images)

The special counsel’s office (SCO) and the Justice Department previously claimed to have no documents to show who handled Page’s iPhone after she turned it in on July 14, 2017, or who improperly wiped it two weeks later, before it could be checked for records, in violation of SCO policy.

But documents released by the Department of Justice (DOJ) on Sept. 11 tell a different story, with three officials certifying that Page turned over her phone and one claiming to have been in possession of it.

“I have her phone and laptop,” an administrative officer with the initials LFW wrote in a July 17, 2017, email to Christopher Greer, an assistant director at the DOJ Office of the Chief Information Officer (OCIO).

Beth McGarry, the executive officer at the special counsel’s office, told Greer in an email sent earlier in the day that Page “returned her mobile phone and laptop.”

On the same day, a property custodian officer, whose name is redacted in the documents, signed a form on which Page certified that she turned in her phone and the officer certified that “all government property has been returned or otherwise properly accounted for.”

The July 17 timing of the two statements and the signature is significant. The DOJ Office of Inspector General (OIG) previously concluded that there were no records of who had the phone after July 14.

The records about Page’s phone are part of a DOJ disclosure that revealed that members of the Mueller team improperly wiped at least 22 iPhones before they could be checked for records.

Then-FBI official Peter Strzok confers with his legal counsel before a joint committee hearing on Capitol Hill in Washington on July 12, 2018. (Alex Edelman/Getty Images)

“These irregularities with the phones of Mueller investigators are either sloppiness or the deliberate destruction of evidence—and it’s probably not sloppiness,” Rep. Devin Nunes (R-Calif.), ranking member of the House Select Committee on Intelligence, told The Epoch Times in an email.

On July 14, Page’s last day at the SCO, McGarry met Page to fill out her exit clearance form. Page checked a box on the form to certify that she “surrendered all government-owned property, including … cellular telephones.” McGarry signed the same form but later told the OIG that “that she did not physically receive Page’s issued iPhone.”

Page told the inspector general that she “had left her assigned cell phone and laptop on a bookshelf at the office on her final day there.”

McGarry left the special counsel’s office for the private sector in March 2019, according to her LinkedIn profile.

“The DOJ OIG investigated the circumstances of the mobile phone issued to Lisa Page by the Special Counsel’s Office,” McGarry told The Epoch Times in an email, referring to the December 2018 OIG report. She didn’t immediately respond to a follow-up query about how to reconcile differences between the findings of the report and the new documents.

The OIG, which interviewed the records officer, McGarry, Page, and LFW for the report, told The Epoch Times that the new documents aren’t at odds with its findings.

“We stand by the information in our text message report about Page turning in the device on July 14,” Stephanie Logan, a senior public affairs specialist at the OIG, wrote in an email to The Epoch Times.

The report concluded that neither Mueller’s office nor the DOJ “had records reflecting who handled the device or who reset it after Page turned in her iPhone on July 14, 2017.”

Page’s phone notably never made it into the hands of the special counsel’s records officer, who told the OIG that she never received the phone to examine it for any government records that would need to be retained.

“Phone not found,” the records officer noted in a log she kept about the records on the phones assigned to the special counsel’s office staff.

The DOJ found the device more than a year later and turned it over to the OIG, which determined that all of the data was deleted from the device on July 31, 2017.

Wiped iPhones

The records officer’s log shows that Page’s iPhone wasn’t the only device to elude an examination for government records. A total of at least 22 iPhones with unique asset tags used by the Mueller team were wiped before the records officer could review the contents, according to an Epoch Times review of four inventory logs and various forms released on Sept. 11.

The Mueller team offered a number of excuses for the deletions. Two people claimed the phones wiped themselves. Others said they erased all the data by accident or had to do so because they forgot their passwords. Andrew Weissmann, a prosecutor, wiped his iPhone twice.

Mueller’s team used a total of 92 iPhones, according to the documents. Four of the phones appear in the inventory logs, but not on the records officer’s log, suggesting they were either recorded without their unique asset tag or evaded the officer entirely. One of the four phones belonged to deputy special counsel Aaron Zebley. Another belonged to Zainab Ahmad, a special counsel attorney.

One phone was partially wiped. Four phones were improperly handed over to the OCIOand wiped before the records officer’s review. As many as seven phones with no asset tags noted by the records officer were either reassigned or wiped before the officer could assess the device for records.

Former special counsel Robert Mueller on Capitol Hill in Washington on July 24, 2019. (Alex Wong/Getty Images)

The pattern of questionable deletions has drawn the attention of lawmakers. Sens. Chuck Grassley (R-Iowa) and Ron Johnson (R-Wis.), the chairmen of the finance and oversight committees, respectively, sent a letter to the DOJ and the FBI last week asking for more information about what happened with the phones.

“It appears that Special Counsel Mueller’s team may have deleted federal records that could be key to better understanding their decision-making process as they pursued their investigation and wrote their report,” Grassley wrote. “Indeed, many officials apparently deleted the records after the DOJ Inspector General began his inquiry into how the Department mishandled Crossfire Hurricane.”

Crossfire Hurricane is the FBI codename for the investigation of the 2016 Trump campaign; Mueller took over the probe in May 2017.

Five months after Page left the special counsel’s office, the DOJ authorized a leak of 375 text messages between Page and Strzok, triggering a media firestorm over what the pair discussed. The initial and the subsequent releases of the texts showed that they expressed hatred for Trump and had a clear preference for his rival, former Secretary of State Hillary Clinton. Strzok told Page that “we’ll stop” Trump from becoming president, discussed an “insurance policy” in case Trump won the election, and mused about impeachment around the time he joined the Mueller team.

Page’s attorneys didn’t immediately respond to a request by The Epoch Times for comment.

The OIG discovered the biased Page-Strzok texts during an inquiry into the handling of the FBI’s investigation of the Trump campaign. After the inspector general informed Mueller of the texts in late July, Mueller removed Strzok from the Russia investigation. Former FBI Deputy Director Andrew McCabe told lawmakers that he learned of the text messages on July 27 and made the decision to remove Strzok the same day. Someone wiped Page’s phone four days later.

Strzok and Page played key roles in the FBI’s investigations of both the Trump campaign and Clinton’s use of an unauthorized email server. The OIG concluded that their bias cast a cloud over the email probe but didn’t ultimately influence the outcome of the investigation.

The OIG began looking for the phones belonging to Page and Strzok after being informed of a six-month gap in the text messages it had recovered. The inspector general received the pair’s four FBI Samsung phones in late January 2018.

On Jan. 26, 2018, Greer reached out to LFW to ask where Page’s SCO iPhone was, because the OIG wanted to speak to the official about the device.

“Yes. I know it is missing. We discovered that first,” LFW wrote back.

The DOJ tracked down the phone eight months later, in early September 2018 and handed it over to the OIG. The records officer later contacted the inspector general to find out if the phone was wiped.

“Yes that’s correct, the device had been reset to factory settings,” the OIG official wrote back.

Three months later, in December 2018, the OIG released the report on its hunt to recover additional text messages Page and Strzok sent on six phones they used, four of which were assigned by the FBI. The effort resulted in the discovery of hundreds of text messages, but none came from the special counsel’s office phones, both of which were wiped before investigators recovered them.

The following January, DOJ officials reached out to Verizon with a request for billing statements to check how many messages Page and Strzok sent on their special counsel’s office phones. Verizon responded by saying no text messages were sent, with a caveat that data did leave the device. Verizon’s report didn’t cover the most common way to send a message on an iPhone—the iMessage app—which uses an internet connection rather than the carrier’s text service.

“Both numbers did have data usage so it could mean that if any messages were sent, it could have been through some type of app but we would not know for sure from our end,” a message from Verizon stated.

Mueller concluded his 22-month investigation having found no evidence of collusion between the Trump campaign and Russia.

SNOW Flakes After Record Software IPO Tyler Durden

Wed, 09/16/2020 – 13:04

Update (1300ET): After soaring from its post-IPO open at $245 to $319, SNOW has erased all its post-open gains and is back below $245…

* * *

The much-hyped IPO of the aptly-named ‘Snowflake’ is about to make many of America’s richest even richer-erer.

It sold 28 million shares Tuesday for $120 apiece, above an already elevated range (SNOW’s initial IPO range was $75-85 on Sept 8; then it was bumped to $100-110 on Sept 14). The Snowflake offering is being led by Goldman Sachs Group Inc. and Morgan Stanley.

The $3.36 billion raised listing ranks as the biggest U.S. IPO this year (and biggest software IPO ever), excluding the $4 billion offering by the special purpose acquisition company, or SPAC, backed by billionaire Bill Ackman.

At its IPO price of $120 a share, the cloud-computing company was worth $33.3 billion, more than Twitter and almost tripling the $12.4 billion it was valued at in a February fundraising round… but by the time it opened at a stupendous $245, SNOW is now worth over $60 billion – bigger than Dell, VMWare, FedEX, CME Group, and bigger than 2 Twitters.

After opening, it shot up to $$319… after being briefly halted!

As a reminder, SNOW now trades at a market cap larger than 400 of the S&P 500 companies.

And who is benefiting from this extreme surge in price?

As Bloomberg reports, Iconiq Capital – a multifamily office whose clients include Facebook’s Mark Zuckerberg, LinkedIn’s Reid Hoffman, and Twitter’s Jack Dorsey – took part in multiple Snowflake funding rounds beginning in 2017. Its 12% stake in the company, purchased for $245 million, is now worth more than $10 billion.

Interestingly, none other than Berkshire Hathaway is buying $250 million of SNOW shares from former CEO Robert Muglia at the IPO price – so already sitting with a massive profit.

Cloud computing “is a secular trend right now,” said Bloomberg Intelligence analyst Mandeep Singh.

“We have already seen Zoom, DocuSign and Datadog do well this year. Investors understand the cloud business model well and that makes a high-growth company like Snowflake attractive.”

Snowflake, founded in 2012, is a rare challenger to Amazon.com Inc. as a provider of data warehouse technology, which compiles information from different systems so clients can analyze it together in the same place. Bloomberg reports that in the fiscal year that ended Jan. 31, Snowflake’s revenue soared 174% to $264.7 million compared with the previous fiscal year, the company reported. In the sixth months that ended July 31, sales were $242 million, a 133% year-over-year increase.

Finally, we can’t help but see the irony of a record-setting IPO of a firm called ‘Snowflake’ as signaling some kind of top in the euphoric millennial-levered rally in stocks since the pandemic trough.

via ZeroHedge News https://ift.tt/2Rzvj68 Tyler Durden

Apple Accuses Epic Games Of “Starting A Fire And Pouring Gasoline On It” In Latest Court Filing Tyler Durden

Wed, 09/16/2020 – 12:54

The legal battle between Apple and Epic Games continued Wednesday as Apple responded to Epic Games request for a preliminary injunction (which, if successful, would force Apple to restore Fortnite to the App Store).

Using scathing language, Apple’s lawyers argued that the gaming company couldn’t prove any lasting injury from the app-store ban, arguing that “Epic started a fire, and poured gasoline on it, and now asks this court for emergency assistance in putting it out,” adding that Epic can fix the problem “by simply adhering to the contractual terms that have profitably governed its relationship with Apple for years”.

Epic first sued Apple on Aug. 13. The judge in the case has already proven unwilling to issue a temporary restraining order against Apple because Epic had, in a major way, brought the app store ban for “Fortnite” on itself. But in a second, more forceful attempt, Epic has beefed up its arguments, claiming that the ban has resulted in not only reputational damage, but lasting economic harm.

First of all, daily active users on Apple’s iOS operating system are down “over 60%” since the game was removed from the app store. The operating system is the biggest platform for Fortnite, with 116 million registered users, or nearly 1/3rd of the 350 million registered users Epic says Fortnite has attracted in total. It also claims 63% of Fortnite users on iOS access Fortnite only on iOS.

Epic claims it “may never see these users again”, due to Apple’s ban, and that the game’s community has been torn apart. Epic has also complained Apple is threatening to delay Epic’s application for a new developer account for “at least a year”.

After the battle between Apple and Epic Games exploded last month, Epic, via “Fortnite”, its immensely popular online shoot-em-up game, launched a campaign against Apple including a #FreeFortnite hashtag, and a tournament in which players could win prizes with anti-Apple messages. It annonced the effort with a video parodying Apple’s infamous “1984” ad bashing Microsoft.

It also released a video parodying Apple’s famous “1984” ad.

Apple has responded forcefully, and thus far, appears to be holding off Epics’ attempt.

However, Apple complained that Epic Games’ push to turn more developers against Apple was only launched for the purposes of publicity, and to try and capitalize on the prevailing public mood. The company’s attempt to generate buzz is already failing, Apple argued.

Apple argued that Epic was a “saboteur”, and that Apple’s ban wasn’t anticompetitive because Fortnite can still be played using other operating systems. “there is nothing anticompetitive about charging others to use one’s service,” Apple concluded.

“The Markets Could Be Disappointed”: Here’s What The Fed Will Say Today Tyler Durden

Wed, 09/16/2020 – 12:45

Looking at today’s FOMC decision at 2pm, and Powell press conference 30 minutes later, both of which will be the Fed’s last public comments before the Nov 3 election (the next FOMC 2-day meeting takes place on Nov 4-5, right after the election) consensus is for a steady policy outcome after the Fed firmly took Yield Curve Control, enhanced forward guidance, and an extension in the QE maturity horizon off the table in its July 28 meeting. As BMO notes, the breadth of expectations run from “little change with an emphasis on the 2023 dots” to “extension of the weighted-average-maturity of QE with firmer forward guidance.” That, however, could prove a disappointment to equities according to BMO’s Ian Lyngen given the Fed’s uber-dovish efforts heretofore, although he lays out four considerations.

First, the Fed has erred on the side of delivering its biggest changes outside of the regularly scheduled FOMC meetings (Jackson Hole the latest example). This is, of course, a function of the emergency nature of the moves. That said, there certainly is logic in de-emphasizing the every six weeks cadence of policy changes as it enhances the Fed’s flexibility – a commodity the FOMC clearly prizes as evidenced by the lack of details around the new average inflation objective.

Second, those in the market forecasting action from the Fed this afternoon offer caveats such as “it would boost sentiment”, “while not immediately additive to the real economy”, “the probably won’t, but should”, etc. – suggesting a collective sense that window-dressing is the most one should hope for at this point. To be fair, a great deal of accommodation has already been provided and the approaching Presidential election – while not so close as to limit the Committee’s actions today – does offer an incremental reason to keep the more dovish options of QE changes, hard forward guidance, or YCC securely in the toolbox and in reserve until a point when the economic outlook takes another material leg lower.

The disparate expectations imply that some subset of the market will be dissatisfied with any Fed action and implicitly caught offsides. This sets up the post-announcement response as potentially choppy, albeit within the confines of the existing trading range.

Fourth, the Fed has routinely demonstrated a bias to get ahead of the market’s expectations for greater accommodation – effectively out-doving the doves. This tendency on the part of Powell is the most compelling reason to anticipate a dovish surprise today ‘while not immediately additive to the real economy.’ See what we did there? This is unlikely to be accomplished simply by a series of SEP that shows policy rates at zero until at least 2024; which is consistent with Eurodollars note with no rates hikes expected until 2025.

With big picture that in mind, here is a detailed breakdown of what Wall Street expects today at 2pm EDT when the Fed publishes its rate decision and staff economic projections, and in the post-meeting press conference with Chair Powell which will commence at 230pm EDT, courtesy of NewsSquawk:

The Fed will keep rates unchanged at between 0.00-0.25%; its new policy framework is dovish, but unlikely to result in changes this week.

The Fed will likely avoid announcing enhanced forward guidance as it waits to see how the recovery plays out. Dovish signaling will stem from the Fed’s updated projections; while growth and unemployment forecasts will likely be nudged up and down respectively, the focus will be on the central bank’s forecasts for rates in 2023 (released for the first time) and on inflation to see if it still sees inflation running below target over its forecast horizon; if it does, the new policy framework implies it will be longer before the Fed begins thinking about lifting rates.

Some changes to QE maturities are a possibility, although not the base case for the September meeting.

Expect Powell to allude to yield curve targeting policies still remaining in its toolkit, following similar remarks from Vice Chair Clarida recently. If asked, Powell will likely again lean back on negative rates, though retain the optionality for the Fed to use them in the future if the situation demands.

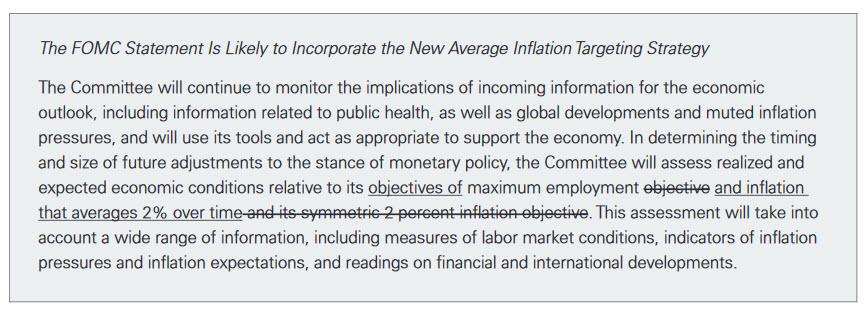

AVERAGE INFLATION TARGETING: The Fed’s new average inflation targeting framework is generally considered to be a dovish development for future policy, although it is unlikely to result in any major policy changes this month. Nevertheless, the Fed might reflect its new inflation regime within its statement. Specifically, the line which refers to the “symmetric 2 percent inflation objective” could be tweaked; Goldman Sachs thinks it will be changed to “inflation that averages 2% over time,” while others think “over time’ might instead be ‘on a sustained basis.”

ENHANCED FORWARD GUIDANCE: Officials seek more clarity on how the recovery is playing out before implementing specific forward guidance, which implies a September unveiling is unlikely. For now, statement tweaks may do much of the heavy lifting for the Fed. Chair Powell will likely still face questions on the theme, particularly since ‘a number’ of officials want rate guidance to be tightened. The general expectation is that the Fed will make these sorts of changes before the end of the year, perhaps in November. Officials appear to be leaning towards an outcome-based version, rather than a calendar-based version.

STAFF ECONOMIC PROJECTIONS: In the absence of other policy changes, the Fed’s dovish signal – that it will keep rates at current levels and keep policy accommodative – will come from the projections. These projections will need to walk a line of reflecting the US economy’s resilience, as well as telegraph the challenges that the economy still faces, and the level of support that is still needed. The Fed will still be keen to impress that the recovery will continue to be protracted, and risks to both growth and inflation are to the downside. Some officials have sounded more upbeat on the labour market than June’s 9.3% end-2020 forecast implies; Robert Kaplan, for instance, said he sees the unemployment rate ending the year around 8%. And on growth, Chair Powell recently said that three-months ago, there was a possibility of a much slower recovery, and of the recovery not going very well at all, but that has not happened; that puts the Fed’s current -6.5% GDP projection in line for an upward revision. The Fed’s June forecasts do not see inflation rising to 2% during its forecast horizon that runs through the end of 2022 (we will start getting 2023 forecasts at the upcoming meeting); if the Fed continues to see sub-2% inflation, the market will take that as another signal that rates will remain at present low levels for an extended period, given its new inflation framework. Finally, with regards to the notorious ‘dots’, the Fed sees no movement in rates through its forecasts, and that is unlikely to change this week. That would be in line with money market pricing (which, incidentally, prices a non-zero probability that rates could be cut into negative territory before 2023; if Powell is asked about negative rates, expect him to be cool on them, while retaining the optionality to keep them in the toolbox for the future).

QE MATURITIES: The Fed’s current QE program is heavily weighted towards shorter-dated maturities, with over half of its current Treasury buying focused on the maturities up to 5-years. Some analysts therefore have made the case that the Fed might extend its maturity horizon. While the general expectation is that the Fed will hold off any major changes, UBS argues that there are costs to waiting, as large amounts of front-end buying intensify future leverage ratio constraints for some banks. UBS says that USD 50bln of purchases in the 5-year+ sector would stimulate more than USD 80bln across the curve. And it argues that the Fed could extract more duration even with a smaller headline purchase amount. Finally, on asset purchases, we will be paying attention whether the Fed enshrines the rate of purchases in its statement (currently around USD 80bln per month, but that is not explicitly stated within its statement); some have suggested that this is something more likely to be seen when the Fed eventually raises the rate of its bond buys.

DOTS: The dot plot is likely to continue to show a baseline of no rate hikes through the end of the forecast horizon, which now extends to 2023. Two participants showed hikes by 2022 in the June projections, so Goldman expects three to show hikes by 2023 in the September projections. While the recovery now looks likely to be quicker than expected in June, the formal adoption of the new framework likely raises the bar a bit for showing rate hikes over the next few years. The neutral rate dots have been quite stable recently, and some expect further convergence toward the 2.5% median.

YIELD CURVE CONTROL: Fed Vice Chair Clarida and Governor Brainard both recently suggested that yield-curve control policies were still in the toolkit, though both believed that they were not likely to be implemented in the near-term. The remarks were particularly notable given that the Fed’s July meeting minutes had heavily leaned against the policy. It is therefore likely that Powell will give a similar nod if he is asked about it at the press conference, and will likely suggest the tool needs more study.

MARKET REACTION: Morgan Stanley says that, for the rates complex, the structural shift in monetary policy supports lower front-end real yields and steeper curves in the medium-term, but the market needs specific details on how the new framework will be implemented. Additionally, MS adds that a long-running QE program and the possibility of more QE will keep a lid on how much the curve can steepen over the medium term. In that sense the USD’s reaction will be a function of how rates markets respond. Traditionally, lower real yields have been a negative for the USD, but context will be needed; “When real yields are falling amid wider breakevens, USD weakness tends to be both consistent and widespread,” MS explains, “however, when real yields fall alongside breakevens or when breakevens are tightening and real yields are rising, USD performance tends to be both positive and far more mixed.”

According to BMO, the departure point for both US rates and domestic equities is relevant insofar as a decidedly mid-range backdrop should clear the way for a ‘clean’ kneejerk response to the Fed’s actions or inactions. This will be useful in calibrating an understanding of investors’ reaction function to any potential (and presumably incremental) change to policy; although as a theme the probability of breaking the trading range in Treasury yields is low given the recent demonstrated resilience of the 60-78.7 bp zone in 10s and the magnetism of 68 bp. And “while there is little question risk assets are at least modestly more vulnerable to a policy disappointment than rates” BMO’s Ian Lyngen adds that “the inability of the early September selloff to leave the S&P 500 below 3400 implies that any post-FOMC weakness will prove, yet another, opportunity for investors to buy the dip.” The bottom line: “we continue to expect the Fed will emphasize rhetoric over action at this juncture.”

STATEMENT REDLINE: Goldman expects the FOMC to modify its post-meeting statement to recognize the new average inflation targeting strategy. Specifically, the Fed will replace the reference to a “symmetric 2 percent inflation objective” with a reference to “inflation that averages 2% over time.”

via ZeroHedge News https://ift.tt/3mCQy5k Tyler Durden

Rocket Fired At US Embassy Baghdad Marks 4th Attack On Western Targets In 48 Hours Tyler Durden

Wed, 09/16/2020 – 12:23

On Thursday sirens range out in Baghdad’s Green Zone alerting personnel at the US embassy of an inbound rocket attack after a series of similar attacks on Western targets in the Iraqi capital over the last 48 hours.

“Iraqi Security Media Cell has confirmed a Katyusha rocket fell inside the Green Zone, specifically near a residential apartment,” an official US military coalition statement said. “Outlaw groups continue to target Iraqis,” it added.

US Embassy in Baghdad’s sprawling Green Zone, via AP.

The day prior, on Tuesday, AFP reported that “three separate attacks in 24 hours have targeted Western diplomatic or military installations in Iraq, security and diplomatic sources said Tuesday, hinting at a new escalation between authorities and rogue groups.”

Previously this week two two Katyusha rockets targeted the U.S. Embassy, however, no one has been hurt in any of the attacks which left only light damage.

It remains unclear exactly which group or groups are behind the attacks, but the State Department has in the past pointed the finger consistently at Iran-backed Iraqi Shia militia groups.

BREAKING: Sirens on at US Embassy in Baghdad #Iraq after reportedly being targeted by Katyusha rocket.

In just the last 48 hours Baghdad has witnessed the following:

a Monday Katyusha rocket attacks on the US embassy

on Monday two explosives devices were detonated, targeting a U.S.-led coalition equipment convoy

a Tuesday morning IED detonation targeting a British Embassy vehicle

a Wednesday rocket attack on the US embassy

During Monday’s attack the US embassy’s C-RAM system, or “Counter rocket, artillery, and mortar” system, was activated in response to the inbound rocket fire.

A week ago the Pentagon announced that a major Trump-ordered American troop draw down from Iraq would begin this month.

CENTCOM chief Gen. Frank McKenzie said while touring a US base in Iraq that troop numbers there will be cut down to from 5,200 to 3,000 this month.

But it seems every time the White House pushes for a sizeable Mideast troop exit, a series of conflict incidents serves to keep the US bogged down and present.

via ZeroHedge News https://ift.tt/2GZ6cHE Tyler Durden

McDonald’s “Running Out Of Burgers” Thanks To Travis Scott Value Meal As “Sandwich Wars” Heat Up Tyler Durden

Wed, 09/16/2020 – 12:05

Business Insider reported Wednesday that the popularity of McDonald’s $6 Travis Scott-branded “Cactus Jack” limited edition value meal has led to restaurants selling more burgers than they can stock, with some even “running out of burgers” as hungry rap fans show up in droves.

McDonald’s released a statement proclaiming the accomplishment Wednesday morning, saying it’s “so lit”.

“No doubt, Cactus Jack sent you…A LOT of you. SO many of you,” McDonald’s said in a statement.

“In fact, it’s been so lit, some of our restaurants have temporarily sold out of some of the ingredients in the meal,” McDonald’s said in a statement. “We’re working closely with our suppliers, distributors, and franchisees to resupply impacted restaurants as quickly as possible.”

That statement was probably a welcome change of pace for Micky D’s comms department, which has spent most of the last month fixated on the company’s battle with former CEO Steve Easterbrook.

Due to the meal’s popularity, franchisees are introducing a strategy of “controlling” the supply of some ingredients.

Due to the popularity of the deal, McDonald’s is temporarily controlling the supply of some ingredients, including Quarter Pounder fresh beef, bacon, slivered onions, shredded lettuce, according to sources with knowledge. More restaurants are expected to run out of these Quarter Pounder ingredients in the coming days, as McDonald’s weathers supply chain disruption.

Controlling supply is a strategy McDonald’s uses to prevent shortages, such as when meat processing plants were shut down earlier this year. However, this is the first time during the pandemic that McDonald’s has actually run out of ingredients — a shortage sparked by massive demand for the Travis Scott Meal, not coronavirus-related supply chain disruptions.

Meanwhile, TMZ reports that Travis Scott is getting fined over a “rowdy gathering” at a Micky D’s over his new $6 meal. Both the rapper and a Micky D’s restaurant in the city of Downey, Calif. were cited after a slew of fans mobbed the store when Scott showed up to greet fans. The city said he failed to file for an event permit, and fined him $100 and the McDonald’s $200.

Imagine getting slapped with a fine just for showing up at McDonald’s. Might make a good rap lyric.

via ZeroHedge News https://ift.tt/35LKUHV Tyler Durden

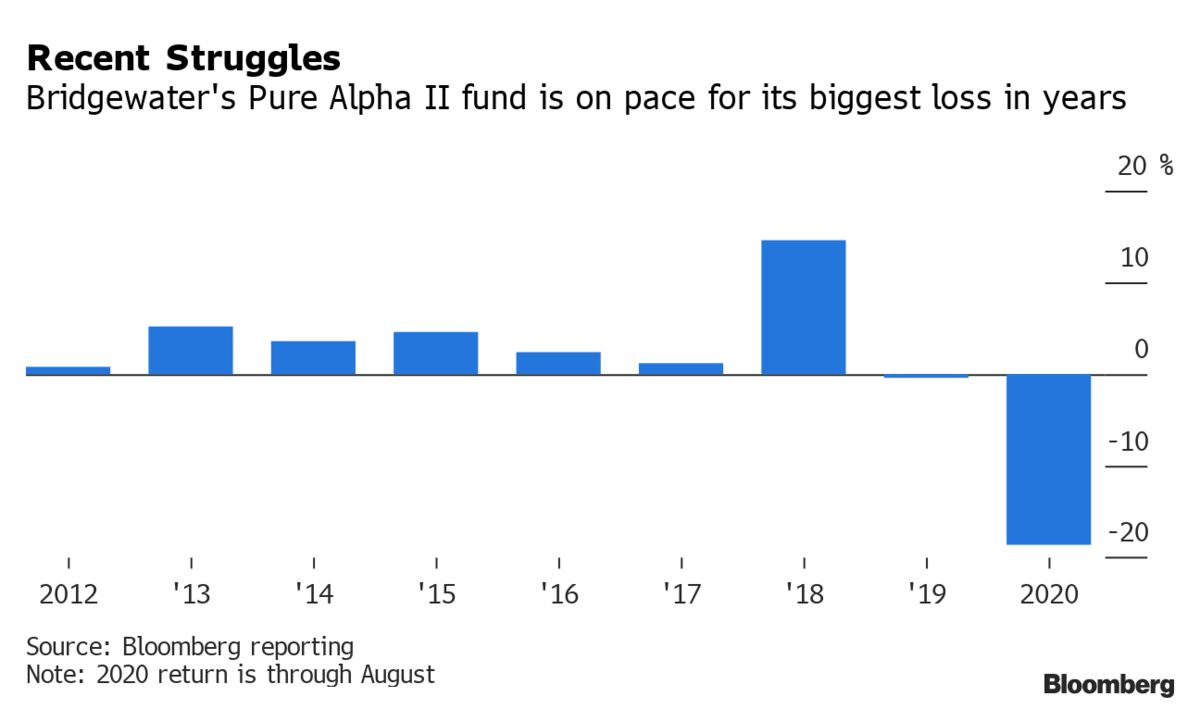

Dalio’s Bridgewater, Down 18.6% YTD, Sees $3.5 Billion In Redemptions And “Dozens” Of Layoffs Tyler Durden

Wed, 09/16/2020 – 11:51

It’s been an ugly year, performance-wise, for the man that the entire industry seemed to be worshiping, without question, heading into 2020. Ray Dalio’s Bridgewater Associates is down 18.6% for the year, as of the end of August.

But, but, but – the “How the Economic Machine Works” video. Didn’t Ray have it all figured out?

Apparently not. In addition to the fund’s worst losses in a decade, there is a “sprawling list of troubles” being dealt with internally, according to Bloomberg. These trouble include internal computer models misreading the market (also known as the New York Fed model), $3.5 billion in redemptions during the first 7 months of the year and Dalio losing an arbitration fight with ex-staffers.

He also has ongoing feuds with his co-cheif executive and has laid off “dozens” of employees, according to the report.

The chaos comes at the worst possible time for Dalio who, after writing “Principles” seemed to be hell bent on cementing his legacy as a financial world legend. But, perhaps among all that book-writing and TV interviews, Ray forgot what his job was in the first place?

Dalio took to TV on Tuesday and defended his fund: “We are the largest hedge fund for a reason. We have never had a significant downturn, all positive years, but we knew that there would come a day. We missed the pandemic going down and that is the reality.”

And what changes has Dalio made to adjust? Apparently none. “We are operating in the same way we have always operated,” he told Bloomberg TV. Dalio says the firm still has 45 commitments from investors, many around $1 billion.

The firm’s key issue, according to insiders, was that it adopted a risk off strategy in March while the market was tanking, and then failed to put risk back on despite the Federal Reserve guaranteeing it would backstop the market with unlimited QE.

Former employees say that the fanfare surrounding Dalio has also “distracted him from the firm”. Dalio doesn’t want to adjust his computer models to add new data that’s standard at other firms, including tracking oil tankers.

There are also several ongoing personnel disputes ongoing. The company’s former co-CEO Eileen Murray sued the company in July over compensation and gender discrimination. Some investors in the fund said this disputed “troubled them”, according to Bloomberg. The company’s head of research is also at odds with the firm over the issue of unequal pay.

Bridgewater has cut dozens of jobs amidst the chaos and its number of investors has dropped from 350 to about 300. Clients that remain on the roster tout the firm’s 10.4% annualized gain since 1991 – and its “unparalleled customer service”.

Employees at the firm have been shaken up by the poor returns and the layoffs, however. Additionally, an arbitration case against Lawrence Minicone and Zachary Squire, two Bridgewater employees that left the firm to start their own, recently showed that Bridgewater lodged allegations of theft of trade secrets against them under false pretenses. This has also left a bad taste in the mouths of current employees.

Bridgewater long has a reputation of an “extreme approach” to secrecy and departing staff, including contracts that make employees ask before they can take new jobs. Bridgewater defends the contracts, which can also prevent employees from trading equities for the rest of their careers, stating: “We believe we are fair and reasonable partners and have no incentive to enforce the restrictions more broadly than necessary.”

Perhaps another trip to Burning Man would clear Dalio’s head?

via ZeroHedge News https://ift.tt/3iDj9oq Tyler Durden

We all know it yet the unspoken truth deserves to be said out aloud.

You all heard the phrases‘Don’t fight the Fed’, and ‘ there is no alternative’. Can we be clear what these phrases really mean? They mean people are buying assets at prices they otherwise wouldn’t because a central planning committee is putting in market conditions that changes their market behavior.

People are paying forward multiples that are higher than they would if they earned higher interest income. The ‘desperate search for yield’ they call it. Think of it as a forced auction. You must pay, and you must pay more because you can’t bid on anything else and neither can anyone else hence there are now bidders for ever less available product (i.e. think shrinking share floats) driving prices wildly higher. And as central banks have become permanently dovish over the past decade Fed meetings are the principal impetus for rallies. Indeed most gains in markets come around days that have Fed Day written on them, a well established history going back decades now.

“In a 2011 paper, New York Fed economists showed that from 1994 to 2011 almost all the S&P 500’s returns came in the 3 days around an FOMC decision. Over this period the index rose by 270%, and most of those gains happened the before, the day of, and the day after a Fed meeting.”

So Pavlovian has the response become that shorts automatically cover ahead of Fed meetings and investors buy ahead of Fed meetings expecting a positive response. The Fed is the market as it’s driving its entire behavior. The “Fed put” they call it. Another phrase that explicitly acknowledges that investors are orienting their risk profile behavior on what this unelected committee does.

And it is this over decade long process of now permanent intervention that has produced the ever widening disconnect in asset prices from the economy:

A perpetual process of intervention that is creating ever wider wealth inequality and is building ever more financial risks, facts that are well recognized by participants.Here is Mohammed El-Erian in his latest opinion piece highlighting the ‘Fed put” and the building risks and disconnects:

“even looser monetary policy is likely to result in further disconnecting financial markets from the real economy (the issue of prosperous Wall Street versus struggling Main Street). This could easily amplify the view that the Fed is aggravating inequality. While officials have tended to brush off – at least in public — the risk for future financial stability of over-valued markets and over-extended new retail investors, it may prove harder now that loose mortgage conditions are decoupling the housing market from forward income-based affordability indicators. Indeed, many signs of excessive financial risk-taking are already flashing yellow or red on the back of the continuously reinforced market notion of a deep, always in-the-money ‘Fed Put’.”

Well there you have it.

The gall of Jay Powell then, who not only has a personal long index portfolio in the tens of millions of dollars, who not only personally benefits from said construct, but then continues to deny the policy’s direct impact on widening wealth inequality, that audacity to lie to the American public about it all is something else.

He can claim unchallenged by the press that the Fed’s policies absolutely do not add to inequality but everybody knows that it does. Shame on him and shame on all the Fed presidents that keep playing along in the game of denial and deception.

All of Wall Street, its compensation, the valuation of companies, all of it is vastly inflated and impacted by Fed bail outs and interventions and now supposedly going forward as well based on the view that the Fed will remain at zero rates for many years to come, independent on what the data may say in the future.

‘The Fed has our backs’ is another one of those phrases lurking out there displaying an attitude of complacency and open admission that because of the Fed investors are engaging in risky behavior they otherwise perhaps wouldn’t were it not for the belief that the Fed will bail them out of risky investing decisions by bringing markets back from the abyss.

And that is the truth, the entire market universe orients itself on these phrases and therefore engages in such behavior driven by the action of this central planning committee that denies this very fact.

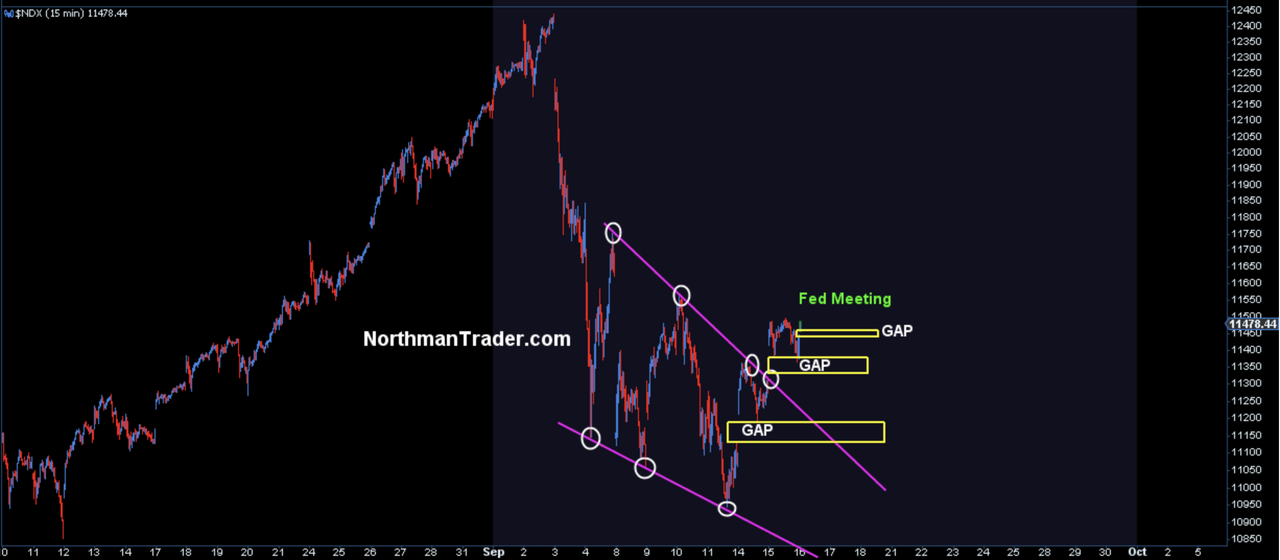

This has nothing to do with free market capitalism. It’s a perverted form of market planning. Now I can’t change the construct and like many I can just play along. For example, last week’s view that $NDX was setting up for a long trade based on a technical pattern was also based on the view that people would once again buy into stocks ahead of a coming Fed meeting during OPEX week no less.

That rally to come I suggested at the end of my recent CNBC interview:

And sure enough they kept piling in ahead of the Fed. Three gap ups in a row this week running like flies toward the light (the Fed):

So yes we can play along with it, but we can also be critical of the construct and the entire dishonesty of the Fed to refuse to acknowledge its role and to blatantly lie about the consequences. And we can highlight the budding financial risks that keep being propagated by this unaccountable committee that operates unchecked and unbalanced self admittedly crossing red lines.

But while the Fed has succeeded again in bailing out Wall Street, its self declared pretend effort to help Main Street has predictably turned into a joke:

So today we all gather again to watch this committee shower us with pretend wisdom. By all means, let’s celebrate the absurdity:

Today millions of investors gather for the regularly scheduled ritual called Fed Day, celebrating free market capitalism by hanging on the lips of what more gifts the head of the central market politburo bestows on the top 10% that own 87% of all stocks.

Let’s call it what it is: A desperate subsidy masking all the structural problems underneath by disconnecting asset prices ever further from the economy & enabling ever larger credit bubbles:

A subsidy benefitting the wealthiest while leaving the poor in the dust, a subsidy based on lies told by idiots signifying nothing other than a reflection of a bankrupt political system that is incapable of developing structural solutions and entirely dependent on ever more debt expansion and cheap money, a house of cards that will crumble when the efficacy of central intervention and the ever desperate efforts to make reality reach their limit.

And that is the unspoken truth.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2ZIi4Va Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}