Capital One Hit With $80 Million Fine, Cease & Desist Order, Over 2019 Data Breach Tyler Durden

Thu, 08/06/2020 – 11:21

The Fed on Thursday announced a new fine imposed on Capital One for a massive data breach last year that impacted more than 100 million people. Within 90 days, the company must also submit a plan to the central bank showing how it will improve protection of customers’ personal information, along with an internal audit of the firm’s risk management protocols.

Capital One has also agreed to pay an $80 million fine to the Office of the Comptroller of the Currency over the major hacking incident, which occurred last year.

The Virginia-based bank and credit card issuer says it has taken steps to tighten security, even before the July 2019 arrest of the suspected hackers who pulled off the attack.

But under these orders, CO will be required to take additional steps.

via ZeroHedge News https://ift.tt/30yPxSP Tyler Durden

Since the first news of pandemic in late January, I’ve been discussing potential accelerants to the unraveling of our fragile financial system.

The system appears stable until a catalyst pushes it off the cliff.

Catalysts come in a variety of forms, from the apparently modest “straw that breaks the camel’s back” to a broad awakening that the status quo simply isn’t capable of adapting successfully to new realities.

Financial catalysts tend to result in sudden, cataclysmic collapses in liquidity, solvency and sentiment.

While the Federal Reserve can “fix” liquidity crises by creating currency out of thin air, that doesn’t make bankrupt firms solvent or make employers hire employees.

Once complacent confidence slides into cautious fear, massive liquidity injections to keep the system from crashing are understood as last-ditch desperation.

Social-political catalysts are slower but much more difficult to reverse.

While the media’s attention has been focused on the protests, two other social-political catalysts are gathering momentum:

1. The failure of our education complex to provide workable childcare/learning solutions

2. The hope of a V-shaped recovery in employment collapses.

There is a class dynamic in these potential catalysts that few mainstream pundits follow to the logical conclusion.

When socio-economic distress is limited to the politically powerless working class — for example, the blatant exploitation of gig-economy and contract workers — the power structure can safely ignore the brewing crisis because the distressed workforce has insufficient economic-political power to threaten the rule of the Power Elites.

But when the top 20% of the workforce that accounts for 50% of all consumer spending and 80% of the citizenry’s political voice is in distress, the Power Elites better pay attention.

Nobody in power really cared if lower-income households struggled with juggling childcare and getting to work; but when Mr. and Ms. Technocrat are struggling, suddenly it’s an issue that can’t be ignored.

The same dynamic is also in play in the 21% unemployment that’s accelerating to 25% unemployment. As long as it was the marginal workforce that was losing jobs, the power structure reckoned unemployment was a solution.

But as the unraveling gains momentum, middle-class jobs will start vanishing and unemployment won’t be enough to pay bloated mortgage payments, property tax bills, etc., and the defaults of student loans, credit cards, auto loans and mortgages will start piling up.

As people awaken to the fact that the V-shaped recovery was a fantasy, sentiment will slide from confidence to angst.

The failure of institutions to adapt to new realities will be impossible to deny, and the choices may boil down to opting out (i.e. assemble informal groups of households that pool resources to hire a private tutor for home-schooling their children) to organized revolt (i.e. teachers’ union strikes).

Sclerotic, hidebound institutions optimized for stability and permanent growth are simply not designed to adapt to sudden, rapid change and disruption of permanent growth.

Systems stripped of buffers are fragile, systems stripped of feedback are fragile, systems that optimize doing more of what’s failed spectacularly are fragile, systems that are little more than fractals of incompetence are fragile, systems that rely on the artifice of denial and fantasy are fragile.

Fragile systems break. This is why the unraveling is accelerating.

via ZeroHedge News https://ift.tt/33Crowr Tyler Durden

“He Abandoned The Deadly Cargo”: Meet The Mysterious Businessman At Center Of The Beirut Blast Saga Tyler Durden

Thu, 08/06/2020 – 10:55

Thus far an official ongoing investigation by Lebanese authorities into the cause of Tuesday’s Beirut port blast, now considered the largest non-military munitions explosion in history, has dubbed it severe “negligence”.

It’s now well known that over 2,500 tons of ammonium nitrate, an ultra-combustible chemical compound utilized in fertilizers and production of explosives, was allowed to sit at the port in a warehouse going back seven years.

Specifically, President Michel Aoun identified that it was no less than 2,750 metric tons of ammonium nitrate that detonated as it was “stored unsafely” — though port officials reportedly attempted to warn the government for years that it must be moved. A number of port officials have been placed under house arrest pending the investigation.

An undated photo of the vessel Rhosus, via The National/EPA

Customs chief Badri Daher has told international media that his agency pleaded with Lebanese courts and high officials to order the chemical removed. Daher says the request for urgent removal was madesix times to the judiciary over the years, all denied.

“This did not happen,” he said. The end result after the dangerous chemical — which is the same use in the deadly 1995 Oklahoma City bombing — was stored there since 2013 (also in undiluted form), was the most destructive blast in Lebanese history, killing over 135 people and injuring more than 5,000 – not to mention an estimated three billion dollars in damage.

“Legal documents, court correspondence and statements by public officials now trying to pass the buck shed light on the operations of the port, which has been dogged by allegations of widespread bribery and controlled in large measure by the militant Hezbollah group,” The Washington Post reports.

And the almost unbelievable story of how the explosive substance got there has emerged. It’s centered on a derelict and leaking vessel leased by a Russian businessman living in Cyprus. In 2013 the man identified as Igor Grechushkin, was paid $1 million to transport the high-density ammonium nitrate to the port of Beira in Mozambique. That’s when the ship, named the Rhosus, left the Black Sea port of Batumi, in Georgia.

UK Daily Mail and The Siberian Times has published the above photograph of Igor Grechushkin, reported to be still residing in Limassol, Cyprus with his wife. Image: Ren TV

But amid mutiny by an unpaid crew, a hole in the ship’s hull, and constant legal troubles, the ship never made it. Instead, it entered the port of Beirut where it was impounded by Lebanese authorities over severe safety issues, during which time the ammonium nitrate was transferred off, and the largely Ukrainian crew was prevented from disembarking, leading to a brief international crisis among countries as Kiev sought the safe return of its nationals.

Meanwhile, Igor Grechushkin – believed to still be living in Cyprus – reportedlysimply abandoned the dangerously subpar vessel he leased, as well as its crew, never to be heard from again.

“…the vessel was abandoned by her owners after charterers and cargo concern lost interest in the cargo. The vessel quickly ran out of stores, bunker and provisions.”

The ammonium nitrate was supposed to be auctioned off, but this never happened. Apparently exasperated customs and dock officials even suggested Lebanese farmers could simply spread it across their fields for a good crop yield. But not even this simple solution was heeded, nor proposals to give it to the Lebanese Army.

During the standoff which created a diplomatic rift between Ukraine and Lebanon: the largely Ukrainian crew was prevented from leaving the ship, even at times struggling to get food.

Via The Siberian Times: “The crew – eight Ukrainian and two Russian men – was forced to stay on board of the vessel while the owner Grechushkin declared himself bankrupt and ‘abandoned the ship’. Lebanese authorities agreed to let six out of ten sailors to leave the country, others were left stranded on the ship for almost a year.

Instead the deadly substance languished at port, and the Rhosus sank in the harbor years later. The last crew members weren’t allowed to leave the ship and return home until August 2014. Grechushkin may have paid for their return tickets at that time.

“Owing to the risks associated with retaining the Ammonium Nitrate on board the vessel, the port authorities discharged the cargo onto the port’s warehouses,” lawyers acting on behalf of creditors wrote in 2015. “The vessel and cargo remain to date in port awaiting auctioning and/or proper disposal,” it added.

And then later, more warnings, which apparently are in writing in legal documents:

“In view of the serious danger posed by keeping this shipment in the warehouses in an inappropriate climate,” Shafik Marei, the director of Lebanese customs, wrote in May 2016, “we repeat our request to demand the maritime agency to re-export the materials immediately.”

Astoundingly, even lawyers which had represented the effectively abandoned crew of the ship (which Ukrainian media at the time said were “hostages” of the Lebanese government) while it had been detained at port warned Lebanese government officials that the sensitive cargo was in danger “of sinking or blowing up at any moment”.

Yet these series of warnings went unheeded for years amid a notoriously corrupt and inept Lebanese system.

Meanwhile, the fate of the man originally at the center of the saga, whose decision to simply abandon the leaky ammonium nitrate laden ship in the first place, remains somewhat of a mystery and is now largely being overlooked in international media reports. Strangely, it doesn’t even appear that Lebanese law enforcement is eager to talk to him just yet.

Cypriot media is saying Igor Grechushkin is not a Cypriot passport holder but is indeed residing in the EU country. Local authorities have indicated they are ready to bring him in for questioning, but they haven’t received a request from either Lebanese authorities or Interpol. Cypriot police spokesman Christos Andreou announced Thursday: “We have already contacted Interpol Beirut and expressed our readiness to provide them with any assistance they need, if and when our assistance is requested.”

Why hasn’t this happened? So far a few scant details have emerged via a Russia-based English language publication called The Siberian Times. It’s also included what it says is the first photograph to have emerged of Grechushkin.

First pictures emerge of a Russian man whose ammonium nitrate cargo detonated in the port of Beirut. The 2,750 tonnes cargo of Khabarovsk-born businessman Igor Grechushkin was detained in Lebanon in 2013 https://t.co/hbu1VJgrespic.twitter.com/yQZqzcBIya

‘The owner of the ship Igor Grechushkin effectively abandoned the ship and the remaining crew.’

‘He is not providing us with money, he completely deprived us of all means of communication.

‘He told us that he went bankrupt and while I don’t believe him, the most important thing is that he gave up on both the people and the cargo’, wrote captain Boris Prokoshev back in June 2014 in a desperate plea to international organisations, diplomats, authorities of Ukraine and the authorities of the port of Beirut to release them.

Igor Grechushkin is reported to be still residing in Cyprus with his wife.

The Daily Mail has since republished the photographs of Grechushkin and his wife, writing that the Russian businessman “currently lives in Cyprus with wife Irina – has been accused of abandoning his ship in Beirut loaded with the lethal load.”

Given that Lebanese officials are now decrying a “crime against humanity” in having stored the deadly cargo at the port in the first place, one would think Grechushkin would at least be subject of investigation along with whatever top Lebanese officials willfully ignored the ticking time bomb in their midst.

via ZeroHedge News https://ift.tt/31rzq8Q Tyler Durden

New Survey Confirms Second Wave Of US Layoffs Is Well Under Way Tyler Durden

Thu, 08/06/2020 – 10:45

Readers may recall in mid-April, the first signs of the second round of layoffs and furloughs appeared. Then by June, high-frequency data of the U.S. economy suggested the recovery reversed as state governors were forced to pause reopenings due to increasing COVID-19 cases and deaths.

Since July, initial and continuing claims have risen, suggesting the worst employment crisis since the Great Depression of the 1930s continues to unfold.

New evidence, published Tuesday in a study by Cornell Law School Senior Fellow and Adjunct Professor, Daniel Alpert, reveals the second round of layoffs is becoming more severe as the fiscal cliff begins.

The study, conducted from July 23 to August 1, by Alpert and RIWI Corp., shows 31% of employees initially laid off or furloughed because of the virus-induced recession were just recently laid off a second time.

Here are highlights from the study titled “New Cornell-JQI-RIWI Survey Shows that the Second Wave of U.S. Layoffs and Furloughs is Well Under Way:”

Of workers who were placed back on payrolls after being initially laid off/furloughed as a result of the COVID-19 Pandemic Crisis, 31% report that they have been laid off a second time, and another 26% of those placed back on payrolls report being told by their employer that they may be laid off again.

37% of respondents employed by third-party employers (i.e., not self-employed) have been laid off/furloughed – at least once – since March 1, 2020.

57% of those initially laid off/furloughed reported being put back on payroll sometime after their initial dismissal, but 39% of such respondents say they were put back on the payroll yet were not asked to return to actual work.

The survey revealed a disturbing trend: The second round of layoffs are happening “in states that have not been experiencing recent COVID-19 surges, relative to those in surging states.”

RIWI conducted the survey, then Alpert and his team analyzed the data. Here’s how the survey was conducted:

“RIWI randomly engaged a total of 10,719 U.S. respondents aged 16+ from July 23 to August 1 on a continuous 24/7 basis with questions to determine who held a private-sector job, which share of those were laid off, which share of those re-payrolled, and then in turn which share was laid off or told they might be laid off (see Appendix for full question and answer set, as well as other technical information). A total of 6,383 respondents fully completed the core questions,” the study said.

As the labor market falters, recovery reverses, fiscal cliff hits, and rent eviction moratorium expires, households across America will be severely pressured in August until the next round of stimulus is passed.

The biggest takeaway from the survey is that there’s no V-shaped economic recovery in the back half of the year, the Trump administration and Congress will need to pass trillions of dollars more in direct payments to tens of millions of broke Americans, or face a crash in consumption. The virus-induced recession has financially ruined the bottom 90% of households.

Alpert said “additional economic shutdowns” due to rising virus cases and deaths will exacerbate the second round of layoffs.

Wall Street is ignoring the deep economic scarring from the virus, as we’ve recently mentioned: permanent job loss now stands at nearly 3 million in June, up from 1.6 million people in February.

Putting this all together, Gary Shilling, the president of A. Gary Shilling & Co., recently told CNBC that Wall Street has misread the shape of the economic recovery, as he warns a 1930s-style decline in the stock market could be ahead.

via ZeroHedge News https://ift.tt/2EOn8Q3 Tyler Durden

Mortgage rates in the U.S. continue to fall to record lows. The average contract interest rate for a 30-year fixed-rate mortgage fell to a record low 2.88% last week compared to 2.99% the previous week.

But, despite record low rates, potential homebuyers are becoming less active as total mortgage application volume fell 5.1% from the previous week according to the Mortgage Bankers Association’s seasonally adjusted index.

Refinance applications dropped 7% last week but remained 84% higher than the same period a year ago. Mortgage data and analytics firm Black Knight calculates that nearly 18 million borrowers could still benefit from refinancing their mortgage. Applications to purchase a home dropped 2% last week and now stand 22% higher than the same period last year.

With the average purchase loan amount rising, fears are growing that some first-time homebuyers are getting priced out of the market.

“Purchase loan balances continued to climb, which is perhaps a sign that the still-weak job market and tighter credit for government loans are constraining some first-time homebuyers,” MBA forecaster Joel Kan said.

Another sign that first-time homebuyers may be stepping back is the average rate for a FHA-backed 30-year fixed-rate mortgage has started to increase. These types of mortgages accounted for 35% of closed sales in June, according to the National Association of Realtors.

Home prices continue to rise as low rates and tight supply pushed the average median home price in July up 8.5% from the same period last year to $349,000, according to realtor.com‘s Housing Recovery Index. 48 of the 50 largest metros areas in the U.S. saw the median listing price jump in July compared to last July.

Inventory dropped by 34.8% in July from the same period a year earlier as none of the metro areas realtor.com tracks saw an increase in inventory. Inventory is going quicker than in June, when inventory dropped by 26.5% from the previous year.

Perhaps confirming the fears over the effects of the coronavirus on city living, condos are faring much worse than single family homes. The median condo sale prices in the U.S. fell by 1.4% in June compared to the same period last year. Condo sales fell by a seasonally adjusted 31.3% in June and 53.5% in May compared to last year, while single family home sales fell by 11.9% and 27.6% in June and May, respectively.

“The pandemic has fundamentally changed what a lot of buyers are looking for in a home,” Redfin economist Taylor Marr said.

“People are spending more time at home and less time at the office or school, and that means buyers want more space and private yards. And because of concerns about the virus, they aren’t as interested in shared amenities like elevators, community pools and gyms, which have traditionally been benefits of condo living.”

It will be interesting to see where the housing market goes from here as a mixture of low rates and inventory, high prices and an uncertain economy all work against each other.

For now, despite the rebound in sentiment, home-buying attitudes remain vastly different from homebuilder optimism.

via ZeroHedge News https://ift.tt/3iegeSB Tyler Durden

Key Wirecard ‘Business Partner’ Turns Up Dead In The Philippines After Mafia Links Exposed Tyler Durden

Thu, 08/06/2020 – 10:05

Wirecard’s collapse was forestalled for years thanks to Germany’s financial regulator BaFin, which aided the fraud by targeting journalists (most notably the FT’s Dan McCrum) who sought to expose the crude shell game used by the company to mask the fact that 2/3rds of its reported profits were pure make-believe.

Two months after one of Europe’s biggest accounting frauds was exposed by an “independent” report ordered by the company, Wirecard’s ex-CEO is under house arrest as he awaits trial for fraud charges, while his former No. 2, ex-COO (and purported Russian intelligence asset) Jens Marsalek, remains a fugitive from justice (it’s believed he’s hiding in Russia). FT reporters digging into Wirecard’s shady payments business have recently stumbled upon a disturbing link to one of Italy’s most powerful crime syndicates: The ‘Ndrangheta, a network of organized crime families based in the southern Italian region of Calabria. Apparently, a significant chunk of the “legitimate” profits that Wirecard managed to generate was tied to its work as a de-facto money laundering network for organized crime groups in Italy, Albania and Russia, the FT reports in a story entitled “Wirecard processed payments for Mafia-linked casino”.

Now, one of the owners of a Wirecard “payments partner” based in Manila who received millions of euros in “inward remittances” from the company over his – and was the subject of an FT investigation more than a year ago as the paper was trying to piece together the elaborate shell game being run by the company. That trek took the paper and its reporters to the Philippines, the country where Wirecard claimed to be hiding some $2 billion in profits that auditors never bothered to check.

That man’s name was Christopher Bauer. And as the FT reported Thursday, Bauer, 44, has apparently died under mysterious circumstances just weeks after Philippine authorities said they were investigating Bauer and his wife, Belinda Bauer, in a probe involving Wirecard’s partner businesses.

Bauer and his death was reported to a civil registry in Manila last week. Filipino officials repeatedly told the FT they couldn’t confirm if the Bauer who died was the same one who ran a Wirecard subsidiary that was, apparently, a key player in the company’s sweeping fraud.

Menardo Guevarra, the Philippine secretary of justice, told the Financial Times he had “to determine first if the deceased person is the same person subject of the ongoing investigation”. He would decide whether further investigation into Mr Bauer’s reported death was necessary after obtaining a copy of the death certificate. The Bauers — identified in an Financial Times investigation last year — owned PayEasy as of 2017, according to public filings, and have represented Centurion Online Payment International, a second partner business, in interactions with Wirecard. Mr Bauer in 2015 “reportedly received an inward remittance from Wirecard Asia for consultancy services rendered”, said Mr Guevarra without disclosing an amount.

On closer inspection, Bauer, it appears, was paid hundreds of millions of euros to bring in what appears to be laundered mafia money through digital gaming companies and other clients of PayEasy, the subsidiary that Bauer owned and ran (but was a critical node in Wirecard’s network).

Bauer also appears to have been closely tied to Wirecard’s fugitive COO Jan Marsalek, who is believed to be an operative working with Russian intelligence.

Mr Bauer, who told auditors from KPMG that he was a Wirecard employee before joining PayEasy some 12 years ago, also owned Froehlich Tours, a bus and coach rental business that shares an office with PayEasy in Manila.

At a meeting in Manila in March, Mr Bauer and Wirecard’s fugitive former chief operating officer Jan Marsalek briefed KPMG and EY on PayEasy’s business, telling the auditors that the company specialised in processing payments for “high-risk clients” in online gaming, gambling and porn, according to a special audit by KPMG.

The Philippine authorities are now investigating how immigration records were fabricated to show Mr Marsalek arriving in the country in June and leaving the next day for China. CCTV footage showed no such arrival.

Notices in a German newspaper appear to confirm Bauer’s death, and social media posts made by family members appear to commemorate his death.

On July 27, Mrs Bauer posted an image of a black ribbon on Facebook, while her daughter posted a photo of an urn bearing her father’s name two days later. Mr Bauer’s family on August 1 published a death notice in a regional newspaper in Hesse, Germany, where his parents are living. Mr Bauer’s parents declined to comment. Mr Bauer’s lawyer did not immediately respond to a request for comment. Munich prosecutors, who are leading the criminal probe into Wirecard in Germany, said they had not received any official notice about Mr Bauer’s death. They declined to comment if an arrest warrant against him had been issued.

One shady character hanging out outside Bauer’s home in Manila told a FT reporter that he had died of a “heart attack”. But considering Bauer’s age, that seems unlikely.

Mr Bauer’s cause of death remains unclear. The civil registry declined to comment, citing the data privacy act. A guard at the Bauers’ gated community said he had died of a heart attack. A group of men playing cards outside the Bauers’ house in Manila said the widow could not comment and suggested speaking to her lawyer, whose contact details they declined to disclose. The men were standing by the property’s gate, which was marked by the logo of a local motorcycle club called Iron Cross Sons, whose website features scantily dressed women with Nazi-themed attire.

The men who spoke to the FT reporter at Bauer’s home were apparently members of a motorcycle club based in the Philippines whose members wear Nazi-inspired insignia, according to their website.

Links to Wirecard’s Russian-intelligence-linked COO? Check. Gangs of Nazis bikers hanging out outside his former home to scare off journalists? Check. Evidence that Bauer was a key link between a multinational corporation once listed on the DAX 30 and organized crime syndicates willing to pay for the privilege of efficiently and safely laundering their money? Check.

We suspect that whatever caused Bauer’s death, it probably wasn’t natural.

via ZeroHedge News https://ift.tt/3i77tKa Tyler Durden

Rabo: “Everything Can Appear ‘Hunky-Dory’…Until The Real Money Runs Out” Tyler Durden

Thu, 08/06/2020 – 09:45

Authored by Michael Every via Rabobank,

Where’s The Beef In This Word Salad?

It’s summertime, and the living isn’t easy – except for the lazy analysis in the summertime market analysis ‘word salads’ we are being fed, which miss the real beef of what is going on,

The US dollar had another bad day Wednesday. No doubt about it, it was mostly unloved. Not against all EM FX, however. TRY, for example, is this morning at 7.05 at the time of writing, and is likely to test much lower yet if the underlying fundamentals —like not having any FX reserves— don’t change. (Which also means EUR/TRY has moved from 6.67 to 8.42 year-to-date by the way.)

One of the big differences for USD this time round, however, was that the Chinese currency suddenly decided it was a developed currency and not an EM one. It also decided to show that widespread –and very real– concerns about the underlying fundamental of a lack of USDs in its vast economy too (at least in relative terms to is size) are misplaced, honest guv: just look at the never-ever-changing USD3.xx trillion in FX reserves! Indeed, USD/CNY was at 6.94 this morning. (Which means EUR/CNY is handily at 8.24, up from 7.81 at the start of 2020. Europe will love that.)

Here’s some of the beef: CNY or CNH are not markets that operate as other markets do, which today is no longer saying as much as it once did, sadly. Both are a political virtue-signalling device rather than something based on real supply and real demand. And right now it suits China to look virtuous ahead of the 15 August phase one trade deal review.

Here’s the rest of the beef: the same global markets that were so desperate for USD back in March that the USD had to extend hundreds of billions of USD in swap-lines to keep them from crashing are now apparently hating the USD so much that we see report after report about how the Dollar is unloved and it’s day is over.

Provided that we all pretend that our economies have fully healed from Covid-19 with no major structural damage, and that central-bank and government stimulus can carry on paying us 80% of salary to go on holiday as normal, and that the US will continue to always bail everyone out as needed with no questions asked, then yes, feel free to sell USD and kick it while it is down (all the way to the level before the crisis began on broad trade-weighted terms).

Just don’t’ forget what you will come screaming for as soon as we see that there is no proper recovery, that there is major structural damage, that government stimulus cannot carry on paying us 80% of salary forever, and neither can the US will continue to always bail everyone out as needed with no questions asked.

And, delicious as they are in hot weather, please don’t eat the word salads. Bloomberg offers this crunchy green take today, for example, repeated in full here:

“USD/CNH is heading lower in the near term and is protected against a sharp correction by the high cost of shorting the yuan. With less than three months to go until the US elections the yuan will be on alert for rhetoric which could weaken it. Yet, thanks to contrasting monetary policies between the Fed and PBOC there is a built in defense mechanism. One year CNH forward points are running at the highest since late 2017, even though spot USD/CNH has been steadily falling for several weeks. The forwards reflect lower USD yields and the PBOC putting rate cuts on hold. And with the PBOC moving away from expansive monetary easing that will sustain relatively high yuan yields. In contrast the Fed is in no position to end its very accommodative policy with the U.S. economy in contraction. Which means it is expensive to short the yuan and that could deter some traders from selling aggressively in the near term. As long as the PBOC continues to maintain an orderly fixing regime the downside for CNH is limited.”

Some of the ingredients above are true, and I have seen so, so many reports that are so, so much worse. Pages must be filled I suppose. (Look who’s talking! I just filled a whole in and most of you didn’t notice! J) To dismantle this salad:

Yes, China has higher rates, which strangely didn’t matter in FX two days ago…but it hasn’t slashed rates because it CAN’T; and it can’t because it is trying to hold a soft peg against USD with not enough FX reserves to back it up, relatively even with capital controls. Yes, there is going to be a US election –and a trade deal review– and this is virtue signal to say ‘we are playing nice!’…because they know what happens if they don’t: it isn’t CNY positive at all. Yes, it is expensive to short CNY, just as it is to short TRY, which has not saved it once the US ran out, has it? And, yes, the PBOC certainly has “an orderly fixing regime” – which is another way of saying it IS NOT AN ACTUAL FREE MARKET, but one where we are TOLD what the value is and where capital controls prevent any ‘haggling’. Why is this obvious fact slathered in layers of mayo to try to disguise how unpalatable it actually is?

Is this all clear on a hazy summer day? Allow me to summarise again:

We are deluding ourselves that we are recovering back to the status quo ante. We aren’t. We are deluding ourselves stimulus to shield us can be sustained forever everywhere. It can’t. We are deluding ourselves the US will be there next time for everyone as desired. It won’t be for some. So, yes, word-salad chefs, everything can look hunky dory due to marvellous, magical , magnificent central-bank liquidity, not the day-to-day jiggery-pokery,…right up until the REAL money runs out; which as Turkey and Lebanon prove, and China is desperate not to prove, is still USD and not the local equivalent. (And as Brazil, with rates art just 2% and negative real rates also risks showing – again.)

Or, if you are a real USD bear, then it is gold and not any fiat currency at all. In which case, real businesses should be panicking and markets collapsing, because a wrenching deflationary accounting and international-trade adjustment that will make the Covid crisis look like a normal day in the office is what looms for years during the transition away from fiat. Yes, you can buy stocks and gold in tandem and do well in the short term – but logically it’s word salad as an end-game.

Anyway, I leave you all to ice-cream, sun-cream, cold beer or wine, and what will no doubt be another very generous serving of word salad from the media today.

via ZeroHedge News https://ift.tt/3fvFK4d Tyler Durden

Over 80% Of Black Americans Don’t Want To ‘Abolish Police’ Tyler Durden

Thu, 08/06/2020 – 09:25

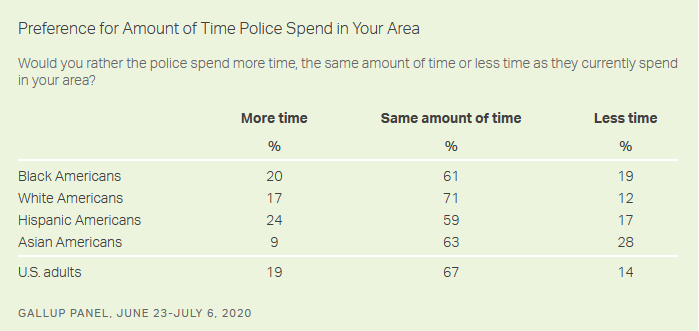

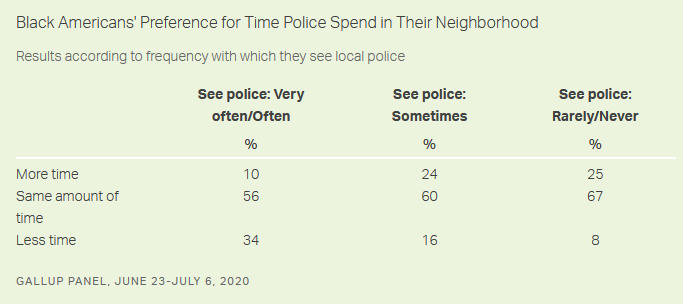

While BLM would have one believe that cops are inherently evil and must be abolished, a new Gallup poll finds that’s most minorities in America don’t feel that way. Of those surveyed, 61% of Black Americans are just fine with current levels of police presence in their area, while 20% say they want more patrols.

Overall, 67% of all US adults prefer the status quo while 19% say they want police to spend more time in their area.

Which group wants the most reductions to policing in their area? Asians, at 28%, followed by Black Americans at 19%, Hispanics at 17% and White Americans at 12%. On average, 86% of American adults want the same or more level of policing in their area.

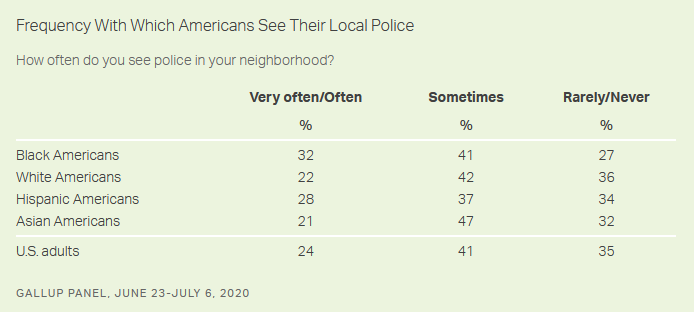

When it comes to how often police are seen in a neighborhood, Asians report the most at 47%, followed by Whites at 42%, Blacks at 41% and Hispanics at 37%.

According to the poll, “the slightly elevated frequency with which Black Americans see police in their neighborhood has limited impact on their preferences for changing the local police presence. About a third of Black Americans who say they often see the police in their neighborhood think the police should spend less time there (34%); however, the majority of adults in this group think they should spend the same amount of time (56%) or more time (10%).”

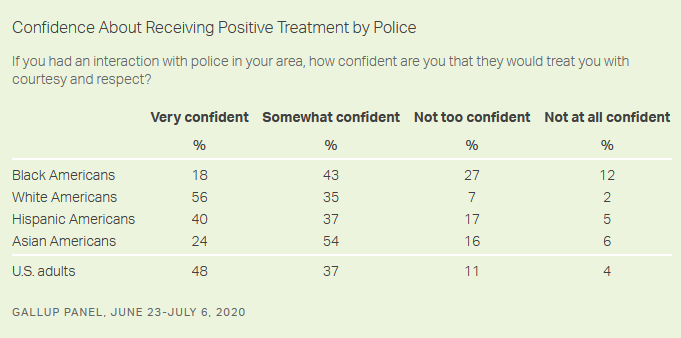

That said, while Black Americans are about as comfortable as the overall population with the amount of police presence in their area, less than 20% of Blacks feel ‘very confident’ that they would be treated with courtesy and respect by the police. 24% of Asians say the same, while 40% of Hispanic Americans and 56% of Whites are confident they would be treated well in an interaction with cops.

When factoring in those who are at least somewhat confident that the police would treat them well, a majority of Black Americans (61%) are generally confident, but this is still below the 85% seen nationally, including 91% of White Americans. -Gallup

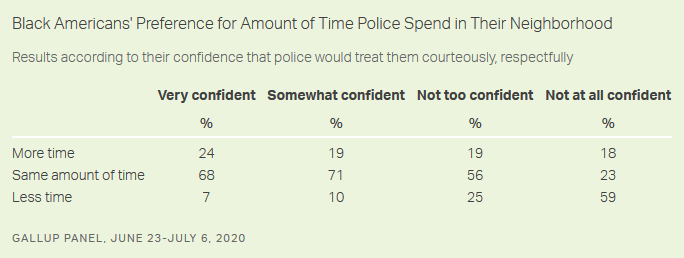

Overall, of the small proportion of Black Americans who are “not at all confident” that the police wouldn’t treat them well, 59% of them want police to spend less time in their area – while the majority of Blacks in America, including those “not too confident” about receiving positive treatment, want cops to spend the same amount of time or more where they live.

Gallup also found:

Notably, simply having an interaction with the police in the past year has no bearing on Black Americans’ preference for local police presence in their area:

Seventy-nine percent of those who have had an interaction with the police in the past 12 months say they want the police to spend more or the same amount of time in their neighborhood; 21% favor less time.

Eighty-two percent of those who have not had an interaction want the same or greater police presence; 18% want less.

What does matter is the quality of the interaction:

Forty-five percent of Black Americans who report not being treated with courtesy or respect by the police within the past 12 months want less of a police presence in their neighborhood. Meanwhile, 55% want the same or more police presence.

By contrast, just 13% of those who did feel they were treated respectfully want the police to spend less time in their neighborhood; 87% want them there as much or more often.

In short, most Black Americans don’t want changes in police presence, though nearly 40% feel they’re less likely to have a positive encounter with cops than other races.

via ZeroHedge News https://ift.tt/2DqB5n3 Tyler Durden

Additionally, the CDS markets are starting to price in an economy is on the verge of collapse,

A view, as we recentlky detailed, reaffirmed by the FT which writes that Turkey’s tourism sector – a key source of economic growth – continues to reel due to convid.

At this time of year, Murat Tugay, who runs the 240-room Hotel Aqua in the Mediterranean resort of Marmaris, should be dealing with a packed guestbook and all the challenges of peak season. Instead, the hotel is closed and Mr Tugay is banking on a late summer recovery. “We still have August. We still have September,” he says.

This implosion in Turkey’s tourism sector comes at a time when President Recep Tayyip Erdogan has been desperately seeking to assure the population (and much needed foreign investors) that all is well, hailing a sharp fall in interest rates and praised measures taken to block “malicious” attacks on the Turkish lira. Such steps, he said, were “strengthening the immune system of our economy against global turbulence.”

That could not be further from how most economists see the Turkish picture. The collapse in tourism as a result of the coronavirus pandemic has left a gaping hole in the country’s finances. Foreign investors have fled, pulling out a large volume of funds from the country’s local-currency bonds and stocks over the past 12 months.

In the face of those outflows, the country has burnt through tens of billions of dollars of reserves this year in a bid to maintain an unofficial currency peg – a move that marks a rupture with a two-decade policy of allowing a free float. But, in a sign that those efforts are floundering, as we showed last week, the lira lurched towards a record low against the dollar even as authorities spent billions trying to defend it.

And now, it appears that Turkey is running out of reserves to sell and “control” the lira, and instead it is resorting to the bazooka approach, one which it can use to nuke the occasional short here and there, but which in the longer run will cripple the Turkish economy, and merely accelerate its downfall.

And sure enough, after the lira briefly strengthened in the spot market on Tuesday – as a result of record surge in overnight rates – it has promptly plunged to a new record low again suggesting that it is no longer shorts that are in the driver’s seat, that Turkey’s panicked attempt to punish them will have little impact on the continued decline in the currency, and that a full blown currency crisis in Turkey may be about to hit.

Finally, things are not about to get any better for the ,as we noted recently, it is not surprising that young Turks in the 21st century do not want to be strangled by the unpredictable dictates of an Islamist regime. Erdoğan might sit down and ask himself: Why do the youths whom he wanted to make “devout” want to flee their Muslim country and live in “infidel” lands?

via ZeroHedge News https://ift.tt/33u5KdT Tyler Durden

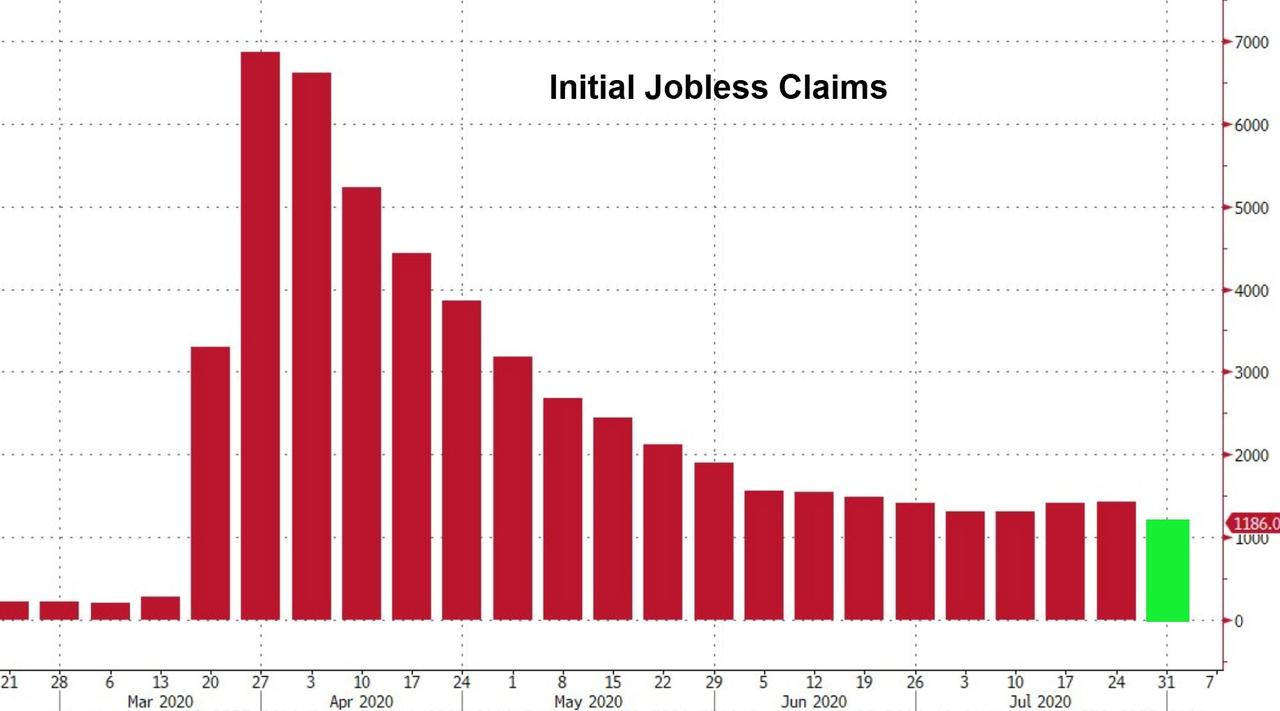

Ahead Of “Big Jobs Numbers”, Initial/Continuing Claims Offers ‘Positive’ Surprise Tyler Durden

Thu, 08/06/2020 – 08:37

Initial Jobless Claims was above a million last week for the twentieth straight week, but, after two straight week of rising, fell last week from 1.435mm last week to ‘just’ 1.186 million new Americans signing up for jobless claims for the first time.

Following yesterday’s plunge in ADP payrolls, Continuing Jobless Claims confounded and fell (improved) after rising last week for the first time in eight weeks…

A total of 55.31 million Americans have now applied for jobless benefits for the first time since the pandemic lockdowns began (that’s over 330 layoffs for every COVID death in America), and massively more than the 22.1 million during the great financial crisis.

When millions of Americans were losing their jobs at the beginning of this pandemic, we were told not to worry because the lockdowns were just temporary and virtually all of those workers would be going back to their old jobs once the lockdowns ended. Well, now we are finding out that was not even close to true. Over the last 18 weeks, more than 52 million Americans have filed new claims for unemployment benefits, and a very large percentage of them are dealing with a permanent job loss. In fact, one brand new survey discovered that 47 percent of all unemployed workers now believe that their “job loss is likely to be permanent”. The following comes from a USA Today article entitled “Almost half of all jobs lost during pandemic may be gone permanently”…

In April, 78% of those in households experiencing job loss felt that that situation would be temporarily. But now, 47% think that job loss is likely to be permanent, according to The Associated Press-NORC Center for Public Affairs Research.

What that number tells us is that we are facing the worst employment crisis since the Great Depression of the 1930s.

All of those permanently unemployed workers are eventually going to need new jobs, but meanwhile the U.S. economy as a whole is in a free fall that is absolutely stunning. On Thursday, we are scheduled to get the GDP number for the second quarter, and everyone is expecting that it will be really bad…

Data due Thursday are forecast to show U.S. gross domestic product plummeted an annualized 34.8% in the second quarter, the most in records dating back to the 1940s, after the spread of Covid-19 prompted Americans to stay home and states to order widespread lockdowns.

This downturn has been particularly hard on small businesses. Just check out these numbers…

Yelp reported 71,500 businesses that were listed on their site have closed for good since March 1.

80% of independent restaurants aren’t sure they’ll survive the COVID-19 pandemic.

Nearly half of all small-business members of the San Francisco Chamber of Commerce lost 100% of their sales or closed down completely.

What a nightmare.

But the third quarter was when the U.S. economy was supposed to come roaring back to life.

We were told that it would be the greatest economic comeback in our history, but instead the numbers are telling us that the economy is actually starting to slow down once again.

In fact, U.S. consumer confidence in July is much lower than it was in June…

U.S. CONSUMER confidence fell in July to a reading of 92.6 as coronavirus cases surged around the country, shuttering some bars and other businesses and raising concerns about the future of the economy.

The Conference Board reported Tuesday that the index fell in July from a reading of 98.3 in June. The drop is more significant than economists predicted, and is due mainly to a decrease in consumers’ economic expectations for the short-term future.

June was supposed to be the month of second-derivative beats in economic data, reaffirming the manic bid in stocks. For Wholesale Inventories it was not.

Against expectations of a rebound from a 1.2% drop in May to a 0.5% drop in June, wholesale inventories actually tumbled 2.0% MoM, the worst since the peak of the great financial crisis…

So it doesn’t look like any sort of a “recovery” is happening.

Instead, it appears that we are sliding into the next chapter of this new economic depression.

In June, 19 percent of all U.S. small businesses were closed, but now that number is up to 24.5 percent.

That certainly isn’t progress.

With each passing day, more companies are announcing layoffs. And every worker that gets laid off is another American that doesn’t have a paycheck to spend. During the last recession, millions of Americans slid out of the middle class, and we are watching it happen again.

Our elected leaders in Washington are desperate to do something about this, and almost all of them seem to agree that more socialist programs are the answer. A fifth “stimulus bill” is being put together but remains stuck in gridlock, and the Urban Institute is warning that if Congress does not hurry we could see the poverty rate in this country rise substantially…

Millions more Americans will be thrown into poverty if Congress fails to enact three policies meant to help families get through economic hardships related to the pandemic, according to a new study by the Urban Institute.

The report finds that the poverty rate for the last five months of 2020 will rise to 11.9% if expanded unemployment-insurance benefits, a second round of stimulus checks, and increased SNAP allotments are not approved, a significant increase over the projected annual rate of 8.9%.

If the Urban Institute thinks that an 11.9 percent poverty rate is bad, just wait until they see what things will be like in this country a few years from now.

Our entire system is in the process of melting down, but it will take some time for the drama that we are watching to fully play out. Our leaders in Washington and the bureaucrats over at the Federal Reserve will keep flooding the system with money in a misguided attempt to fix things, and this will result in exceedingly painful inflation.

The cost of everything (including essentials such as food) will be going way up, and that means that your money will increasingly become less and less valuable.

If you could print your way to prosperity, Venezuela and Zimbabwe would be the wealthiest nations on the entire planet today.

At this point, almost everyone in Venezuela is a “millionaire”, but almost everyone is also living in extreme poverty.

History has shown that wildly printing money doesn’t work, but the U.S. is going down the exact same path, and it isn’t going to be pretty.

Even though things are quite crazy out there right now, this is our window of opportunity to get prepared for the troubled times that are ahead, because things are not going to be getting any easier from here on out.

* * *

And with the latest round of virus relief continuing to be stuck in gridlock, we suspect things will get depressingly worse before they get better.

via ZeroHedge News https://ift.tt/3gC2Ya3 Tyler Durden

{kind=link}

{kind=link}

{kind=link}