Musk Publicly Praises China For Second Time This Month At Conference Held By China’s Cyberspace Administration

The latest leg of Elon Musk’s China ass kissing tour commenced this weekend in the form of a pre-recorded stream at the World Internet Conference, which was hosted by the Cyberspace Administration of China.

This marks the second instance this month where Musk took an opportunity to praise China for its work in the EV space.

Musk said that China was the “global leader in digitalization” during the event, CNBC reported.

Musk also continued by saying that Tesla would be expanding their investments in China: “My frank observation is that China spends a lot of resources and efforts applying the latest digital technologies in different industries, including the automobile industry, making China a global leader in digitalization. Tesla will continue to expand our investment and R&D efforts in China.”

The Tesla CEO also called out data protection, reassuring those listening that Tesla stores certain types of data locally.

“At Tesla, we are glad to see a number of laws and regulations that have been released to strengthen data management,” Musk said.

He continued: “Tesla has set up a data center in China to localize all data generated from our business here, including production, sales, service and charging. All personally identifiable information is security stores in China without being transferred overseas. Only in very rare cases, for example, spare parts orders from overseas is data approved for transfer internationally.”

We don’t know about you, but that sure makes us feel better.

Recall, we pointed out days ago when Musk praised Chinese automakers – also known as Tesla’s competition – as “the most competitive in the world”. Musk also said China had “great potential” as a nation for electric vehicles.

In another pre-recorded appearance at the World New Energy Vehicle Congress, Musk said: “I have a great deal of respect for the many Chinese automakers.”

Data security was also a topic Musk talked about, stating that it was the “cornerstone” of the EV industry as it develops.

Then Musk appeared to make a backhanded allusion that Tesla would be turning over whatever data the CCP wanted: “Tesla will work with national authorities in all countries to ensure data security of intelligence and connected vehicles. With the rapid growth of autonomous driving technologies, data security of vehicles is drawing more public concern than ever before.”

Musk continued: “Public sentiment and support for electric vehicles is at a never before seen inflection point because they know it is the future.”

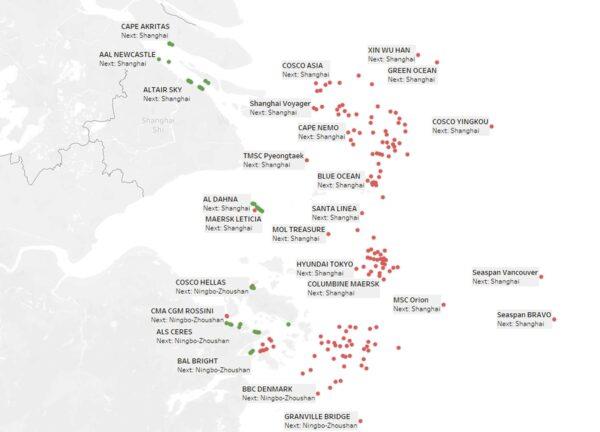

There are over 60 container ships full of import cargo stuck offshore of Los Angeles and Long Beach, but there are more than double that — 154 as of Friday — waiting to load export cargo off Shanghai and Ningbo in China, according to eeSea, a company that analyzes carrier schedules.

The number of container ships anchored off Shanghai and Ningbo has surged over recent weeks. There are now 242 container ships waiting for berths countrywide. Whether it’s due to heavy export volumes, Typhoon Chanthu or COVID, rising congestion in China is yet another wild card for the trans-Pacific trade.

Congestion in Chinese ports that slows the flow of exports is bad news for U.S. importers but it could temporarily alleviate pressure on the ports of Los Angeles and Long Beach.

“The devil in these things is the whiplash effects,” Simon Sundboell, founder of eeSea, told American Shipper. “What you’d rather have is more stability, not these swings, and I think what everybody fears is that the swings will become even more volatile. When the system is already this stretched, all of these unexpected events can be a causal factor in congestion.”

Ships follow the money

A major driver of congestion on both sides of the Pacific Ocean: Landside capacity (terminals, trucking, rail, warehousing) is limited, but the vessel capacity of a single ocean trade lane is highly flexible.

While the number of ships in the world is finite, operators can shift ships to wherever they make the most money. And the trans-Pacific is now a particularly lucrative trade: Spot rates including premiums can top $20,000 per forty-foot equivalent unit (FEU).

“These assets [ships] are super-mobile,” said Sundboell. “What’s happening now is the opposite of what dogged the industry for the past 20 years. Five years ago, people were asking: How can the trans-Pacific rate drop from $2,000 to $1,500 [per FEU] in the space of just six days? It was because you could take a vessel from one place and sail it someplace else, and suddenly there were more ships and a price war and rates dropped.

“Now we’re seeing the opposite,” he said. As ship operators pile more capacity into the trans-Pacific, congestion rises, delays mount, the incentive for shippers to pay premiums is supported, and all-in rates remain at record highs.

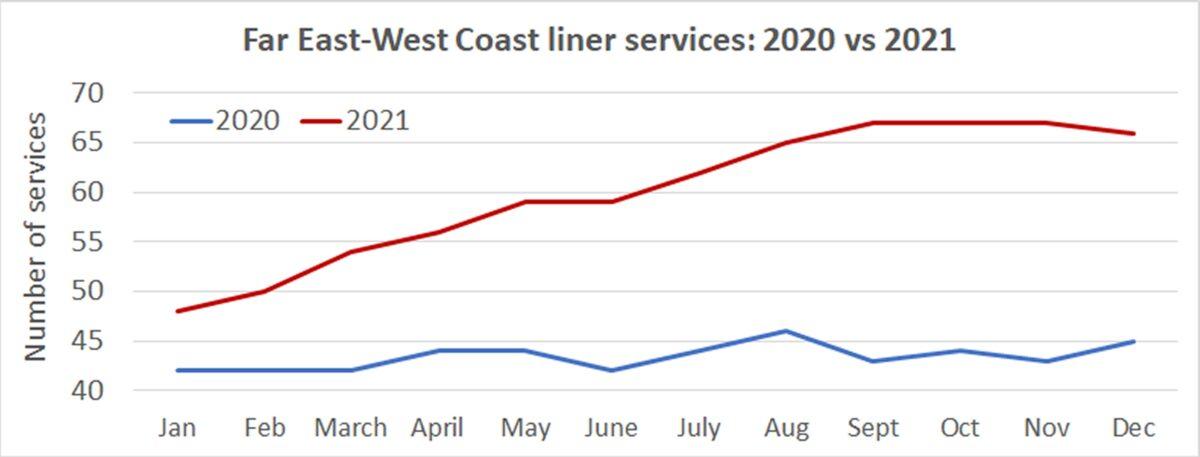

Surging number of services

According to eeSea, the number of Far East-West Coast services has surged from 48 in January to 67 this month. In contrast, the number of services on this lane stayed fairly steady last year, at 42-46.

In addition, ships are being drawn from other trades to serve as “extra loaders” (ships that perform one-off voyages). In some cases, multiple ad hoc ships are doing multiple round trips — a hybrid of an extra loader and a scheduled service.

“We’re definitely seeing carriers pulling ships from Asia-Middle East and Asia-Africa and putting them into the trans-Pacific trade,” said Sundboell.

“Whether it’s for one round trip as an extra loader or whether it becomes semipermanent, I don’t even think the carriers know themselves right now. They’re just playing the market and if it makes more economic sense to take a ship from the Middle East and put it in the trans-Pacific, they’ll do it, whether it’s for one month, three months or six months — which is why nobody knows what this network is going to look like six months from now.

“The line managers in Copenhagen and Geneva and Marseille are looking at yields per container and costs per container. And not just per container. They’re looking at it per day, and per container-TEU [twenty-foot equivalent per]-mile.”

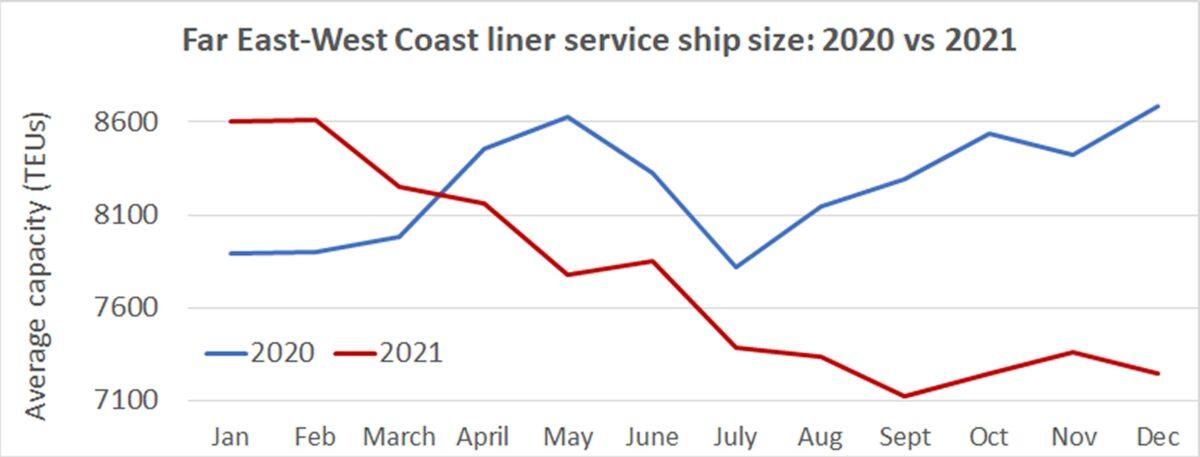

Trans-Pacific ships getting smaller

Yet another driver of increased trans-Pacific congestion: There are not only more ships, but the ships are getting smaller, meaning that more vessels are needed to carry the same TEUs.

According to eeSea, the average capacity of ships serving Asia-West Coast services was 8,601 TEUs in January and is 7,125 TEUs currently, a decrease of 17%.

Smaller average vessel size “would definitely slow things down further,” said Sundboell.

Some operators have added trans-Pacific capacity by buying ships in the secondhand market or leasing them in the charter market. Most of the ships available for purchase or charter in 2021 have been in smaller size categories.

Liner companies’ switching of capacity from other trades is also pulling down average size, because the trades being cannibalized use lower-capacity ships. “The reason you have smaller vessels coming in is that they’re taking them from the Middle East and Africa trades,” said Sundboell.

How does this end?

Ship operators can put as many ships as they want into the trans-Pacific to chase record spot rates, leaving other trades short. But ultimately, the imbalance should self-correct.

“It becomes something that balances itself out,” explained Sundboell, noting that if ships are removed from other trades, rates in those trades would rise to the point where it would entice ships back.

“At a certain point, the rates of the trades you’re leaving increase too much or the cost of having the ships sitting at anchor becomes too much [in terms of lost future cargo],” said Sundboell.

In Q1, when anchorages filled off Los Angeles/Long Beach, carriers were unable to get enough ships back to Asia in time to load cargo, so they had to “blank” (cancel) a large number of sailings, which reduced congestion in Q2.

Given the extreme anchorage situations both off China and Southern California, a repeat of the blank-sailing scenario seems likely in Q4 – a worrisome prospect for importers.

Lack of visibility

But even companies like eeSea that track blank sailings cannot definitely say what will happen in Q4.

In the first half of 2020, when carriers were blanking sailings due to lockdown-induced demand drops, they announced voyage cancellations months in advance, providing an important signal to the market. This year, there is far less notice, because blank sailings are being caused by congestion, not lower forward demand.

According to Sundboell, “For November, there are only eight blank sailings [on Asia-West Coast] and only three in December, but that is just because the carriers have not communicated them yet. We only put a blank sailing into our system when it is confirmed by the carrier.”

Pre-COVID, he said, carriers believed they were tied down by long notice periods for service changes. “But corona gave them a platform to take out capacity with short notice,” said Sundboell. “Now they’re trying to get more capacity in, but they’ve definitely taken the liberty of being both more volatile with their capacity and with the ‘forecasting’ of their service.

“And I think that’s what’s causing the frustration among the BCOs [beneficial cargo owners; the shippers]. A BCO hates having to be forced to get used to the fact that the vessel is always 10 days late — or that they won’t even know when it’s coming. I don’t think that’s what the carriers are aiming to do, but they’ve certainly found wiggle room to change services on short notice that they’ve never had before.”

Lawyers & Scientists Are Building A Case For Why Natural Immunity Should Be Treated Same As Vaccination

Now that at least one employer in the health-care field – Michigan’s Spectrum Health – has decided to accept proof of natural immunity from prior infection as reason to waive its vaccination mandate for all employees, legal expert (and the reporters who love to quote them) are wondering: will the legality of proving natural immunity potentially win out in court?

The answer to that question, they say, will depend – as all things COVID-related do – on “the science”, that nebulous and frequently shifting concept of how prior infection impacts immunity to new variants (and whether vaccine’s do as well).

According to a report in Yahoo Finance, the notion that natural immunity is superior is already gaining support in the legal world. Presently, a handful of studies from different countries offer a conflicting view of whether natural immunity actually is superior to vaccinated immunity, or a combination of prior infection and vaccination

Since it’s likely the federal government’s aim to roll out vaccine mandates that cover practically every US worker (they’re not too far off already), the issue of natural vs. vaccine immunity and whether some individuals should receive exemptions based on their antibody levels almost certainly be adjudicated in the federal courts.

“I think that a judge might reject a rule that’s been issued by a body, like the U.S. Department of Labor or by a state, that has not been sufficiently thought through as it relates to the science,” Erik Eisenmann, a labor and employment attorney with Husch Blackwell, told Yahoo Finance.

As we reported when it was first published,a report out of Israel suggests that natural immunity could be many times more effective than the Pfizer vaccine at preventing infection with the delta variant. That study has yet to be peer-reviewed, however, and the world is anxiously awaiting the results.

However, another peer-reviewed study cited by the CDC looks at dozens of cases in the US where certain people who tested positive for COVID never ended up generating the antibodies, which, science dictates, are necessary to fend off future infection.

The CDC also published a study of 246 Kentucky residents, concluding that vaccination offers higher protection than a previous COVID infection. The CDC said the study went through a “rigorous multi-level clearance process” before submission, but now some are concerned it’s slightly out of date since it pre-dates the rise of delta.

But as far as supporting natural vs. vaccinated immunity goes, this study is another big one: A C A June study by the Cleveland Clinic and Washington University tracked 52,238 Cleveland Clinic employees found that within 1,359 previously infected and unvaccinated people, none contracted a subsequent COVID-19 infection over the five-month study. The findings led authors to conclude that prior infection makes a person “unlikely to benefit from COVID-19 vaccination.”

Then there’s this:

In a smaller study conducted by Washington University School of Medicine and published in Nature, senior author Ali Ellebedy, PhD, an associate professor of medicine and of molecular microbiology, found antibody-producing cells in the bone marrow of 15 of 19 study subjects 11 months after their first COVID-19 symptoms. “These cells will live and produce antibodies for the rest of people’s lives. That’s strong evidence for long-lasting immunity,” Ellebedy said.

The legal and scientific standards are intertwined here, but as more data develops that appears to validate the argument that natural immunity is at least as effective as vaccinated immunity, it’s more likely that lawyers will succeed in convincing judges that the standard should be “immunity by any means.”

Arizona Senate Hears Of Multiple Inconsistencies Found By Election Audit

Authored by Jack Phillips and Mimi Nguyen Ly via The Epoch Times (emphasis ours),

Arizona lawmakers were told on Friday during a hearing on an audit conducted in the state’s most populous county of inconsistencies uncovered during a forensic audit into the 2020 election.

The Maricopa County audit was commissioned by Republicans in the Arizona Senate.

Senate President Karen Fann, a Republican, issued a letter on the same day to Arizona Attorney General Mark Brnovich recommending further investigation following the audit’s findings. In the letter, she raised concerns over signature verification on mail-in ballots, the accuracy of voter rolls, the securing of election systems, and the record-keeping of evidence related to the elections.

“I am therefore forwarding the reports for your office’s consideration and, if you find it appropriate, further investigation as part of your ongoing oversight of these issues,” Fann told Brnovich in the letter.

Brnovich, a Republican running for the U.S. Senate, said in a statement, “I will take all necessary actions that are supported by the evidence and where I have legal authority. Arizonans deserve to have their votes accurately counted and protected.”

His office said that its Election Integrity Unit “will thoroughly review the Senate’s information and evidence.” Specific allegations cannot be commented on until the review is complete, the office added.

Fann said Friday at the hearing that the audit had faced unnecessary obstruction from Maricopa County officials, who went to court in a bid to try to block the audit and subpoenas from the state Senate. While the forensic audit did not uncover a significant difference in the total vote tallies—the difference was only hundreds in the final report— evidence was uncovered of numerous other anomalies, including statutes being broken and chain of custody not being followed, Fann added.

Cyber Ninjas, a Florida-based company hired by the state Senate to conduct the audit, said its review involved over 1,500 people and a total of over 100,000 hours. While the company said it only found in the recount a vote discrepancy of 994 in the presidential race and 1,167 in a U.S. Senate race, the report highlighted potential issues with a combined total of 53,305 ballots.

Maricopa County on Friday issued a series of statements on its Twitter page in response to findings laid out in a purported draft audit report of Cyber Ninja’s forensic audit that had been released ahead of the Senate audit hearing.

The draft audit report’s figures did not entirely correlate with that of Cyber Ninja’s final report. Fann said Friday at the hearing, “As you know somebody leaked one of the draft reports out over the last 24-48 hours. It was a draft report, so I can tell you that what’s in that is not entirely what’s in the final report.” However, some key allegations in the draft report regarding ballots did match that of the final report.

According to the Cyber Ninjas’ final report, 23,344 mail-in ballots were received from voters’ previous addresses.

“Mail-in ballots were cast under voter registration IDs for people that may not have received their ballots by mail because they had moved, and no one with the same last name remained at the address. Through extensive data analysis we have discovered approximately 23,344 votes that may have this condition,” the report states.

Cyber Ninjas noted in its report that if ballots are sent by forwardable mail, this would violate the Arizona Elections Procedures Manual.

“The Senate should consider referring this matter to the Attorney General’s Office for a criminal investigation as to whether the requirements of ARS 16-452(C) have been violated,” the company stated in the report.

Maricopa County refuted the allegation on Friday, saying, “Mail-in ballots are not forwarded to another address.” It also asserted that voting from a previous address “is legal under federal election law,” such as in the case of American military and overseas voters. The county also said it had 20,933 one-time temporary address requests for the 2020 general election.

9,041 More Ballots Returned by Voter Than Received

Cyber Ninjas found that 9,041 more ballots were returned by voters than were sent to them.

According to the report, “9,041 more ballots show as returned in the EV33 Early Voting Returns File for a single individual who voted by mail than show as sent to that individual within the EV32 Early Voting Sent File.” “In most of these instances, an individual was sent one ballot but had two ballots received on different dates.”

Auditors later noted they were told that some of the discrepancies “could be due to the protected voter list,” but were not able to validate that. Maricopa County released a statement to similar effect on Friday.

The county disputed the finding on Twitter, saying the majority of times when there are multiple entries in the EV33 file are when voters “returned a ballot without a signature or with a signature discrepancy,” and in such cases, election staff contact the voter.

Cyber Ninjas: Voters Potentially Voted in Multiple Counties

Cyber Ninjas noted that some 5,295 ballots were affected by voters who potentially voted in multiple counties.

The company said that it had compared Maricopa County’s list of all its voters who cast a ballot in the election (also referred to as the VM55 Final Voted File) to the equivalent files of the other 14 Arizona counties, to find a total of 5,047 voters with the same first, middle, last name, and birth year, representing some 10,342 votes among all the counties.

“The Ballot Impacted was calculated by the total number of votes (10,342) and subtracting the number of maximum number of potential unique people (5,047). This yielded 5,295,” the report said.

Separately, the company found that the number of ballots tallied in the official Maricopa results were 3,432 more than the total number of people who voted.

“The official result totals do not match the equivalent totals from the Final Voted File (VM55),” Cyber Ninjas said (P12).

Cyber Ninjas said the finding is significant because “the number of individuals who showed up to vote should always match the number of votes cast.” The company recommended that legislation “that would require the Official Canvass to fully reconcile with the Final Voted File” should be considered.

Cyber Ninjas said in another finding that there were 2,592 more duplicate ballots than original ballots sent to duplication—a process for replacing damaged or improperly marked ballots with a new ballot that preserves the voter’s intent.

“This is probably one of the more interesting parts … that we had more duplicates than original ballots,” Cyber Ninjas CEO Doug Logan said in his presentation on Friday. “According to our counts from our audit, we had 26,965 original ballots and we had 29,557 that were duplicate ballots, and those numbers should be the same.

“Based on the numbers received from Maricopa county, we should have had 27,869 of both originals and duplicates and they should have matched up perfectly,” he added.

Other findings of the ballots impacted included 2,382 in-person voters who had moved out of Maricopa County, and 2,081 voters who moved out of state during the 29-day period preceding the election. Responding to the findings, the county said it had completed separate spot checks and found “no discrepancies” for either of the figures.

Cyber Ninjas also reported that there were 1,551 votes counted in excess of voters who voted, as well as a slew of other categories of findings that affected a smaller number of ballots, such as 397 mail-in ballots sent without there being a record of them having been sent, 393 ballots that had incomplete names, 282 votes cast by individuals who “were flagged as deceased,” and 198 votes cast by individuals who registered to vote after the Oct. 15 deadline, among other smaller categories.

17,322 Duplicates of Early Voting Ballot Return Envelopes

Shiva Ayyadurai, who was commissioned by the Senate to “check the signatures or lack thereof” on the early voting ballot (EVB) return envelopes, said during Friday’s presentation that the audit “reveals anomalies raising questions on the verifiability of the signature verification process.”

Ayyadurai said that his team was hired only to verify whether the envelopes contained a signature—not whether the actual signature matched that of the voter in question.

Of the 1,929,242 return envelopes provided by the Senate, 17,322 duplicates were found, with some voters having cast the same ballot three to four times, according to Ayyadurai’s report (pdf). He noted that Maricopa county’s canvass report, meanwhile, did not report any duplicates.

In response to duplicated ballot allegations, Maricopa County wrote Friday, “Re: duplicated ballots. Every time a voter has a questioned signature or a blank envelope, we work with that voter to cure the signature. That’s our staff doing their job to contact voters with questioned signatures or blank ballots. Only one ballot is counted.”

Among other several key findings, Ayyadurai noted that over 25 percent of the duplicate ballots were received between Nov. 4 and Nov. 9, 2020.

Auditors stated in their report that “according to the Master File Table (MFT) of the drives, a large number of files on the Election Management System (EMS) Server and HiPro Scanner machines were deleted.”

“These files would have aided in our review and analysis of the election systems as part of the audit,” the report reads. “The deletion of these files significantly slowed down much of the analysis.”

Maricopa denied the allegation in a Twitter post on Friday, saying, “Maricopa County strongly denies claims that @maricopavote staff intentionally deleted data.” The county also said it has “backups for all Nov. data & those archives were never subpoenaed.”

While auditors finished part of the audit that deals with the ballots, they say an evaluation of voting machine equipment is ongoing.

“Because the Maricopa County Board of Supervisors and the Arizona Senate have recently settled their dispute concerning outstanding subpoena items, this portion of the audit is not yet complete,” the Cyber Ninjas’ report states.

Response to Findings

Jack Sellers, Chair of the Maricopa County Board of Supervisors, said in a statement in response to the Senate audit hearing, “The Cyber Ninjas’ opinions come from a misuse and misunderstanding of the data provided by the county and are twisted to fit the narrative that something went wrong.”

“Once again, these ‘auditors’ threw out wild, damaging, false claims in the middle of their audit and Senate leadership provided them the platform to present their opinions, suspicions, and faulty conclusions unquestioned and unchallenged. Today’s hearing was irresponsible and dangerous.”

Arizona Democrats, meanwhile, pounced on the auditors’ report.

“The Cyber Ninjas embarrassed Arizona for months, violated voters’ trust, refused transparency, and stuck AZ taxpayers with a multi-million dollar bill. What’d they find? Biden won,” Secretary of State Katie Hobbs, a Democrat who has frequently criticized the audit and is trying to become Arizona’s next governor, wrote on Twitter. “The so-called leaders who allowed and encouraged this need to be held accountable in 2022.”

But Fann has long said that the goal of the audit was to improve Arizona’s election system and wasn’t designed to overturn the results.

“Our No. 1 goal is to make sure those laws are followed,” Fann said during Friday’s hearing, adding that there are “a lot of people” with questions about the state’s election integrity. Citing a poll, Fann said that 45 percent of Arizona’s voters had significant distrust in the election system.

Ahead of the official release of the report on Friday afternoon by the state Senate, Trump said the audit uncovered “significant and undeniable” fraud in the 2020 presidential election.

“The audit has uncovered significant and undeniable evidence of fraud!” he said in an emailed statement. “I have heard it is far different than that being reported by the fake news media.”

Trump added, “Until we know how and why this happened, our elections will never be secure. This is a major criminal event and should be investigated by the Attorney General immediately.”

Arizona was one of several key swing states, including Georgia, Pennsylvania, Nevada, Michigan, and Wisconsin, that were certified for Biden during the Nov. 3 election. Trump won those states, with the exception of Nevada, in 2016. According to official results, Biden won Arizona over Trump by a margin of just over 10,000 votes.

Maricopa County hasn’t responded to The Epoch Times’s request for comment.

Despite Record Cargo Backlogs, Ports Of L.A. And Long Beach Still Don’t Operate Around The Clock

Some of the busiest U.S. ports, including many in California, are still struggling with how to deal with significant cargo backlogs.

Yet, despite the backlog, the busiest U.S. port still shuts down for hours on most days and is closed on Sundays, the Wall Street Journal reports. “Tens of thousands” of containers remain stuck at the ports of Los Angeles and Long Beach. More than 60 ships are lined up to dock, the report says.

More than 25% of all American imports pass through one of the two ports. LA and Long Beach collectively manage 13 private container terminals. Long Beach officials finally said last week they would try operating 24 hours a day between Monday and Thursday. LA says it’s going to keep existing hours and wait for the rest of the supply chain to extend their hours first.

Gene Seroka, executive director of the larger Port of Los Angeles, said: “It has been nearly impossible to get everyone on the same page towards 24/7 operations.”

Ports in places like Asia and Europe, for contrast, have operated around the clock “for years”, the report notes.

Uffe Ostergaard, president of the North America region for German boxship operator Hapag-Lloyd AG said: “With the current work schedule you have two big ports operating at 60%-70% of their capacity. That’s a huge operational disadvantage.”

As the shortage continues, all members of the supply chain including truckers, warehouse operators and railways, are blaming each other for the shortages of products. All parts of the supply chain are also struggling with a shortage of labor.

A longshore shift at either of the two ports used to be either 8AM to 4PM or 6PM to 3AM. Overnight shifts of 5 hours were “rarely used” because they are up to 50% more expensive, the report says.

The International Longshore and Warehouse Union says their members will work a third shift, but only after the pileup of containers is fetched out of the port so there is space.

Frank Ponce De Leon, a coast committeeman at the ILWU, said: “Congestion won’t be fixed until everyone steps up and does their part. The terminal operators have been underutilizing their option to hire us for the third shift.

Meanwhile, elsewhere in the supply chian, Federal safety regulations prevent commercial truck drivers to 11 hours of driving in a 14 hour workday. Port truckers like to start early in the morning so they can maximize the number of loads they can transport in a day.

Tom Boyle, chief executive of Quik Pick Express LLC, a trucking and warehousing provider, told the Journal: “The biggest issue it probably comes down to is labor.”

Rail operator Union Pacific says it sees most delays when it picks up cargo from ports and hands it to trucks at destinations.

Wim Lagaay, chief executive of APM Terminals North America, who operates at the port of LA, said: “If you work a gate 24/7 it will improve your velocity. Up to 30% of overall truck appointments are not met because there are not enough trucks, drivers or chassis.”

Matt Schrap, chief executive of the Harbor Trucking Association, added: “There is too much congestion from empty containers on terminals. The shipping lines aren’t moving the boxes out, which is preventing us from returning empties that we are storing in our yards.”

Mario Cordero, executive director at the Port of Long Beach concluded: “It’s impossible to effectively move such volumes if we don’t move to 24/7 operations across the supply chain. They do it in other parts of the world.”

More people than usual made the trip all the way over here to my blog to be sure to tell me how clueless I am and there was a lot of defeatism in the comments on Zerohedge that all converged around a theme that governments will simply not permit the use of cryptocurrencies once their existence ceases to suit them.

I’ve been involved in cryptos since 2013, and for a long time I too was strategizing out the game theory around why would governments permit cryptos to gain traction.

It wasn’t until relatively recently, that I started to fully grasp something I read a long time ago, before all this crypto business ever started. It was in a rather obscure book by one W R Clement called Quantum Jump: A survival guide for the new Renaissance and it helped me understand the key point of today’s post.

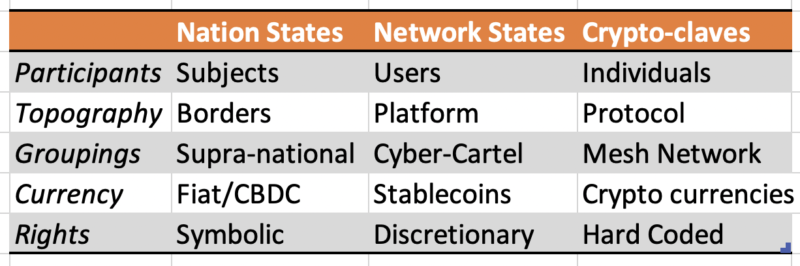

I started alluding to it in A Network State Primer that described how what we understand as “the nation state” is in the process of losing relevance to ascendent network states and crypto-claves. You can chart out the structural differences between those three different governance models based on what the architecture of the monetary layer is:

When it comes to technological leaps like the internet and then public key cryptography and decentralized, non-state, sound money; those who eschew the new paradigms generally do so because they have difficulty fitting the new model into their worldview.

People like Alvin Toffler called this “Future Shock” and he ascribed it mostly to an accelerating rate of change. He wasn’t wrong about that, but what Clement layered atop of that was the ascending level of abstraction.

In the 1400’s the seemingly innocuous discovery of perspective opened the floodgates to the Gutenberg Press and double-entry accounting which opened the path for the Renaissance, the Enlightenment and the Industrial Revolution. Each revolution occurred despite the objections of the incumbent power structures of their day, and that made for volatile, even violent transitions.

In the mid-90’s people were trying to wrap their heads around “cyberspace”. Somebody once wrote in Mondo2000 (I can’t remember who it was, sorry) that “cyberspace is where you are when you’re on the phone”. Meanwhile US lawmakers were calling the internet “a series of tubes”.

That contrast results from differing levels of abstraction.

Which brings us to the entire point of today’s post.

Levelling up to the next plateau of abstraction alters the architecture of the intellectual constructs upon which systems are based. What worked at the lower level of abstraction not only doesn’t work at the higher abstraction levels, it malfunctions. Clinging to it creates absurdities. Atrocities.

Further, once the level of abstraction jumps, it is the proverbial Promethean dynamic. In this chapter of history, Satoshi has stolen the secret of fire from the Gods and given it to the people. (He did so anonymously, I presume, in an effort to avoid the part where his gizzard is eaten by vultures for all eternity).

But it’s done now, humanity possesses the secret of decentralization and cryptography and nothing short of a complete and total system collapse can undo the newfound cognitive horizons that will accompany it. If society stays on the rails, then the new model will keep spreading at that higher level of abstraction and it will keep accelerating.

In other words, now that cryptos have created non-state, decentralized, open source money, the dynamics of finance and economics have irrevocably changed, and there’s nothing the priests of the temple at The Fed can do about it.

Any attempt by nation states and central banks to preserve the old system, to extend the lifespan of their fiat currencies by porting them into digital forms like CBDCs are simply trying to linearly extrapolate something into a landscape that has fundamentally changed. Faster horses in a new era of cars.

This is what no-coiners do not understand, granted, because many of them are engaged in livelihoods which depend on them not understanding it:

It is not a question of whether governments will permit Bitcoin and cryptocurrencies to exist.

It is a question of whether governments can successfully adapt to the new reality created by the dawning of the decentralized era.

So while policy makers can and will regulate the on-ramps and off-ramps (the exchanges), this is to be expected and it’ll be around these chokepoints where some sort of equilibrium between these two monetary universes will take form.

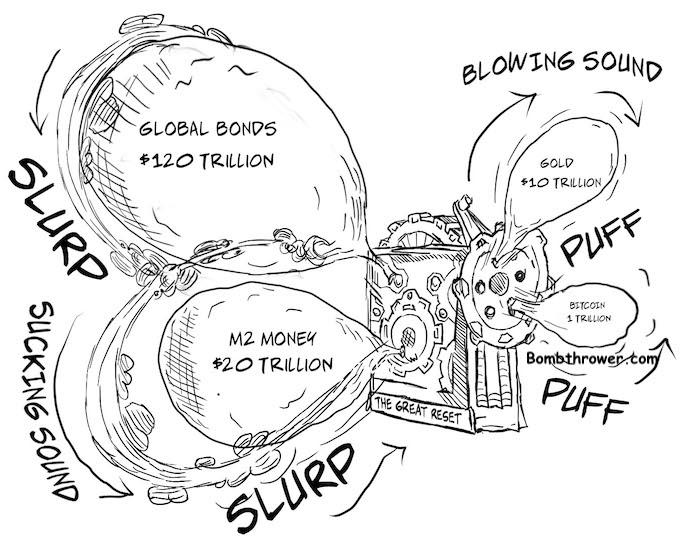

This diagram depicts the core thesis of The Crypto Capitalist Letter. It’s that the institutionalized financial repressions of NIRP, ZIRP, targeted inflation and coming regimes of UBI, MMT and CBDC-driven social credit are such that capital will exodus from the global bond and fiat bubbles over into the anti-fiat world. Anti-fiat includes gold and silver, it includes real estate, income producing businesses, commodities, intellectual property and cryptos.

It is true that regulations can ramp up and clamp down and become more repressive, for awhile. But as we’re seeing in the world today, the pandemic emergency response is wearing thin and people’s patience for things like lockdowns and mandatory vaccinations is beginning to wane. Here in the West, people were willing to have their freedoms curtailed to meet the exigencies of a global crisis, but they will not countenance government overreach as a way of life. In an ironic sense, the kind of Big Government that may have previously taken decades to creep into intolerable levels may have just accelerated its own rejection and obsolescence with the near ubiquitous, rampant mishandling of COVID.

No matter what happens, the nation state monopoly over the issuance of money is over. That’s why it really doesn’t matter if governments “ban” cryptos. Increasingly higher levels of wealth and capital that are moving into the crypto economy are on a one-way mission: it has no intention of ever returning to the fiat side of the system.

China Bans Advertisements For ‘Cosmetic Beauty’ Loans

A few weeks ago, Beijing abruptly scrubbed one of China’s most famous actresses from the Chinese Internet, then outlawed the portrayal of “sissy men” – that is, men dressed effeminately, weak or woman-like (the South Korean boy band sensation BTS comes to mind) in Chinese movies and TV.

Now, as President Xi pushes China to embrace more elements of its Marxist-Leninist founding principles, another cosmetics-related order comes down from on high.

This time, Reuters reports that China on Monday banned advertisements for so-called “medical beauty loans” from playing on televisions, radios and online platforms, saying such advertisements enticed young people with low interest rates, while misleading consumers and causing other “adverse effects”.

With the Evergrande debt crisis still in the news, the timing of this latest crackdown is interesting. It seemingly kills two birds with one stone. It’s pressing back against cosmetic surgeries which are becoming increasingly popular in the US and China. Many original Communists looked down on makeup and fashion, and cosmetic surgery likely would have been forbidden in many early Communist societies. It was once said that the original Bolsheviks didn’t wear makeup.

Beijing has also recently cracked down on out-of-control online fandoms where fans sometimes would even have plastic surgery to look more like their idols.

As one CNBC reported out, the decision to ban advertisements for these types of loans might not have been on anyone’s ‘bingo card’ for what Beijing might do next.

Medical beauty loans def wasn’t in my bingo card for what China will go after next

Also: if they did this in Lebanon that would truly be the end of the nation https://t.co/X74hPfirS4

President Biden and his allies in Congress are having a rough time winning support for a new, historic, gigantic spending plan, but they knew who to call for help.

On Friday, Gov. JB Pritzker joined Biden on a Zoom call to with local reporters to make the case for the pending federal legislation.

You may know the bill as the “$3.5 infrastructure bill,” which is what it has been commonly called in the media.

But that’s just a testament to media distortion. It’s not $3.5 billion and it’s not infrastructure.

A primary gimmick being used, it said, is pretending that programs intended to be permanent expire, which they say obscures “the true cost of the legislation and put program beneficiaries at risk.”

A Wall Street Journal editorial detailed various “time shift gimmicks” and also explained how some states will be stood up for paying, on their own, part of the cost of new, universal pre-K entitlement and free community college. Hence, their preface: “Behold one of the greatest fiscal cons in history.”

“The press has reported almost none of this,” said the Journal about the phony cost estimates.

The Biden’s Administration’s answer to the cost issue is astonishing, even by its standards. The cost is actually “zero,” they say. Biden himself said the cost is “nothing.” On what basis? They claim they will raise taxes enough to cover the cost.

How’s that for chutzpah? As long as you are billing taxpayers, you can say it costs nothing.

And infrastructure is only a small part of what it’s about, even by CNN’s charitable description: “The sweeping 10-year spending plan marks the biggest step in Democrats’ drive to expand education, health care and childcare support, tackle the climate crisis and make further investments in infrastructure.”

The bill in fact includes a massive expansion of multiple government dependency programs, which CNN tried to list, based on “what we know so far,” as they candidly put it last week. Does anybody really know besides a few insiders?

Adding to the guesswork, House Speaker Nancy Pelosi signaled over the weekend that the size of the bill may be negotiated down, but she also said the first vote may come as early as today, Monday. If that happens, don’t expect most members of Congress to have an honest understanding of what they will be voting on.

What’s most troubling is the timing of the expansion of dependency programs. If ever there was a time to move people out of government dependency and into employment it is now. It doesn’t get any better than this. Jobseekers today have the best job market in American history – over 10 million jobs are unfilled while just 9 million are unemployed. Many employers are desperate for workers. The bill’s supporters, however, measure success by how many can be added to government programs.

The U.S Chamber of Commerce has it right: “This reconciliation bill is effectively 100 bills in one representing every big government idea that’s never been able to pass in Congress,” Chamber President and CEO Suzanne Clark said. “The bill is an existential threat to America’s fragile economic recovery and future prosperity. We will not find durable or practical solutions in one massive bill that is equivalent to more than twice the combined budgets of all 50 states.”

Getting back to the Pritzker and Biden Zoom call with local reporters, why did they do it that way? Why not also release the tape of the call so we could see for ourselves? Instead, we got only the media’s post-digestion remains. Dare I say that we should be suspicious of how Biden and Pritzker deal with questions and the media, and with what comes out at the end?

If the subsequent reports in Crain’s and the Chicago Tribune are correct, Pritzker spoke primarily about the expansion of benefits directed toward children. One is child care, lack of which “is holding back our recovery,” he said.

Child care costs no doubt have always been a problem that keep some people from working, but did it occur to any of the reporters on the call to ask Pritzker this: Why would child care be more of an issue today, with the state’s unemployment rate at 7%, than it was before the pandemic when the rate was under 4%? To our knowledge, nobody ever asks that question.

And think about the expansion of the per-child tax credit in the pending legislation, which is the most expensive element in the bill. In concept, that’s a popular idea and has significant bipartisan support, primarily because it is projected to lift many out of poverty. The credit would be for $3,000 to $3,600 per child, depending on age.

But it’s hardly for the poor alone. The credit does not even begin to phase out until relatively high income levels — $75,000 for single parents and $150,000 for married couples. There would be no work requirement to get the credit, and the pending bill would end long-standing rules requiring a child to be a relative of the person taking the credit, as CNBC reported. Instead, whoever is caring for the child could take the credit, regardless of whether they’re related. Seems like a formula for abuse and a step toward making the federal government the family provider.

Whatever the issues are with the pending legislation, Pritzker undoubtedly is thrilled with the prospect of more federal cash flowing into Illinois. That would allow him to kick the can again on addressing the state’s structural deficit, and continue to announce program after program of new spending as he has been doing recently with federal assistance already received.

Biden Gets Booster Shot, Says 97% Of Americans Need To Be Vaxx’d To Return To Normal

Just like he did when he received his first jab last year (before he was president), President Joe Biden, 78, posed for the cameras on Monday as he received his first booster jab while cameras clicked and flashed, and he delivered some brief remarks to the public.

The FDA granted an emergency use authorization last week for booster doses of Pfizer’s COVID-19 vaccine six months after the completion of the two-dose course for those 65 and older, those with some underlying conditions and those who work in high-risk environments. The Centers for Disease Control and Prevention also recommended a booster shot for these groups of people.

Video of Biden’s third inoculation circulated widely on Twitter Monday. Before he received the jab, Biden delivered a brief statement, claiming the White House is preparing for a possible government shutdown as leaders struggle to pass a budget by the end of this month.

Speaking on Monday, Biden emphasized that even though booster shots are important, getting fully vaccinated with the two-dose regimen is even more so.

“Let me clear. Boosters are important. But the most important thing we need to do is get more people vaccinated,” the president said before getting his jab. “The vast majority of Americans are doing the right thing. Over 77% of adults have gotten at least one shot. About 23% haven’t gotten any shots, and that distinct minority is causing an awful lot of us an awful lot of damage for the rest of the country. This is a pandemic of the unvaccinated. That’s why I’m moving forward with vaccination requirements wherever I can.”

The president said he thinks the US is “awful close” to having enough of its population vaccinated though he added that he’s not a scientist. “But one thing is for certain. A quarter of the country can’t go unvaccinated and us not continue to have a problem.”

As for the Moderna and J&J jabs, boosters will likely be approved for those as well.

“Well, I think what’s going to happen is you’re going to see that, in the near term — or we’re probably going to open this up anyway,” he told reporters after a speech on the administration’s vaccination campaign. “They’re constantly looking at — we’re looking at both Moderna and J&J. And we’re both — as I said in the speech — in addition to that, we’re also looking to the time when we’re going to be able to expand the booster shots, basically, across the board.”

At one point during the briefing, Biden said in response to a question that the US vaccination rate would need to be essentially 100% for the American economy to return to “normal”.

REPORTER: How many Americans need to be vaccinated before getting back to normal?

BIDEN: Well, I think, look — I think we get the vast majority. 97, 98 percent. pic.twitter.com/mQ4ekSH5jN

To be clear, that directly contradicts findings from scientists who believe COVID is now endemic in the human population and will never go away completely.

Furthermore, here is the all-knowing Fauci in May:

“If we get to the president’s goal – which I believe we will attain – of getting 70 percent of people getting at least one dose, adults that is, by July 4, there will be enough protection in the community that I really don’t foresee there being the risk of a surge.”

Bear in mind that Norway, which has just lifted 100% of all its COVID restrictions and has actually returned to normal, has a 67% vaccination rate among its population.

Readers can watch two clips from the briefing below:

North Korea Launches “Unidentified Projectile” Into Sea Of Japan

Just days after Pyongyang said they’re open to “constructive” talks with South Korea, and two weeks after the rogue nation fired a “new type long-range” cruise missile, South Korea’s Yonhap News Agency reports North Korea fired at least one unidentified “projectile” from its eastern coast Tuesday. The latest tick-up in missile firings comes as tensions between the U.S. and China continue to boil, and a US British warship sailed through the Taiwan Strait on Monday.

Details are scant at the moment, and there’s no confirmation if the projectile was a ballistic missile banned under U.N. Security Council resolutions and or how many were fired and how far it traveled.

“Tuesday’s launch could be designed to test whether the South would still brand it as a provocation,” Yonhap said. It was noted the projectile landed in the Sea of Japan.

Three days ago, the powerful sister of North Korean leader Kim Jong Un, Kim Yo Jong, made a surprise statement indicating Pyongyang would be open to talks with South Korea but on condition that Seoul would press the Biden administration to relax the U.S. continued crippling sanctions on the isolated country. The latest firing may indicate talks are not going well.

Two weeks ago, North Korea test-fired a “new type long-range” cruise missile that would give the country a “strategic significance of possessing another effective deterrence means for more reliably guaranteeing the security of our state and strongly containing the military maneuvers of the hostile forces,” North Korea’s state-owned media KCNA said.

If the projectile is confirmed to be a ballistic missile, it would be the third launch this year.

Today’s launch most likely had Beijing’s full blessing (if not direct order) as Sino-U.S. relations continue to deteriorate.