WaPo Settles $250 Million Lawsuit With Covington Teen Nick Sandmann Tyler Durden

Fri, 07/24/2020 – 14:45

The Washington Post has settled a $250 million defamation lawsuit filed by Covington Catholic High School student Nick Sandmann for an undisclosed amount, after the teen claimed the left-leaning news outlet ‘led the hate campaign’ against him following a racially charged January, 2019 incident at the March for Life Rally at the Lincoln Memorial.

Sandmann was viciously attacked by left-leaning news outlets over a deceptively edited video clip from the incident, in which the teenager, seen wearing a MAGA hat, appeared to be mocking a Native American man beating a drum (a known political grifter who lied about the incident, and stole valor).

The following day, a longer version of the video revealed that Sandmann did absolutely nothing wrong – as the Native American, Nathan Phillips, aggressively approached Sandmann and beat a drum in his face.

In a tweet on his 18th birthday, Sandmann wrote “On 2/19/19, I filed $250M defamation lawsuit against Washington Post. Today, I turned 18 & WaPo settled my lawsuit.”

On 2/19/19, I filed $250M defamation lawsuit against Washington Post. Today, I turned 18 & WaPo settled my lawsuit. Thanks to @ToddMcMurtry & @LLinWood for their advocacy. Thanks to my family & millions of you who have stood your ground by supporting me. I still have more to do.

But, Mousie, thou art no thy-lane, In proving foresight may be vain; The best-laid schemes o’ mice an’ men Gang aft agley, An’ lea’e us nought but grief an’ pain, For promis’d joy!

– Robert Burns, To a Mouse, on Turning Her Up in Her Nest With the Plough (in extract), 1785

A Really Neat Bridge

The grand plans of our local officials in Long Beach have been foiled by the coronavirus bug. After seven years of construction, at a cost of $1.5 billion, they can’t even hold a proper ribbon-cutting.

The special occasion is the grand opening of the new, yet to be named, Gerald Desmond Bridge replacement. To prevent the spread of COVID-19, a virtual ceremony is planned for the Friday leading into the Labor Day weekend.

Virtual ceremonies, like professional baseball games with recorded fan noises, are Dumb with a capital D. But, perhaps, this is the fitting grand opening of an edifice that was planned and constructed for a world that may never arrive.

Certainly, the new bridge structure, which has the highest vertical clearance of any cable-stayed bridge in the U.S., is a remarkable engineering achievement. The cable-stayed design also has a signature aesthetic. We’ve watched it go up over the years; it really is extraordinary.

The two towers rise up to roughly 515 feet above mean sea level, and include 40 cables per tower. The bridge’s linear extent is approximately 8,800 feet. The cable-stayed span alone is 2,000 feet.

Construction included 18 million pounds of structural steel, 75 million pounds of rebar, and 300,000 cubic yards of concrete. The new bridge will improve connection between downtown Long Beach with Terminal Island, and through the Port of Long Beach / Port of Los Angeles mega San Pedro Bay ports complex.

The old Gerald Desmond Bridge that it’s replacing was constructed in 1968. According to Duane Kenagy, capital programs executive at the Port of Long Beach, the old bridge had become “functionally obsolete.”

Maybe so. But the new bridge, while really neat, may be functionally unnecessary.

Here’s why…

Global Trade Contractions

To meet the relentless expansion of international trade over the last 20 years, berths have been widened, and channels have been deepened to accommodate the definitive absurdity of perpetual credit creation: The CMA CGM Benjamin Franklin. This mega container ship, if you’re unfamiliar with it, is over 20 stories tall, the width of a 12 lane freeway, and longer than four football fields. It has enough cargo space to hold 90 million pairs of ‘Made In China’ shoes.

The purpose of the bridge replacement is to provide greater clearance into the Port’s Inner Harbor for mega container ships. The general philosophy of the bridge’s proponents is that global trade expands in perpetuity. Hence, more and more space will be needed for more and more next generation container ships. There’s even 50-years of data to support this belief. But that doesn’t mean what is will always be.

From a practical standpoint, global trade has expanded without interruption for so long that only senior citizens – if they still have their wits about them – can remember anything different. Yet, global trade hasn’t always expanded. In fact, there have been long episodes of contractions in global trade that have played out over long secular trends for thousands of years.

The Silk Road, for example, was established by the Han Dynasty of China in 130 BC, and allowed for continuous trade between east and west for nearly 1,600 years. In addition to economic trade, the Silk Road was also a conduit for culture and knowledge among its network of civilizations.

However, this trade route eventually came to an end. When the Byzantine Empire fell to the Turks in 1453 AD, the Ottoman Empire closed the Silk Road and cut all ties with the west. Geopolitical trends turned inward towards isolation.

There are also more recent examples of contractions in global trade…

Best Laid Schemes

Those willing to look back to the first half of the 20th century will discover something that goes counter to their life experience. Global trade, as a proportion of total economic activity, went down between the onset of World War I and the 1960s. That’s a near 50 year run of declining global trade.

Could another half-century contraction of global trade happen again? At the moment, it’s very well possible that one has already commenced.

Just last month, for instance, cargo volume at the Port of Long Beach declined by double digits. Container Management offers the grim particulars:

“The Port of Long Beach had an 11.1 percent year-on-year drop in container volumes for June due to a lower demand for goods and cancelled sailings related to the COVID-19 pandemic.

“Total volume for June 2020 was 602,180 twenty-foot equivalent units (TEUs) with imports declining by 9.3 percent to 300,714 TEUs and exports down 12.2 percent to 117,538.

“Decreased consumer spending and ongoing health concerns led to economic uncertainty for the first half of 2020 which, in turn, resulted in a 6.9 percent less containers handled compared to 2019 for a total of 3.4 million TEUs.

“Combined, Long Beach and Los Angeles (the San Pedro Bay ports complex) had 41 cancelled sailings in the first half of 2019. This year, it was 104.”

The impetus for the trade contraction is both a politically motivated trade war, and economic seizure from government lockdown orders. The long-term ramifications of these developments will persist for decades. But for now, the local public officials are counting on a strong recovery and future growth. Long Beach Harbor Commission President Bonnie Lowenthal is bullish on future trade:

“The economic recovery is going to take some time, but we are optimistic for the future of the port and our partnerships with labor and the entire goods movement industry.”

Lowenthal’s optimism is largely misplaced. The best-laid schemes of mice and men often go askew, and leave us nothing but grief and pain. In this case, they also leave us with a signature bridge structure; a lasting monument to an extended era of global trade that has come and gone.

via ZeroHedge News https://ift.tt/2WSGMka Tyler Durden

“Shut The Eff Up Forever” – Morning Show Host Slams Biden For Calling Trump “The First Racist President” Tyler Durden

Fri, 07/24/2020 – 14:05

Political affiliations and preferences are a funny thing, especially in the US, where black and latino Democratic voters repeatedly chose former Vice President Joe Biden over his more progressive rivals (Bernie, Warren), as well as DNC insider favorite Kamala Harris (whom the Bernie Bros successfully tarred as “Cop-mala”).

Biden’s unwavering popularity with minority voters is one of the few legitimate strengths in the Biden column. Of course, the most jarring thing about Biden and his campaign right now is the fact that he’s reportedly been hiding out in his basement and only doing a limited number of speeches and media appearances. The few campaign-related interviews Biden does do are inexplicably buried by mainstream (ie Democratic Party-aligned) media orgs, if they’re covered at all.

One example of this occurred earlier this week, when one of the most popular radio hosts in the country – “The Breakfast Club” radio host Charlamagne Tha God – derided Biden and his penchant to mistakenly violate progressive orthodoxies, saying he “wished [Biden] would shut the eff up forever” and go back to hiding in the basement.

Biden’s mistake? Saying that Trump was the “first” racist American president. Even though the founding fathers and their immediate successors have been dead for centuries, Charlamagne insisted that at least 12 former presidents owned slaves. That’s not actually true. According to at least one source, eight former presidents owned slaves. Admittedly, this distinction doesn’t exactly dilute Charlamagne’s point.

“I really wish Joe Biden would shut the eff up forever and continue to act like he’s starring in the movie ‘A Quiet Place’ because as soon as he opens his mouth and makes noise, he gets us all killed, OK?” the radio host said. “There’s already so many people who are reluctantly only voting for Joe Biden because he’s the only option and because Donald J. Trump is that trash.”

Here’s the context. Charlamagne was referencing a comment Biden made Wednesday in one of his few public statements. The comment earned Biden a place as “Donkey of the Day” on “The Breakfast Club.”

On Wednesday, Biden took aim at the president’s alleged racism, suggesting it’s historic compared to his predecessors.

“No sitting president has ever done this… No Republican president has done this. No Democratic president. We’ve had racists and they’ve existed and they’ve tried to get elected president. He’s the first one that has,” Biden said.

However, Charlamagne declared the presumptive Democratic candidate Thursday’s “Donkey of the Day” for his comments.

Then, Charlamagne did something unexpected (for a morning show host on a show that mostly focuses on entertainment and pop culture): He wipped out the polling data.

Charlamagne then cited polling that showed a wide enthusiasm gap between Biden and Trump, noting that it’s “not good” for the Democrat to be lacking excitement among his voters, and suggested Biden’s latest remarks will further contribute to the “lack of enthusiasm.”

“Old white male leadership has failed America and there is nothing worse than an old white male [who] can’t recognize the faults and flaws of other old white males,” Charlamagne told listeners. “Racism is the American way. Donald Trump is not the first. And sadly, he won’t be the last, right? He’s just more overt with his racism than most presidents in recent times.”

Biden better announce his VP pick – the candidate has promised to pick a black woman for the position – quick, Charlamagne said. Because the VP isn’t going to be able to ride the BLM wave into the Oval Office if he doesn’t make some commitments.

via ZeroHedge News https://ift.tt/2CN6UpH Tyler Durden

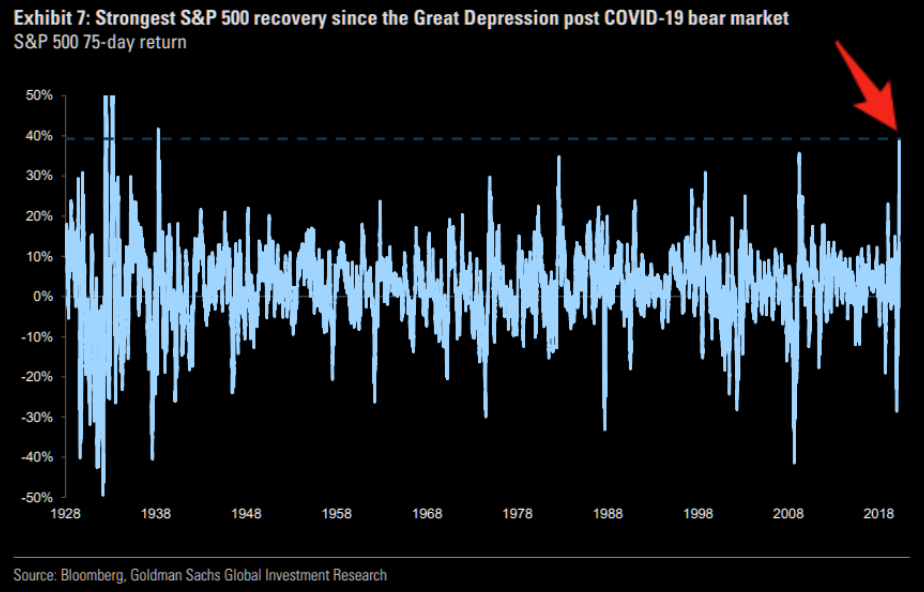

There has been a growing concern over Technology stocks as investors “Party Like It’s 1999.” While no two periods are the same, the outcomes often are. For longer-term investors, if we are amid another “Tech Bubble,” the biggest challenge is navigating it and “living to tell about it.”

That certainly seems an apropos statement after watching the financial markets plunge 35% in March to recover back to positive territory by July. Interestingly, this is the fastest rebound in the market since 1938 but is occurring against a near economic depression.

Here are some current stats:

-34.7% Annualized GDP Growth (-8.675% for Q2) via Atlanta Fed GDPNow Estimate

~50-million people unemployed

-4.2% personal income

-104.2 billion decrease in international transactions for Q1 (Q2 will be markedly worse)

-54.6 billion decrease in international trade of goods and services.

~30% decline in corporate profits

~35% decline in corporate earnings based on current estimates

There is no precedent for such a dichotomy between the markets and the economy. Yet, as stated, this is the fast recovery in the market since 1938. Just not so much for the economy.

As I said, we certainly live in “interesting times.”

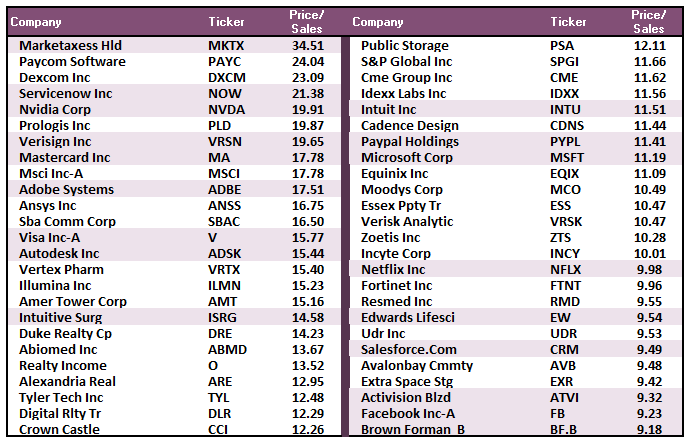

Part of those discussions related to similarities seen at previous market peaks where investors threw “caution to the wind” and paid astronomical prices to own the “hot stocks.” To this point specifically, we quoted Scott McNealy, then CEO of Sun MicroSystems, who chastised investors for paying 10x Price-to-Sales for his company. That was in 1999. Today, investors are doing it again.

Of course, much of this is “forgotten history” as many investors today were either a) not alive in 1999, or b) still too young to invest. For the newer generation of investors, the lack of “experience” provides no basis for the importance of “valuations” to future outcomes. That is something only learned through experience.

Just as was the case in 1999, investors believe that stocks are essentially a “one-decision” investment. You buy them, and they only go up in price. In 1999, a large majority of these companies were financially unstable or grossly overvalued at best. Today, as shown above, it isn’t much different.

Bubbles Are About Psychology

In 1999, there was “no one” saying there was a “Tech Bubble.”As Mark Hulbert recently noted, it was quite the opposite. It also smacks of current sentiment as well:

“After reading through my newsletter archives from January 2000, I was struck by the similarities between now and then. For example, one newsletter editor in mid-January 2000 said he was encouraged that the Fed was signaling that it wouldn’t be raising rates as aggressively as previously thought. Another said, “inflation is dead.” A third celebrated the strength of the economy, as evidenced by robust consumer spending in the Christmas season that had just ended.

Sound familiar? To be sure, these similarities don’t mean the U.S. market is at or near a top. It does illustrate the false comfort we gain when telling ourselves a bear market can’t happen since the economy is strong, inflation is moribund, and the Fed is accommodative.”

As Mark goes on to note, the extension of valuations is concerning. However, valuations are a poor measure of market “bubbles.” Why? Because “bubbles” are a “psychological phenomenon” where investor “greed” completely overrides “logic” and “restraint.”

“Greed” Really Isn’t Good

Throughout history, all market crashes have been the result of things unrelated to valuation levels, such as liquidity issues, government actions, monetary policy mistakes, recessions, or inflationary spikes. Those events were the catalyst, or trigger, that started the “reversion in sentiment” by investors.

Market crashes are an “emotionally” driven imbalance in supply and demand.

Such has nothing to do with fundamentals. It is strictly an emotional panic, which is ultimately reflected by a sharp devaluation in market fundamentals. As Bob Bronson once penned:

“It can be reasonably assumed that markets are sufficient enough that every bubble is significantly different than the previous one, and even all earlier bubbles. It’s to be expected that a new bubble will always be different from the previous one(s). Investors will only bid prices to extreme overvaluation levels if they are sure it is not repeating what led to the last, or previous bubbles.

Comparing the current extreme overvaluation to the dotcom is intellectually silly.

I would argue that when comparisons to previous bubbles become most popular, like now, it’s a reliable timing marker of the top in a current bubble. As an analogy, no matter how thoroughly a fatal car crash is studied, there will still be other fatal car crashes, even if drivers avoid the previous accident-causing mistakes.”

Comparing the current market to any previous period in the market is rather pointless. The current market is not like 1995, 1999, or 2007? Valuations, economics, drivers, etc. are all different from cycle to the next. Most importantly, however, the financial markets adapt to the cause of the previous “fatal crashes.”Still, that adaptation won’t prevent the next one.

Signs Of Exuberance

So, if “bubbles” are specifically a function of “speculative appetite,” there should be some relevant indications suggestion that such exists.

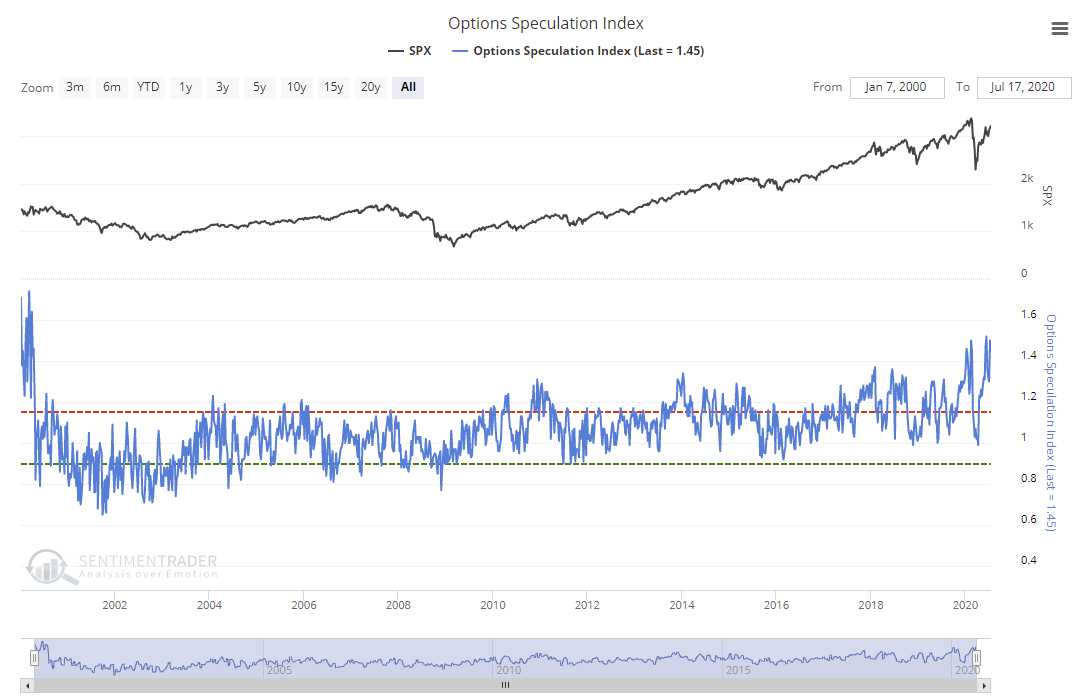

One of the best measures of “exuberance” is looking at “options speculation.” Options are leveraged bets for market participants, which can, and often do, wind up worthless in value. There have only been two previous points in history where options speculation was this high – February 2020 and March 2000.

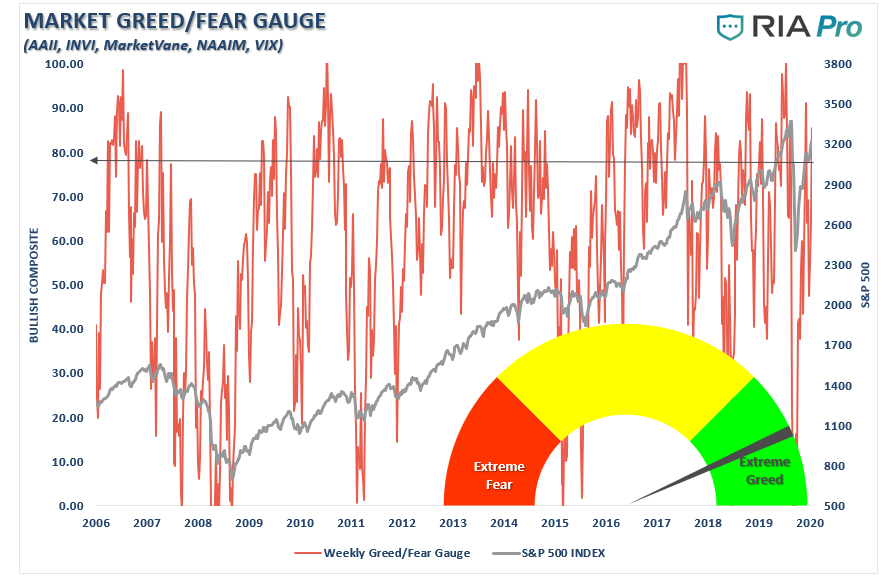

The RIAPro “Fear/Greed” gauge is based on both retail and professional investor positioning in the markets. That indicator is well back into “greed “ territory.

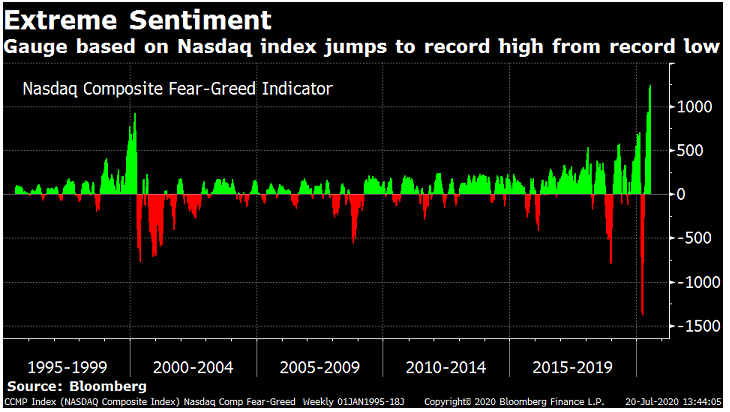

However, those measures are more reflective of the broader markets. Like 1999, the real exuberance is in the Nasdaq, where sentiment has jumped to a record high.

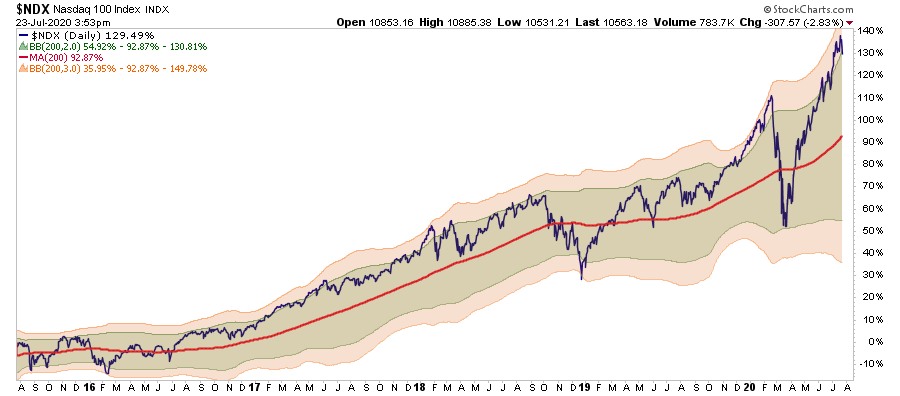

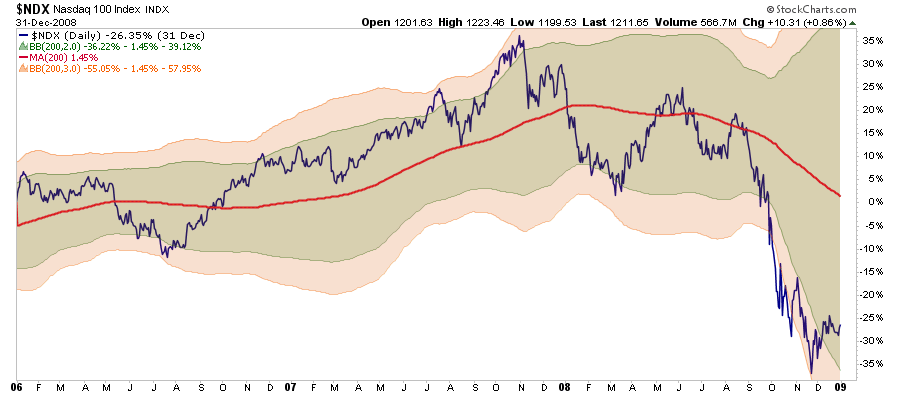

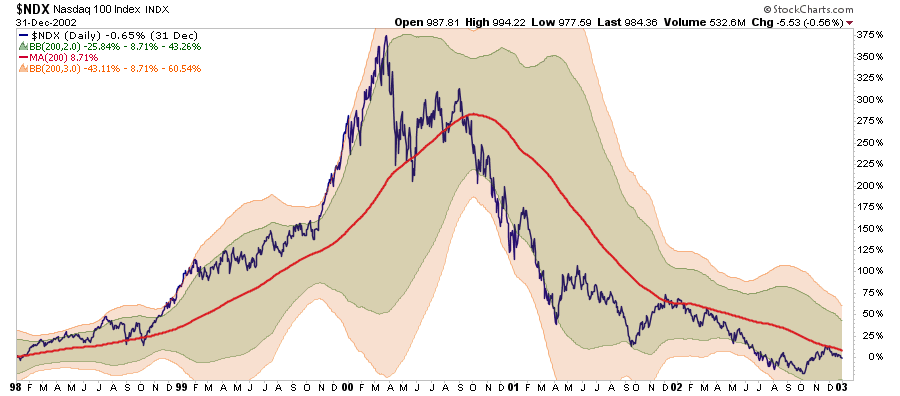

Furthermore, a reflection of the underlying “greed” is in the market’s price relative to its longer-term moving averages. The chart below shows the 2- and 3-standard deviation ranges of the Nasdaq 100 index from the underlying 200-dma.

Longer-term moving averages are the “gravity” to prices. The greater the deviation from the long-term moving average, the greater the “pull” on prices. With regularity, extreme deviations in one-direction lead to a “mean reverting” event in the other. Currently, the Nasdaq 100 index is trading 3-standard deviations above the 200-dma. The last time was this past February.

But we saw it previously in August and November of 2007.

And, of course, in 1999-2000.

While such deviations do not necessarily mean that a massive correction is imminent, it does suggest elevated risk. When prices become this extreme, it only takes a little “nudge” to start a correction.

History Doesn’t Repeat

“History Doesn’t Repeat Itself, but It Often Rhymes” – Mark Twain.

Again, none of this suggests the market is going to crash tomorrow. But a mean-reversion process is coming, it is inevitable, the only question is of the timing.

Remaining fully invested in the financial markets without a thorough understanding of your ‘risk exposure’ will likely not have the promised result you desire.

My job, as a steward of our client’s assets, is to participate in the markets while keeping a measured approach to capital preservation. Since it is considered “bearish” to discuss investment “risk,” then I guess you can call me a “bear.”

Just make sure you understand I am still in “theater,” we are just moving much closer to the “exit.”

As we saw in March, when someone does eventually yell “fire,” we want to make sure there is easy access to an “exit.”

Defining Our Job

“The more things change, the more they remain the same.”

If you have been around the markets for any length of time, you can quickly spot the “pigeons at the poker table.” They are the ones that rationalize why prices can only rise, why “this time is different,” and focus only on the bullish supports. Trying to “draw to an inside straight” is not impossible, it just leads to losses more often than not.

But therein lies an important point.

As investors, our job is NOT making a case for why markets will go up.

Read that again.

Coming up with reasons why markets will rise is a pointless endeavorwhen you are already invested.

If the markets rise, terrific. We all made money, and we are the better for it. However, that is not our job.

Our job is to analyze, understand, measure, and prepare for what will reduce the value of our invested capital.

Period.

How To Survive The Tech Bubble

If we are to accumulate capital over the long-term, the most important thing to ensure success is to avoid large capital losses.

Therefore, our job as investors is quite simple:

Capital preservation

A rate of return sufficient to keep pace with the rate of inflation.

Expectations based on realistic objectives. (The market does not compound at 8%, 6% or 4%)

Higher rates of return require an exponential increase in the underlying risk profile. Such tends to not work out well.

You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that you cannot afford to waste.

Portfolios are time-frame specific. If you have a 5-years to retirement but build a portfolio with a 20-year time horizon (increasing draw-down risk,) the results will likely be disastrous.

With forward returns likely to be lower and more volatile than promised by the mainstream media, the need for a more conservative approach is rising. Controlling risk, reducing emotional investment mistakes, and limiting the destruction of investment capital is the formula for investment success.

The Rules

The following investment guidelines are not new, nor totally unique, but are ones I have learned, and relearned, over the last 30 years.

Investing is not a competition. There are no prizes for winning but there are severe penalties for losing.

Emotions have no place in investing.You are generally better off doing the opposite of what you “feel” you should be doing.

The ONLY investments that you can “buy and hold” are those that provide an income stream with a return of principal function.

Market valuations (except at extremes) are very poor market timing devices.

Fundamentals and Economics drive long-term investment decisions – “Greed and Fear” drive short-term trading. Knowing what type of investor you are determines the basis of your strategy.

“Market timing” is impossible– managing exposure to risk is both logical and possible.

Investment is about discipline and patience. Lacking either one can be destructive to your investment goals.

There is no value in daily media commentary– turn off the television and save yourself the mental capital.

Investing is no different than gambling– both are “guesses” about future outcomes based on probabilities. The winner is the one who knows when to “fold” and when to go “all in”.

No investment strategy works all the time. The trick is knowing the difference between a bad investment strategy and one that is temporarily out of favor.

As an investment manager, I am neither bullish or bearish. I simply view the markets through the lens of statistics and probabilities. Our job is to manage the inherent risk to investment capital.

Yes, markets have always recovered their losses, but that isn’t the same thing as making money.

via ZeroHedge News https://ift.tt/39qOG9r Tyler Durden

Goldman Anticipates 50% Cut To Unemployment Supplement Tyler Durden

Fri, 07/24/2020 – 13:25

As US initial claims surge back to 1.4m and the $600 weekly unemployment boost set to lapse on Friday, Goldman Sachs’ chief economist Jan Hatzius thinks lawmakers will end up cutting the supplemental benefits in half – if they’re able to reach an agreement at all. Though given the chances of lawmakers letting Americans die on the vine into a contentious election, it looks like this experiment in quasi-universal basic income is here to stay in some form or another.

Speaking via phone on Thursday, Hatzius told Bloomberg that anticipates the $600 weekly stipend will be reduced to $300 – though he notably didn’t address the possibility of a temporary extension – a stopgap solution supported by Republicans which has faced opposition from key Democrats.

And as Rabobank’s Michael Every noted earlier, “Until Congress can agree on something new, we are about to find out what an economy looks like when you throw tens of millions into unemployment…”

Goldman’s Hatzius, meanwhile, also anticipates $200 billion in new funding for cities and states.

“If that doesn’t show up, state governments are going to be in very serious financial trouble, and you’re going to see serious cutbacks,” he said.

If Congress delivers something along those lines, the economy will continue to grow, but he warned that “you’re still going to see some negative impacts, because the unemployment insurance is less generous than it was before.” There’s also a possibility that nothing gets passed, and in that case Hatzius sees a return to outright economic contraction. -Bloomberg

Whatever happens in the near term, Goldman’s outlook is still sour – with unemployment remaining elevated for years despite Hatzius noting that “this is a much more rapid recovery than we’ve seen in the past,” adding “We’re still above 4% for the next four years,” he said of the US jobless rate.

Because of this, Hatzius and his team aren’t expecting the fed to hike rates for another five years, and assumes that Fed Chairman Jerome Powell and his colleagues will issue some type of “outcome-based guidance” in which they won’t commit to hiking rates until inflation above 2% is sustained and unemployment remains below a certain threshold.

via ZeroHedge News https://ift.tt/2D0zP9M Tyler Durden

Jim Grant has long been skeptical of the mechanization of the Federal Reserve. He was warning about the distortions created in the markets and broader economy caused by the central bank’s monetary policy long before the monetary Hail Mary it threw up in response to the coronavirus pandemic.

In the WSJ piece, Grant asserts that the Fed’s zero interest rate monetary policy is hopelessly distorting the economy and policymakers, Powell in particular, should find a bit of humility.

Ground-scraping interest rates turn savers into speculators and quarantined millennials into day traders. They facilitate overborrowing, suppress market signals, misdirect investment dollars and promote the dubious business of turning well-financed public companies into heavily indebted private ones. Concerning the future and its side effects, Mr. Powell should admit how little he knows — he and the rest of us.”

Conventional wisdom holds that given the economic shutdowns, the central bank had to “do something.” Grant takes a position similar to Peter Schiff who has said the Fed policy isn’t helping and it’s actually hurting. During his Fox Business interview, Grant said it was doomed from the start.

The Fed faced kind of an insuperable difficulty, right? Without revenue, things don’t work. And there is no kind of monetary policy that is designed to supplant the absence of commerce. That’s what they faced in March.”

The Fed may have acted with good intentions, but as Grant put it, investors aren’t really concerned with “motives or necessity.” All that really matters is outcomes. The outcomes won’t be good.

So, what does all this mean?

It means a uniquely aggressive monetary stance. It means interest rates no longer are prices that reliably direct investment flows and valuations. Interest rates are the artificial constructs of the Fed that is doing its best to step in and make something happen in the absence of economic activity as we used to know it. So, interest rates distort judgments and flows. And the amount of money that the Fed has created is itself a distorting factor.”

Peter has been warning about a dollar crash and looming inflation for months. Grant expressed concern as well.

The Fed wants us to believe that we should believe that there will be no inflation out of all this and to me that is a vast unknown. We have America’s fasted peacetime money-growth coexisting with the all-time 4,000-year record lows in interest rates. It’s a most curious and troubling juxtaposition there.”

Grant said aggressive moves by governments and central banks are unwise.

I think what we have is a monetary moment that is unprecedented and therefore calls for extreme caution and great humility on the parts of all of us.”

Grant pointed out that commodity prices are at their lowest level compared to the Dow in about 120 years.

That, to me, kind of lights a light. It reminds us that there may be an extreme valuation out there that might be inviting capital rather than thought to be repelling it.”

Grant said that he is “confidently bullish” on precious metals.

We feel that they are an alternative to what is happening in equities and in bonds.”

Gunshot To Head, Parkinson’s Disease, Deaths In Palm Beach Incorrectly Attributed To COVID-19 Tyler Durden

Fri, 07/24/2020 – 12:45

When it comes to overinflated coronavirus death counts, we recently outlined how a fatal motorcycle accident in Florida was added to the state’s COVID-19 death toll. Still, no precise data shows just how overinflated death counts are on a state by state level.

We have to rely on real journalism, such as a new report via CBS12 West Palm, that made a shocking discovery about deaths being incorrectly attributed to the virus.

CBS12 said a 60-year old man who died from a gunshot blast to the head was labeled as a virus death. A 90-year old man who fell and died from a hip fracture was another. Even a 77-year old woman who died of Parkinson’s disease was somehow labeled a virus-related death.

h/t CBS12

CBS12’s I-Team investigated these statistical anomalies by combing through the Medical Examiner’s spreadsheet of all people who recently died of the virus in Palm Beach County.

What they found are “eight cases in which a person was counted as a COVID death, but did not have COVID listed as a cause of contributing cause of death.”

For more color on how a COVID-19 death is determined, it must be an immediate or underlying cause of death. So a gunshot to the head, a falling accident, and or Parkinson’s disease certainly doesn’t fit the defined criteria of classifying these deaths as virus-related.

Residents in South Florida are furious about the overinflated death toll:

“I think it is completely misleading,” said Rachel Eade, a Palm Beach County resident who has been researching the same issue.

“We need to remove those cases that are not COVID exclusive, and we need to be giving people that information,” said Eade, who is one of the plaintiffs suing Palm Beach County for its mask mandate.

Eade told the I-Team she’s been digging around in medical reports and said, out of the 581 deaths, only 169 deaths are listed as COVID-19 without any contributing factors.

Florida Gov. Ron DeSantis recently told Fox News that his staff has been informed about virus deaths being incorrectly reported.

DeSantis said, “I think the public, when they see the fatality figures, they want to know who died because they caught COVID.”

“If you’re just in a car accident – and we have had other instances where there is no real relationship, and it’s been counted, we want to look at that and see how pervasive that issue is as well.”

Palm Beach County Medical Examiner’s office and Operations Manager Paul Petrino told the I-Team the eight cases were, in fact, errors. He said his medical staff was in the process of relabeling those deaths.

Readers may recall, we pointed out last week how virus deaths could be overinflated, here’s Dr. Scott Jensen on Fox News in April providing more color on the situation.

If virus-related deaths are being overinflated in Florida, is the same being done in other states?

via ZeroHedge News https://ift.tt/2CJs1cA Tyler Durden

The admin panel used by hackers to access over one hundred accounts can be used by over 1,000 twitter employees — two former Twitter employees revealed.

More than 1,000 Twitter employees and contractors had access to the internal admin panel that enabled last week’s Twitter hack of 130 high profile accounts.

According to Reuters on July 24, two former employees have shed light on just how vulnerable Twitter’s security was — and may still be. They said that, in addition to employees, contractors like Cognizant could also have access.

Former chief security officer at AT&T Edward Amoroso, told Reuters that such powerful controls should not be available to so many people.

“That sounds like there are too many people with access,” he said, adding that staff should have limited rights with responsibilities split up as well as multiple checks and balances in place for adjusting sensitive information.

“In order to do cyber security right, you can’t forget the boring stuff.”

What happened?

On July 15 attackers accessed Twitter’s admin panel allowing them to take control of any Twitter account, post tweets from them and access personal information including private messages.

They posted scam Bitcoin (BTC) ‘giveaways’, by promising to send back double any sum received. All told, the scammers got away with around 12 BTC.

High profile accounts taken over include Tesla founder Elon Musk, former United States President Barack Obama, Amazon owner Jeff Bezos, Microsoft co-founder Bill Gates and 2020 U.S. presidential candidate and former Vice-President Joe Biden. Other celebrities, politicians and top business personalities also lost control of their accounts.

Twitter and the FBI are working together to investigate the breach, with regular updates from Twitter on their findings. On Jul 23, the company revealed that in “up to 36 of the 130 targeted accounts, the attackers accessed the DM inbox, including 1 elected official in the Netherlands.”

To recap:

🔹130 total accounts targeted by attackers

🔹45 accounts had Tweets sent by attackers

🔹36 accounts had the DM inbox accessed

🔹8 accounts had an archive of “Your Twitter Data” downloaded, none of these are Verified

Twitter has also revealed they are looking for a new security head in order to improve security and employee training.

Security experts are concerned that the required upgrades to Twitter’s security and processes may not be complete before the U.S. elections on Nov. 3 with other countries potentially having the ability to manipulate the outcome through social media account take-overs.

Network security company Tenable founder Ron Gula asked:

“Does Twitter do enough to prevent account takeovers for our presidential candidates and news outlets when faced with sophisticated threats that leverage whole-of-nation approaches?”

via ZeroHedge News https://ift.tt/3eZ0tNw Tyler Durden

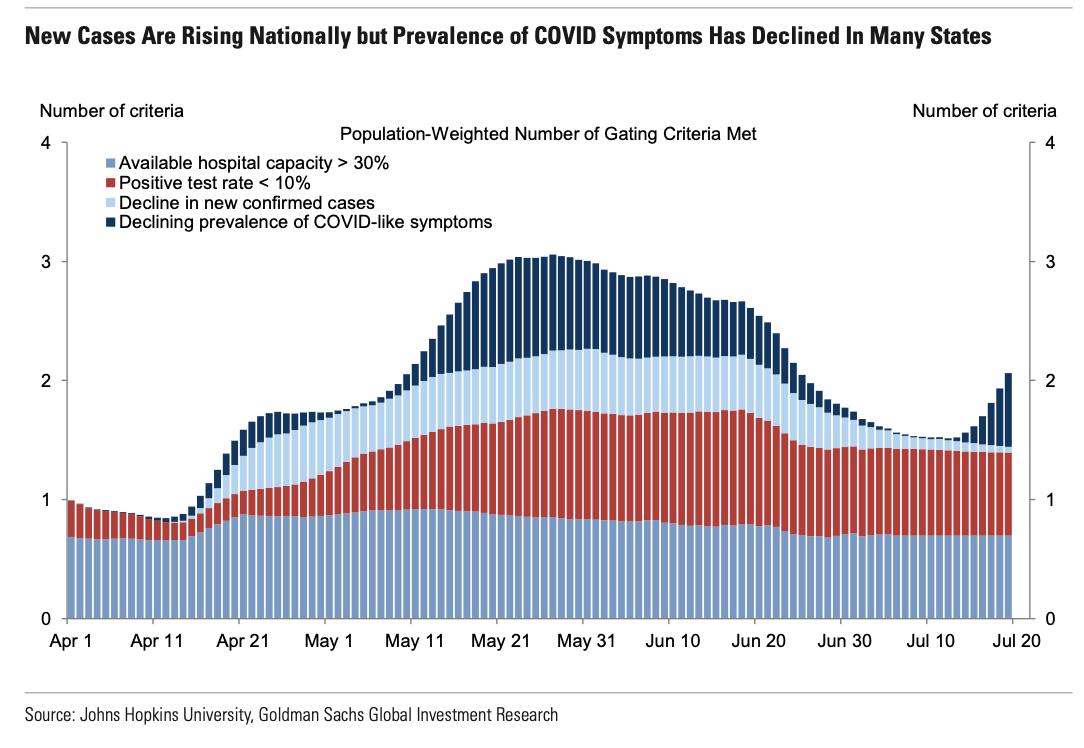

Some Optimism From Goldman: The Number Of New COVID Cases Is Starting To Flatten Tyler Durden

Fri, 07/24/2020 – 12:05

As the US reports more than 1k deaths for the third straight day, reporters are mostly focusing on this milestone, along with the US surmounting the 4 million-case mark, as the biggest COVID-19-related stories of the day. But a team of market-focused analysts at Goldman Sachs pointed out that the daily case totals in some of the worst hit Sun Belt states appear to have finally plateaued.

Earlier, Texas Gov Greg Abbott sat for an interview with Joe Kernen and Andrew Ross Sorkin during the first hour of CNBC’s “Squawk Box” where he argued that social distancing measures and the closure of bars etc undertaken in his state are working, before pleading with viewers to please wear a mask in public.

“Let me be very clear we do not want to shutdown again. The only way we can go about the process of not shutting down is for people to embrace this process of wearing a face mask,” says @GregAbbott_TX on #COVID19. pic.twitter.com/6NDkONcNWK

Though the tone of most of the media coverage might suggest otherwise, Abbott insisted that Texas has definitively passed its infection peak, and that Texans must continue to assiduously follow the government’s advice if they want to see the outbreak dissipate.

As it turns out, Abbott has gotten some unexpected help from a team of analysts at Goldman Sachs, who argued in their latest COVID-19 daily US update that there are reasons for optimism, even as Paul Krugman opines that Italy’s handling of its coronavirus response has outshone the US, despite the fact that Italy’s case-fatality rate and deaths per 100k people rate were both higher than in the US, according to Johns Hopkins Data.

Anyway, as the team from Goldman writes, it looks like some of the worst-hit states are finally seeing their case numbers plateau, eve as the national new-case numbers continue to trend higher (looking at the 7-day average).

And while the GS team noted that governors are probably still “reluctant to push forward” with reopening measures, the time to reimpose sweeping lockdowns appears to have come and gone.

* * *

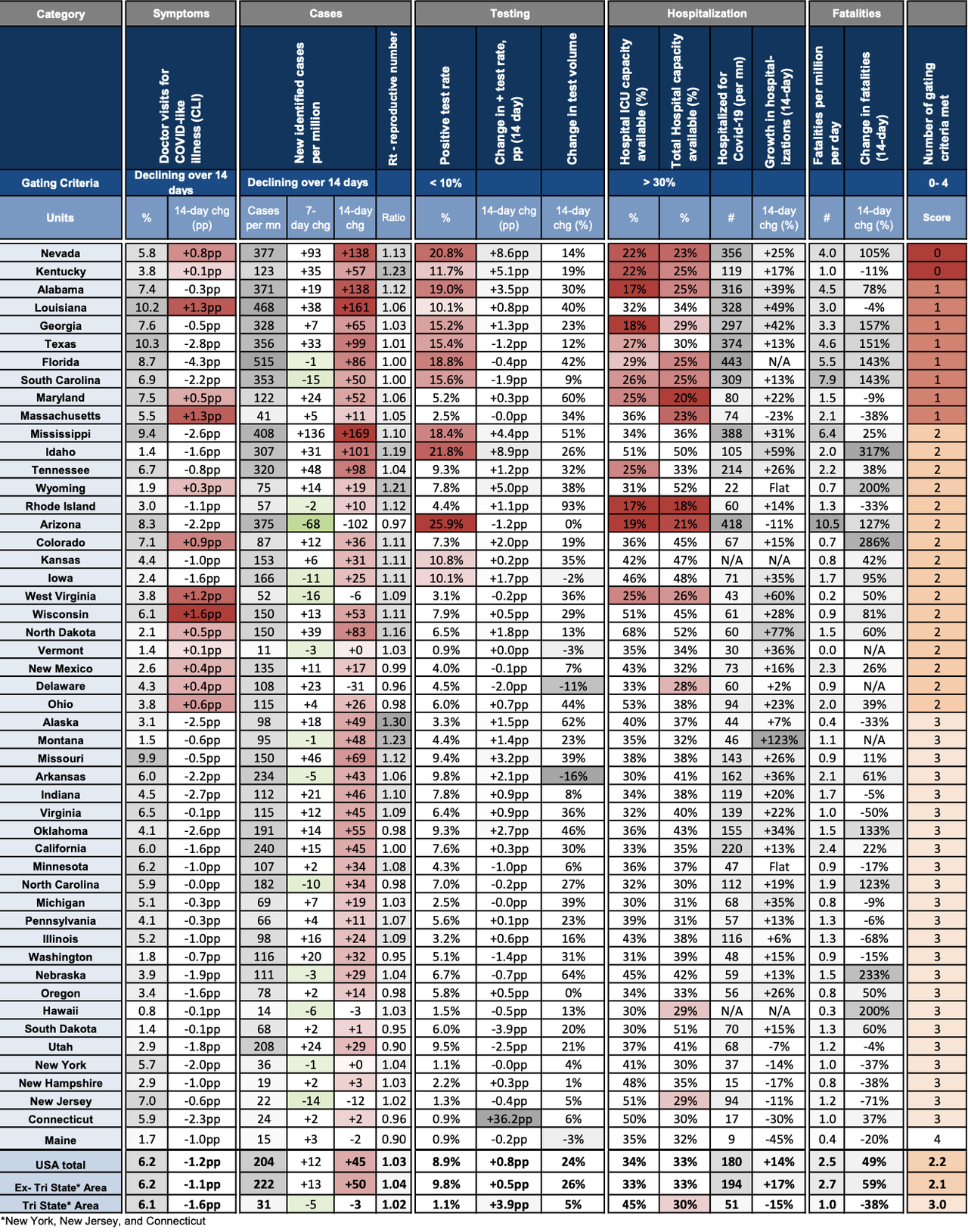

The number of new cases per day is very high but apparently flattening in a few states that experienced significant virus resurgence over the past week, including Arizona, Florida, and South Carolina. Meanwhile, the number of new cases per day is elevated and surging higher in a handful of other states including Nevada, Alabama, Louisiana, Mississippi, Idaho, and Tennessee. Nationally, new cases continue to rise further on average and remain on upward trajectories in a majority of states.

Hospitalizations and fatalities also continue to rise further nationally and sharply in some states. In Louisiana, some hospitals have halted non-emergency surgeries in order to increase available capacity to accommodate greater numbers of COVID-19 patients.

The average number of the four gating criteria the federal government recommends to proceed with reopening that states are meeting has risen over the past few days as prevalence of COVID-like illness symptoms has declined in several states, potentially suggesting downward pressure on case growth. But with the level of new cases already very high in several states and on average nationally, state government officials may remain reluctant to push forward with reopening.

The number of new cases per day is very high but apparently flattening in a few states that experienced significant virus resurgence over the past week, including Arizona, Florida, and South Carolina. Meanwhile, the number of new cases per day is elevated and surging higher in a handful of other states including Nevada, Alabama, Louisiana, Mississippi, Idaho, and Tennessee. Nationally, new cases continue to rise further on average and remain on upward trajectories in a majority of states.

Hospitalizations and fatalities also continue to rise further nationally and sharply in some states. In Louisiana, some hospitals have halted non-emergency surgeries in order to increase available capacity to accommodate greater numbers of COVID-19 patients.

The average number of the four gating criteria the federal government recommends to proceed with reopening that states are meeting has risen over the past few days as prevalence of COVID-like illness symptoms has declined in several states, potentially suggesting downward pressure on case growth. But with the level of new cases already very high in several states and on average nationally, state government officials may remain reluctant to push forward with reopening.

* * *

Source: Goldman Sachs

via ZeroHedge News https://ift.tt/3hxhcsN Tyler Durden

How great a burden can even an unrivaled superpower carry before it buckles and breaks? We may be about to find out…

Rome was the superpower of its time, ruling for centuries almost the entirety of what was then called the civilized world.

Great Britain was a superpower of its day, but she bled, bankrupted and broke herself in the Thirty Years War of the West from 1914-1945.

By Winston Churchill’s death in 1965, the empire had vanished, and Britain was being invaded by a stream of migrants from its former colonies.

America was the real superpower of the 20th century and became sole claimant to that title with the collapse of the Soviet Union between 1989 and 1991, an event Vladimir Putin called “the greatest geopolitical tragedy of the 20th century.”

Has America’s turn come? Is America breaking under the burdens it has lately assumed and is attempting to carry?

Today, at the presidential library of Richard Nixon, who ushered Mao’s China onto the world stage, Secretary of State Mike Pompeo is laying out a strategy of containment and confrontation of a China that is far more the equal of the USA than was the USSR.

Writes Hudson’s Institute’s Arthur Herman:

“In the 1960s, manufacturing made up 25% of U.S. gross domestic product. It’s barely 11% today. More than five million American manufacturing jobs have been lost since 2000.”

China controls the production of 97% of the antibiotics upon which the lives of millions of Americans depend. She provides critical components in the production chains of U.S. weapons systems.

Beijing commands more warships than the U.S. Navy and holds a trillion dollars in U.S. debt. Moscow never had this kind of hold on us.

Writes Herman:

“Since 2000, America’s defense industry has shed more than 20,000 U.S.-based manufacturing companies. As the work those companies once did domestically has shifted overseas, much of it has gone to China. From rare-earth metals and permanent magnets to high-end electronic components and printed circuit boards, the Pentagon has slowly become dependent on Chinese industrial output. Asia produces 90% of the world’s circuit boards — more than half of them in China. The U.S. share of global circuit-board production has fallen to 5%.”

Decoupling from China and re-industrializing America would be an immense undertaking. But unless and until we do it, we remain vulnerable.

Another decades-long struggle, this time with China, like the Cold War that consumed so much of our attention and wealth from the 1940s to 1991, is not the only challenge America faces.

Through NATO, the U.S. is still the principal protector of almost 30 European nations. And despite Donald Trump’s promise to end our forever wars, 8,500 U.S. troops remain in Afghanistan, 5,000 in Iraq, hundreds in Syria, thousands more in Kuwait and Bahrain.

There are other huge new claims on America’s time, attention and resources.

Some 145,000 Americans have perished in five months of the coronavirus pandemic, more U.S. dead than all the Americans soldiers lost in Korea, Vietnam, Iraq and Afghanistan.

A thousand Americans are dying every day, a higher daily death toll than in World War II and the Civil War combined.

The U.S. economy has been thrust into something approaching a second Depression. The 2020 deficit runs into the trillions of dollars. Our national debt is now far larger than our GDP and soaring. Tens of millions are unemployed. And the shutdowns are beginning anew.

From the protests, riots, rampages and statue-smashing of the last two months, it is apparent that millions of Americans detest our history and heroes. Though nowhere in recorded time have 42 million people of African descent achieved the measures of freedom and prosperity they have in the USA, we are daily admonished that ours is a rotten and sick society whose every institution is shot through with “systemic racism.”

The racial divisions are almost as ugly as during the riots of the 1960s in Harlem, Watts, Newark and 100 cities that exploded after the assassination of Dr. Martin Luther King.

In the numbers of citizens now shot and killed every week, great American cities such as Baltimore, St. Louis, Detroit and Chicago are looking more like Baghdad.

The Democratic Party is promising to take up the issue of racial reparations for our original sin of slavery. The first order of business, we are told, is ending inequality — of income, wealth, educational attainment and health care. The racial disparity in police arrests, prosecutions, incarcerations and school expulsions, must end.

But if the trillions we have spent to address these inequalities since the Great Society days have failed to make greater progress, why should we believe that we even know how to succeed, absent the imposition of a rigid socialist egalitarianism of results?

The Old Republic is facing a stress test unlike any it has known since the Union was threatened with dissolution in the Civil War.

via ZeroHedge News https://ift.tt/39ok9t3 Tyler Durden

{kind=link}