Over 40 Million Jobless In 10 Weeks – “Nobody Ever Imagined It Would Get This Bad So Fast” Tyler Durden

Thu, 05/28/2020 – 08:33

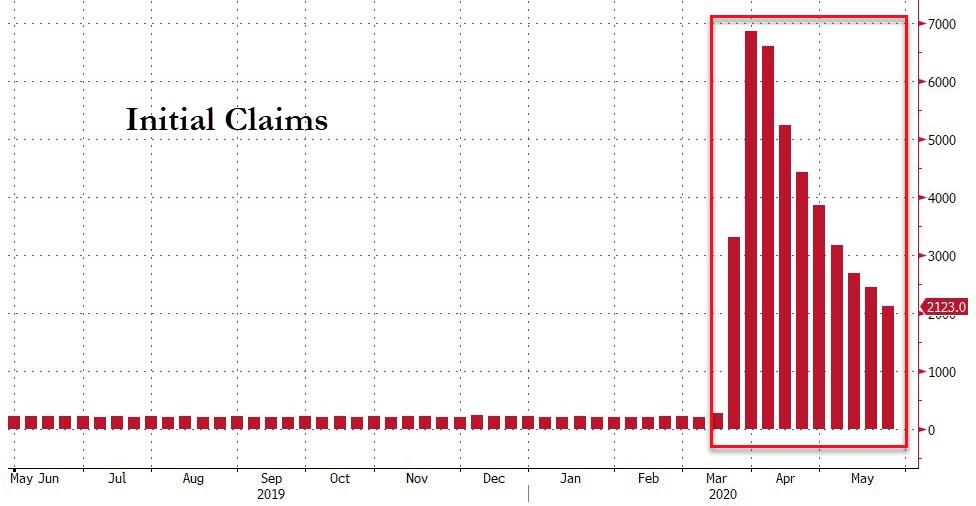

In the last week 2.123 million more Americans filed for unemployment benefits for the first time (versus the 2.10mm expected).

Source: Bloomberg

That brings the ten-week total to 40.767 million, dramatically more than at any period in American history

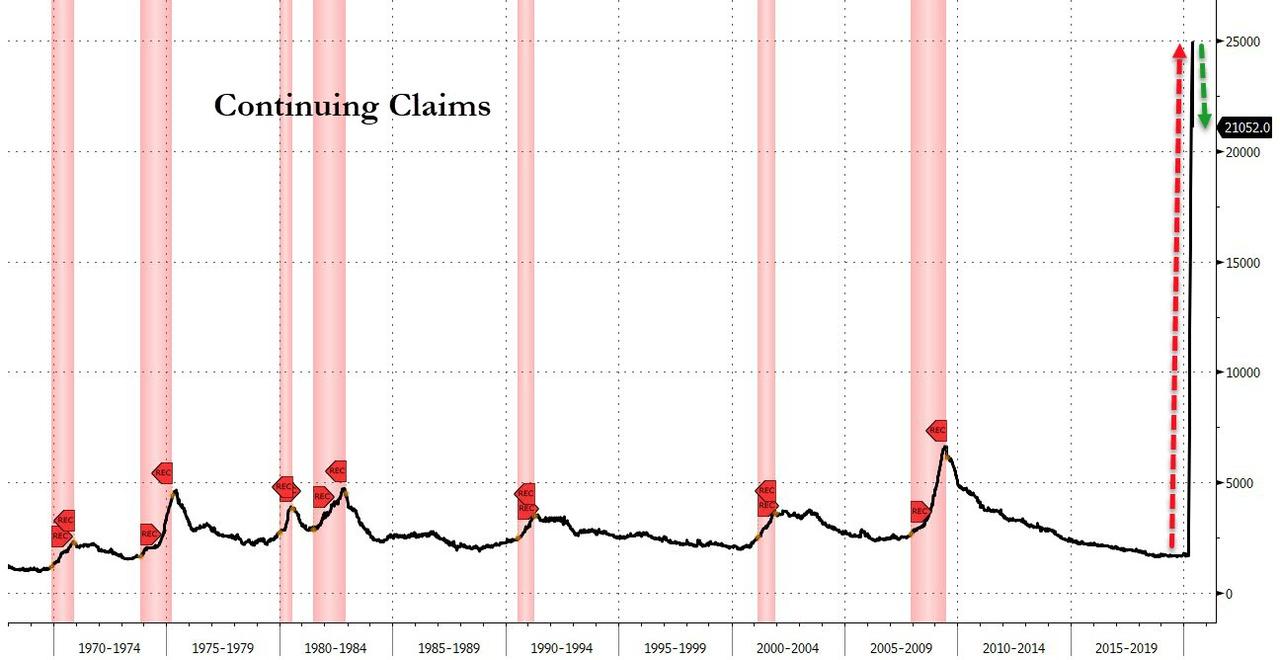

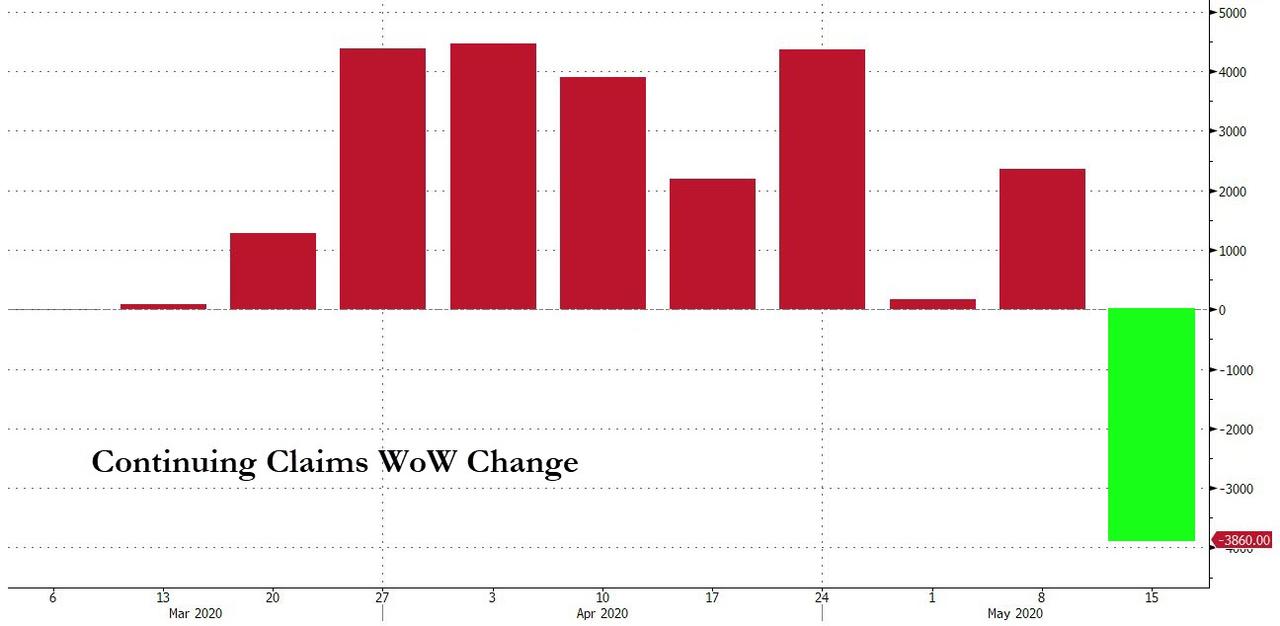

But continuing claims declined last week as it appears some of the reopenings are seeing people come off the dole…

Source: Bloomberg

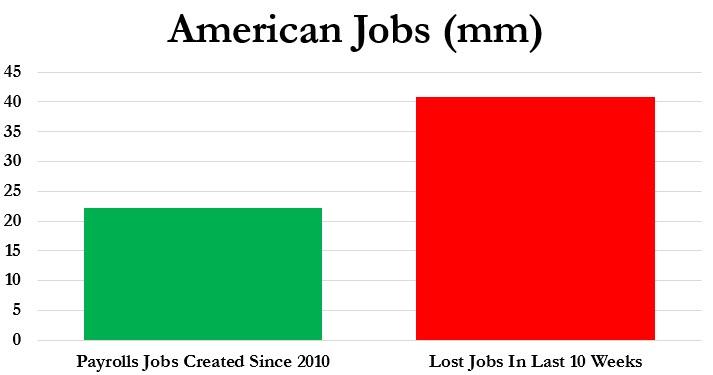

And as we noted previously, what is most disturbing is that in the last ten weeks, almost twice as many Americans have filed for unemployment than jobs gained during the last decade since the end of the Great Recession… (22.13 million gained in a decade, 40.767 million lost in 10 weeks)

Worse still, the final numbers will likely be worsened due to the bailout itself: as a reminder, the Coronavirus Aid, Relief, and Economic Security (CARES) Act, passed on March 27, could contribute to new records being reached in coming weeks as it increases eligibility for jobless claims to self-employed and gig workers, extends the maximum number of weeks that one can receive benefits, and provides an additional $600 per week until July 31. A recent WSJ article noted that this has created incentives for some businesses to temporarily furlough their employees, knowing that they will be covered financially as the economy is shutdown. Meanwhile, those making below $50k will generally be made whole and possibly be better off on unemployment benefits.

Additionally, families receiving food stamps can typically get a maximum benefit of $768, but through the increase in emergency benefits, the average five-person household can get an additional $240 monthly for buying food.

But, hey, there’s good news… stocks are near record highs and Treasury Secretary Steven Mnuchin said he anticipates most of the economy will restart by the end of August.

Finally, it is notable, we have lost XXX jobs for every confirmed US death from COVID-19 (100,442).

Was it worth it?

As Michael Snyder writes,if you tried to warn people in late 2019 that about 40 million Americans would lose their jobs by the middle of 2020, nobody would have believed you. Personally, I operate a website called “The Economic Collapse Blog”, and I wouldn’t have believed you either. Even though I have been loudly warning that this sort of an economic crisis was coming, I never imagined that we would lose so many jobs in such a short period of time. As I discussed the other day, more than a quarter of all jobs in the United States have already been wiped out, and the job losses just keep on coming. In fact, Boeing is currently in the process of laying off thousands of highly skilled workers…

Nearly 13,000 Boeing workers, mostly in the US, are set to lose their jobs in the coming weeks, as cuts at the American aerospace giant take effect.

More layoffs are expected, some of which may affect the UK.

The reductions had been expected since Boeing revealed plans last month to slash its global workforce by 10% – or roughly 16,000 jobs.

A lot of those are very high paying jobs with good benefits, and they will not be easy to replace.

Meanwhile, major retailers all over America keep going down one after another. On Wednesday, we learned that Tuesday Morning has decided to file for bankruptcy…

Off-price retailer Tuesday Morning filed for Chapter 11 bankruptcy protection Wednesday with plans to close more than a third of its stores.

Tuesday Morning had been struggling when the coronavirus pandemic began and went into a free fall when it was forced to temporarily close its locations due to the crisis.

Just like the Boeing jobs, these are jobs that are never going to come back.

At this point, there is no way that I can write about all of the companies that are laying off workers, but one more example that I found to be quite notable is the fact that even CBS News is letting people go…

“I’m really sorry,” network president Susan Zirinsky said Wednesday on an all-staff Zoom meeting about the cuts. “There is not a person who won’t be missed.”

CBS News was hit hard by a round of corporate cost-cutting that saw “a single-digit percentage” of the network’s news staffers laid off, according to an estimate given by network president Susan Zirinsky during a Wednesday afternoon all-hands conference.

The corporate elite that own CBS News have very deep pockets, and Americans are watching more news than ever right now, and so it is definitely not a good sign for the economy that even CBS News feels forced to lay off workers.

Of course many unemployed workers are not exactly “deeply suffering” yet because of the huge weekly bonuses that they are getting from the federal government right now.

Earlier today, I was directed to a post on a popular Internet forum where a newly unemployed worker was describing how great his life has become now that he is unemployed…

Before COVID I was miserable.

I had a job working $14.75/hr and hated waking up most days. I’ve since been laid off (obviously) but am one of those who is making much more by NOT working.

I used to make $550-600 per week depending on my hours but since COVID began, I’m clearing just over $1000/week. My gf is in the same situation and she’s also clearing just over $1000.

Without any job to go to, he can now spend his days endlessly hanging out with his newly unemployed girlfriend, and he claims that he can’t even imagine ever going back to his old life…

Today we plan to do some hiking since it’s going to be so nice out and I’ll be using my new grill to cook up some steak tonight. The gf is kind of a wine snob so she likes to splurge on really nice reds (which I’ll definitely be having later as well).

I really don’t understand people who say they’re more stressed or are fighting with their gf/wife more than before. It makes absolutely no sense to me. These have been the best 2 months I’ve had in a while. I can’t imagine going back to my old life and way of doing things. NOT HAPPENING!

The only thing that isn’t ideal right now is not being able to travel normally but I only vacationed once or twice a year before due to work/money issues. Now I’m able to save $800-1000/month with COVID stimulus and bonus so we’ll definitely be taking a nice vacation at some point this summer.

The bad news for this young couple and for tens of millions of other unemployed Americans is that President Trump and the Republicans in the U.S. Senate do not plan to extend the unemployment bonuses once they expire in July.

So from that point forward, there will be millions upon millions of Americans that are not able to pay their monthly bills.

In fact, the New York Times is already warning that we will soon be facing “a wave of evictions as government relief payments and legal protections run out for millions of out-of-work Americans”…

The United States, already wrestling with an economic collapse not seen in a generation, is facing a wave of evictions as government relief payments and legal protections run out for millions of out-of-work Americans who have little financial cushion and few choices when looking for new housing.

The hardest hit are tenants who had low incomes and little savings even before the pandemic, and whose housing costs ate up more of their paychecks. They were also more likely to work in industries where job losses have been particularly severe.

Initially, the generous unemployment bonuses that Congress passed were supposed to help tide unemployed workers over until this pandemic went away.

But what if it sticks around for multiple years like the Spanish Flu did?

And the Washington Post is now trying to convince us that there is “a good chance” that COVID-19 “will never go away”…

There’s a good chance the coronavirus will never go away.

Even after a vaccine is discovered and deployed, the coronavirus will likely remain for decades to come, circulating among the world’s population.

Yes, this virus could become a “permanent crisis”, and without a doubt the elite are already trying to use it to fundamentally reshape our society.

And as long as a certain percentage of the population is deeply afraid of this virus, economic activity will continue to be depressed at levels that are way below what we would consider to be “normal”.

As the New York Times has admitted, “an economic collapse” is already here, and it is going to be incredibly painful.

via ZeroHedge News https://ift.tt/2X9pDDr Tyler Durden

“Smoke pourin’ out a box car door… in the final end he won the wars, after losing every battle..”

Yesterday evening, I got away from the madness. I sat on the back of my boat in the sun having a chat with my chum Robert Hillman. He’s an uber-quant with Central Bank and Hedge Fund experience who now runs Neuron Capital, the economic modellers. Over a couple of socially distanced beers we discussed the virus, the economy, prices and markets. This morning’s porridge is loosely based upon what I can recall of our “debate” about virus risks and how the economy is likely to develop. (Very nice beers… How many? I have no idea..)

I started by explaining my current thesis:

Over the past few weeks there has been an extraordinary shift in the market’s mindset. We have moved from expectations of a stock market wipe-out and bond Armageddon into a full-blown expectations led rally. This is not about a bear-trap rally anymore – although it might become one again if the virus confounds us! In the next few days, I confidently expect stocks will make new record highs as governments are bounced (rightly or wrongly) into re-opening the global economy.

There is nothing normal about what’s happening. We are stuck in the middle of an economic crisis completely unlike anything that’s ever happened before. It’s not about banks or collapsing financial confidence. It’s a demand/supply shock and more – something wholly outside any previous experience. But, it’s something we are adapting to.

Investors are fully aware of the scale of the Coronovirus economic damage and the unknown consequences its’ triggered. They are now developing investment ideas on where this crisis and prices go next as economies rush to reopen. They are also factoring in how government bailouts and QE infinity have effectively shifted sentiment away from the precipice’s edge towards more positive uplands, and how new virus treatments and vaccines could ameliorate the crisis.

Markets are discounting prices for recovery.

The result is a rally in value stocks – i) those with clear economic upside from the end of lockdown, and ii) those where prices over-reacted and tumbled too far as we bought the worst-case coronavirus scenarios. (As always there are risks associated with guessing what future prices and activity will be. This time its even more dangerous because we still know so little about the virus and the complexity of this crisis on growth and economic activity.)

Let me illustrate the upside moves with one stock:

Ryanair’s stock price tumbled 50% from €16.05 in early February to €8.15 in Mid-March. Sentiment held the future of flying for business and holidays was toast – finished potentially for years. Aviation was the economic sector most shattered by the virus. It was game over for airlines, airports and plane makers. But since May 15th,Ryanair has rallied 45% from €8.45 to €11.74. The stock is still down 26% from its Feb peak, but the perception has shifted from airline stocks being doomed, to how much will they recover.

The market for airline stocks is anticipating how lockdown easing will change the bear scenario completely. Analysts are pointing to Southern European countries’ desperation to kick start tourism – which is an opportunity for Low Cost Carriers to get back into the mass-travel market. They expect initiatives like the UK imposing a 14-day quarantine from early June will be unravelled. The airlines are not going to accept flying planes 33% full because of social distancing. Holidaymakers will not accept the additional costs. I expect planes will be full again by August.

As lockdown restrictions ease, a more pragmatic approach to travel will be fuelled by the airline lobbyists: as virus deaths have been so concentrated in the elderly and infirm, then younger travellers and families should be able to take the miniscule virus risks, while the vulnerable continue to self-isolate. We’ll no doubt see Mick O’Leary make some incendiary remark about how it’s perfectly safe to fly in one of his sardine cans because the chances of anyone under 40 dying of the virus are less than a lightening strike.

We are seeing a similar effect right across the economy: a re-evaluation of how much virus triggered fears over-sold the market. The financial media is full of stories about the global economy emerging from its coronavirus hibernation. Activity is picking up everywhere. Governments are under enormous pressure to facilitate opening their economies. Every single business owner and industrial sector will come up with half-a-dozen reasons why their business is going to benefit from re-opening, and why they should be allowed to do so.

BUT!

We remain in dangerous times…

First, we still don’t really know as much as we should about the virus. We know it’s not just a flu because of all the other damage to our bodies it can do. We don’t fully understand infection and transmission – although we are getting there. What we do know: if you are one of the 20% who get it bad.. it’s very bad indeed.

The big questions about the virus remain: how many people are susceptible who could cause another crisis in the health services? Robert from Neuron Capital expects the next few weeks will provide answers – if lockdown easing results in increasing cases its likely to be on a regional basis. We know infections in places heavily hit, like London, are now minimal, but if contacts start to rise again, we could see the need for local lockdowns in cities in regions that went into lockdown before the virus took off. (That’s what seems to be happening in Korea’s new infections this morning – new regional outbreaks.)

Second, the economy has taken a massive shock in terms of supply and demand. Although this crisis is totally unlikely any previous financial crisis – money is running out at many firms. Despite all government support and the trillions raised by large corporates on the bond markets, its clear many mid-sized and smaller companies are struggling to qualify for rescue packages or loans. The Bank of England said 30% of UK coporates have liquidity buffers for 3 months or more. Neuron dug deeper and reckon less than 20% of firms in sectors like Transport Equipment and Machinery have such a buffer.

There are going to be breakdowns. After we discussed the US Volvo factory that had to shut soon after reopening because of supply issues, Robert said: “the low cash buffers in some manufacturing firms could be particularly concerning for further supply chain disruption, especially where customers have little or no ability to substitute other products.”

And, we are going to get a massive shift from growth investment strategies towards cost containment – which is why companies will cut costs and jobs. (Some firms may increase investments to build market share as the smart contrarian move! Expect to see lots of distressed asset plays in coming months in commercial property, housing, logistics and oil!)

Third, lest we forget equity and bond markets looked overpriced before we’d ever heard of COVID-19. We were already talking about the numbers of “Zombie” companies that couldn’t survive a full blown financial or economic crisis, and how a rates rise would result in massive number of defaults. The virus crisis was a trigger, but swift action by the authorities has kept the Zombies on life-support (???) (Zombies on Life Support? That must be about the most confused metaphor I’ve ever employed..!)

It’s difficult to argue that record stock prices, record bond market issuance and record low yields and bond spreads are justified when the global economy has just undergone such a fundamental shock with massive unemployment and rising debt nailed on?

I put a significant slice of my own investment portfolio into cash, anticipating a major correction in prices, and was prepared to pile back in once it happened. But I missed the bottom. It came too early. I was unconvinced by the price recovery that began in March. I am certainly not tempted to put my cash back to work when stocks are now a gnat’s crotchet of where they were pre-crisis.

Fourth – and this is the big problem… Consensus is breaking down. For a few weeks the globe was united against the virus. We saw cooperation on the grand scale. Then it started to breakdown. The virus has become another front in the developing China/US cold war.

Here in the UK, we’re witnessing a second Civil War break out. Its broadly aligned the same way as the Brexit civil war, but trust in the government is evaporating even faster. Polite discussion about the safest and most effective way to reopen the economy has been buried in bitter polemic and hyper-emotional fury over what the government has done and hasn’t. Boris has squandered his popularity and allowed his detractors to seize the moral high-ground. There has been enormous wasted energy focused on the pointless Dominic Cummings saga. April’s “wartime” unity has turned to bitter recrimination.

The sad fact is the Government hasn’t really done anything wrong (except for not doing the politically astute thing of shooting Cummings (twice) when it had the chance.) Economically Sunak has made all the right noises. The debates about Lockdown timing are pointless – the government acted on advice (which was based on limited information) and while mistakes were clearly made, the reasons the UK has the highest numbers in Europe probably make sense – for instance, London is unlike any other city in terms of connections and density.

The economy will recover.. but I suspect there is still a lot of noise to come..

Meanwhile.. in a galaxy far far away…

I will comment on the European Union’s €1.5 trillion power grab and the mutualisation of European debt in depth tomorrow (I hope).

TO BE CLEAR:

I don’t have any problem with the plans for the EU to increase its budget to finance crisis recovery. It’s a wonderful, generous and brave initiative. If workers in Germany, and the rest of prosperous Europe value increased European unity so highly let them make it happen! If they are willing to pay the pensions of Southern European workers, for their taxes to fund these economies and everything else that goes with them, while sacrificing yet more of their democratic sovereignty to the unelected Brussels nomenklatura, then good luck with this laudable European initiative. (US readers…. historically based sarcasm alert.)

via ZeroHedge News https://ift.tt/2XGRWs1 Tyler Durden

Futures Tread Water In Calm Before US-China Storm, Trump Twitter Crackdown Tyler Durden

Thu, 05/28/2020 – 08:11

The S&P’s remarkable stretch of posting gains in the overnight session continued for another day, with the S&P rising as high as 3,053, and last trading 9 points higher at 3,044, tracking global stocks higher, with Europe’s Stoxx 600 rising 1.3% to session highs as investors weighed again increased friction between America and China and the official passage of China’s National Security Law in defiance of Trump, against fresh fiscal stimulus promised by the European Union. Treasuries edged up, while the dollar was modestly lower even as traders “treaded water” ahead of further escalations in the US-China clash.

The S&P – which hit a three-month high on Wednesday, closing above the key psychological level of 3,000 amid growing evidence of a pick up in business activity – continued its levitation on Thursday despite a dip in Nasdaq futures, which turned lower amid fear President Trump’s upcoming social media executive order will target tech heavyweights and open door for penalties. Chipmakers, which are sensitive to China’s growth, were also under pressure, with Intel Corp and Advanced Micro Devices Inc dropping about 1% each in premarket trade.

In a bright spot, Boeing Co climbed 4.2%, the most among the 25 Dow components trading before the bell, after the planemaker said it had resumed production of its 737 MAX passenger jet at its Washington plant.

President Donald Trump has promised action over China’s new national security legislation for Hong Kong by the end of the week, and on Wednesday Mike Pompeo said the US will no longer consider Hong Kong autonomous from China, setting the stage for further sanctions.

Analysts have warned the souring relations between the world’s two largest economies in recent weeks over trade and the handling of the coronavirus outbreak pose the biggest threat to the stock market’s strong rally off the March lows, although so far markets have largely ignored such a risk. Today investors will also ignore the Labor Department’s latest data which is expected to show that more than another 2 million Americans sought unemployment benefits for the 10th straight week.

The Stoxx Europe 600 rose for a fourth session, a day after the EU boosted its spending pledge to battle the impact of the coronavirus to €2.4 trillion. A gauge of euro-area confidence inched up from a record low, adding to the bullish mood.

Earlier in the session, shares climbed throughout most of Asia, even as Hong Kong’s Hang Seng Index flirted with the lowest level since March after the U.S. said it could no longer certify Hong Kong’s political autonomy, a move that could have far-reaching consequences. Asian stocks were led by finance and industrials, after rising in the last session. Markets in the region were mixed, with Japan’s Topix Index and India’s S&P BSE Sensex Index rising, and Hong Kong’s Hang Seng Index and Taiwan’s Taiex Index falling on fears of a China crackdown. The Topix gained 1.8%, with DLE and Enish rising the most. The Shanghai Composite Index rose 0.3%, with Beijing Jingyuntong Tech and Gree Real Estate posting the biggest advances.

Here is a recap of the latest mostly chronological back and forth between the US and China, courtesy of RanSquawk

US House passed bill calling for sanctions on Chinese officials related to the crackdown on Uighur minorities as expected with the final vote count at 413-1, which sends the bill to US President Trump for signing.

China Embassy in US reiterated Hong Kong affairs are internal, while it added that US Security legislation is very narrow and China will take all necessary counter measures for meddling. Furthermore, it stated that China legislature will vote on security bill today and the law would allow China to establish security bases in Hong Kong to provide stability as per the Basic Law approved between China and Hong Kong.

Beijing is “prepared for the worst case scenario” with the US. Chinese government advisers said China expected tensions with the US to escalate, but Beijing’s retaliation would depend on US action, cited by SCMP. (SCMP) While the Global Times reported that China could strongly retaliate if US takes action on Hong Kong; could target US service industries.

China’s Parliament has voted to approve the Hong Kong National Security Bill, as expected. Subsequently, US to reportedly expel Chinese students with military school ties, according to sources via NYT.

Chinese Embassy said it is strongly dissatisfied and firmly opposes the Canadian court’s decision on the Huawei CFO, while it added that Canada is an accomplice to the US efforts to harm Huawei and Chinese tech, as well as urged for the immediate release of the CFO.

Economic optimism was boosted overnight by St. Louis Fed President James Bullard who said the American economy may already have bottomed even as Coronavirus deaths reached 100,000. Australia’s central bank chief said that country’s downturn may not be as severe as first thought. Investors have responding to the recovery by rotating into value stocks most punished in the coronavirus crash. Norwegian Cruise Line and Royal Caribbean Cruises are up more than 25% on Wall Street this week, while Europe’s TUI AG tour operator, Cineworld Group and EasyJet Plc airline have surged more than 35%. Traders will be closely watching today’s unemployment numbers in Washington for further clues on the state of the U.S. economy.

In rates, Treasuries traded in a narrow range with belly outperforming ahead of 7-year note auction at 1pm ET, the final event of this week’s cycle. Firm US equity index futures limited gains for Treasuries while bunds outperform after German regional CPI data. TSY yields were lower by ~1bp across belly intermediates while long-end trades slightly cheaper, steepening 7s30s by ~1.5bp ahead of 7Y supply event; bunds outperform by 2bp vs. Treasuries while gilts lag by 1.2bp

In FX, the Bloomberg Dollar Spot Index pared an earlier advance as European stocks advanced and U.S. equity futures were mostly higher, with traders weighing the reopening of economies against escalating tensions between Washington and Beijing. The euro touched its strongest level against the dollar since April 1 in the Asian session, only to give up those gains in London trading and hover around the 1.10 handle; yields on bunds and Treasuries edged lower. The pound swung between gains and losses; gilt yields reversed an early climb ahead of a speech by BOE’s Saunders where traders may look for his thoughts on negative interest rates. The Norwegian krone and the Canadian dollar were the worst performers as oil prices edged lower ahead of a weekly report over crude oil inventories. The Aussie recovered after earlier falling against the greenback as the world’s biggest economies continued to spar over a new security law in Hong Kong and China’s handling of the virus pandemic.

In commodities, WTI July and Brent August futures saw a session of modest losses thus far with the contracts meandering just around 32.60/bbl and 35.50/bbl respectively (vs. low of USD 31.14/bbl and USD 34.35/bbl) with some pointing to sentiment-led losses amid the rising tensions between US and China, whilst a surprise build in API Inventories (+8.7mln vs. Exp. -1.9mln) only added to the bearish tone.

U.S. economic data calendar includes second estimate 1Q GDP, durable goods orders, initial jobless claims (8:30am), April pending home sales (10am) and May Kansas City Fed manufacturing (11am); personal income/spending, PCE deflator, MNI Chicago PMI and University of Michigan consumer sentiment revision are ahead Friday

Market Snapshot

S&P 500 futures up 0.2% to 3,041.75

STOXX Europe 600 up 0.9% to 352.97

MXAP up 0.8% to 150.65

MXAPJ down 0.01% to 474.14

Nikkei up 2.3% to 21,916.31

Topix up 1.8% to 1,577.34

Hang Seng Index down 0.7% to 23,132.76

Shanghai Composite up 0.3% to 2,846.22

Sensex up 1.6% to 32,123.07

Australia S&P/ASX 200 up 1.3% to 5,851.10

Kospi down 0.1% to 2,028.54

German 10Y yield fell 1.0 bps to -0.424%

Euro down 0.09% to $1.0996

Italian 10Y yield fell 4.8 bps to 1.331%

Spanish 10Y yield fell 1.0 bps to 0.636%

Brent futures down 0.9% to $34.43/bbl

Gold spot up 0.7% to $1,721.09

U.S. Dollar Index down 0.2% to 98.92

Top Overnight News

Chinese lawmakers approved a proposal for sweeping new national security legislation in Hong Kong, defying a threat by U.S. President Donald Trump to respond strongly to a measure that democracy advocates say will curb essential freedoms in the city

Donald Trump is poised to take action Thursday that could bring a flurry of lawsuits down on Twitter, Facebook Inc. and other technology giants by having the government narrow liability protections that they enjoy for third parties’ posts, according to a draft of an executive order obtained by Bloomberg

Economic sentiment in the euro area rose to 67.5 in May from a record low 64.9 after companies started to reopen across the continent following the easing of pandemic restrictions; missed an forecast rise to 70.6

The global jobs slump caused by the coronavirus pandemic is bottoming out, if data from LinkedIn is a guide. The social networking platform says the percentage of its members who joined a new employer stabilized over the past six weeks, after plunging in March

Measures of high- frequency data and confidence increasingly suggest a bottom has been reached in the worst global recession since the Great Depression

Citigroup Inc. will gradually start bringing traders back to its London offices in the coming weeks as U.K. leaders continue to craft plans to ease social distancing restrictions

Asian equity markets traded mixed as China concerns counterbalanced the momentum from a firm Wall St handover where ongoing reopening efforts and a continued resurgence of cyclicals underpinned the major US indices. ASX 200 (+1.3%) was higher with the top weighted financials sector leading the broad gains in the index although energy lagged following a pullback in oil prices which was exacerbated by bearish inventory data, while Nikkei 225 (+2.3%) benefitted from favourable currency moves and the KOSPI (-0.1%) failed to stay afloat despite the BoK delivering a widely expected 25bps rate cut to bring the 7-Day Repo Rate to 0.50%. Elsewhere, Hang Seng (-0.7%) and Shanghai Comp. (+0.3%) were choppy with mainland China initially supported after another firm liquidity effort by the PBoC which injected CNY 240bln through 7-Day Reverse Repos. However, the gains were short-lived and Hong Kong markets underperformed due to the ongoing US-China tensions with Trump administration said to be considering suspending Hong Kong’s preferential tariff rate for exports to US which means they could face the same tariffs US had imposed on mainland China. Furthermore, Global Times suggested the nuclear option of dumping USD-denominated assets was among the tools for China to exert financial pain on the US and China’s Embassy in US stated that Beijing will take all necessary counter measures for meddling, while the US House passage of the sanctions bill for Uighur human rights abuses and Huawei’s CFO losing a key battle in the extradition case, all added to the ongoing toxic relationship between the world’s top economic powerhouses. Finally, 10yr JGBs were flat amid similar uneventful after-hours trade in T-notes and indecisiveness in stocks, as well as mixed results at today’s 2yr JGB auction.

Top Asian News

Nissan Reports Losses, New Turnaround Plan to Seek Growth

Taiwan Lowers 2020 Growth Forecast as Virus Weighs on Economy

Japan Says Economy Worsening Rapidly Even as Shutdowns Ease

European equities (Eurostoxx 50 +0.9%) have started the session on the front-foot once again as optimism surrounding reopening efforts across the continent continues to out-muscle concerns over mounting US-China tensions. HK-exposed HSBC (-2.1%) and Standard Chartered (-1.3%) are trading lower following reports that the Trump administration is reportedly considering suspending Hong Kong’s preferential US tariff rate for exports to US in response to China’s (now passed) security law. However, this is yet to have any major follow-through to broader sentiment with price action in Europe taking a similar shape to those of recent sessions with travel & leisure names top of the pile once again. Specifically, for the sector, easyJet (+8.5%) are trading higher after announcing that summer demand indications are improving and the Co. is to consult on a proposal to lower its headcount by up to 30%. In sympathy, Deutsche Lufthansa (+4.2%), Ryanair (+2.8%), IAG (+2.3%) are all trading firmer once again. However, it is worth noting that the Stoxx 600 travel & leisure index is still trading lower by around 30% YTD. In-fitting with the theme of optimism surrounding travel names and reports yesterday that Boeing has resumed production at its Renton facility and will gradually ramp up output over the year, supplier Safran are trading higher by 2.8%. Elsewhere, support has been seen for the tech sector with the likes of Dialog Semiconductor (+3.8%), STMicroelectronics (+3.8%) and Infineon (+3.1%) bolstered by US-listed Micron Technology raising its Q3 revenue forecast yesterday. To the downside, Centrica (-3.3%) are a noteworthy laggard with the Times noting that the Co. could be at risk of losing its place in the FTSE 100. The article also noted that Carnival, easyJet, Meggitt, ITV, M&G and Prudential could also face the chop in what could be one of the largest reshuffles since the GFC.

Top European News

Swedish Dirty Money Affair Brings Bankers Closer to Police

Euro- Area Confidence Inches Up From Record Low as Lockdown Eased

In FX, there was little action thus far in the broader Dollar and index as the latter pivots 99.000 having printed an overnight base at 98.773 and a current high at its 100DMA at 99.034. Tensions between US and China will remain a theme with no apparent signs of subsiding for now – with Hong Kong no longer deemed autonomous from China and Beijing reiterating its readiness to retaliate over interference. USD/CNY traded on the softer side of 7.1530-7.1680 band after the PBoC set a firmer CNY fixing than expected, albeit weaker vs. yesterday. CNH meanwhile remains flat around 7.1450 vs. USD after the pair yesterday threatened a fresh record high at 7.1965. In terms of scheduled events State-side, today’s docket sees US Durable Goods and Q1 GDP (2nd) with the former expected to deteriorate further whilst the latter expects no revisions. Fed’s voter Williams is unlikely to add much meat to the bones following yesterday’s remarks.

AUD, NZD, CAD – All choppy within tight ranges vs. the Buck after earlier sensitivity to the escalating spat between US and China. AUD/USD dipped below 0.6600 despite RBA governor Lowe firmly dismissing negative rate – with some pointing to profit-taking amid trade risk. The pair recovered off lows around 0.6590 vs. high 0.6635. Elsewhere, the RBNZ Financial System Policy chief played down financial stability concerns from negative rates. The Kiwi reversed its earlier move lower but remains sub-0.6200 vs. the Dollar, having had failed to sustain gains above its 100 DMA at the round figure. Meanwhile, the Loonie also tracks softer energy prices with USD/CAD gaining ground above its 100 DMA (1.3709) and eyes a retest of 1.38 to the upside ahead of Q1 Canadian Current account data and stale average weekly earnings for March.

GBP, EUR – Mixed trade with Cable choppy whilst EUR/USD treads water at 1.1000 following an uneventful start to the session. The Single currency side-lined German regional prelim CPIs – largely followed the expectations for the nationwide release – alongside a mixed EZ sentiment survey. EUR/USD sees EUR 960mln opex at 1.0995-1.1000 with a further EUR 900mln between 1.1020-25 ahead of a Fib level around the 1.1050 psychological level. Saunders did little to change the overall narrative by said it safer to err on the side of easing too much and then tighten if necessary. Meanwhile, the wider focus remains on any hiccups over negotiations both regarding the EU Recovery Fund among EU27 and post-Brexit trade FTA between UK and the EU.

JPY, CHF – Safe-haven FX trade on the softer side in daily ranges but more so on Dollar influence amid an indecisive risk tone. USD/JPY prods its 50/55 DMAs at 107.84-86 ahead of session highs 107.89 (low 107.67) and with a chunky USD 1.8bln in options expiring at stroke 107.90. USD/CHF oscillates on either side of 0.9700 but within a tight range of 0.9670-9705 relative to yesterday’s trade.

RBA Governor Lowe said they will maintain expansionary settings until progress is being made towards employment and we are confident on inflation and said there will be a further decline in employment for May but jobs data was not as bad as previously thought. Lowe also stated that 25bps Cash Rate is effectively as low as it can go and that rates are to stay this low for some years and that they could purchase more government bonds if more QE is needed but does not currently see a need to do so, while he suggested that negative rates are extraordinary unlikely which come with a cost to the financial system and that he doesn’t think negative rates will work. (Newswires)

In commodities, WTI July and Brent August futures see a session of modest losses thus far with the contracts meandering just around USD 32.60/bbl and USD 35.50/bbl respectively (vs. low of USD 31.14/bbl and USD 34.35/bbl) with some pointing to sentiment-led losses amid the rising tensions between US and China, whilst a surprise build in Private Inventories (+8.7mln vs. Exp. -1.9mln) only added to the bearish tone. Some downside could be emanating from reports that Russian Co’s have been raising concerns regarding maintaining cuts with Energy Minister Novak after softly rejecting an extension of current cuts past June – stating that the market could rebalance sometime between June/July. Elsewhere, spot gold sees inflows and investors stock up on the yellow metal ahead of potential US-China tit-for-tat measures. Prices gain a firmer footing above USD 1700/oz and reside around session highs north of USD 1720/oz.

US Event Calendar

8:30am: Durable Goods Orders, est. -19.05%, prior -14.7%

8:30am: Cap Goods Orders Nondef Ex Air, est. -10.0%, prior -0.1%

8:30am: Cap Goods Ship Nondef Ex Air, est. -12.2%, prior -0.2%

8:30am: GDP Annualized QoQ, est. -4.8%, prior -4.8%

8:30am: Personal Consumption, est. -7.5%, prior -7.6%

8:30am: GDP Price Index, est. 1.3%, prior 1.3%

8:30am: Core PCE QoQ, est. 1.8%, prior 1.8%

8:30am: Durables Ex Transportation, est. -15.0%, prior -0.4%

8:30am: Initial Jobless Claims, est. 2.1m, prior 2.44m; Continuing Claims, est. 25.7m, prior 25.1m

9:45am: Bloomberg Consumer Comfort, prior 34.7

10am: Pending Home Sales MoM, est. -17.0%, prior -20.8%; Pending Home Sales NSA YoY, est. -28.65%, prior -14.5%

11am: Kansas City Fed Manf. Activity, est. -22, prior -30

DB’s Jim Reid concludes the overnight wrap

Every night when I’m home, which is unsurprisingly all the time at the moment, I tend to put the twins to bed and my wife puts Maisie to bed. Out of nowhere last night Maisie asked me to put her to bed for the first time in ages. I wasn’t warned as to how her bedtime routine had changed since I last did it. Unless she was having me on she gets two stories and then is allowed two questions that she wants answers to. Her two questions last night to me were 1) how is conditioner and shampoo made? and 2) how are mirrors made? I had no idea so rather than bluff my way through I showed her a couple of YouTube videos on my phone explaining it. She then said “Daddy, I’d be so much cleverer if you bought me a phone”. She’s 4 and three quarters!! However at least she didn’t ask me to explain why US equities are within a few percentage points of their all-time high again even though large parts of the global economy remain closed. I’m not sure there’s a video for that. Maybe I’d show her a clip of an oil well gushing as a symbol for the remarkable liquidity out there at the moment.

On that note global equities continued their rally yesterday as optimism around vaccines, economies reopening, and the unveiling of a proposal for a €750bn EU recovery fund outweighed another exchange of salvos in the recent US-China sparing match.

The rally indeed survived a US midday dip after an announcement that the US would no longer consider Hong Kong politically separate from China. At that point, the S&P fell to -0.47% on the day. However, by the end of the session the S&P 500 had finished up +1.48% to close over 3000 for the first time since March 5 – reaching an 11-week high. Also helping were remarks by Dr. Fauci, the U.S. government’s top infectious-disease expert, who said there’s a “good chance” a vaccine may be available by November or December.

Yesterday’s rally was much like the day before, with virus laggards leading the broad index while the recent winners lagged. All 24 industry groups finished higher, but one element of the recent leg higher to pay attention to is the into-value-out-of-growth rotation. Bank stocks led yesterday’s rally, up +6.70% on the day and up +15.09% over the last 2 days, compared to the +0.42% Technology sector’s 2-day return. A remarkable turn.

Europe also rose as the STOXX 600 climbed +0.24%. The DAX was up +1.33% and at a 10-week high, the CAC was up +1.79%, the FTSE was +1.26%, while the FTSEMIB also barely outperformed the broader index at +0.28%.

Europe was generally feeding off the European Commission recovery fund plan. President von der Leyen presented a proposal for a €750bn EU recovery instrument, €500bn of which would be distributed in the form of grants and the other €250bn in loans to member states. The debt would be repaid through higher future contributions to the EU budget and possible new revenue streams, including an Emissions Trading Scheme, a tax on high-emission imports and a tax on digital companies. The plan still requires the support of EU member states, and while Chancellor Merkel and President Macron have offered their support, some of the northern countries have balked at the idea of offering grants rather than loans. This comes on top of an EU Budget of €1100bn over the next seven year that roughly matches the pre-COVID-19 proposal from February. See our European economists views on the new proposals here.

The EC’s proposal came shortly after ECB President Lagarde announced that the euro-area economy is set to see output shrink by between 8-12% this year, in line with the central bank’s most pessimistic forecasts. Lagarde will have a better idea when the numbers are published in early June, but said “it’s likely we will be in between the medium and severe scenarios.” In light of the need for further stimulus, Lagarde was confident that higher public spending would not cause a debt crisis. This is especially true if the spending is used to increase country’s productivity, the “use of debt is not only recommended, it’s the way to go.”

The news of the pending recovery plan and especially the mix of grants and loans proposed were net positive for peripheral spreads yesterday. Greek 10yr bonds tightened the most (-9.4bps) to German 10yr bunds. Italian BTPs were -6.3bps tighter, while Portuguese bonds tightened -7.0bps. Spanish bonds, on the other hand, were mostly unchanged.

German 10yr bond yields were +1.5bps higher to -0.414%. In other sovereign debt, US 10yr treasuries rallied even as equities continued to outperform with yields -1.1bps lower to 0.685%. European credit also benefited from the news yesterday, with high yield cash spreads -25bps tighter. Euro IG tightened -7bps on the day, while US HY and IG cash spreads tightened -5bps and -2bps respectively.

Oil prices had their worst day in some time though as news came out that Moscow wanted to scale back its cuts once the current agreement lapses in July. Even though President Putin and Saudi Arabia later pledged to continue coordinating ahead of the OPEC+ meeting in early June, WTI front-month futures fell -4.40%, the largest one-day fall in a month, while Brent crude futures fell -3.79%, the most since 11 May.

Overnight, Asian markets have traded more mixed with the Nikkei (+1.24%) and ASX (+1.08%) posting gains while the Hang Seng (-1.81%) and Shanghai Comp (-0.35%) are down following the US announcement mentioned at the top. The Kospi has also faded to trade down -0.83% after the Bank of Korea cut rates by 25bps to a record low of 0.5%. The BoK also cut the GDP growth target to -0.2% yoy from a forecast of +2.1% yoy growth in February. One talking point from the press conference was the reference by Governor Lee to “should it be deemed necessary to expand the accommodative stance of monetary policy further, we could actively respond with policy tools other than rates”. Our economists have previously suggested that the BoK could go down the YCC route.

Moving on. The positive risk moves yesterday were weighed down somewhat by another round of tensions tightening between the US and China. Following reports on Tuesday that the US was looking to sanction China over implementing a new national security law, which would curtail the rights and freedoms of Hong Kong citizens, Secretary of State Pompeo said yesterday that the U.S. has certified Hong Kong is no longer autonomous from China politically. The move could have consequences on Hong Kong’s special trading status with the US. The CCP-aligned Global Times posited that a countermeasure to Pompeo’s move would be to expedite the new security law’s progress. After the market closed, the US House voted almost unanimously (413-1) to pass the Senate’s bill authorizing sanctions against Chinese officials for human rights abuses against Muslim minorities. The bill now goes to President Trump’s desk, who has not indicated how he will proceed. On the trade front, there was a Bloomberg report that China is looking to buy Brazilian soybeans – while not bidding for American soy yesterday – in a sign that the country is readying for another round of tensions with the US. With virus cases appearing to remain in-check in most developed economies and economies starting to slowly reopen, a deterioration in this relationship may be risk factor to pay attention to.

Yesterday, there was not much data to mention, though the Fed released its Beige Book, which collects anecdotal information on current conditions. The highlights included that many contacts expressed hope that overall activity would increase when businesses reopened, but that the outlook remained uncertain and they were pessimistic about the pace of recovery. The other development of note was the challenges to get employees back to work, including workers’ health concerns, limited access to childcare, and generous unemployment insurance benefits. Also in the US, the Richmond Fed manufacturing survey came in at -27 (vs. -40 expected), up from -53 last month. In Europe, France released business and manufacturing confidence readings. Business confidence was up to 59 (below the 69 expected) from 53, while manufacturing confidence was up to 70 (below the 85 expected) from 68 (revised down from 82). The absolute readings of both confidence indicators are near the record lows seen in 2009 and 1993.

In terms of data for today, weekly jobless claims are likely to continue improving but still remain over three times as high as the pre-coronavirus record high. Our US economists are forecasting a 2.1m reading for the week through May 23, compared to the 2.438m last week. Individual states continue to have problems with the massive number of initial filers and so there may be heavy revisions. If initial claims do come in less than last week, they will have slowed for their eighth straight week, a strong signal we are likely well beyond the peak.

To the rest of the day ahead now, data out of Europe will include consumer and economic confidence readings for the Euro Area, Italy’s May consumer confidence index levels and Germany’s preliminary May CPI print. In the US, the second estimate of Q1 GDP will be released along with the aforementioned weekly initial jobless claims. There will also be US durable goods orders, capital goods orders, pending home sales and May Kansas City Fed manufacturing activity readings. The Bank of Korea will release their monetary policy decision, in addition to remarks from the Fed’s Williams. Finally, earnings releases include Salesforce, Costco, Dollar General, and Nissan.

via ZeroHedge News https://ift.tt/2zDqJ1d Tyler Durden

“Internet Platforms Aren’t Arbiters Of Truth” – Zuckerberg Blasts Twitter For Tagging Trump Tweets As “Misinformation” Tyler Durden

Thu, 05/28/2020 – 07:52

As President Trump prepares to sign an executive order targeting “left-leaning bias” on American social media platforms, Facebook CEO Mark Zuckerberg has embarked on a round of interviews with cable news – ostensibly to discuss Facebook’s new Work From Home policy – where he castigated Twitter CEO Jack Dorsey for voluntarily transforming Twitter into an “arbiter of truth”.

Asked to comment in Twitter’s decision to tag two Trump tweets as “misinformation” by CNBC’s Andrew Ross Sorkin, Zuckerberg replied that “I don’t think that Facebook or internet platforms in general should be arbiters of truth…Political speech is one of the most sensitive parts in a democracy, and people should be able to see what politicians say.”

Although Facebook does use independent fact-checkers to screen content, they’re really only there to “catch the worst of the worst stuff.”

“The point of that program isn’t to try to parse words on is something slightly true or false…in terms of political speech, again, I think you want to give broad deference to the political process and political speech,” Zuck said.

This isn’t exactly a surprise: Facebook said back in October that it would allow political ads on its platform, even if they contained “misinformation”. The left threw a screaming tantrum over this decision, while conservatives applauded the Facebook CEO for standing up to the left’s rage politics.

Still, Facebook has lines that nobody – including politicians – are allowed to cross. Zuck cited a recent incident where Facebook removed a post by Brazilian President Jair Bolsonaro touting hydroxychloroquine and chloroquine as ‘miracle cures’ for the coronavirus, despite research showing the medications might be harmful to patients suffering from severe COVID-19 symptoms.

“There are clear lines that map to specific harms and damage that can be done where we take down the content,” he said. “But overall, including compared to some of the other companies, we try to be more on the side of giving people a voice and free expression.”

Zuckerberg made similar comments during a recent appearance on Fox News.

Asked about Trump’s threat to crack down on social media companies for discriminating against conservatives, the CEO said that fighting censorship with censorship didn’t strike him as the correct response.

“I have to understand what they actually would intend to do,” Zuckerberg said in response to the president’s warning. “But in general, I think a government choosing to to censor a platform because they’re worried about censorship doesn’t exactly strike me as the the right reflex there.”

In a series of tweets, Twitter CEO Jack Dorsey doubled-down on his decision, and insisted that Twitter wasn’t positioning itself as an “arbiter of truth”.

Fact check: there is someone ultimately accountable for our actions as a company, and that’s me. Please leave our employees out of this. We’ll continue to point out incorrect or disputed information about elections globally. And we will admit to and own any mistakes we make.

This does not make us an “arbiter of truth.” Our intention is to connect the dots of conflicting statements and show the information in dispute so people can judge for themselves. More transparency from us is critical so folks can clearly see the why behind our actions.

Per our Civic Integrity policy (https://t.co/uQ0AoPtoCm), the tweets yesterday may mislead people into thinking they don’t need to register to get a ballot (only registered voters receive ballots). We’re updating the link on @realDonaldTrump’s tweet to make this more clear.

But as Zuckerberg pointed out during his conversation on CNBC, there’s already been a flood of media coverage of Trump’s tweets, plus thousands of angry replies calling Trump a racist and a liar.

If Twitter users can’t “connect the dots” on their own, is it really Twitter’s responsibility to do readers’ critical thinking for them?

Watch CNBC’s full Mark Zuckerberg interview below:

via ZeroHedge News https://ift.tt/36AFQV8 Tyler Durden

Senator Says China Tariffs Will Now Apply To Hong Kong As Beijing Approves “National Security” Law Tyler Durden

Thu, 05/28/2020 – 07:06

Update (0800ET): During an interview on CNBC Thursday morning, GOP Sen. Pat Toomey said he expects China tariffs will be expanded to also apply to Hong Kong as the US prepares to strip the ‘special administrative region’ of China of its preferred trade status. Wall Street analysts pointed out on Wednesday that the move could disrupt some $38 billion in bilateral trade between the US and HK.

SEN. TOOMEY: HONG KONG MAY BECOME SUBJECT TO CHINA TARIFFS… seems like its all in the price and will just hurt HK status as a trading and financial hub

One day after the US declared that Hong Kong is no longer “autonomous” from Beijing, China’s Politburo Standing Committee on Thursday officially wove a controversial new “National Security” resolution that was approved during last week’s National Party Congress into Hong Kong’s ‘Basic Law’ – the de facto constitution left by the British – in defiance of President Trump, and a broader backlash across the West, which has repeatedly stood up to defend Hong Kong’s freedoms.

According to the NYT, Beijing will probably initiate a far-reaching ‘crackdown’ to impose the new law on Hong Kong once it takes effect in September.

Activist groups could be banned. Courts could impose long jail sentences for national security violations. China’s feared security agencies could operate openly in the city.

As we reported last night, losing its ‘special status’ conferred by the US could strip Hong Kong of its ‘international city’ designation. As one expert said, Beijing no longer cares about “killing the golden goose” – that is, closing what has been for decades a critical portal to the West and the global financial system.

It’s still unclear how many of Hong Kong’s freedoms Beijing intends to strip away: this won’t become clear until later in the year.

Per the NYT, Hong Kong’s Chief Executive Carrie Lam appeared to hint that certain civil liberties might not be an enduring feature of Hong Kong life. “We are a very free society, so for the time being, people have the freedom to say whatever they want to say,” said the chief executive, Carrie Lam, noting, “Rights and freedoms are not absolute.”

Though US equity futures pointed to a higher open again on Thursday, analysts cautioned that the growing tensions could trigger a massive “risk off” move in markets in the situation escalates. Pictet’s Luca Paolini said on Bloomberg Television that markets seem to be ignoring this because they’re assuming it’s just rhetoric.

“For now it’s just words, but if the escalation takes place it’s the worst possible time to have this kind of escalation considering the global economy continues to be incredibly weak,” Paolini said.

via ZeroHedge News https://ift.tt/2XaDWYw Tyler Durden

White House Expels Chinese Grad Students With Ties To People’s Liberation Army Tyler Durden

Thu, 05/28/2020 – 06:33

As President Trump prepares to sign a bill imposing new sanctions on Chinese officials involved with the country’s sprawling security state, the White House has just unveiled its latest measure to turn up the pressure on Beijing: Chinese grad students with ties to the PLA will be barred from returning.

The news comes as China’s Politburo Standing Committee officially weaves a new “National Security” law effectively barring political dissent into HK’s Basic Law, according to the NYT.

Per the NYT, the Trump administration plans to cancel the visas of thousands of Chinese graduate students and researchers studying at US Universities who have ties to the People’s Liberation Army, according to anonymous administration officials.

This isn’t the first time the White House has considered barring some or all Chinese students in the US. Back in 2018, the FT reported that the Trump administration had considered banning all Chinese students from the United States – an idea that was attributed to Trump advisor Stephen Miller.

And according to the NYT, this measure has been in the works for some time, and was being considered before China moved to crack down on Hong Kong’s autonomy.

Moreover, this might not be the end of Trump’s retaliation: The president has a long list of possible responses to China’s plans to impose a national security law on Hong Kong, according to Assistant Secretary of State for East Asian and Pacific Affairs David Stilwell, who spoke to reporters last night.

via ZeroHedge News https://ift.tt/3gx4nza Tyler Durden

Swiss National Bank Ready To Buy Much More Tech Stocks To Weaken The Franc Tyler Durden

Thu, 05/28/2020 – 06:30

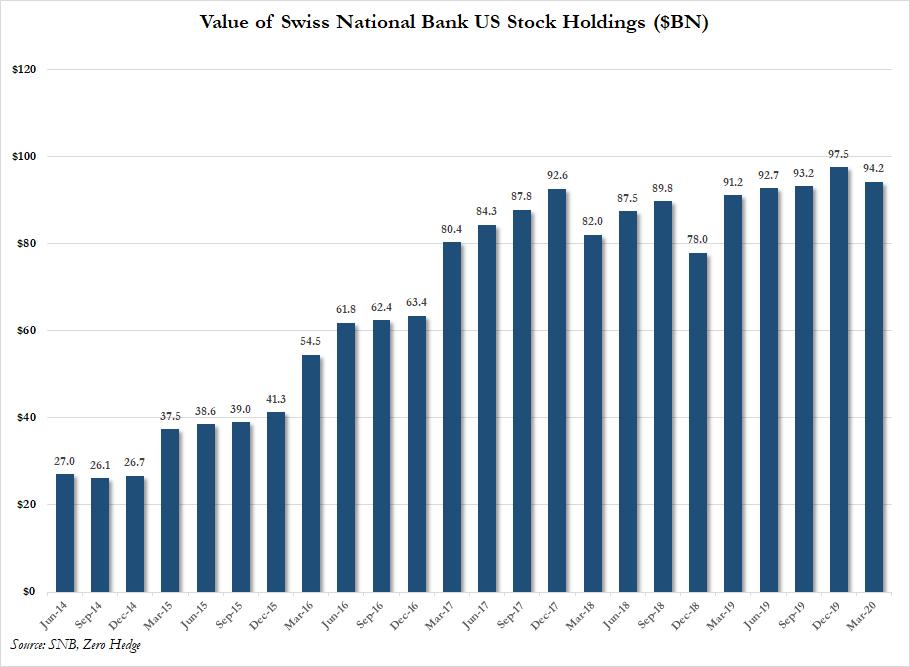

Two weeks ago, with traders and analysts wondering who has been aggressively buying stocks in the past 2 months as markets tumbled – besides retail investors of course – we gave the answer: the money-printing (literally) hedge fund known as the Swiss National Bank.

As we explained then, we showed that as the value of the SNB’s US equity holdings increased more than threefold, from $26.7 billion in Dec 2014 to $97.5 billion in Dec 2019….

… the SNB had kept its total holdings relatively flat for the past year, conserving its dry powder for just the right occasion, an occasion which materialized in March, and the Swiss National Bank went on a buying spree as markets crashed, adding roughly 22% (on average) to its top positions.

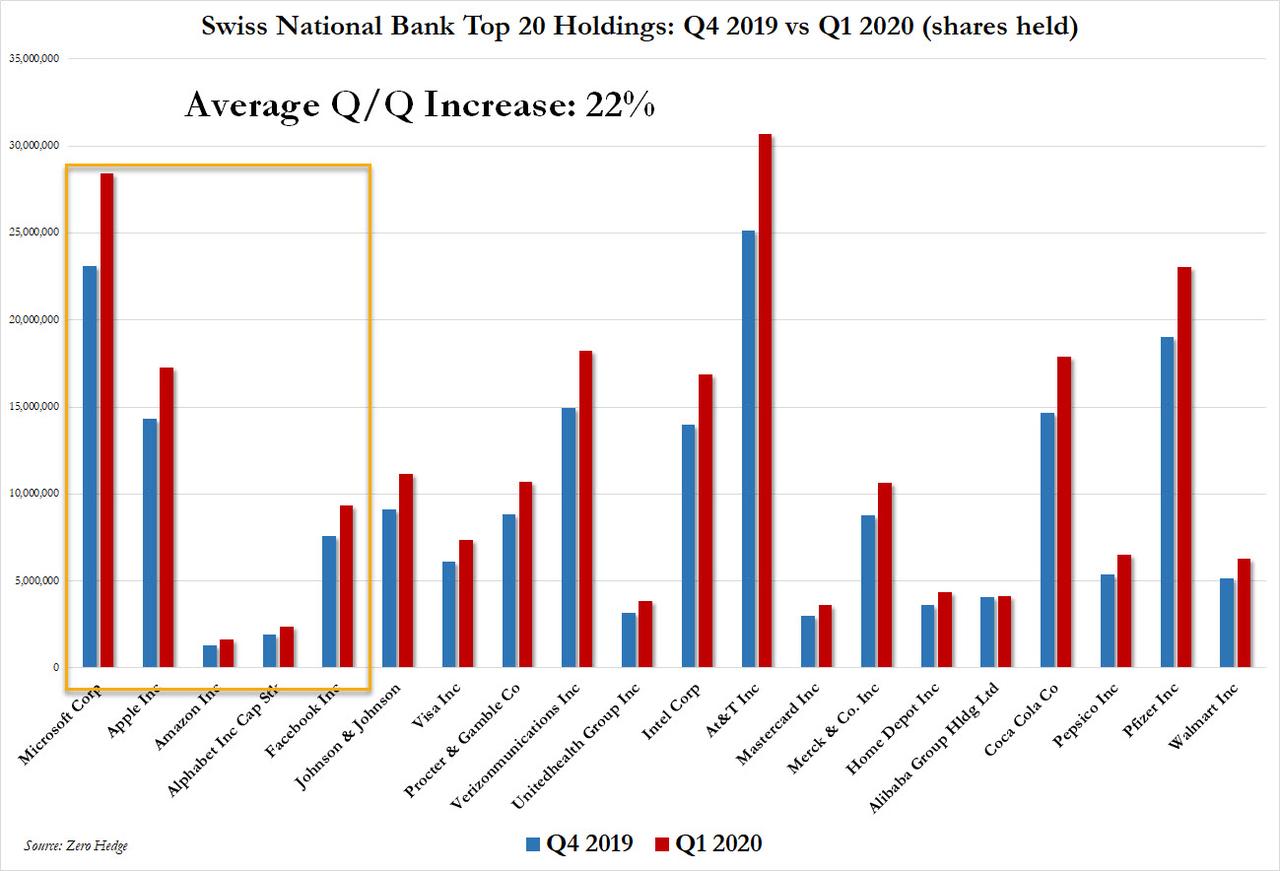

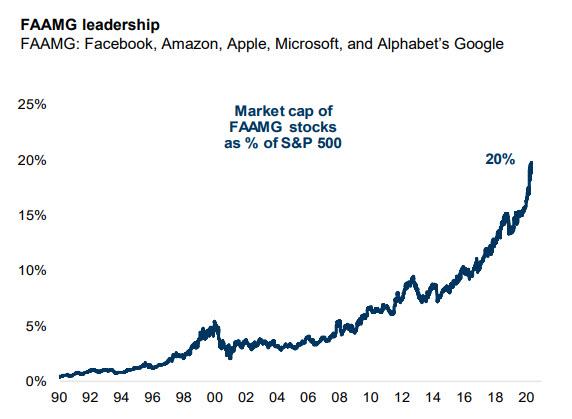

Also according to the SNB’s latest 13F, as of March 31, the central bank owned $4.5 billion in Microsoft shares, $4.4 billion in Apple, $3.2 billion in Amazon, $2.7 billion in Google and $1.6 billion in Facebook, also known as the FAAMG stocks which as everyone knows by now, have become the market leaders, accounting for over 20% of the S&P’s market cap.

And the punchline: the SNB added approximately 22% to its holdings of each of the FAAMGs in Q1 as follows:

MSFT: +23%

AAPL: +21%

AMZN: +23%

GOOGL: +22%

FB: +23%

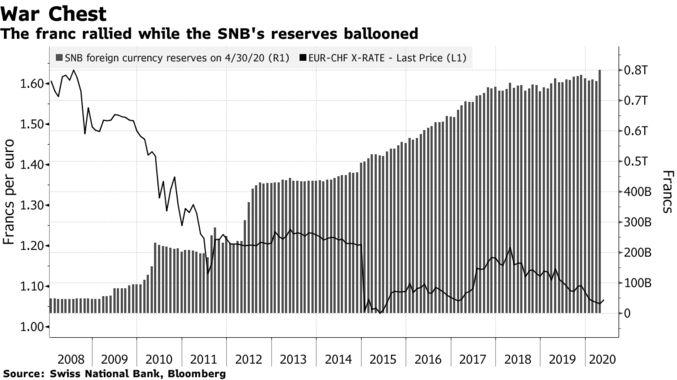

In short, to keep the value of its portfolio of US stocks relatively flat at $100BN, the SNB unleashed a massive buying spree that boosted its FAAMG holdings by over 20%, which in turn sent the bank’s foreign currency reserves – roughly $100BN of which are parked in the US stock market – to an all time high.

As a reminder, the SNB is one of the few central banks – the BOJ being the other – which openly buys equities in order to keep the value of the Swiss franc from rising too rapidly. The fund flow is simple: the SNB prints CHFs, which it then sells for USDollars – in the process depressing the value of one of the world’s most sought after safe haven currencies – and uses the proceeds to buy US stocks of which it owns about $100 billion. In many ways, this is similar to what the Fed does, only instead of buying Tsys, MBS, and now corporate bonds, the SNB is buying equities.

Simple enough.

And now, in order to convinced currency speculators to stay away from the Swiss Franc which, similar to the dollar, has seen an impressive surge in recent months, the Swiss National Bank announced on Wednesday that is intervening more heavily in the foreign exchange market to weaken the franc and can further cut interest rates, if a cost-benefit analysis warrants such a step, SNB President Thomas Jordan said.

“We have room to maneuver for both instruments,” Jordan said at a panel discussion hosted by UBS Group AG. “It’s clear that we have the possibility to cut rates if necessary.”

He may be telling the truth, although some wonder: with the SNB having cut the Swiss deposit rate to a record low -0.75% plus a pledge to wage foreign exchange market interventions to keep the franc in check, some have suggested that it is approaching the reversal rate beyond which any further cuts hurt not help the economy. Yet with pressure on the haven currency rising as a result of the coronavirus pandemic, Bloomberg notes that Swiss central bank officials said they’d picked up the pace of activity, something we already discussed when we noted that in Q1 the SNB unleashed a massive buying spree of US stocks.

Addressing the SNB’s policy dilemma, whereby further rate cuts may now be self-defeating, Jordan said any policy step required a cost-benefit assessment and that the SNB would enlarge its balance sheet via interventions if the pros outweighed the cons. And due to the unique nature of the SNB, what Jordan really meant, is that he is willing to buy even more tech stocks should the franc continue to rise.

We bring this up just in case there is still confusion just who was buying FAAMGs and tech names as everything else crashed.

We also bring it up to bring some clarity to a truly bizarro world: one where, the worse the global economy gets, the more aggressively at least one central bank to buying US tech stocks.

via ZeroHedge News https://ift.tt/2X9EkGH Tyler Durden

To exorcise my worst fears about the coming decade, I chose to write a bleak chronicle of it.

If, by December 2030, developments have invalidated it, I hope such dreary prognoses will have played a part by spurring us to appropriate action.

Before our pandemic-induced lockdowns, politics seemed to be a game. Political parties behaved like sports teams having good or bad days, scoring points that propelled them up a league table that, at season’s end, determined who would form a government and then do next to nothing.

Then, the COVID-19 pandemic stripped away the veneer of indifference to reveal the political reality: some people do have the power to tell the rest of us what to do. Lenin’s description of politics as “who does what to whom” seemed more apt than ever.

By June 2020, as lockdowns began to ease, left-wing optimism that the pandemic would revive state power on behalf of the powerless remained, leading friends to fantasize about a renaissance of the commons and a capacious definition of public goods. Margaret Thatcher, I would remind them, left the British state larger, more powerful, and more concentrated than she had found it.

An authoritarian state was necessary to support markets controlled by corporations and banks. Those in authority have never hesitated to harness massive government intervention to the preservation of oligarchic power. Why should a pandemic change that?

As a result of COVID-19, the grim reaper almost claimed both the British prime minister and the Prince of Wales, and even Hollywood’s nicest star. But it was the poorer and the browner that the reaper actually did claim. They were easy pickings.

It’s not hard to understand why. Disempowerment breeds poverty, which ages people faster and, ultimately, readies them for the cull. In the shadow of falling prices, wages, and interest rates, it was never likely that the spirit of solidarity, which soothed our souls during lockdowns, would translate into the use of state power to strengthen the weak and vulnerable.

On the contrary, it was megafirms and the ultra-rich that were grateful socialism was alive and well. Fearing that the masses, condemned to the savage arena of unfettered markets amid a public-health disaster, would no longer be able to afford to buy their products, they reallocated their spending to shares, yachts, and mansions. Thanks to the freshly printed money central banks pumped into them via the usual financiers, stock markets flourished as economies collapsed. Wall Street bankers assuaged their guilt, lingering since 2008, by letting middle-class customers fight over the scraps.

Plans for the green transition, which young climate activists had put on the agenda before 2020, were given only lip service as governments buckled under towering mountains of debt. Precautionary saving by the many reinforced the economic depression, yielding industrial-scale discontent on a browning planet.

The disconnect between the financial world and the real world, in which billions struggled, inevitably widened. And with it grew the discontent that gave rise to the political monsters I was warning my left-leaning friends about.

As in the 1930s, in the souls of many, the grapes of wrath were growing heavy for a new, bitter vintage. In place of the 1930s soapboxes from which demagogues promised to restore dignity to the disgruntled masses, Big Tech provided apps and social networks perfectly suited for the task.

Once communities surrendered to the fear of infection, human rights seemed an unaffordable luxury. Big Tech developed biometric bracelets to monitor our vital data around the clock. In cahoots with governments, they combined the output with geolocation data, fed it all into algorithms, and ensured that the population received helpful text messages informing them what to do or where to go to stop new outbreaks in their tracks.

But a system that monitors our coughs could also monitor our laughs. It could know how our blood pressure responds to the leader’s speech, to the boss’s pep talk, to the police announcement banning a demonstration. The KGB and Cambridge Analytica suddenly seemed Neolithic.

With state power re-legitimized by the pandemic, cynical agitators took advantage. Instead of strengthening voices calling for international cooperation, China and the United States bolstered nationalism. Elsewhere, too, nationalist leaders stoked xenophobia and offered demoralized citizens a simple trade: personal pride and national greatness in exchange for authoritarian powers to protect them from lethal viruses, cunning foreigners, and scheming dissidents.

Just as cathedrals were the Middle Ages’ architectural legacy, the 2020s left us tall walls, electrified fences, and flocks of surveillance drones. The nation-state’s revival made the world less open, less prosperous, and less free precisely for those who had always found it hard to travel, to make ends meet, and to speak their minds. For the oligarchs and functionaries of Big Tech, Big Pharma, and other megafirms, who got on famously with the strongmen in authority, globalization proceeded apace.

The myth of the global village gave way to an equilibrium between great-power blocs, each sporting burgeoning militaries, separate supply chains, idiosyncratic autocracies, and class divisions reinforced by new forms of nativism. The new socioeconomic cleavages threw the prevailing features of each country’s politics into sharp relief. Like people who become caricatures of themselves in a crisis, whole countries focused on their collective illusions, exaggerating and cementing pre-existing prejudices.

The great strength of the new fascists during the twenties was that, unlike their political forebears, they did not even have to enter government to gain power. Liberal and social-democratic parties began to fall over one another to embrace xenophobia-lite, then authoritarianism-lite, then totalitarianism-lite.

So, here we are, at the end of the decade. Where are we?

via ZeroHedge News https://ift.tt/2Xap8sP Tyler Durden

Bannon And Partners Score Victory In Legal Battle Over Italian Training Academy, So Italy Files Criminal Charges Tyler Durden

Thu, 05/28/2020 – 05:30

Steve Bannon and his associates were handed a win in his ongoing legal battle over the fate of his populist training academy, which had its 19-year lease to a 13th century monastery revoked last year by the Italian Ministry of Culture.

After hearing arguments several weeks ago, three administrative judges ruled that the state has no right to revoke the lease awared to Bannon and his partner Benjamin Harnwell – a British conservative who founded the Dignitatis Humanae Institute (The Institute for Human Dignity, or DHI).

The Abbey of Trisulti, which sits on land owned by the Ministry of of Culture, will house to Bannon and Harnwell’s training academy for European nationalists – if they win the next phase of their legal entanglement with the Ministry, which says it plans to appeal the decision to Italy’s Council of State, according to Reuters.

Harnwell – a former conservative British politician, says he hopes to resume restorations on the property, and that registration for an on-line program taught from the United States would begin shortly.

Bannon and Harnwell’s fight is far from over, however. According to ArtNet, the judges ruled that the Ministry of Culture failed to seek an annulment of the contract within the legally allotted time period – so Bannon and crew won on a technicality.

The judges left the Ministry a loophole, however, pointing out that in order to prevail the Ministry must prove their allegations against DHI in a criminal court. Within 48 hours, Rome’s Attorney General announced that DHI is now facing criminal prosecution over supposed contractual crimes.

“We stood by the monastery, the community and Italy during this pandemic when it would have been easy to walk away,” Bannon said in a statement issued through Harnwell. “We now launch the program of learning and training that will make the world more prosperous, more secure, and more healthy for everyone.”

via ZeroHedge News https://ift.tt/2XA1fde Tyler Durden

The flow of natural gas from Russia to Europe via the Yamal-Europe pipeline crossing Poland completely stopped on Tuesday after a two-and-a-half-decade-old transit deal between Russia and Poland expired and after the COVID-19 pandemic battered gas demand in Europe.

The Russia-Poland transit deal for natural gas from the Yamal peninsula to Germany, via Belarus and Poland, expired on May 17. Poland has aligned its legislation with the energy regulations of the European Union (EU) and Polish operator Gaz-System began offering capacity bookings on the Polish section of the Yamal-Europe pipeline in accordance with EU regulations.

Poland has been trying to wean itself off Russian energy supplies and has become one of the first eastern European countries to have booked U.S. liquefied natural gas (LNG) cargoes.

With the end of the gas transit agreement with Russia, Poland is moving to a more liberalized natural gas market, but it expects that Russia will continue to send similar volumes of gas before the transit deal expired, a Polish official told Reuters last week.

For July 1 through October 1, Poland’s Gaz-System has already sold 80 percent of the capacity on the pipeline made available as a result of termination of the transit contract, the company said on May 15. The remaining available capacity will be auctioned in June, July, and August at monthly auctions for monthly volumes.

But the capacity bookings for the first days following the expiration of the gas transit showed little appetite for gas in Europe, according to analysts.

Gaz-System told Reuters that the capacity booked for Sunday was much lower than for the previous days. So, “there is no need for the pumping stations to work for 24 hours a day at such low orders for the transit service,” the company said.

Commenting on the drastic decline in gas flows from Russia via Poland, VTB Capital said in a note, as carried by Bloomberg:

“Such a significant reduction in gas transit is primarily driven by weak demand in Europe amid warm winter, high levels of gas in underground storage and demand distortion due to Covid-19.”

Can’t The ECB just print up some more demand? or more pipelines?

via ZeroHedge News https://ift.tt/3dc72fl Tyler Durden