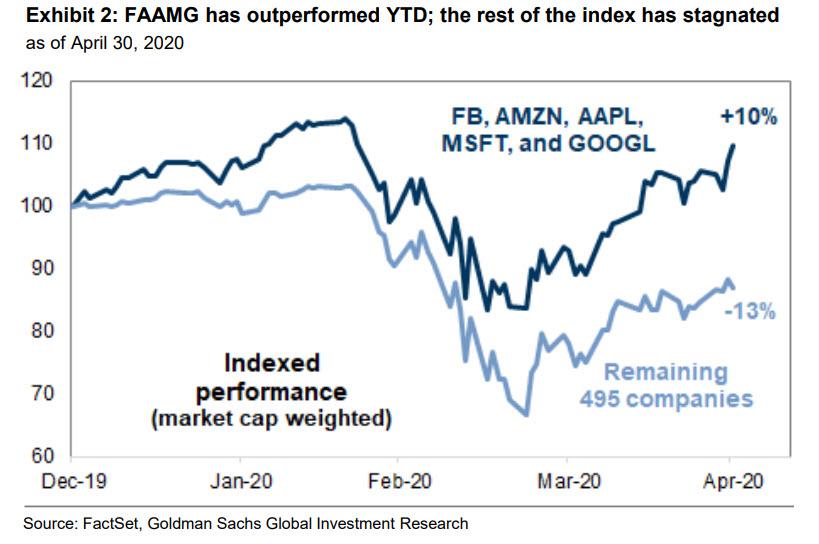

The FAAMGs Are Up 10% In 2020; The Remaining 495 S&P Stocks Are Down 13%

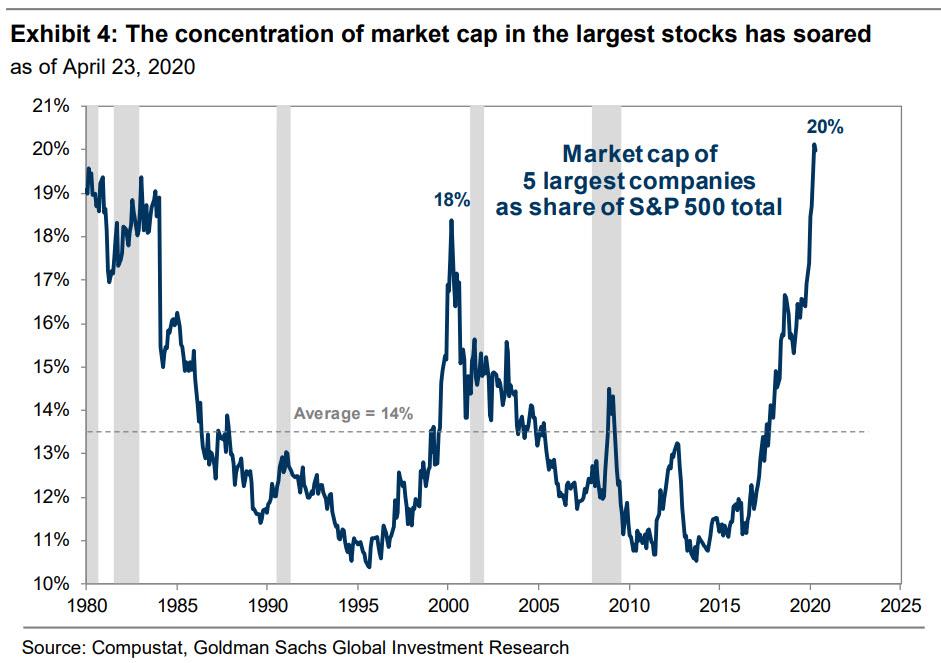

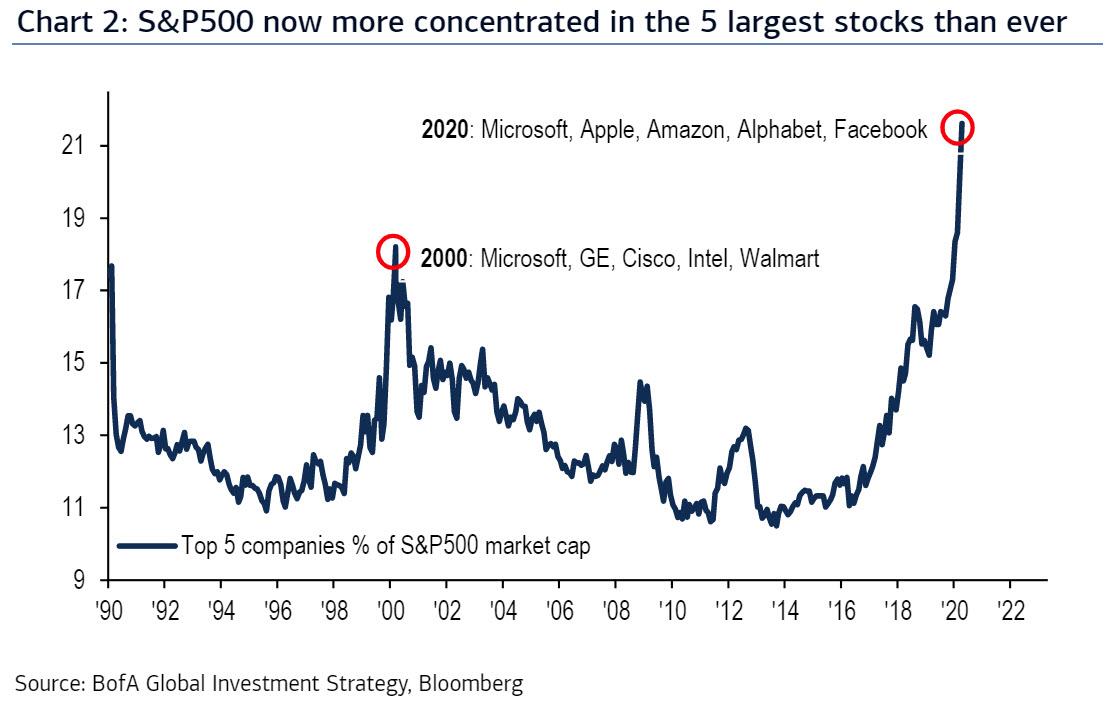

One week ago, Goldman triggered a selloff in growth and momentum stocks, when it pointed out that the five largest S&P 500 stocks, the FAAMGS (or MSFT, AAPL, AMZN, GOOGL, FB) have risen to account for 20% of index market cap, representing the highest concentration on record…

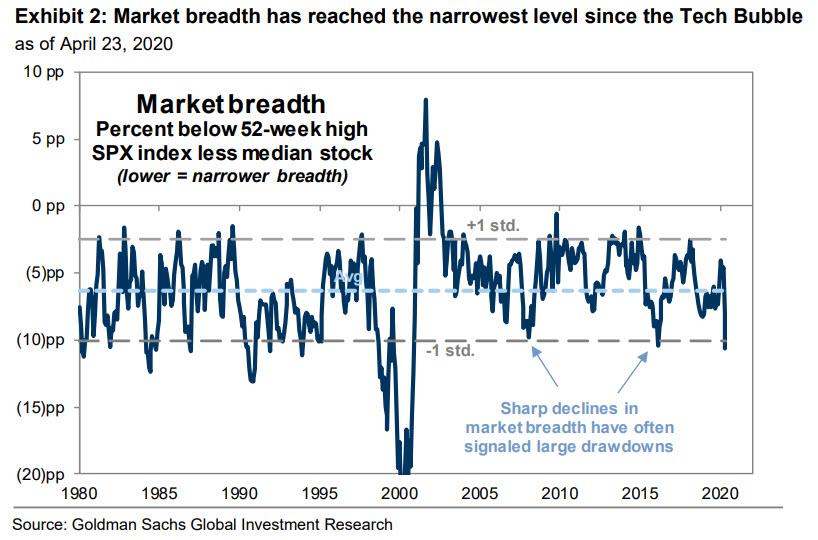

… resulting in the lowest market breadth since the tech bubble…

… and warning that “narrow market breadth is always resolved the same way” as “narrow rallies lead to large drawdowns as the handful of market leaders ultimately fail to generate enough fundamental earnings strength to justify elevated valuations and investor crowding. In these cases, the market leaders “catch down” to weaker peers.”

Fast forward to this weekend when Goldman’s David Kostin has published part two of his curious vendetta against the FAAMGs, although this time easing back somewhat, and while again warning that “the relative outperformance of market leaders eventually gives way to underperformance” he concedes that “timing the reconciliation is difficult” especially since “all five stocks reported earnings this week, and the strong results suggest a catch-down is unlikely to be imminent.”

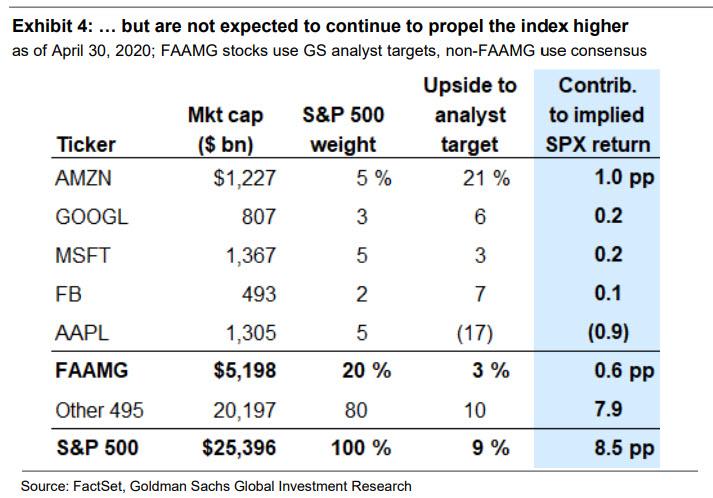

Yet while a momentum crash may not be imminent (even if Nomura’s quant disagrees), Kostin does not let go, and repeats that the “multi-year outperformance of Facebook, Apple, Amazon, Microsoft, and Google has led to record-high equity market concentration and narrow market breadth” with AMZN (+24%) and MSFT (+12%) have even posted positive absolute YTD returns vs. -9% for S&P 500. Furthermore, demonstrating the record low breadth and surge in dispersion, Goldman points out that although the S&P500 trades just 14% below its all-time high, the median S&P 500 constituent still trades 23% below its record high. As a measure of breadth, this 9 percentage point gap ranks in the 15th percentile since 1980.

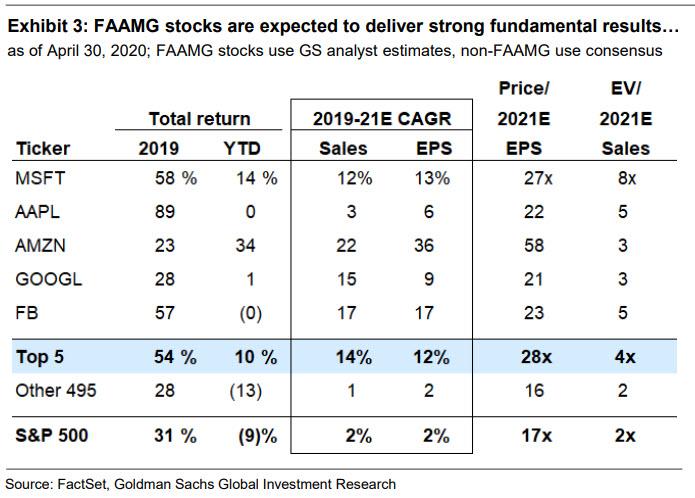

Further demonstrating the unprecedented divergence between the top 5 tech names, many of which are not only still employing buybacks and some, such as Apple, further adding to their buyback authorization, Goldman notes that its equity analysts forecast these 5 stocks alone collectively will post 2019-2021 CAGR sales and EPS growth of 14% and 12% vs. 1% and 2% for the other 495 constituents. But the group of five stocks has upside potential of just 3% to GS analyst price targets vs. 10% for the other 495 firms based on consensus estimates.

In short, as we wrote – jokingly – two weeks ago, that “The Market Is Now Just 5 Stocks”, that’s precisely what has happened, with investors dumping everything but the top 5 names, and creating the biggest “hedge fund/mutual fund/retail/momentum hotel” ever assembled in the FAAMGs. And here another stunning statistic from Goldman: YTD the 5 biggest stocks are up 10% while the remaining 495 S&P500 companies are lower by a collective 13%.

But this is where the good news ends, because in renewing its feud with the “Big 5”, Kostin writes that while Goldman expects the FAAMGs to post CAGR sales and EPS growth of 14% and 12%, respectively, vs just 1% and 2% for the remaining 495 S&P companies, trading at a record 28x expected 2021 EPS, the FAAMGs have very limited upside potential of just 3% to the GS analyst price targets. The other 495 firms trade at 16x 2021 EPS and have 10% upside to targets.

In other words, while the priced to absolute perfection – and growth – FAAMGs are expected to deliver strong fundmanetla results…

… since almost every is long them, they are no longer expected to propel the index higher.

If Goldman is right, and the FAAMG’s loss of market leadership coupled with Buffett’s recent stock sales and warning that markets remain too high (and propped up by the Fed), it is not clear just why anyone would keep buying here, suggesting that the coming week may indeed be painful for the bulls, although they too have a backstop: should stocks suffer another 20% plunge in the next week or so, Powell – whose reputation is now “all in” stocks – will have no choice but to announce that the Fed will start buying equities in his Hail Mary attempt to prevent the final crash.

One final point: this being Goldman, it is virtually guaranteed that the bank is twisting the truth if not outright lying because at the same time as it warns – for the second week in a row – that there is just 3% of upside for the FANGs, the bank recaps its latest analyst actions on the FAAMGs which, it will come as no surprise to anyone, were all raises , to wit:

AMZN PT from $2,900 to $3,000

MSFT PT from $162 to $185

GOOGL PT from $1,250 to $1,425

FB PT from $170 to $220

AAPL PT from $236 to $243

So how does one make any sense of i) Goldman warning that the Big 5 are about to cause a sharp market “drawdown” due to their massive concentration while at the same time ii) Goldman analysts hike all the FAAMG price targets? Simple: it’s Goldman.

Over two thousand years ago, Marcus Tullius Cicero devoted his life to a struggle to preserve the best of the Roman Republic – constitutional checks on power, the rule of law and, to a significant degree for the age, democracy and individual rights.

It’s all there in Cicero’s story – all of today’s battles for the same goals. Some of those battles were small and some large, some fought in court and some on the battlefield, but many were ultimately decided not by law or armies but by the power of public opinion.

And so it has been for the centuries since Cicero. A Star Wars sequel gave us a modern adage for the role of public opinion: Liberty dies with thunderous applause.

For those reasons, it’s particularly alarming to see the public’s opinion about the clear illegality of Governor JB Pritzker’s emergency stay-at-home orders, which is indifference.

That indifference is almost universal in Illinois’ press. Editorial condemnation of the order’s illegality has been almost nonexistent. A particularly sad example was an April 23 Chicago Tribune editorial. Flattening the curve is good, it said, so hurrah for extending the order. No mention of its illegality.

Same with the general public.Polling says 93% of Illinoisans approve Pritzker’s orders, including 75% who said they strongly approved. Illegality apparently is of no consequence.

Maybe the public thinks this is about some petty “technicality.” Maybe they think it doesn’t matter because the order is sensible.

But Pritzker’s orders are illegal, flagrantly so, and it matters. State authorization for the nearly unlimited power asserted under the orders limits them to 30 days. But Pritzker claims he can extend that to eternity simply by issuing successive 30-day orders forever, an arrogant, autocratic and untenable interpretation of the statute.

More importantly, the orders violate a range of of constitutional rights. No effort was made to confine the orders to legitimate public safety goals and tailor them to respect those rights. They reflect no rational basis for the lines between what is permissible and impermissible and, as they apply to many Illinoisans, the orders would not survive the strict scrutiny courts say the constitution demands insofar as they impair certain constitutional rights.

The arguments presented by the Illinois Attorney General in a memorandum defending the orders are cringeworthy:

We’ve broken the 30-day limit before so we can do it again, goes one of those arguments. If the AG were right that past illegalities render laws unenforceable, there would be little left of any law, this being Illinois.

Governors don’t need statutory authorization anyway, goes another argument, because they hold “supreme executive power.” Checks and balances mean nothing to the AG, apparently, nor do individual rights. President Donald Trump and Vice President Michael Pence were roundly ridiculed by the right and the left when they made the same claim regarding the presidency last month.

The General Assembly hasn’t convened to cut off Pritzker’s emergency powers, says the AG, so there’s no issue. Sorry, but inaction by the legislature does not extend time limits written in statutes or suspend basic rights. That’s particularly important when the legislature is controlled by the governor’s allies, as now.

The order will reduce infections and save lives – that basic argument runs throughout the AG’s memorandum. But that justification contradicts the initially stated justification for the order, which was not that it would save lives but merely spread infections out over a longer time frame to ensure hospitals were not overloaded. Illinois surpassed that goal weeks ago. More fundamentally, the AG’s office just doesn’t seem to get that Pritzker’s actions, whether wise or not, must be authorized by the General Assembly and reasonably tailored to fit the need. If the merits of Pritzker’s actions are so clear he could easily have reconvened the legislature to give him extended authority.

Pity us if those arguments are accepted and become precedent.

They were made in the appeal of a temporary restraining order issued on April 27 against extension of the first stay-at-home order. The lawsuit underlying the order is being refiled and probably will be appealed. We can only hope not only that the rule of law prevails but that the general public comes to understand what is at stake.

January will mark the 60th anniversary of John F. Kennedy’s inaugural address.

JFK’s Inaugural Address

The torch had passed, he said, to a new generation of Americans “unwilling to witness or permit the slow undoing of those human rights to which this nation has always been committed.”

The torch passed again since then. Will this generation permit what JFK’s would not?

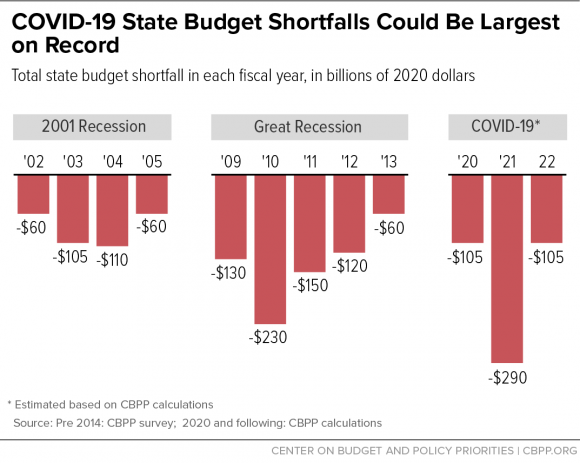

Newsom Says California Went From Surplus To ‘Tens Of Billions In Deficit’ In Weeks, Won’t Get By Without Federal Help

California Governor Gavin Newsom (D) says the nation’s most populous state has flipped from ‘tens of billions in surplus’ to deficits over the course of weeks.

“Last year I did a May revise with a $21.4 billion budget surplus,” Newsom said on Friday during his daily coronavirus briefing, according to Bloomberg. “This year I will be doing a May revise looking at tens of billions of dollars in deficit. We just went tens of billions in surplus in just weeks to deficits.“

Newsom, a first-term Democrat, is scheduled to revise his budget proposal by May 14 with the latest estimates on revenue and spending. In January, he proposed a $153 billion general-fund budget that increased spending by about 2% from the current year that ends June 30 and socked away about $5 billion more into rainy day funds. –Bloomberg

With 30 million unemployment claims filed since the coronavirus pandemic resulted in the shutdown of broad swaths of the economy, states are reporting that they’ll need at least $1 trillion in aid from the federal government – which has already doled out over $2.2 trillion in relief for business loans, stimulus checks, expanded unemployment benefits and small business assistance.

And with a lack of tax revenue, states with bloated budgets and massive entitlement programs are facing significant pain in the months ahead.

“I’m doing everything I can to work with cities and counties, but we are not going to be in a position, even as the nation’s fifth-largest economy, to provide for the needs of all the cities and the counties without federal support,” said Newsom.

Meanwhile, in a Thursday memo, Newsom’s finance director ordered departments to significantly slash spending immediately using strict measures, including bans on new goods and service contracts.

This is part of the ongoing Jackpot Chronicles, looking at four possible Coronavirus scenarios or lenses…

The last instalment was “Force Majeure”, which posited a complete breakdown in seemingly permanent institutions. As it may turn out, these seemingly immovable edifices may not survive this economic collapse and may not be part of “the new normal” that emerges out the other end.

Conspiracy theories make for tricky subject matter for anybody who tries to look deeper than the veneer of conventional narratives. What we are expected to accept unquestioningly out of mainstream circles is sometimes less plausible than what we are expected to dismiss as conspiracy theories.

It gets even more distorted when inversions or backwardations occur between what is fringe and what is, ostensibly, “fact”.

Russiagate was a conspiracy theory, a batshit crazy one that was platformed as common knowledge by multiple mainstream media outlets for over two years. There are still people walking around believing that the current US president was installed as a Manchurian candidate by the Kremlin, and you’re the one in the tin-foil hat for pointing out how disconnected from reality that actually is.

This is typical of the hall of mirrors you enter when trying to understand the dynamics of conspiracy theories. Even the term “Conspiracy Theory” is itself the subject of conspiracy theories. The legend goes that the term was invented by the CIA to marginalize pesky truthers (another loaded word) that were finding all kinds of holes in the official explanation of the JFK assassination.

Whether it’s the implausibility of a “magic bullet” in Dealey Plaza or what many building engineers and pilots have to say about 9/11, the official explanatory cover for such world-changing events are so riddled with inconsistencies and flaws that they can only be believed by those who do not examine them.

The danger in admitting to oneself that at least some aspects of the most pivotal events of our era are not what they seem, is that it can pull you into a downward spiral where everything becomes a conspiracy and nothing is as it seems. We all know somebody who thinks every news story, every event that occurs is a direct outcome of some shadowy cabal that controlled the event, manipulated the circumstances that precipitated it, and selected the outcome to serve their own agenda.

This is not to say that people and groups don’t conspire, that societal elites don’t have a self-serving agenda and that moral hazard and pathological opportunism do not play a significant role in outcomes. In essence, that’s politics. But here’s the crucial duality of conspiracy theory:

To the degree that all major events being manipulated behind the scenes by hidden conspirators is actually impossible, so to is the degree to which the mainstream media explanations of events are mostly inaccurate and at times infantile.

Into this milieu, enter the tin-foil-hats, and things become inordinately more precarious. What we get is a type of three-body-problem writ large where the three independent forces can be described by three age-old adages, ( all of which are possibly apocryphal quotes):

“Never ascribe to conspiracy what can be explained by stupidity” (a.k.a Hanlon’s Razor, often attributed to Napoleon Bonaparte)

“Never let a good crisis go to waste” (Winston Churchill)

“Never believe anything until it is officially denied” (Bismarck)

What we experience as outcomes can be rendered in a Venn diagram between the above drivers: Overall stupidity, self-dealing and duplicity.

As I’ve been exploring a lot lately, we live increasingly in something that resembles a cyberpunk bizarroverse. One where the explanatory powers of mainstream media is in secular decline and our institutions have largely discredited themselves. Two powerful coping mechanisms are

1) to pretend nothing is wrong and that business as usual can continue even thought the underlying scaffolding of the system is imploding (hypernormalisation)

2) subscribe to some non-sanctioned narrative that purports to reconcile the discrepancy between what we believe should be happening with what we are actually experiencing.

For my part, I find the most useful components of both conspiracies and consensus is that they are both known to provide an explanation of events that I can reliably assume as having near zero accuracy. A useful concept for this came out of Douglas Adams’s Hitchhikers Guide to the Galaxy. In it his concept of the recipriversexcluson describes a number whose value can be only be defined as anything but itself. Whatever the expert consensus is saying is happening or will happen, is the one thing you can you dismiss out of hand. Same goes for most conspiracies.

Introducing the Gell Mann Amnesia Effect

The last idea I’ll introduce is that mainstream media has itself, become a type of conspiracy theory. There is less reporting, less actual journalism and mostly punditry and editorializing. Ben Hunt gives us the concept he calls The Gell Mann Amnesia Effect (the phenomenon was originally described by Michael Crichton):

“Briefly stated, the Gell-Mann Amnesia effect is as follows. You open the newspaper to an article on some subject you know well. In Murray’s case, physics. In mine, show business. You read the article and see the journalist has absolutely no understanding of either the facts or the issues. Often, the article is so wrong it actually presents the story backward—reversing cause and effect. I call these the “wet streets cause rain” stories. Paper’s full of them.

In any case, you read with exasperation or amusement the multiple errors in a story, and then turn the page to national or international affairs, and read as if the rest of the newspaper was somehow more accurate about Palestine than the baloney you just read. You turn the page, and forget what you know.”

I noticed this phenomenon years ago, but didn’t have a name for it. In my case, most articles I read in the mainstream press about the domain name system, DNS, and naming in general are so bad as to be cringeworthy. This is one of my faves:

(Answer: No it isn’t. She’s talking about the people who hold pieces of a cryptographic key that signs the internet root zone. Although she doesn’t know that.)

Applying all this to Coronavirus narratives, we can look at what a specific narrative says is or will happen, what it probably preludes from happening.

So when a politician says we may have to be on lockdown for 2 years, I assume we won’t.

When some expert says we may stop shaking hands as a society, I don’t bank on it.

When people on Youtube say 5G causes Coronavirus, I’m pretty sure it doesn’t.

When they say the virus was engineered and released deliberately to bring about a totalitarian police state, I think that gives too much credit to the people who run governments (see Venn diagram).

When people say Bill Gates is the anti-christ, I’m pretty sure he isn’t. And when they say he’s a humanity saving genius who will solve this problem, I’m pretty sure he isn’t that either.

So where does all this get us?

Enter Radical Uncertainty.

This is the title of Mervyn King and John Kay’s latest book. King was the Governor of the Bank of England from 2003 to 2013 and presided over the Global Financial Crisis, writing about his experience in his previous book The End of Alchemy. Kay is an economist who held various positions in academia (former Dean, Oxford Business School, also London School of Economics) and author of Other People’s Money.

Their central theme is that many problems we face are inherently unknowable and that no amount of data or sophisticated modelling is going to get us anywhere near a reliable probability of what any of it means, or what will happen.

Radical uncertainty cannot be described in the probabilistic terms applicable to a game of chance. It is not just that we do not know what will happen. We often do not even know the kinds of things that might happen. When we describe radical uncertainty we are not talking about ‘long tails’ — imaginable and well-defined events whose low probability can be estimated, such as a long losing streak at roulette. And we are not only talking about the ‘black swans’ identified by Nassim Nicholas Taleb — surprising events which no one could have anticipated until they happen, although these ‘black swans’ are examples of radical uncertainty.‘?

We are emphasizing the vast range of possibilities that lie in between the world of unlikely events which can nevertheless be described with the aid of probability distributions, and the world of the unimaginable. This is a world of uncertain futures and unpredictable consequences, about which there is necessary speculation and inevitable disagreement — disagreement which often will never be resolved. And it is that world which we mostly encounter.

So the ramifications of radical uncertainty go well beyond financial markets; they extend to individual and collective decisions, as well as economic and political ones; and from decisions of global significance taken by statesmen to everyday decisions taken by the readers of this book.

Radical Uncertainty means gearing our efforts toward coherently responding to events as opposed to insisting on modelling them with an eye toward achieving optimal outcomes, be that “full employment”, a targeted inflation rate or the elimination of the business cycle.

“Governments choose policies to maximise social welfare. A moment’s introspection is enough to tell us that they don’t. They could not conceivably have the information required to do so. They do not know all the available options, and they are uncertain what the consequences of them will be. They do not even know whether what they wish for today will be what they still want if they achieve it tomorrow….the notion that a government could calculate what maximises social welfare is simply ridiculous. The consequences of policies and actions are far too uncertain….”

It is arguable that many of the problems we experience today, such as debt bubbles and brittle supply-chains are the result of trying to prevent bad outcomes of the past instead of facing them head on and taking the requisite pain when they happened (no bailouts, allowing the over-leveraged to fail). But they didn’t and this is a major reason why the pandemic, when it finally hit, is having such a disastrous effect for something that all else considered, isn’t as deadly as pandemics of the past.

Ironically, Radical Uncertainty was written just before the outbreak, it’s publication date was March 17, just as things were really coming unglued…

“The Black Death will not recur – plague is easily cured by antibiotics (although the effectiveness of antibiotics is under threat) – and a significant outbreak of cholera in a developed country is highly unlikely. But we must expect to be hit by an epidemic of an infectious disease resulting from a virus which does not yet exist. To describe catastrophic pandemics, or environmental disasters, or nuclear annihilation, or our subjection to robots, in terms of probabilities is to mislead ourselves and others. We can talk only in terms of stories. And when our world ends, it will likely be the result not of some ‘long tail’ event arising from a low-probability outcome from a known frequency distribution, nor even of one of the contingencies hypothesised by Martin Rees and colleagues, but as a result of some contingency we have failed even to imagine.”

So as I try to balance out these varying imperfect narratives from mainstream sources, official sources, and the tin foil hats, I try to use them more as filters than as having explanatory power.

I eliminate what the prominent futurists say will happen

I try to eliminate the reason why conspiracists say something is happening

I severely discount what the MSM says is happening.

Then I look at what’s left and try to make sense of it. To that end I think that all most of the hysterical outcomes, in terms of millions of deaths, mandatory implants, FEMA camps, are outside the realm of possibility.

That said, I am bracing for a mother of all economic depressions, rampant inflation, joblessness, war on cash and basically everything described in the second part of Graham Summers’ The Everything Bubble (tl/dr Inflation, NIRP, War on Cash, Bail Ins and wealth taxes).

While I don’t think of these anticipated events in terms of a coordinated global conspiracy to screw all the plebes (again, consult the Venn diagram), I do expect that the rationalizations of these events along with the narratives justifying them will be rife with conspiracy-sounding elements. This brings us back to the hall-of-mirrors aspect of what is conspiracy versus what is propaganda in such times as these.

For the next edition of The Jackpot Chronicles I decided to rename the “Mandatory Pollyanna” scenario. That’s the one where central planners and bureaucrats manage to “save” the economy yet again. However the cost of that would be to undertake an LBO of the entire economy and running it as a centrally planned utility. I’ve decided to rename that one “The Great Bifurcation”, after the the inevitable result of that would be emergence of an even more pronounced and starkly divided Two Tier Society.

* * *

To get alerted when the next edition comes out or to get on the list in general, sign up here, or follow me on Twitter here.

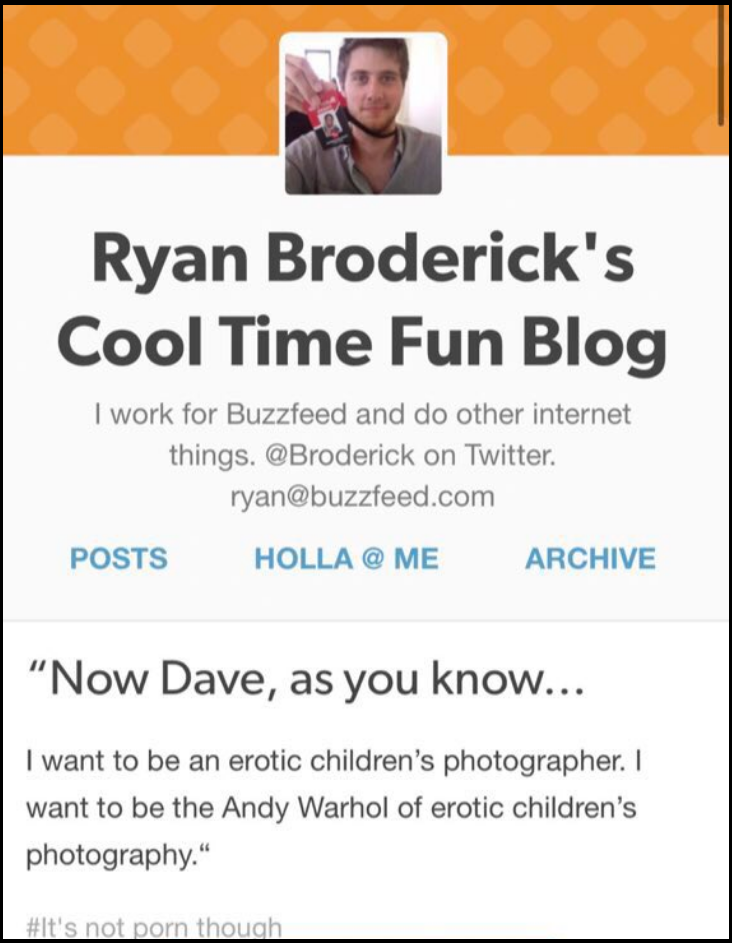

China Using Alleged BuzzFeed Pedo’s Wuhan Lab Article For Propaganda War Against United States

Remember BuzzFeed senior writer and boy band aficionado Ryan Broderick – who wrote in January that we ‘doxed’ a Chinese scientist who we ‘falsely accused of creating the coronavirus as a bioweapon’?

We didn’t – the information was publicly available, the word “bioweapon” wasn’t used in the article, and we suggested the scientist, Peng Zhou, may know “something” about the origins of the coronavirus. Peng, his mentor, and his lab are now the focus of a wide-ranging investigation by the so-called ‘Five Eyes’ western intelligence agencies – much to the chagrin of those who seek to silence us.

This Ryan Broderick:

Indeed, Broderick wrote a BuzzFeed hit piece after we brought international attention to Zhou, head of the Bat Virus Infection and Immunization Group at the Wuhan Institute of Virology.

And while Zhou was researching “the molecular mechanism that allows Ebola and SARS-associated coronaviruses to lie dormant for a long time without causing diseases,” his mentor, Shi Zhengli, co-authored a controversial paper in 2015which described the creation of a new virus by combining a coronavirus found in Chinese horseshoe bats with another that causes human-like severe acute respiratory syndrome (SARS) in mice. This research sparked a huge debate at the time over whether engineering lab variants of viruses with possible pandemic potential is worth the risks.

Now, Zhou and Zhengli’s experimentation with bat coronavirus is under official investigation.

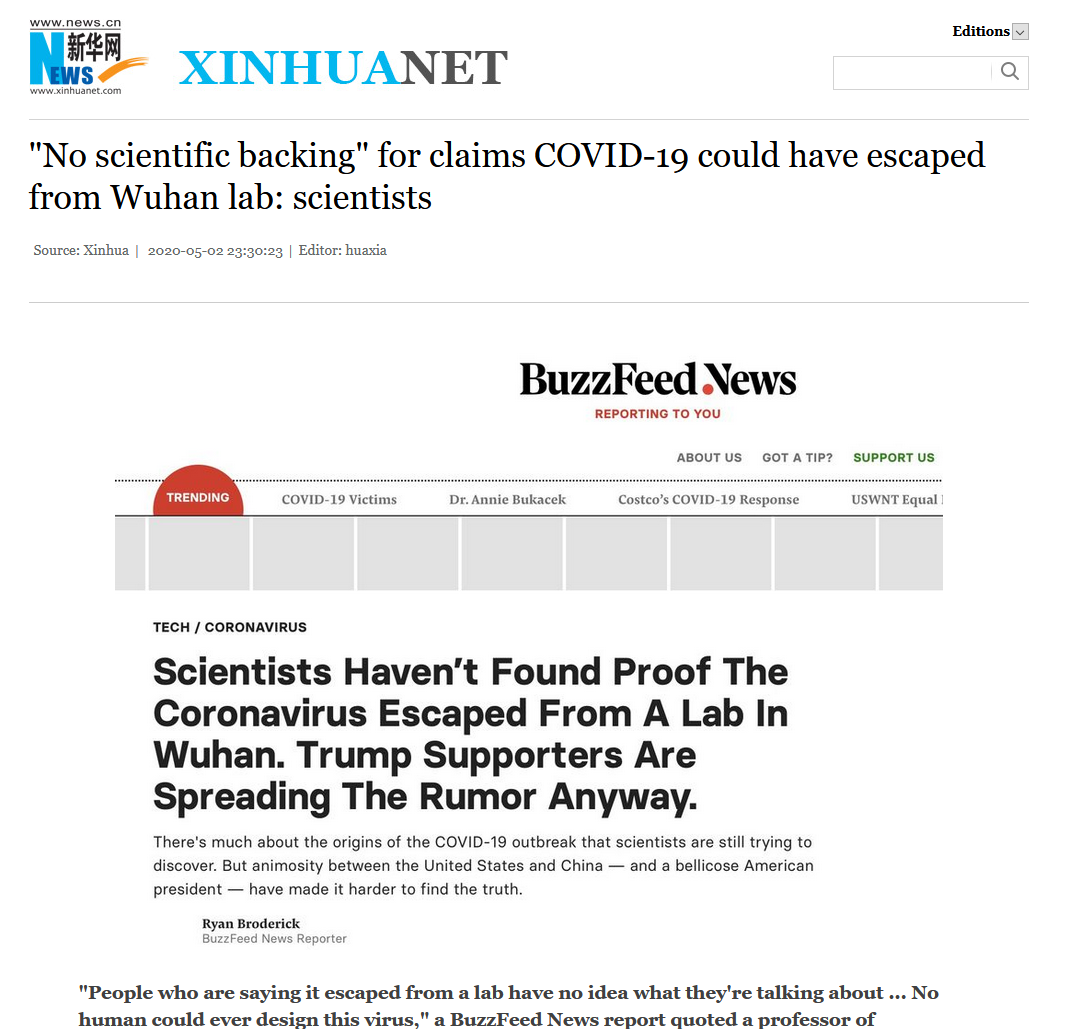

Broderick, meanwhile, is at it again – authoring an April 22 BuzzFeed article titled “Scientists Haven’t Found Proof The Coronavirus Escaped From A Lab In Wuhan. Trump Supporters Are Spreading The Rumor Anyway,” in which Broderick conflates ‘originating in a Wuhan lab’ with ‘it was genetically engineered,’ when the current stance of the Trump administration is that a natural bat coronavirus escaped, or was released, from the Wuhan Institute of Virology.

The comments section of Broderick’s full-throated defense of Beijing caught the eye of China’s state-owned Xinhua News Agency, which used Broderick’s article for CCP propaganda, using the headline “”No scientific backing” for claims COVID-19 could have escaped from Wuhan lab: scientists.”

WASHINGTON, May 2 (Xinhua) — There is “no scientific backing” for the two claims floated recently by some U.S. politicians and media outlets that COVID-19 could be human-made and have escaped from a laboratory, scientists have said.

“The origin of the novel coronavirus is a legitimate area of scientific inquiry, in which there are still open questions,” said an article posted on April 22 on BuzzFeed News.

The piece, written by reporter Ryan Broderick and based on interviews with several scientists, is titled “Scientists Haven’t Found Proof The Coronavirus Escaped From A Lab In Wuhan. Trump Supporters Are Spreading The Rumor Anyway.” –Xinhua News Agency

Let’s review a few comments from Ryan’s original article, however. Seems even BuzzFeed readers aren’t buying his shit:

Not a Trump supporter, and this novel coronavirus could have certainly come from a lab. The Wuhan Virology lab was doing gain-of-function research on the bat coronavirus, and this style of research has been widely critisized by scientists for decades due to how unsafe it is: https://www.the-scientist.com/…/lab-made-coronavirus…. Iterations of SARS have escaped from labs before, so this is not an unprecedented occurance. https://www.the-scientist.com/…/sars-escaped-beijing… US diplomatic cables from 2018 warned of how unsafe this particular lab was: https://www.washingtonpost.com/…/state-department…/ China scrubbed a photo of the Wuhan Virology lab which appeared in a Chinese newspaper last year which showed a broken seal on one of their refridgerators:https://www.mirror.co.uk/…/photos-inside-wuhan-lab-show… the US is not the only country to investiage this claim: the UK, France and Australia have all followed suit. Screw you Buzzfeed for slandering a credible theory as coming from a populist demagogue.

And another:

The evidence strongly points to a Wuhan lab origin. There is no controversy here.

And another:

Broderick continues to conflate two separate issues

1. Natural vs manufactured 2. Transmission from leak in lab vs animal to human in Wuhan wet market

Even a three year old can identify the issues: why does Broderick continue to struggle with this?

Perhaps Ryan should revive his ‘Cool Fun Time Blog’ and try to resist publishing pedophilic material that can be archived for time immemorial. We’re guessing the CCP wouldn’t use it in a propaganda war against the United States, but who knows.

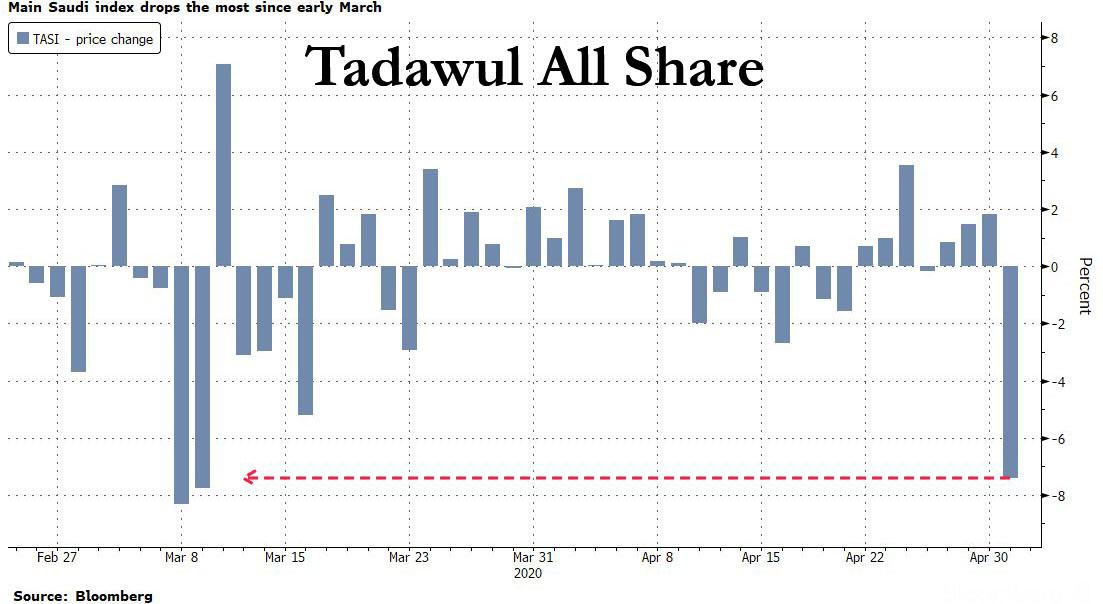

Tadawful: Saudi Stocks Crash After FinMin Warns Of “Biggest Crisis In Decades”

It looks like the dead bat bounce is over.

Yesterday we cautioned that “Selling in May” may be a good risk strategy for 2020, and for traders in Saudi Arabia that warning is already being validated with Saudi stocks crashing the most in almost two months following a Moody’s outlook cut and the kingdom’s finance minister saying that “painful” measures including deep spending cuts, are needed to respond to the coronavirus crisis and crash in oil prices, while Saudi officials said a whopping 70% of Mecca’s population is already likely infected with the coronavirus.

One day after Warren Buffett surprised the videoconferencing Omaha pilgrims when he said that he had dumped all his airlines holdings and was holding out for lower stock prices, the benchmark Saudi stock index, the Tadawul All Shares, closed down 7.4%…

… the biggest one day drop since the whole coronavirus crash started on March 9.

Saudi Aramco dropped by 5.2% to 30 riyals per share, while major lenders including Al Rajhi Bank, National Commercial Bank and Saudi British Bank plunged at least 6.7%.

It wasn’t just Saudi Arabia – where more than 100 Saudi stocks retreated between 9.5% and 10% – saw violent selling. Stocks in Kuwait, the United Arab Emirates, Qatar, Egypt and Israel also declined. In Dubai, 10 stocks including Deyaar Development, Damac Properties and Dubai Investments fell between 4.8% and 5%, the maximum allowed limit.

The Saudi selling was triggered after Finance Minister Mohammed Al-Jadaan, who is seen as “the voice of the Saudi government and leadership”, said in an interview with Saudi television station Al-Arabiya that the world’s biggest oil exporter hasn’t witnessed “a crisis of this severity” in decades, adding that government spending will have to be cut “very deeply”, something we touched on earlier. His comments, according to Bloomberg, were a sharp change in tone from more reassuring remarks he gave about the economy one week before.

Commenting on Al-Jadaan’s ominous warning, Yasin, from Al Dhabi Capital in Abu Dhabi said that Al-Jadaan “was a voice that brought back people to the reality that post-corona and the lower oil prices are here to stay for a while.”

“Investors also read that this is a signal that other Gulf governments will have to take a similar stance and therefore we saw negative reflection spreads to U.A.E. markets…. The question to many is: will the other economic activities recover substantially to help offset some of the drop in oil revenues in 2020, or will it stay muted in H2/2020 and therefore keep the pressure on spending this year and next at least?”

As a result, investors “took it as a warning of much higher spending cuts to come than the original 20%-30% expected earlier in the crisis.”

There were more bad news earlier, when on Friday Moody’s cut the government’s outlook to negative from stable due to ““increased downside risks to Saudi Arabia’s fiscal strength”, even as the rating was kept at A1 for now.

In addition to concerns about the local economy, and Buffett’s tongue-in-cheek warning that a second wave of selling is coming, there is also the specter of a new war of words between the US and China to worry about: “The smokescreen of another bilateral issue ahead between the U.S. and China over the origins of the coronavirus pandemic will pick up steam,” Jameel Ahmad, a markets analyst at FXTM in London, told Bloomberg.

In addition to a fiscal crisis, the Kingdom may soon be dealing with a funding crisis as well: the collapse in crude prices and the government’s drop in foreign reserves, which plunged by a record $27BN in March…

… is putting more pressure on the Saudi riyal. For now, however, prices for 12-month dollar-riyal forward contracts are well short of their all-time high reached in 2016.

Commenting on the drop in reserves, Al Jazeera said that when the kingdom last stared down the crash in crude in 2014, it wielded reserves that peaked at over $735 billion. The stockpile was down by over a third just three years later, channeled almost entirely toward deficit spending.

And now, Saudi Arabia is blowing through its reserves at the fastest pace in at least two decades, even as the government is barely using the holdings to cover fiscal needs. Following its debut in international bond markets in 2016, borrowing covered most of the budget deficit in the first quarter.

With its buffers already fragile and the economy waylaid by the coronavirus, Saudi Arabia is looking to scale back spending and rely more on debt. Straining under lockdown to contain the spread of the pandemic, the kingdom is also bracing for a second impact from the oil rout and unprecedented production cuts negotiated by OPEC and its allies, after a damaging price war between Russia and Saudi Arabia.

Goldman Sachs predicted that the central bank’s reserves, down more than 100 billion riyals ($27 billion) in March alone, will stabilize soon. “Despite a further anticipated decline in oil revenues in the second quarter, we expect the rate of reserve burn to slow,” Farouk Soussa, a Goldman Sachs economist, said in a report.

That said, Goldman thinks that a currency devaluation would be too costly for Saudi Arabia and the better option is to adapt to the oil shock through fiscal changes, although it is very much unclear how much demand there is for Saudi debt which isn’t and probably never will be backstopped by the Fed. Well, remove that “never” – there will come a time when the Fed will own everything.

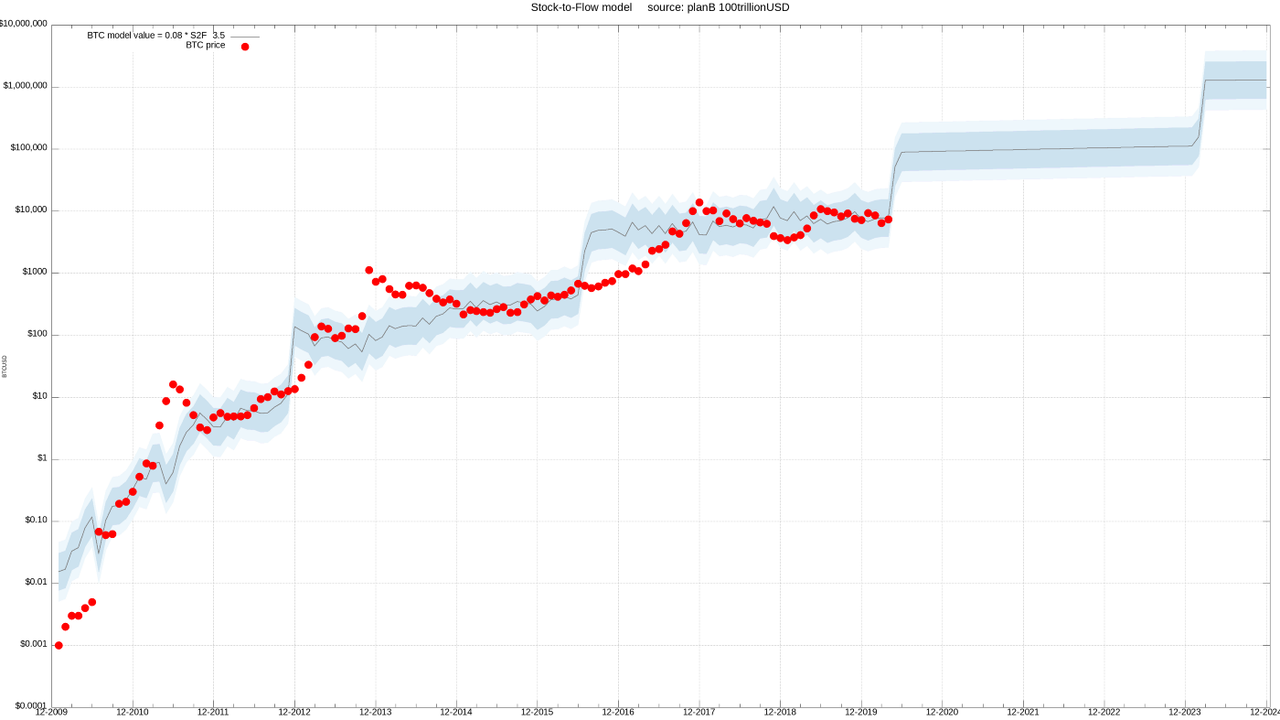

Crypto analyst and Twitter personality, PlanB, recently said Bitcoin is serious business as he recapped the asset’s journey over the last decade.

“This thing is not a toy anymore,” PlanB told Peter McCormack in a May 1 podcast episode.

“It’s maybe not an asset anymore as well,” he said, adding, “It is going to be much bigger than that.”

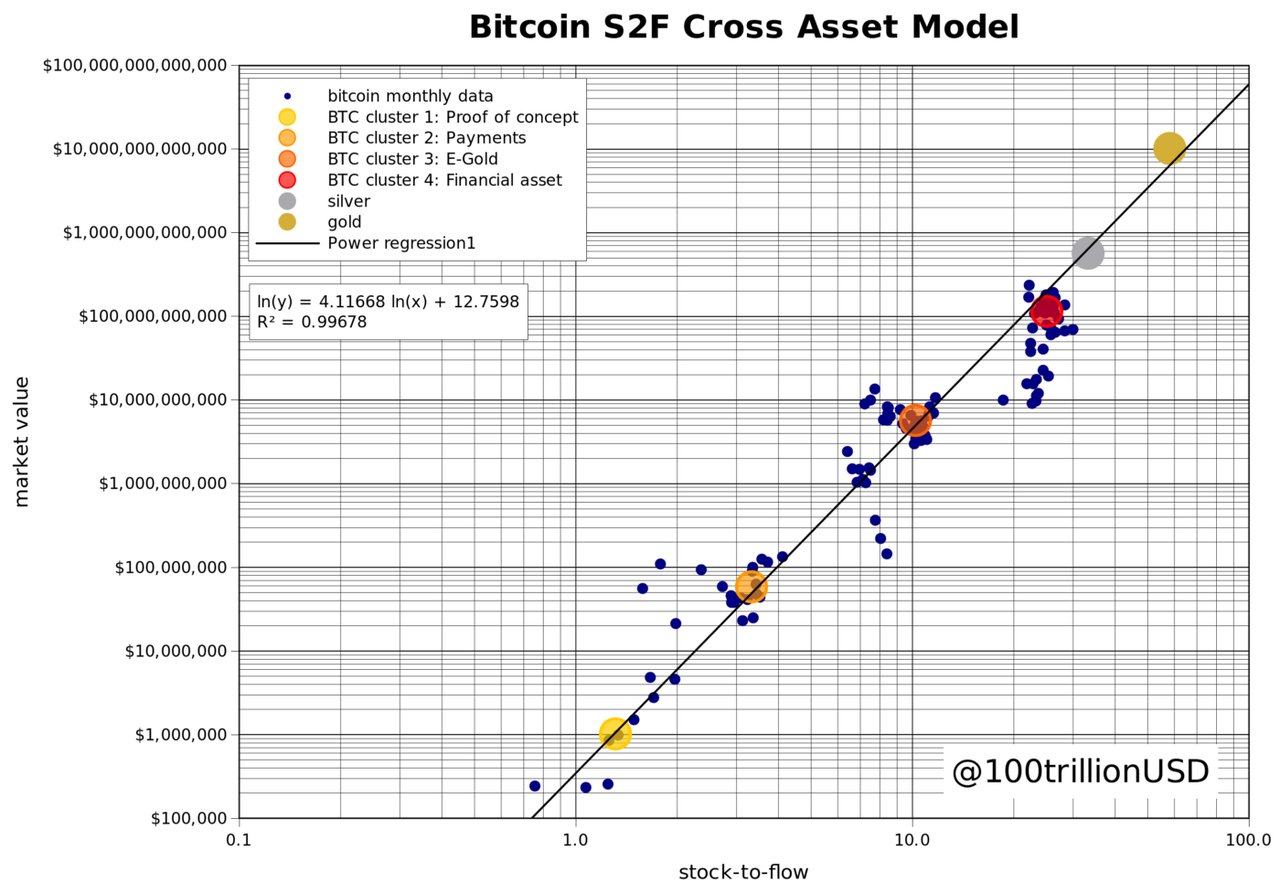

PlanB created a concept for Bitcoin’s growth compared with its supply

PlanB is known around the crypto space for his stock-to-flow model. The model takes into account Bitcoin’s block reward, or current inflation, and halving events, factoring those into the asset’s price.

According to that data, PlanB plotted a few future price targets for Bitcoin, ultimately showing the asset’s potential for a $1 million price tag down the road.

PlanB published an updated version of his model in an April 27 blog post, making gold and silver part of the equation, while taking the time component out.

Bitcoin started out as a toy

Referencing its early beginnings roughly a 11 years ago, PlanB said Bitcoin began its journey as a proof-of-concept, or PoC, for a peer-to-peer digital cash system. “It was kind of a toy,” McCormack said — a description PlanB agreed with.

PlanB noted Bitcoin did not even hold a $1 million dollar market cap in its first two years, although the landscape subsequently changed.

“Then came the transition,” he said. “It went from a toy, magical internet money, to dollar parity,” he said, describing the credibility Bitcoin gained when it hit $1 per coin.

The analyst explained Bitcoin’s price and usage journey over the years, as its identity transitioned from a payment avenue, to a status similar to gold, to its current position as a financial asset.

PlanB did mention the possibility of another transition, although he chose not to provide any speculation on what that might include exactly. The analyst and podcast host also dove into a bevy of other points and concepts in the hour-long podcast episode.

Investing Legend Sees A Second Great Depression For Stocks By 2023

The name of Kiril Sokoloff, author of the weekly WILTW (What I Learned This Week) newsletter through his advisory firm 13D Global Strategy & Research, needs no introduction on this website for the simple reason that over the past few years we have often published his highly insightful excerpts (most recently one month ago with “A Corporate-Debt Reckoning Is Coming“).

Which is why the latest “Lunch with the FT” feature by the FT’s Rana Foroohar may be of interest to readers curious about Sokoloff’s background and how over the past four decades he became one of the most closely sought after independent thinkers and strategists on Wall Street (he works out of St. Thomas in the US Virgin Islands, unaffiliated with any bank), and why his clients – which include Mukesh Ambani, Sam Zell and Raymond Kwok – are quite happy to pay thousands of dollars for a subscription.

We find 13D fascinating, and one of the world’s best newsletters for many reasons by the main one is that Sokoloff’s overarching philosophy – fiscally conservative, rational, measured – is congruent with ours: as the FT notes, Sokoloff “has been trying to make the financial elite see the dangers of seeking to solve the problems of debt with more debt“, something we too have been doing since 2009 but obviously to absolutely no success.

As the FT continues, “the topic is timelier than ever, given that central-bank balance sheets — already huge before Covid-19 — are headed into the stratosphere, as policymakers struggle to cope with the crisis, not to mention the popping of a debt bubble that grew for years before it.”

Sokoloff is, of course, referring to this.

In any event, we’ll let readers catch up on the FT’s profile of the WILTW author at their leisure, but we did want to highlight one particular aspect of his interview: namely what he believes may be in store.

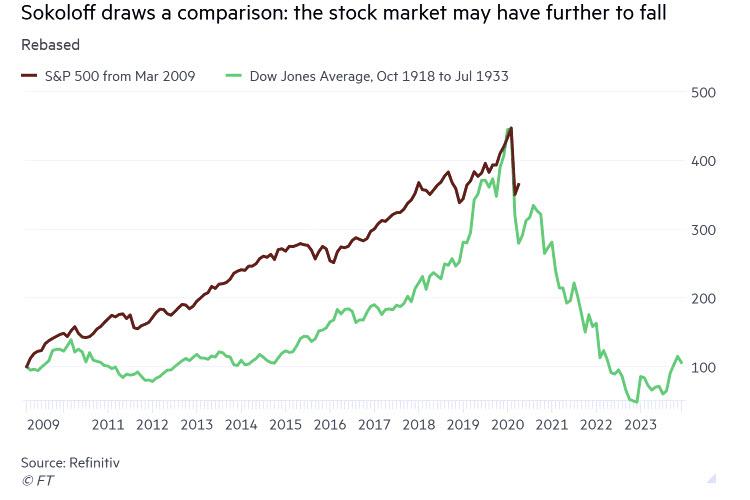

As Foroohar writes, in preparation for her interview “I’ve been… reading Depression-era journalist Garet Garrett’s 1932 book A Bubble That Broke the World, recommended to me by Sokoloff as a primer for our age, since it covers how central-bank actions contributed to the debt-driven run-up to the stock market crash of 1929 and the Great Depression.”

More apropos, Sokoloff also sent the author a chart which compares the Dow Jones between 1918 and 1932 to the current period, a chart which we have also shown repeatedly on this website in recent weeks, months and years. Why that particular chart? Because as the FT explains, it shows that “the rise and the fall are frighteningly similar to the period from 2009 onwards.”

If history is a guide, stocks have further to go before they hit bottom. That’s Sokoloff’s view, anyway. Then as now, he says, “central bankers were pushing on a string”, trying in vain to whip up a real economic recovery with monetary policy.

And here is what Sokoloff believes will what happens when, again, “central banks push on a string”:

How does Sokoloff – who has traditionally been upbeat, optimistic and generally bullish – justify his outlook so apocalyptic it could be taken from a post on that tinfoil conspiracy theory website Zero Hedge? Here’s how:

“The more debt you add [via monetary and even some fiscal policy], the more unproductive the debt becomes,” says Sokoloff, who is now positioned at the dining table in front of his screen. It’s not a popular view these days. Austerity is out, and MMT — the notion that a country that controls its own currency can print it freely to fund deficit spending without worry — is in. (MMT stands for “modern monetary theory” or “magic money tree”, depending on your viewpoint.) But Sokoloff believes the stimulus programmes being launched in the US, Europe and many other parts of the world will very likely end in tears.

“I think we’re at the beginning of a long-term period of deflation, falling prices and the loss of pricing power. The only way out of it will be to have a long period of austerity, and to get the US savings rate up dramatically.” He points as an example to the US in the period during the second world war, when federal budget deficits were high, well over 20 per cent of GDP in some years (compared to what may be some 20 per cent-plus by the end of this year) but the personal savings rates of Americans were positively Chinese — as high as 25 per cent including income gains from the war and net exports, as opposed to 8 per cent or so before the Covid-19 crisis — boosted by wartime rationing.

One-upping Sokoloff, we have created a better chart that more clearly lays out what happens if one tacks on the Great Depression outcome to the current Dow Jones. In short, we should see the Dow dropping to the Great Depression-equivalent low of roughly 10,000.

There is good news: after its plunged to all time lows, the Dow traded in a tight range for several years before eventually blasting off to unprecedented highs. What triggered it? Why World War II of course.

Which is why any true comparisons to the Great Depression era should also consider the cataclysmic event that ended it, and look forward to a similar outcome over the next few years.

The pace at which emerging market economies are losing FX reserves is staggering. In March, emerging economies lost around $1.5 billion in foreign exchange reserves per day, according to Bloomberg.

Saudi Arabia alone lost $27 billion in reserves in March, according to Goldman Sachs, and it is one of the countries with the best capacity to endure the current crisis.

China, that still hods $3 trillion in FX reserves despite the crisis, is also among the strongest countries in FX reserves, but the apparently large level is offset by a large US-dollar denominated debt liability. As such, China’s 60% of China’s reserves are there to cover existing liabilities.

India is also one of the strong countries. As a large importer of commodities, the current slump in activity and lower commodity prices has allowed India to maintain a very healthy level of reserves.

Which countries are suffering the most? Argentina, Brazil, Mexico, South Africa, Turkey rank among the most impacted.

What is causing this collapse in reserves and rising dollar shortage?

The decline in global trade and economic activity due to the forced lockdown weakens export revenues. The outlook for 2020 is bleak with trade possibly declining by between 13% and 32%., according to the World Trade Organization. Some recovery is expected in 2021, but the likelihood of recovering 2019 global trade activity before 2023 is small.

The collapse in commodity prices destroys the trade balance of producer nations. Not only demand is falling to unprecedented levels, but storage is also filling up rapidly and overcapacity at producer nations is building to decade-highs. This problem is not happening just in oil and natural gas, but also in coal, aluminum, soja and, to a lesser extent, in copper.

Local currency collapse leads to central bank intervention. Central banks in emerging economies were smart in 2008-2011 and kept their reserves at very good levels, significantly above foreign currency liabilities. However, the recent slump in many currencies relative to the dollar has caught many emerging market central banks unprepared. Despite the massive increase in the balance sheet of the Federal Reserve and almost unlimited quantitative easing, many emerging currencies have collapsed and led to their central banks to sell dollars to defend the currency, a big mistake. reserves fall, and the currency remains weak.

Since 2009, many emerging markets have ignored the risk of building imbalances and have entered into large twin deficits (fiscal and trade), as well as issued record-level of US-dollar denominated debt because domestic and international investors did not want local currency risk. This means that emerging markets face a massive wall of US-dollar denominated maturities of more than $2 trillion in the next two years while refinancing and new debt requirements soar.

The Federal Reserve will continue to increase money supply… But investors have abandoned the risky “carry-trade” of suing cheap dollars to buy high risk emerging market exposure. Understandably, investors have pulled more than $120 billion in emerging market financial assets in March.

The “Sudden Stop” in emerging economies that I warned of in my book Escape from the Central Bank Trap (BEP 2017) is happening in front of us. It means that even with massive easing from the Fed, many economies will not see a large flow of funds into local investments, and the countries with the largest fiscal and monetary imbalances simply stop receiving foreign funding.

Some readers may see this as a great opportunity for China to extend massive loans in Yuan to address the rising shortage of dollars. There is only one problem. The economies that face the sudden stop will sell those Yuan to buy US dollars and repay loan commitments which could create a risk of capital flights in China that the country cannot afford, especially when it is managing its reserve base as well as it can.

The only thing that can reverse the sudden stop or mitigate it is a return to normal economic activity. Even so, the likelihood of investors jumping on the “negative dollar carry trade” of the past is very low.

Did FBI Operative’s Lie Launch Flynn Investigation, And Did IG Horowitz Run Cover?

For those who haven’t been paying attention, recently unsealed materials in the case against former Trump National Security Advisor Mike Flynn all but prove that the FBI set him up with a perjury trap (a ‘squeeze’ which even Bloomberg‘s Eli Lake says ‘undermines the rule of law’).

And as the case against Flynn continues to unravel, perhaps the most important dots have been connected by investigative researcher @JohnWHuber, better known as “Undercover Huber” on Twitter, who makes a cogent argument that Stefan Halper – the portly spy who the FBI used to conduct espionage on the Trump campaign during the 2016 US election – may have sparked the Flynn investigation after lying to the FBI.

What’s more, IG Michael Horowitz’s report makes no mention of the lie, or the recently-learned fact that the FBI tried to close the Flynn case, dubbed ‘Crossfire Razor’, in Jan. 2017, only for agent Peter Strzok to go ‘off the rails‘ and demand it not be closed.

Why did the IG Report completely ignore Stefan Halper’s lies to the FBI about @GenFlynn, and leave open the possibility that Halper may even have triggered the opening of the CI case against him?

According to the IG, Stefan Halper (referred to as “Source 2”) met with the Crossfire Hurricane team twice (in Aug 11 and 12, 2016) and told them “he had been previously acquainted with @GenFlynn”. *This was immediately before the FBI opened a case on Flynn on Aug 15, 2016*

The IG report is silent on anything Source 2 might have said specifically about Flynn. It’s also silent on the fact the Washington Field Office of the FBI tried to close the Flynn case on 01/04/2017. Both are going to be important in a second.

We now know from the FBI’s draft “Electronic Communication” dated 01/04/2017 (trying to close the Flynn CI case, stopped by Strzok at the direction of Comey, McCabe or both) confirms the “CH” team “contacted an established FBI CHS to query about” Gen Flynn & held a “debriefing”

This “event” very likely refers to when Flynn spoke at the Cambridge Intelligence Seminar in Feb 2014, and the suspicious Russian-linked person supposedly in the cab was @RealSLokhova (who also attended, and briefly spoke to Flynn)

Except that story is a *lie*. Halper wasn’t at that event.He witnessed nothing, because he wasn’t there. And the cab ride almost certainly didn’t happen either, because @RealSLokhova says she was picked up from the event by her Husband. And she’s willing to say that under oath.

There are multiple pictures of that Cambridge Seminar event (attended by about 20 people). Flynn was there, as was Richard Dearlove (former head of MI6), and Christopher Andrew (then mentor of @RealSLokhova and “unofficial” historian of MI5). But Halper wasn’t. Not in any photos.

“No one remembers Halper attending the event because, in truth, Halper was not there”

Halper’s lawyers never challenged that statement. Even when the federal Judge dismissed @RealSLokhova’s case (for other reasons), he did not challenge that claim, only saying that “even assuming it was false” that Halper “attended” the dinner, it wasn’t defamatory to claim he did

Halper’s lawyers even noted @RealSLokhova’s claim it was a “falsehood” to say Halper attended the Feb, 2014 Cambridge event, and then NEVER defended it as *true*, just that it wasn’t *defamatory*, and non-actionable.

And the FBI trying to close the case on Flynn is great evidence Halper’s “attendance” at this event so he could see this suspicious cab ride is false. The FBI never tried to interview @RealSLokhova, or anyone at the dinner. Why? Because it would have proven their own source lied.

FYI, WaPo, WSJ and NYT have all published stories claiming that Halper attended that Feb 2014 event. None have any evidence that’s true. All the stories are anonymously sourced to Halper or Halper’s buddies. There never will be any evidence Halper was there, because he wasn’t.

So when Halper told the FBI that he was “previously acquainted” with Flynn, and “witnessed” this suspicious cab ride, HE WAS LYING TO THE FBI. And at the time, he was a paid Confidential Human Source – the only one cited in the @carterwpage

FISA, other than Steele.

That’s big.

But what’s arguably bigger is WHEN Halper told this lie about Flynn. When else could Halper claimed to have been “acquainted” with Flynn if not this Feb 2014 dinner (the only time Flynn attended the Cambridge seminar Halper helped organize)?

Now, maybe Halper told the FBI about the dinner after the CI case was opened. But that’s NOT in the IG report, despite Halper’s other meetings with the FBI being in there. In fact the IG report says nothing about Halper and Flynn, other than what I quoted

In addition, FBI’s Jan 4, 2017 draft Closing EC doesn’t say when this “debriefing” with Halper happened either. The wording sort of implies it was after the case was opened, but never says it

So it is possible that a lie from Halper actually triggered opening the case on Flynn?

What else did the FBI have? Their own laughable “predicate” appears to be that Flynn worked for Trump, attended an RT dinner (at the time, @RepAdamSchiff

had previously appeared on RT!), and was “linked” to Russians (Er, he was the former head of DIA under “Russian reset” Obama)

Ah, but all of those things were already true between Aug 1 and Aug 10, 2016, which is when the FBI opened cases on Page, Papadopoulos and Manafort – BUT NOT FLYNN. That didn’t happen until Aug 15. He’s the odd one out.

Flynn obviously already worked for Trump. He already had these “links”, and he’d already attended the RT dinner long ago. The thin gruel of Russian “links” and working for Trump was enough to open cases on all the others, but NOT Flynn.

But what did the FBI have extra before they opened the case? Stefan Halper telling them about being “previously acquainted” with Flynn – which almost certainly refers to that Feb 2014 Cambridge dinner, where he was never “acquainted” with Flynn at all.

Oh, & even if Halper told this lie *after* the case was opened on Flynn, the FBI mustn’t have found it credible because they never tried to properly investigate it, and then even tried to close the case anyway. So that means at best the lie came between Aug 15, 2016 & Jan 4, 2017

What else was happening between Aug 16 & Jan 17? Oh yeah, the FBI was using a person they should have suspected of lying to dirty people up – Halper – as a CHS wearing a wire on @carterwpage, @GeorgePapa19 and others, AND relying on Halper as “Source #2” in the FISA warrant apps

Then, incredibly after their own source lies to them about Flynn to dirty him up, the FBI have the audacity to charge Flynn with lying to them! Corrupt dirty cops isn’t an adequate description. And for all we know, Halper is STILL on Wray’s FBI books as a paid confidential source

Finally, IG Horowitz blew this line of inquiry, and didn’t mention anything about the FBI trying to close the case on Flynn in Jan 2017. Horowitz also admitted hasn’t seen any evidence that any of Halper’s information was ever corroborated during his entire time as an FBI source

Durham can do what the IG didn’t, and solve this mystery quite easily with a few interviews and record checks.

Or, the DOJ/USG can keep Halper on his retainer and ignore this. Either way, we’ll know what’s up

/ENDS

UPDATE: It gets worse@SidneyPowell1 says that “SSA 1” (Joe Pientka) wrote that Jan 4, 2017 EC closing the Flynn case

AND according to the IG report, Pientka personally approved those Aug 2016 meetings with Halper & his handler & was briefed on both meetings

{kind=link}