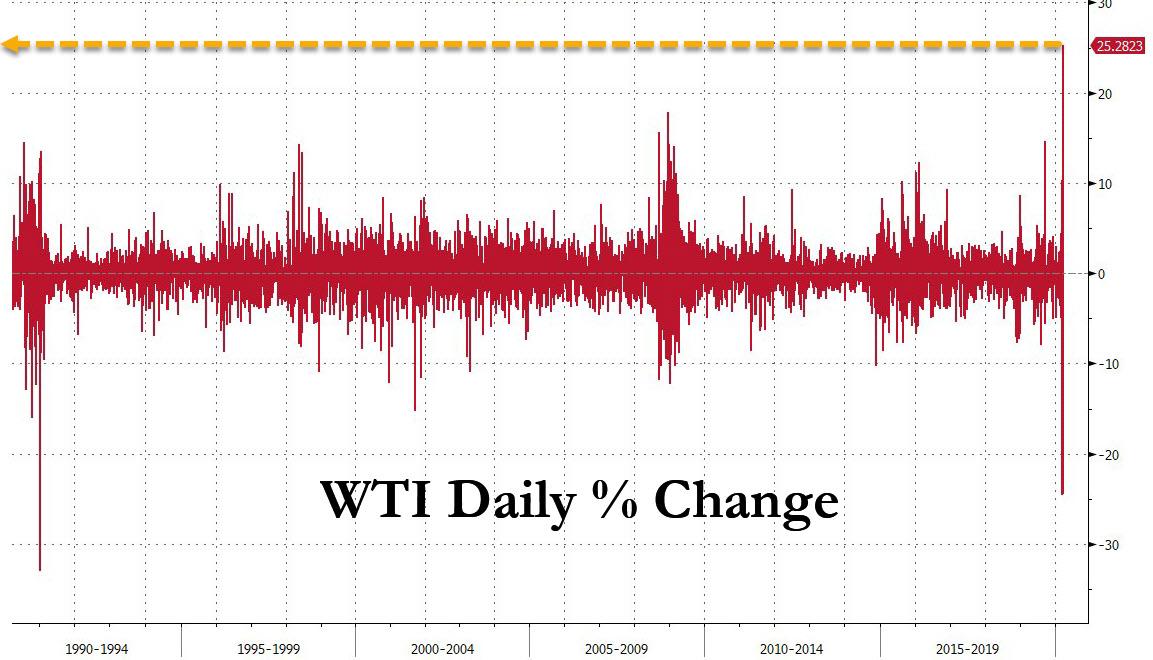

One day after oil crashed by a near record 25%, a move which made some sense in light of the historic dollar short squeeze and surge to all time highs in the Bloomberg dollar index, today oil has rebounded violently, and after rising as much as 26%, WTI settled up $4.85 at $25.22, or 23.81% higher…

… its biggest one day move on record!

There was no actual catalyst, although some oil traders cited a rogue rumor that emerged just before the big spike according to which “Putin has instructed Novak to engage the #Saudis 🇸🇦 to resume #OPEC+ supply cuts.”

Remarkably, today’s record surge took place even as the dollar index continued to soar, suggesting the move was most likely a counter-trend short squeeze.

That said, putting the move in context, despite today’s record surge, oil is still down 17% for the week.

Netflix To Cut Traffic Stream To European Networks By 25% For 30 Days

Netflix announced on Thursday afternoon that it will cut traffic to its European networks by 25% for 30 days to preserve internet functionality amid the coronavirus crisis, following discussions with European Commissioner Thierry Breton.

The issue of Netflix’s internet hogging – as a reminder video streaming is the single largest user of internet bandwidth – emerged as more people have been staying and working at home in an attempt to slow the virus’ spread, resulting in growing concern about whether the net has the bandwidth to withstand increased usage.

European Union commissioner Thierry Breton had raised the issue with Netflix CEO Reed Hastings and suggested via Twitter that people at home not stream video in high definition if they can and instead watch in standard definition.

“Teleworking & streaming help a lot but infrastructures might be in strain,” Breton tweeted Wednesday. “To secure Internet access for all, let’s #SwitchToStandard definition when HD is not necessary.”

After additional discussion between Hastings and Commissioner Breton, Netflix said in a statement sent to USA TODAY, “given the extraordinary challenges raised by the coronavirus – Netflix has decided to begin reducing bit rates across all our streams in Europe for 30 days. We estimate that this will reduce Netflix traffic on European networks by around 25% while also ensuring a good quality service for our members.”

Following the report, Breton said “I welcome the very prompt action that Netflix has taken to preserve the smooth functioning of the Internet during the COVID19 crisis while maintaining a good experience for users.”

Netflix did not say how much of a reduction its various streams would get. Streaming standard-def movies or TV shows require about one-third the bandwidth of HD video, about one gigabyte for SD video in an hour, compared to 3GB for HD, according to Netflix.

Initially, Netflix simply said Breton, a France-hailing commissioner in charge of the EU’s single market, had risen an important issue, a spokesperson for the streaming provider told CNN, which first reported the exchange. “Commissioner Breton is right to highlight the importance of ensuring that the Internet continues to run smoothly during this critical time,” Netflix said in a statement to USA TODAY. “We’ve been focused on network efficiency for many years, including providing our open connect service for free to telecommunications companies.”

The provider’s open connect program gives companies such as Comcast and Verizon a more direct connection between its network and Netflix’s servers for improved delivery of content.

Internet traffic “is up no doubt,” said Sajid Malhotra, chief financial officer of online video delivery company Limelight Networks.

But internet congestion “happens by region and then within a region by carrier,” he said. “I don’t know what exactly drove the EU to issue the statement that they did. Maybe they were just seeing the trends and extrapolating if those trends continue out further and further then they could have problems.” He also said that congestion is “a manageable issue and it is not universal.”

asking viewers to opt for lower-resolution video is not out of line, says Cam Cullen, vice president of marketing for networking company Sandvine. His research has found YouTube, which always generates the most mobile traffic, has surpassed Netflix as the top traffic generator overall during the recent global health crisis.

“We are definitely seeing big jumps in usage around the world as people are staying in their homes,” Cullen told USA TODAY. “This is not only streaming, but other traffic types that cause streaming issues – gaming, file sharing, software updates, telework, and VPNs.”

Verizon on Tuesday said it saw an increase of 75% over its networks in the past week due to online gaming, with video streaming up more than 12% and overall web traffic up by about 20%. Last week, several major broadband providers loosened restrictions and boosted internet speeds for customers.

Few people watch their investments daily but rather chose to peek at them every now and then. This is the main reason a lot more Americans are not waking up today sick to their stomach and in near panic from the devastation markets have wreaked upon their savings as trillions of dollars have vanished into a big black hole. After the carnage in the market today a young gal told me the market would jump right back, she knew this because her boyfriend, also rather young, worked for an accountant and knew about these things. Most likely they think this because in their short lives they have never witnessed anything but a market that always rapidly recovered and moved ever higher. This is the basis of, “buy the dip” which has been a market trading mantra for years and years.

The sad reality is when markets fall they sometimes do not come back. The article below looks at the damage and pain being foisted upon some average Americans nearing retirement. Back in early 2017, I penned an article that delved into the subject of high-earning Americans, where their wealth came from, and just as importantly where it was stored. This got me thinking about the so-called wealth effect as well as how all that wealth was held. Many of the really big earners in recent years have benefited greatly from the surging stock prices as much of their income has come from financial markets and gains in equities. This also is true for the many working Americans that have invested in a 401K and other savings instruments.

[ZH: Global aggregate bond and stock paper wealth has crashed $25 trillion since Feb 21st and all global gains from stocks and bonds since the Dec 2018 lows have now been erased…note that bonds are still up just over $5 trillion, hedging against the just over $5 trillion losses from stocks]

Wealth Can Rapidly Vanish

Imagine the shock this morning of a fictitious couple named Joe and Jill Average that are nearing retirement with a net worth last month of around 250 thousand dollars when they check to see how they are doing after hearing “murmurs” the market has slipped. If three-quarters of their nest-egg was in the market, they will be horrified to find that the mere pullback of stocks in recent weeks has ripped away over 60 thousand dollars or around 25% of their wealth.

Rising markets have become the pathway to a better future for many people. After more than a decade of rising stock prices, many people have come to assume this is normal and the trend would continue. When people have more than they need or want to put money away for a rainy day where do most store it? For many people, the answer is into some form of intangible investment that promises good returns. When rating people on a “wealth chart” by how many tangible assets they own you might be shocked to find much of the wealth people own is in the form of intangible assets that can be full of risk.

Safely Storing Away Wealth Not Always Easy

In our modern world, the possibility of cyber-crime or cyber-theft raises the risk to even a higher level but an even greater example of how wealth can rapidly vanish into a big black hole is evident in the recent stock market action where trillions of dollars are now simply gone. Paper wealth can be viewed as a promise of future value. Unfortunately, this leaves much of society and many rich individuals vulnerable to rapid financial loss if the tides of fortune shift or if values rapidly change.

Currently not only are we faced with banks paying little in the way of interest but we must also fear they or the government might reach in and seize part of our money. By adopting policies that spurred people to pull their money out of banks and other safe investments in search of higher yields we have driven up stock prices. Some of these stocks have reached unbelievable multiples.

People often do not understand money and wealth. Myths about both run rampant and become intertwined with deeply rooted personal feelings acquired or passed down from parents. These feelings often muddy and skew how people deal with wealth. An example would be anyone who felt deep down that money was the root of all evil would react to winning the lottery far differently than someone with the belief that you can buy happiness. I have even heard poor people say they didn’t see much point in buying a ticket for a lottery of several hundred thousand dollars because “that’s not much money” Today the use of the B-word “billions” is so prevalent in society it is understandable many people live with distorted values.

Annuities, pensions, stocks and such promises of future payment tend to dominate the list of favorite vessels in which to store wealth and many of these are leveraged to maximize returns and garner higher yields on our investment. Cash is another option but holding it in your possession leaves one open to theft and means the money will earn no interest. What is often missing or overlooked is tangible fully paid for items and things that are likely to hold their value and in the direct possession of the owner. People tend to avoid tangible assets in their control because they are often inconvenient. Valuables can be a pain to have about and they often need to be insured which also calls attention to their existence.

Truth be told most people are not overly endowed with discipline this includes many people that amass a fortune. This often means that many wealthy people tend to “misplace” or lose track of where they have placed their wealth. Sometimes it is simply put into a system that is on autopilot. Years ago I purchased a property from a doctor on contract. The doctor having also bought the property on contract had me send the payments to the man he purchased it from so he would not be bothered. After many years I contacted the doctor to discuss a discount for a cash payoff and his accountant discovered the first seller had been paid off years before but continued taking the money. Needless to say, the doctor was shocked and getting his money back proved difficult.

When you subcontract out control of your wealth or turn it over to a money manager you often get promises but no ironclad guarantee. Confidence in a money manager can quickly be dashed, all the people invested with Bernie Madoffdiscovered just how suddenly things can go south and promises turn hollow. While it has become both fashionable and common in recent years to let someone who knows and specializes in financial planning and markets to control this segment of our lives I feel it is a big mistake and a derelictionof duty. If wealth came with a warning notice it would say, “Holder Beware, This Commodity May Vanish, Spoil, Or Grow Obsolete At Any Time!”

Trump To Intervene In Russia-Saudi Price War At “Appropriate Time” After Crude Hit $20

As Congressional voices and US oil companies have grown louder in urging President Trump to mount a muscular pushback against the Russians and Saudis flooding the market following their spat early this month that triggered an ongoing oil-price war — which lately witness crude falling to $20 yesterday— the administration has said it plans to get involved at “the appropriate time” and hopes to find a “middle ground”. Trump said Thursday at a White House briefing: “They are in a fight on price, on output,” and indicated that “At the appropriate time I will get involved.”

Early this month the Saudis were caught completely off-guard when Putin said Russia would ignore Riyadh and OPEC+ plans to significantly cut production, effectively and dramatically overturning the balance of power in the oil world while declaring war on US shale, sending crude prices crashing and leaving dozens of American producers teetering on bankruptcy.

The WSJ reports Thursday that the White House could be ready to jump into the fray: “The administration is considering intervening in the Saudi-Russian oil-price war with a diplomatic push to get the Saudis to cut oil production and threats of sanctions on Russia aimed at stabilizing markets, according to people familiar with the matter.”

Image source: AFP

But it appears sanctions are what backed the Russians into a corner in the first place — enough to riska price war which the Kremlin claims it can weather for years to come.

On Wednesday North Dakota Republican Senator Kevin Cramer wrote a letter to Trump declaring “We will not be bullied,” and urging a position of strength against“Foreign nations… now using the environment of the worldwide spread of COVID-19 to flood the market and cripple our domestic energy producers.”

Sen. Cramer further condemned Russia’s “bullying tactics” which have “become the norm” — but in a rare lashing out at our ‘partner’ also took Saudi Arabia’s “concerning” actions to task.

Trump seemed to respond to these concerns, saying a day later: “It’s very devastating to Russia, because their whole economy is based on that and we have the lowest oilprices in decades. I would say it’s very bad for Saudi Arabia.”

“I spoke with numerous people… and we have a lot of power over the situation. We are trying to find some kind of a medium ground,” Trump said.

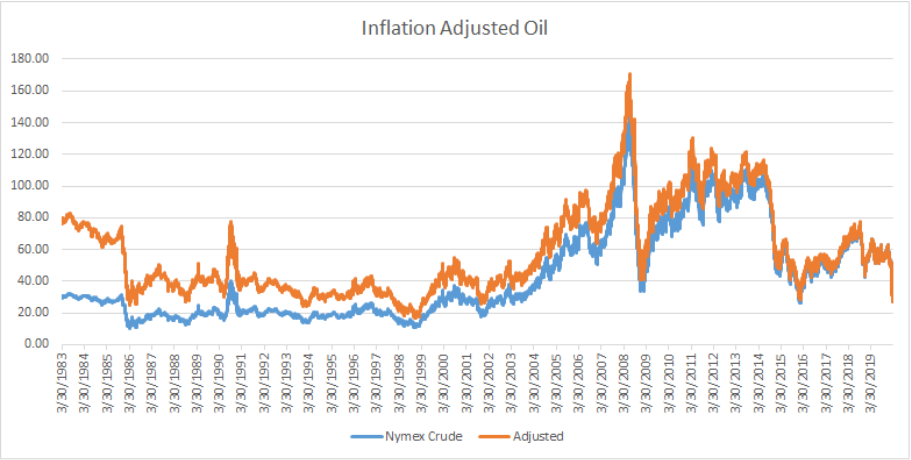

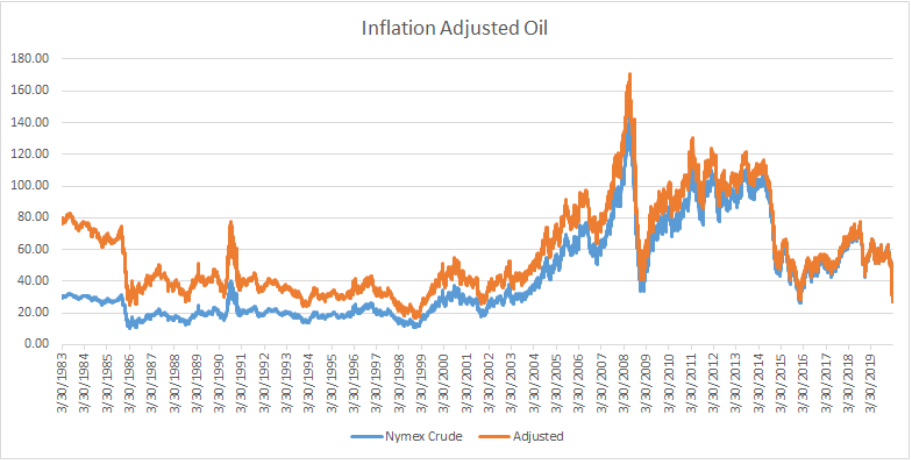

Long-term chart of inflation-adjusted front-month Nymex WTI oil futures, via Dow Jones Market Data.

The WSJ describes further that the potential new strategy would aim to resolve the Russia-Saudi price war which could involve State Dept. level engagement with the Saudis and more critically direct dialogue through the National Security Council, also with threats of yet more sanctions on Russia.

However, the Russians appear ready and willing to unleash vengeful chaos on global markets aimed at its geopolitical enemies while hunkering down, with the Saudis too showing willingness to play chicken.

Amid Trump’s statements and the new reports the WTI rallied in what could be a record-setting single day, increasing by 22.28% in afternoon trading – though still trading down double digits since the start of the year.

Meanwhile, the current OPEC agreement to curb production will expire on April 1st, after which it’s expected Russia, Saudi Arabia and UAE will dump a flood of cheap crude onto the market.

Are you prepared for the nationwide shutdown that is happening now to last for the next 18 months? You may not believe that such a thing will happen, but the federal government apparently does. A 100 page government plan marked “For Official Use Only // Not For Public Distribution or Release” was obtained by the New York Times, and it paints a very bleak picture of what is coming.

If the projections in this document are anywhere close to accurate, large numbers of Americans will die, the U.S. economy will completely implode, and we will see widespread civil unrest. So let us pray that the assessments in this government plan turn out to be dead wrong.

A federal government plan to combat the coronavirus warned policymakers last week that a pandemic “will last 18 months or longer” and could include “multiple waves,” resulting in widespread shortages that would strain consumers and the nation’s health care system.

The 100-page plan, dated Friday, the same day President Trump declared a national emergency, laid out a grim prognosis for the spread of the virus and outlined a response that would activate agencies across the government and potentially employ special presidential powers to mobilize the private sector.

I can’t even imagine what our country would look like if current conditions stretched into the middle of 2021.

As a nation, I don’t believe that we would be able to handle it.

“Shortages of products may occur, impacting health care, emergency services, and other elements of critical infrastructure,” the plan warned. “This includes potentially critical shortages of diagnostics, medical supplies (including PPE and pharmaceuticals), and staffing in some locations.” P.P.E. refers to personal protective equipment.

Meanwhile, the overall economy continues to collapse at a staggering pace. A former economic adviser to President Trump is now warning us that the U.S. economy could lose up to a million jobs this month alone…

Kevin Hassett, who served as a top economic adviser to President Trump until last summer, said Monday that the United States economy could shed as many as one million jobs in March alone because of layoffs and hiring freezes related to the coronavirus.

“If you have normal job disruption, and hiring just stops,” Mr. Hassett said, “you’ll have the worst jobs number ever.”

But if this pandemic continues to escalate, a million jobs lost will just be a drop in the bucket.

The National Restaurant Association is predicting the unprecedented carnage is only just beginning, on Wednesday writing a letter to the White House and Congress detailing an estimated $225 billion in sales will be wiped out over the next three months, crucially prompting the loss of between five and seven million jobs.

Remember, that is just one industry.

The retail industry is also being completely devastated as well, and we just learned that the largest operator of shopping malls in the United States is shutting them all down…

Simon Property Group, the largest owner of shopping malls in the nation, is closing all of its malls and retail properties because of the coronavirus outbreak.

The closings start at 7 p.m. local time Wednesday and the malls are expected to end March 29, the Indianapolis-based company said in a news release.

Of course they won’t actually open back up on March 29th if this pandemic continues to get worse.

So far, COVID-19 has killed less than 200 Americans.

If our society is being this disrupted now, what will things be like if the death toll becomes 1,000 times larger?

For years, I have warned that our economy was extremely vulnerable, and now that is becoming exceedingly obvious to everyone. It certainly didn’t take too much of a push to burst all the bubbles and send everyone into a severe panic, and now the economy is collapsing at a pace that is absolutely breathtaking.

According to NBC News, state unemployment websites all over the nation are crashing because so many people are suddenly applying for unemployment benefits…

Workers who have suddenly found themselves without a paycheck because of the growing coronavirus pandemic in the United States are now dealing with another frustration — state unemployment websites crashing because of high traffic.

From Oregon to New York and Washington, D.C., officials and Twitter users have highlighted the problem after the mass closing of restaurants, retail stores and other businesses as part of the effort to slow the spread of the virus.

Tomorrow morning most Americans will wake up assuming that their jobs are safe. But right now an increasing number of people are being let go without any advance warning whatsoever. Here is one example…

Eileen Hanley was wrapping up her weekend and getting ready for the week ahead on Sunday evening when an email popped up in her inbox with the subject line “COVID-19 uncertainty.” It was from her boss at the small Manhattan law firm where she worked part time as a receptionist.

“We hope you are feeling well during this time,” the email began. Then it cut to the chase: The firm was losing revenue because of the outbreak, and it would have to eliminate “a number of positions,” including hers, “effective immediately.”

We have never seen anything like this before.

Things were tough during World War II, but it was actually a time when the country geared up and worked extremely hard to defeat the enemy.

But now economic activity all over America is being brought to a screeching halt. In fact, we just learned that the three largest automakers have shut down all of their U.S. factories…

Detroit’s Big Three automakers plan to temporarily close all U.S. factories as the coronavirus sweeps across the country.

The companies bowed to pressure from union leaders and employees who called for protection from the pandemic that’s spread to more than 212,000 people in nearly every country across the globe.

As a nation, we would survive a 30 day shutdown.

But if life doesn’t get back to normal for “18 months”, we are going to witness a societal meltdown of epic proportions.

This week, investor Bill Ackman told CNBC that “hell is coming”, and he warned that unless the entire country is shut down simultaneously for an extended period of time “America will end as we know it”…

“What’s scaring the American people and corporate America now is the gradual rollout,” Ackman told Scott Wapner on “Halftime Report” on Wednesday. “We need to shut it down now. … This is the only answer.”

“America will end as we know it. I’m sorry to say so, unless we take this option,” he said. Ackman added that if Trump saves the country from the coronavirus, he will get reelected in November.

I believe that he makes an excellent point, but I would take it one step further.

If the entire world shut down for 30 days, this pandemic would quickly be brought under control. If only the U.S. shuts down, it is inevitable that the virus would keep coming back into the country as the pandemic continues raging elsewhere on the globe.

Of course we aren’t going to get the entire globe to agree to shut down simultaneously for 30 days.

So this outbreak will continue to spread and the case numbers will continue to grow.

For a long time I have been warning that something would come along that would burst all the bubbles and trigger a horrifying economic meltdown.

Now it is upon us, but now is not a time for fear.

With God’s help, we will get through this.

But life is not going to go back to the way it was before.

Next Stimulus Deal To Include “Rapid Injection Of Cash” For Small Businesses

The next stimulus deal will include targeted lending for certain industries, which Senate Majority Leader Mitch McConnell (R-KY) called a “rapid injection of cash” for small businesses, according to Bloomberg.

During opening floor comments on Thursday, McConnell said that the Senate is looking to quickly draft and pass legislation that will provide swift relief to businesses and individuals struggling amid the coronavirus pandemic, as businesses, schools and airports have become virtual ghost towns.

The GOP stimulus proposal will call for direct payments to middle-income individuals and families — the centerpiece of Trump’s $1 trillion stimulus plan — as well as $250 billion to $300 billion in relief for small businesses, tens of billions of dollars in loans for the airline industry and an array of health measures, according to lawmakers familiar with the talks.

Senate Republicans say the direct payments will be modeled on the rebates sent out by the George W. Bush administration in 2008 to mitigate the effect of the financial crisis, payments that were phased out for individuals with income exceeding $75,000 and joint income more than $150,000. –The Hill

That said, the next deal will hinge upon successful negotiations between McConnell and top Senate Democrat, Chuck Schumer of New York – who “don’t have much of a working relationship” according to The Hill.

Senators have hope that the two can put their differences aside and move forward during a Thursday meeting.

The toxic relationship between the two was on public display almost daily during President Trump’s impeachment trial earlier this year. But senators think the leaders can put aside past fights to hash out a deal, despite some major differences between the two parties.

Sen. John Cornyn (R-Texas) said Republicans and Democrats have “always come together” during national crises like the 9/11 attacks.

“We’ll do it again,” he said.

Other Republicans, however, are wary of Schumer’s motives and think he may try to gain a political advantage ahead of the November election, when Democrats are hoping to win back the Senate. –The Hill

Democrats say the plan should be to expand health care resources, boost unemployment benefits and freeze student loan payments.

Schumer has been called out for playing political games, according to some.

“It’s disturbing to see [coronavirus] politicized as Chuck Schumer has done on the floor of the Senate,” said Senate Republican Policy Committee Chairman John Barrasso (WY) in an appearance on Fox News.

Schumer spoke with Treasury Secretary Steven Mnuchin twice on Wednesday, where he warned that Democrats will push back against any relief package that is geared towards bailing out giant corporations instead of workers.

“If there are going to be some of these corporate bailouts, we need to make sure workers and labor come first. That people are not laid off. That people’s salaries are not cut,” Schumer said in a statement.

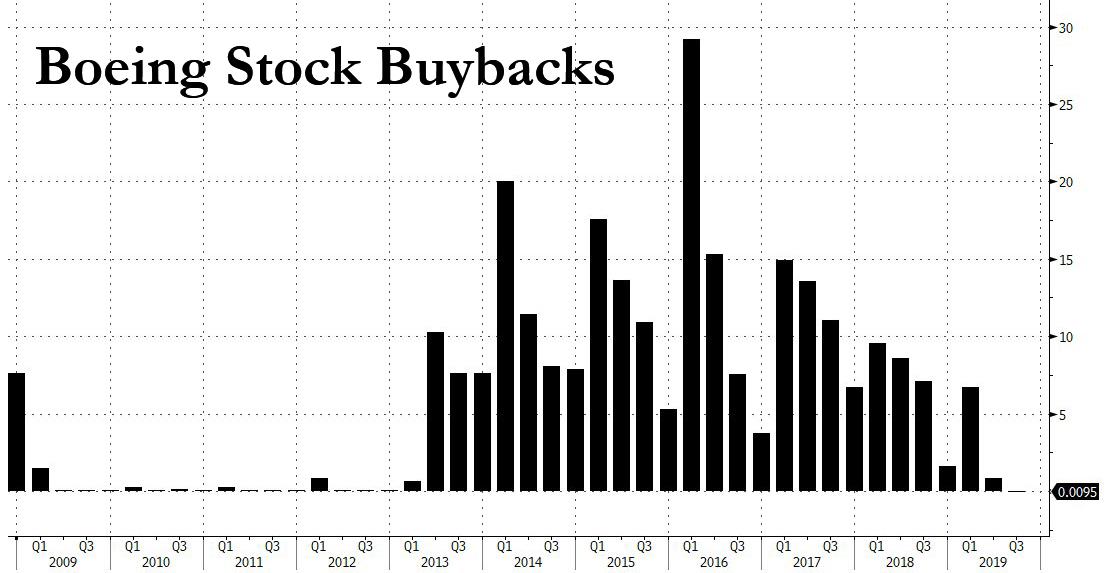

Schumer noted that U.S. airlines have spent tens of billions of dollars on stock buybacks in recent years. American Airlines and Southwest Airlines have spent $12 billion and $11 billion, respectively, on stock buybacks since 2014.

“They have to put their workers first if they’re going to get this help,” Schumer said.

Summing up the Republican and Democratic priorities as the talks start, the Democratic leader said “a lot of them overlap” but added “there are some things that we’re going to want.”

McConnell urged senators on Wednesday night to “stay close” to the Capitol in case there’s a sudden breakthrough, telling colleagues “while we don’t know exactly how long it will take to get this done, everyone knows that we need to do it as quickly as possible.” –The Hill

GOP Senators expect talks to extend into next week.

“I would guess we’re there by next Friday,” said one Republican senator as to when President Trump might receive the bill.

A scientific study has found that had China acted sooner to combat the spread of their coronavirus, then the spread could have been almost entirely avoided, and it would not have become a global pandemic.

Research out of the University of Southampton in the UK, based on world population mapping funded primarily by the Bill and Melinda Gates Foundation, discovered “that if interventions in [China] could have been conducted one week, two weeks, or three weeks earlier, cases could have been reduced by 66 percent, 86 percent and 95 percent respectively – significantly limiting the geographical spread of the disease.”

Study author Dr Shengjie Lai, of the University of Southampton, comments: “Our study demonstrates how important it is for countries which are facing an imminent outbreak to proactively plan a coordinated response which swiftly tackles the spread of the disease on a number of fronts.”

“A study published in March indicated that if Chinese authorities had acted three weeks earlier than they did, the number of coronavirus cases could have been reduced by 95% and its geographic spread limited.”

Director of the University of Southampton’s WorldPop group, Professor Andy Tatem, adds: “We have a narrow window of opportunity globally to respond to this disease and given effective drugs and vaccines are not expected for months, we need to be smart about how we target it using non-drug-related interventions.”

“Our findings significantly contribute to an improved understanding of how best to implement measures and tailor them to conditions in different regions of the world.” Tatem continued.

It has become clear that the first cases of the Chinese virus were reported in mid-late November and early December, with scientists even estimating that the first jump of the virus from animals to humans probably occurred in October in the city of Wuhan.

Instead of acting immediately, the Chinese government waited until January 23rd before issuing quarantine orders to the 11 million people living in Wuhan.

The communist state was also actively working to suppress and punish doctors and scientists who tried to get warnings out, and lied to the world by claiming there was “no evidence” of human-to-human transmission.

“Chinese laboratories identified a mystery virus as a highly infectious new pathogen by late December last year, but they were ordered to stop tests, destroy samples and suppress the news.”

They covered it up for a over month, brutally silenced whistleblowers, lied to the rest of the world and facilitated a geographic spread that would have been reduced by 95% if they’d been honest.

It is disgustingly racist to blame a country for the spread of a virus simply because of horrifying sanitary conditions at wet markets, animal cruelty involving sickening cross-contamination, & dictatorial suppression of information that could have averted this global pandemic.

Boeing, Which Demands A Bailout, Is Only Now Considering Cutting Its Dividend

Having sparked public outrage after demanding politely asking for a $60 billion bailout earlier this week after repurchasing tens of billions of its own shares over the past decade…

… resulting in record corporate leverage…

… leverage which now means the company is on the verge of collapse as cash flows grind to a halt, but more importantly which funded record management equity-linked bonuses and spawned some very rich shareholders, at least until this month, Boeing has finally decided to “punish” its shareholders and according to the WSJ, the aerospace giant is now considering cutting its dividend as well as launching mass layoffs at its jetliner plants, as America’s largest manufacturer grapples with an unprecedented disruption to the global airline industry.

What is shocking is that it took until the Boeing stock price lost more than two thirds of its value amid rising solvency fears, that Boeing took the “draconian” step of limiting how much cash it would syphon out to its shareholders. Maybe Boeing’s new management team was hoping to quietly sneak through not only dividend but buybacks, all funded by the upcoming multi-billion taxpayer bailout?

Oh, and it’s worth noting that Boeing – which is pretending that the bailout would go toward keeping its employees in their jobs – will also slash thousands of jobs, because if shareholders are punished, workers must be too.

To be sure, on one hand there is little Boeing could have done to prevent the fallout from a viral superbug escaping the Wuhan Institute of Virology. On the other, instead of injecting trillions into the bank accounts of its shareholders, the company could have been building a rainy day fund for times just like this because, guess what, it’s pouring.

“Nobody’s flying,” a Boeing official said. In response, Delta Air Lines this week said it had cut 70% of its flying until demand improves and is parking 600 jets, two-thirds of its fleet. It won’t take any new jets this year. Delta also said officers would take a 50% pay cut until the situation normalizes. Additionally, airlines are deferring deliveries from this year after the near-collapse in passenger traffic, and cancellations are on the rise, starving Boeing of new cash and draining liquidity in the form of deposit refunds.

That said Boeing is not alone: its European rival, Airbus, whose shares have fallen almost as much as Boeing’s this year, is also seeking government support in Europe. Its global supply network is entwined with that of Boeing, raising questions about how packages on both sides of the Atlantic could be structured.

Texas Man Arrested After “The Virus Has Become Airborne” Hoax Post Sparks Chaos

As states across the US raced to shut down businesses, limit mass gatherings, and enforce social distancing last week amid the Covid-19 outbreak, one Texas millennial was arrested after he sparked chaos in East Texas for lying on social media about contracting the deadly disease, reported CBS Austin.

The Tyler County District Attorney’s Office said they received numerous complaints about a man claiming on social media that he tested positive for coronavirus on March 13. Deputies made contact with 23-year-old Michael Lane Brandin of Woodville, Texas, for his Facebook post, where he claimed that he had contracted the virus and health officials at Tyler County Hospital told him that the virus has become airborne.

Michael Lane Brandin of Woodville, Texas

Sheriff Bryan Weatherford told KJAS that Brandin turned himself in on Tuesday and was charged with False Alarm, which is a class A misdemeanor, and Tyler County Judge Jacques Blanchette set his bond at $1,000.

Brandin in jail

District Attorney Lucas Babin said the young man’s Facebook post caused panic across East Texas. He said phone lines at Tyler County Hospital were tied up with concerned residents.

Babin said Brandin told Tyler County investigators that he wrote the post as a “social experiment” to make a point that everything online can’t be trusted. Babin said the young man did it for attention.

Babin wrote a Facebook post reminding residents:

“Knowingly communicating, initiating, or circulating a false report/false alarm of COVID-19 that one *knows is false or baseless*, and that would ordinarily cause action by an official or interrupt the occupation of any place of assembly, can be a criminal offense in the State of Texas.”

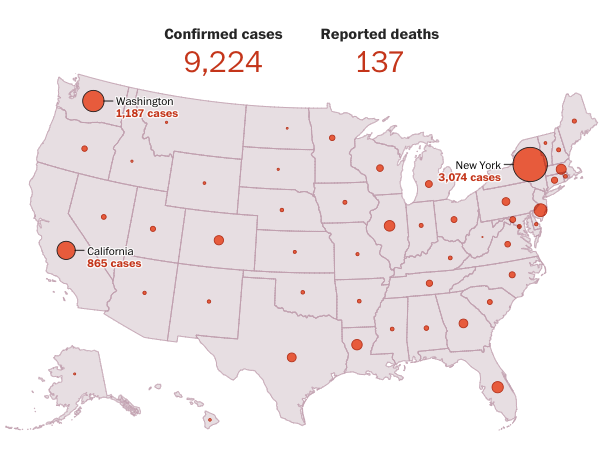

As of Thursday morning, Texas has 201 confirmed cases. The US is now pushing above the 9,200, with 137 deaths. The move in cases this week has been exponential and will likely continue throughout the month.

{kind=link}

{kind=link}

{kind=link}

{kind=link}