Spanish police are taking a page out of China’s Orwellian playbook by using drones to patrol and yell at their civilians who are disobeying the CoViD-19 quarantine.

The country issued a state of emergency on Friday, and on Saturday the government ordered everyone in the country to stay home for all but the most crucial trips outdoors, according to Business Insider. Now, much like China did earlier this year, Spanish police are using drones to demand that citizens stay indoors without having to approach them and risk spreading the virus.

Police in Spain have been using drones to check the streets for anyone ignoring Spanish orders to stay home during the coronavirus outbreak

Video from the BBC shows police speaking into a radio and urging people walking through a Madrid park to go home. That message is then relayed into a drone utilizing a loudspeaker flying overhead demanding Spain’s citizens quarantine themselves inside their homes.

In Spain, all schools, restaurants, bars, sports venues, and cultural centers have been ordered closed, and social gatherings are also forbidden under declaration of a National Emergency. Spain has been one of Europe’s hardest hit countries, after Italy, with a death total of 509 deaths and 11,000 cases of infections according to Johns Hopkins map at the time of this report.

Most of Spain’s cases have been recorded in the Madrid region, according to the Spanish Health Ministry.

“We won’t hesitate to use all the measures we have at our disposal to look out for your safety and everyone’s safety,” the city’s police department said on Twitter. “Although some of you will give us a hard time.”

Spain’s prime minister Pedro Sanchez called for unity and cooperation announcing the new measures to combat the CoViD-19 virus, the Independentreported.

— Policía Municipal de Madrid (@policiademadrid) March 14, 2020

“I want to tell the workers, the self-employed and businesses that the government of Spain is going to do everything in its power to cushion the effects of this crisis,” Sanchez said. “Spain is demonstrating in these critical hours that it has the capacity to overcome adversity.”

“We are facing very difficult weeks of efforts and sacrifices. Some important rights must be limited if we want to beat the virus,” Sanchez also said.

Those who break the rules of the quarantine in Spain can be fined up to €600,000 and face prison time for their negligence.

The state of emergency will last two weeks, though may be extended if the situations warrants.

BoE’s Bailey To Print Unlimited Money, Tells Short Sellers “Just Stop” Amid Covid-19 Chaos

BoE governor Andrew Bailey said on Wednesday that the central bank stands ready to pump unlimited amounts of money into the economy.

Speaking to journalists on a conference call, quoted by Financial Times, Bailey said the central bank is prepared to pump liquidity into markets via its new commercial paper facility. He said this would limit economic damage produced by the virus crisis.

BREAKING: Bank of England governor, Andrew Bailey, just said he’s willing to print unlimited quantities of money and pump in into the economy.

Ironic coming from a man that last month said those holding bitcoin should “be prepared to lose all of your money” pic.twitter.com/JDQpQ2HBVE

He told members of the financial community that they must stop ‘exploiting’ vulnerable business by betting against them:

“Anybody who says, ‘I can make a load of money by shorting’ [aggressively betting on the value of specific companies continuing to fall] which might not be frankly in the interest of the economy, the interest of the people, just stop doing what you’re doing.”

Bailey made it clear that financial markets will remain open as a sign of confidence. He said firms who are thinking of reducing staff must reconsider because support from the central bank and government can lessen the shock.

He urged firms to “stop, look at what’s available, come and talk to us [or] the government before you take that position,” adding that support will be supplied to citizens as well.

The hardest-hit UK industries have so far been airliners, retailers, restaurants, movie theaters, and much of the services industry, as it has completely ground to a halt as the government enforces social distancing measures to flatten the curve to slowdown infections. As of 2018, the services sector accounted for at least 80% of the UK economy.

Baily said emergency loans have been available by the central bank to companies that have already fired employees. He told BBC News:

“I would emphasise the point that it’s critical that we support the needs of the people in the country.”

Baily took the reins from Mark Carney at midnight on Monday and has already faced an economic crisis on par to a decade ago as helicopter money is now needed to save the economy from crashing.

The BoE is expected to cut interest rates from .25% to .10% and resume quantitative easing when it meets next week. Bailey isn’t a supporter of NIRP and has pushed measures to shield businesses and workers from virus impacts.

Italy’s healthcare system is in a state of almost total collapse. As of today, 31,506 people in Italy have been infected with the coronavirus; of which 2,503 people have died. The numbers continue to grow. Hospitals are overwhelmed. Doctors have to choose which sick person to save and which sick person not to save.

The country has almost completely shut down. Many businesses are running in slow motion or have stopped. Prisoners are staging uprisings. Millions of people have been ordered to stay home and are allowed out only briefly to buy food. Most shops are shut. All public gatherings are prohibited, even funerals. Big cities look like ghost towns.

No other Western country has been so severely affected by the pandemic as Italy. Why?

First, Italy has an aging population. The median age of Italians is 47.3 years; one in four Italians is over 65. In addition, the country’s birth rate is extremely low: 1.29 children per woman. Even before the coronavirus pandemic, Italy was a dying country. Sadly, the virus has accelerated the process.

Second, the authorities and medical personnel apparently underestimated the danger. Although the Italian government had suspended flights for days from China and Hong Kong from January 31, Italian doctors were saying that the illness was just a “bad flu“. On March 9, an epidemiologist, Silvia Stringhini, wrote: “The media are reassuring, the politicians are reassuring, while there’s little to be reassured of”.

Third, the Italian health system is in appallingly bad condition. There are not enough intensive care units and, as everywhere, the possibility of a major crisis simply was not anticipated. In Italy there are 2.62 acute-care hospital beds per 1,000 residents (by comparison, the number in Germany is 6.06 per 1,000 residents). The Italian health system is entirely run by the government. A public health care service (SSN, Servizio Sanitario Nazionale) pays the doctors directly, limits their number, and sets the maximum number of patients they can treat per year (1,500).

Government-run healthcare always ends up being about the government trying to cut its costs rather than to help its citizens. Private clinics do exist, but represent only a small part of the care offered (the public system represents 77% of total health-care spending. (The only country in Europe where the figure is higher is the United Kingdom, where the figure is 79%.) Public hospitals must manage shortages, and when an exceptional situation occurs, rationing care leads to horrific choices. A recent report by Siaarti (Società Italiana di Anestesia Analgesia Rianimazione e Terapia Intensiva) bureaucratically offers “ethical recommendations for admission and intensive treatment in exceptional conditions of imbalance” and speaks of “consensual criteria of distributive justice” to justify not treating certain patients and leaving them to die.

Fourth, and rarely mentioned, is that Italy today is evidently home to a large Chinese community (more than 300,000), made up of people who arrived in the past two decades and who work in the textile and leather sector. Many of the Chinese living in Italy are from Wuhan and Wenzhou, and some had just been in Wuhan and Wenzhou for the Chinese New Year on January 25, when the Chinese authorities could not hide the epidemic any longer. These Chinese had returned to Italy from China before the Italian government suspended flights from there. The epidemic emerged in Lombardy; Bergamo, one of the capitals of the Italian textile industry, was one of the first cities affected.

Before the pandemic, the Italian economy was already in a state of stagnation; now, as people stay home and shops shut, it will probably plunge into a recession. Italian banks, since mid-February, have lost 40% of their market value. Major financial upheavals seem on the way.

The Italian government was hoping for help from the European Union, but neither the other member states nor the European Union itself has given any at all. Maurizio Massari, Italy’s ambassador to the European Union, said at a recent European summit on the pandemic, that Brussels should go beyond “engagement and consultations”, and that Italy needed “quick, concrete and effective actions”. He got nothing.

Christine Lagarde, president of the European Central Bank, refused to lower interest rates to help Italy; it was a statement Italian leaders took as a demonstration of contempt. Italian President Sergio Mattarella said that Italy expected “solidarity from the EU institutions,” not “moves that could hinder Italy’s actions”. “Italy,” said Matteo Salvini, leader of the Lega party, “has been given a slap in the face”.

The dismissive attitude of the EU and the other members states seems to have been dictated by the fear of sliding into a situation as calamitous as that of Italy.

All European countries have an aging population, even if less than Italy’s (the median age in Germany is 46.8; in France it is 41.2; in Spain it is 42.3). No country in the European Union has taken a clear, hard look at the danger Europe is facing.

“The coronavirus is very contagious,” France’s minister of health, Agnes Buzyn, said on January 26, “but much less serious than we thought”.

The borders between France and Italy were not closed in time (only Austria and Slovenia closed their borders with Italy early), and Italians who wished to go to France were not stopped. The health systems of other European countries are not better prepared than the Italian one was. In Spain, Insalud (Instituto Nacional de Gestion Sanitaria), an organization equivalent to the Italian system, exists, and shortages and rationed care are the rule. The German (Krankenkassen) and the French (Sécurité Sociale) health insurance systems also operate on the same principles as those in Italy and Spain, and produce similar results. The economies of the main countries of the European Union were in a state of stagnation before the pandemic, and, like the Italian economy, are likely to plunge into a recession soon, too.

At the time of publication, 11,826 people were infected in Spain, 7,695 in France, and 9,360 in Germany. In Spain, 533 people have died; in France, 148 people, and in Germany only 26. As in Italy, the numbers escalate fast.

On March 11, German Chancellor Angela Merkel said to journalists who were accusing her of doing nothing, “60 to 70% of Germans will be infected with the coronavirus”. Lothar Wieler, President of the Robert Koch Institute, the German government agency in charge of disease prevention and control, added that it was necessary to “avoid overloading hospitals” and to let the epidemic gain ground slowly over time.

An adviser to French President Emmanuel Macron told a journalist at Le Figaro that the strategy of France was the same as in Germany: the decision was made to “let the epidemic run its course and not try brutally to stop it”. He suggested that the official will was to create “herd immunity“, a term first used in the United Kingdom by Sir Patrick Vallance, the UK government’s chief science adviser. He had said that the aim of the British government was to accept that a significant number of the citizens of a country would be infected, recover, and therefore be immunized. The French and German authorities evidently found inspiration in Sir Patrick’s remarks.

The British government, faced with criticism from the World Health Organization, replied that “herd immunity” was not a stated policy, but no statement by the German or French governments said that “herd immunity” was not the policy they chose.

Umair Haque, the British Director of the Havas Media Lab, wrote:

“Herd immunity describes how a population is protected from a disease after vaccination by stopping the germ responsible for the infection being transmitted between people. Letting an entire nation be rampaged by a lethal virus for which there’s no vaccine? How much death and mayhem would that cause, by the way?”

“Europe has now become the epicentre of the pandemic, with more reported cases and deaths than the rest of the world combined, apart from China,”noted Tedros Adhanom Ghebreyesus, director general of the World Health Organization. “More cases are now being reported every day than were reported in China at the height of its epidemic.” Sadly, all available data show that he is right.

On March 11, President Donald Trump announced that the US was suspending all flights between the United States and Europe, a decision fully justifiable to save American lives. The next day, nevertheless, the heads of the European Union could not resist trying to maul the president: “The EU disapproves of the fact that the U.S. decision to impose a travel ban was taken unilaterally and without consultation,” they said.

It is to be hoped that by now notions of ”herd immunity” have been abandoned, and that the EU gets back to salvaging for Europe whatever it can.

China Takes Axe To Alternative Energy Funding, Slashing Subsidies For Solar And Wind

Things might be going from bad to worse for Elon Musk and his merry band of alternative energy cultists in China. While Musk is currently in the midst of criticism from the Chinese government related to a bait and switch he is pulling on vehicle hardware (while blaming the coronavirus), the Chinese government appears to be set on slashing additional alternative energy subsidies in 2020.

China is going to cut its budget for new solar power plants in half this year and plans on completely ending handouts for offshore wind farms, according to Caixin.

It is the latest in a string of moves by the Chinese government to cut support for renewable energy. The attitude has shifted in recent years as manufacturing costs have dropped. The government now seems focused on getting renewable energy to stand on its own.

On Tuesday, China’s National Energy Administration (NEA) announced it had cut this year’s subsidies for new solar power projects by 50% to 1.5 billion yuan ($215.8 million). “Of the total, it has earmarked 1 billion yuan for large solar projects, which will be divvied out through auctions. The remainder will be used for residential solar systems,” Caixin reports.

China is also doing away with subsidies for new offshore wind farms this year and is ending subsidies for new onshore projects in 20201.

Shi Jingli, a professor at a research institute under China’s top economic planner said: “Cutting subsidies for new renewable energy projects is a reasonable measure to allocate funds more wisely. The generous subsidies given to offshore wind farms over the past few years have weighed on the central government’s finances and caused severe deficits in subsidy funding.”

Jingli continued: “Considering the damage that the coronavirus outbreak has done to businesses, the NEA has extended the application period for the auctions until mid-June. It has also given solar and wind farm operators an additional month to apply to connect their projects to the country’s power grid, which is necessary for a power plant to start selling electricity.”

Meanwhile, new installations of solar power capacity plunged 40% last year after the country installed 26.81 gigawatts of new capacity. Numerous other projects underway have already hit major delays due to the coronavirus outbreak and supply chain disruptions.

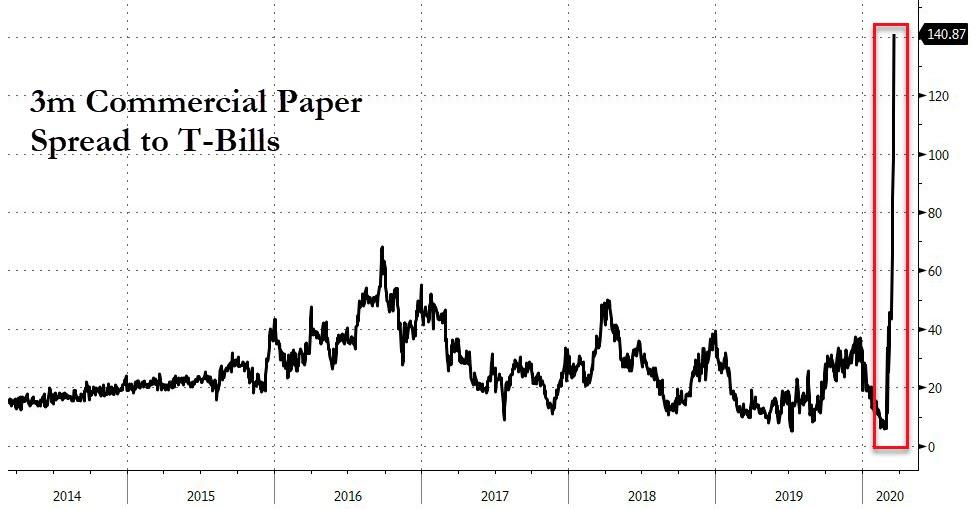

Lehman Playbook Continues: Fed Unveils Another Bailout Fund To Avoid Money Market Funds ‘Breaking The Buck’

The four-letter acronyms for ‘bailout’ continue to play out exactly like during the Lehman crisis (as we previewed here), as The Fed desperately tries to hold the backbone of the entire global financial markets together with whack-a-mole buying programs to avoid investors seeing behind the curtain of the whole Potemkin Village.

The second (MMIFF)was designed to provide liquidity for money market mutual funds, stimulating them to extend the term of their money market investments.

Instead of scrambling for overnight assets because of liquidity fears, this would help maintain demand for term securities in the money market. Although no loans were made under the MMIFF, the facility could be useful this time. While CPFF helps issuers of commercial paper, money market mutual funds are still in need of liquidity.

A related facility, which peaked at $140bn in 2008, was the Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF)which provided funding for depository institutions purchasing asset-backed commercial paper from money market mutual funds.

As if one needs reminding, one of the more dramatic events from the 2008 crisis was the sight of mutual funds trading below $1 – so-called ‘breaking the buck’.

When money-market investors fear they won’t get back their capital it will make a bad situation into a real crisis.

As the biggest buyers of commercial paper, this bailout facility is clearly aimed, once again, at being another effort to reduce the spiking risks (and freeze) in the critical short-term liquidity markets.

And so, paging through the “OMFG, what do we do now that didn’t work in the past”-playbook, this new facility will make loans available to eligible financial institutions secured by high-quality assets purchased by the financial institution from money market mutual funds.

We wait to see how effective this latest four-letter-word will be in calming the savage beast of a global dollar shortage.

The Federal Reserve Board on Wednesday broadened its program of support for the flow of credit to households and businesses by taking steps to enhance the liquidity and functioning of crucial money markets.

Through the establishment of a Money Market Mutual Fund Liquidity Facility, or MMLF, the Federal Reserve Bank of Boston will make loans available to eligible financial institutions secured by high-quality assets purchased by the financial institution from money market mutual funds.

Money market funds are common investment tools for families, businesses, and a range of companies. The MMLF will assist money market funds in meeting demands for redemptions by households and other investors, enhancing overall market functioning and credit provision to the broader economy.

The term sheet below details the types of assets, including unsecured and secured commercial paper, agency securities, and Treasury securities, that are eligible, as well as additional information. The MMLF program will purchase a broader range of assets, but its structure is very similar to the Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility, or AMLF, that operated from late 2008 to early 2010. The MMLF is established by the Federal Reserve under the authority of Section 13(3) of the Federal Reserve Act, with approval of the Treasury Secretary. The Department of the Treasury will provide $10 billion of credit protection to the Federal Reserve in connection with the MMLF from the Treasury’s Exchange Stabilization Fund.

Term Sheet:

Money Market Mutual Fund Liquidity Facility

Facility: To provide liquidity to Money Market Mutual Funds (“Funds”), the Federal Reserve Bank of Boston

(“Reserve Bank”) would lend to eligible borrowers, taking as collateral certain types of assets purchased by

the borrower from Funds (i) concurrently with the borrowing; or (ii) on or after March 18, 2020, but before

the opening of the Facility.

Borrower Eligibility: All U.S. depository institutions, U.S. bank holding companies (parent companies

incorporated in the United States or their U.S. broker-dealer subsidiaries), or U.S. branches and agencies of

foreign banks are eligible to borrow under the Facility.

Funds: A Fund must identify itself as a prime money market fund under item A.10 of Securities and Exchange

Commission Form N-MFP.

Advance Maturity: The maturity date of an advance will equal the maturity date of the eligible collateral

pledged to secure the advance made under this Facility except in no case will the maturity date of an advance

exceed 12 months.

Eligible Collateral: Collateral that is eligible for pledge under the Facility must be one of the following types:

1) U.S. Treasuries & Fully Guaranteed Agencies;

2) Securities issued by U.S. Government Sponsored Entities;

3) Asset-backed commercial paper that is issued by a U.S. issuer, is rated at the time purchased from the

Fund or pledged to the Reserve Bank not lower than A1, F1, or P1 by at least two major rating agencies

or, if rated by only one major rating agency, is rated within the top rating category by that agency; or

4) Unsecured commercial paper that is issued by a U.S. issuer, is rated at the time purchased from the

Fund or pledged to the Reserve Bank not lower than A1, F1, or P1 by at least two major rating agencies

or, if rated by only one major rating agency, is rated within the top rating category by that agency.

In addition, the facility may accept receivables from certain repurchase agreements.

Rate: Advances made under the Facility that are secured by U.S. Treasuries & Fully Guaranteed Agencies or

Securities issued by U.S. Government Sponsored Entities will be made at a rate equal to the primary credit

rate in effect at the Reserve Bank that is offered to depository institutions at the time the advance is made.

All other advances will be made at a rate equal to the primary credit rate in effect at the Reserve Bank that is

offered to depository institutions at the time the advance is made plus 100 bps.

Fees: There are no special fees associated with the Facility.

Collateral Valuation: The collateral valuation will either be amortized cost or fair value. For asset-backed

and unsecured commercial paper, the valuation will be amortized cost.

Credit Protection by Department of the Treasury: The Department of the Treasury, using the Exchange

Stabilization Fund, will provide $10 billion as credit protection to the Reserve Bank.

Non-Recourse: Advances made under the Facility are made without recourse to the Borrower, provided the

requirements of the Facility are met. For avoidance of doubt, borrowers under the MMLF will bear no credit

risk.

Regulatory Capital Treatment: Separately and consistent with the purposes of the MMLF, the Board, the

OCC, and FDIC will act to fully neutralize the impact of a depository institution holding company or depository

institution’s participation in the facility for purposes of regulatory capital requirements, including risk-based

capital and leverage requirements. The Board, OCC, and FDIC will fully exempt from risk-based capital and

leverage requirements (i) any asset pledged to the MMLF and (ii) any asset purchased from a Fund on or after

March 18, 2020 that the firm intends to pledge to the MMLF upon opening of the Facility.

Program Termination:No new credit extensions will be made after September 30, 2020, unless the Facility is

extended by the Board of Governors of the Federal Reserve System.

* * *

So this better all be fixed by September?

The market for now was completely unimpressed by this latest effort:

As Republican and democrat politicians hold emergency meetings to decide how to avoid a meltdown of Wall Street, the smell of hyperinflation looms in the air as much today as it did in Germany during the opening months of 1922. This week, markets were propped up by a record breaking offering of $1.5 Trillion in liquidity injections over the coming months (added to the $9 trillion already injected over the past six months), and rather than deal with the real reasons for this oncoming financial collapse, the media has brainwashed the west that everything would have been just fine, “if only coronavirus had not become a pandemic”.

But what is really being bailed out here exactly and why? Is this money actually making it to the real economy? Is it being invested to rebuild America’s farms, businesses and industry?

It is my contention that Trump is genuine in his desire to “drain the swamp” and rebuild America’s lost industrial base. I also genuinely believe that Trump wishes to establish positive relations with Russia, China and other sovereign nation states which has drawn the ire of the international deep state. However Trump’s potentially fatal blind spot appears to be his tendency to believe the lie that Wall Street’s wellbeing is somehow indicative of America’s wellbeing.

If Trump is intelligent, (and his previous calls for Glass-Steagall’s restoration, and American System practices imply that he knows a thing or two), then rather than bailing out Wall Street by unleashing more gasoline onto the fire, it were better that he took the lessons of 1933 and established a new Pecora Commission for 2020.

What was the Pecora Commission?

Many are aware of the economic meltdown of October 24,1929 that ushered in four years of depression onto America (and much of the western world). However not many people are aware of the intense fight that was launched by patriots in both parties against the Wall Street/deep state parasite of that age which prevented both a fascist coup against the newly elected Franklin Roosevelt while also crippling Wall Street’s command of American life. In spite of whitewashing revisionist history books that contaminated the past 70 years, America’s recovery from the depression never occurred without a life or death struggle and this struggle was made possible, in large measure by the courageous work of an Italian lawyer from New York. This man’s name was Ferdinand Pecora.

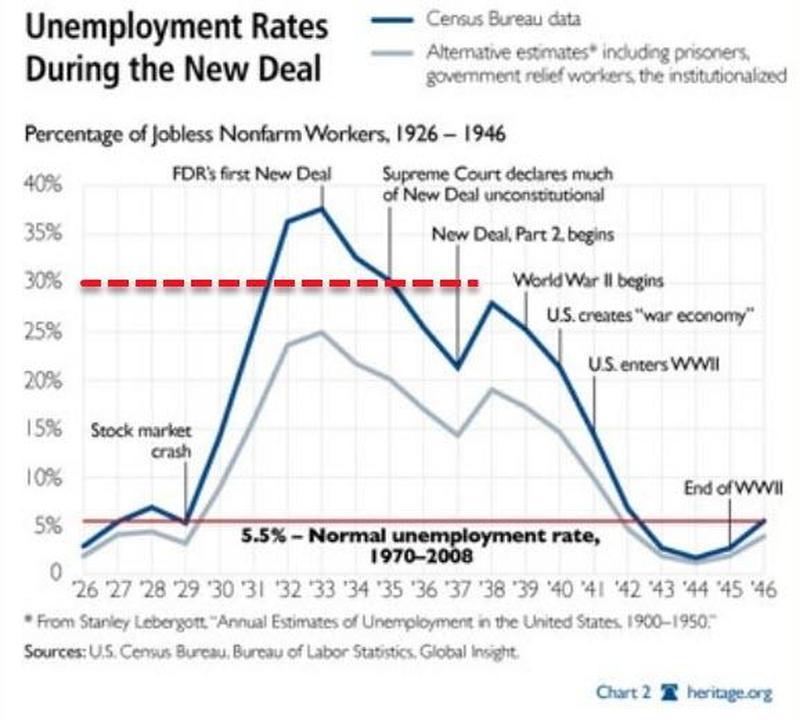

By 1932, when Senators Peter Norbeck (R-SD) and George Norris (R-NB) spearheaded the establishment of the U.S. Committee on Banking and Currency, the American economy was on life support and the people were so desperate that a fascist dictatorship in America would have been welcomed with open arms if only bread could be put on the table. Unemployment had reached 25%, while over 40% of banks had gone bankrupt and 25% of the population had lost their savings. Thousands of tent cities called ‘Hoovervilles’ were spread across the USA and over 50% of America’s industrial capacity had shut down. Thousands of farms had been foreclosed and the engines of American industry had grinded to a screeching halt.

Across the ocean, the fascist regimes of Germany, Italy and Spain were growing more powerful by the day fed by injections of hundreds of millions of dollars of capital by London and Wall Street bankers. Notable among these pro-fascist financiers was none other than Bush family patriarch Prescott, who provided millions in loans to Hitler’s bankrupt Nazi party in 1932 (and continued doing business with the party through 1942- having only stopped after being found guilty for “trading with the enemy”).

The Committee on Banking and Currency was a relatively impotent body when it began in 1932, but when Senator Norbeck called in Ferdinand Pecora to lead it in April 1932, everything began to change. A first generation Italian-American, Pecora was forced to quit high school after his father was injured in order to support his family. Years later, the young man found work as a clerk in a law firm, and managed to work his way through law school, passing the bar in 1911. His unimpeachable reputation earned him the animosity of powerful NY financiers who ensured that his successes in prosecuting brokers never resulted in attaining Attorney General, where he made a name for himself shutting down over 100 illegal brokerage houses that speculated on fraudulent securities during the depression.

Within days of accepting the Washington job as Chief Council of Norbeck’s committee (for the meager salary of $250/month), Pecora was granted broad subpoena powers to audit banks and drag the most powerful men in America to testify in the committee’s hearings.

In his first two weeks, Pecora made headlines by auditing the books of major Wall Street banks and pulled in pro-fascist National City President Charles Mitchell (then preparing to advise Benito Mussolini) to testify. Within days, Mitchell’s team of expensive defense attorneys could do nothing but watch in despair as the powerful financier admitted to short selling his own bank’s stocks during the depression, scamming depositors with purchases of Cuban junk debt and avoiding taxes for years. Mitchell was forced to resign in shame followed days later by NY Stock Exchange Chair Dick Whitney- who left the court in handcuffs.

This crackdown on Wall Street’s abuses were highly publicized and put the spotlight on the criminal schemes used to gamble with savings and commercial bank deposits on securities and futures markets which led to the orchestrated collapse of the bubble economy in 1929 (ironically much of the bubble built up during the “easy-money days” of the “roaring 20s” was centered in the housing market). Pecora’s crackdown also set the tone for the incoming Roosevelt administration.

Unlike the previous 1911 Pujo Commission led by Senator Charles Lindberg Sr. which also exposed Wall Street’s abuses of power, the Pecora Commission was supported by a President who actually cared about the Constitution and amplified Pecora’s powers even further. When FDR was told that supporting Pecora’s exposures of financial crimes would hurt the economy, the President famously responded with “they should have thought of that when they did the things that are being exposed now.” FDR followed up that warning by encouraging the attorney to take on John Pierpont Morgan Jr.

Rather than controlling an American institution as many believed 70 years ago and today, J.P. Morgan Jr. was actually running an operation that had earlier been created in the mid-19th century as part of a British infiltration of America. As historian John Hoefle pointed out in a 2009 EIR study:

“The House of Morgan was, in truth, a British operation from its inception. It began life as George Peabody & Co., a bank founded in London in 1851 by American George Peabody. A few years later, another American, Junius S. Morgan, joined the firm, and upon Peabody’s death the firm became J.S. Morgan & Co. Junius Morgan brought in his son, J. Pierpont Morgan, to head the New York office of J.S. Morgan, and the New York office became J.P. Morgan & Co. From its original role in helping the British gain control of American railroads, the Morgan bank became a leading force in the oligarchy’s war against the American System, using the deep pockets of its imperial masters to become a powerhouse in not only finance but steel, automobiles, railroads, electricity generation, and other industries.”

By 1933, the House of Morgan grew into a multi-headed hydra controlling utilities, holding companies, banks and countless other subsidiaries.

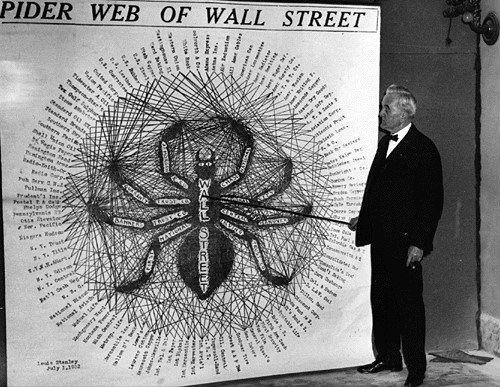

Senator George Norris showcasing a chart of Wall Street power

When J.P. Morgan jr. was called to testify, the banker carried a midget on his lap in mockery of the “circus of the commission”. As the questions began however, the arrogant banker was caught off guard by Pecora’s proof of Morgan’s secret “preferred clients lists” of politicians whom the banker owned and who received stock offerings at discount rates. Named among the thousands of traitors on this list, Pecora revealed former president Calvin Coolidge, Coolidge’s Treasury Secretary Andrew Mellon (a Schacht-Hitler supporter from the start), financier Bernard Baruch, Supreme Court Justice Owen Roberts and Democratic Party controller John Jacob Raskob. Raskob was not only a major speculator but was also the leader of the American Liberty League which tried repeatedly to overthrow FDR between 1933-1939 and worked to ally America with axis powers from 1939-1941.

Morgan’s god-like ego was brought down to the level of mortals when the flustered banker was only able to answer “I can’t remember” repeatedly when asked if he had paid taxes over the past 5 years. As it turned out, by the end of the trial, it was revealed that NONE of the subsidiaries of the House of Morgan paid any taxes during the entire period of the depression, and were caught gambling with depositors assets from commercial accounts. These revelations didn’t sit well with a population dying of starvation across the streets of America.

Similar displays of corruption were made of the heads of Kohn Loeb, Chase Bank, Brown Brothers Harriman and others.

Faced with these revelations, The Nation magazine famously reported“If you steel $25, you’re a thief. If you steal $250 000, you’re an embezzler. If you steal $2.5 million, you’re a financier.”

Pecora’s ally Sen. Burton Wheeler said “the best way to restore confidence in our banks is to take these crooked presidents out of the banks and treat them the same as we treated Al Capone.”

FDR Drains the Swamp

With the light cast firmly upon the dark shadows where vile creatures like J.P. Morgan and other financial gremlins reside, the population was finally able to start making sense of what injustices befell them during the years of post-1929 despair. While not every banker went to prison as Wheeler or Pecora would have liked, examples were made of dozens who did and many more whose careers were shamefully ended. Most importantly however, this exposure gave Franklin Roosevelt the support needed to drain the swamp and impose sweeping reforms upon the banks.

In the first hundred days, FDR was able to:

1) Impose Glass-Steagall banking separation (forcing Wall Street banks to break up their functions and preventing speculators from gambling with productive assets)

2) Create the Federal Deposit Insurance Corporation (FDIC) that protected citizens’ savings from future crises

3) Create the Securities Exchange Commission to provide oversight to Wall Street’s activities and on whose body Pecora was appointed commissioner in 1934.

4) Unleash broad credit through the Reconstruction Finance Corporation (RFC) which acted as a national bank bypassing the private Federal Reserve, channeling $33 billion to the real economy by 1945 (more than all private commercial banks combined)

5) Impose protective tariffs on agriculture, metals and industrial goods to stop dumping of cheap products in America and rebuild America’s physical economy

6) Create vast public works, like the Tennessee Valley Authority, Grand Coulee dams, Hoover dams, St Laurence development and countless other projects, hospitals, schools, bridges, roads and rail under the New Deal that acted in many ways then as China’s Belt and Road Initiative has in our modern age. Unfortunately, Roosevelt died before this new form of political economy could be internationalized abroad in the post-war years as an anti-colonial program.

Ferdinand Pecora’s Commission shaped the dynamics of America so intensely by its simple power of speaking the truth, that efforts to run a fascist coup against FDR using a general named Smedley Butler also came undone before it could succeed. Butler played along with Wall Street’s plans for some months before deciding to publicly blow the whistle in congress. Butler exposed the intension to use him as a “puppet dictator” leading thousands of American legionnaires in a storming of the White House displacing FDR.

It is often forgotten today, but in the early days of the 1920s-1930s, the Legion was modeled on Mussolini’s fascist squadristi and even its leader Alvin Owsley made explicit in 1921 saying:

“If need be the American Legion is ready to protect the institutions of this country and its ideals, in the same way as the Fascists have treated the destructive forces threatening Italy. Don’t forget that the Fascists are for today’s Italy what the American Legion is for the United States.”

Butler’s startling revelations amplified FDR’s popular support and inoculated much of the population from the fake news pouring out of Wall Street propaganda agencies spread across the media.

“Under the surface of the governmental regulation of the securities market, the same forces that produced the riotous speculative excesses of the ‘wild bull market’ of 1929 still give evidence of their existence and influence. Though repressed for the present, it cannot be doubted that, given a suitable opportunity, they would spring back to their pernicious activity.”

Pecora went onto deliver one more warning which current generations should take seriously“Had there been full disclosure of what has been done in furtherance of these schemes, they could not long have survived the fierce light of publicity and criticism. Legal chicanery and pitch darkness were the bankers’ stoutest allies.”

Today’s oncoming economic meltdown can only be prevented if the lessons of 1933 are taken seriously and patriots who actually care about their nations and people stop legitimizing the casino economy of fictitious capital, derivatives, debt slavery and anti-humanism that has become so commonplace across the governing strata of the technocratic and banking elite today trying to control the world. This elite, just like the financiers of the 1920s, doesn’t care ultimately for money as an end but sees it merely as a means for imposing fascist forms of governance onto the world population. In the same way that FDR’s Wall Street/London enemies sought a world government under Nazi enforcers then, today’s heirs to that anti-human legacy are driven by a religious-like commitment to “manage” a new collapse of world civilization under a Green New Deal and World Government.

So why accept that dystopic future when a brighter one is offered us by the Multipolar alliance today led by Russia and China?

100 Iranians Die By Alcohol Poisoning After Ethanol Consumption For Virus “Cure”

As the world grapples with this once in a century pandemic, bizarre stories and sometimes extremely dangerous examples of people’s ‘home remedy’ attempts at combating the virus are popping up more and more.

Yesterday we detailed the story of the South Korean church which infected 46 people by the strange “remedy” of spraying salt water into their mouths thinking it would “kill” the virus; however, they used the same spray bottle, not bothering to disinfect it.

And now a new one from hard-hit Iran, which Tuesday saw state TV issue an alarming prediction that “millions” of its citizens could die: some Iranians areturning to ingesting industrial-grade ethanol and methanol thinking this can disinfect them and mitigate exposure.This has led to mass alcohol poisoning, state media has reported.

Methyl Alcohol file image

“More than a hundred Iranians have died from alcohol poisoning in recent weeks in the mistaken belief that industrial-grade ethanol and methanol will help ward off the coronavirus ravaging the country, according to local media reports,” writes Bloomberg.

The reports note that nationwide over 1,000 have been treated for alcohol poisoning related to ‘home remedy’ attempts to disinfect themselves. The ‘treatment’ reportedlybegan as a rumor, which authorities have lately sought to combat.

And the semi-official Iranian Students News Agency has reported 61 deaths in Fars province alone by this method, which adds up to five times more fatalities than official confirmed coronavirus deaths in that area.

Other deaths from consumption of the potentially fatal substances were also reported throughout the country. Bloomberg tallies it at 100 or more, citing state sources.

Iran on Wednesday reported a huge single-day jump in fatalities, reportedly the biggest within a single 24-hour period thus far in the country as another 147 people died.

This brings the official death toll in Iran to 1,135 and a total of 17,361 confirmed cases, amid dire reports that “millions” are expected to be infected before the pandemic dissipates.

Markets are just beginning to latch on to the economic consequences of the coronavirus. Central banks are slashing interest rates and beginning to throw new money into the mix and governments are increasing deficit spending.

Few analysts have yet to understand the enormous consequences of the coronavirus for missed payments and accumulating current debt, which is and will rapidly drain liquidity from wholesale money markets. It is increasingly certain that the eurozone’s banking system will require rescuing from insolvency with knock-on consequences for the global monetary system. Concern over the consequences for the $640 trillion OTC notional derivative market, particularly for $26 trillion of fx swaps, is so far absent.

Continuing on our theme that the fates of the dollar and US Treasury values are closely bound, the extraordinary overvaluation of the bond market will translate into a collapse for both. This article charts how the collapse of the dollar and financial asset values is likely to progress and concludes that we are witnessing the end of the neo-Keynesian fiat currency fantasy, which will be done and dusted with surprising rapidity.

Only then will sound money, after varying time periods for different nations, return.

Setting the scene…

This week we got into the red meat of Scene One of the final Act of the financial tragedy currently staged in global markets. It is a drama that has run on the air of hope for a hundred years, with an ending that now appears to be unexpectedly sudden. We face no less than the destruction of a financial system whose twin pillars are fiat currencies and financial assets, built on the sands of monetary expansion and debt financing. The evidence of its commencement is best encapsulated in Figure 1, of the world’s reserve currency. This is where everyone was meant to seek sanctuary from lesser currencies, in order to have the liquidity to pay the coupons on their dollar debts.

It is turning out not to be so, with the dollar suddenly appearing to enter a new bear market. Meanwhile, this week saw the entire US Treasury yield curve briefly submerged under 1%, an event bifurcated from the collapsing dollar.

There is no doubt that the coronavirus is having a serious economic impact. Much has been written about the disruption of supply chains, and clearly people are staying at home and stockpiling necessities. Sales of automobiles and other durable goods have crashed. Now the politicians are falling ill. Investors have reacted by dumping equities and buying government bonds, a flight to safety by Keynesian investment managers seeking the comfort of Nurse for fear of something worse. Consequently, government bond prices have become even more detached from the true reality of where financial risk resides.

Amazingly, almost no investment manager has bought physical gold for his or her clients: gold-backed ETFs and derivatives are only paper claims on gold, so by having counterparty risk and the lack of true possession don’t count as true safety. Physical gold has been effectively banned from managed portfolios, being classified as unregulated, deterring investment managers from having to justify buying gold to their compliance officers. The related asset class is so downgraded that gold and silver mining shares remain unfashionable, with the Amex gold bugs index (HUI) standing at about one third of its 2011 peak while the gold price is in new high ground against nearly all fiat currencies.

Monetary debasement will really accelerate from here…

Monetary and market distortions could have persisted for longer if it were not for the fact that the coronavirus disruption is accompanied by considerable payment dislocation. Companies still have fixed costs when they have no sales, either because customers are not turning up or their supply chains have stopped delivering products. Where companies have cash at their banks, they will draw it down, forcing their banks to go into the money markets, either through LIBOR or repos to make up the balance, sell government bonds, or foreclose on borrowers. Where companies do not have cash, they will test their working capital facilities, likely to force their banks to cover increased lending in wholesale money markets. Where banks experience drawdowns on both sides of their balance sheets, outstanding bank credit contracts, sending the sort of signal that terrifies central bankers.

The situation will be increasingly reflected by central banks having to back-stop both liquidity and bank reserves through repos and new rounds of quantitative easing. In an interesting paper, Zoltan Pozsar of Credit Suisse describes the process that leads to what he terms deficit agents in supply chains (businesses experiencing payment failures) turning their banks into deficit agents as well.

Pozsar demonstrates that a reluctant Fed will have to backstop not just escalating domestic dollar deficits but global ones as well, and he assumes for the purpose of clarity that foreign central banks will manage the payment crises in their own currencies. Being a money market technician, he does not address the debasement issue because that is not his brief. But clearly, he describes a process where the dollar will have to be debased if financial asset values, particularly of government bonds, are to be maintained.

We see unfolding the process whereby both the dollar and financial assets are losing value, with the dollar losing it first. And while a weakening dollar may from time to time lend support to financial asset prices, measured in sound money their combined values will decline.

The second scene in the final act of our financial tragedy will be wholesale liquidation of US Treasury holdings by banks in New York and also by foreign governments to obtain dollars to satisfy their liquidity demands. The Fed will have to supply as much liquidity as it takes to accommodate the American banks and will reduce the Fed funds rate to discourage them from selling Treasury bills and bonds. As for foreigners, they are not the Fed’s first priority.

Let us assume liquidity problems should not become acute for the few foreign central banks with existing USD liquidity swap lines with the Fed. Under the existing 2013 agreement, these are only the ECB, Bank of England, Swiss National Bank, Bank of Canada and Bank of Japan. While additional temporary swap agreements might be arranged with others, it is only likely to happen in a response to liquidity stresses rather than in anticipation.

China, Korea and Taiwan as well as other nations with dollar-centric supply chains in their domains will probably have to unwind their long-dollar fx swap positions and sell T-bills and Treasuries in order to release the necessary liquidity. The end result is that in funding the US deficit, the Fed will have to not only absorb significant new debt through quantitative easing, but it will have to buy up existing debt sold by foreign holders if it is to maintain US Treasury yields at anything like current levels.

In this, mainstream opinion has been wrongfooted: foreigners certainly have dollar obligations to satisfy in an economic slump, but they already own the dollars. The thirst of foreigners for dollar liquidity will not be satisfied by the purchase of more dollars, but by the liquidation of their existing dollar assets. And to the extent that this leads to a contraction in bank credit the Fed will have no alternative but to sacrifice the dollar by increasing the base money quantity in order to absorb it all.

Furthermore, there is an unknown quantity of fx swaps taken out by US hedge funds to strip out interest rate differentials between euros and yen on one side, and the dollar on the other. It is a trade that will have built in quantity but deteriorating in quality since April 2018, when it first became clear to American based investors and speculators that the euro and yen were seemingly stuck with negative interest rates in perpetuity, while the Trump stimulus would likely lead to higher dollar rates. Now that the Fed is closing down the rate differential by cutting its funds rate these arbitrages need to be unwound, leading to substantial liquidation of T-bills, USTs and dollars to repay obligations in euros and yen. No wonder the chart of the dollar’s trade weighted index is so bearish.

Hopefully, the hedge fund problem will not replicate the crisis in September 1998, when the Long-Term Capital Management hedge fund failed. But even if that risk is contained, there will be a significant contraction of outstanding bank credit in dollar markets. Being sold on Irving Fisher’s description of how contracting bank credit led to the 1930s depression, the Fed is likely to respond by turning its liquidity taps full on.

The fiscal position is not good either. The current year US budget deficit, estimated by the CBO to be over a trillion dollars, will begin to look like running at an annualised rate of nearly twice that. The Fed could also find itself monetising not only the bulk of new Treasury flows but absorbing sales by foreigners of UST bonds, T-bills and agency debt as well. If so, it will end up increasing its balance sheet by many trillions, unless, that is, the Fed adjusts its priorities to protect the dollar. But the cost of doing so would be the inevitable destruction of US Government finances when the Fed refuses to monetise its debt. That simply won’t happen.

The sacrifice of the dollar as the Fed inevitably fails to maintain financial asset values will truly mark the end of the fiat currency era, since no other fiat currency can exist with the world’s reserve currency thoroughly debased and its financial assets in a state of collapse. This is a simple statement with complex issues behind it, including but not limited to the following:

The valuations placed on government bonds are so divorced from economic reality that after the initial shock in equity markets has passed, they will be exposed to a seismic downwards adjustment in prices.

Corporate bond markets will face an even greater collapse as risk premiums widen, leading to a spate of bankruptcies in the private sector and losses on collateralised loan obligations held by the banks on a systemically threatening scale.

Hedge funds which have taken out fx swaps have already lost the interest rate arbitrage opportunity following the Fed’s recent cut in the funds rate. Furthermore, with T-bills yielding only 0.37%, further cuts in the funds rate are a racing certainty. Unwinding these fx swaps is one factor that will put significant downward pressure on the dollar.

A reduction in outstanding derivatives will be the consequence of banks desperate to free up liquidity for their own balance sheets. The cost of hedging risk will increase significantly and in many instances become unavailable. Hedge funds and the like will be forced to restrict their activities, raising the possibility of widespread losses and potential failures in financial asset markets.

A glance at their share prices confirms that major European banks are already in trouble and they have long been at severe risk of failure, a fact which has been concealed by the ECB’s provision of liquidity. If nothing else, a new escalation of non-performing loans brought about by the coronavirus now threatens to collapse Italian, French, German, Spanish and other eurozone nations’ commercial banks despite the ECB’s efforts. A coordinated G-20 global bank rescue scheme involving open-ended monetary expansion by central banks is likely to be instigated in a widespread act of currency inflation.

A general liquidation of foreign-owned dollar assets and selling of dollars is likely to follow.

Only then will the wider public begin to realise the full faith and credit in their governments and currencies which they take for granted are worthless.

The confluence of these threats to financial assets and the world’s reserve currency makes it almost certain that this time attempts to rescue the world from another financial crisis will fail. The twin pillars in the Keynesian endgame, whereby the future of financial assets has become tightly bound to the purchasing power of currencies, will both be destroyed by market forces acting like Sampson pushing the pillars apart until the temple’s collapse killed all the Philistines.

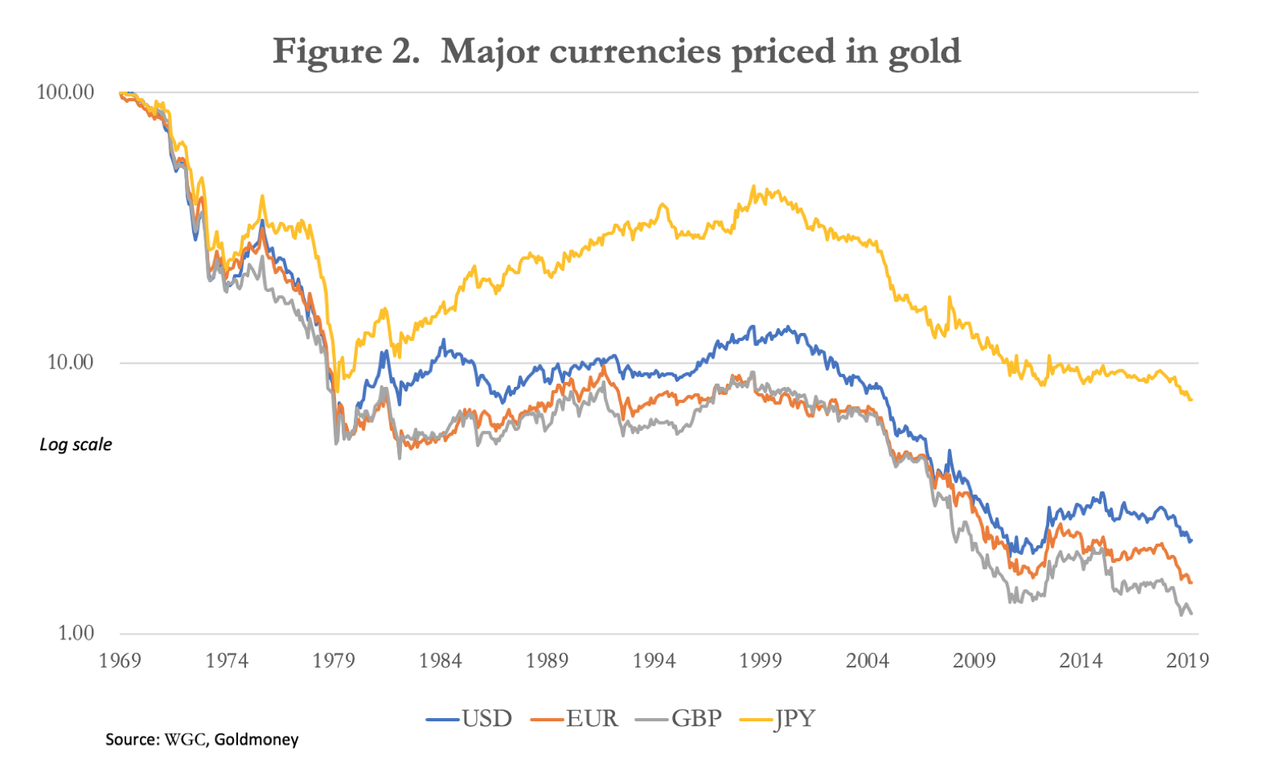

Comparing fiat to sound money

Figure 2 shows that since the gold pool failed in the late 1960s the four major currencies (including the euro’s components prior to 1999) have lost substantially all of their purchasing power, compared with that of gold. The most debased is sterling, which retains only 1.19% of its 1969 purchasing power, followed by the euro at 1.56%, the dollar at 2.22% and the yen at 7.4%.

The failure of the gold pool and the subsequent abandonment of the post-war Bretton Woods agreement was the last significant monetary failure. The first in modern times was the 1934 devaluation of the dollar from $20.67 to $35 per ounce of gold, thirty-five years before. On this timeline the next failure appears to be overdue.

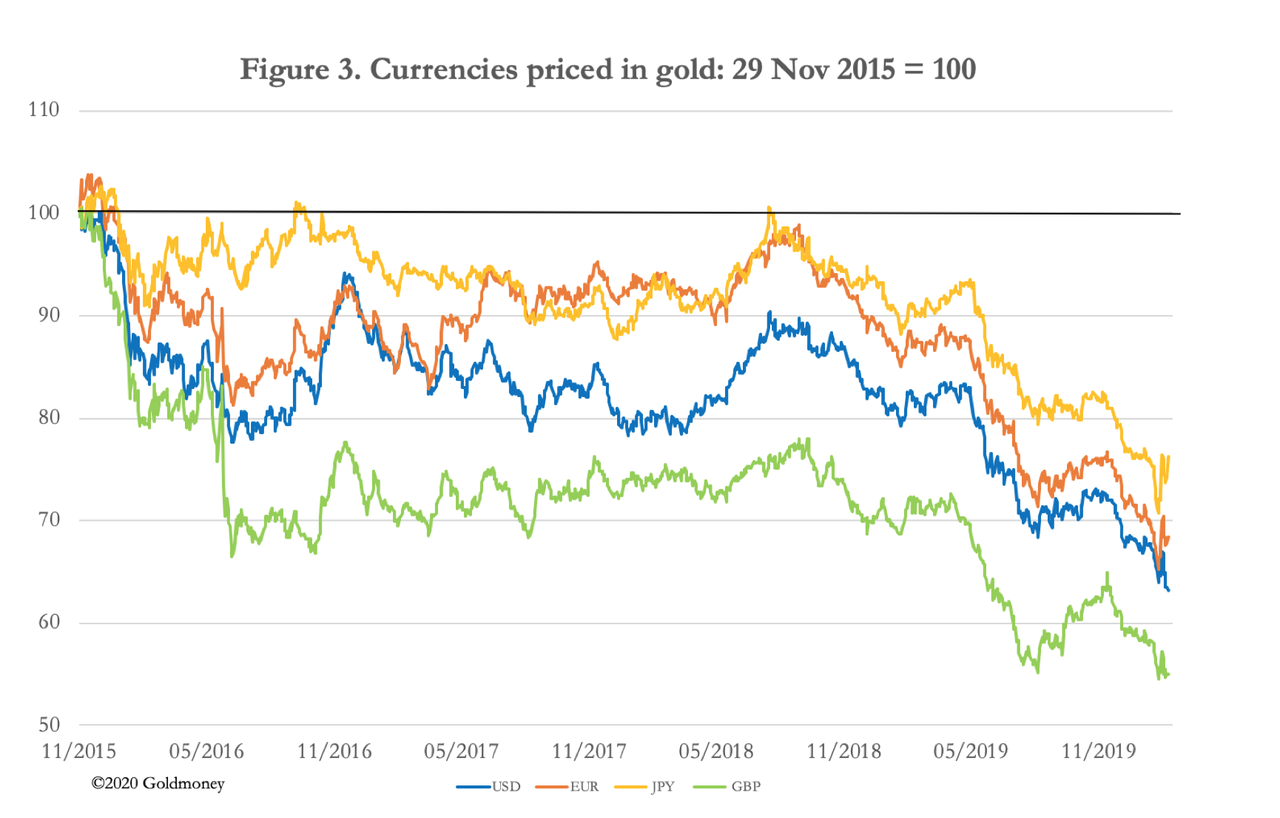

The current situation has the makings of leading into an even greater monetary event, as government spending spirals beyond control without the means to fund it, except by monetary inflation. It has already been anticipated by a renewal in the bear market in the major currencies measured in gold terms, dating from late-2015 and is illustrated in Figure 3.

These represent significant losses ahead of the currency debasement which is now becoming increasingly certain in the coming months. It is extraordinary that this marked devaluation of currencies has occurred with very few commentators noticing.

If we refer back to John Law’s Mississippi bubble, which is the best model for what is now unfolding, the loss of all purchasing power for his fiat currency happened in less than a year. Law’s livre began the final phase of its decline in November or December 1719 and by the following September there was no exchange rate against sterling, indicating it was worthless. From November 1719 Law accelerated his purchases of shares in his Mississippi venture ahead of its merger with his bank, the Banque Royale, paid for by issuing unbacked paper livres which began to noticeably undermine its purchasing power.

Sticking with Law’s failure as a template for ours today, we can similarly expect the Fed on behalf of the US Government to issue new money for the purpose of maintaining financial asset values, mainly of US Treasury bonds, but by extension of equity prices as well.

Following the current panic into perceived safety, a second phase will likely evolve, being driven by the collapse of government bond prices. Currently, they are over-valued on a combination of unrecognised price inflation, which based on independent estimates is probably closer to ten per cent than two, and a flight to perceived safety from other financial assets. That process will come to an end, and the condition of government finances, which ultimately depend upon the wealth and health of the productive economy, are bound to be reassessed in the light of the slump in business activity and a more realistic assessment of price inflation.

To sum up, the following developments are likely in the coming months in approximate order, with some running concurrently:

Base money will be increased substantially to offset a contraction in bank credit and to give banks extra liquidity to compensate for becoming deficit agents as supply chains dislocate and retail sales of non-essentials goods and services collapse. We have already seen daily repos by the Fed increasing from about $40bn in recent weeks to between $130bn to $200bn currently.

“Helicopter money” in various guises, such as deferral of tax payments and business rates to help provide liquidity, will shift to governments some of the deficits building up in businesses. Mortgage payment holidays are offered in some countries. Helicopter money is already being provided to investors through share support operations, such as the Bank of Japan’s purchases of ETFs, which is likely to be expanded. In Hong Kong, each citizen is being given HK$10,000.

Within a month or two there will almost certainly have to be bank bailouts in Europe, which will require additional monetary commitments by the ECB and the national central banks. This will likely lead in turn to widespread liquidation of euro commitments for speculation and arbitrage. Loans in the trillions have been taken out in euros as the counterpart in fx swaps to the dollar. As these positions are squared the euro will rise and the dollar will fall, transmitting a eurozone banking crisis into liquidation of UST-bills and short-term US Government coupon debt by US hedge funds. A heightened risk of counterparty failure in fx swaps could spread to other derivative markets, requiring bailouts of non-banks, including major hedge funds. Failure to do so or a bungled operation such as tinkering with mandated bail-ins could hasten the collapse of stocks and other financial assets.

A declining dollar will increase portfolio liquidation pressures on foreigners, leading to indiscriminate offerings of US Treasuries, agency debt and equities. The Fed will have to take on not only the financing of an increasing budget deficit, but also absorb foreign sales of dollar-denominated securities if it is to retain control of prices.

At this stage it will become increasingly obvious to domestic bank deposit holders that the dollar’s purchasing power is being destroyed by the Fed’s escalating asset support commitments. In effect, the Fed will be the only significant buyer of financial assets, paid for through quantitative easing on a far greater scale than that which followed the Lehman crisis.

In the absence of other buyers of US Treasuries and the loss of purchasing power for the dollar, bond prices will sink, which will make it virtually impossible for the US Treasury to fund a ballooning deficit. An election year creates extra difficulties leading to uncertain political outcomes. But by the time President Trump is due to stand for re-election, over a million elderly and poor Americans might have died from the coronavirus, socialist Democrats might be in the ascendant and the dollar could become worthless.

With the dollar as the world’s reserve currency and nearly all other fiat currencies having taken their cue from it since the Nixon shock in 1971, they also seem doomed to failure with the dollar.

Where will the money go?

In the three months before the collapse of his scheme, sellers of shares in his Mississippi venture required John Law to replace them with new buyers, and when they could not be found he substituted them by buying shares with new livres issued for the purpose. Today’s price support system which rigs government bond prices is exactly the same concept as that deployed by John Law, except it is on a global scale.

Law’s experience showed that in an asset and monetary collapse, apparent wealth simply vanishes, destroyed along with the medium of exchange. Theoretically, if there are no buyers at any price the collapse to zero is immediate and no one extracts any value to be redeployed elsewhere. The Mississippi bubble also showed that the purchasing power of sound money, always gold or silver, is at least retained. For this reason, it is more than likely a rising price for monetary gold will happen without very much gold needing to be purchased.

Being dominated by mathematical economists, current thinking in financial asset markets does not often admit to this. But as the central banks show increasing difficulty in maintaining the combined values of currency and bonds, the price of gold and silver in fiat currency terms will rise significantly. More correctly described, the ratios of fiat currencies to gold will fall, as illustrated in Figures 2 and 3 above.

Gold and silver are reliable money, chosen by the people as economic actors. The journey to their reinstatement will require the destruction of the unsound currency issued by the state, which is simply a distorting monopolist and therefore a distorter and destroyer of economic values. Only then can gold and silver re-emerge as circulating money, or more practically, reliable and trusted paper and electronic substitutes for them. Gold and silver are emblems of economic freedom, and while the transition will only be very reluctantly accepted by the state, a better monetary future will beckon.

It is in this light we should anticipate the money to replace dollars, euros, yen and pounds. In Asia they will be better placed than western nations to return to sound money, with Russia having substantially replaced its reserve dollars with gold, which could easily be legislated into a gold exchange standard for the rouble. China will be in a position to do the same for the yuan. In theory, getting to the point where monetary stability returns will be easier for some governments than for others. The capitalist nations, and China perhaps to a lesser extent, have subsumed Keynesian economics deep into their collective psyche, so deep that it has replaced entirely an understanding of free market economics.

Governments with extensive welfare obligations will find it an enormous challenge to maintain the balanced budgets required to ensure that a new monetary system will endure. They have been socialising wealth for too long to understand the simple fact that if you wish your nation to be prosperous you must allow the people to create and retain it. You must also make them responsible for their own affairs and make it clear to them that no one individual, lobbyist or interest has a right to government intervention. The function of government must be limited to making and administering criminal and contract law and protecting the realm, with strictly limited welfare provision.

A government that works in a sound money environment absorbs and administers only a minor part of its national economy. The loss of political power is always widely resisted, but the redeployment of national resources from a wealth-destroying state to free-market production has been shown to produce remarkable benefits in surprisingly little time. If, that is, the political class is wisely led by statesmen not in thrall to the common economic fallacies of John Maynard Keynes and John Law.

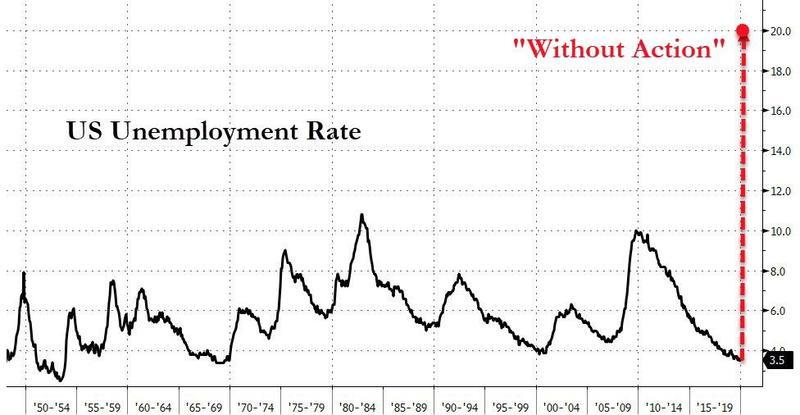

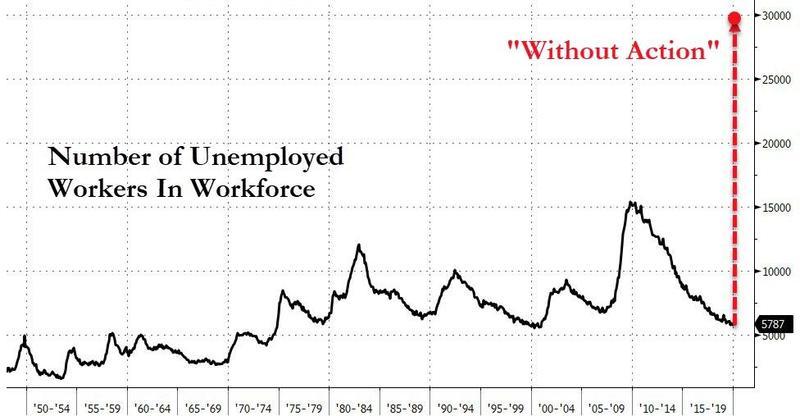

Nearly 20% Of Households Have Already Lost Work Due To Pandemic-Shutdowns

The arrival of helicopter money in the form of two $1,000 checks to most Americans is the government’s acknowledgment that the economy crashed, and upwards of 30 million people could be unemployed due to the Covid-19 outbreak shutting down cities and towns across America.

A new NPR/PBS NewsHour/Marist poll has shown that 1 in 5 households have already experienced a layoff or reduction in work hours thanks to social distancing measures enforced by the government that is grinding local economies to a halt.

People across the country are staying home, avoiding large crowds, and ordering food on Amazon, as the fast-spreading virus is rapidly infecting people in New York, Washington state, and California. Confirmed cases have now been recorded in all 50 states.

The federal government missed containment windows to implement social distancing policies by nearly a month, and this means cases are likely to be exponential in the days or weeks ahead. Deaths have stayed low at this point because ICU treatment capacity at major hospitals has yet to be overwhelmed, but when they do, America could be the next Italy.

Bill Gates said on Wednesday that virus shutdowns could last upwards of ten weeks. The most affected industries have so far been restaurants, bars, hotels, casinos, cruise ships, and airlines, but as we noted last week, the ripple effect has collapsed the entire gig and service economy.

The poll was conducted on March 13-14, shows layoffs and reduced hours had already hit 18% of households. Lower-income households were hit the hardest, at least a quarter of them were making $50,000 per year had the most hours cut or experienced the most significant amount of job losses. It also showed a third of households had at least one person who had a significant change in work routine associated with the virus impact. College students were the most susceptible to job disruption.

Most of the jobs that experienced reduced hours or have been entirely cut have been blue-collar and service or retail jobs, which cannot be conducted remotely.

We noted last week that the virus crisis was expected to crash the gig and service economy. With more than 50 million Americans, or about 44% of all US workers, aged 18-64, are considered low-wage and low-skilled, have insurmountable debts (with limited savings), including auto, student, and credit card debts, are working in the gig-economy via side hustles and are most vulnerable to job losses as Covid-19 has likely triggered the next recession.

What’s about to happen next could be absolutely terrifying, as Treasury Secretary Steve Mnuchin warned the US unemployment rate could spike to a stunning 20% without stimulus directed at businesses and households.

With a total labor force of around 160 million, this would mean virus-related impacts on the gig and service economy could lead to a sudden spike to over 30 million unemployed without policy action.

Those are depression-era levels of job losses… which is prompting the Trump administration to resort to helicopter money.

Maybe the real reason why the National Guard is being deployed across the country is the possibility that a Covid-19 pandemic could lead to social destabilization as millions lose their jobs and supermarkets run out of food. Who would’ve thought America is transforming into the next Venezuela?

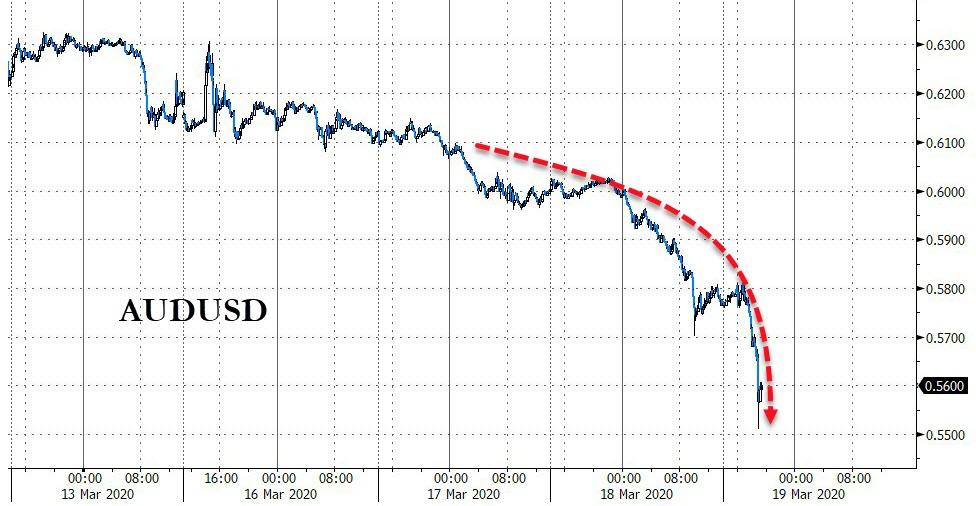

Global Dollar Buying Panic Sparks AsiaPac FX Collapse, US Equity Futures Crash

The global scramble for dollars amid a massive shortage has rolled around the AsiaPac time-zone and is leaving a bloody trail across every asset-class.

FX is in freefall with Aussie collapsing at the fastest rate since Lehman…

Source: Bloomberg

Kiwi is back to its weakest since 2009…

Source: Bloomberg

Yen is tumbling once again…

Source: Bloomberg

Won is getting whacked…

Source: Bloomberg

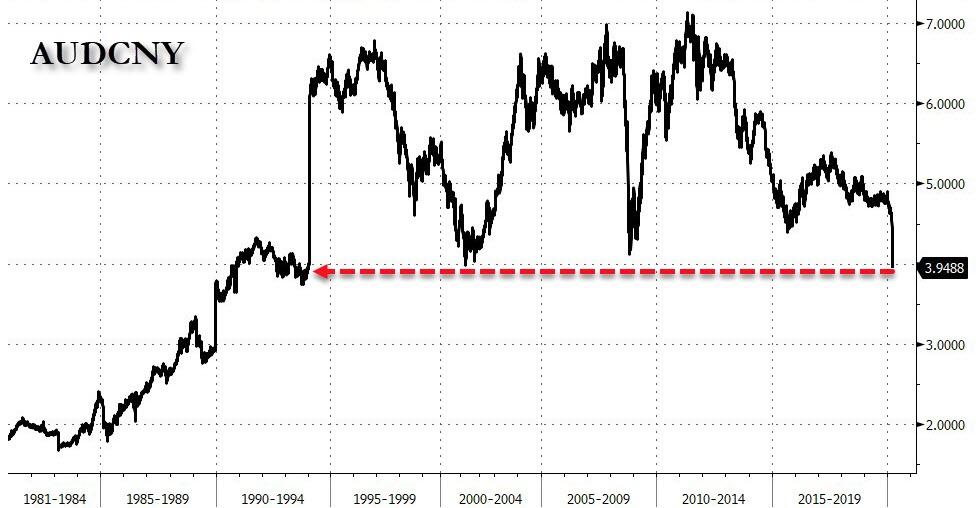

And Aussie has crashed to its weakest against the offshore yuan ever and weakest against onshore yuan since Dec 1993…

Source: Bloomberg

And overall, AsiaPac FX is crashing to its weakest against the USDollar since 2004…

Source: Bloomberg

And the liquidation continues in US equity markets with Dow futures down over 800 points, erasing the after ramp in stocks…

And losses in AsiaPac stocks are accelerating…down 27% from January highs

Source: Bloomberg

And JPY Basis-Swaps are signaling extreme dollar shortage continues…

Source: Bloomberg

This all has the smell of a massive global macro fund liquidation and the contagious impact of that leveraged unwind across the global risk markets.

As Bloomberg’s Stephen Spratt details, desks continue to speak of the “sell everything” mentality in markets with huge liquidations and de-leveraging taking place everywhere.

The data stacks up. Looking at the three-day change in open interest across major June bond futures as of close of play Tuesday, the reduction in positions is the equivalent to $150 billion in 10-year cash Treasury bonds ($140m/dv01*). Here’s 3-day open interest change:

Schatz: -135,295

Bobl: -45,931

Bund: -178,221

Buxl: -17,566

OATs: -41,475

BTPs: -41,176

Gilts: -28,055

US 2y: -158,991

US 5y: -44,059

US 10y: -129,381

US 20y: -60,865

US 30y: -26,798

JGBs: -36,534

As one veteran Aussie trader exclaimed (who happened to be on the right side of the collapse in the currency):

“I love the smell of global macro fund liquidations in the morning…”

With currencies flash crashing across Asia on Thursday, central bankers may be looking back at the remedies used then.

As Bloomberg’s Mike Wilson suggests, the tear the U.S. dollar was on back in 1985 was brought to an end when five central banks gathered in New York’s Plaza Hotel and came up with what became known as The Plaza Accord.

Source: Bloomberg

That sent the dollar into a steep slide that lasted until about the end of 1987.

With the Aussie, kiwi and won just free-falling, it looks like a similar sort of coordinated intervention may be needed to stop the dollar now, especially until the world is deemed free of coronavirus impacts.

{kind=link}