DOJ Orders First Shutdown Of Website Selling Fraudulent COVID-19 Cure

The US Department of Justice (DOJ) announced on Sunday that “it has taken its first action in federal court to combat fraud related to the coronavirus (COVID-19) pandemic” via the shutdown of a website offering a cure.

Detailed in the civil complaint filed on Saturday, the operators of the website “coronavirusmedicalkit.com,” which claimed to sell vaccine kits for COVID-19, were engaged in a “wire fraud scheme seeking to profit from the confusion and widespread fear surrounding” the virus crisis.

“Information published on the website claimed to offer consumers access to World Health Organization (WHO) vaccine kits in exchange for a shipping charge of $4.95, which consumers would pay by entering their credit card information on the website. In fact, there are currently no legitimate COVID-19 vaccines and the WHO is not distributing any such vaccine,” the DOJ said.

US District Judge Robert Pitman ordered the site to shut down on Saturday, according to his statement. As of Monday morning, a search of the site comes up with a blank webpage with a text that reads: “Sorry… coronavirusmedicalkit.com could not be found.”

Assistant Attorney General Jody Hunt of the DOJ’s Civil Division said the government will be actively monitoring the internet for other COVID-19 fraud-related websites or schemes:

“The Department of Justice will not tolerate criminal exploitation of this national emergency for personal gain,” said Hunt. “We will use every resource at the government’s disposal to act quickly to shut down these most despicable of scammers, whether they are defrauding consumers, committing identity theft, or delivering malware.”

“Attorney General Barr has directed the department to prioritize fraud schemes arising out of the coronavirus emergency,” said US Attorney John F. Bash of the Western District of Texas.

“We therefore moved very quickly to shut down this scam. We hope in the future that responsible web domain registrars will quickly and effectively shut down websites designed to facilitate these scams. My office will continue to be aggressive in targeting these sorts of despicable frauds for the duration of this emergency.”

“At a time when we face such unprecedented challenges with the COVID-19 crisis, Americans are understandably desperate to find solutions to keep their families safe and healthy,” said Special Agent in Charge Christopher Combs of the FBI’s San Antonio Field Office.

“Fraudsters who seek to profit from their fear and uncertainty, by selling bogus vaccines or cures, not only steal limited resources from our communities, they pose an even greater danger by spreading misinformation and creating confusion. During this difficult time, protecting our communities from these reprehensible fraud schemes will remain one of the FBI’s highest priorities.”

The DOJ provided very few details about the scope of the fraud but said an investigation is ongoing.

The intervention by the DOJ comes after New York Attorney General Letitia James sent a cease-and-desist order to televangelist Jim Bakker, ordering him to stop promoting an alleged cure for the virus.

James has also ordered Alex Jones to stop making misleading claims about virus cure related products offered on Infowars.com.

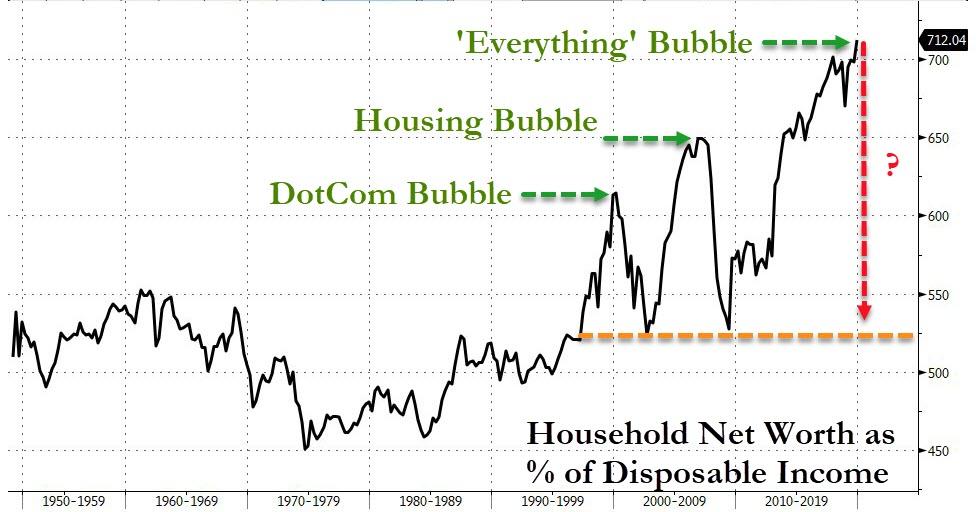

The years since the 1970s are unprecedented in terms of their volatility in the price of commodities, currencies, real estate and stocks. There have been 4 waves of financial crises: a large number of banks in three, four or more countries collapsed at about the same time. Each wave was followed by a recession, and the economic slowdown which began in 2008 was the most severe and most global since the great depression of the 1930s.”

Manias, Crashes and Panics – Kindelberger and Aliber

Interestingly enough 1971 was the year when Nixon took the world off the gold standard, which had been in effect since 1944. Fiat-bugs please note.

More to the point, however. Booms and busts have always been normal in a capitalist economy. But in recent years this has been a feature which has been exacerbated by and involves that part of the economy indicated by the acronym FIRE (Finance, Insurance and Real Estate) and its growing importance in the economy in both qualitative and quantitative terms.

Financialisation is a process whereby financial markets, financial institutions, and financial elites gain greater influence over economic policy and economic outcomes. Financialisation transforms the functioning of economic systems at both the macro and micro levels. Its principal impacts are to:

elevate the significance of the financial rent-seeking sector relative to the real value-producing sector

transfer income from the real value-producing sector to the financial sector

increase income inequality and contribute to wage stagnation

Since 1970 this part of the economy has grown from almost nothing to 8% of US Gross Domestic Product (GDP). This means that one dollar in every ten is associated with finance. In terms of corporate profits finance’s contribution now represents around 40% of all corporate profits in the US. This is a significant figure and, moreover it does not include those overseas earnings of companies whose profits are repatriated to their countries of origin.

Thus, the increasing presence and role of finance in overall economic activity and the increase of profits channelled to the financial sector represent the salient indicators as to what has been termed financialization. It is argued by some that financialization may put the economy at risk of debt deflation and prolonged recession.

Financialisation operates through three different conduits:

changes in the structure and operation of financial markets,

changes in the behaviour of nonfinancial corporations, and

changes in economic policy.

Countering financialisation calls for a multifaceted agenda that:

restores policy control over financial markets

challenges the neoliberal economic policy paradigm encouraged by financialisation

makes corporations responsive to interests of stakeholders other than just financial markets

reforms the political process so as to diminish the influence of corporations and wealthy elites

The rent-seeking nature of finance is common to all forms of insurance, banking, monopolistic pricing, and property. This has not always been the case, or at least wasn’t as pronounced as it is at present. There was a time when the banking system was junior partner in the relationship between banks and industry. Banks provided industry with loans for investment with a view to maximising profit for both. This is patently not the case today.

Generally speaking, banks will lend for property purchases, stock buy-backs, and perhaps loans for dubious mergers and acquisitions. Moreover, when we speak of ‘profits’ this has now assumed a rather obscure meaning. Profits were generally understood as a realization of surplus value.

Firms made stuff – goods and services – which had a value, which was then sold on the market at a profit. Given the competitive nature of the system, firms invested in increased capital formation and output which increased productivity, surplus value and ultimately profit.

With regard to Investment banks like Goldman Sachs and the commercial banks they do not create value; they are purely rent-extractive. For example, commercial banks make a loan out of thin air, debit this loan to the would-be mortgagee who then becomes a source of permanent income flow to the bank for the next 25 years.

Goldman Sachs makes year-on-year ‘profits’ by doing – what exactly? Nothing particularly useful. But then Goldman Sachs is part of the cabal of central banks and Treasury departments around the world. It is not unusual to see the interchange of the movers and shakers of the financial world who oscillate between these institutions. Hank Paulson, Mario Draghi, Steve Mnuchin, Robert Rubin … on and on it goes.

This financialised system now moves in ever-increasing levels of instability. But what did we expect when the whole institutional structure – its rules, regulations and practises – were deregulated and finance was let off the leash.

Thatcher, Reagan, the ‘Big Bang’ had set the scene and there was no going back: neoliberalism and globalization had become the norm. From this point on, however, there followed a litany of crises mostly in the developing world but these disturbances were in due course to move into the developed world. Serial bubbles began to appear.

US stock prices [which of course would only ever go up] began to decline in the Spring of 2000, and fell by 40% in the next three years. Whilst the prices of NASDAQ stocks decline by 80%.”

Manias, Panics and Crashes – Kindleberger and Aliber

Chastened monies moved out of this market and into property speculation. It is common knowledge what happened next. The run-up to 2008 was floated on a sea of cheap credit. The price of stocks pushed property prices to vertiginous heights until – pop, went the weasel.

The reason was quite simple. Any boom and bust has an inflexion point where boom turns to bust. This is when buyers incomes, and borrowers inability to extend their loans could no longer support the rise in the price level. Euphoria turned to panic as borrowers who once clamoured to buy were now desperate to sell. 2008 had arrived.

The strange thing, however, regarding the property price boom-and-bust was that it was based upon pure speculation. Prices went up, prices went down. Some – a few – made money, quite a few lost money. Investors were wondering what had happened to their gains which they had made during the up phase. Where had all that money gone?

The short answer is – nowhere. It was never there in the first place. It was fictitious capital. Gains which had appeared and then disappeared like a will ‘o’ the wisp. As opposed to physical capital – machinery, labour and raw materials, and money capital which enabled through purchase the production of value to take place, we have fictitious capital which is a claim on future production. If my house goes up by 10% that is a capital gain, if everybody’s house goes up by 10% that is asset-price inflation

Fictitious capital is a by-product of capitalist accumulation. It is a concept used by Karl Marx in his critique of political economy. It is introduced in chapter 25 of the third volume of Capital. Fictitious capital contrasts with what Marx calls “real capital”, which is capital actually invested in physical means of production and workers, and “money capital”, which is actual funds being held.

The market value of fictitious capital assets (such as stocks and securities) varies according to the expected return or yield of those assets in the future, which Marx felt was only indirectly related to the growth of real production. Effectively, fictitious capital represents “accumulated claims, legal titles, to future production’’ and more specifically claims to the income generated by that production.

The moral of the story is that it is not possible to print wealth or value. Money in its paper representation of the real thing, e.g., gold, is not wealth it is a claim on wealth.

Of course, this would be lost on establishment economists, bankers, and financial journalists, whose view is that the policy should be QE, liquidity injections, and so forth. A one-trick pony.

And what has all of this to do with Coronavirus? Well, everything actually.

I take it that we all knew that the grotesquely overleveraged world economy was heading for a ‘correction’ but that’s a rather a soothing description. “Massive correction” would be a better description. That is the nature of the beast. The world was a bubble of paper money looking for a pin. It found one.

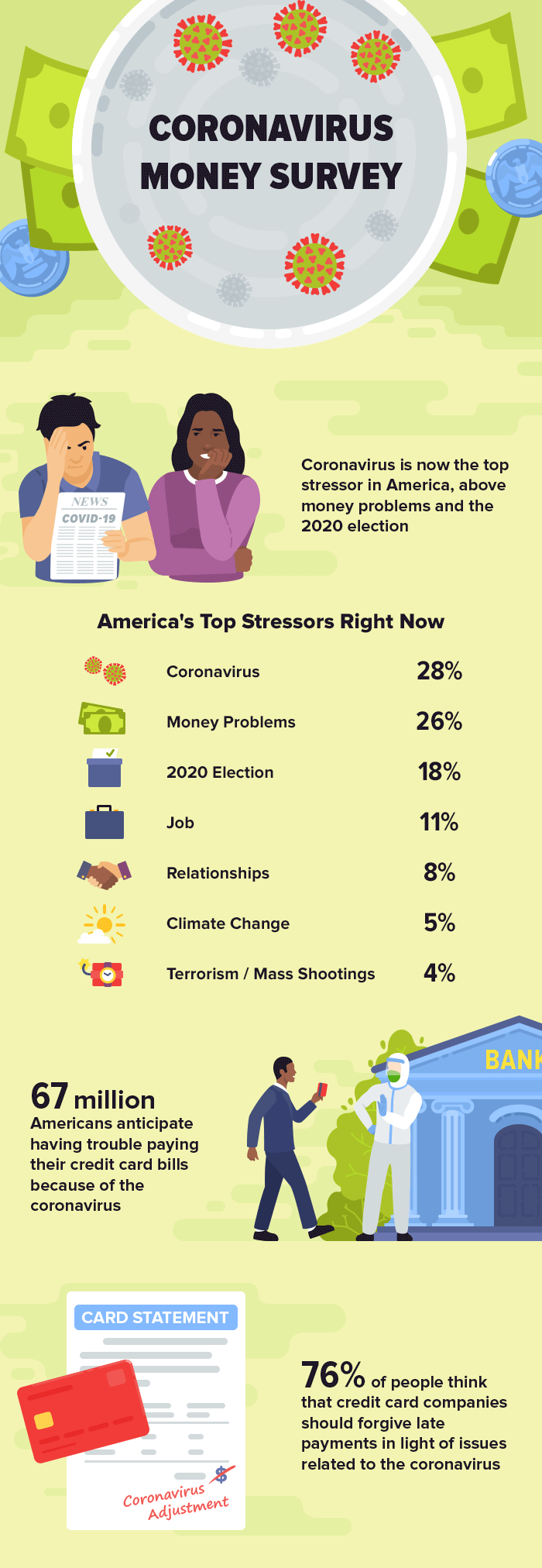

67 Million Americans Could Miss Their Credit Payments Thanks To Virus Crisis

As social gatherings are limited and businesses shutter operations to reduce the spread of COVID-19, millions of Americans could be laid off in the next couple of months as the economy dives into a depression.

Most of the job loss will be seen across both the services and manufacturing sectors. The National Restaurant Association estimates that five to seven million jobs could be lost in the next three months. While Treasury Secretary Steve Mnuchin said if government stimulus is not directed at businesses and households, upwards of 33 million jobs could be eliminated.

With a depression imminent, WalletHub anticipates 67 million Americans could have difficulty servicing their credit cards due to virus impacts. As we’ve routinely pointed out, credit card usage soared to a record high in December.

“Roughly 67 million Americans anticipate having trouble paying their credit card bills because of the coronavirus. Their struggles could easily ripple through the economy if left unaddressed, especially considering the more than $1 trillion in credit card debt currently owed by U.S. consumers,” said WalletHub CEO Odysseas Papadimitriou.

According to WalletHub’s survey completed on March 9-12, the virus is the most significant stressor among Americans. The second stressor is money problems, then the 2020 election, and people’s current job situation.

“We’ve seen a lot of panic buying as a result of the coronavirus, with people purchasing things like toilet paper en masse, largely because they don’t know what else to do. Furthermore, 94 million Americans have canceled or plan to cancel travel plans due to the coronavirus,” said WalletHub analyst Jill Gonzalez.

“Less apparent, however, is the panic saving that people are engaged in right now. Around 158 million Americans, or roughly 63% of adults, say they are saving more, as opposed to buying more, as a result of this crisis. If there’s a bright side to all of this, people saving more money than usual might just be it.”

Credit card companies have started rolling out relief programs to affected customers.

“Yes, credit card companies should give relief to affected customers, just like they’ve done during major natural disasters in recent years,” Papadimitriou said.

We wonder if the proposed stimulus checks for Americans, ranging from $1,000 to $2,000 per person, will be used for paying credit card bills or be used at Costco stores to buy toilet paper and milk?

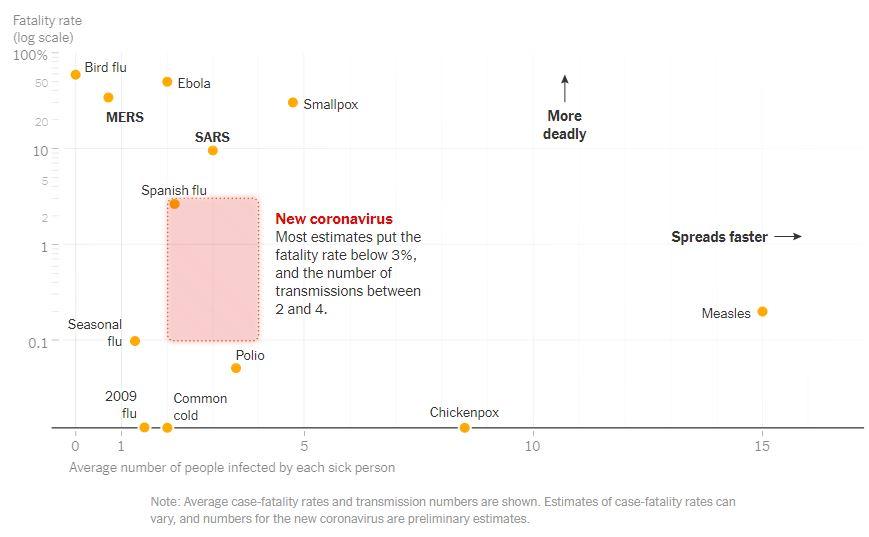

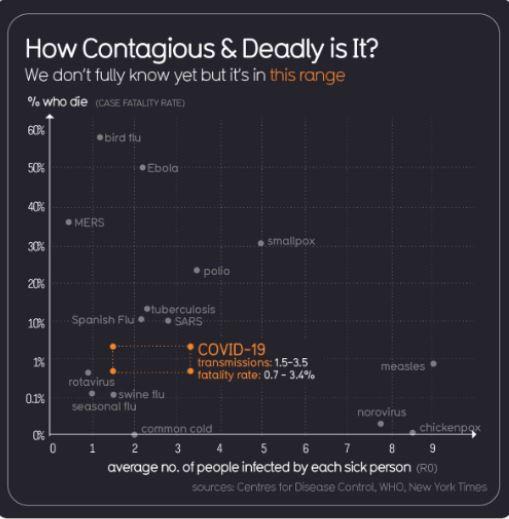

With hoops “out” and exponentials “in” (referring to March Madness, the 2020 pandemic definition), there’s a new, customary disclaimer on economics and financial sites. Mine says that I, too, knew nothing about infectious disease modeling only two months ago. But I’m catching up, just like everyone else. By now, I might have reached a “Dummies Guide” standard, and I’ll keep this article at about that level.

So with that preface out of the way, I’ll first offer a health warning of sorts about a type of COVID-19 chart that’s popular with market bulls. Here’s a version that appeared in the New York Times:

And here’s a second version that uses the same axes but with different data:

The second chart bounced around Twitter for awhile and then appeared on at least one financial site – to support a breezy message that people should stop panicking and start preparing for a surprise melt-up in stocks.

And why do the charts need a health warning? The problem is the horizontal axis—showing the statistic that epidemiologists call R0—which is presented as though it’s the only information you need to understand how widely a disease spreads.

In fact, modelers who actually use R0 stress that you can’t summarize the spread of an epidemic with that single input. They say that R0 changes with time and place—it’s not actually a constant. Also, it can approximate the spread of a disease only if the entire population is vulnerable. Critical factors such as prior immunities are handled through other model inputs, not R0.

More to the point, we already know how widely COVID-19 is spreading, and we can readily compare that information to every other disease that’s already come and gone. So let’s stop pretending that R0—an incomplete and imprecise contagion statistic—somehow does a better job than ripping off the blindfold and watching what’s really happening, in real time.

The reality-based approach tells us that SARS, to pick one comparable, peaked at about 8000 cases in 2003. By contrast, COVID-19 is rocketing through the hundreds of thousands, certain to hit millions and by some forecasts billions. That’s a stark difference that seems highly relevant, and yet you won’t find it on the R0 chart, no matter how many versions you conjure up.

The eyes-open approach also says to be wary of claims that “we’re very close to a melt-up” or “the bottom may be closer than you think” or “we’ve probably seen the worst.” (Those are just a few of the bullish stock market predictions we’ve been seeing lately.) To explain why, I’ll first extend the analysis I shared in my last article.

Case Trajectory Update

For background, my March 2 article showed how the confirmed case trajectory could evolve if the most bearish epidemiological forecasts prove accurate. This time, I’ll set the forecasts aside and examine how the trajectory has changed in recent weeks.

I’ll exclude both China and Iran, because their reported numbers fail to match the on-the-ground evidence. I’ll then divide everyone else into two groups:

South Korea and Singapore, which I’ll call the “most prepared” group (MPG). These countries implemented a variety of effective disease-containment strategies after suffering from other epidemics in recent years.

The rest of the world, which I’ll call the “least prepared” group (LPG). That naming might be unfair to a few other well-prepared countries, but further regrouping wouldn’t materially change the conclusions.

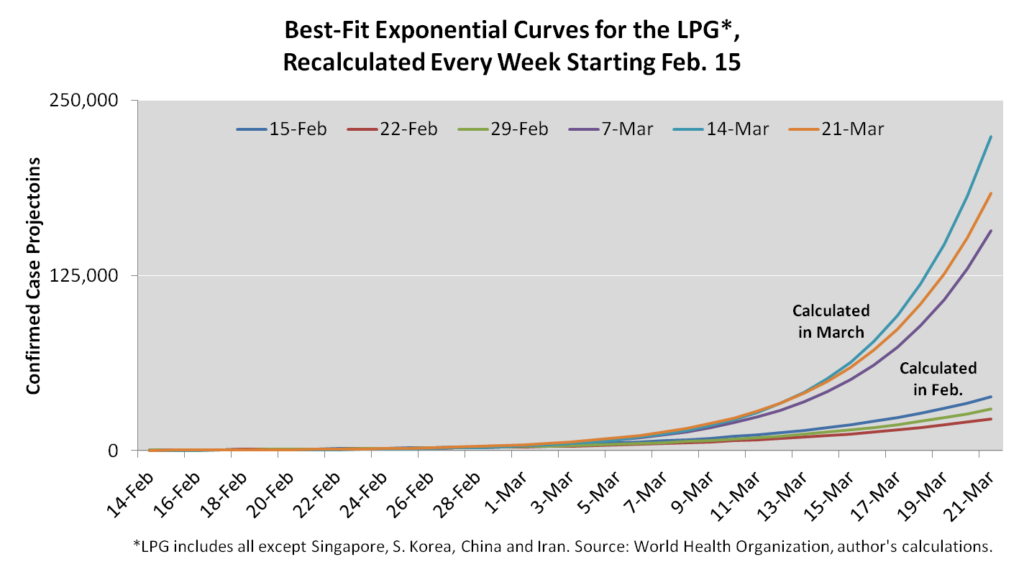

Here are the confirmed cases for each group through March 21:

As of today, the MPG has successfully “flattened the curve,” whereas the LPG continues to see exponential growth. Here are the best-fit exponential curves for the LPG, calculated on a weekly basis from February 15 until March 21:

The weekly curves steepened sharply in March, probably due to increased testing. But let’s take a closer look. The next chart shows the daily evolution for the “steepness statistic,” which is the part of the exponential function that determines the trajectory:

According to the chart, the case trajectory has passed through two stages since late February:

It steepened almost continuously as testing activity increased.

It then peaked on March 14 and started to flatten.

So that’s the past, but what about the future? How quickly, if at all, will the steepness statistic fall?

I doubt anyone can answer that with precision, especially with countries such as the U.S. only recently ramping their testing. But it sure seems as though the overall trend should continue downwards. With the extreme containment measures currently in place, it’s hard to imagine any other result. Or maybe I just don’t want to imagine a different result.

Either way, let’s be optimistic. Let’s agree that the March 14 peak delivers good news. It says the first derivative of the daily new case count is no longer rising day-after-day-after-day. That might be hard to conceptualize, but it’s exactly how these processes change direction. The first derivative turns downwards, and then the daily new case count turns downwards, and then the inflection point becomes apparent to all.

Implications for Stock Prices

Now for the bad news, which is that I’ve just exhausted my supply of good news, at least when it comes to stock prices. As the case trajectory flattens, we should see bursts of optimism that push prices higher, but probably not a market bottom. The problem is the two elephants that seem in no particular hurry to leave the room.

Businesses have shut down more suddenly and completely than ever before.

We have no idea when the business shutdowns will end.

Let’s say restaurants, bars, stores, factories, offices, schools, entertainment venues and transportation hubs reopen in about eight weeks. That seems possible, but it’s probably not sustainable. If political leaders remain consistent, any newfound infections would then send businesses right back out of work. In my county, for example, all nonessential businesses were told to close just as the confirmed case count climbed from 1 to 2.

In the meantime, we’re about to be bombarded with the worst economic data releases we’ve ever experienced. The economy is probably contracting even more sharply than it did during the 1933 national bank holiday, which is the only comparable I can think of. At a time when people withdrew cash from banks to make purchases, the bank closures brought much of the economy to a sudden halt. But the bank holiday only lasted seven days.

Others point to the 1980 and 2008-9 recessions, but in those instances the economy shrank organically. This time, it’s literally being locked down. I fail to see how those past recessions—or any past recessions, for that matter—can shed much light on the present one. And I can say the same thing about past pandemics, which have never before triggered worldwide, government-mandated business closures.

So instead of looking at, say, stock market returns in 1980, 2008-9 or during any other recession or major calamity, I expect the key to the market’s performance to lie in the answer to this straightforward question: At what point does our capacity to treat COVID-19 patients allow businesses to reopen?

Notably, at least one policy maker has pledged not to restart the economy until fatality risks reach zero. That approach might not be universal, but it doesn’t seem that far from consensus within the political class. Elsewhere, though, commentators are challenging that consensus, stressing connections between economic decline and public health. See, for example, this editorial by the Wall Street Journal and this commentary by a contributor to the CFA Institute’s Enterprising Investor blog.

Clearly, my question doesn’t have a single “correct” answer, and yet it might be the most important piece of the current policy mix. To stray briefly from financial to societal commentary, I hope policy makers develop their answers carefully. The WSJ might have summarized the predicament best when writing that “no society can safeguard public health for long at the cost of its economic health.”

Now bringing the discussion back to stock prices, the answer to my question determines when the cloud of uncertainty finally lifts. It determines when investors can resume normal financial analysis, and when commentators predicting the next bull market might finally be onto something.

Bottom Line

No doubt, market volatility brings opportunities. Long-term investors are finding value as the market falls, and even short-term traders are finding buying opportunities as prices bounce wildly up and down.

But risk tolerance is paramount. For those unable to stomach losses on new holdings, my nickel’s worth of advice is to be cautious. I’ve shared my most optimistic chart – showing a declining case trajectory – but I don’t expect it to turn the tide in the stock market. For that, we’ll need more clarity about when we can once again claim “the business of America is business.” That’s at least weeks and possibly many months away.

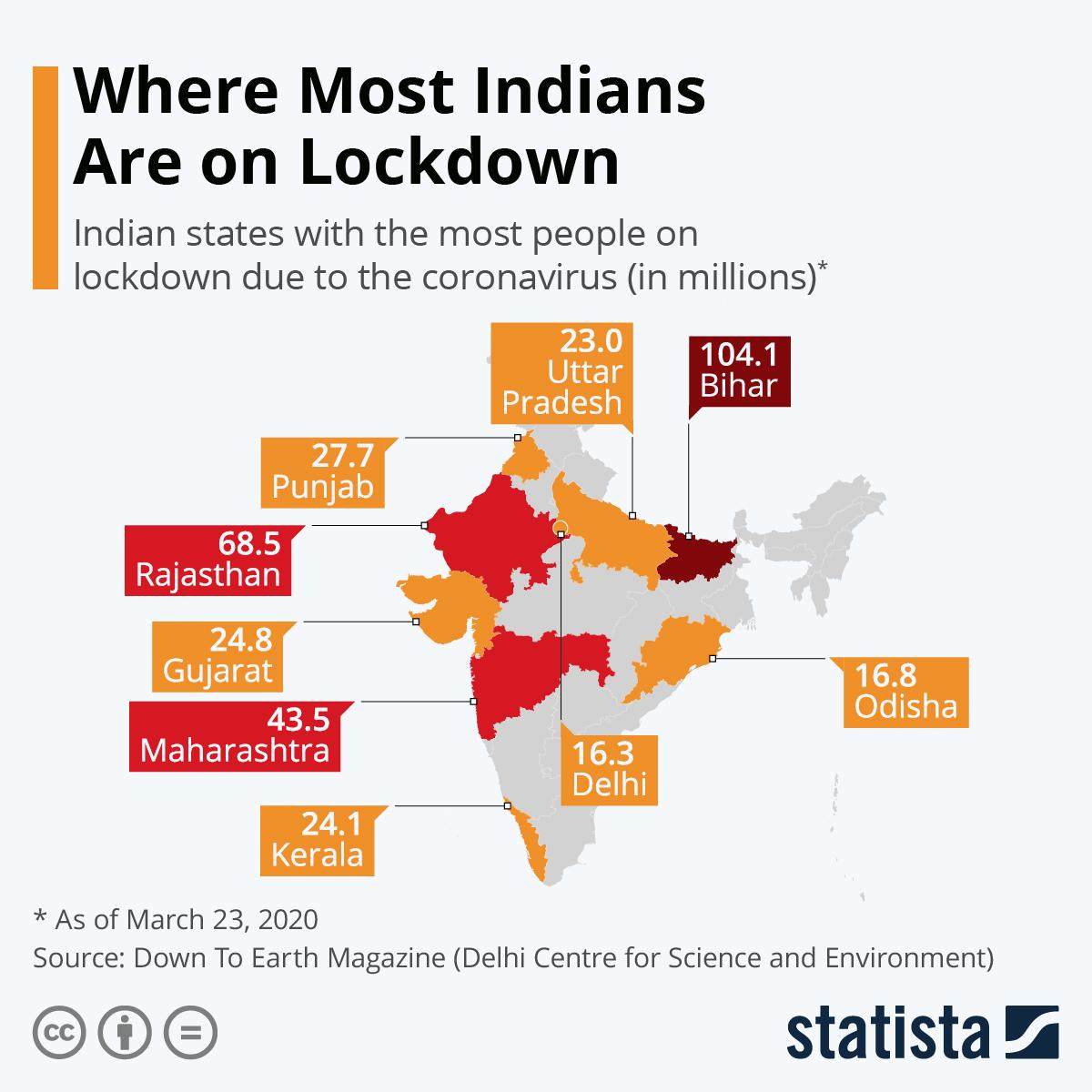

“Biggest Lockdown In World History” – India Paralyzed As COVID-19 Crisis Unfolds

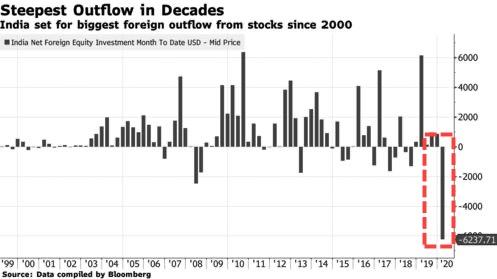

Indian stocks crashed on Monday, suffering their worst single-day loss on record, as domestic and foreign investors were absolutely terrified that a nationwide lockdown triggered by a COVID-19 outbreak could crash the economy.

The NIFTY 50 is the flagship index on the National Stock Exchange of India, plummeted 12.98% to a near four-year low of 7,610.25 on Monday.

The Indian rupee hit a record low of over 76 against the dollar and puts pressure on the Narendra Modi government and the Reserve Bank of India (RBI) to ramp up emergency response efforts to protect a crashing currency and economy.

Modi’s “Make-in-India” program, an attempt to revive the economy and diversify its manufacturing sector away from automobiles to bolster its aerospace and defense sectors, has miserably failed.

The economy has come to a screeching halt as residents in 75 districts across the country, including in major cities, such as the capital New Delhi, Mumbai, and Bangalore have been forced into mandatory quarantine by the government until March 31.

India is the second-largest country in the world, and has reported only 467 cases and ten deaths.

The lack of test kits has made it virtually impossible for the Ministry of Health and Family Welfare to detect community spreading of the virus. As test kits come online, India could be staring at a pandemic.

Actions by the government already suggest the virus crisis is getting worse. In the last day, India launched the world’s most extensive social distancing lockdown of 1.3 billion people to flatten the pandemic curve to slow down the infection rate.

Nearly a billion Indians stayed indoors on Sunday.

Flight bans and the cancellation of all passenger trains in the country is another attempt to limit the spread. The country’s hospital system is poorly equipped and doesn’t have enough hospital beds and ICU-level treatments to handle a massive influx of virus patients.

“This is the biggest lockdown in world history,” said Raghu Raman, a former soldier with the Indian Army and founder of the National Intelligence Grid, an umbrella database aimed at countering terrorism.

“This strategic pause gives decision-makers more time to arrest the exponential spread of the virus and evaluate tradeoffs.”

Foreign investors aren’t sticking around to see if the virus crisis will abate in the near term – they’re currently dumping Indian assets at an unprecedented pace.

Oxford Economics estimates India’s January-April growth forecast to be around 3%, a level not seen since the global financial crisis.

Bloomberg Economics says that the Indian government needs to spend at least 1% of GDP, or about $30 billion, to respond to the virus outbreak.

India’s manufacturing hubs have ground to a halt as companies have been forced to shutter operations for virus containment purposes. Maruti Suzuki India Ltd., Tata Motors Ltd., Toyota Kirloskar Motor, Hero MotoCorp., Samsung Electronics Co. and LG Electronics Inc., Mahindra Group, TVS Motor Co., Kia Motors Corp., Renault Nissan Automotive India Private Ltd., and Yamaha Motor India are some of the large multinationals that have recently suspended operations.

The government’s principal economic adviser Sanjeev Sanyal warned that “waves of default” of corporate debt could be imminent. There’s a record 5.9 trillion rupees of corporate debt maturing this year.

Finance Minister Nirmala Sitharaman said last week that the government would announce a relief package for companies in the near term. The RBI is expected to slash interest rates and inject 1 trillion rupees into the economy on April 3.

We noted back in December that India’s economy was “in a very deep crisis,” which was a month before the world figured out about a virus outbreak in Wuhan, China.

It was only earlier this month that India organized a rescue plan for the nation’s fourth-largest private bank as a long-running crisis among shadow lenders threatened to spill over into the banking system.

With a nationwide lockdown underway, India’s economy could be on the brink of a significant downturn that would be absolutely devastating for the Modi government.

The word ‘pandemic’ bears a similarity to the word ‘panic’ and indeed ‘pandemonium’. In fact ‘pandemic’ evokes an almost instant flush of fear in those easily manipulated by mass media, before any details have even touched the surface or context in which the word is being used.

Those who plan the major moves on the chess-board of covert human control know that by leading with the word ‘pandemic’ they have an instantly effective weapon at their disposal to psychologically weaken the resistance of individuals vulnerable to irrational and impressionistic mindsets.

So, in a world heavily conditioned by the proclamations of the mass media, the fear weapon has huge psychological power.

As we have all witnessed over the past months, the Coronavirus story has been unleashed with barely contained lascivious delight by news media under orders from the purveyors of malevolent missions against mankind. Pumped-up to maximum volume and dispersed globally, the deliberately designed fear message has the instant effect of making the majority of people feel powerless. The Big problem is at large – and we the people feel small. This is the beginning of entrapment which colors every aspect of daily life.

Most of humanity has undergone a process of education which depends for its effectiveness on the perceived power of some ‘authority’ to exert an unquestioned controlling influence over the general direction of life. A source of influence that depends for its continuing effectiveness on never being subjected to rational scrutiny, or genuine examination of any kind. Such is the beguiling power of full-on indoctrination.

In the battle now raging for ‘who controls the world’, some of the largely hidden or disguised controlling agents of planetary life – are now appearing on the surface. And that’s why chaos and fear are very much ‘flavor of the month’. The Corona Contagion is chock full of idiosyncrasies; in fact, there are so many nonsensical factors associated with media attempts to report on what’s going on, that one can only feel dazed and confused should one try and follow the script in real-time.

However, what has become all too clear is the fact that large numbers of people are being herded – and are not resisting. The scare tactics being employed are more dangerous than the virus that is the excuse for deploying them. Under this induced state of psychosis, all manner of tricks can be perpetrated on mankind – and that is precisely what we are witnessing at this time.

Many reading this will already be familiar with the ambitions of the controlling deep state ‘elite’ and will know that a pre-planned phase of social and economic chaos is a key factor in their attempted roll-out of totalitarian New World Order. We are now in this phase. Its success depends upon a large body of people following the instructions passed down by the political puppets of the deep state and by the cowardly repetition of these instructions by the mainstream media.

Once again, the fear card plays a key role. This time, in keeping a constant level of anxiety and hysteria on the boil, while working to ensure that those able to recognize the true nature of the scam are coerced into not stepping out of line, thereby risking their job, security or status within the rigidly enforced master/slave relationship of the status quo.

The whole sick edifice maintains its momentum based upon pure top-down deception and exploitation. Yet those at the receiving end largely choose to remain oblivious of the fact that they are being used and abused for the benefit of a fascist ideal. By not rebelling in the face of such treatment – but instead by complying with it – a mute populace establishes the basis of its own debasement and slavery.

These methods have been practiced over and over again in the history of the world, and each time hind-sight reveals the motivation to have been an obsession with power and control, and the perpetrators to be a small number of psychopathic despots. Whether taking the form of military might, religious dogma or modern-day corporate and banking control freaks, provided the drama has been well stage-managed and the ‘might has produced fright’, the hegemons get their way.

How well is the roll-out being stage-managed on this occasion – and what is the plan?

Owing to the trans-planetary link-ups that take place today, the ‘master plan’ is no longer a regional or national affair, but a global one. The main players have hatched the plot long before any of us get to know about it and gatherings like the Davos Economic Summit and Bildergerger meetings are used to gain consensus on the timing and methods to be deployed.

In the case of Covid-19, its appearance on the scene – or at least the spreading of the story about something nasty going under this name – is timed to divert attention from the speeding-up of the installation of what are deemed to be important spokes in the creation of a totalitarian New World Order. For example, the roll-out of 5G microwave modulated WiFi; a digitalised smart grid and ‘internet of things’; a robotic transport system; facial recognition population surveillance programmes; new strains of genetically modified organisms and vaccines, and so forth. However, the predominant game plan is to ‘re-set’ global finance so as to appear to be supporting the euphemistically named Green New Deal with its holy grail ‘Zero Carbon’.

The fact that China has likely been the initial bio-weapon target, does not detract from a more widespread aim to disrupt the world economy as a whole.

The effectiveness of this disruption depends upon the greater part of the populus being swept along in a bubble of blind belief in the authenticity of the ‘virtual’ story line. A line which disguises the very actual imposition of a fascist state.

I would say that the stage-management is pretty poor this time around. The plethora of contradictory and irrational clamp-down actions being imposed in the name of containing the bogey bug stretches the credibility of the operation to the braking point. In point of fact it’s a farce; but a farce which involves actual deaths and the support of a police state, cannot simply be laughed-off.

Instead, it can be put under the spotlight and be seen for what it is, a planned manipulation of the people and resources of this planet, whose main goading-tool consists of the well-rehearsed art of spreading fear and panic. And this, in turn, to undermine the rational and common sense based gift which we have all been blessed with from birth, and which – when in good order – can clearly see through the facade and hold the line of reason and truth.

Many have seen this ‘order out of chaos’ drama coming for years. The chaos bit is with us right now and very visible. The ‘order’ is to follow and consists in the emergence of a peacemaker – or peace plan – that involves the lead croupiers raking the chips off the roulette board and cashing them into their temporary satisfaction. Thus allowing for a little holiday period in which the weak-kneed can rejoice at their survival and bless the emergence of the ‘new order’, under the authority of no matter who or what, so long as they can believe that the world has been saved from anarchy and ruin.

Every one of us whose knees have not turned to jelly and whose brains have not turned to mind-controlled pulp must take this moment to declare ourselves, boldly and resolutely with these four words “We do not consent”.

There’s a surprise in store for the cowardly imposers of chaos – it is our time that’s coming and – not theirs. For ours is the True World Order which aligns with Universal Law, not the false laws of a manipulated status quo.

It is our re-emergent marriage with Universal Truth that is going to oust this scare loaded pandemic and all similar manifestations of dark-side deception that have gripped this planet for far too long. Our true-world-order is going to take on this obsessed and demonic dynasty, so that it stumbles, falls and fails to rise again.

Seize this auspicious moment – and let us be joined as one in an unwavering commitment to get off our knees and stand firm in the cause of defeating the ghosts of chaos and fear.

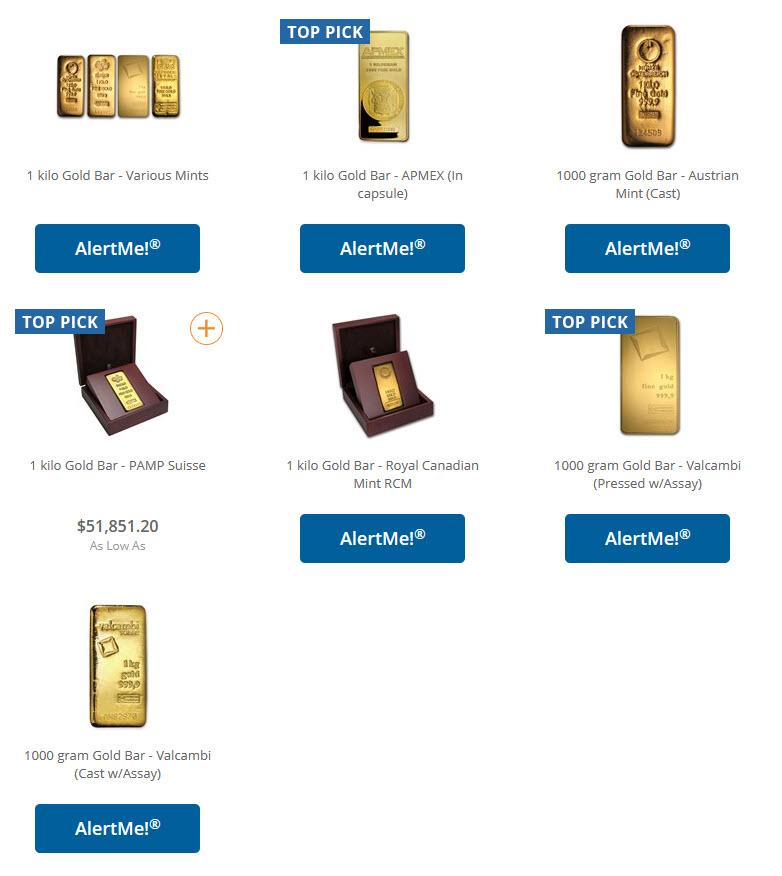

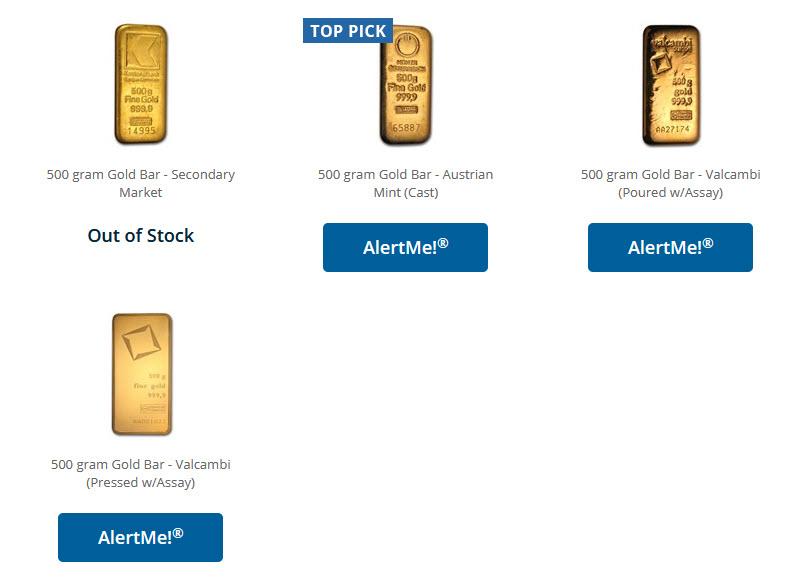

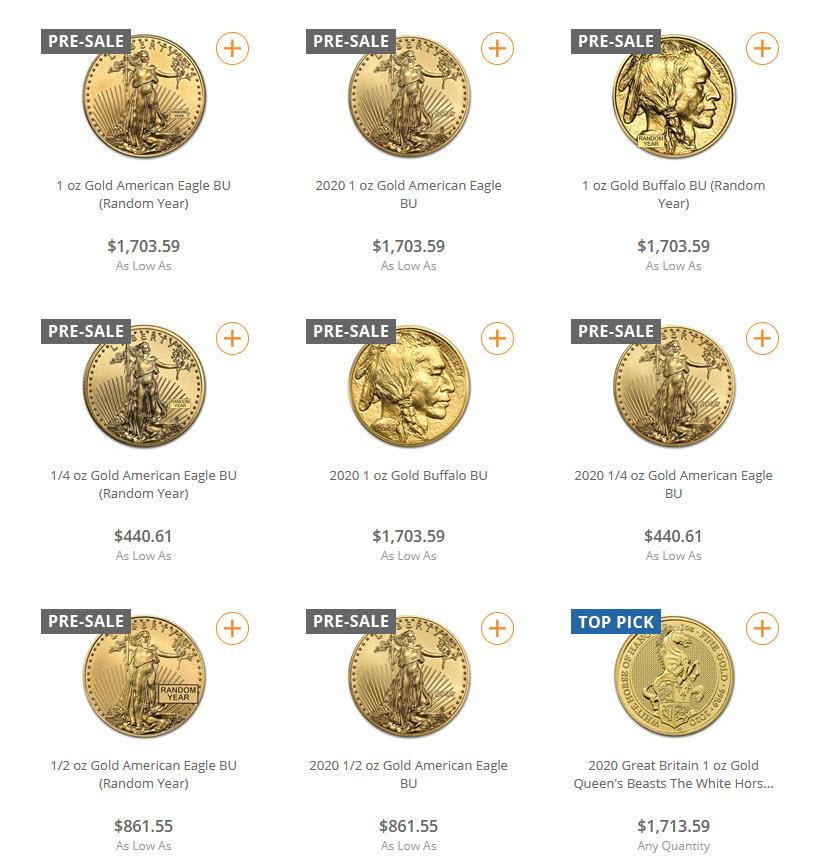

“It’s Selling Like Toilet Paper”: If You Haven’t Bought Physical Gold Yet, It’s Probably Too Late

Over the past decade, one of the most fascinating observations in the world of precious metals has been the bizarre decoupling in the supply/demand dynamics and thus pricing, between paper and physical gold.

As gold became increasingly financialized in recent years – through futures, ETFs, derivatives and so on – and as the impact of “financialized” gold became the dominant price-setting factor in a world where the nominal volume of “paper gold” traded is now orders of magnitude greater than “physical”, a bizarre decoupling emerges every time there is a major market stress event. A pattern that has emerged is that during periods of “bathwater” liquidation, when levered asset managers are forced to dump paper gold to cover margin calls in different parts of their book, sending the price of gold sharply lower also happens to be when physical gold buyers step up amid concerns over the viability of either the financial system and/or the reserve currency.

The result, as discussed last week, is that “the price of physical gold decouples from paper gold” resulting in an arbitrage that physical gold buyers, i.e., those who don’t have faith in gold ETFs such as the GDX or simply prefer to have possession of the metal, find especially delightful as it allows them to buy physical gold at lower prices than they would ordinarily have access to.

The immediate next step is a surge in demand for physical gold that results in precious metal vendors and exchanges becoming sold out in very short notices. Take for example the largest US precious metals exchange, APMEX, where any attempt to buy gold in size, or rather weight (because the truly rich who need to park several millions can’t be bothered with individual gold coins and instead go for the 400 oz brick or 1 kilo bar), finds, well, nothing because everything is sold out, and not just for bars…

But don’t take our word for it: as that beacon of pro-fiat, anti-hard money dogma, the Financial Times, reports this morning, traders have reported and lamented a growing global shortage of gold bars, as the coronavirus outbreak both disrupts supply and stokes demand, “with one business comparing the frenzied buying of the yellow metal with the consumer rush for toilet roll.”

Of course, the fact that gold makes for very expensive toilet paper and is thus available to a far more exclusive audience, one that can spend substantially more on the yellow metal, was lost on the FT, so here’s the recap: there is a wholesale flight out of “paper” and into physical among some of the world’s richest people.

One thing the FT does get right is that “retail investors in Europe and the US have bought up gold and silver bars and coins over the past two weeks in an effort to protect their money from the collapse in global stock prices and many currencies.” And with the Fed now set to unleash unprecedented dollar destruction by injecting over $625 billion in freshly printed fiat into the system this week alone…

… concerns about the collapse of currencies will only grow.

But what is more concerning is that it’s not just a demand problem: supply chains are also freezing, and Europe’s largest gold refineries have struggled to keep up because of the region’s widening shutdown. Valcambi, Pamp and Argor-Heraeus are all based in the Swiss town of Ticino, near the border with Italy. Local authorities announced in recent days that production in the area was to be temporarily halted.

Unfortunately, just like everything else, gold refiners are also shutting down, ensuring that any gold shortages will persist for months at least.

Just heard the same from another major Swiss refinery – they are also closing the plant due to the virus.

CLARIFICATION: One Swiss refinery is near the Italian border and is offline, the other is in the center of Switzerland and will take orders for which one must pay upfront but since they are fully booked for four weeks, there is no visibility on delivery timing. #counterpartyrisk

With supply collapsing and demand soaring, one would hardly think that the price of gold would plunge, and yet that’s precisely what happened much of last week as funds dumped paper gold, leading to the abovementioned paradoxical divergence in paper and physical prices.

And since gold vendors are constrained by the price of spot which is largely determine in the paper market, the result is that retailers are reporting shortages and delays of up to 15 days on shipments as demand has surged. Markus Krall, chief executive of German precious metals retailer Degussa, said it was struggling to meet customer appetite for gold bars and coins and had to turn to the wholesale markets. Demand is running at up to five times the normal daily amount, he said.

“We are being creative to find new sources but what is driving it all are the measures by authorities to stop coronavirus. This is so unpredictable,” added Mr Krall.

Rob Halliday-Stein, founder and managing director of Birmingham-based BullionbyPost, said the situation was unprecedented. “Basically we’re selling as soon as we get stock on location in secure vaults — but we’re restricted to what we can get hold of, it’s a bit like toilet roll.”

Another irony: while London’s gold vaults are full of gold bars, they are of the 400-ounce “good delivery” variety traded (and rehypothecated) among large banks (and central banks) such as HSBC and JPMorgan, not the smaller bars that retail customers buy, which tend to be 1kg (35 ounces) or lighter.

“I don’t think you will find a kilobar presently in Europe and the US for love nor money,” Ross Norman, a veteran gold trader, said. “It’s quite extraordinary.”

And speaking of Apmex, its CEO Ken Lewis told the FT that in the past week that “product has become increasingly difficult to source as the market becomes more volatile day by day”.

The company said it had purchased more than 1m ounces of silver grain and bars, more than 20,000 American Gold Eagles coins, thousands of gold bars, and “anything else we can find utilising our many partners and mint relationships”.

And all of that gets sold out the moment it becomes available for sale.

JM Bullion, another US-based precious metals retailer, said customer orders would be delayed by 15 days, and introduced a minimum order size (as did Apmex).

BullionStar, a Singapore-based precious metals retailer, said it is paying a premium to buy back silver and gold coins from customers in an effort to replenish supplies, according to Ronan Manly, one of its analysts. “There’s a disconnect between prices in the physical gold market and the prices you see on your screen,” he said, repeating precisely what he wrote here several days ago.

Trump Is Finally Happy With Powell: “I Called Him Today And I Said ‘Jerome, Good Job'”

It finally happened.

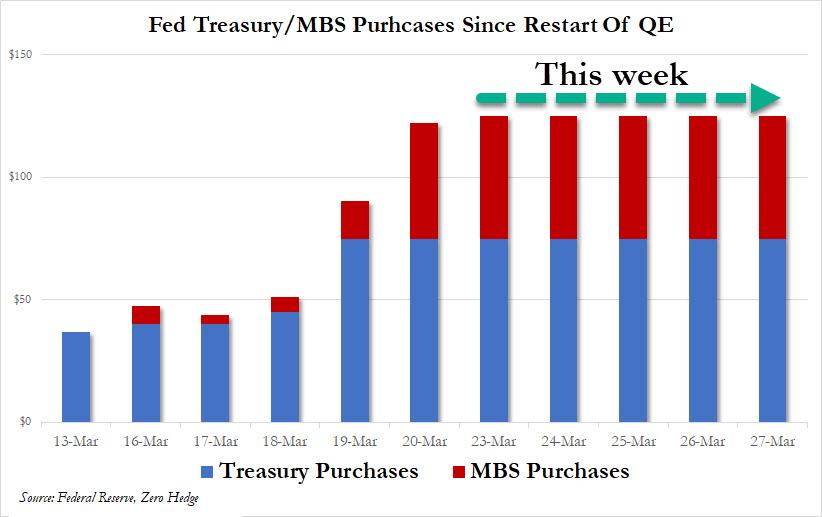

After the Fed cut rates to zero, launched unlimited QE, is on pace to buy $1 trillion in Treasurys and MBS in 2 weeks, backstopped pretty much every asset class and announced it would purchase bonds, loans, commercial MBS,munis as well as the LQD ETF, Trump is finally very happy with Fed Chair Jerome Powell, ironically on the same day Powell signed the dollar’s death warrant.

Here’s what Trump said on Powell.

“I am happy with him. I really think he’s caught up and he’s done the right thing. And I think ultimately we will be rewarded because of the decision he made over the last — he’s really stepped up over the last week.”

“I called him today and I said ‘Jerome, good job.”

“He was a little bit slower than what I’d have liked, in the sense of what he was doing.”

“But today I called up Jerome Powell and I said ‘Jerome you’ve done a really good job.’ I was proud of him. It took courage. Ultimately you’re going to see the fruits — he’s not finished. He’s got other arrows in the quiver.”

“I’m very happy with the job he did.”

“I am happy with him, I really think he’s caught up,” Trump said of Fed Chair Jerome Powell at the White House #Covid19 briefing pic.twitter.com/cRyaFIJfpa

For those who missed it, here is how Jerome Powell finally managed to get Trump to crack a smile:

Today, the FOMC expanded its large scale asset purchase program by promising to purchase ‘in the amounts needed.’ One week ago, the FOMC had said it would purchase $500bn of Treasury securities and at least $200bn of agency MBS; Half of that amount was fully purchases within a week.

The FOMC also announced that the agency MBS purchases will include agency commercial MBS.

The Fed also made CPFF more generous in terms of pricing and opened CPFF and MMLF to a wider set of assets.

The Board of Governors relaunched the Term Asset-Backed Securities Loan Facility (TALF), providing loans in exchange for ABS.

The Fed also announced it would buy corporate bonds and loans in both the primary and secondary markets.

The Fed also said it expected to announce soon the establishment of a Main Street Business Lending Program to support eligible small-and-medium sized businesses.

All that’s missing is for the Fed to start buying stocks and literally paradrop dollars from a helicopter. Trump will find both delightful.

* * *

Whoever Timestamps things, please Timestamp this post and check back in 10 years when the fiat monetary system as we know it is long gone.

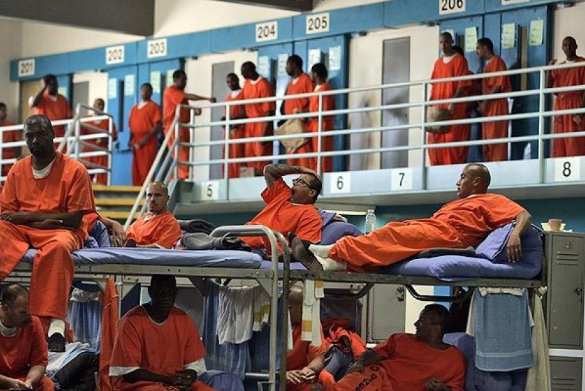

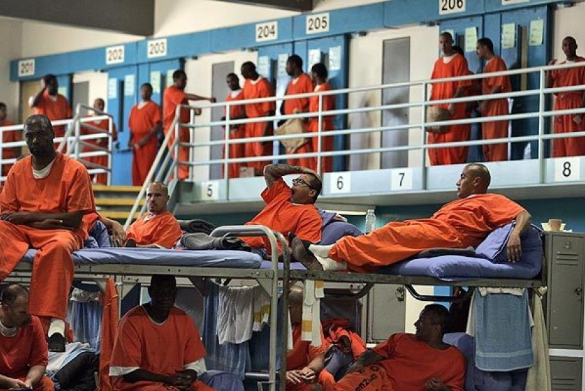

Rights advocates and Democrats holding state and federal elected offices across the United States are doubling down on demands for the release of “at-risk” inmates and more preventive measures in jails and prisons to prevent mass outbreaks of the new coronavirus, which has killed at least 473 people and infected over 35,000 nationwide as of Monday morning.

Three Democratic congressmembers from New York—Reps. Nydia Velázquez, Hakeem Jeffries, and Jerrold Nadler—joined David Patton of the Federal Defenders, Anthony Sanon of the union representing corrections officers at the Metropolitan Detention Center, correctional medical experts Dr. Brie Williams and Dr. Jonathan Giftos, and New York City Councilmember Brad Lander for a virtual press conference Sunday. “The COVID-19 pandemic has turned our nation’s jails and prisons into ticking time bombs,” said Patton during the press conference.

Image via Los Angeles Times

“This is no time for business as usual. Unless federal courts and federal prosecutors take immediate and bold action to reduce our federal prison population and limit the intake of new prisoners, we will face a humanitarian crisis of enormous magnitude,” Patton added.

A goal of the event was to pressure the Southern and Eastern Districts of New York to halt new arrests for nonviolent charges and release from federal jails inmates who are at risk of serious illness or death if they contract COVID-19.

The press conference came after House Judiciary Chair Nadler sent a pair of letters to U.S. Attorney William Barr in recent weeks asking how the Federal Bureau of Prisons and U.S. Marshals Service is repsonding to the pandemic. In the latest letter (pdf) Thursday, Nadler and Rep. Karen Bass (D-Calif.) called for considering the release of “vulnerable” inmates, such as “persons who are pregnant, who are 50 years old and older, and who suffer from chronic illnesses like asthma, cancer, heart disease, lung disease, diabetes, HIV, or other diseases that make them vulnerable to COVID-19 infection.”

President Donald Trump said Sunday that his administration was weighing the release of some incarcerated people following the first known COVID-19 case involving an inmate—a man at Metropolitan Detention Center in Brooklyn. California officials announced Sunday night that an inmate at California State Prison in Los Angeles County has also tested positive for the virus, after five cases among staff at three other state facilities.

Corrections experts and rights advocates have warned for weeks that, as Maria Morris of the ACLU wrote earlier this month, “prison and jail populations are extremely vulnerable to a contagious illness like COVID-19” because “conditions in correctional facilities are highly conducive to it spreading” and many inmates “are in relatively poor health and suffer from serious chronic conditions due to lack of access to healthcare in the community, or abysmal healthcare in the correctional system.”

Williams is a University of California San Francisco professor of medicine who focuses on healthcare in correctional settings, particularly for the elderly and chronically ill. “The possibility for accelerated transmission and poor health outcomes of COVID-19 in prisons and jails is extraordinarily high,” she warned. “Coordinated, preemptive, thoughtful, and decisive action around decreasing the population in prisons and jails with public health at its center will save lives in prisons, jails, and in our communities. Business as usual will not.”

Image: Los Angeles Times via Getty Images

Noting that first known COVID-19 case involved an inmate in her district, Congresswoman Velázquez called for “rapid, proactive department-wide steps” to protect inmates and staff in correctional facilities, including the “compassionate release of incarcerated people who are elderly or have underlying health conditions, and who pose no risk to public safety.”

Velázquez also urged federal prisons and jails “to implement streamlined procedures to release individuals who have not been convicted of any crimes and are awaiting trial in prison or jail” and pressed the U.S. Attorneys’ Offices to “exercise maximum restraint in terms of bringing additional individuals into the court and jail system.”

As Giftos, former medical director of Correctional Health Services at Rikers Island, put it: “Jails simply cannot protect patients and staff from a viral pandemic affecting the city.” Giftos, now the medical director at Project Renewal, which treats NYC’s homeless population, added that “the only measure that will meaningfully impact the spread and harm of coronavirus in the jail-system is to depopulate—to release as many as possible to continue their cases in the community—with a focus on those at highest risk of complications.”

Some courts and states have moved to prevent the spread of the virus in correctional settings. Cuyahoga County Court in Ohio ordered the release of certain inmates from the county jail earlier this month and the New Jersey Supreme Court on Sunday approved an agreement (pdf) among the state attorney general’s office, county prosecutor’s association, the public defender’s office, and state’s ACLU chapter to release up to 1,000 people in county jails beginning Tuesday.

“Unprecedented times call for rethinking the normal way of doing things, and in this case, it means releasing people who pose little risk to their communities for the sake of public health and the dignity of people who are incarcerated,” ACLU-NJ executive director Amol Sinha said in a statement. “This is truly a landmark agreement, and one that should be held up for all states dealing with the current public health crisis.”

After a Sunday announcement that a correctional officer at Cook County Jail in Chicago tested positive for COVID-19, Cook County Public Defender Amy Campanelli was scheduled to present an emergency petition Monday demanding the release of “vulnerable” detainees, according to the local ABC News affiliate. The Chicago Sun-Timesreported that “several” people deemed “highly vulnerable” to the coronavirus were released from the facility last week.

Local faith leaders planned a socially distanced prayer vigil outside the Cook County Jail for Monday morning ahead of the hearing. Rev. Rachel Birkhahn-Rommelfanger of the Northern Illinois Conference of the United Methodist Church explained in a statement from the Chicago Community Bond Fund that “our faith calls us to advocate for the release of people incarcerated in the jail whose lives are at risk because of COVID-19. We are in an unprecedented crisis that calls for unprecedented action.”

Who knows maybe once this is all over, Twitter will be forced to lay off its pro-establishment content nazis and the platform that started off as an experiment in free speech will finally return to its roots.

And ironically, that is almost what they did… except for one thing – if you’re an ‘average joe’, ‘blog’, or ‘Trump supporter’, you’ll still be banned; but if you’re a government official, you’re allowed to say whatever you want about the origins of COVID-19 and not get censored, suspended, or banned.

Twitter says coronavirus is “affecting our content moderation capacities in unique ways” and it cannot “take enforcement action on every Tweet that contains incomplete or disputed information” about the virus.

“Official government accounts engaging in conversation about the origins of the virus and global public conversation about potential emergent treatments will be permitted, unless the content contains clear incitement to take a harmful physical action.”

As many know, following ZeroHedge’s permanent ban from the platform, it appears in recent months Twitter has taken it upon itself to become the supreme arbiter of all that is politically correct, noble and just(or at least is not frowned upon by the Chinese Communist Party) in this cruel world where readers are completely unable to make up their minds on their own without a blue bird telling them what they should or should not read, and what, in its eyes, is arbitrary fake news.

And now, following Chinese officials completely unsubstantiated claims that the virus emerged in the US, Twitter changes its policy?

But, it would seem – given our permanent ban, that telling people to ask someone what happened using public info is “clear incitement to take harmful physical action” but that making completely unsubstantiated claims about another global superpower that could quite easily escalate into social unrest, xenophobia, and inevitably war – is fine if it’s done by a government?

{kind=link}

{kind=link}