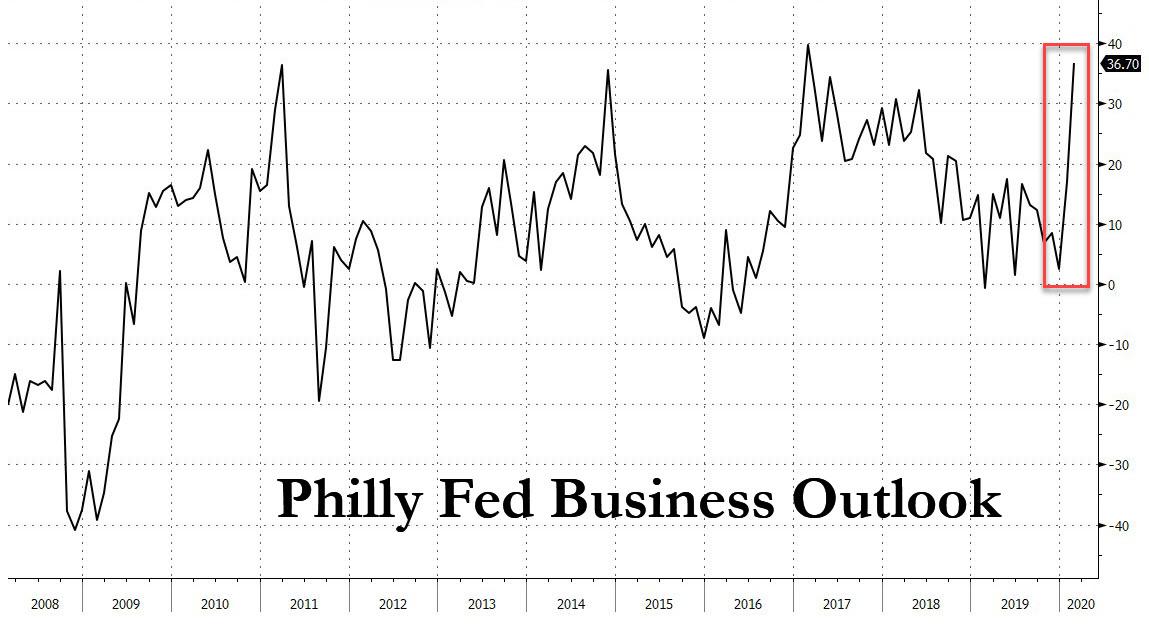

Philly Fed Unexpectedly Soars To Second Highest Since Financial Crisis

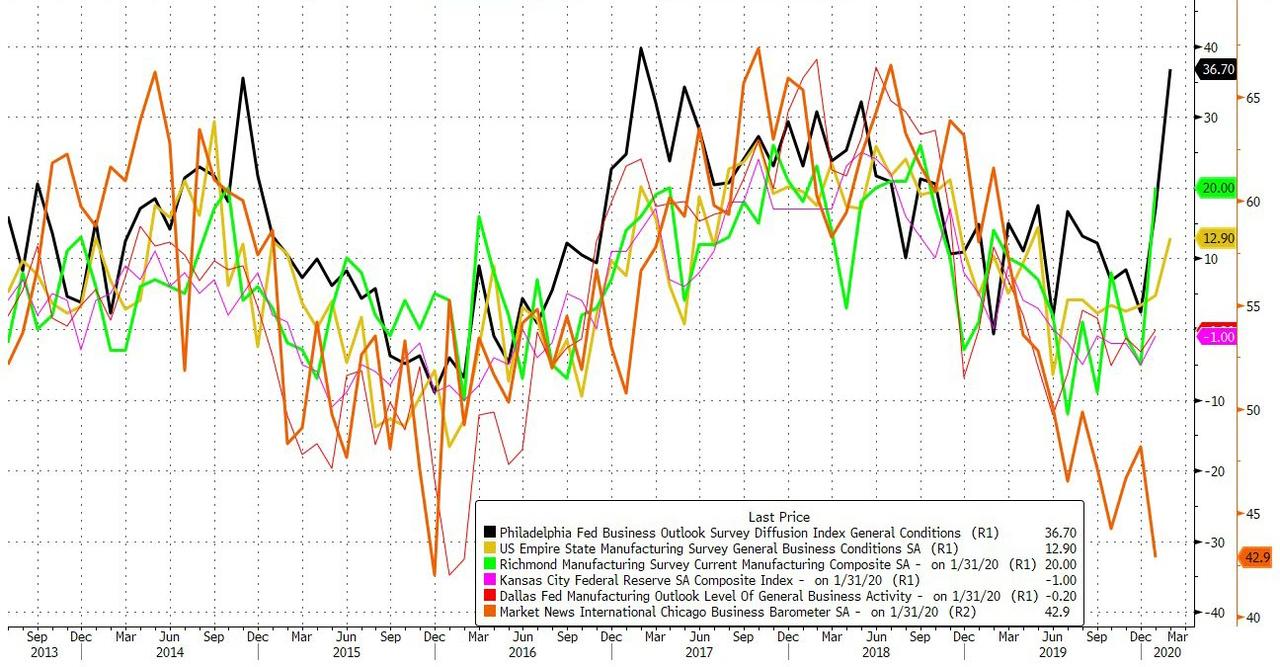

Anyone expecting the coronavirus pandemic to hit regional Fed surveys following the recent plunge in the Chicago PMI was in for a disappointment this week, when first the NY Fed’s Empire State mfg survey unexpectedly printed at the highest since mid-2018, and then moments ago the Philly Fed blew it out of the ballpark with a massive surge in its business outlook survey, where the current general activity rose nearly 20 points this month to 36.7, smashing expectations of a drop from 17.0 to 11.0, and the highest index reading since February 2017. More importantly, this was the second highest print since the financial crisis.

The Philly Fed was merely the latest regional Fed to not confirm the recent weakness telegraphed by the Chicago PMI which earlier this month tumbled to the lowest level since 2015.

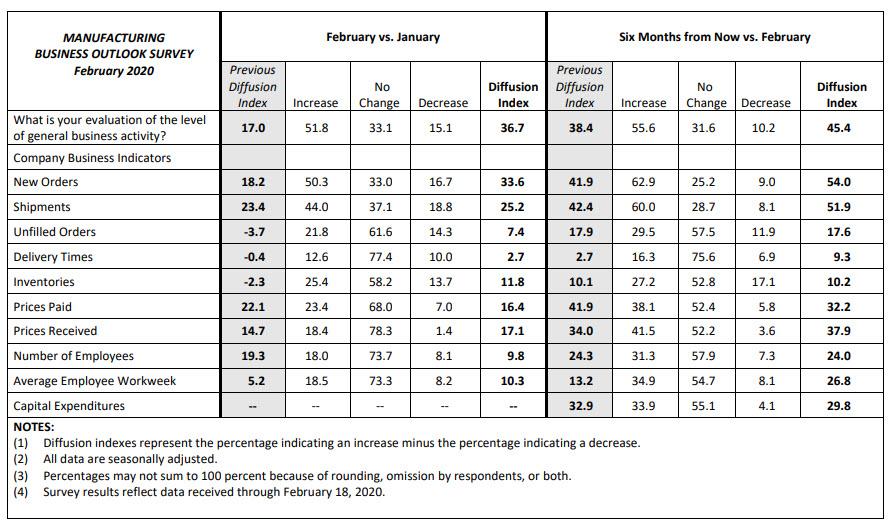

Commenting on the monthly report, the Philadelphia Fed said that “the survey’s current indicators for general activity, new orders, and shipments increased this month,suggesting more widespread growth. The firms reported expansion in employment, although at a moderated pace from January. The survey’s broad future indexes also showed improvement this month, indicating that growth is expected to continue over the next six months.”

That said it wasn’t clear just what catalyst sparked such manufacturing sector euphoria, aside perhaps form a delayed kneejerk reaction to the Trump trade war ceasefire.

The percentage of firms reporting increases(52 percent) this month exceeded the percentage reporting decreases(15 percent). As shown in the table below, the index for new orders increased 15 points to 33.6, its highest reading since May 2018. Over 50 percent of the firms reported an increase in new orders, up from 46 percent in January. The current shipments index increased 2 points. Both the unfilled orders and delivery times indexes moved into positive territory this month, suggesting slightly higher unfilled orders and slower delivery times.

To be sure, it wasn’t all roses: while firms reported overall increases in manufacturing employment this month, the current employment index decreased 10 points to 9.8. Just 18 percent of the firms reported higher employment, compared with 28 percent last month. The average workweek index, however, increased 5 points.

Alas, don’t expect this number to be repeated with the latest batch of private sector PMIs starting tomorrow, with trade war far in the rearview mirror and instead businesses now freaking out over what the collapse in Chinese supply chains means for the profits and viability.

The billionaire’s self-bankrolled presidential bid was torn to shreds in the opening minutes of Wednesday’s Democratic debate as his opponents skewered him for his checkered past on sexual harassment and his record on stop-and-frisk.

While there was no clear winners – though Mayor Pete Buttigieg perhaps came out the least ‘scathed’, there was a clear loser… billionaire Mike Bloomberg who saw his odds collapse in real-time (albeit rescued by a miraculous intra-debate bid)…

But by the end, Bernie had extended his lead and Bloomberg was relegated back to an also-ran…

Right out of the gate, Bloomberg was under attack with Massachusetts Sen. Elizabeth Warren landed perhaps the biggest (and first punch), making the former Big Apple mayor visibly squirm and roll his eyes in frustration.

“I’d like to talk about who we’re running against, a billionaire who calls women ‘fat broads’ and ‘horse-faced lesbians,’” she said from the Paris Theater.

“And, no, I’m not talking about Donald Trump. I’m talking about Mayor Bloomberg.”

It didn’t stop there as former Vice President Joe Biden attacked Bloomberg for “throwing close to 5 million young black men up against a wall” while mayor of New York City and said he only stopped after President Barack Obama intervened in his stop-and-frisk policy.

Minnesota Sen. Amy Klobuchar accused Bloomberg of “hiding behind his TV ads.”

Former Vice President Joe Biden hammered him for opposing Obamacare.

Former South Bend, Indiana, Mayor Pete Buttigieg called him “a billionaire who thinks that money ought to be the root of all power.”

Warren also attacked him over his record of sexist comments and challenged him to release women from nondisclosure agreements with his company, Bloomberg LP, so they could openly discuss any claims of sexual harassment.

Bloomberg: “We have a very few nondisclosure agreements.”

Warren: “How many is that?”

Bloomberg: “Let me finish. None of them accuse me of doing anything other than, maybe they didn’t like a joke I told.”

His response provoked a groan from the audience.

This is not just a question of Mike Bloomberg’s character—it’s a question about electability. We’re not going to beat Donald Trump with a man who silences women with who knows how many nondisclosure agreements. #DemDebatepic.twitter.com/ozPFghxU8s

But, Warren’s attack made some sense, as The Epoch Times’ Roger Simon noted, for all his attacks on Donald Trump, Bloomberg has more in common with Trump than anyone on the stage, certainly miles more in common with the president than he does with Sanders, his primary Democratic adversary at this point.

Sanders midway through took umbrage at Bloomberg for implying Bernie was a communist or, perish the thought, that socialism often leads to the totalitarian curse of communism.

“Let’s talk about Democratic Socialism. Not communism, Mr. Bloomberg. That’s a cheap shot. Let’s talk about what goes on in countries like Denmark, where Pete correctly pointed out; they have a much higher quality of life …We have socialism for the very rich. Rugged individualism for the poor,” Sanders stated, ripping into Bloomberg.

Sanders called it a “cheap shot.” It wasn’t. It was the truth.

But, after all is said and done President trump was probably the biggest gainer overall, gleefully mocking the Bloomberg as “stumbling, bumbling and grossly incompetent” in an early tweet:

“Mini Mike Bloomberg’s debate performance tonight was perhaps the worst in the history of debates, and there have been some really bad ones. He was stumbling, bumbling and grossly incompetent.”

Adding that

“If this doesn’t knock him out of the race, nothing will. Not so easy to do what I did!”

Billionaire activist Tom Steyer, a Democratic White House hopeful who did not qualify for the debate in Nevada, offered a surprising assessment Thursday of the winner: President Trump.

“Well, I saw the person who won the debate last night whose name is Donald Trump,” Steyer said.

“I saw so much bickering between Democratic candidates tearing each other down and going after each other and forgetting the fact that what really counts is beating Donald Trump in November of 2020. I saw people going after each other’s personality and records instead of remembering in fact the Democratic Party needs to win in November.”

Overall, as Robert Wenzel concludes, there was little in terms of substance. It was all about candidates sparring over details of various interventionist programs.

Perhaps it became most absurd when the six statists debated the so-called differences between socialism, communism and capitalism–as if they knew.

Bloomberg did not take it all lying down and some sense of rationality kicked in amid the hubbub…

“I can’t think of any way to get Americans to reelect Donald Trump than for them to listen to this conversation! This is absurd!”

That’s the most honest thing anyone said last night.

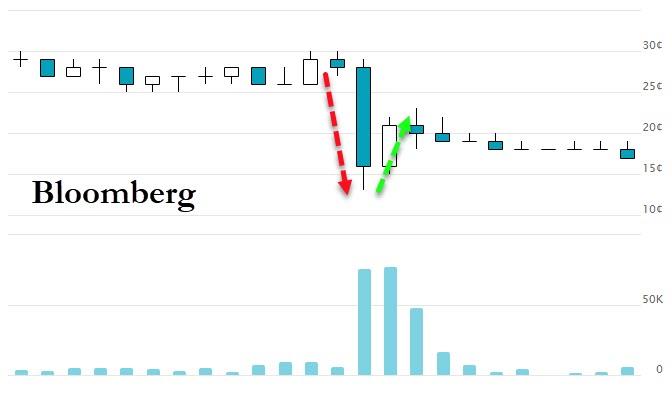

Epstein Mentor Les Wexner Leaves L Brands, Sells 55% Stake In Victoria’s Secret For $525 Million

Les Wexner is stepping down as chairman and CEO of L Brands as the company prepares to sell a 55% stake in its flagship brand, Victoria’s Secret, to private equity firm Sycamore Partners for $525 million, according to a pair of reports from Bloomberg and WSJ.

Wexner

Last month, we reported that Wexner, a longtime friend, benefactor and mentor to financier pedophile Jeffrey Epstein, was preparing to sell the company that he essentially built and led for decades.

Morgan Stanley Can’t Believe What’s Going On: “All Aboard The Crazy Train”

Submitted by Chris Metli, executive director in Quantitative Derivative Strategies at Morgan Stanley

All Aboard!

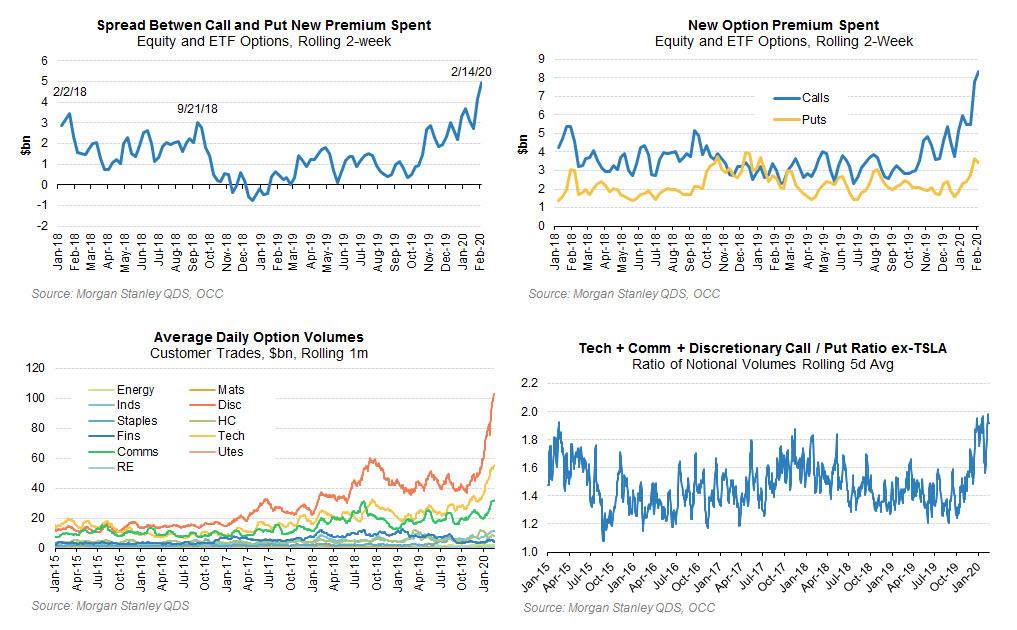

Fed ‘liquidity’ has powered the S&P 500 to a 16% gain since they announced Permanent Open Market Operations in October 2019, while the NDX is up a cool 26% (total returns). The rally makes sense in the context of a Fed that is continuing to print money until at least April, and beyond that likely continues to try to fight the structural forces of deflation with the only tool they have. But at the same time consensus is that the rally in Tech/Growth continues, and investors should be increasingly concerned with some of extremes being priced into markets.

The below is a non-exhaustive list of data points that highlight just how crazy some things have become. In this environment adding beta or Growth/Tech exposure carries too much risk in QDS’s view. Instead investors should consider rotating out of their most stretched single-stock positions and into call options (i.e. stock replace, keeping upside but limiting downside), or hedging the most vulnerable areas of the market – Crowded stocks (MSXXCRWD) or Growth vs Value (MSZZGRVL). See last week’s Factor Volatility is Here to Stay for details.

Turning to the data – first consider that breadth over the past six months has been the narrowest since at least 2005, with only 38% of S&P 500 constituents outperforming the index.

Low breadth has pushed the concentration of market cap within the S&P 500 to the highest level since at least 2005. US Strategist Mike Wilson has highlighted that the five largest companies are all Tech names and currently make up 18% of the S&P 500 market cap, but less than 14% of the total S&P 500 earnings (see US Equity Strategy Weekly Warm Up: Concentration Should Lead to Opportunities from Jan 13th 2020). Taking a broader measure of concentration (the HHI index = the sum of squared weights) shows that overall concentration of market cap is this highest since at least 2005. Even more extreme is the sector concentration, which has been steadily rising since 2019 but has gone parabolic in the past few months.

Options investors are not being left out either, with investors spending more premium buying new single-stocks calls over the last two weeks than at any point since at least January 2018. Note that previous peaks of new premium spend in calls versus puts were just before the Feb 2018 and Oct 2018 selloffs. Much of the activity in options has been in Tech, Communications, and Discretionary stocks (yes TSLA, but the increase in activity is broader than that), and the notional volume of calls relative to puts in these sectors has reached historical highs.

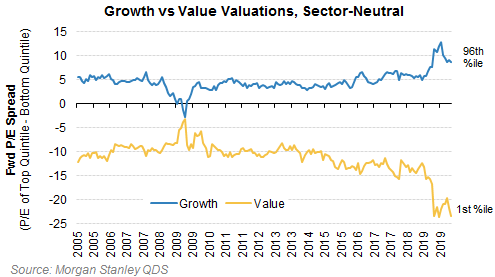

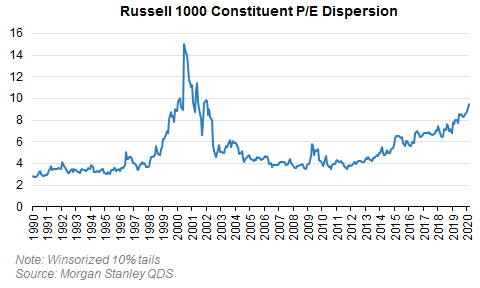

The outperformance of Growth versus Value is greater over the last 3 months than at any point since May 2008. This divergence in performance is pushing Growth versus Value valuations wider, and the dispersion in valuations across the Russell 1000 is now the highest since 2001.

Yes, the Tech bubble was worse on many metrics – Tech and Communications were over 35% of global market cap then versus just 25% now, and this bubble could keep growing. But the fact that the Tech bubble is increasingly becoming the relevant time period that people are comping to is in and of itself concerning…

This concentration in Tech and secular growth names reflect a continuation of the massive flight to quality on the back of expectations for middling economic growth but an easy Fed. There are signs of instability in the market (in particular regarding factor volatility and correlations – see QDS’s Factor Volatility is Here to Stay Feb 14th 2020) which means that the bar is lower for a violent unwind of crowded positioning. While most of the sector and factor themes are highly correlated (Growth vs Value, Large vs Small, Defensives vs Cyclicals, Winners vs Losers, etc), Growth vs Value (MSZZGRVL) and Crowded stocks (MSXXCRWD) are the most at risk in QDS’s view.

Dollar Roars, Futures Slide On Surge In New Virus Corona Cases In Japan, South Korea

S&P futures slipped, Asian stocks eased and European markets were a sea of red even as the relentless dollar juggernaut continued on Thursday, as virus cases rose in South Korea and Japan even as China added more stimulus via a rate cut to support its economy.

US equity futures first pushed higher reaching just shy of 3,400 before turning lower after Japan reported two deaths from passengers holed up on the formerly quarantined Diamond Princess viral cruise ship, with South Korea confirming its first fatality from the disease shortly after. China reported a large drop in new cases which was due to yet another change in the definition of “infection”, but that came together with a jump in infections in South Korea, two apparent deaths in Japan and researchers finding that the virus spreads more easily than previously believed

Corporate earnings also disappointed with ViacomCBS slipping in the premarket after its quarterly revenue missed estimates. Underwhelming results from AXA SA and Telefonica SA dragged the Stoxx Europe 600 Index lower. In Asia, stock gains in Shanghai, Tokyo and Sydney were countered by declines in the rest of the major markets.

European shares eased from record highs on Thursday, as a raft of disappointing earnings added to fears about the global impact of the coronavirus outbreak after research suggested it was more contagious than previously thought. The European Stoxx 600 dropped 0.3%, led by a 1.2% fall in insurance stocks after Swiss Re posted a lower-than-expected annual profit. The reinsurer’s shares dropped 4.2% to a two-week low. A 4.6% fall for Spain’s Telefonica weighed on the benchmark index after the telecoms group said one-off charges in Mexico and Argentina hurt its annual profit. The stock was also the biggest decliner on the Spanish bourse. Joining a growing list of companies to put a number on the impact from the coronavirus epidemic, Franco-Dutch airline Air France-KLM SA forecast an earnings hit of as much as 200 million euros ($216 million) by April. Its shares fell 6.5%.

Analysts said European equity investors were in a wait-and watch mode ahead of flash readings of the PMI on manufacturing activity in the euro zone, due on Friday. “You’ve got the manufacturing PMIs tomorrow, which is probably the most important figure this week because they may show the early impact of the coronavirus on demand and the supply chain,” said Connor Campbell, analyst at Spreadex.

Earlier in the session, MSCI’s broadest index of Asia-Pacific shares outside Japan fell 0.6%, led by falls of 0.8% on Hong Kong’s Hang Seng and South Korea’s KOSPI. Markets in the region were mixed, with the Shanghai Composite Index and Australia’s S&P/ASX 200 Index rising, while Thailand’s SET and South Korea’s Kospi index fell. Trading volume for the MSCI Asia Pacific Index members was 26% above the monthly average. In the latest news about the health emergency, South Korea reported its first death from the coronavirus, with infected patients doubling in one day. Japan confirmed two deaths from a quarantined cruise ship. The Topix gained 0.2%, with Yuki Gosei Kogyo and V-Cube rising the most. The Shanghai Composite Index rose 1.8% to an almost one-month high

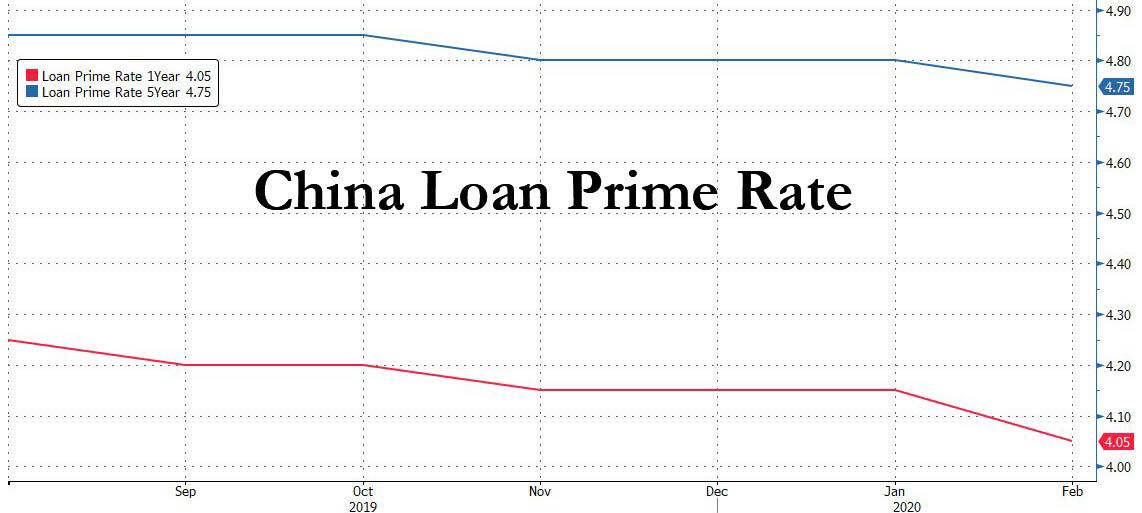

China cut its benchmark lending rate earlier on Thursday, as anticipated, with both the 1 and 5 Year LPR cut by 5 bps, adding to a slew of measures in recent weeks aimed at cushioning the virus’ impact on the economy.

That kept Chinese stocks supported, while Japan’s Nikkei advanced 1% as an overnight slide in the yen is a boon for exporters, though the mood was more nervous elsewhere.

“I think there’s a realisation that before we get all the stimulus measures that people have been frothing about, you’ve got to deal with a lot of companies that are finding themselves with impairment charges or indeed solvency problems,” said Sean Darby, global equity strategist at Jefferies in Hong Kong, before adding something we have been pounding the table on for the past month: “Markets have taken a step back because the authorities won’t do any major stimulus until they are completely sure the virus has stopped, because there’s no point in doing it when people are sitting at home.”

Bingo. If and when the algos figure this out, watch out below.

China had 394 new cases on Wednesday, the lowest since Jan. 23, after Beijing reversed an earlier, broader definition of “infection” to represent fewer cases and get people to get back to work; so far that approach has failed. More than 2,100 people have died from the coronavirus in China, with eight deaths in other countries but not including the two from the quarantined cruise ship in Japan.

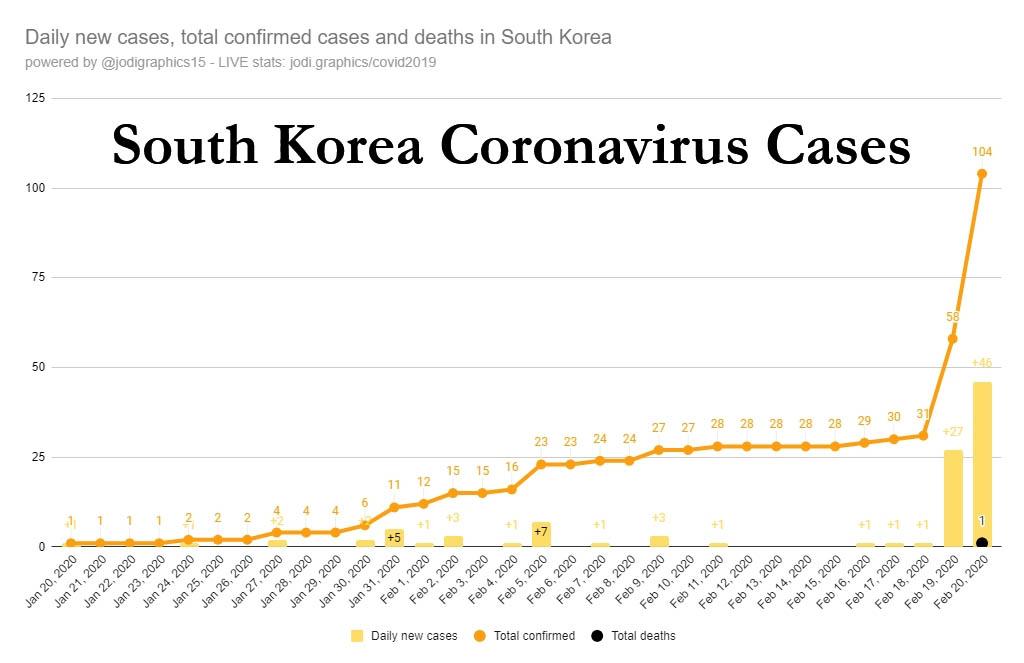

However, overnight the attention was not on China but rather its neighboring countries: South Korea’s government reported 31 new cases of coronavirus on Thursday, after a new outbreak traced to a church, bringing the number of people infected in the country to 104.

In Japan, where the government has come under intense criticism for its handling of an outbreak on a cruise ship carrying about 3,700 people, broadcaster NHK reported that two passengers in their 80s had died.

In FX, dollar’s strength climbed to the highest level in more than four months and the Swiss franc gained on haven bids while the yen extended its slump, weakening past 112 per dollar, with market participants ascribing a host of reasons, ranging from disappointing economic news to early positioning before the fiscal year-end next month.

The Yen plunged nearly 1.4% against the dollar, its sharpest fall in six months, and 2% against the Norwegian krone – its sharpest daily drop in almost three years. “Nearness to China and dependence on China have not helped the yen as a risk-off. We have seen the yen and gold diverging for a while and this may not be the end of it,” said Shafali Sachdev, head of FX in Asia at BNP Paribas Wealth Management. “The kind of classic correlations between U.S. yields and the yen, those have been kind of breaking down…we need to see past this virus situation to see whether the yen will regain its safe-haven status.” The skittish mood had investors punishing the Australian dollar, sending it down 0.6% to an 11-year low of $0.6633 after a surprise rise in unemployment.

The flight to safety was observed across most assets, with treasuries and European higher and gold surging to a seven-year high.

Elsewhere, oil prices added to overnight gains while gold loitered around $1,609 per ounce. U.S. crude last sat 25 cents firmer at $53.54 per barrel and Brent added 16 cents to $59.28.

Economic data include initial jobless claims, Philadelphia Fed survey. The Southern Company, Newmont and Hormel Foods are due to report earnings

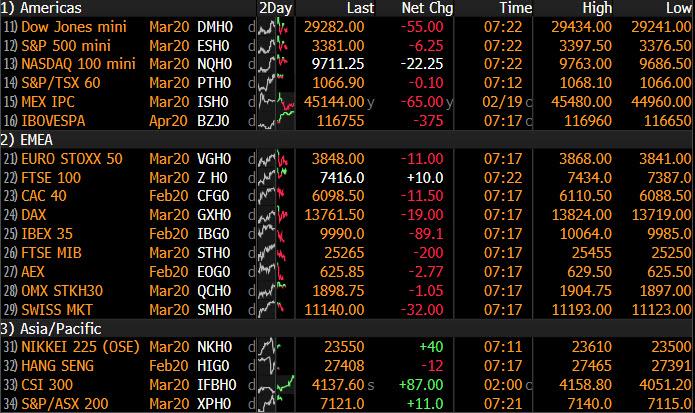

Market Snapshot

S&P 500 futures down 0.1% to 3,385.25

STOXX Europe 600 down 0.3% to 432.58

MXAP down 0.5% to 167.59

MXAPJ down 0.5% to 551.21

Nikkei up 0.3% to 23,479.15

Topix up 0.2% to 1,674.48

Hang Seng Index down 0.2% to 27,609.16

Shanghai Composite up 1.8% to 3,030.15

Sensex down 0.4% to 41,157.48

Australia S&P/ASX 200 up 0.3% to 7,162.49

Kospi down 0.7% to 2,195.50

German 10Y yield fell 0.4 bps to -0.422%

Euro down 0.02% to $1.0803

Brent Futures up 0.07% to $59.16/bbl

Italian 10Y yield rose 2.2 bps to 0.787%

Spanish 10Y yield fell 1.2 bps to 0.259%

Brent Futures up 0.1% to $59.18/bbl

Gold spot down 0.1% to $1,610.13

U.S. Dollar Index little changed at 99.71

Top Overnight News

The global death toll climbed to 2,129 and the number of confirmed cases reached 75,730. Hubei province reported a sharp drop in new cases after another change in the way China diagnoses infections, raising questions over the reliability of the data

U.K. retail sales jumped the most in almost two years in January, ending the worst run for British stores on record and adding to signs of an economic rebound. Sales excluding auto fuel rose 1.6% from December, the biggest increase since May 2018. Economists were expecting a rise of 0.8%.

The bond market is signaling approval of U.K. Prime Minister Boris Johnson’s planned spending spree. With the March 11 budget looming into view, the average cost of government borrowing is close to the lowest levels on record

The world’s largest container shipping company, is positioning itself for a strong rebound in two months, based on an expectation that the fallout of the coronavirus on global trade may soon peak

Indonesia’s central bank cut its benchmark interest rate by 25 basis points to 4.75% after a three-month pause as the spread of the coronavirus threatens growth in Southeast Asia’s biggest economy

Asian equity markets traded mixed having pared a bulk of earlier gains despite the promising lead from Wall Street which saw the S&P 500 and Nasdaq print fresh record highs. The optimistic sentiment in the region faded following the number of coronavirus cases in South Korea rising by 60%, and amid reports of two deaths from the Japanese cruise ship. Nonetheless, ASX 200 (+0.3%) was buoyed by its large-cap mining and energy sector, following recent gains in the respective complexes. Nikkei 225 (+0.4%) initially posted gains of over 1.5% with upside originally fuelled by a considerably weaker JPY, although the index later pulled back with a chunk of its transport stocks in the red, and amid reports that multinational companies are avoiding travel to and from Japan over fears that the country will be the next hotspot in the outbreak. Elsewhere, Hang Seng (-0.9%) erased opening gains and underperformed as a bulk of its stocks reversed course into negative territory, and with its heavyweight financial sector on the defensive. Meanwhile, Shanghai Comp (+1.0%) rebounded with a vengeance in late trade and topped the 3000 mark for the first time since before the Lunar New Year, after initially swinging between gains and losses despite the expected stimulus measures by the PBoC, as traders were cautious following the case jump in South Korea and deaths on the cruise ship off Yokohama, with the former prompting South Korea’s KOSPI (-0.5%) to trade with losses of almost 1.0% at one point.

Top Asian News

China Nears Takeover of Troubled HNA as Virus Rocks Economy

7- Eleven Owner Said in Exclusive Talks for Marathon’s Speedway

Ping An Insurance Full Year Net Income Misses Estimates

Vietnam to Order Loan Interest Rate Cuts for Virus-Hit Companies

European indices kicked the session off on a relatively directionless footing before seeing modest downticks amid increased fears over the spread of coronavirus outside of China. Focus in recent trade has been placed upon developments in Japan and South Korea with the former reporting two passenger deaths abord the Diamond Princess cruise ship off the coast of Yokohama, whilst the latter announced a marked pickup in coronavirus cases (total now stands at 104 vs. Prev. 51) and its first death. Sectoral performance has been a mixed bag thus far with price action largely dictated by a slew of large cap earnings, which has seen Telefonica (-5.7%), act as a drag on the Telecom sector following disappointing 2019 profit metrics. Elsewhere, to the upside, post-earnings, Smith & Nephew (+8.5%), Schneider Electric (+5.2%), Fresenius Medical (+4.2%), Fresenius SE (+4.2%), Maersk (+3.7%), Lloyds (+3.3%), Bouygues (+2.7%) and BAE Systems (+2.5%) lead the charge for the Stoxx 600. To the downside, Air France (-8.9%), disappointing earnings release has hampered other airline names, including Deutsche Lufthansa (-3.2%) and RyanAir (-1.8%), whilst corporate updates from Swiss Re (-4.9%) and Axa (-3.0%) has triggered losses in their respective shares.

Top European News

Irish Lawmakers Begin Search For PM After Sinn Fein Surge

Maersk CEO Predicts ‘Sharp’ Rebound After Coronavirus Peaks

Britons Return to the Stores After Johnson Election Victory

Death of Bond Vigilantes Clears Path for U.K. Fiscal Splurge

In FX, USD began the session on a firmer footing once again after taking out overnight highs of 99.778 to print a session high thus far of 99.875. Once again, there has been little in the way of fresh fundamental catalysts behind the USD move with gains instead largely as a result of weakness elsewhere, namely the JPY. Early doors in Europe, USD/JPY took out the overnight high of 111.59 before taking out 112.00 to the upside (current high of 112.18), which could open up a test of the April 26th high at 112.40. Explanations for the JPY have varied with some leaning on the traditional arguments of selling of JPY by Japanese pension planners to buy US assets; however, others favour focusing on recent disappointing data prints for Japan (Monday’s GDP figures) and concerns over the ramifications of the coronavirus for the nation, something which could impair the Tokyo Olympics this summer. If JPY declines continue to accelerate, 100.00 in the DXY looks a reasonable bet, with 100.50 marking the April 18th 2017 high.

EUR – Price action for the shared currency has largely been dictated by the “King USD” after gains in the greenback knocked the pair below yesterday’s low of 1.0782, with the session trough at 1.0778 (gap support from April 2017) at the time of writing. Should the EUR continue to fall victim to the USD, technicians’ eye 1.0761 which was the 20th April 2017 high, with not much in the way of support until the 1.0700 figure. From a fundamental perspective, the main highlight on today’s docket from the Eurozone comes via the minutes from the January ECB meeting (full preview available via the research suite of the website). That said, participants are unlikely to glean too much in the way of fresh insight from the Bank with the meeting itself providing little in the way of fireworks as policymakers tread water ahead of the upcoming strategic review. Furthermore, greater policy guidance from the ECB since the meeting has come from commentary via President Lagarde who noted that low interest rates and low inflation have significantly reduced the scope for the ECB and other central banks to ease monetary policy in the face of an economic downturn.

GBP – Momentum for GBP early doors was driven by the pick-up in the USD before the pound dug in and reclaimed 1.2900 to the upside after printing a low of 1.2874, just above the multi-week low of 1.2873 seen on February 10th. Sentiment for the GBP was also bolstered by encouraging retail sales metrics, with all four metrics exceeding expectations amid a pickup in clothing and footwear sales, helping to add to the evidence-pile for those championing the so-called “Boris-bounce”. That said, gains for GBP were relatively fleeting with perhaps some in the market apprehensive amid simmering tensions between the UK and EU this week ahead of upcoming trade negotiations at the beginning of next month.

AUD/NZD – Focus for the antipodes has largely fallen on AUD given overnight employment figures which saw modest downside in AUD/USD upon the release despite the headline employment change topping estimates (led by full-time employment), as the unemployment rate rose more than expectations, although money market pricing for a March RBA rate cut was largely unchanged. AUD went on to take out stops at 0.6650 before printing an eventual low at 0.6623 (10yr low!); note there is a large AUD 2.1bln expiry in AUD/USD at 0.6700. NZD has also been weighed on during the APAC and EU session in sympathy with Aussie losses with the NZD/USD pair being dragged from just shy of 0.6400 to take out 0.6350 to the downside and print a low of 0.6335.

CNY/KRW/TRY/ZAR – USD/CNH saw little action on the expected PBoC LPR rate reductions, although the pair saw upside amid a firmer Dollar, and stabilised ~7.0300. China has continued to reassure the market over the fallout of the coronavirus with the Commerce Ministry stating they will roll out targeted support measures in a timely way to mitigate the impact on firms and consumption. However, some in the market have raised concern over newly revised guidelines by Chinese authorities in classifying coronavirus designations, something which could potentially obfuscate matters further. On the coronavirus footing, USD/KRW rose from ~1191.00 and breached mild resistance at 1198.40 (3rd Feb high) before eclipsing 1200.00 to the upside during the APAC session amid increased coronavirus cases in South Korea. Elsewhere, overnight, TRY experienced a spiker higher amid thinned volumes and alongside broad EM FX weakness, USD/TRY immediately rose from ~6.0800 to levels north of 6.1000 before completely paring the move to reside on a 6.09 handle. Finally, ZAR has seen some softness relative to EM peers amid an announcement from ESKOM that rolling blackouts will be impose in South Africa from today until Saturday, something that will act as a further drag on activity ahead of next week’s budget announcement.

In commodities, WTI and Brent prices are essentially unchanged on the day with less that USD 0.15/bbl of variation from flat at present. Newsflow specific to the complex has been slow for much of the session, with price action initially moving in tandem with the overall risk picture as main equity bourses are similarly little moved overall. Focus overnight was on the ongoing demand concerns stemming from the coronavirus, with reports this morning of a death in South Korea prompting some mild weakness; as well as the private crude inventories which printed a larger than expected headline build. Although, the internals did feature surprise/bigger draws for gasoline and distillates respectively. As we await Russia’s stance on the JTC’s recommendations interest was piqued by remarks from Energy Minister Novak but to no avail on the production cut recommendations; although, he did firmly push back on the need for an early meeting which, alongside the short proximity to the original March date, means a early meeting is all but off the table. Looking ahead, today sees the release of the EIA weekly crude report at the slightly later time of 16:00GMT/11:00EST; expectations are for a build of 2.49mln which would be just over half of the API’s 4.2mln build last night; while internal estimates are in proximity to those forecast for last nights numbers. Moving to metals, where spot gold is currently little changed but is comfortably above the USD 1600/oz mark, with a YTD high of USD 1612.93/oz yesterday which takes us back to levels not seen since 2013

US Event Calendar

8:30am: Philadelphia Fed Business Outlook, est. 11, prior 17

8:30am: Initial Jobless Claims, est. 210,000, prior 205,000; Continuing Claims, est. 1.72m, prior 1.7m

Back from a 2-day trip to Madrid and a bit upset that in the season that Liverpool potentially break all records for winning streaks and points accumulation, I go to watch a game they lose! Thankfully there is a second leg. I got home last night to a daughter screaming due to a 39.2C temperature and a frazzled wife with tonsillitis who in half term has had to look after all three terrors without help due to our nanny being bed bound and at home in her last week. It’s fair to say my wife wasn’t particularly interested in me going through how sad I was that Liverpool had lost the night before and where they could improve for the second leg.

Talking of bruising encounters, the Democratic nomination debate in Nevada has just finished. This was the first featuring Mr Bloomberg and it’s fair to say that he had to absorb a large amount of attacks from the other candidates on his past record as Mayor of New York and lack of Democratic credentials. Predictit’s odds on Bloomberg winning the nomination fell from 29% to 16% at one point during the course of the debate, with no one candidate gaining particularly from that decline. The former mayor is not on the ballot in Nevada on Saturday so we will have to wait to hear from voters on Bloomberg. It will be interesting to see if there is any hit to his polling, because it is likely that – given the amount of money he has spent on TV ads already – many more Super Tuesday voters are likely to see his ads than have watched last night. Bloomberg has already spent more on the first few months of his 2020 presidential campaign than former President Barack Obama did on his entire 2012 bid.

Staying with overnight news, Asian markets are seeing a little increase in concerns about the coronavirus as 2 people from the quarantined ship died in Japan and South Korea reported another 31 confirmed cases thereby raising worries over the spread of the virus outside China. However, China’s Hubei province reported the smallest increase in confirmed cases (349) in recent times but it has to be interpreted with some caution as it came on the back of another change in the counting methodology. Total deaths in China now stand at 2,118 with confirmed cases at 74,576.

On a related note, the PBoC continued with its easing measures to support the Chinese economy by lowering the 1yr loan prime rate to 4.05% from 4.15% previously and the 5yr loan prime rate to 4.75% from 4.80%. On a more micro level, Qantas Airways said overnight that it is slashing capacity on international flights to China, Hong Kong, Singapore, Japan and Thailand by 15% and freezing recruitment as the coronavirus drives down travel demand. It added that the reductions will remain in effect until at least the end of May.

A quick refresh of our screens shows that markets are trading mixed this morning with the Nikkei (+0.38%) and Shanghai Comp (+0.75%) up while the Hang Seng (-0.69%) and Kospi (-0.47%) are down. However, the Nikkei is off its early highs of as much as +1.73% on the news of the 2 deaths mentioned above. Elsewhere, futures on the S&P 500 are down -0.14% and yields on 10yr USTs are down -1.3bps.

This comes after normal service resumed in markets yesterday with US equities back to hitting new all-time highs after shrugging off the Apple Q1 revenue warning. The S&P 500 finished +0.47% higher last night while the NASDAQ rallied to the tune of +0.87% and is only 1.86% away from 10,000 and a landmark that will be sure to get a lot of press. In fact it was a very strong day for tech with semiconductor stocks up +2.57% – the sixth gain of at least 2% this year – with the NYSE FANG index up +2.33% for its seventh consecutive daily gain. Apple, Amazon and Google now have a combined market cap of $3.54tn – nearly half a trillion more than the CAC and DAX combined.

It’s not just the US that is getting its turn in the spotlight though. The STOXX 600 yesterday closed at a new record high following a +0.83% gain. The MSCI EM index is also up +5.08% from the recent lows and within 12% of the all-time highs. What’s curious about all this though is that Gold continues to rise – up +0.63% yesterday (+6.22% YTD) finishing at the highest level in USD terms since March 2013 – and the yield curve continues to flatten with 2s10s down -0.7bps to +13.8bps and to the flattest level since November. 30y Treasuries are also trading only a shade above 2% and are down -37.7bps this year already.

So risk on and many safe havens performing well. China stimulus stories appeared to provide the sufficient ammo risk needed yesterday with an HNA nationalisation story in the early afternoon probably the most interesting. Indeed Bloomberg reported that the government of Hainan is in talks to take control of HNA with the core airline assets to be potentially sold off to other local companies. It’s possible that we get an update very soon. So, clearly the bail-out is a near term positive but it does highlight some of the stresses and leverage in China’s financial system and economy.

Back to yesterday, where European bonds generally rallied (Bunds -1.1bps) but with BTPs the exception (+2.2bps) possibly partly on news that global investors sold EU3.8b of Italian bonds and bills in December, in the latest data from the European Central Bank. Treasuries yields climbed slightly by +0.03bps to 1.564%. Credit also continued to tighten. Renault bonds were weaker however after the car maker was another to fall victim to a ratings downgrade, pushing bonds into fallen angel territory. Indeed Renault’s near EUR5bn of bonds will enter EUR HY indices next month and will immediately become a top 10 issuer making up just shy of 2% of the index.

The FOMC released the recent January meeting minutes yesterday, and there was little new news. There was no discussion of the impact of the coronavirus and the Committee mostly stayed on message that policy remains appropriate barring a material reassessment. Officials like Chair Powell have been saying that it’s still too early to assess the impact and the minutes indicate that was certainly true in Jan. On inflation targeting, the Committee discussions seemed to lean against adopting a symmetric inflation range so as to not convey being comfortable with below average inflation. The balance sheet was the other major topic, with repo operations planned through April though gradually reduced through that time.

In other news, trade headlines were a focal point again yesterday with EU trade chief Hogan telling EU lawmakers that work on a revised trade truce will go on for the next few weeks. It’s worth noting that headlines in recent weeks had suggested that talks had centered on a mini deal so a move to a truce is perhaps more realistic. Our economists yesterday made the point that the biggest obstacle appears to be the US demanding that the EU gives way on agriculture. This has been a focus not only for Trump but also Congress. The question then becomes – are there enough low hanging fruit on food/agriculture (previously EU agreed to take more soya and beef imports from US) that can make the US happy to do a mini deal while not crossing the bigger red lines that the EU has on agriculture.

Elsewhere, all the data in the US was by and large better than expected. That was particularly the case for the housing data where January housing starts declined a lot less than expected (-3.6% mom vs. -11.2% expected) while permits surged +9.2% mom (vs. +2.1% expected). That’s a post crisis high for permits now with upward revisions to the prior month also included, however it’s likely that the warm weather has been a big driver. As for PPI, the headline and core ex food and energy readings both rose +0.5% mom, exceeding expectations for +0.1% and +0.2% respectively. Significantly, the health care component which feeds into PCE was strong also, rising +0.4% mom.

In the UK the latest inflation data was slightly higher than expected. The January core reading rose two-tenths to +1.6% yoy while the headline rose to +1.8% yoy (vs. +1.6% expected). Measures of RPI and PPI also rose. While the tick higher for core CPI will have been of some comfort it’s worth noting that the latest print is still a tenth below the BoE’s estimate for January. A reminder that today and tomorrow we get retail sales data and the latest PMIs in the UK, however so far the data has shown signs of improvement since the election. Sterling was weaker yesterday nonetheless, falling -0.60%.

Finally before the day ahead Craig Nicol, Credit Strategist and a member on my team, has just gone live with a podcast called ‘Green Bonds – Increasingly Relevant in the Corporate Bond Market. The podcast is based on a report Craig published earlier this month (link here) exploring the stratospheric growth of the green bond market. Listen on http://www.dbresearch.com/podzept/ or subscribe on iTunes, Apple Podcasts, Spotify.

Looking at the day ahead, this morning data due out in Europe includes March consumer confidence in Germany, January CPI in France and January retail sales in the UK. The February CBI survey for orders and selling prices is also due out in the UK. This afternoon we’ll also get February consumer confidence for the Euro Area while in the US the only data due is the February Philly Fed index, weekly jobless claims and January leading index. Away from the data the Fed’s Barkin and ECB’s Guindos are due to speak while the ECB’s minutes from the last policy meeting are also due. Worth watching also is the EU leaders meeting where the EU budget is due to be negotiated.

Morgan Stanley Is Buying E-Trade For $13 Billion, Outmaneuvers Archrival Goldman With Pivot To Retail

Tired of being outmaneuvered by its formidable longtime rival, Goldman Sachs, Morgan Stanley has epically one-upped the Vampire Squid with a deal to buy E*Trade Financial Corp. in what would be the largest takeover by major US bank since the financial crisis, and firmly stake MS’s future on managing money for retail customers.

The $13 billion takeover price offered by MS is a 30% premium to E*Trade’s Wednesday close.

Goldman pivoted toward retail a few years ago when it became a regulated retail bank and launched its “Marcus” retail-banking platform, and its even more infamous partnership with Apple for its ‘Apple credit card’, though analysts say the bank’s foray into the new business line has been rocky at times.

According to Japanese government officials, both of the virus-related fatalities were Japanese citizens in their 80s who had been moved off the ship more than a week ago for treatment in a Japanese hospital.

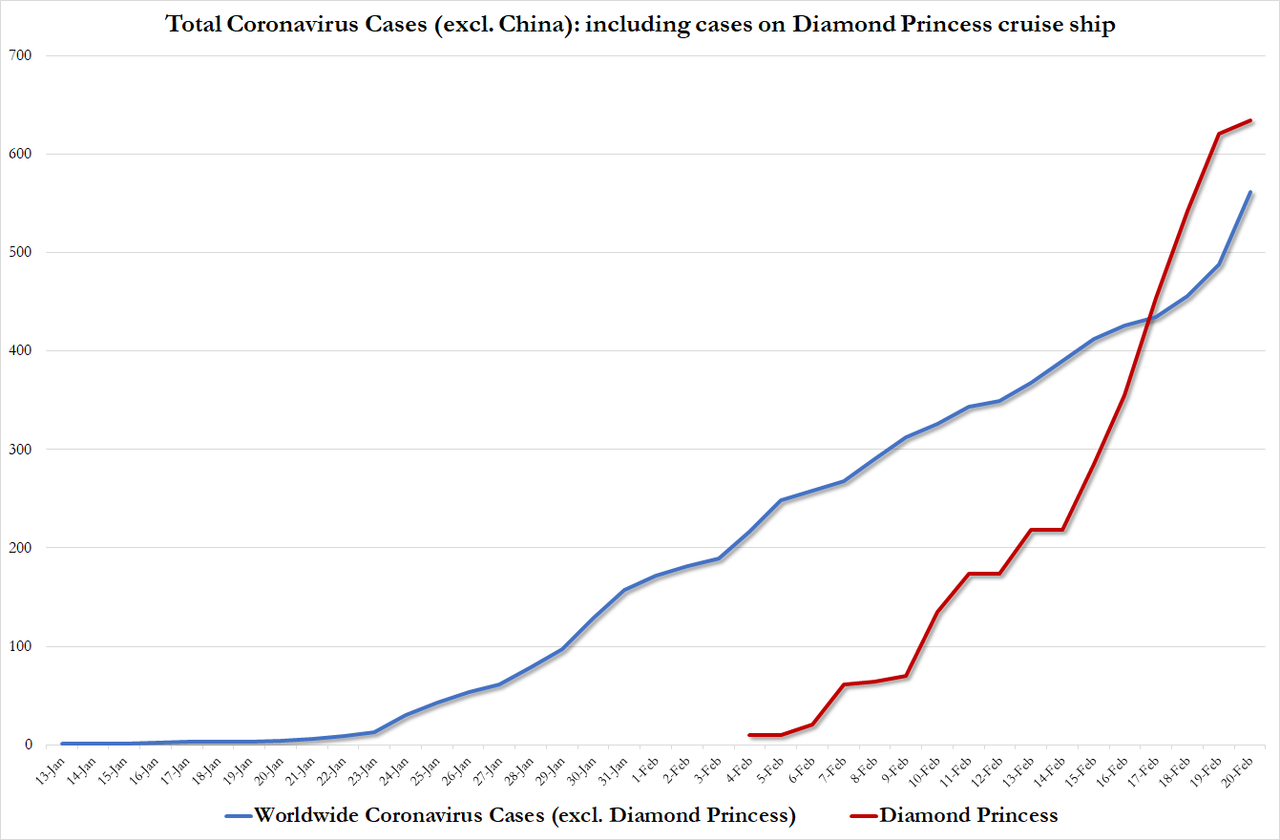

The latest reports Thursday morning confirmed another 13 cases aboard the DP bringing the total to 634. The odds that individuals being released from the 2 week quarantine on Thursday and Friday might have contracted the virus, but have yet to show symptoms, remains high. The death in South Korea raised the death toll ex-China to 10.

Even as President Xi does everything in his power to present an image of success to the Chinese people – in his speeches, he claims the Chinese government’s strict quarantines have been an unmitigated success – global experts, including the WHO, have warned that the disease will continue to spread globally, and that the end of this crisis is still far from certain.

And as new confirmed cases dropped substantially on Wednesday in Hubei, everywhere else, the rate of new infections is accelerating.

In South Korea, the number of cases soared by almost two-thirds to 104 overnight, further emphasizing our observation that the number of cases ex-China has started to accelerate notably as the curve starts to resemble an exponential progression.

One WHO health expert told a Japanese TV station on Thursday that the virus is “a moving target” making it difficult to collect information and treat people: “Nobody has ever had to deal with this situation before, this is a new virus on a ship with 4,000 people, there are no guidelines for that.” He added that he suspects there was a substantial amount of transmission before it arrived in Yokohama, adding that it was “not possible” to isolate everybody individually.

The WHO senior epidemiologist was responding to claims made by another expert in infectious disease that the Japanese had failed to observer proper quarantine protocols.

Back in Korea, the mayor of Daegu, a city of 2.5 million where 10 South Koreans contracted the disease from a church service, asked residents to stay indoors. Iran also reported two infected that then died.

Experts suspect that one woman in Daegu may have infected at least 40 others by going to her Christian church, according to Yonhap. The alleged ‘superspreader’ is the reason for the huge jump in new cases on Thursday. Experts say the city is now facing an “unprecedented crisis” following the spike in cases.

Cases are also surging in Singapore, where Deutsche Bank confirmed that an employee in its Singapore office had contracted the virus.

Adding to its woes, Iran reported three new cases on Thursday a day after it confirmed two virus-related deaths in the city of Qoms.

Warnings about the virus’s economic blowback are increasing, as Goldman said Thursday that stocks aren’t completely pricing in the risks from the virus.

Meanwhile, Air France-KLM, Qantas, and the global container shipping giant Maersk became the latest companies to warn about the financial impact from the continued spread of the coronavirus.

As President Xi balances the risks to tens of thousands of lives on one hand, and keeping his promise to double the size of China’s economy by 2020 on the other, it seems the leadership in Beijing are beginning to believe their own propaganda. Premier Li Keqiang, Xi’s No. 2 who is in charge of the committee managing the crisis, local governments should seek to increase the rate of resumed production and work, according to China Central Television.

Put another way: Come on in, the water’s fine, and if you get the virus and die, we’ll cremate your body and tell your family you died of “pneumonia”.

The spate of deaths rattled investors overnight, and US equity futures are pointing to a lower open on Thursday, and a rush of risk-off trading in Asia has pushed the BBG dollar index to a 4-month high following the latest piece of evidence that the coronavirus isn’t simply “another flu”.

Macron Ends Unsupervised Imam Program Over Risk Of ‘Separatism’

With Emmanuel Macron’s popularity in freefall and his allies taking hits, the French President has yet again attempted to appease France’s growing populist movement – announcing on Tuesday that he would end a program which allowed foreign countries to send imams and other religious teachers in order to crack down on “separatism.”

“The problem is when in the name of a religion, some want to separate themselves from the Republic and therefore not respect its laws,” said Macron, speaking from the eastern French city of Mullhouse, adding that his government would combat “foreign interference” in how Islam is practiced – as well as how its religious institutions are organized within the country, according to France 24.

Of note, France is home to Europe’s largest Muslim community – estimated at around 6 million, or 8% of the population. The country has long sought to assimilate Muslim nationals and residents.

Macron said he plans to end a programme created in 1977 that allowed nine countries to send imams and teachers to France to provide foreign language and culture classes without any supervision from French authorities.

Four majority-Muslim countries – Algeria, Tunisia, Morocco and Turkey – were involved in the programme, which reaches about 80,000 students every year. Around 300 imams were sent to France every year by these countries, and that those who arrived in 2020 would be the last to arrive in such numbers, said Macron. –France 24

Macron’s government has asked the French Muslim Council (CFCM) – which represents Islam in France – to find solutions to train Imams on French soil in order to ensure that they can speak French and do not spread radical Islamist views.

The announcement comes less than a month before municipal elections in France – suggesting that perhaps Macron is simply pandering to angry French citizens by adopting his political opponents’ nationalism.

The measures were part of a much-anticipated intervention less than a month before municipal elections in France. Macron’s speech came at the end of a visit to Mulhouse, home to a large Muslim community that has been the focus of the French government’s campaign against Islamism.

The new rules were intended to counter Islamic extremism in France by giving the government more authority over the schooling of children, the financing of mosques and the training of imams, said Macron. –France 24

“This end to the consular Islam system is extremely important to curb foreign influence and make sure everybody respects the laws of the republic,” said Macron.

“We cannot have Turkey’s laws on France’s ground. No way,” Macron added.

According to the report, Turkey runs a “vast network of mosques inside the country and abroad under the powerful Diyanet, or Directorate of Religious Affairs,” which President Recep Tayyip Erdogan has received a significant boost in funding – to the point where critics accused Ankara of using it as a foreign policy tool in order to extend Turkey’s soft power.

In recent years, France has suffered a spate of radical Islamic terror attacks. In November of 2015, Muslim terrorists attacked the Bataclan theater and other sites, killing 130 people in the deadliest attacks since WWII. Most of the attackers were French or Belgian nationals who were indoctrinated into radical Islam while in Turkey before traveling to Iraq and Syria to fight with ISIS.

We set up a ‘brain trust’ in the Cafe in order to write a combined sitrep for The Saker Blog about the Coronavirus. The new name in the taxonomy is COVID-19 but let’s stick to Novel Coronavirus for now. It is of course too early to come to any conclusions, but we can start isolating the discernible high level trends and perhaps get an early glimpse as to what effect the outbreak may have geopolitically and economically, although it is very early days.

We will not attempt to look at the technical picture here – the numbers of recoveries, the death rates and the infection rates, rates of transmission, life of virus on surfaces and so on because the technical picture is not yet clear and all data is in a state of flux with opposing and inconsistent reports from all sides. One cannot expect otherwise as the world is still shooting at a rapidly moving target in terms of statistical ground and epidemiological analysis.

In addition, we have professional organizations like the WHO and the CDC not really in lockstep and giving different pronouncements on a professional level. It is too early to draw conclusions.

What people are saying:

Let us look for a moment as to what ‘people are saying’.

(If you want to end up deeply into conspiracies, I would suggest you go to subReddits /r/Coronavirus and /r/China_Flu )

What ‘people are saying’ runs the gamut from messages received in meditation, prayer, even channeling, and this information is being put out there as valid for everyone else in the face of no definitive information you can hang your hat on.

Every talking head on youtube has suddenly turned into an expert, both on China and on the Novel Coronavirus. Every uninformed blockhead has now turned into a specialist. Every Twitter feed out there now considers itself an insta-influencer.

Most of the western alternative news medias have suddenly decided to follow their governmental lead on China, and the message is overwhelmingly that Brutal China is indeed very Brutal and very Bad.

China is attacking her own people to reduce population

Lab Accidents happen. (this is of course a pragmatic view, but usually Level 4 laboratories are situated very far away from the center of busy cities).

Wuhan was on the point of massive riots, Hong Kong Style against their government

The Chinese government is lying and not reporting correctly. The death rate is much higher.

The Chinese Defense Forces are riddled with virus infected soldiers, and they are being contained somewhere else. There is no information on this excepting wild speculation.

Every non-flattering video from China is being passed along salaciously; usually grainy and one cannot really figure out where it is from – no markings, road signs, store names or anything where anything can be identified. The scuttlebut is that these mostly security camera videos and actively distributed by Falun Gong. Your guess on this is as good as mine.

As you can see from this list, and it is by no means exhaustive, all over the show, and there are literally 10’s more of these

What the timing indicates

The timing is suspicious no matter how you look at it.

Manufacturing usually shuts down or goes slow over Chinese New Year / Spring Festival which can last as much as 15 days. So, economically, this was a good time for a virus (if China ‘did it’).

On the other hand, this holiday gives rise to the greatest migration of people on our planet which also makes it an ideal time to infect a population (if someone outside of China ‘did it’).

The timing so close to the signing of the of the US/China Phase I Trade Agreement, which the Chinese referred to as only a ‘cease fire’ in the trade war, and the US referred to as a great breakthrough, is suspicious. The Chinese were indicating that they are very hesitant to even go to a phase II negotiation. And of course, there is a black part of the actual agreement that we do not know about.

The Main Tropes

1. The main trope out there is that this is a bioengineered bioweapon. But right at that point opinions diverge so widely that one can only ask questions, and not conclude anything.

2. The second trope is that people are being arrested widely. We’ve seen reports of arrests in Canada and in the US, and out of Harvard. Here is but one.

3. The third trope is that China is “The Sick Man”, and we hate them for dumping this virus on the rest of us. Let me just say that the level of invective against China is not only unprecedented, it is also suspicious. Rebranding of the Coronoa Virus to the Chinese Virus is proceeding apace, even though it has a formal name now – COVID-19. In my life I have never seen such an overt manipulation of the common headspace such as this, since ‘weapons of mass destruction’.

4. The fourth trope is that the US, on a public and governmental basis has decided to vilify China, correctly or incorrectly. Note Mr Pompeo. Is he only taking an opportunity that is presented to him, or does he know more than what we think?

5. The fifth trope is that the civilizational fear against China is suddenly out in the open for everyone to see. It is almost a morphic resonance of fear expressed against China and that China is the culprit. However, we don’t really know who the culprit is actually. We don’t even know if there is a culprit.

Is China the culprit, or is China the victim, or is this a virus that spread from animal to human or has it escaped from some or other lab by accident (or on purpose)? We do not know any of this and this trope just creates more FUD (fear, uncertainty and doubt).

6. The sixth trope is that China is wrong no matter what she does. Quarantine and even forced quarantine is expressed by the blockheads of Brutal China Cracking Down on Their People, without thinking what is actually necessary to do for this kind of outbreak, no matter where it comes from. One after the other video supposedly from China showing the so-called Brutal Chinese government is distributed with relish, with nary a thought that you and I are actually being protected by these heavy handed tactics. The snoflakes are out in force talking about human rights, yet, by the looks of things, China is going all out protecting the many.

Because there is a strange consistency in what the State (used generally) says, and what the alternative media says, this is more worrying than anything else. On the one hand nobody can believe the State, and on the other hand alternative media is reproducing and disseminating the message of the State.

7. The seventh trope is that the few voices, even here on The Saker Blog, that try to look at this realistically are drowned out in the general societal willingness to believe the worst. Viva free speech!?!

The formal state, and the western alternative media are generally in lockstep on this issue.

China is now attempting to go back to work. We do not know how successful this is, but some are trying to measure the actual air pollution to try and figure out if China has gone back to work, or not. Economically China has also given guidance to business, saying that this event is a force majeure, known colloquially in contractual terms as ‘an act of God’, and therefore they can renegotiate contracts, delivery dates and completion.

Let us look at what is clear.

China is fighting for its life. The death-toll or even containment is not truly visible in any numbers as yet. This will have tremendous impact on supply lines and not only on China’s economy, but all parts of the international supply chain, upstream and downstream. China is acting on expressed unhappiness of their people. They are firing those who do not perform, who put red-tape in the path of directly fighting this virus. It may look brutal to lock people into their homes, but how many do they save by this action? Where do these get food? It is in the Chinese media that food gets delivered. This is something that the western youtube pundits (and their a-hole brothers) forget to report, although this is open and publicized in the Chinese media.

This is a catastrophe. It is not a flu, it is not a common cold, it is not something that 5G brought onto China, it is not God punishing the Godless red commies. Whatever it is, it is a catastrophe with world-wide consequences. We do not know enough to come to any meaningful conclusions except to say that considering the timeline, we are right to be suspicious and we may be right to prepare with the basic masks, gloves and limited public exposure, i.e., not visiting large gatherings, for a period of time.

If this virus continues, it will have societal impact that may be severe – we won’t shake hands, we won’t hug babies, social interaction will be vastly compromised, and a few more common contact methods like music concerts or sporting activies for humans will be left by the wayside.

If it continues much beyond the current level, the extensive economic fallout cannot be estimated. You and I and no analyst in the world can truly get their arms around the economic fallout and the breakdown of worldwide supply chains. Who knows, we may be out of a specific little part for a normal service of a vehicle, we may be out of medicines (the idea of the many people that are taking anti-depressants and such types of medicines having to go cold-turkey is quite scary, and there may be a severe shortage of simple medical equipment, like masks and gloves that are even now getting hard to source – just try buying masks on Amazon).

In the current analysis and according to what we have available, we do not yet know enough to be meaningful. Much more than that is pure speculation and gives rise to other agendas being seeded into the public narrative.

What is clear, is that fear, uncertainty, and doubt is rife and people are terrified…

Credit Suisse MD Dies In Freak Accident After Slipping Through Chairlift And Being Suffocated By His Own Jacket

Almost exactly 10 years ago, we detailed the tragic death of Gerard Reilly in a skiing accident – the point man on Repo 105, the point person for E&Y’s “investigation” into the Matthew Lee whistleblower campaign, Lehman’s Level 2 and Level 3 asset valuation, the brain behind the idea to spin off Lehman’s commercial real estate business, Lehman’s Archstone investment, and likely so much more:

[Reilly] was skiing alone on the John’s Bypass Trail, a connector between the Excelsior and Lower Cloudspin ski runs that’s accessible from either the Cloudsplitter Gondola or the Summit Quad chairlift, when he left the trail and hit a tree. A skier following behind Reilly witnessed the incident and contacted ski patrol.

…not only was he was a decent skier but he was over 6’4″ tall and wearing a helmet – it may always be a mystery to us how he succumbed to his injuries so fast…

The reason we bring this up is that an investigation continues in Colorado after the death of a skier in the popular tourist town of Vail.

The skier, 46 year old Jason Varnish of New Jersey, was Credit Suisse Managing Director, and served as the bank’s global head of prime services risk

In what can only be described as a freak accident, Varnish reportedly died of asphyxia and his death was ruled an accident after he slipped through the seat of the lift and his coat got caught. The incident took place at the Blue Sky Basin section of the Vail Ski Resort.

The skier reportedly suffocated to death after being “caught in a chairlift” and the incident marks about the 8th skier death in Colorado this year, which marks a pace slightly lower than last year, according to the Washington Post.

Kara Bettis, local coroner, commented:

“We are still investigating how this whole situation happened. According to our initial investigation, the deceased slipped through the seat of the chair lift and his ski coat got caught up in the chair.”

His folding seat was left in the upright position, so when Varnish went to sit down, he slipped through the seat before his coat got caught around his head and neck, cutting off his airway. Ski patrol then performed CPR, but Varnish was pronounced dead at the hospital.

Joseph Bloch, a Colorado attorney who litigates ski incidents, immediately seemed to blame the operators of the lift:

“They should’ve just hit the stop button, there’s an emergency stop and there’s a slow stop and if they’re doing their job they could hit the slow stop before the guests are loading.”

The lift was closed for the remainder of the day and the following day, but Vail Resorts then released a statement defending its lifts as having been inspected and as properly functioning.

Beth Howard, the resort’s CEO, said:

“Vail Mountain and the entire Vail Resorts family express our sincere condolences and extend our support to the guest’s family and friends.”

Nice touch, Beth. At least you didn’t offer the family free lift tickets…