Trade Bust? China Won’t Increase Grain Import Quotas Despite Promise To Buy More American

China has pledged to increase more purchases of U.S. farm goods but never confirmed the exact amount for the phase one trade agreement.

Han Jun, the vice-minister of agriculture and rural affairs, was quoted by Caixin on Tuesday as saying Beijing won’t increase its annual import quotas for wheat, corn, and rice, reported Reuters.

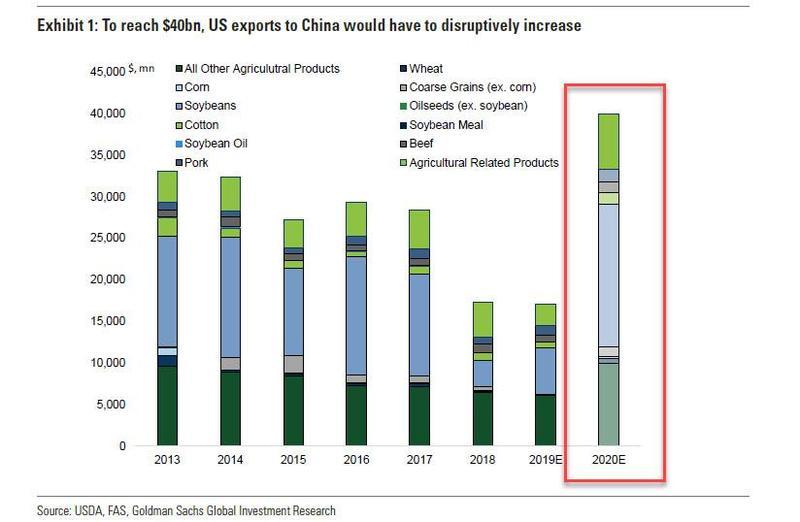

This comes at a time when the Trump administration has pressured China to double its $24 billion pre-trade war purchases of U.S. farm goods to nearly $40 billion – a move that would serve as an election win for President Trump and help alleviate pressures on struggling Central and Midwest farmers.

Han is also part of the trade negotiating team, said last month that China would increase annual quotas on wheat, rice, and corn. But as of Tuesday, Han and the trade team have changed their minds saying the quotas “won’t adjust for one country.”

Refinitive data shows purchases of the three grains from the U.S. totaled around $534 million.

“Although there’s certainly types of high-quality wheat that China would look to import, maxing out the tariff rate quota would also weigh on domestic producers,” Darin Friedrichs, senior Asia analyst at INTL FCStone, said in a note Monday.

“China will be facing a tough balancing act of trying to satisfy the U.S. demands for large agriculture purchases, while also not hurting the rural population,” Friedrichs added.

Last month, we said with absolute certainty that China wouldn’t uphold the trade agreement. There’s just no way that China would increase U.S. farm good imports by 235% in 2020. It’s not just because China is protecting its domestic agricultural markets, but rather, it’s because Brazil and Argentina have ramped up shipments of grains to the Asian country.

Goldman Sachs points out in a recent note that any massive increase in Chinese purchases from the U.S. “would likely be hugely disruptive to global agriculture markets, primarily crowding out Argentine and Brazilian supplies that have taken substantial market share since 2017 due to the trade war and much weaker currencies.”

To get a sense of just how improbable such a surge in Chinese imports from the U.S. is, here is a visual representation of what this “disruptive increase” in U.S. agriculture exports to China would look like…

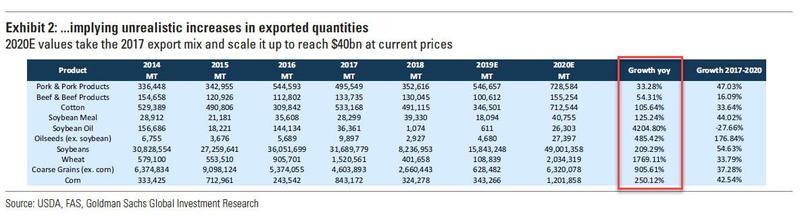

… and also why the assumption in exported quantities to China is, as Goldman points out, thoroughly “unrealistic.”

And while China promised a “best-effort” to purchase $40 billion in farm goods from the U.S. in 2020, it appears hard targets won’t be met. Does this mean more tariffs are on the way for non-compliance?

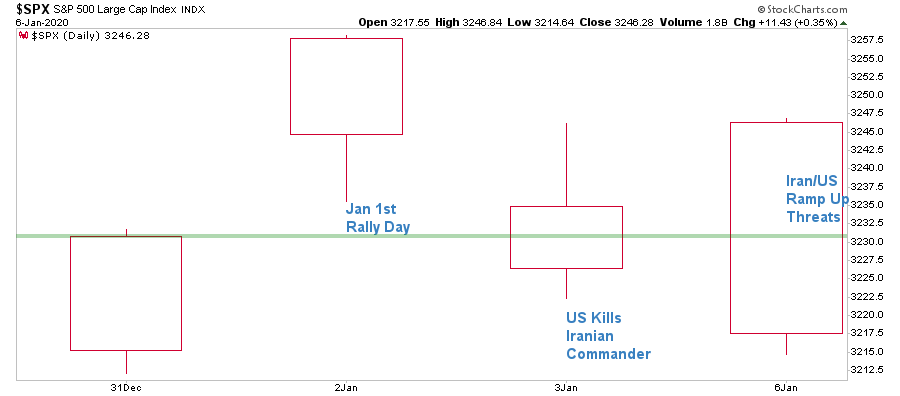

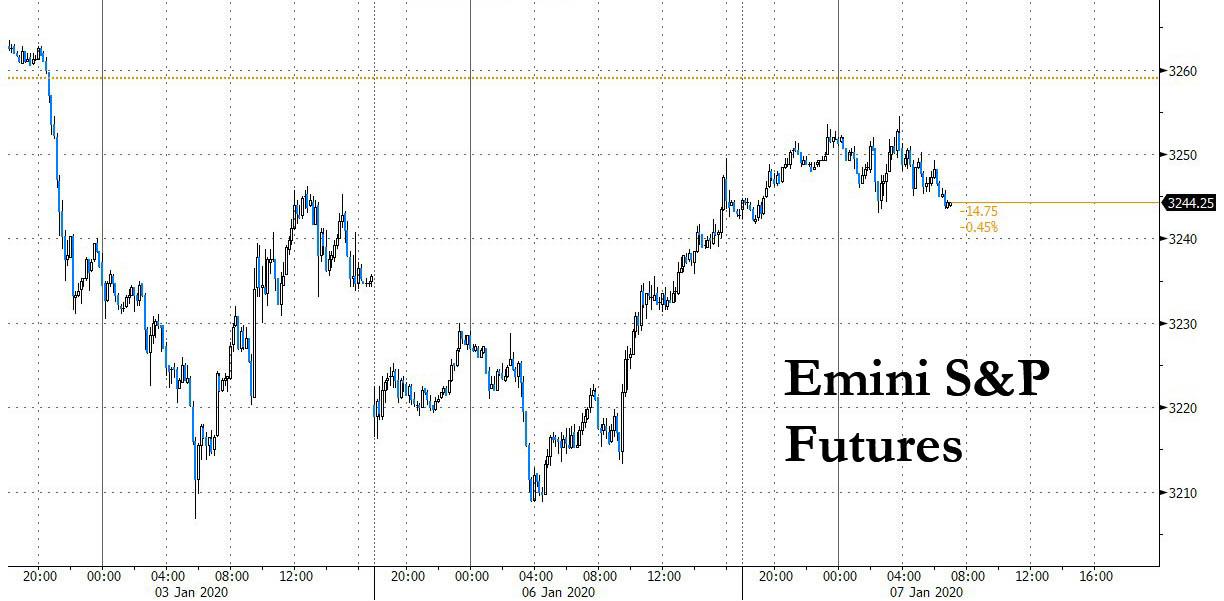

You would think that with the U.S. taking out a top Iranian commander, threats of military action flying between the U.S. and Iran, not to mention the “Selective Service” website crashing over concerns of World War III, the markets would be in full “sell” mode.

Due to the spread of misinformation, our website is experiencing high traffic volumes at this time. If you are attempting to register or verify registration, please check back later today as we are working to resolve this issue. We appreciate your patience.

If you thought that would be the case, you were wrong.

Here is the market from the beginning of the year through yesterday’s close.

The dismissal by the market of the situation with Iran suggests only a couple of things:

The market sees no inherent risk from Iran other than a lot of “saber rattling,” or

Given the Federal Reserve’s recent transition to a “do anything” monetary policy stance, all “risks” are being dismissed under the assumption the Fed has become a “cure all” for any market ill.

Since this is a technical post on the financial markets and investing, I won’t get into all the risks inherent from a conflict with Iran. However, if we assume there are indeed “risks” with Iran, then it becomes apparent the market is betting on the Fed.

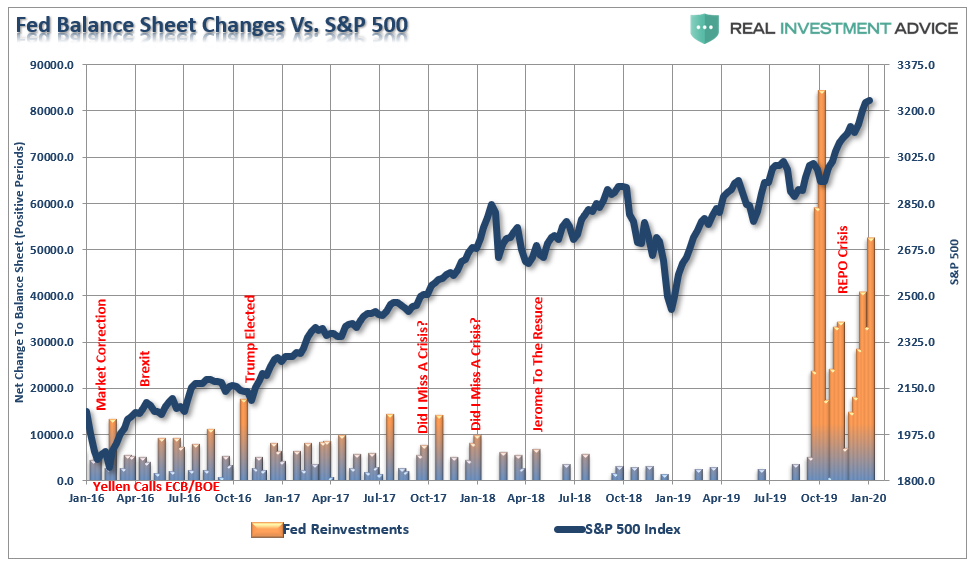

As I noted in this past weekend’s missive, the Fed has been dumping massive amounts of liquidity into the system over the last few weeks. To wit:

“But concerns over potential Iranian conflict quickly abated as the markets returned their focus to the Federal Reserve, and the continued pump of monetary liquidity into the markets.

Currently, we are told there is ‘nothing to worry about’ concerning the financial system. Maybe, but the amount of liquidity being injected dwarfs all previous injections by massive proportions.

Those injections continue to run unabated currently, which has lulled the markets into a more extreme state of complacency. This can see in the low reading of bearish investors and the suppressed levels of the put/call ratio. Both suggest there is “no fear” of a market correction currently. (h/t Soberlook)

Here is the investor conundrum.

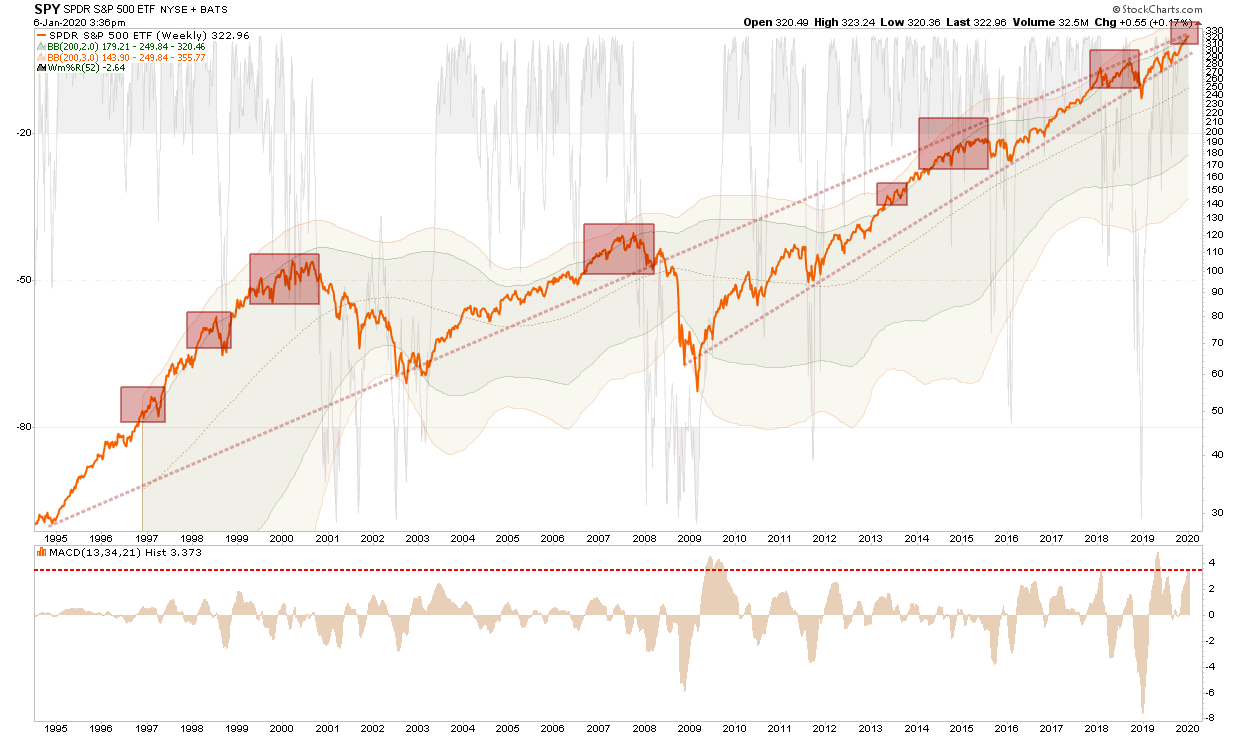

With the market currently onregistering of the monthly buy signals, which confirmed the bull market in the S&P 500 had resumed following the 2018 Fed/Trade induced sell-off, there is also the risk of a short-term correction. Previously, when the market was this extended, deviated from longer-term means, and excessively bullish, a correction has always occurred. The problem for investors is maintaining patience in the process.

The chart below shows the issues. When the market becomes more than 2-standard deviations above the 200-WEEK (4-year) moving average, you have gotten a correction, or a deeper mean-reverting event. However, since this a weekly chart, those corrective processes can take some time to occur. This lures investors into thinking “this time is different,”just before an event has tended to reduce their investment capital

Optimistically Cautious Short-Term

In the short-term, our outlook remains optimistically cautious due to the aforementioned ongoing liquidity injections from the Federal Reserve. As we noted to our RIAPro Subscribers yesterday (Try Free For 30-Days):

“The markets remain positively biased but have gotten overly extended in the short-term. We suggest remain long current holdings, but take profits and rebalance risks in positions accordingly. We will likely have a much better entry point in the next couple of months to ‘buy’ into.”

While we remain optimistic on stocks over the next couple of months, as we are in the “seasonally strong period” of the year, there are several risks which need monitoring closely.

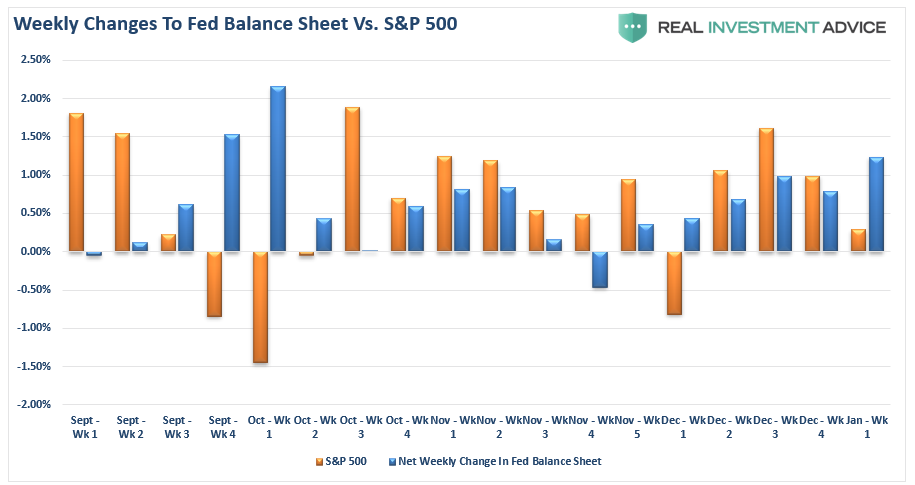

The most obvious risk is a reversal of the Fed’s monetary policy. Currently, the Fed’s balance sheet has almost entirely reversed last year’s decline. Subsequently, changes in the S&P 500 have closely tracked weekly changes to the Fed’s balance sheet. As noted last week:

Of course, it should be expected that if the Fed reverses those flows, then equities will likely follow suit.

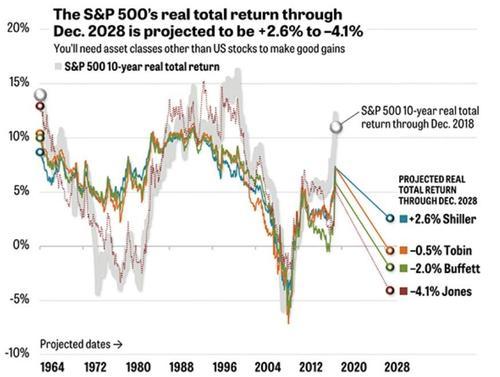

Secondly, ultimately, will be valuations.

Yes, I know that “valuations” do not seem to matter currently, however, it is important to realize they will eventually matter, and they will matter a lot.

Currently, the S&P 500 trading roughly 20x current reported earnings estimates of $161.87 per share for the end of 2020, based on data from S&P Dow Jones. Going back to the year 1988, on average, the S&P 500 trades for around 16x times trailing earnings estimates. But it isn’t just P/E ratios which are rich. As we discussed yesterday, multiple measures of the markets are trading at levels which have denoted much lower rates of returns going forward.

What this suggests is that for equities to see a continued, and significant, advance in 2020, it will require investors to continue paying higher prices for equity ownership. While this may seem to make sense in a “low-interest rate” world, historically overpaying for earnings growth has often turned out poorly.

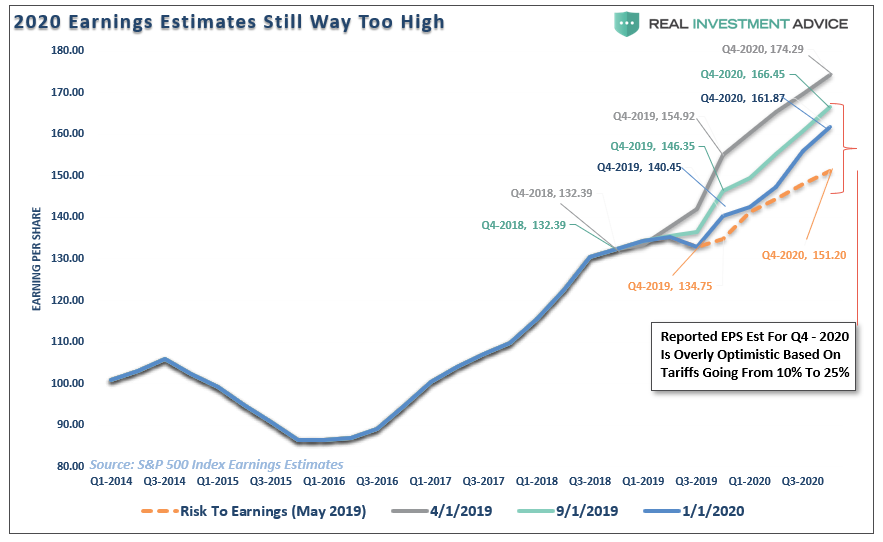

In other words, what investors are betting on is that earnings will catch up with price. However, currently, there is no evidence such will be the case as earnings have been repeatedly ratcheted lower since April 2019.

As shown in the chart below, earnings for the entire 2020 period started at $174.29/share. At that time, the beginning of April, the S&P 500 was trading at 2892. While the forward P/E seemed reasonable at 16.5x earnings, which was roughly equal to the long-term average, this assumed earnings estimates were correct. However, with the S&P 500 trading, as of yesterday’s close, at 3246, estimates for 2020 have fallen to just $161.87. That $12 decline in estimates, combined with a 354 point (an 11.8% advance) in the market, brings that forward P/E multiple to a rather expensive 20.05x reported earnings.

Of course, the risk to investors is that earnings growth fails to recover as we head further into 2020. Currently, there is evidence from the manufacturing, employment and wage data which suggests such could indeed be the case.

The Path Ahead

What is clear is that the path ahead for stocks is much less certain than a year ago when we were coming off deeply depressed sentiment levels, and the Fed was rapidly reversing monetary policy from “tightening” to “easing.” With equities now 30% higher than they were then, the Fed mostly on hold in terms of rate cuts, and “repo” operations slated to end in the next couple of months, it certainly seems that expectations for substantially higher market values may be a bit optimistic.

Furthermore, as noted, if signs of economic improvement don’t start to lift expectations for earnings growth into the last half of the year, it could prove problematic given current valuations.

However, if the economy does show improvement, it could result in yields rising on the long-end of the curve, which could also make stocks less attractive. This would effectively keep a lid on just how much risk some investors will be willing to take, and the price they are willing to pay.

One thing is for certain, the sharp rise in stocks in 2019 has left prices at levels that already seem expensive on numerous measures. As such it will required investors to take on increasing levels of risk if prices are going to push higher this year. While this is certainly not an improbability given the current levels of complacency and optimism, it is just worth noting that outcomes of such endeavors have always been poor.

There is one true axiom of the market which is always forgotten.

“The market has a habit of sucking investors in to inflict the most pain possible.”

Just make sure you aren’t one of them.

If you feel you must chase the markets currently, then at least do it with a set of guidelines to follow in case things turn against you. We printed these a couple of weeks ago, but felt there are worth mentioning again.

Move slowly. There is no rush in adding equity exposure to your portfolio. Use pullbacks to previous support levels to make adjustments.

If you are heavily UNDER-weight equities, DO NOT try and fully adjust your portfolio to your target allocation in one move.This could be disastrous if the market reverses sharply in the short term. Again, move slowly.

Begin by selling laggards and losers. These positions are dragging on performance as the market rises and tend to lead when markets fall. Like “weeds choking a garden,” pull them.

Add to sectors, or positions, that are performing with, or outperforming, the broader market.

Move “stop loss” levels up to current breakout levels for each position. Managing a portfolio without “stop loss” levels is like driving with your eyes closed.

While the technical trends are intact, risk considerably outweighs the reward. If you are not comfortable with potentially having to sell at a LOSS what you just bought, then wait for a larger correction to add exposure more safely. There is no harm in waiting for the “fat pitch” as the current market setup is not one.

If none of this makes any sense to you – please consider hiring someone to manage your portfolio for you. It will be worth the additional expense over the long term.

While we remain optimistic on the markets currently, we are also taking precautionary steps of tightening up stops, adding non-correlated assets, raising some cash, and looking to hedge risk opportunistically.

Just because it isn’t raining right now, doesn’t mean it won’t. Nobody has ever gotten hurt by keeping an umbrella handy.

Overnight Risk Rally Fizzles After Iran Vows “Historic Nightmare” Retaliation

After putting fears about World War III aside on Monday, when stocks opened sharply lower only to close at session highs and the S&P on the verge of a new record, overnight concerns about the impending middle east conflict returned when shortly after 2am ET, Ali Shamkhani, the head of Iran’s national security council, roiled markets when he said that Iran is evaluating 13 possible retaliations on the U.S. for killing a Solemani, adding that “even if the weakest of these scenarios gains a consensus, its implementation can be a historic nightmare for the Americans.” The menacing comments from Shamkhani briefly roiled markets, and established a ceiling for the Emini.

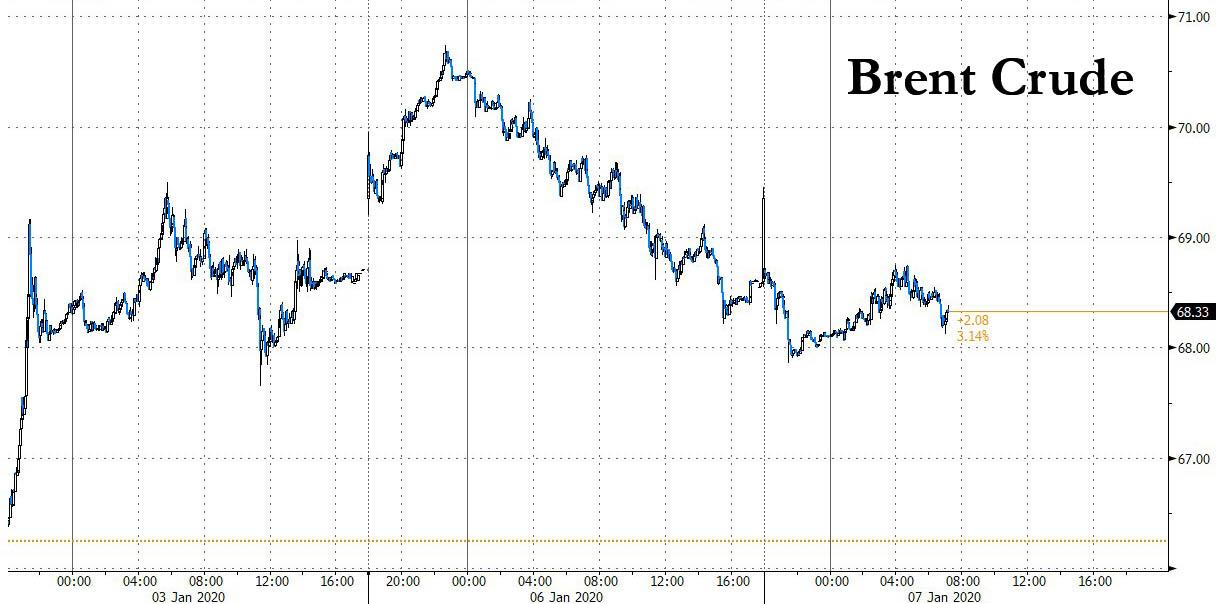

Following the Iranian threat, S&P 500 futures gave up all of the morning’s advance before steadying. Despite the wobble in S&P futures, world shares steadied in delayed response to Monday’s US rally, while oil and gold pulled back from multi-month/year highs on Tuesday after dramatic post-new year moves, as investors judged that prospects of an all-out conflict between the United States and Iran had eased.

After a strong rally, oil gave back much of its gains amid signs that Iran would be unlikely to strike against the United States in a way that would disrupt supplies. Brent crude futures fell 44 cents to $68.48 a barrel, having been as high as $70.74 on Monday, while U.S. crude dropped 34 cents to $62.93.

European equities meanwhile rose as much as 0.7%, tracking similar gains in Asia, before cutting gains in half. Technology stocks were among the top picks in Europe, mirroring trends in the U.S. overnight.

Earlier in the session, MSCI’s index of Asia-Pacific shares ex-Japan recouped almost all of Monday’s losses, led by health care and consumer staples, and rebounding from a drop on Monday amid U.S.-Iran tensions. Investor concerns over the Middle East flare-up have begun to ease, even as the U.S. ordered additional forces into the region, and Iran said it is assessing 13 scenarios to respond to the American killing of its top general, Qassem Soleimani. Most markets in the region were up, with Japan’s Topix index gaining the most since Nov. 5. Kweichow Moutai Co. and Industrial and Commercial Bank of China Ltd. led China’s Shanghai Composite Index higher, while Reliance Industries Ltd. and HDFC Bank Ltd. drove gains in India’s S&P BSE Sensex Index.

Meanwhile emerging markets, which had been hit hardest by spiking oil prices, bounced back on Tuesday, with stocks up 0.4%. That left the MSCI world equity index, which tracks shares in 49 countries, just 0.5% from a record high.

“Geopolitical risk has always felt much worse for markets in the heat of the moment than it does in hindsight, but it’s always possible that the next one will bring us into a different era,” Deutsche Bank strategist Jim Reid said (see more below). “Markets got a lift from the lack of follow-through (after the air strike) as yesterday progressed, and by the end of the session had actually staged a reasonable recovery,” Reid added.

With risky assets starting 2020 on the back foot as Tehran and Washington traded threats after a U.S. air strike on Baghdad airport killed a top Iranian commander, on Monday the mood began to calm, helping U.S. shares recover ground. The Dow ended 0.24% higher, the S&P 500 0.35% and the Nasdaq 0.56%.

Marija Veitmane, a senior strategist at State Street, said she sticks to her expectation of a slight improvement in economic and earnings outlook: “The world is well stocked with oil and can stomach short disruptions, while large U.S. shale production should soften its impact,” said Veitmane, brushing aside worries that an oil price spike would dent global growth.

“There are a lot of developments in play but none of them are really that major,” John Normand, JPMorgan’s head of cross-asset fundamental strategy, told Bloomberg TV. “There are a lot of headlines that seem alarming at first blush and we dig a bit deeper, to me none of these are big derailers for the move up in risky markets this year.”

He was, of course, referring to the ongoing QE4 move in the Fed’s balance sheet, which continues to grow at a pace of about $100 billion per month.

As risk was bid, safety plays were out of favor, with gold retreating to $1,567 an ounce, after scaling a near seven-year peak overnight. At the same time, eurozone government bond yields edged up from around three-week lows. German bunds were little changed while U.K. gilts sold off; the pound gained versus the euro as the U.K. raised its debt-sales target for financial year 2019-2020, spurring bets the government is planning an expansionary new budget that could fuel inflation

The sense of calm also saw the yen lose much of its safe-haven gains, while the dollar advanced versus all G-10 peers; the euro declined even as the region’s retail sales picked up more than forecast in November; separate data showed euro-area inflation accelerated in December in line with the median economist forecast, while core inflation remained unchanged.

The Australian dollar led declines among G-10 currencies, dropping as much as 0.9% on geopolitics. Australia’s currency had weakened earlier after a decline in job advertisements and as the bush- fire crisis boosted the odds for a central bank interest-rate cut.

Curiously, overnight Bitcoin broke above $8,000 overnight and is up 13% since the U.S. drone attack in Iraq last week. Though it is not seen as a safe-haven asset given its wild swings, the surge has coincided with the equities sell off.

Looking at the day ahead now, the highlights in terms of data come in the US with the December ISM non-manufacturing likely to be of particular focus. We’ll also get the November trade balance, November factory, durable and capital goods orders in the US. This morning in Europe we got the preliminary December CPI report for the Euro Area and Italy along with November retail sales data for the Euro Area. Also as mentioned the UK Parliament returns from recess, with MPs due to debate the Brexit Withdrawal Agreement Bill.

Market Snapshot

S&P 500 futures up 0.2% to 3,250.25

STOXX Europe 600 up 0.6% to 419.16

MXAP up 0.9% to 171.33

MXAPJ up 0.6% to 554.78

Nikkei up 1.6% to 23,575.72

Topix up 1.6% to 1,725.05

Hang Seng Index up 0.3% to 28,322.06

Shanghai Composite up 0.7% to 3,104.80

Sensex up 0.4% to 40,830.27

Australia S&P/ASX 200 up 1.4% to 6,826.44

Kospi up 1% to 2,175.54

German 10Y yield rose 1.1 bps to -0.276%

Euro down 0.1% to $1.1183

Brent Futures down 0.5% to $68.60/bbl

Italian 10Y yield rose 1.4 bps to 1.191%

Spanish 10Y yield rose 1.5 bps to 0.409%

Brent Futures down 0.5% to $68.60/bbl

Gold spot down 0.1% to $1,563.51

U.S. Dollar Index up 0.03% to 96.70

Top Overnight News from Bloomberg

Iran is assessing 13 scenarios to respond to the U.S. killing of Qassem Soleimani, the influential general in charge of foreign operations, and even the weakest of those options would be a “historic nightmare” for the U.S., Ali Shamkhani, the head of Iran’s national security council, was quoted as saying by Iran’s semi-official Fars news agency

U.K. Chancellor of the Exchequer Sajid Javid promised to unleash “a decade of renewal” when he outlines his budget on March 11 as he seeks to ready the U.K. for its departure from the European Union

Spain’s Socialist leader Pedro Sanchez looks set to secure the narrowest of victories in parliament on Tuesday to take power in Spain with the backing of the anti-austerity party Podemos.

Brevan Howard Asset Management’s flagship hedge fund returned 8.4% last year, building on its 2018 gain and helping to pause a bleeding of assets

Asian equities posted gains across the board following a less pronounced but positive handover from Wall Street in which the major indices experienced a modest recovery from the prior session’s losses. ASX 200 (+1.4%) was propped up by its largest-weighed financials as yields recouped from recent downside. Nikkei 225 (+1.6%) retraced some of the prior session’s hefty losses whilst welcoming recent favourable currency moves. Elsewhere, Hang Seng (+0.4%) and Shanghai Comp (+0.7%) conformed to the overall risk appetite – and with the former supported by gains in large-cap financial stocks. China Vice Agricultural Minister said China will not increase annual grain import quotas to accommodate higher US farm purchases. This refutes rumours that China may raise or scrap its corn import quota following a phase one trade deal with the US

Top Asian News

China Targets Internet Giants in Antitrust Law Overhaul

China’s Next Crisis Brews in Taiwan’s Upcoming Election

Disney Faces Pressure to Help Ease Hong Kong’s Housing Crisis

European bourses are firmer this morning, in a turn-around from yesterday’s dismal start to the week (Euro Stoxx 50 +0.5%). Notably, the Dax, which gave up the 13000 handle yesterday, has stayed well-clear of this mark to the downside; with the bourse having printed a cash high of 13266 and a future peak at 13260. Similarly, in contrast to yesterday, and indeed Friday, sectors are all firmly in positive territory with exception of energy names, where yesterday’s outperformers such as Shell (-0.8%) and BP (-0.7%) are under pressure; although, this is to the benefit of airlines such as Air France (+1.5%) and eastJet (+1.4%). Additionally, this downside in the aforementioned energy names is weighing on the FTSE 100 (+0.1%) this morning; with the bourse relatively flat at present. Other notable movers this morning include, Morrisons (+2.5%) after issuing their Christmas sales update and noting that PBT and exceptionals is likely to be within analyst forecasts for FY19/20. At the other end of the Stoxx spectrum are Standard Life Aberdeen and Man Group with both weighed on by broker moves.

Top European News

Premier Oil to Buy North Sea Assets From BP for $625 Million

Vestas to Invest in 5,000 New Vehicles in Massive E-Car Push

U.K. Soccer Team Sunderland Kicks Off Sale After Fan Backlash

Aston Martin Slumps After ‘Disappointing’ Year of Profit Decline

In FX, already feeling the adverse effects of natural disaster, anecdotal data overnight revealed a sharp decline in the number of Australian jobs advertised on the web and in newspapers to highlight the economic impact of the raging bushfires, with dovish RBA implications. Hence, the Aussie has weakened appreciably across the board, with Aud/Usd slipping through 0.6900 and the 200 DMA (0.6897), while Aud/Nzd has also breached a key chart level at 1.0367 (18 December 2019 low) as the Kiwi contains contagious losses against its US counterpart within 0.6642-80 parameters.

USD – Aside from gleaning traction from the underperformance in Antipodean peers, the Greenback is consolidating off recent lows vs major rivals on a combination of technical and other factors awaiting further developments on the geopolitical front (namely Iran’s response to the US airstrike targeting and killing a top IRGC leader). The DXY has pared declines towards 96.500 and appears more settled in a 96.620-835 range ahead of the upcoming services ISM that could be pivotal for near term Fed policy given the disappointing manufacturing survey and expectations for a firmer headline than previous.

CHF/EUR/CAD/JPY/GBP – As noted above, all weaker against the Buck with the Franc back below 0.9700 and not really inflated by Swiss CPI returning to positive territory in y/y terms, Euro fading ahead of 1.1200 and Loonie losing momentum alongside oil prices in advance of 1.2950 in the run up to Canadian trade data due alongside the US balance for direct comparison. Meanwhile, having met stiff resistance at 108.00 on several occasions of late the Yen is now deriving support from offers said to be capping the headline pair at 108.50, but the Pound has waned markedly after a stop driven rally in Cable on a break of 1.3180 (just above Monday’s peak) to 1.3200+ that pushed Eur/Gbp back under 0.8500 with more gusto and just under 0.8470 before the cross retraced some lost ground.

SEK – Some respite for the Swedish Crown via a less contractionary services PMI, but Eur/Sek is still elevated above the 10.5000 level in contrast to Eur/Nok holding shy of 9.8500.

EM – Although the Dollar has made advances elsewhere, Yuan strength off a marginally firmer PBoC midpoint fix has bucked the general trend, as Usd/Cnh eases back towards mid-December lows not far from 6.9200 and a series of key chart supports closer to 6.9000 amidst reports from the Chinese side alluding to the signing of Phase 1 in the not too distant future.

In commodities, the crude complex has dropped into negative territory, with WTI and Brent down by around USD 0.30/bbl at present and approximately USD 1.0/bbl at worst in overnight APAC trade. Newsflow from the Middle-East continues to emerge with the latest pertinent reports noting that Iran is, according to a Fars report, considering 13-scenarios as retaliation against the US. Additionally, a Senior Iranian Official has stated that Iran is prepared to come back to full compliance with the Nuclear Deal. Note, Iran has following the assassination of Soleimani made clear that they are to conduct nuclear related operations on their own accord, disregarding the Nuclear Deal; as such, these remarks potentially indicate a pivot in Iran’s stance against the US and Western powers. However, its worth highlighting that the conditions around their potential return to the deal are not known and previously Iran has indicated sanction relief is a pre-requisite for this type of action. Looking ahead, today sees the funeral of Soleimani and as such participants will now be more actively anticipating/awaiting a response from Iran as the initial mourning period comes to an end. Elsewhere, turning to metals, spot gold is back in positive territory after dipping overnight to a low of USD 1555/oz, prices are now comfortably back above the USD 1560/oz mark; but remain well off yesterday’s multi-year high at USD 1582/oz. Separately, iron ore prices are bolstered following on from China’s main steel making city of Tangshan lifted its level 2 smog alert which was implemented late last week.

US Event Calendar

8:30am: Trade Balance, est. $43.7b deficit, prior $47.2b deficit

10am: ISM Non-Manufacturing Index, est. 54.5, prior 53.9

10am: Factory Orders, est. -0.8%, prior 0.3%

Durable Goods Orders, est. -2.0%, prior -2.0%

Factory Orders Ex Trans, prior 0.2%

Durables Ex Transportation, prior 0.0%

Cap Goods Orders Nondef Ex Air, prior 0.1%

Cap Goods Ship Nondef Ex Air, prior -0.3%

DB’s Jim Reid concludes the overnight wrap

I spent the evening last night taking down Xmas decorations before more bad luck could descend on my flu and bed ridden family. Normally my wife won’t let me anywhere near the decorations as when she last did, 11 months later she found them in such a mess the following Xmas that it took her as long to sort out/untangle as it did to put them up. I’ll let you know how she reacts on December 1st 2020 when the boxes come back down from the attic.

The first full day back for many in the market was busy spent digesting the fallout from the US/Iran tensions. In fairness there wasn’t much new to add from the weekend headlines so for now we’re still in a state of flux as to which way we go next. After the drone attacks on Saudi oil refineries in September there were expectations that the impact would linger for weeks or months, but in reality the market largely moved on within 24-48 hours. This does feel quite different though given the scale of the action and the war of words since. However it would be impressive if market professionals had a clear view on how this will all pan out. If you do though please get in touch and let me know. Throughout my career geo-political risk has always felt much worse for markets in the heat of the moment than it does in hindsight but it’s always possible that the next one will bring us into a different era.

Our oil analyst Michael Hsueh last night suggested that oil infrastructure and shipping is better protected now than it was last year and that the risks of retaliation are perhaps higher away from oil now. This could include cyber warfare. As such he doesn’t think the higher risk premium in oil will last for a prolonged period. See his note here for more.

The good news for now though is that markets got a lift from the lack of follow through as yesterday progressed and by the end of the session had actually staged a reasonable recovery from the lows. In fact the turnaround was so much so that by the close of trade yesterday, the S&P 500 was up +0.35%, recovering from futures being down -0.83% early in the European session. The steady rally puts the index back slightly higher for 2020 now. The NASDAQ also recovered to close +0.56%, and in Europe the STOXX 600 pared a drop of as much as -1.36% to close down ‘just’ -0.41%. Meanwhile oil faded from the highs with Brent crude now trading back below $70/bbl this morning at $68.14. It did touch a high of $70.74 yesterday having closed on Friday at $68.60 and at around $66 on NYE before the strike. For context the last time it closed above $70 was back in May so we haven’t managed that yet in this episode.

Looking at other assets, the move towards safe havens abated somewhat yesterday. The Japanese yen was actually the worst-performing G10 currency yesterday, having been the best-performing on Friday, while gold faded back to close up +0.87%, though this was still its highest level since April 2013. Over in fixed income, 10y Treasuries ended the session +2.1bps, in spite of the fall in yields earlier in the session, while the 2s10s curve saw a slight steepening of +0.3bps. In Europe, gilts underperformed thanks in part to stronger than expected PMI data from the UK (more on that below), ending +3.0bps, while 10yr bund yields ended the session unchanged.

The big event today is the services ISM in the US which will give us hints as to how the US economy closed last year.

Overnight Bloomberg has reported that the US Vice President Mike Pence will deliver an address on the Trump administration’s Iran policy next Monday. Elsewhere, the US denied media reports which circulated a letter suggesting that it had agreed to pull its forces from Iraq. Army General Mark Milley, chairman of the Joint Chiefs of Staff, said that the letter was a draft and should never have been sent. Elsewhere the Washington Post reported that senior Trump administration officials have begun drafting sanctions against Iraq with one of the officials saying that the plan was to wait “at least a little while” on the sanctions decision in order to see whether Iraqi officials followed through on their threat to push U.S. troops out of the country.

This morning in Asia markets are following Wall Street’s lead. The Nikkei (+1.46%), Hang Seng (+0.45%), Shanghai Comp (+0.26%) and Kospi (+0.92%) are all up alongside most indices in the region. As for Fx, currencies of oil importing Asian countries like South Korea (+0.599%) and India (+0.301%) are advancing this morning on cooling oil prices while the Japanese yen is down -0.10%. Elsewhere, futures on the S&P 500 are up +0.24% while in commodities spot gold prices are down -0.23%. As for overnight data, Japan’s December services PMI came in at 49.4 (vs. the 50.6 flash) while the composite PMI stood at 48.6 (vs. 49.8 last month).

Back here in the UK, MPs will be returning to Parliament today, where they will resume debate on the Withdrawal Agreement Bill that implements the Brexit deal into UK law. The House of Commons is scheduled to debate the bill over the next 3 days, but with the government having an 80-seat majority in the Commons following last month’s election, there aren’t expected to be any issues over its passage. Elsewhere, the Telegraph reported overnight that the UK government will deliver its budget on March 11. Chancellor Sajid Javid’s first budget is likely to be expansionary as during the election campaign he promised to loosen constraints on borrowing to the tune of up to £20 bn a year for capital spending.

Away from the geopolitical newsflow there were a number of data points to digest yesterday. On the remaining PMIs, the final December services reading for the Euro Area was revised up 0.4pts to 52.8 – a four month high – leaving the composite at 50.9 and therefore the highest since August when it hit 51.9. That composite reading is consistent with growth of around +0.1% qoq in Q4. At a country level we saw a decent upward revision to Germany’s services PMI (52.9 from 52.0) while Italy (51.1 vs. 50.9 expected) and Spain (54.9 vs. 53.9 expected) both beat. For completeness, here in the UK the services PMI rose 0.7pts to 50.0 (vs. 49.1 expected) which helped to hold the composite at 49.3, with sterling up around +0.6% against the US dollar yesterday following the better-than-expected performance. So, overall a modest positive in Europe albeit with the data clearly overshadowed yesterday by the Middle East tensions.

Over in the US the services PMI was also revised up, by 0.6pts to 52.8 which is the highest reading since July. It’s worth noting that the employment component was little revised but nevertheless has nearly fully recovered the plunge that occurred this summer. Finally on the data, German retail sales in November rose by +2.1% (vs. +1.0% expected), while the previous month’s numbers were revised to show a smaller contraction than previously thought.

Looking at the day ahead now, the highlights in terms of data come in the US this afternoon, with the December ISM non-manufacturing likely to be of particular focus. We’ll also get the November trade balance, November factory, durable and capital goods orders in the US. This morning in Europe we’re due to get the preliminary December CPI report for the Euro Area and Italy along with November retail sales data for the Euro Area. Also as mentioned the UK Parliament returns from recess, with MPs due to debate the Brexit Withdrawal Agreement Bill.

Iran Evaluating 13 Retaliation Scenarios To Inflict “Historic Nightmare” On US

Breaking a 5-day silence over its response for the US killing of General Qassem Soleimani, on Tuesday Iran said it was assessing 13 scenarios to inflict a “historic nightmare” on the US. “Even if the weakest of these scenarios gain a consensus, its implementation can be a historic nightmare for the Americans,” Ali Shamkhani, the head of Iran’s national security council, was cited by Fars news agency, adding that, “For now, for intelligence reasons, we cannot provide more information to the media.”

Iranian officials previously said that U.S. forces in the region will be targets, and overnight the Iranian parliament on Tuesday designated the Pentagon and affiliated companies as terrorists. In response, the U.S. issued a warning to shipping in the Middle East over the possibility of Iranian action against U.S. maritime interests, the Associated Press reported, citing a statement.

Mohammad Javad Zarif, Iran’s foreign minister, said Tuesday that the U.S. would suffer consequences for the killing of Soleimani “at a time and place of Iran’s choosing.” Zarif added the U.S. must leave the Middle East and warned that if they don’t, a new multi-generational war could erupt.

The leader of the Islamic Revolutionary Guard Corps (IRGC), Major General Hossein Salami, told tens of thousands on Tuesday for the burial of Soleimani in the city of Kerman that Iran was ready to “set ablaze those places Americans hold dear” over the killing of the former commander. Thousands chanted “revenge, revenge,” as the IRGC leader declared “we will take revenge. The revenge will be vigorous and unwavering, woeful, and terminal.”

“We will surely take revenge, but if America dares takes any action, we will set alight those places Americans hold dear. They know where those places are.”

“We will burn the places they love”

IRGC Commander Hossein Salami reaffirms Iran’s vow to avenge the death of Qasem Soleimani pic.twitter.com/bCqxco1nsL

And while the world await for Iran to pick one or more of the 13 scenarios, on Monday the Pentagon dispatched additional forces to the Middle East, even as conflicting signs emerged about Washington’s commitment to remaining in Iraq.

The three-ship Bataan Amphibious Readiness Group was ordered to move to the Persian Gulf region from the Mediterranean, where it has been exercising, according to a U.S. official. The group, which includes about 2,200 Marines and a helicopter unit, follows the deployment of about 3,500 soldiers from the Army’s 82nd Airborne to Kuwait late last week.

Dozens Killed During Stampede At Iranian General’s Funeral

What some observers described as the largest public outpouring of grief in Iran since Ayatollah Khomeini’s funeral in 1989 wasn’t free from bloodshed, as dozens died during a stampede in Monday’s funeral procession for Qassem Soleimani, the iconic Iranian general killed by the US during a visit to Baghdad last week.

According to WSJ, 32 people died during the stampede, and another 190 were injured, as the crowd panicked during the ceremony in Iran’s Kerman province, where Suleimani was set to be buried on Tuesday, after the ceremony was postponed as crowds from the procession blocked vehicles from getting to the cemetery on Monday. Other reports put the death toll as high as 40.

The regime said the stampede was caused by overcrowding, and denied that the stampede was the result of an attack. Government officials said ambulances were ready along the route of the procession in case of an incident.

Video from the scene that circulated on social media appeared to show first responders desperately trying to revive injured men lying on the ground.

Meanwhile, Iranian leaders issued more threats of retaliation on Tuesday, the fourth and final day of mourning for the general. And as if that weren’t enough, Iran’s Parliament on Tuesday passed a bill labeling the entire US military as a terrorist organization.

“I say the last word first. We will take revenge,” said Maj. Gen. Hossein Salami, a commander of the Islamic Revolutionary Guard Corps, speaking at Gen. Soleimani’s funeral procession in Kerman province.

“If they make another move, we will set fire to the place they love,” said Gen. Salami, according to Iran’s Tasnim news agency.

In a telling example of just how much time it can take for news to trickle out of Iran, word of the deadly stampede only reached western media outlets early Tuesday morning in New York. Most of the footage from the funeral hit early on Monday, which is when footage of Ayatollah Khamenei chanting at the state funeral (he also appears to be crying).

I am not shocked by the incompetence of Ayatollah Khamenei. Much of his prayer recitation over #QassemSulaimani was wrong. He doesn’t know how to pray or structure sentences properly and is totally ignorant of ‘plural and singular’ rules. Yet he’s the “Deputy of the Infallibles.” pic.twitter.com/VC1tvsamr0

— Imam of Peace / Pray for Peace… (@Imamofpeace) January 6, 2020

But apparently, because of the stampede, Suleimani’s body hasn’t actually been buried yet, and Western media outlets claimed that many of the 1 million or so attendees (roughly 1% of Iran’s population) only attended because they feared retaliation from the state.

Carlos Ghosn Says He Has “Actual Evidence” Of Government Conspiracy As Japan Moves To Arrest His Wife

As Japanese officials investigate Carlos Ghosn’s criminal escape and authorities around the world make what we imagine will be only the first round of arrests, Fox Business’s Maria Bartiromo offered the first taste of what Ghosn plans to reveal later this week during what’s expected to be his first press conference since his great escape.

Bartiromo, who said she spoke to Ghosn via phone over the weekend (she previously sat down with Ghosn’s wife back in April), said that Ghosn plans to provide “actual evidence” and documentation proving that his arrest was the result of a coup inside Nissan, and that the Japanese judicial system ultimately went along with it because the government didn’t want to see Nissan merged with Renault.

Meanwhile, according to a WSJ report published Tuesday morning, Japan is trying to arrest Carole Ghosn, the executive’s wife, on suspicion of perjury. In a statement, prosecutors allege that Mrs. Ghosn lied during sworn testimony in April before the court handling her husband’s case.

Specifically, they said she lied about contacts with an unidentified individual shortly after Ghosn’s arrest in November 2018. It’s unlikely that she will be apprehended, though, as she has already traveled to Lebanon, where she has reportedly been reunited with her husband, something she described as “the best gift of my life.”

Ghosn told Bartiromo that he plans to “name names”, including identifying Japanese government officials who he believes were behind his 2018 arrest on ambiguous financial misconduct allegations.

The former auto titan said giving up his position as CEO at Nissan to his eventual successor, Hiroto Sakawa, put him in a “dangerous position,” and now believes that he should have left Japan, instead of staying in the country for Sakawa’s benefit. Ghosn told Bartiromo that he was “really unnerved and upset” that he failed to anticipate and understand the unfairness of the Japanese justice system, adding that the “straw that broke the camel’s back” was being blocked from speaking with his wife.

Ghosn’s great escape – which was reportedly masterminded by a former green beret and professional security consultant – is a great embarrassment for the Japanese government, since surveillance camera footage clearly shows Ghosn absconding – walking right out of his apartment in defiance of his house arrest order – to take a high-speed rail across the country.

The executive of course must now watch his back in Lebanon: It’s possible that bounty hunters could be looking to kidnap him, though he’s likely well-fortified and living in an undisclosed location.

Ghosn said that he’d be willing to have his case heard by “any court outside of Japan.” Remember, the Japanese government wins 99% of criminal trials.

Bartiromo said the big press conference will follow on Wednesday or Thursday.

Many of Ghosn’s supporters believe that some kind of corporate skullduggery ultimately led to his arrest, and that the financial charges are merely window-dressing. A NYT reporter first explored the issue in a lengthy profile published more than a year ago.

The British Royal Navy will escort UK-flagged vessels going through the world’s most vital oil choke point, the Strait of Hormuz, amid a sudden spike in tensions in the Middle East after the U.S. carried out an air strike in Baghdad that killed a high-ranking Iranian general.

“The government will take all necessary steps to protect our ships and citizens at this time,” Defence Minister Ben Wallace told media, as quoted by Reuters.

To this end, the HMS Montrose and the HMS Defender will be deployed in the region again, after last year they escorted UK-flagged ships through the Strait of Hormuz following the seizing of an Iranian oil tanker by Gibraltar with the help of the UK that angered Tehran.

In retaliation, Iran captured a UK-flagged vessel in the Strait of Hormuz. The deployment of the HMS Montrose and the HMS Defender followed, with the UK and the United States urging other countries to join a coalition for the protection of vessels sailing through the vital oil chokepoint.

Since then, UK-Iran tensions have been defused, after London released the Iranian tanker and Tehran reciprocated the gesture. Yet now, with Iran threatening to retaliate for the U.S. assassination of the leader of the Quds force of the Islamic Revolutionary Guard Corps Qassem Soleimani and with Iraq’s parliament voting in favor of the withdrawal of all foreign troops from its territory, tensions are running high again.

According to Reuters, Wallace called his U.S. counterpart, Mark Esper, and advised restraint.

“Under international law, the United States is entitled to defend itself against those posing an imminent threat to their citizens,” Wallace said in what could be construed as defence of the targeted air strikes that killed Soleimani and prompted a hostile verbal response from Tehran and anti-American demonstrations in Iraq.

Oil prices have been trending higher as a result of the latest developments, with Brent crude breaking the $70 ceiling for the first time in several months and West Texas Intermediate moving closer to $65 a barrel.

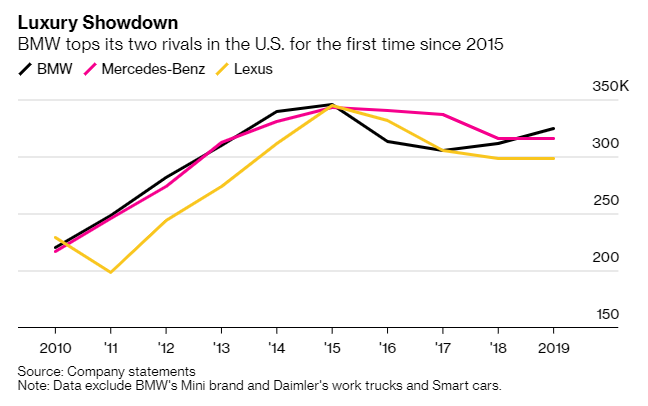

BMW Outsells Mercedes-Benz For The First Time In Four Years

BMW has passed Daimler’s Mercedes-Benz in the U.S. for the first time since 2015 after not only blowing out its rival in the fourth quarter, but also bucking an ugly U.S. auto sales trend that we highlighted just days ago, where most manufacturers saw sales collapse to end 2019.

BMW sold 35,746 cars and SUVs in the month of December, finishing the year ahead of Mercedes by more than 8.700 units. The company’s revival in the U.S. can be attributed to filling out its SUV lineup with its massive X7 – after keeping dealers and customers waiting for the vehicle for nearly a decade, according to BNN.

Mercedes, on the other hand, faced challenges with supplier bottlenecks at its lone U.S. assembly plant in Tuscaloosa, Alabama. It was only able to sell 316,094 vehicles in 2019 – just 135 more than the year prior, according to Bloomberg.

But it may not be a clean victory for BMW after all…

The SEC is continuing an investigation into BMW’s sales practices, as we reported on just weeks ago. The SEC is lookaing at whether BMW’s sales figures have been manipulated and whether or not the automaker has engaged in “sales punching”, a practice that encourages dealers to register cars despite them not being sold.

Meanwhile, we pointed out days ago that other auto manufacturers had an atrocious end to the year in terms of U.S. sales.

Fiat Chrysler sales for Q4 fell 2% despite “robust” demand for the company’s Ram pickup trucks. GM deliveries fell 6% in the quarter and Toyota saw sales fall 6.1% in December, handily missing estimates for a 0.8% gain.

And Toyota wasn’t the only automaker that missed estimates in grand fashion: Honda was also expected to report a modest gain in sales, but posted an ugly 12% drop in sales for the quarter.

Expectations were lower for Nissan, who was expected to post a drop of 22.1% but missed even those pessimistic expectations by posting a monster 29.5% loss for the quarter.

The leader of the Italian populist right-wing party, The League, and former Minister of Interior Matteo Salvini is one of Europe’s most controversial politicians. A recent poll shows that he is Italy’s most trusted party leader with 39% voter approval.

The Populist

Despite his popularity, the media and the political elite brands him as “far-right,” but since most people in the E.U. agree with his ideas and positions, center-right is a more appropriate term. More than anything, he is a populist. Populism can be neutrally defined as politics that is popular among ordinary people while despised and rejected by the ruling elites.

Matteo Salvini

As such, populism is not an ideology but a symptom of anti-democratic elitism. Voters only turn to populists when the establishment over a long period arrogantly refuses to listen to the will of the people. Salvini echoes the growing European discontent with the globalist project and the deconstruction of the nation-state.

Dramatic Entry And Exit

Salvini’s entry into the Italian government was as filled with drama as his exit. Initially, his party was called The Northern League and wanted the affluent northern parts of Italy to be a separate state. However, after growing Italian E.U. skepticism and worries about mass immigration, the party reinvented itself to become a national populist party against multiculturalism, eurocracy, and globalism.

In 2018, the two populist parties, The League and Five Star Movement, blasted onto the political stage by winning a substantial majority. Right-wing parties secured a whopping 70% of the votes. Neither of the two gained enough support on their own to form a government, so they joined in a coalition with Salvini as deputy prime minister and minister of interior.

Salvini immediately took steps to curb illegal immigration and was relentlessly attacked by the left. In August 2019, The League was so popular in Italy that Salvini called for a new election, citing inner friction with its coalition party as the reason. The Five Star Movement, which had fallen precipitously in the polls, decided to respond by breaking one of its core promises to its voters: Never collaborate with the left.

Salvini and his party were ousted from government and replaced by an unpopular center-left party as a coalition partner.

Not Game Over

Salvini lost power in Italy, but he may still have the last laugh. As a minister, he gained respect and popularity not only in Italy but all over Europe. He had proven that illegal immigration could easily be stopped by cracking down on N.G.O. human trafficking. During his administration, the Italian government also threatened to cut funding for the U.N. and invest at least €1 billion in North Africa to prevent migrants from trying to cross illegally into Italy.

These and other policies have rendered The League the most popular party, with the potential to govern alone, or possibly with the national-conservative Brothers of Italy.

However, much can still happen. The next general election may come as late as 2023, and by that time, Italy’s political landscape may have radically changed. The underlying issues and problems with migration and multiculturalism are not going away. All over the world, national populist parties are surging, and the most likely outcome of the next election is, therefore, that Salvini will be the next prime minister with a similarly robust mandate as Prime Minister Boris Johnson in the U.K.

Europe Scrambles As Heiko Maas Declares “Beginning Of The End” For Iran Nuclear Deal

Many have naturally predicted that the first two things to go following the Soleimani assassination will be American troops from Iraq and the 2015 Iran nuclear deal. Indeed Iran this weekend declared that its conformity to any remaining aspects to the deal will go out the window.

And in confirmation of Tehran’s Sunday “no limits” declaration that it will fully blow past uranium enrichment limits, German foreign minister Heiko Maas warned on Monday the killing of Soleimani marks the “first step towards the end” of the nuclear deal.

“What was announced is not in line with the nuclear agreement… [the situation] has not got easier, and this could be the first step towards the end of this agreement, which would be a big loss,” Maas told German public radio station Deutschlanfunk. “We will now weigh this up very, very responsibly,” he added.

File image via YNet News

Meanwhile the European signatories to the 2015 JCPOA, which have consistently attempted to salvage the deal since the US withdrew in May 2018, are urging Tehran to come back to its commitments. Britain, France, and Germany are demanding that Iran reverse the countermeasures adopted since the Trump administration’s withdrawal from the deal.

A joint statement from Boris Johnson, Emmanuel Macron, and Angela Merkel issued a joint statement on Monday calling for the Islamic Republic to refrain from further “proliferation” and “to reverse all measures inconsistent with the JCPOA.”

However, as Bloomberg notes, “The statement was noteworthy for not mentioning Trump or the U.S. action explicitly.”

The Europeans seem to be largely paralyzed in the wake of the unexpected and brazen US action to take out Iran’s most important military general.

German Foreign Minister Heiko Maas during a prior visit to Iran, file image.

What is clear is that it has taken more than 48 hours for Macron, the U.K.’s Boris Johnson and Germany’s Angela Merkel to issue a common stance calling for a reduction of tensions — showing they may be struggling to hold a united front.

Commenting on the European ambivalence Secretary of State Mike Pompeo told Fox News on Sunday: “Frankly, the Europeans haven’t been as helpful as I wish that they could be.”

The US top diplomat added: “The Brits, the French, the Germans all need to understand that what we did, what the Americans did, saved lives in Europe as well.”

{kind=link}

{kind=link}