When people tick off the components of the “everything bubble” they usually omit US housing, for a couple of reasons.

First, bubbles don’t normally recur immediately in the same asset class, because memories of past carnage need to fade before investors can be seduced back into irrational optimism. Since housing was the epicenter of the last boom/bust cycle, no one is looking there for evidence of new bubbles.

Second, the action in housing has been more gradual than in the 2000s, so it hasn’t generated a lot of breathless headlines about speculators making killings with other people’s money.

But this expansion has gone on for such a long time that even modest annual price gains have taken home prices back into bubble territory. And now the news is starting to reflect it. From today’s DollarCollapse.com “Real Estate” links list:

To recap, home prices are above their 2007 bubble peaks in many places while the wages of potential homebuyers have barely risen, which is squeezing ever-larger numbers of people out of the market.

Yet somehow the buying continues. This may not qualify as a mania, but it’s definitely looking dysfunctional, because where can a sector go from “record low affordability” if it wants to keep rising?

Going forward, one of two things has to happen.

Either buyers go on strike, as they (and their mortgage lenders) recognize that houses are a bad deal at current prices and mortgages written at those prices are unlikely to be paid off.

Or the government tries to keep the party going by lowering interest rates to make future mortgages easier to manage.

Since a dramatic slowdown in the housing market would take the rest of nominal GDP down with it, that will of course be seen as unacceptable, leading calls for lower rates, a weaker dollar and various other kinds of stimulus like tax cuts paid for with bigger deficits.

Put another way, even if housing doesn’t crash, the need to keep prices elevated is one more impetus for what looks like a tidal wave of monetary ease coming our way.

As we head into year-end, Goldman Sachs continues its tradition of taking stock of Top of Mind themes and highlighting what to look for next year.

On the heels of a 2018 characterized by solid growth and poor asset performance, 2019 has delivered the reverse. Indeed, growth has slowed considerably over the past year with our global current activity indicator (CAI) currently running around 2.6% versus 3.4% on average in 2H 2018. Meanwhile, a simple US 60/40 portfolio had one of the best risk-adjusted returns since the 1960s.

The strong asset performance was driven in large part by the Fed’s dovish pivot early in the year. With other central banks around the world following suit, easier monetary policy pushed rates globally down to or beyond historical lows. These shifts marked a decisive turn in the equity market cycle with equity markets—feeling somewhat comforted by the so-called “Powell put”— reaching new highs. In fact, equities had one of their best years since the initial recovery from the Global Financial Crisis, but almost all of the gains came from multiple expansion rather than profit growth, which was close to flat or even negative across the major economies.

This large market disconnect – with bond yields at or near all-time lows and equity indices at all-time highs—raised questions about how markets were viewing the growth outlook, and whether that view differed between bonds and equities—with equities just more optimistic. Our short answer: no. That’s because, scratching under the surface, equities were pricing their fair share of growth concerns as reflected, for example, in the outperformance of defensive sectors for much of the year.

Indeed, growth concerns prevailed for most of 2019 owing largely to the ongoing US-China trade war, which escalated further when President Trump imposed new tariffs on China in September and threatened additional tariffs slated for later in a “currency manipulator” following a sharp depreciation in the Yuan, which has helped to somewhat offset the impact of the trade war on the Chinese economy. As a result, currency wars became a new front in the ongoing trade war. And this development has evolved beyond US-China relations; President Trump recently announced his intention to impose tariffs on metals imports from Argentina and Brazil in response to the large depreciation in those countries’ currencies, which he argues is harming US farmers that compete with South American producers (but no official action has been taken.)

Beyond trade-related tensions, geopolitical risk also flared elsewhere later in the year, with Brexit uncertainty rising as the October 31st deadline for the UK withdrawal from the EU approached with no clear way forward, and a drone attack on Saudi Arabia’s Abqaiq oil processing facility—the largest such facility in the world—led to the single-largest disruption in global oil supply in history.

But looking ahead to 2020, we believe that some of these political/policy uncertainties that loomed over economies and markets this year are set to fade. In recent days, the US and China agreed to a “Phase 1” trade deal in which China has committed to large purchases of US goods and services as well as structural changes in areas ranging from intellectual property to currency policy in exchange for a cancellation of the next tranche of US tariffs and some rollback of existing tariffs. In our view, this likely marks the end of tariff escalation in the current US-China trade war.

And, just as the good trade news hit, the Conservatives won a decisive victory in the UK general election, finally clearing the path for an orderly withdrawal of the UK from the EU. This major hurdle for Europe was overcome in a year in which European elections led to critical leadership transitions on the continent that—despite fears of a growing populist influence— largely saw outcomes consistent with policy continuity.

Overall, we expect this decline in political uncertainty— combined with a positive impulse from financial conditions, a resilient consumer and some fiscal expansion in places like Europe (though likely not as much as they need) to lead to a sequential growth pickup in 2020, with global growth rising to 3.4% (from about 3.1% this year), led by the US and the UK.

We believe this sequential improvement should provide a broadly supportive environment for risky assets in 2020. That said, in recent months, markets have already begun to price a better growth outlook, which has been reflected, for example, in a sharp rotation towards pro-cyclical assets, and which has already pushed risky assets to relatively rich levels. And we don’t think monetary policy will provide a similar tailwind to markets this year given our expectation that the Fed—as well as the ECB and the BOJ—will keep interest rates on hold despite continued White House pressure for easier monetary policy. Although this pressure continues to raise concerns about central bank independence, with the Fed nevertheless recently pausing rate cuts, fears of political influence in central bank decision making doesn’t seem to be playing out so far (although we still view the bond markets as an indirect channel for such influence.)

In our view, all of the above suggests positive but lower returns across assets in 2020, with total equity returns across the major regions ranging from the mid-to high-single digits, US 10yr Treasury yields rising modestly above 2% and the Dollar index remaining relatively rangebound in the near term before weakening moderately on signs of improving global growth.

But while the growth and policy outlooks provide some reasons for mild optimism, of course political uncertainty is not entirely behind us. There is little doubt that the 2020 US presidential election in particular will be a major market focus throughout the year with policies on everything from taxes, to trade, to healthcare to buybacks (where we’ve still seen a fair amount of Congressional attention but no legislative action) all in question. But here we continue to emphasize that the outcome of the Congressional elections will likely be just as important as the presidential election in terms of material policy changes in most of these areas (save trade!).

In the words of the wise

“Central banks should have constrained missions centered on maintaining monetary system stability…The more they stray into other areas, the greater the distributional effects, and so the greater the temptation-or even the need-to re-politicize them by the back door.”

– Sir Paul Tucker, Former Deputy Governor, Bank of England

“People underestimate how reliant on liquidity the global financial system has become; at almost 40% of GDP, global liquidity is crucial.”

– Rick Rieder, CIO of Global Fixed Income, BlackRock

“There is now only a limited amount of stimulant left in the bottle, and the sooner we use it, the sooner it will run out.”

– Ray Dalio, Founder and Co-CIO, Bridgewater Associates

“Fundamentally…not much has changed… it’s just that the market swung from looking at things optimistically to looking at them pessimistically.”

– Howard Marks, Co-founder and Co-Chairman, Oaktree Capital Management

“It is crucial to have a group of people who analyze the economy with respect to the long-run goals of economic policy…politicians have a much shorter timeframe in mind than is consistent with achieving these goals.”

– Donald Kohn, Former Vice Chair, US Federal Reserve

“There is no shortage of things to worry about. I would simply say…that as the US continues to pull back, its alliances grow weaker, and international institutions fail to keep up with new challenges, instability is likely to go up in the world. So the future is likely to be far more turbulent than the recent past.”

– Richard Haass, President, Council of Foreign Relations

“At the ELB—when monetary policy is constrained—the case for fiscal policy to support demand and help maintain output at potential becomes compelling.”

– Olivier Blanchard, former Chief Economist, IMF

“Given the behavior of the past several years, I would not rule out additional [ECB] policy mistakes, such as a rate hike even if it is unwarranted…there seem to be other factors-legal challenges, politics-that influence [ECB] decisions.”

– Athanasios Orphanides, former member, ECB Governing Council

“ If a company buys back stock for the wrong reasons and good investments are turned down, that is troubling. But addressing that problem requires a scalpel not a bludgeon.”

– Aswath Damodaran, Professor, NYU Stern School of Business

“Trapping resources in larger and older businesses not only inhibits the overall size of the pie…but also tends to reinforce the unequal distribution of the pie.”

– Steven Davis, Professor, The University of Chicago Booth School of Business

“The reality is that the EU is a challenging project. But even today the forces of integration are stronger than the emboldened forces of disintegration.”

– Jose Manuel Barroso, fmr. President of European Commission

“The US is underestimating the influence of the hardliners, or hawks, in China and the degree to which Chinese nationalism and anti-American sentiment has grown since the early 1990s. This is the biggest mistake we have made over the last several decades.”

– Michael Pillsbury, Director for Chinese Strategy, Hudson Institute

“While I don’t think the Fed is cutting rates because the White House is telling them to, you can’t completely separate the politics from the market signals feeding into the Fed’s decision-making.”

– Jan Hatzius, GS Chief Economist

“ The complexity for the US is that the more the US intensifies the trade war, the more pressure there is for a weaker Yuan. And the challenge for the world is that if China tries to offset weak trade with the US with a weaker Yuan, that puts more pressure on other economies to depreciate their currencies in order to avoid losing out to China.”

– Brad Setser, Senior Fellow, Council on Foreign Relations

“Trump’s actions have led to a more unified nationalist resentment of the US-and a view that not just Trump, but American society, is trying to contain China’s rise.”

– Susan Shirk, Chair, 21st Century China Program

“The likelihood that President Trump wakes up and says it’s time to go to war with Iran is probably zero. His lack of desire for another war in the Middle East is one of the few positions he’s maintained consistently from the get go.”

– Richard Nephew, Senior Research Scholar, Columbia University

“I think we should keep a longer-term perspective. Yes, interest rates are low, and they may be low for a while, but they won’t be low forever. And when they rise of course the cost of debt will increase again.”

– Alberto Alesina, Professor, Harvard University

“Just because manipulation is a smaller concern today doesn’t mean it will stay that way. I worry that it will be a problem in the next recession.”

– Joseph Gagnon, Senior Fellow, Peterson Institute for International Economics

Revisiting 2019 Themes… Crossword Style

Source: Goldman Sachs

Across:

2. This treaty that was implemented in 2009 gave expanded powers to the European Parliament (Issue 78).

7. According to Richard Haass, President of the Council on Foreign Relations, the Middle East matters for many reasons beyond just _____ resources (Issue 83).

11. After rate cuts and quantitative easing programs, the financial world is now often described as awash with _____ (Issue 80).

12. Athanasios Orphanides, fmr. member of the ECB Governing Council, believes that the _____ guided inflation too low by not allowing its balance sheet to expand sufficiently after the global financial crisis (Issue 76).

13. In 2014, government purchases of _____ currencies declined significantly as the global economy recovered (Issue 82).

14. Ray Dalio, Founder and Co-CIO of Bridgewater Associates, is concerned that _____ policy will be dangerously low on power in the next few years (Issue 80).

15. Michael Pillsbury, Director for Chinese Strategy at the Hudson Institute, argues it is imperative that China earn its way out of _____—a view that President Trump has consistently held (Issue 79).

21. Steven Davis, Professor at the University of Chicago Booth School of Business, believes that buybacks don’t affect the level of _____ in the economy; they only affect its distribution (Issue 77).

22. The Federal Reserve does not have a mandate to target the _____ rate (Issue 82).

24. With markets performing well after the Fed’s dovish pivot, some observers have suggested that there is “a _____ put” on the S&P 500 (Issue 76).

25. Howard Marks, Co-Founder and Co-Chairman of Oaktree Capital Mgmt., believes that over the past two years, markets were excessively _____ (Issue 75)

26. Joseph Gagnon, Senior Fellow at the Peterson Institute for International Economics, worries that currency _____ will be a problem in the next recession (Issue 82).

27. Given substantial evidence of a large tax _____, Alberto Alesina, Professor of Political Economy at Harvard University, believes that any fiscal expansion should focus on cutting taxes rather than on increasing spending (Issue 84).

28. The notion that debt accumulation reduces capital formation is only true when the economy is at full _____ (Issue 84)

29. _____ took out an ad in the NY Times in 1987 to discuss how the US was being disadvantaged by foreign countries in the trade area (Issue 79).

30. Support for _____ parties has increased significantly across Europe (Issue 78).

Down:

1. The Trump administration’s policy toward Iran included pulling out of the 2015 _____ agreement (Issue 83).

3. The Federal Reserve set itself an inflation target under the chairmanship of _____ (Issue 81).

4. Buybacks have been the single largest source of US _____ demand each year since 2010 (Issue 77).

5. Over the past several years, rising _____ were the main drivers of global equity returns (Issue 75).

6. Historically, the Federal Reserve has had to cut rates by roughly_____ percentage points on average during recessions (Issue 80).

8. This country has the largest amount of seats in the European Parliament (Issue 78).

9. The Federal Reserve ended its balance sheet _____ sooner than expected (Issue 76).

10. Olivier Blanchard, fmr. Chief Economist of the IMF, does not blame fiscal or monetary policy for weak growth in Japan, instead saying it has to do with _____ (Issue 84).

16. Aswath Damodaran, Professor at the NYU Stern School of Business, thinks of buybacks as _____ dividends, in that they can vary from year to year depending on how much cash a company has (Issue 77).

17. US economic recoveries have never lasted more than this many years (Issue 75).

18. Susan Shirk, Chair of the 21st Century China Program at UC San Diego, believes that _____ technologically from China will ultimately weaken US technological innovation (Issue 79).

19. Sir Paul Tucker, fmr. Deputy Governor of the Bank of England, regards central banks as the _____ pillar of unelected power (Issue 81).

20. US sanctions imposed on Iran over the past two years have included a demand that oil exports effectively go to _____ (Issue 83).

23. Donald Kohn, fmr. Vice Chair of the US Federal Reserve, believes that central bank independence is still important today despite an environment of low _____ (Issue 81).

* * *

Finally, here’s Howard Marks

“I don’t believe that we’re in a bubble, and I don’t think we’re going to have a crash…But for an investor, I think the next five years simply aren’t going to be as good as the last ten.”

– Howard Marks, Co-Founder and Co-Chairman, Oaktree Capital Management

As a busy 2019 in the oil and gas industry ends, analysts are busy issuing predictions about next year and what they would mean for oil markets and prices.

This year saw a mix of some of the more predictable events – such as OPEC and Russia extending their cooperation pact, twice – and a ‘black swan’ such as the September attacks on Saudi oil facilities which cut off 5 percent of daily global oil supply for weeks.

As black swans are, by definition, unpredictable, analysts focus on predicting the ‘knowns’ in the market for 2020 as they see them at the end of 2019.

There are many factors to watch in oil markets next year, both in the U.S. and globally.

For the sake of simplicity, here are 10 of the most important predictions and factors to watch in the oil and gas industry in the United States and worldwide.

Independent energy analyst David Blackmon has summed up some predictions, concerning mostly the U.S., for Forbes.

And these are:

1) U.S. shale production will continue to grow

U.S. shale growth is slowing down, but all analysts and organizations still expect oil supply from the United States to continue to rise in 2020. Growth may be slower, due to reduced capex from drillers, but U.S. will still be the main contributor to non-OPEC supply growth next year.

2) Rig count will remain stable

Despite the fact that the U.S. oil and rig count declined by more than 250 units this year to December 20 compared to the same time last year, the number of active oil rigs last week saw an increase of 18 rigs—the first double-digit growth since the beginning of April, according to Baker Hughes data.

3) U.S. oil and LNG exports will continue to rise

Exports of U.S. oil and liquefied natural gas (LNG) are expected to grow with the increase in infrastructure capacity in 2020.

The United States exported more crude oil and petroleum products than it imported in September 2019—the first month in which America was a net petroleum exporter since monthly records began in 1973, the U.S. Energy Information Administration (EIA) said earlier this month.

Total U.S. crude oil and petroleum net exports are expected to average 570,000 bpd in 2020 compared with average net imports of 490,000 bpd in 2019, according to EIA’s latest Short-Term Energy Outlook (STEO).

4) Oil and gas prices will remain range-bound in 2020

Rising production from non-OPEC nations not part of the OPEC+ deal, driven by the U.S., Brazil, and Norway, is expected to keep a lid on oil prices, while OPEC+ cuts and an expected pick-up in global economic and oil demand growth will keep a floor under prices.

5) Sudden supply outages will have smaller impact on oil prices

Due to the growing non-OPEC supply, unexpected and short-lived outages are likely to have a smaller impact on oil prices than they would have on markets five or ten years ago, analyst Blackmon says.

Case in point—the mid-September attacks on critical Saudi infrastructure sent oil prices soaring—with WTI Crude touching a five-month high of $62.90 a barrel—but just for one day, as slowing demand growth and a protracted trade war weighed on prices.

6) Bankruptcies in the U.S. shale patch are set to grow

The number of bankruptcies and companies seeking protection from creditors is expected to rise in 2020, continuing the trend from 2019.

Haynes and Boone estimated at end-September that the U.S. oil and gas industry had 33 filings year to date in September, more than the number of filings in each of 2017 and 2018, at 24 and 28 filings, respectively.

With reduced capital availability in equity and debt markets, more of the smaller companies could struggle through the next year.

7) U.S. oil and gas mergers & acquisitions are poised to rise

A growing number of distressed U.S. oil and gas firms and few funding options could mean that the ‘smaller guys’ could be acquired by bigger shale players or the smaller guys could team up to scale operations and cut costs.

Signs of consolidation in U.S. shale have already started to emerge, and the wave is expected to continue in 2020.

Shareholders of Callon Petroleum and Carrizo Oil & Gas approved an all-stock merger last week.

Two months ago, Parsley Energy and Jagged Peak Energy announced that Parsley would buy Jagged Peak in an all-stock transaction valued at US$2.27 billion, including Jagged Peak’s debt.

“The inevitable consolidation in the Permian has started and Jagged Peak made a decisive move to team up with the right partner,” said S. Wil VanLoh, Jr., a Jagged Peak director and the founder and CEO of Jagged Peak’s controlling shareholder, Quantum Energy Partners.

In its Q3 2019 Oil & Gas deals insights, PwC said:

“In the quarters ahead, we expect to see more companies merging to create scale, companies continuing to focus on generating positive cash flows and shareholder value, while struggling companies will become more amenable to being acquired or seeking restructuring through bankruptcy.”

Internationally, the key factors to watch in oil markets will be:

8) How oil demand growth will fareas the U.S.-China trade dispute de-escalates

Oil prices hit a three-month high on December 13 amid growing optimism of a phase-one trade deal. In the days following the announcement that a phase-one deal had been reached, China removed six chemicals and oil derivatives from its list of tariffed U.S. imports.

9) How OPEC+ cooperation will proceed after March 2020

Another key factor to watch is what OPEC and its Russia-led non-OPEC partners will do after March 2020, when the current agreement for deeper cuts expires. The next move by the cartel and its allies will largely depend on how oil demand growth will fare in the typically low-demand growth season in Q1. The move will also depend on how much oil OPEC and friends will have managed to withhold from the market compared to plans—that is, whether all members will have fallen in line and stopped cheating.

10) Sudden supply outages in restive regions

Oil market participants will continue to monitor developments in Libya and Iraq, which could suddenly tighten the market more than anyone had intended to.

After yesterday’s dismal 2Y auction, which printed at the lowest bid to cover since 2008, few were looking forward to today’s 5Y auction which would come in an environment of even worse liquidity coupled with a continued selloff across the Treasury complex this morning.

Yet to everyone’s surprise, the sale of $41 billion in 5Y notes was nothing short of stellar, with the high yield coming in at 1.756%, which while above last month’s tailing stop of 1.587%, stopped through the When Issued 1.772% by a whopping 1.6bps, the biggest stop through since February 2016!

Also unlike yesterday’s disappointing 2Y auction, the internals today were quite impressive, with the bid to cover virtually unchanged from November’s 2.50, at 2.49, the second best since July 2018, and well above the 2.38 six auction average.

Finally the takedown was also on the strong side, with Indirects taking down 62.4%, above the recent average of 59.9%, and with Directs taking down 16.1%, the most since August 2019, Dealers were left holdings 21.5%.

In kneejerk response to the stellar 5Y auction, yields have tumbled across the curve which was to be expected for an illiquid session, yet the 10Y rate plunging from 1.94% just before the auction to a sub 1.90% print shows just how little liquidity there is in the bond market at this moment.

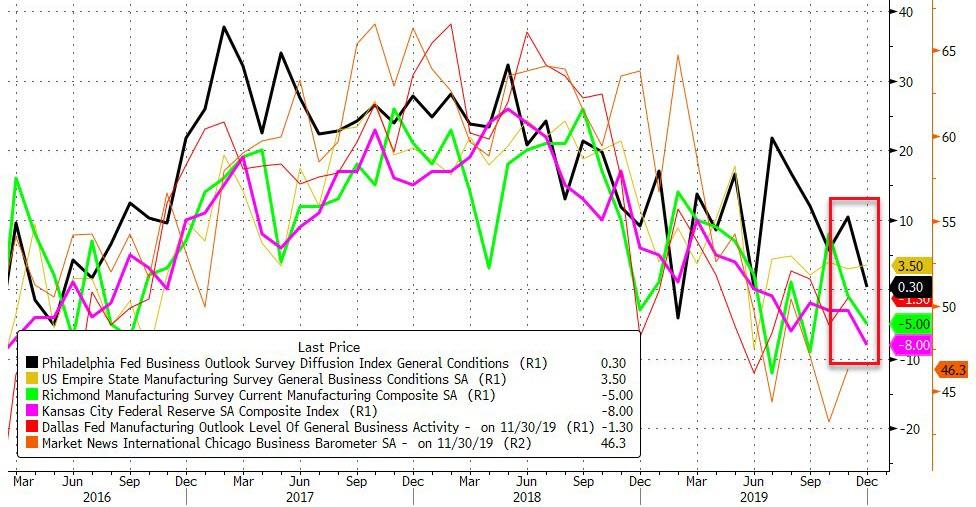

Richmond Fed Tumbles Into Contraction, Confirms Regional Fed Survey Slump

Confirming the pessimistic plunges in Kansas City and Philadelphia, The Richmond Fed’s Manufacturing Survey disappointed, tumbling to -5 from -1 last month (and expectations of a bounce to +1).

Source: Bloomberg

Under the hood was more worrisome:

Shipments fell to -6 after -2 the prior month

New order volume slowed to -13 after -3 the prior month

Order backlogs were unchanged at -11 after -11 the prior month

Capacity utilization slowed to -12 after 2 the prior month

Inventory levels of finished goods increased to 22 after 15 last month

Inventory levels of raw goods rose to 21 after 20 last month

So, inventories up, new orders and shipments tumbling?! Doesn’t sound like a renaissance in America to us.

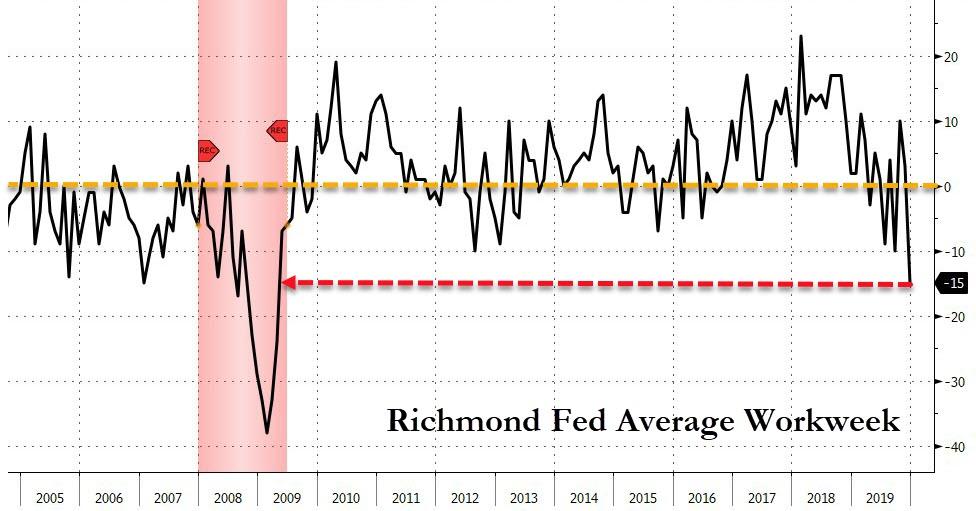

And the average workweek crashed to its worst since April 2009…

Source: Bloomberg

Of course, as long as the PMIs are rebounding no one will pay attention to this… yet

House Democrats may conduct a second impeachment of President Trump, according to lawyers for the Judiciary Committee.

In a Monday court filing reported by Politico, House Counsel Douglas Letter argued that they still need testimony from former White House counsel Don McGahn, which may uncover new, impeachable evidence that Trump attempted to obstruct the Russiagate investigation (of a crime he didn’t commit).

“If McGahn’s testimony produces new evidence supporting the conclusion that President Trump committed impeachable offenses that are not covered by the Articles approved by the House, the Committee will proceed accordingly — including, if necessary, by considering whether to recommend new articles of impeachment,” reads Letter’s filing.

Underscoring this point, House lawyers say if McGahn’s testimony yields more evidence of obstruction it could lead to “new articles of impeachment.” pic.twitter.com/DXiEl0KXwL

The Democrats also argue that “McGahn’s testimony is critical both to a Senate trial and to the Committee’s ongoing impeachment investigations to determine whether additional Presidential misconduct warrants further action by the Committee,” adding that McGahn’s testimony may also be relevant to future legislation which may stem from the details of Trump’s conduct.

And while DOJ lawyers acknowledged in a Monday brief that the legal fight over McGahn isn’t moot, the fact that the House Judiciary Committee moved forward with impeachment on a completely different matter removes the urgency to resolve their case.

“The reasons for refraining are even more compelling now that what the Committee asserted — whether rightly or wrongly — as the primary justification for its decision to sue no longer exists,” wrote lawyers for the DOJ. The agency also argues that the Mueller impeachment investigation is over, when House lawyers and lawmakers have described it as ongoing and active, according tothe report.

McGahn’s participation in House impeachment proceedings was blocked by the White House, which claimed “absolute immunity” for advisers.

President Trump chimed in over Twitter followingthe Monday court filing, quoting “Fox and Friends” host Brian Kilmeade, who said “now all of a sudden they are saying maybe we’ll go back and visit the Mueller probe, which is absolutely unbelievable, and shows they don’t care about the American public’s tone deafness…”

….the American public’s tone deafness – & it should be intolerable, because the American people have had it with this.” @kilmeade@foxandfriends The Radical Left, Do Nothing Democrats have gone CRAZY. They want to make it as hard as possible for me to properly run our Country!

DOJ attorneys argued that the upcoming Senate trial is yet another reason for the judicial branch to refrain from the case.

“If this Court now were to resolve the merits question in this case, it would appear to be weighing in on a contested issue in any impeachment trial,” wrote DOJ lawyers. “The now very real possibility of this Court appearing to weigh in on an article of impeachment at a time when political tensions are at their highest levels — before, during, or after a Senate trial regarding the removal of a President — puts in stark relief why this sort of interbranch dispute is not one that has ‘traditionally thought to be capable of resolution through the judicial process.’”

“This Court should decline the Committee’s request that it enter the fray and instead should dismiss this fraught suit between the political branches for lack of jurisdiction,” they added.

The highly probable and downright inevitable unwind of today’s trifecta of financial asset bubbles: stocks, corporate credit, and Treasury bonds may soon morph into brutal bear market. The end game is unstoppable in our view and approaching fast. The Fed is between a rock and a hard place. It has been printing money like it’s the depth of the Global Financial Crisis while stocks and corporate credit are flying high reflecting a dangerous combination. The panic stimulus at this point in the business cycle is completely understandable, but it is only hastening the unwind of the imbalances the central bank has created and been impossibly trying to maintain. The idea that money printing is an insurance policy that does not come with a cost is simply wrong.

Repo Crisis

The Fed is in fight-or-flight mode because there are very real credit bottlenecks in the plumbing of the banking system that have created a US Treasury funding emergency. The central bank has been forced to add $364 billion of Treasury securities to its balance sheet over last four months and has committed to another $471 billion though mid-January. The money printing was necessary to fight a repo market funding shortage that warns of a systemic financial crisis in the making. Usually when the repo alarm bell flashes, it’s too late. Because of the Fed’s swift action, mayhem was averted but likely only in the very short-term. Major imbalances remain. One huge problem is that investors at large do not even know what a repo crisis means, so they have been interpreting the cash injections as a reason to go all in on risky assets. The bullish investor sentiment and positioning among investors last week reached the highest levels we have ever seen. Such ebullience in the past has been associated with major stock market tops. Today, we have structural imbalances and catalysts to make that a highly likely scenario, potentially even as we head into year end.

The Fed miscalculated the level of reserves it should have kept in the system so that banks can smoothly supply credit to the securities and FX markets and fulfill their regulatory capital requirements at the same time. So, it was a complete surprise on September 17, when US Treasury repo funding market froze up and the overnight rate jumped as high as 10% that day. Since then, the Fed has been trying to prevent a disorderly deleveraging of the entire financial system. Short-term interbank lending is the core of the entire financial system. When repo rates spike, it means there is not even enough cash in the system for banks to support the Treasury market, let alone the rest of the securities and FX markets to allow their normal functioning. For instance, when the repo rate jumped in September 2008, it froze the global financial system and bankrupted Lehman Brothers, so it’s a big problem.

The repo rate is also the short-term financing cost for financial institutions such as hedge funds to buy Treasury securities on margin including buying long duration Treasuries to speculate on a declining interest rates and/or deflation. It is one side of the popular risk parity trade among large hedge funds and institutional investors. In 2019, investors crowded into long duration Treasuries as the yield curve inverted in anticipation of a recession. The 10-year yield had its biggest year-over-year decline ever. After such a move, this trade simply became too crowded. In our view, it has already played out. Today, we believe there is a strong case for rising global yields on the long end of the curve as we explain below.

One thing the average investor is likely not paying attention to is the selloff on the long end of the Treasury curve which indicates that the repo funding problem may not been contained yet. Rising long-dated yields preceded the September shock and have only continued during the emergency Fed injections. Large hedge funds and institutions have crowded into leveraged long bond positions which rely on repo funding. If credit tightness continues these positions could be forced unwind creating more market instability necessitating the official beginning of the QE4. It’s key to note that it’s not just US Treasuries but the entire global sovereign long end that has been selling off.

Running Hot

The Fed’s monetary policy is running hot and long-term interest rates aren’t aligned accordingly. John Taylor, a Stanford University economist once considered to lead the Federal Reserve, developed a formula to calculate where the Fed funds rate should hypothetically be according to inflation rates, strength of the labor market, and potential output of the economy. Using that as our baseline for interest rates, the Fed isn’t just running an aggressive inflationary policy on the short end of the curve, long-term rates are also notably out of balance. For instance, the 10-yr yield vs. the Baseline Taylor Rule rate is now at its most extreme in 44 years. Inflation became a problem during all times this spread went negative. What makes this issue even more unique is the fact that on top of running an extreme loose rate policy, the Fed is printing money in a massive way. It’s hard to say monetary policy won’t come at a major cost this time.

This is not only a domestic phenomenon. We see this issue worldwide. Germany’s case, for instance, is twice as extreme. According to the Taylor rule formula, short term interest rate should be close to 8%. In contrast, ECB rates are close to -0.5% while bunds’ 10-year yields are at -0.22%. The spread of between German long-term rates and its baseline Taylor rule rate is now at its highest level in history.

Below are similar disparities across the globe to consider. Most of them are in Europe, but almost the entire world should start seeing more pressure on long-term interest rates to rise while global central banks continue to run aggressive monetary policies to foster a global economic expansion now nearing exhaustion while funding record indebted governments.

The Labor Market and Consumer Confidence – Falling into Place

Stocks are on pace for their best performance in 22 years all the while many key fundamentals such as corporate earnings and industrial production have been deteriorating all year. Continued gains for the broad stock market in 2020 are highly improbable in our view as even more of the key fundamentals in the jobs and consumer market are only just starting to roll over from exuberant extremes.

Among the many imbalances and catalysts we cited in last month’s recent research letter, the over-extended labor market is showing significant signs of cooling. The lagging and contrarian unemployment rate from the Bureau of Labor Statistics remains near cycle lows, just like it always does at the peak of a business cycle, right before a market downturn and recession. Meanwhile, three leading employment indicators are showing signs of significant cracks:

(1) Declining BLS Job Openings;

(2) Spiking DOL Initial Jobless Claims; and

(3) A recent plunge in the ADP Employment Report

The ADP report calls into question the more optimistic BLS job numbers with the largest negative divergence since 2010. The year-over-year change for ADP payrolls is decelerating in a pattern last seen directly ahead of the Global Financial Crisis. What’s crucial is that the 3-month rolling average of ADP payrolls leads the rate of change in unemployment rate by 3 months with a correlation of almost 0.9!

We have likely reached peak consumer complacency, another key piece of the macro puzzle. After retesting tech bubble levels, the Bloomberg Personal Finance Survey index is now falling and significantly diverging from the Conference Board’s Consumer Confidence. With the jobs market topping out, we believe consumer confidence will be the next shoe to drop.

Cost of Capital Poised to Rise

The bull case for stocks rests on one major liquidity force, the cost of capital. That’s driven by the availability of credit and the strength of company fundamentals. When looking at equities broadly, aggregate earnings per share for Russell 3000 index just started to fall on a year over year basis. Furthermore, corporate balance sheets never looked so weak. Leverage ratios are at record highs, and in contrast, companies with a junk credit status are now borrowing money at their lowest levels since the peak of the housing bubble. For instance, the Bloomberg Barclay High Yield (Ex-Energy) Index today is at its lowest premium to 10-year Treasuries since June of 2007.

When default risk returns and interest rates spike higher, many of these low-credit-quality businesses will not survive. Since WeWork had to scrap its plans to go public and other recent new issues broke below their IPO price, investors have been turning their focus away from top-line growth towards companies that have underlying free cash flow profitability, or at least a clear path to get there soon. We believe this shift in mindset is already forcing companies to either raise prices of goods and services or cut costs to improve margins, and we expect this trend to continue. These changes should have a significant impact on consumer prices, labor markets, and the business cycle.

In this backdrop, we question if the demand for low-rated bonds will remain strong relative to higher quality assets. Junk bonds only yield 180 basis points higher than median CPI! It’s the lowest level in the history of the data.

To add to the bearish thesis, the 3-month implied volatility for put options on JNK, a high yield corporate bond ETF, is now at its lowest level ever. Prior cyclical lows in volatility preceded significant selloffs in this ETF as well as overall stocks. We view this as an opportunistic entry point to short junk bonds ahead of a business cycle downturn that is fast approaching.

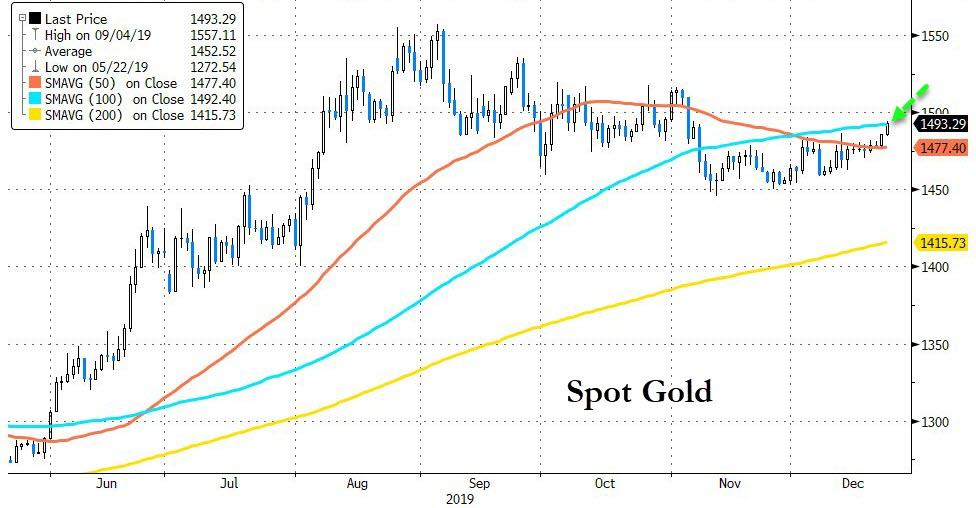

Precious Metals

Precious metals are poised to benefit from what we consider to be the best macro set up we’ve seen in our careers. The stars are all aligning. We believe strongly that this time monetary policy will come at a cost. Look in the chart below at how the new wave of global money printing just initiated by the Fed in response to the Treasury market funding crisis is highly likely to pull depressed gold prices up with it.

The imbalance between historically depressed commodity prices relative to record overvalued US stocks remains at the core of our macro views. On the long side, we believe strongly commodities offer tremendous upside potential on many fronts. Precious metals remain our favorite. We view gold the ultimate haven asset to likely outperform in an environment of either a downturn in the business cycle, rising global currency wars, implosion of fiat currencies backed by record indebted government, or even a full-blown inflationary set up. These scenarios are all possible. Our base case is that governments and central banks will keep their pedals to the metal to attempt to fend off credit implosion or to mop up after one has already occurred until inflation becomes a persistent problem.

The gold and silver mining industry is precisely where we see one of the greatest ways to express this investment thesis. These stocks have been in a severe bear market from 2011 to 2015 and have been formed a strong base over the last four years. They are offer and incredibly attractive deep-value opportunity and appear to be just starting to break out this year. We have done a deep dive in this sector and met with over 40 different management teams this year. Combining that work with our proprietary equity models, we are finding some of the greatest free-cash-flow growth and value opportunities in the market today unrivaled by any other industry. We have also found undervalued high-quality exploration assets that will make excellent buyout candidates.

We recently point out this 12-year breakout in mining stocks relative to gold now looks as solid as a rock. In our view, this is just the beginning of a major bull market for this entire industry. We encourage investors to consider our new Crescat Precious Metals SMA strategy which is performing extremely well this year.

Zero Discounting for Inflation Risk Today

With historic Federal debt relative to GDP and large deficits into the future as far as the eye can see, if the global financial markets cannot absorb the increase in Treasury debt, the Fed will be forced to monetize it even more. The problem is that the Fed’s panic money printing at this point in the economic cycle may hasten the unwinding of the imbalances it is so desperate to maintain because it has perversely fed the last-gasp melt up of speculation in already record over-valued and extended equity and corporate credit markets. It is reminiscent of when the Fed injected emergency cash into the repo market at the peak of the tech bubble at the end of 1999 to fend off a potential Y2K computer glitch that led to that market and business cycle top.

After 40 years of declining inflation expectations in the US, there is a major disconnect today between portfolio positioning, valuation, and economic reality. Too much of the investment world is long the “risk parity” trade to one degree or another, long stocks paired with leveraged long bonds, a strategy that has back-tested great over the last 40 years, but one that would be a disaster in a secular rising inflation environment.

With historic Federal debt relative to GDP and large deficits into the future as far as the eye can see, rising long-term inflation, and the hidden tax thereon, is the default, bi-partisan plan for the US government’s future funding regardless of who is in the White House and Congress after the 2020 elections. The market could start discounting this sooner rather than later.

The Fed’s excessive money printing may only reinforce the unraveling of financial asset imbalances today as it leads to rising inflation expectations and thereby a sell-off in today’s highly over-valued long duration assets including Treasury bonds and US equities, particularly insanely overvalued growth stocks. We believe we are in the vicinity of a major US stock market and business cycle peak.

T. Rowe Price Invests $1.3 Billion In Rivian EV Startup As It Dumped Tesla In 2019

Baltimore-based T. Rowe Price Associates Inc. plowed nearly $1.3 billion in the latest investment round into electric vehicle (EV) startup Rivian on Monday, reported Reuters.

T. Rowe and BlackRock Inc. were the two major players in the latest investment round for the Plymouth, Michigan-based company as it gears up to compete with Tesla.

“This investment demonstrates confidence in our team, products, technology, and strategy,” Rivian CEO RJ Scaringe said in a statement.

T. Rowe spent the first half of 2019 dumping at least 80% of its shares of Tesla, while it has quietly funded companies that could be considered future competitors in the race to develop EVs.

Besides Rivian, the investment firm has made an equity investment in Cruise, the autonomous-automobile startup of General Motors Co. It has also invested in autonomous-vehicle startup Aurora Innovation Inc., whose CEO helped Alphabet build Waymo.

“T. Rowe Price is excited to invest in Rivian as it moves the innovation frontier forward with its compelling sustainable transport solutions for both consumers and businesses,” T. Rowe Price Growth Stock Fund Portfolio Manager Joe Fath said.

Amazon recently ordered 100,000 EV delivery vehicles from Rivian. The first Amazon EV vans will hit the roads in 2021.

Ford invested $500 million in Rivian in April and will support the startup in ramping up production in 2020.

“We want to maintain a meaningful value in the ownership and future of that company,” Ford spokesman T.R. Reid said.

Sources told Reuters last month that Rivian will be building a battery-powered Lincoln SUV, expected to be released in 2H22.

And as Elon Musk pumps shares of Tesla to $420.69, Tesla’s biggest institutional investor, Baillie Gifford, recently said Musk needs help running the company.

“He needs help, and I mean that psychologically as much as practically,” said Gifford.

T. Rowe’s quick jump in 2019 from Tesla to Rivian shows the competition is quickly expanding, and Musk’s EV domination is likely to fade in the early 2020s.

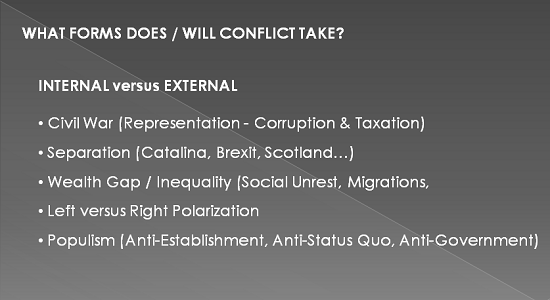

Geopolitics has moved from a slow-moving, relatively predictable chess match to rapidly evolving 3-D chess in which the rules keep changing in unpredictable ways.

A declining standard of living in the developed world, declining growth for the developed world and geopolitical jockeying for control of resources make for a highly combustible mix awaiting a spark: welcome to the era of intensifying chaos and the rapid advance of new weapons of conflict as ruling elites attempt to stamp out dissent and global powers pursue supremacy by whatever means are available.

Gordon Long and I discuss these dynamics in a new video The New Weapons of Conflict (28:30) that explores the drivers of increasing global chaos and a permanent state of intensifying conflict in both domestic (internal) and global (external) affairs.

Domestic conflict is erupting and intensifying across the globe: political polarization and populism, driven by soaring wealth/income inequality and the decay of the social contract and the erosion of standards of living, and social disunity and disorder as cooperation has failed to fix what’s broken.

Geopolitical conflicts are now expanding across a vast spectrum from endless wars in contested regions to cyber-meddling in other nation’s domestic affairs, cyber-warfare via theft of intellectual property and targeting essential digital infrastructure, economic sanctions and currency-based warfare, along with a wide array of disruptive military technologies, including “first strike”-enabling hypersonic weaponry, anti-missile technologies and space-based weaponry.

The relative stability of the Cold War has given way to a multi-polar world in which nations are competing with a host of other nations, including erstwhile allies and economic/trade rivals. Geopolitics has moved from a slow-moving, relatively predictable chess match to rapidly evolving 3-D chess in which the rules keep changing in unpredictable ways.

There’s much more in the program; click on either graphic to go to the video:

With so many sparks flying, the combustible mix is looking increasingly unstable, chaotic and risky.

{kind=link}