Stocks Tumble After Ross Says Trump Will Hike Tariffs If No China Deal By Dec 15

Following the latest dismal ISM data which sent US equity markets tumbling, traders were on the prowl for any hints what the US may do over the next major catalyst in the US trade war: the December 15 deadline for more tariffs.

An answer came moments ago when Commerce Secretary Wilbur Ross told Fox Business Network that President Trump will increase tariffs on China if Washington and Beijing can’t reach a trade agreement by the December 15 deadline.

“Well you have a logical deadline Dec. 15,” Ross told FOX Business’ Stuart Varney in an exclusive interview. “If nothing happens between now and then, the president has made quite clear he’ll put the tariffs in – the increased tariffs.”

Confirming that this is not just a hollow threat, Ross also explained that raising tariffs on Dec 15. won’t “interfere with this year’s Christmas” as retailers have already stocked up, adding that it’s a “really good time if we have to put more tariffs on.”

The fact that with exactly two weeks left until the tariff deadline the US is once again warning China that a deal has to be reached is hardly supportive of “optimism”, especially one day after China made it clear that it would only agree to a Phase 1 deal if the US agreed to roll back tariffs, something which Navarro would never agree as it would both destroy any leverage the US has over China and would crippled Trump’s negotiating credibility.

As a result, stocks which were already near session lows, took another leg lower…

… as did the Chinese yuan which continues to drift ever further away from the “lucky” 7 level.

Outraged By Trump’s Fake Orgasm, Lisa Page Gives ‘Teen Vogue’-Tier Pre-FISA Interview

With a week to go before the long-awaited DOJ Inspector General’s report on the FBI’s conduct surrounding the 2016 election, former agency lawyer Lisa Page would like everyone to know that she’s the real victim.

Speaking with the Daily Beast‘s Molly Jong-Fast, who challenged her on exactly nothing (such as whether she altered Mike Flynn’s 302 form, or what the ‘insurance policy‘ was, or if she coordinated with the Washington Post on a “media leak strategy”), Page insists that her hatred of Trump never influenced her work investigating him, and that while she prefers to live in obscurity – she was compelled to tell her side of the story after President Trump mocked her with a fake orgasm routine at a rally last month – and not because of IG Michael Horowitz’s FISA report due on December 9th.

Lisa Page is a “survivor” now.

Pay no attention to the IG report that said her corruption caused irreparable harm that “goes to the heart of the FBI’s reputation for neutral fact finding and political independence.” https://t.co/32cF4Fg2XX

Horowitz has circulated the report to key figures for legal review, and is rumored to clear to clear Page and other FBI officials of letting their raging hatred of Trump (and love of Clinton) color their work – hence the ‘Teen Vogue’ – tier puff piece. We’re sure she’ll go into greater detail when she writes a book on the whole ‘matter.’

Highlights

Trump’s Oct. 11 impression of her sleeping with Strzok pushed her over the edge. “Honestly, his demeaning fake orgasm was really the straw that broke the camel’s back.“

Her extramarital affair with FBI agent Peter Strzok while they were both investigating Trump and Clinton was “the most wrong thing I’ve ever done in my life.”

“And that’s when I become the source of the president’s personal mockery and insults. Because before this moment in time, there’s not a person outside of my small legal community who knows who I am or what I do. I’m a normal public servant, just a G-15, standard-level lawyer, like every other lawyer at the Justice Department.”

Page is”slightly crumbly around the edges the way the president’s other victims are,” and is experiencingsomething beyond PTSD.

Does it feel like a trauma? “It is. I wouldn’t even call it PTSD because it’s not over. It’s ongoing. It’s not a historical event that is being relived. It just keeps happening.”

…

“It’s almost impossible to describe” what it’s like, she told me. “It’s like being punched in the gut. My heart drops to my stomach when I realize he has tweeted about me again. The president of the United States is calling me names to the entire world. He’s demeaning me and my career. It’s sickening.”

Page is always on edge – avoiding people in MAGA hats as she lives in daily anguish.

“I’m someone who’s always in my head anyway—so now otherwise normal interactions take on a different meaning. Like, when somebody makes eye contact with me on the Metro, I kind of wince, wondering if it’s because they recognize me, or are they just scanning the train like people do? It’s immediately a question of friend or foe? Or if I’m walking down the street or shopping and there’s somebody wearing Trump gear or a MAGA hat, I’ll walk the other way or try to put some distance between us because I’m not looking for conflict. Really, what I wanted most in this world is my life back.”

In response to Trump suggesting she committed treason, Page insists “[T]here’s no fathomable way that I have committed any crime at all, let alone treason…“

Page insists that Trump wasn’t the target of the 2016 investigation into his campaign, and that the FBI learned of “the possibility that there’s someone on the Trump campaign coordinating with the Russian government in the release of emails, which will damage the Clinton campaign.”

“We were very deliberate and conservative about who we first opened on because we recognized how sensitive a situation it was,” Page says. “So the prospect that we were spying on the campaign or even investigating candidate Trump himself is just false. That’s not what we were doing.”

Her text messages with Strzok were ‘cherry picked’ and ‘out of context.’

Page felt abandoned by the FBI and Justice because of the release of the messages and because the bureau issued no statement defending her and Strzok. “So things get worse,” she continues. “And of course, you know, those texts were selected for their political impact. They lack a lot of context. Many of them aren’t even about him or me. We’re not given an opportunity to provide any context. In a lot of those texts we were talking about other people like our family members or articles we had sent each other.”

At the end of the day, Page wants us to know that she’s the real victim here. Perhaps she can provide those missing 19,000 text messages for some even better context?

“I’m completely nonpartisan you Walmart-smelling Trump supporters” – Lisa Page

A video out of China shows a man being called in and interrogated by authorities for the crime of criticizing the police on social media.

The clip shows the man handcuffed to a metal chair as he is asked personal questions.

“Why did you complain about police on QQ and WeChat?” police ask the man.

He is then grilled about his screen name and activity in a group chat on the WeChat platform.

China spies on social media conversations. Then they bring dissidents in for a real-life chat. I’d say we’re AT LEAST five years away from that over here, so no worries. pic.twitter.com/HjXzqsgr8S

“Why did you talk about the traffic police online…what’s wrong with police confiscating motorcycles?” he is then asked.

The man attempts to come across as apologetic but is then asked again, “Why did you badmouth the police? Do you hate the police?”

The man explains that he was drunk when he made the comments and is then asked to apologize to the police.

“I’m so sorry, I’m wrong, I know, I know that now, please forgive me, I won’t do it again ever,” he states.

Under its social credit score system, China punishes people who criticize the government, as well as numerous other behaviors, including;

Bad driving.

Smoking on trains.

Buying too many video games.

Buying too much junk food.

Buying too much alcohol.

Calling a friend who has a low credit score .

Having a friend online who has a low credit score.

Posting “fake news” online.

Visiting unauthorized websites.

Walking your dog without a leash.

Letting your dog bark too much.

Back in August, the Communist state bragged about how it had prevented 2.5 million “discredited entities” from purchasing plane tickets and 90,000 people from buying high speed train tickets in the month of July alone.

Citizens will also be forced to pass a facial recognition test that runs them through the social credit score database before being allowed to use the Internet.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

US equity markets surged overnight on China and European PMIs but have accelerated losses this morning after US Manufacturing ISM (and construction spending) disappoints.

Dow futures are down over 300 points from overnight highs…

The dollar is also being dumped…

Source: Bloomberg

For now, bonds refuse to move much after their ugly selloff overnight, but the short-end is outperforming…

Source: Bloomberg

Seems like we are going to need a “China deal is close” tweet to save the market.

US Manufacturing Survey Disappoints, New Orders/Employment Plunge

After China’s “surprise” PMI beat…

…and Europe’s ‘bottoming’…

…the world seems convinced that everything is awesome again (despite China Industrial Profits collapsing at a record pace) and expectations were for US Manufacturing surveys to extend their rebound in November.

Markit’s final Manufacturing PMI for November beat expectations, printing 52.6 (from 52.2 flash and 51.3 in October)

ISM’s Manufacturing survey for November missed expectations, printing 48.1 (from 49.2 exp and 48.3 prior)

This is the highest PMI since Feb 2019.

Source: Bloomberg

According to Markit, manufacturing output and new order growth rates improve to 10-month highs with the fastest rise in employment since March, but business confidence remains subdued.

And, according to ISM, new orders and employment both contracted further…

“A third consecutive monthly rise in the PMI indicates that US manufacturing continues to pull out of its soft patch. New orders and production are rising at the fastest rates since January, encouraging increasing numbers of firms to take on more workers. Exports are also back on a rising trend, firms are buying more inputs and re-building inventories, adding to the signs of improvement.

“Some caution is needed, as these improved survey numbers merely translate into very subdued growth in comparable official gauges of manufacturing production and factory payrolls. Business sentiment also remains worryingly subdued, with expectations about future output growth well down on earlier in the year and running at one of the lowest levels seen since comparable data were first available in 2012.

“Firms remain very concerned about the disruptive effects of tariffs and trade wars in particular, both in terms of rising prices and weakened demand, though the survey also saw further worries among manufacturers that the economy could slow in the upcoming presidential election year as customers delay spending and investment decisions.”

So one is left wondering, given this global rebound in ‘soft’ survey data, whether the terrifying global depression that was forecast due to Trump’s unilateral trade war was just more “Project Fear”-driven propaganda… or is this the eye of the global trade hurricane?

Rabobank: “The Global Institutional Architecture Is Collapsing”

Submitted by Michael Every of Rabobank

It’s December, and the start of the season of good will to all and peace on earth. Not much of that about, of course.

In the UK, the election has been interrupted by the terrorist attack at London Bridge, which both sides are naturally playing politics with in different ways (The Left is soft on terrorists vs. police underfunding and foreign policy, etc.); the latest opinion polls suggest Labour continues to make up some ground but remains well behind, but London Bridge may perhaps see that impetus stalled. Let’s see if the imminent arrival of US President Trump tips the scales, as President Obama did on Brexit, or if he can hold off on commenting as protocol dictates.

In Germany, Angela Merkel’s coalition partners the SPD have just elected new leadership, and they have veered to the left, hardly a surprise against this global backdrop, but likely accelerating the eventual collapse of the current government and opening up questions about what any new one could look like. Instability, or at least uncertainty, at the heart of the Eurozone is certainly not going to be welcome to investors – yet could it herald an imminent fiscal shift?

Tomorrow and Wednesday will also see the 2019 NATO summit, again in London, where the world’s largest military alliance will get together and try to decide what it is for and if it still has a purpose. Trump continues to put pressure on all members to spend the pledged 2% of GDP to keep it a fighting force vs. Russia, and perhaps China(?): relatively few do or show they even want to (e.g., Germany). He’s is also going to bring up Huawei and 5G to discuss. President Macron of France has called NATO “Brain dead” due to the absence of US leadership–I thought it was leading?–and has suggested it should shift from seeing Russia or China as potential enemies and refocus on terrorism: does France keep its nuclear deterrent to deal with events like London Bridge? President Erdogan of Turkey, the second-largest contributor militarily after the US, has no problems making friends with Russia and China–he is buying Russian weapons now–but has publicly called Macron “Brain dead” too. And Jeremy Corbyn, who would of course be the UK PM in under two weeks if the polls are wrong or misleading, has stated that NATO should be used to fight inequality: bomb the rich? Or spend as much on defence as he is pledging on everything else to rebuild British (defence) industry and provide quality jobs? It should make for a remarkable meeting one way or another: at the very least, it will be a world-class exercise in papering-over-cracks.

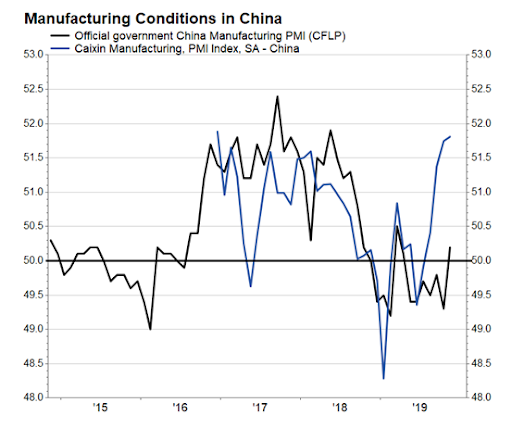

Does this actually matter for markets? Well, it depends. If the markets in question are only looking at things like the bounce in Chinese PMI data (the headline PMI rose to 50.2 from 49.3 in October, and the private Caixin index edged up to 51.8 from 51.7), or at US Black Friday spending (brick and mortar sales were up 4.2% y/y according to First Data, and on-line shopping pulled in USD7.2bn, up 14% y/y), then perhaps not – all is well with the world! Or the same markets might instead focus on China’s Global Times reporting that Beijing is insisting on the US rolling back tariffs for a trade deal, NOT just the delay of the looming 15 December tariffs, as the price of any ‘phase one’ – in which case all is decidedly not well. Expect USD/CNY and USD/CNH to continue to hover around the Lucky Seven level until this is resolved, of course. (But underlying our CNY bearishness, the data the market isn’t talking about this morning is that China is apparently set to see just 11m births in 2019 in a population of 1.4 billion. That’s down from 15.2m in 2018 and 17.2m in 2017. If true, its demographics are vastly worse than the already-poor projections: it is going to be very old long before it is rich enough to retire, and growth will suffer without automation, innovation, or immigration.)

Yet from data to the bigger picture: consider it was the likes of NATO that built the post-Cold War (1?) world within which these global markets now operate. As Polanyi pointed out back in The Great Transformation, though not in so many words, ‘free markets aren’t free’ – they are carved out of the political jungle with force, and require constant tending to stop them from being over-run. In that respect, we can posit that the problems in NATO are symptomatic of a broader collapse of the global institutional architecture in the face of populism.

But does that matter in a world which, as Branko Milanovic argues in his new book, and as markets continue to price for, capitalism is actually triumphant and there is no genuine alternative being offered by NATO’s enemies? Perhaps not, which of course fully supports our house view that on rates, “lower for longer” is now “lower forever”. China’s (and Russia’s) state-capitalist models certainly imply lower forever as the cost of capital is suppressed for national/geostrategic goals; in the West, markets are as utterly reliant on central-bank largesse, which hasn’t had any geostrategic goals up to now, but which may be about to get some.

Yet this does not mean there won’t be major financial market volatility if the architecture crumbles. You cannot think of a world dominated by multi-polar state-capitalism vs. a retreating more-free-market US-dominated system without seeing: 1) huge shifts in the USD and all resultant markets – either up, as its rivals falter, or down as its rivals combine to topple it (with what exactly?!); and 2) uncomfortable parallels with the pre-WW1 period. Like I said, not much peace on earth, sadly.

Another sign of the end of institutional architecture. The Apostrophe Society has closed down after admitting defeat in its quest to get Brits to understand when and how this simple but crucial grammar point is used (where tired eyes mean even The Global Daily occasionally falls short). So thats it for its members hopes for its vs. its; and a full societal circle from cave painting to Renaissance men-of-letters back to emojis beckons with a thumbs up. Perhaps current fuzzy market pricing fits perfectly in age where nobody can communicate properly anymore.

And another sign of crumbling related to architecture: Aussie building approvals slumped 8.1% in October, more than reversing the surprise 7.2% surge seen in September and vs. a consensus -1.0% figure. That puts them down -23.6% y/y. Likewise, Q3 Aussie company operating profits were -0.8% q/q vs. an expected 1.0% gain, and inventories -0.4% not the -0.2% consensus. Somehow Aussie yields are still up on the day despite those clear recession warnings: perhaps the apostrophe was in the wrong place.

Trader Mocks China’s ‘Surprise’ PMI Bounce: “When The World Wants To Be Happy, Who’s Going To Argue?”

Authored by Richard Breslow via Bloomberg,

With a few exceptions, that no one seems particularly bothered by, the economic numbers have come in to the upside today. Pride of place goes to China’s Caixin PMI. The mixed sub-components, notwithstanding. You know where traders’ heads are at when the focus is on the manufacturing number being the highest in almost three years, rather than the warts within the report. Nary a soul is raising the usual questions about the numbers’ veracity. When the world wants to be happy, who’s going to argue? Certainly not global equity markets.

Fixed-income markets had the self-respect to sell off. Hard actually…

Source: Bloomberg

Talk of recessions and further rate cuts will have to be suspended until further notice. Or we get the first share sell-off in the new year. It seems that the equity rally is so convincing that portfolio managers are questioning whether they need their bonds as must-have hedges for their stock holdings. If such thoughts continue, we could be in for a very interesting month. It’s tempting to get carried away. Which hasn’t been a great strategy this year.

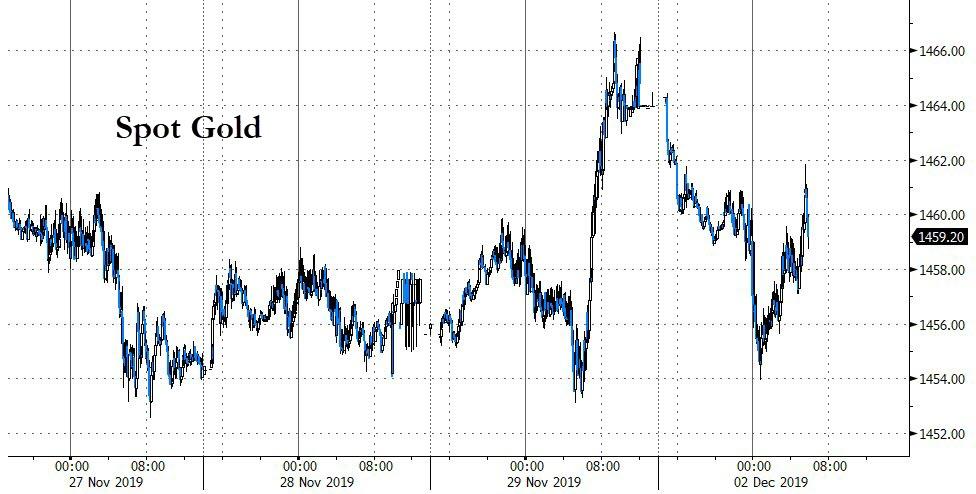

Gold looks like it’s collapsing until you realize that, so far at least, it’s having an inside day from this past Friday.

Source: Bloomberg

And the Dollar Index refuses to get excited about anything.

Even though we have been assured that biggies like sterling and the euro are “in play.” Emerging market currencies never got the feel-good memo and can get no traction.

This is a market in search of a narrative.

And the only one it can comfortably settle on is the belief, rightly or wrongly, that equities remain the best game in town. Some would argue the only one. And why not? Everyone seems to be rooting them on.

You won’t be hearing any central bankers talking about asset bubbles. Especially in December. But you will be assured that favorable financial conditions are good for one and all. “We have room to do more” isn’t a favorite punchline because of anxiety over the prospects for the upcoming non-farm payrolls numbers. If anything the whisper number is creeping up.

I was reading a research report this morning, which laid out the issues they thought would be front and center in the U.S. presidential election. All relevant. Especially during debates. But the lack of including the level of the S&P 500 seemed like an overly squeamish, and mistaken, omission.

Over the holiday, I was fascinated by three separate conversations. They were certainly instructive.

One was on a farm where everyone avowed to being a staunch Republican.

Another with liberal and well-heeled suburbanites. Purportedly with mixed affiliations.

And, lastly, a table of New Yorkers who claim, one and all, to be committed Democrats.

In each case, the strength of the stock market was the great unifier. And a popular subject of discussion. No one was complaining. Or simply trying to be polite. Something to keep in mind. It made me wonder what they were actually giving thanks for. And to whom.

If you want to properly handicap election polls, you need to keep in focus what is actually on voters’ minds. Perhaps that’s why there have been so many surprises. And the U.S. isn’t the only country with choices to make.

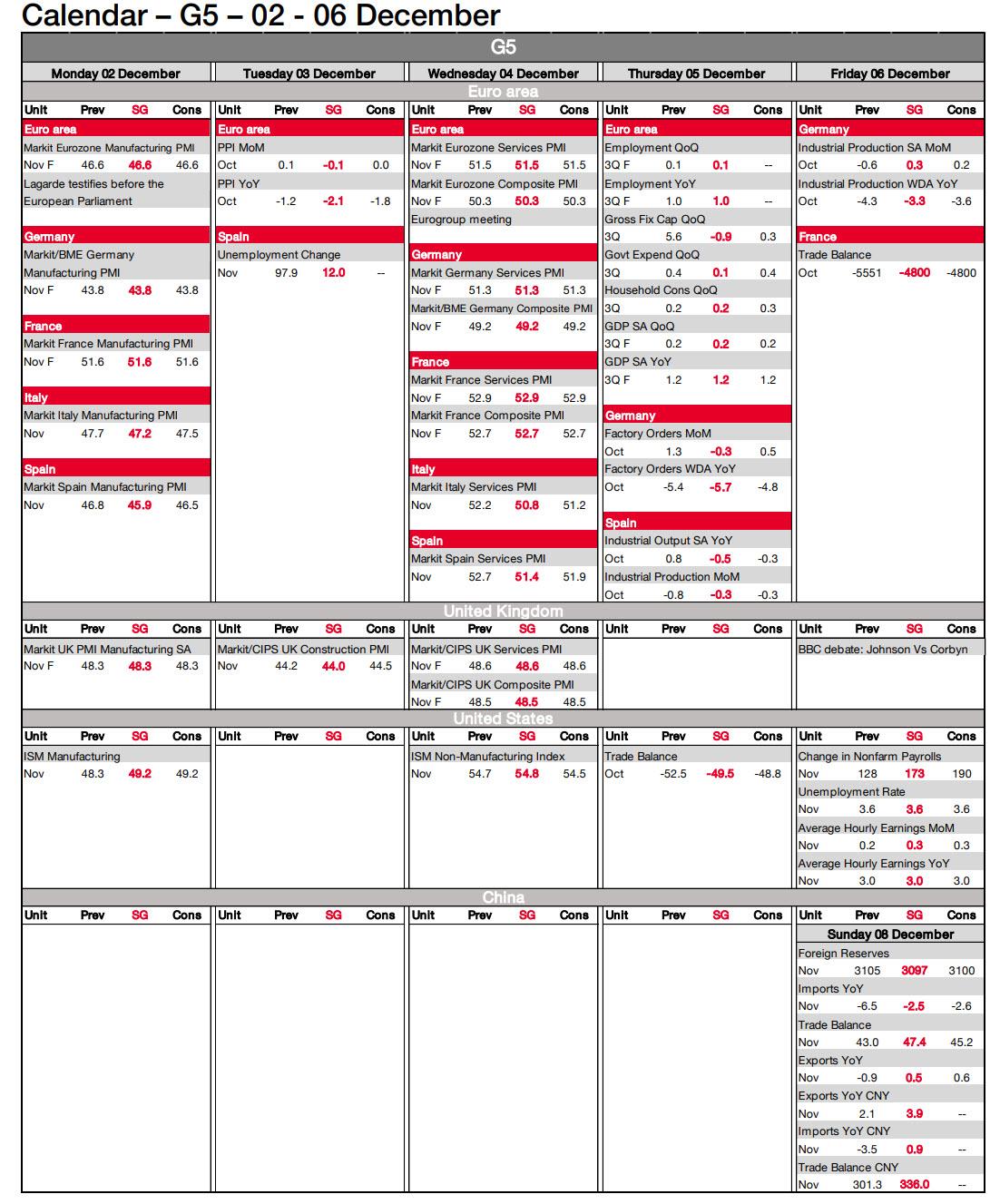

Key Events In The Week Ahead: PMIs, ISMs, Payrolls And Politics

While the period after Thanksgiving is traditionally when trading desks wind down for the year as most PMs and algos head for the hills of Aspen and Chamonix, there is still economic data to digest with this first week of December hosting a number of critical events that will set the agenda for markets running up to Christmas.

As DB’s Jim Reid notes, data releases include global PMIs (today and Wednesday), the US jobs report (Friday) and the US ISM figures (today and Wednesday). We’ll hear from ECB President Lagarde (today), and get policy decisions from central banks in Canada (Wednesday), Australia (Tuesday) and India (Thursday), while there’ll be another UK election debate between the two main party leaders (Friday) and a NATO leaders summit in London (Tuesday-Wednesday). With only just over a week to the U.K. election all eyes on whether Trump’s visit to London (starting today ahead of NATO) creates political capital for the opposition parties keen to link Mr Trump to Mr Johnson. Finally the German SPD 3-day party conference starting on Friday is now a must watch given the shock leadership results over the weekend.

Today is global manufacturing PMI day before the services and composite PMIs come out on Wednesday. China has given the world a boost by seeing the official manufacturing gauge at 50.2 (49.5 expected), the first 50+ print since April and up from 49.3 in October. Non-manufacturing rose to 54.4 (consensus 53.1) from 52.8 last month. There is some chatter about strong seasonal helping but overall this will be seen as positive news. Meanwhile, China’s November Caixin manufacturing PMI also came in higher than consensus at 51.8 (vs. 51.5 expected).

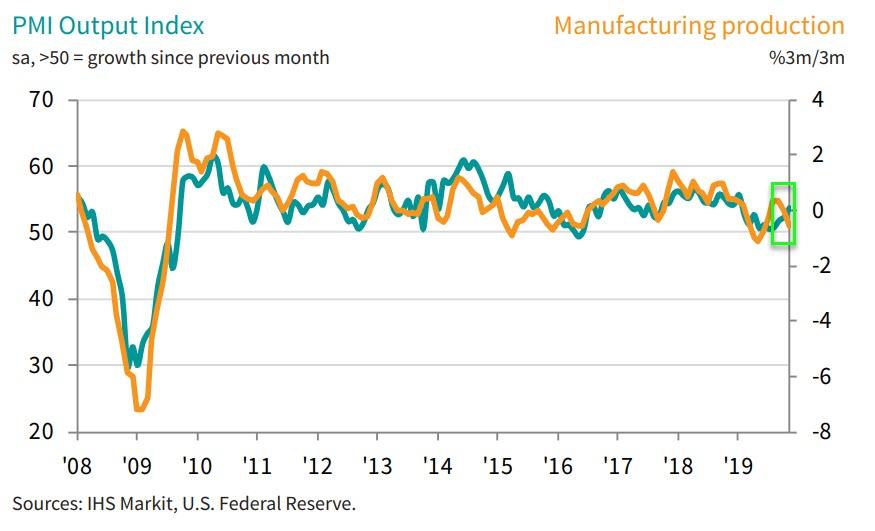

Moving forward and as for the rest of the global PMIs, the flash numbers mean we do have some initial indications of how the global economy performed into November but if momentum is improving this can be picked up between the flash and final numbers. The flash Euro Area services PMI fell to 51.5 while the manufacturing reading rose to 46.6, and the consensus is expecting the final Euro Area PMI readings to remain in line with the flash ones. A breakdown of European PMIs is shown below courtesy of Swiss Life:

In the US, we’ve also got the ISM releases, with the manufacturing report today before the non-manufacturing index comes out on Wednesday. The manufacturing reading has been below 50 since August (49.2 expected, 48.3 last month), although the non-manufacturing index has held up better, at 54.7 last month.

The other big highlight of the week comes with the US jobs report on Friday. In October, the +128k increase in nonfarm payrolls was the slowest pace of job growth since May but was better than expected with upward revisions to earlier months. The consensus is looking for a rebound to +190k in November. Meanwhile the unemployment rate and average hourly earnings yoy growth are expected to remain at 3.6% and +3.0% respectively. Other US data on factory orders, the trade balance and durable goods orders on Thursday will also help set the tone through December.

In Europe, slightly less is happening in terms of data aside from the PMIs, but we will see German factory orders and industrial production figures released for October on Thursday and Friday respectively. With the German economy having avoided a technical recession in Q3 with +0.1% qoq growth, attention will focus on whether the data heading into Q4 has shown further signs of stabilization. Finally, for the Euro Area as a whole, Thursday sees the October retail sales figures coming out, along with the final reading for Q3 employment and GDP.

Turning to central banks, with the Fed in their blackout period, the main event this week is likely to be ECB President Lagarde’s appearance before the Economic and Monetary Affairs Committee of the European Parliament today. This is the first Monetary Dialogue with the committee since Lagarde became ECB President, and it’ll be worth keeping an eye on whether she talks about the upcoming strategic review of monetary policy.

Other political events to watch out for include the annual UN climate change conference in Madrid from today, which will be taking place over the next two weeks. Then here in London we have a summit of NATO leaders on Tuesday and Wednesday. And finally, ahead of the UK general election on December 12, there’ll be the second head-to-head debate between Prime Minister Johnson and Labour leader Corbyn on Friday.

Courtesy of DB here is a day-by-day calendar of events:

Monday

Data: November manufacturing PMIs from South Korea, Indonesia, Japan, China, India, Russia, Turkey, Italy, France, Germany, Euro Area, South Africa, UK, Brazil, Canada, US and Mexico, Japan November vehicle sales, US November ISM manufacturing, October construction spending, South Korea final Q3 GDP, Japan November monetary base

Central Banks: ECB’s Lagarde, Rehn, Holzmann speak

Politics: UN Climate Change conference begins

Tuesday

Data: UK November construction PMI, Euro Area October PPI, Australia final November services and composite PMIs

Central Banks: Reserve Bank of Australia decision, ECB Executive Board nominees Panetta and Schnabel speak

Politics: NATO summit begins

Wednesday

Data: November services and composite PMIs in Japan, China, India, Russia, Italy, France, Germany, Euro Area, UK, Brazil and US, Australia Q3 GDP, US weekly MBA mortgage applications, November ADP employment change, ISM non-manufacturing index

Central Banks: Bank of Canada decision, Fed’s Quarles speaks

Thursday

Data: Germany October factory orders, November construction PMI, Euro Area October retail sales, final Q3 employment, GDP, US November Challenger job cuts, weekly initial jobless claims, October trade balance, factory orders, final October durable goods orders, nondefense capital goods orders, Canada October international merchandise trade, Japan October labour cash earnings, household spending

Central Banks: Reserve Bank of India decision, BoJ’s Harada, Fed’s Quarles speak

Friday

Data: Germany October industrial production, France October trade balance, Italy October retail sales, Canada November unemployment rate, net change in employment, US November nonfarm payrolls, unemployment rate, average hourly earnings, final October wholesale inventories, preliminary December University of Michigan sentiment, October consumer credit

Politics: German SPD party conference begins, UK TV debate between Prime Minister Johnson and Labour leader Corbyn.

* * *

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the ISM manufacturing index on Monday, the ISM non-manufacturing index on Wednesday, and the November employment report on Friday. There no speaking engagements from Fed officials this week, reflecting the December FOMC blackout period.

Monday, December 2

10:00 AM ISM manufacturing index, November (GS 50.1, consensus 49.5, last 48.3); Our manufacturing survey tracker edged up by 0.2pt to 51.2 in November, following stronger regional manufacturing surveys on net. After its first increase following six straight declines in October, we expect the ISM manufacturing index to rise 1.8pt further to 50.1 in November.

10:00 AM Construction spending, October (GS +0.6%, consensus +0.4%, last +0.5%): We estimate a 0.6% increase in construction spending in October, with scope for increases in both private and public construction spending growth.

Tuesday, December 3

There are no major economic data releases scheduled.

Wednesday, December 4

08:15 AM ADP employment report, November (GS +135k, consensus +155k, last +125k); We expect a 135k gain in ADP payroll employment, reflecting some drag from increased jobless claims and lower October payrolls. While we believe the ADP employment report holds limited value for forecasting the BLS nonfarm payrolls report, we find that large ADP surprises vs. consensus forecasts are directionally correlated with nonfarm payroll surprises.

10:00 AM ISM non-manufacturing index, November (GS 54.9, consensus 54.5, last 54.7); We expect the ISM non-manufacturing index to edge up by 0.2pt to 54.9 in the November report, partly reflecting further improvement in our non-manufacturing survey tracker (+1.1pt to 54.5).

Thursday, December 5

08:30 AM Initial jobless claims, week ended November 30 (GS 215k, last 213k); Continuing jobless claims, week ended November 23 (last 1,640k): We estimate jobless claims increased by 2k to 215k in the week ended November 30, following a 15k decline in the prior week.

08:30 AM Trade balance, October (GS -$48.5bn, consensus -$48.9bn, last -$52.5bn): We estimate the trade deficit decreased by $4.0bn in October, reflecting a decline in the goods trade deficit.

10:00 AM Factory Orders, October (GS flat, consensus -0.5%, last -0.6%); Durable goods orders, October final (last +0.6%); Durable goods orders ex-transportation, October final (last +0.6%); Core capital goods orders, October final (last +1.2%); Core capital goods shipments, October final (last +0.8%): we estimate factory orders were flat in October following a 0.6% decrease in September. Durable goods orders moved up in the October advance report, driven in part by an increase in aircraft orders.

Friday, December 6

08:30 AM Nonfarm payroll employment, November (GS +195k, consensus +190k, last +128k); Private payroll employment, November (GS +195k, consensus +190k, last +131k); Average hourly earnings (mom), November (GS +0.3%, consensus +0.3%, last +0.2%); Average hourly earnings (yoy), November (GS +3.1%, consensus +3.1%, last +3.0%); Unemployment rate, November (GS 3.6%, consensus 3.6%, last 3.6%): We estimate nonfarm payrolls increased 195k in November, reflecting a 46k rebound from the end of the General Motors strike and a modest rebound in employer surveys following the de-escalation of the trade war. We also note that November payroll growth tends to accelerate in tight labor markets, as labor supply constraints may incentivize firms to pull forward hiring or reduce end-of-year layoffs. On the negative side, the late Thanksgiving holiday this year (the 28th) may reduce the number of retail workers included in the November payroll figures. We also expect a 5k drag in Census employment following the completion of this year’s address canvassing. We estimate an unchanged unemployment rate at 3.6%, as the household survey may be due for a pause after 407k average gains over the prior three months. Finally, we estimate average hourly earnings increased 0.3% month-over-month and 3.1% year-over-year, reflecting favorable calendar effects, scope for a rebound in supervisory earnings, and continued wage pressures.

10:00 AM University of Michigan consumer sentiment, November preliminary (GS 98.0, consensus 97.0, last 96.8); We expect the University of Michigan consumer sentiment index increased by 1.2pt to 98.0 in the preliminary December reading, following firm readings in other confidence measures.

10:00 AM Wholesale inventories, October final (last +0.2%)

Federal Reserve Proposes New Rule To Let Inflation Run Hot Ahead Of Next Recession

As the Federal Reserve remains unable to stoke inflation and refuses to factor in asset price inflation, it has now considered launching a new rule that would let inflation run above its 2% target to make up for lost inflation, reported the Financial Times.

Though the Fed’s policies are to protect big Wall Street banks and keep liquidity ample in the financial system, their policies have overwhelmingly created deflation through supporting zombie companies and blowing financial bubbles.

To make up for lost inflation, the Fed will temporarily increase the target range above 2%. The policy would require “making it clear that it’s acceptable that to average 2 percent, you can’t have only observations that are below 2 percent,” said Eric Rosengren, president of the Federal Reserve Bank of Boston, who recently spoke with FT.

Fed members have expressed concerns that reverting the federal funds rate to the zero lower bound will drive inflation expectations lower, a real risk of Japanification.

Officials have remarked that the fed funds rate is so low compared to historical standards, that any given recession could make monetary policy ineffective, though there’s a real threat negative interest could be seen.

Fed members have been experimenting with new monetary tools ahead of the next downturn.

Janet Yellen, former chair of the Fed, said the new rule could be like “forward guidance,” which enabled the Fed to pressure short-term interest rates lower. This eventually allowed longer-term rates to fall as well.

Rosengren said, “future committees might not be as comfortable with that formulaic approach. This is why I prefer something that is a little bit more flexible, maybe not as constraining, but makes it a little clearer that we should be having [some inflation readings] over 2 percent.”

Fed governor Lael Brainard, spoke with reporters last week, said the new rule is to complex to elaborate on with the public. She said if inflation drops, the Fed should allow inflation to run hot, perhaps in a range of 2 to 2.5%.

In plain English, the Fed is afraid that its policies are Japanifying the US economy and are willing to let inflation run above target. The strategy clearly shows the Fed is making up policy as it goes ahead of the next recession, where monetary policy will be less effective than ever before.

If you have a good paying job, you should probably try to hold on to it as hard as you can, because those types of jobs are steadily becoming rarer. Since 1990, the U.S. economy has produced millions of jobs, but as you will see below nearly two-thirds of them have been low wage jobs. Of course this is one of the biggest factors causing the systematic erosion of the American middle class. Today, half of all U.S. workers make less than $33,000 a year, but meanwhile the cost of living has been steadily increasing. Housing costs, health insurance and other basic necessities have been rising much faster than our paychecks have, and this has put an enormous amount of financial stress on hard working American families.

A job making making chicken sandwiches at Popeye’s is not equivalent to a structural engineering job. In other words, the quality of the jobs that we create is perhaps even more important than the number of jobs that we create.

Yes, the U.S. has been creating a lot of jobs in recent years, but meanwhile the overall quality of our jobs has degraded rapidly…

Although the U.S. is on a record streak for job creation, many Americans still feel like they can’t get ahead. It’s not their imagination. The past three decades have seen the economy churn out more and more jobs that offer inadequate pay, a group of researchers found.

“The history of private-sector employment in the U.S. over the past three decades is one of overall degradation in the ability of many American jobs to support households — even those with multiple jobholders,” they wrote.

In fact, if you go back to 1990 about half of all jobs in the U.S. were good jobs.

But since that time, a whopping 63 percent of the jobs that have been created have been “low-wage, low-hour jobs”…

“In 1990, the jobs were pretty much evenly divided,” said Daniel Alpert, a founder of Westwood Capital and one of the creators of the index. In the process of running the numbers, he said, “We discovered that 63% of all jobs that were created since 1990 were low-wage, low-hour jobs. That was a pretty stunning statistic.”

So what is the answer?

In the past, you could make good money in America even if you just had a high school education. There were millions upon millions of high paying manufacturing jobs in this country, but at this point most of those high paying jobs have been shipped to other nations where wages are far, far lower.

Today, our young people are being greatly encouraged to get a college education so that they can compete for the dwindling number of good paying jobs. Of course there aren’t enough good paying jobs for all of our college graduates, but at least with a college degree you have a better chance of landing one.

Unfortunately, getting a college education has become oppressively expensive, and our young people have been taking on enormous amounts of debt as a result.

In fact, Time Magazine says that the total amount of student loan debt in the United States is now over 1.5 trillion dollars…

Today more than 44 million Americans have outstanding student loan debt, which has become the one of the biggest consumer debt categories. All told, student debt in the U.S. now totals more than $1.5 trillion.

Sadly, that number has almost doubled over the past decade. We have never seen a student loan debt bubble of this magnitude in the entire history of this country, and student loan debt delinquency rates are soaring.

As the issue of college affordability continues to be a prominent talking point on the campaign trail ahead of the 2020 presidential election, a new study shows that the cost of a college education is still increasing at a rate that far outpaces inflation.

The study, put out by the financial technology company Self, found that on average, college costs have risen $2,835 since 2015, increasing 112 percent more than the rate of inflation during the same period.

At this point, you are probably asking one very important question.

Where in the world is all of that money going?

Well, one recent study discovered that “administrative bloat” is the biggest factor that is driving up costs…

“Administrative bloat contributes enormously to the high and rising cost of tuition. In recent years, non-teaching personnel in higher education have exploded,” Pulliam said. “At some colleges bureaucrats outnumber faculty. The ‘diversity bureaucracy’ has proliferated at many schools. UT employs nearly 100 people in its diversity department, some of whom are paid in the six figures. Unnecessary and overpaid administrators are responsible for much of the increased overhead borne by students in the form of tuition increases.”

So as you pay off your student loan debt for decades to come, you can be comforted by the fact that the associate provost for diversity and inclusion at your college is bringing home more than $100,000 a year.

And perhaps that is the solution for the U.S. economy as a whole. If we just create enough “diversity” and “inclusion” administrative jobs, then we can all make six figures a year and the U.S. middle class will be restored.

Of course I am being facetious. The truth is that if we ever want to restore the U.S. economy to greatness, we need to start making things in this country again. We need jobs that add real value to our society, and we need an economic environment that respects and encourages innovation.

Unfortunately, what we have today is just the opposite. We are consuming far more wealth than we are producing, many of our “good paying jobs” are administrative or government jobs that add very little value to our society, and our small businesses are being strangled to death by rules, regulations and oppressive levels of taxation.

The only way that we have been able to maintain our debt-fueled standard of living is by piling up the biggest mountain of debt in the history of the world, and if we continue on the path that we are on there is no way that our story is going to end well.

We desperately need a return to common sense economics, but unfortunately common sense appears to be in short supply in America today.