There are still wide swaths of documentation kept under wraps inside government agencies like the State Department that could substantially alter the public’s understanding of what has happened in the U.S.-Ukraine relationships now at the heart of the impeachment probe.

As House Democrats mull whether to pursue impeachment articles and the GOP-led Senate braces for a possible trial, here are 12 tranches of government documents that could benefit the public if President Trump ordered them released, and the questions these memos might answer.

Daily intelligence reports from March through August 2019 on Ukraine’s new president Volodymyr Zelensky and his relationship with oligarchs and other key figures. What was the CIA, FBI and U.S. Treasury Department telling Trump and other agencies about Zelensky’s ties to oligarchs like Igor Kolomoisky, the former head of Privatbank, and any concerns the International Monetary Fund might have? Did any of these concerns reach the president’s daily brief (PDB) or come up in the debate around resolving Ukraine corruption and U.S. foreign aid? CNBC, Reuters and The Wall Street Journal all have done recent reporting suggesting there might have been intelligence and IMF concerns that have not been fully considered during the impeachment proceedings.

State Department memos detailing conversations between former U.S. Ambassador Marie Yovanovitch and former Ukrainian Prosecutor General Yuriy Lutsenko. He says Yovanovitch raised the names of Ukrainians she did not want to see prosecuted during their first meeting in 2016. She calls Lutsenko’s account fiction. But State Department officials admit the U.S. embassy in Kiev did pressure Ukrainian prosecutors not to target certain activists. Are there contemporaneous State Department memos detailing these conversations and might they illuminate the dispute between Lutsenko and Yovanovitch that has become key to the impeachment hearings?

State Department memos on U.S. funding given to the George Soros-backed group the Anti-Corruption Action Centre. There is documentary evidence that State provided funding to this group, that Ukrainian prosecutor sought to investigate whether that aid was spent properly and that the U.S. embassy pressured Ukraine to stand down on that investigation. How much total did State give to this group? Why was a federal agency giving money to a Soros-backed group? What did taxpayers get for their money and were they any audits to ensure the money was spent properly? Were any of Ukrainian prosecutors’ concerns legitimate?

The transcripts of Joe Biden’s phone calls and meetings with Ukraine’s president and prime minister from April 2014 to January 2017 when Hunter Biden served on the board of the natural gas company Burisma Holdings. Did Burisma or Hunter Biden ever come up in the calls? What did Biden say when he urged Ukraine to fire the prosecutor overseeing an investigation of Burisma? Did any Ukrainian officials ever comment on Hunter Biden’s role at the company? Was any official assessment done by U.S. agencies to justify Biden’s threat of withholding $1 billion in U.S. aid if Prosecutor General Viktor Shokin wasn’t fired?

All documents from an Office of Special Counsel whistleblower investigation into unusual energy transactions in Ukraine. The U.S. government’s main whistleblower office is investigating allegations from a U.S Energy Department worker of possible wrongdoing in U.S.-supported Ukrainian energy business. Who benefited in the United States and Ukraine from this alleged activity? Did Burisma gain any benefits from the conduct described by the whistleblower? OSC has concluded there is a “substantial likelihood of wrongdoing” involved in these activities.

All FBI, CIA, Treasury Department and State Department documents concerning possible wrongdoing at Burisma Holdings. What did the U.S. know about allegations of corruption at the Ukrainian gas company and the efforts by the Ukrainian prosecutors to investigate? Did U.S., Latvian, Cypriot or European financial authorities flag any suspicious transactions involving Burisma or Americans during the time that Hunter Biden served on its board? Were any U.S. agencies monitoring, assisting or blocking the various investigations? When Ukraine reopened the Burisma investigations in March 2019, what did U.S. officials do?

All documents from 2015-16 concerning the decision by the State Department’s foreign aid funding arm, USAID, to pursue a joint project with Burisma Holdings. State official George Kent has testified he stopped this joint project because of concerns about Burisma’s corruption reputation. Did Hunter Biden or his American business partner Devon Archer have anything to do with seeking the project? What caused its abrupt end? What issues did Kent identify as concerns and who did he alert in the White House, State or other agencies?

All cables, memos and documents showing State Department’s dealings with Burisma Holding representatives in 2015 and 2016. We now know that Ukrainian authorities escalated their investigation of Burisma Holdings in February 2016 by raiding the home of the company’s owner, Mykola Zlochevsky. Soon after, Burisma’s American representatives were pressing the State Department to help end the corruption allegations against the gas firm, specifically invoking Hunter Biden’s name. What did State officials do after being pressured by Burisma? Did the U.S. embassy in Kiev assist Burisma’s efforts to settle the corruption case against it? Who else in the U.S. government was being kept apprised?

All contacts that the Energy Department, Justice Department or State Department had with Vice President Joe Biden’s office concerning Burisma Holdings, Hunter Biden or business associate Devon Archer. We now know that multiple State Department officials believed Hunter Biden’s association with Burisma created the appearance of a conflict of interest for the vice president, and at least one official tried to contact Joe Biden’s office to raise those concerns. What, if anything, did these Cabinet agencies tell Joe Biden’s office about the appearance concerns or the state of the various Ukrainian investigations into Burisma?

All memos, emails and other documents concerning a possible U.S. embassy’s request in spring 2019 to monitor the social media activities and analytics of certain U.S. media personalities considered favorable to President Trump. Did any such monitoring occur? Was it requested by the American embassy in Kiev? Who ordered it? Why did it stop? Were any legal concerns raised?

All State, CIA, FBI and DOJ documents concerning efforts by individual Ukrainian government officials to exert influence on the 2016 U.S. election, including an anti-Trump Op-Ed written in August 2016 by Ukraine’s ambassador to Washington or efforts to publicize allegations against Paul Manafort. What did U.S. officials know about these efforts in 2016, and how did they react? What were these federal agencies’ reactions to a Ukrainian court decision in December 2018 suggesting some Ukrainian officials had improperly meddled in the 2016 election?

All State, CIA, FBI and DOJ documents concerning contacts with a Democratic National Committee contractor named Alexandra Chalupa and her dealings with the Ukrainian embassy in Washington or other Ukrainian figures. Did anyone in these U.S. government agencies interview or have contact with Chalupa during the time the Ukraine embassy in Washington says she was seeking dirt in 2016 on Trump and Manafort?

Late last week, Amazon founder Jeff Bezos gave away nearly $100 million to more than a dozen charities across the United States.

It would take the average person more than 1,000 centuries to accumulate that much money. Yet Bezos gave it away in a single day.

And it’s not like that was the first time he’d ever given to charity. Bezos has already donated billions of dollars to other philanthropic endeavors.

You’d think that such generosity would be appreciated. Yet when Forbes announced Bezos’ gift last week, Twitter user punkassbamboo complained:

“A whopping .09% of his net worth. Thanks so much Jeff.”

This is classic Bolshevik mentality: punkassbamboo and his fellow Bolsheviks see themselves as victims… and everyone else as the enemy. And no matter what the enemy does, it’s never enough.

So despite giving away $98.5 million to help the homeless, Bezos is just a stingy billionaire asshole.

The legions of Bolsheviks like punkassbamboo, of course, have absolutely no trouble finding sympathetic politicians who threaten to confiscate the wealth of businesses, entrepreneurs, and anyone who has achieved success.

Every single Bolshevik politician plays the same tune: rich people are selfish, corporations are bad, and there’s too much wealth concentrated in the hands of the few.

Bernie Sanders constantly tells his supporters that the 3 wealthiest people in the country have more money than the bottom 50%.

He’s right; the wealth gap in the United States hasn’t been this extreme since right before the Great Depression.

And these Bolsheviks feel compelled to ‘fix’ this.

US Presidential candidate Cory Booker, for example, absurdly proposes to tax unrealized capital gains, while Elizabeth Warren wants a wealth tax.

They’re both remarkably stupid ideas, but they’re essentially different variations of the same concept: confiscating legitimately earned wealth.

And this is the part that I find truly incredible– because, when you think about it, there are actually TWO ways of closing the wealth gap.

You could either make wealthy people less wealthy.

Or you can help poor people become less poor.

But they never, ever once, have considered the second approach. They ONLY focus on the first one. Raise taxes on rich people. Raise taxes on corporations.

Wealthy people are wealthy for a reason: they’ve either started a successful business, or they have incredible financial acumen.

Yet the Bolsheviks never say, “Let’s make it easier for punkassbamboo to build relevant skills, raise capital, start a business, and become a successful millionaire entrepreneur.”

But do you know who has done that? Jeff Bezos.

Amazon is such a massive economic force that it has spawned entire industries of people who earn a good living providing services and selling products through the platform.

Bezos has made it possible for anyone with zero skills, poor education, and almost no capital, to start a business selling products on Amazon.

There are thousands of websites and YouTube videos to learn how to do this FOR FREE. And Bezos has made it so easy that a budding Amazon entrepreneur can be up and running in a matter of hours.

And the amount that you can earn online is substantial.

I’ve mentored dozens of Amazon business owners at my annual entrepreneurship workshop–

One former student was selling more than $20 million of products per year with just one employee, and others became so successful that they sold their Amazon businesses for several million dollars.

None of these entrepreneurs came from money. They built successful businesses from scratch by educating themselves and capitalizing on the opportunity that Jeff Bezos created.

Something tells me that no one has ever become a millionaire because of Elizabeth Warren… and no one ever will.

Elizabeth Warren lists more than 50 detailed plans on her website. They include things like breaking up tech companies, taxing wealthy people, keeping low-paying manufacturing jobs in the US, etc.

But not a single plan focuses on closing the wealth gap by making it easier for people like punkassbamboo to become successful.

Frankly that doesn’t fit the Bolshevik agenda.

Success has a funny way of building someone’s confidence and independence. When you work hard and become successful, you begin to see yourself achieving even more.

But Bolshevik politicians depend on their supporters seeing themselves as victims, not as champions.

Their power comes from keeping people angry, afraid, and downtrodden.

So they’ll never aim to close the wealth gap by helping poor people become successful.

Tad Rivelle, Chief Investment Officer of the Californian bond house TCW, doubts that the Central Banks can prevent the impending economic downturn. He spots increasing signs of stress in the credit sector and recommends holding safe assets to be prepared for turmoil in the financial markets.

Mr. Rivelle, who rarely gives interviews, views the prospects on the financial markets with skepticism. In his opinion, it’s clear that the business cycle is in its final stages. He warns that the power of unconventional monetary policy is largely exhausted and nervousness in the credit sector is growing.

Against this background, he advises a defensive calibration of the portfolio and a careful approach when it comes to security selection – especially in the investment grade segment where many companies are more leveraged than their rating indicates.

Mr. Rivelle, the rally in stocks has lost some of its momentum recently. Nevertheless, the S&P 500 is near its all-time high. What’s your take on the current market environment?

We’re very skeptical of taking risks in this market since there is fairly abundant evidence that we’re in a late cycle type of environment. Equity valuations are largely following the script of the central banks: The central banks say dance, and the equity market is dancing. In contrast, debt investors increasingly say: «There is nothing in it for me to get on the dance floor because as a debt investor, all I get back is a 100 cents on the dollar». We’re the asset class that’s always at risk of loss. The Federal Reserve can say and do whatever it wants. But if it can’t get the private sector to follow through with cheap financing and debt markets become skeptical of providing favorable financing, I don’t know where you go with that.

Globally, there’s around $ 12 trillion in negative yielding debt. How do you approach such a market as a veteran fixed income investor?

It’s an absurdity and an artificial condition. For instance, a Swiss company like Nestlé finds itself in some kind of financial paradox: They can issue negative yielding debt in Swiss francs and then use the proceeds to buy back their own equity. If you want to reflect on this philosophically: Why have any equity at all? You could just buy it all back. That leads to the next observation: Your assets theoretically are producing benefits and your liabilities are producing benefits, too. This would imply there’s no cost running your business at all. This is obviously a hint that markets didn’t get to negative interest rates through a negotiation process between borrowers and lenders. Rates were pushed off the cliff by the central banks.

What are the consequences of these artificially low interest rates?

The collective and extraordinary expansion of central bank balance sheets has powered the «bull market in everything». But these absurd policies aren’t going to work for the long term. In this cycle, the Zeitgeist has been that the central banks have the capacity to maintain growth and prosperity. In others words: If you control the financing right to corporations and consumers, you can make the economy grow forever. This flies in the face of common sense. Economics used to always be about the idea that you need to incentivize producers to make efficient choices. If you give them the right incentives, they will raise the bar in terms of value addition and growth over time. But when you artificially chose your rates, you are doing the opposite. You’re causing bad choices by definition.

Where are such bad choices evident today?

The low rate environment has created excesses in a lot of areas. It has driven up asset prices, and as you drive up enterprise multiples, you drive up leverage multiples. Look at private equity: The best idea that most institutional investors say is in their portfolio is private equity. That’s strange since the whole concept of private equity is basically that you buy up businesses, you put a lot of leverage underneath them, you don’t mark things to market – at least not the same way as the public markets do – and you create this illusion of low volatility investments. So you have a system where company managers get enabled to say ridiculous things to their investors like: «We don’t care about profits». I don’t think we would have a company like WeWork if we didn’t have an environment where investors are thinking that they need to invest in a fairy tale because they can’t earn a return any other way.

What’s your take the WeWork disaster?

WeWork was one of these situations hiding in plain sight. There were plenty of people who expressed skepticism. Yet, you had money center banks playing along, making loans and adding to the credibility of it. So you had a fairy tale: You had a $47 billion unicorn two or three months ago that now had to be rescued. I’ll go further: If SoftBank didn’t rescue WeWork, would you really want to find out what the lawsuits are going to discover when the Limited Partners sue SoftBank? When they ask: «How did we get to $47 billion, exactly?» And while you’re at it, you might be even doing that in a court in Riyadh. So maybe this point, the best course of action is just to pay everybody off and then figure out what to do.

Where are other disasters hiding in plain sight?

When you get to the last phase of the cycle, you need to be thinking about what could go wrong, because there is very little probably that’s going to go right. Today, a lot of carnage has come to the fracking area. There are a lot of E&P capital structures that are evidently no longer financeable in the capital market. A lot of these businesses are probably going into bankruptcy. Also, you see stress in automotives, in semiconductors and in retail. What’s more, it’s fair to say that the bank loan market represents one of the significant risks out there.

What are red flags investors should watch out for?

The number of high yield credits trading at spreads over a thousand basis points over treasuries has been rising all year long. Also, you’re seeing a lot more volatility in the leveraged lending space. Credit Investors increasingly are firing first, and ask questions later. This speaks back to another of the excesses in this cycle. Traditionally, the deal was that if you are a leveraged company, you were given two choices in the debt markets: Door number one, you can show the world what your financials are, adhere to the public standards, issue high yield bonds and report to the SEC and your debt investors what’s going on. Door number two: If you don’t want to show your numbers you had to get your hands tied behind your back. The lenders will give you the money but they won’t let you do much of anything with it because they want to make sure you’re not doing something stupid while they can’t watch you.

And what’s going on in this cycle?

This cycle, we have moved to an environment where what was a covenant heavy bank loan market has become a covenant light bank loan market. As a debt investor, you don’t have transparency and you have no ability to constructively restrict what management is doing. Private equity plays into this dynamic because it has used its market power to negotiate on behalf of its portfolio companies. So we’ve seen a worsening of covenants and credit agreements. Some of this relates back to a basic dynamic that the Fed and other central banks have put their hand on the scale: They’re basically communicating that they want to make it so easy for borrowers that lenders are saying: «Cash is burning a hole in my pocket. I need to do something with it.»

How does this end?

This is how it all ends badly. Think about the DNA of markets. Let’s say, you want to buy a house. In a red-hot market, you show up at the first day and there’s twenty people looking to buy. You want to do your due diligence and ask about the foundation, the roof and maybe the crazy neighbor. Finally, you get hold of the seller and he’s like: «I don’t have time. I’m not answering your questions. The only thing I want to hear from you is how much over the full offer price you want to pay.» That’s the way the credit markets were in 2017. «Drive-by» deals were done and investors like ourselves got the call in the morning saying: «Company XYZ is raising $ 500 million, you’re in or you’re out?» So no time for due diligence.

That doesn’t sound like prudent behavior.

Now, fast forward a couple of years and suppose you’re in a stone-cold housing market. You list your house, you wait three weeks and finally, some barely qualified buyer walks through the door and wants to know about your foundation, your roof and the crazy neighbor. After you’re done answering his questions, he’s got more and more questions because he recognizes intuitively that every time you can’t answer a question, he can make a worse case assumption and use it as justification to knock your price down. So suddenly the market has become completely illiquid and very hostile.

At which stage are we in the credit markets today?

Generally, if you’re involved in a bank loan that doesn’t have the parameters a CLO would naturally buy, the sponsorship is thin. If everything is fine, you probably won’t experience a lot of volatility. But miss your earnings or communicate some bad news and investors drop challenged credits like «hot potatoes.» That’s logical because your business has been operating in the dark. You haven’t told your lenders anything for years. Now, the only news you’re giving them is bad news. So they have to assume that this bad news hasn’t just happened yesterday, but there are deeper ongoing issues. They want out, but there is no bid on the other side. That’s why a liquidity crisis is all but inevitable.

How long until these developments evolve into a bigger issue for the financial markets?

We thought it was going to happen two years ago. Credit markets look late cycle, manufacturing looks pretty late cycle and corporate profitability, as well. So the proliferation of negative rates may also suggest that central bank policy has reached exhaustion. It’s almost like negative rates are the last thing central bankers are trying to make it work.

What are the chances of a recession against this backdrop?

It’s a little hubristic to say we’re going to have a recession in the next twelve months. What’s not hubristic is to say that these policies are not working and we will inevitably have a recession. Didn’t we try this at least once or twice before? Didn’t the Soviet Union have zero percent interest rates? Didn’t they have recessions? Maybe it wasn’t visible in the official statistics, but their recessions were manifested by longer lines at food stores.

What have zero percent or negative interest rates to do with that?

Artificial asset prices distort resource allocation and growth. Look at the fact that Sears and Kmart are for all intents and purposes just about to disappear on the scrap yard of history. All the resources invested in stores, labor and capital, are worthless. So the faster you get rid of it, presumably the better off you’re ultimately going to be. Recessions are not optional, they are inevitable. It’s the process in which it’s all getting washed out and rearranged. It’s like: «Don’t you want to get to the passing lane eventually? Or do you want to be stuck in the right line because you’re afraid of change?» Eventually you have to do it anyway.

An important piece of the puzzle is the US consumer. How healthy are households in the United States financially?

The US consumer is divided: You have the middle- and upper-class consumer, which seems to be in fine shape at the moment. You wouldn’t expect differently because consumer proclivity to buy is a function of income, employment and housing prices. So middle class people in general feel more secure with employment as high as today and their house worth 20% more versus what it was ten years ago. On the other hand, the subprime consumer is more credit dependent and metrics there are not really good. We’re seeing deterioration in delinquency rates and charge-offs for the lower range of credit counterparties. The problem is, that this is where a lot of growth ultimately comes from, from the marginal buyer.

What does it mean in terms of Fed policy? Are more rate cuts coming down the road?

Let me be maximally charitably to the Fed: They have no backing by elected officials from either party to do anything but lower rates in response to incremental economic weakness. So it’s fair to say that if the economy weakens they will lower rates more, regardless of what they say. It won’t happen this year, I presume. But I guess in 2020 they’re going to cut rates again. We invented central banks because we figured out that the banking system, if left to its own faith, is too volatile and that we need a state sponsored institution to cushion the blow. But somehow, we went from there to the Fed buying $ 60 billion of T-Bills a month, calling it not Quantitative Easing, and central banks in Europe and Japan imposing negative rates.

What’s the yield on the ten-year treasury going to be in a year from now?

I would say somewhere around where it is today, between 1.5 and 2%. But that’s just a wild guess. It’s a question of timing and causation: If this becomes a global led downturn you have to assume that US rates are going lower. But you can also imagine other scenarios. US rates being above overseas rates has brought huge capital inflows and people are getting very used to the idea that these capital inflows will always hold down US rates. But what’s going to happen when these flows reverse for who knows what reasons and US rates go up?

What should a prudent investor do under these circumstances?

You should adapt your underwriting standards to the kind of environment that you are in. So, beginning a couple of years ago, we adopted our underwriting standards to be much more careful with respect to the types of risks we’re taking throughout our whole portfolio. In other words: Stay vigilant, focus on staying liquid, focus on safe assets and wait for volatility to present opportunity.

So how does a robust bond portfolio look?

It was Benjamin Graham pointing out that bond selection is a negative art. That’s especially true in the late cycle. Cycles die in large measure because capital gets tied up in unprofitable enterprises. So you need to think long and hard about what claims are breakable and can suffer catastrophic and permanent price declines. There may be a time to own breakable assets, but after they break and not before.

What are such breakable assets today?

There will be plenty of breakable assets and a lot of them will be in the high yield and bank loan market. Some maybe even in the investment grade market. Today, 11% of investment grade issuers are levered more than five times, an 27% are levered more than four times. In this context, you could make a pretty good case that 50% of BBB debt would have a high-yield rating based on leverage alone.

Where are better places to invest?

We’re counselling to divide your assets between bendable assets and riskless assets for the liquidity issues that we’re going to encounter. I would put treasuries and agency mortgages as the risk-off, liquid part of the portfolio. You can’t retire on them or really do anything with it. But you can own them tactically to finance the expansion of your bendable assets: Assets that are exposed to mark-to-market risk, meaning they go up and down, so they may be exposed to liquidity risks. But they provide you yield today and their claims will survive into the next cycle, if you have done your categorization right.

What are attractive bendable assets?

Bendable is what we refer to as true investment grade credit. Also, AAA-rated commercial mortgage-backed and asset-backed securities as well as senior non-agency residential mortgage-backed securities. Stuff that we’re invested in obviously. In some cases, AAA-rated CLO tranches can potentially make some sense, too. And, if you can find them, some high yield securities maybe, or a few emerging market securities. You try to find companies with a wide enough moat around what they’re doing, like regulated utilities as long as they’re not in California where you have a special environment with damage claims from wildfires.

US Consumer Confidence Tumbles For 4th Straight Month Despite Soaring Stocks

‘Hope’ improved marginally in November, according to The Conference Board, but the headline consumer confidence data dropped for the 4th straight month as current conditions slipped.

Consumer confidence in Nov. fell to 125.5 vs. 126.1 prior month.

Present situation confidence fell to 166.9 vs. 173.5 last month.

Consumer confidence expectations rose to 97.9 vs. 94.5 last month.

Consumers’ appraisal of current-day conditions was less favorable in November. The percentage of consumers claiming business conditions are “good” rose slightly from 39.7 percent to 40.2 percent, but those claiming business conditions are “bad” also increased, from 11.0 percent to 13.8 percent.

Source: Bloomberg

Confidence continues to ebb on a YoY basis…

Source: Bloomberg

“Consumer confidence declined for a fourth consecutive month, driven by a softening in consumers’ assessment of current business and employment conditions,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board.

“The decline in the Present Situation Index suggests that economic growth in the final quarter of 2019 will remain weak. However, consumers’ short-term expectations improved modestly, and growth in early 2020 is likely to remain at around 2 percent. Overall, confidence levels are still high and should support solid spending during this holiday season.”

Additionally, those saying jobs are “plentiful” decreased from 47.7 percent to 44.8 percent, while those claiming jobs are “hard to get” increased from 11.6 percent to 12.7 percent.

And all of this as stocks hit record high after record high.

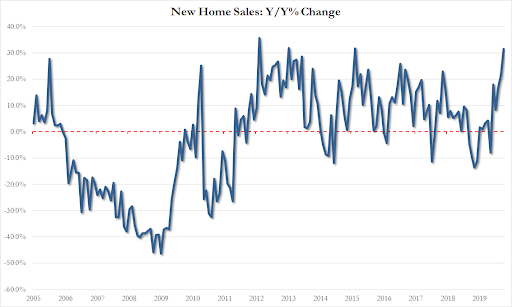

US New Home Sales Pace Highest In 12 Years As Median Price Plunges

Following the upside surprise in existing home sales, new home sales were expected to rebound after September’s dip.

However, a massive upward revision for September (from -0.7% to +4.5%) meant that October new home sales slipped 0.7%…

Source: Bloomberg

A major jump YoY…

The 733k SAAR is much higher than the expected 705k, and the fastest pace in more than 12 years, adding to signs of sturdy housing demand amid lower prices and borrowing costs.

Source: Bloomberg

Even with the gains, the pace of new home sales remains well below levels reached during the housing boom of the 2000s, when purchases peaked at 1.39 million.

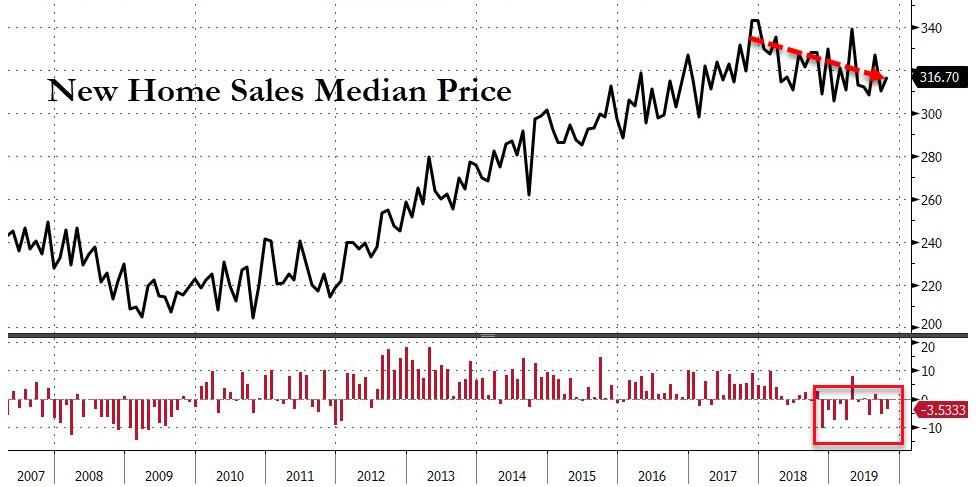

Notably though the median sales price decreased 3.5% from a year earlier to $316,700…

Source: Bloomberg

Purchases of new homes rose from the prior month in the West and Midwest, while declining in the Northeast and South.

The number of properties sold for which construction hadn’t yet started rose to 250,000, the highest since 2007.

As the issue of college affordability continues to be a prominent talking point on the campaign trail ahead of the 2020 presidential election, a new study shows that the cost of a college education is still increasing at a rate that far outpaces inflation.

The study, put out by the financial technology company Self, found that on average, college costs have risen $2,835 since 2015, increasing 112 percent more than the rate of inflation during the same period.

“While it is somewhat understandable for universities to increase costs in line with inflation, especially when you consider the number of wages and resources needed to keep a university running, the price hikes we have found in some states are double (if not triple) the rate of inflation; posing the question of where is this money going,” Self CEO James Garvey said in an emailed statement to The College Fix.

The analysis found that “university students are paying $29,133 on average across all states just to attend. This is an increase of $2,835 for every year of tuition above the prices student were paying in 2015.”

It also found that across all states, Montana had the sharpest increase in college costs, with the average cost going up 30 percent in the past four years. Alaska was close behind with a 28 percent increase, and Texas rounded out the top three with an average cost increase of 20 percent.

Texas education watchdog Mark Pulliam told The College Fix in an email that the increase in costs in Texas was likely due to an increase in bureaucratic hirings.

“Administrative bloat contributes enormously to the high and rising cost of tuition. In recent years, non-teaching personnel in higher education have exploded,” Pulliam said.

“At some colleges bureaucrats outnumber faculty. The ‘diversity bureaucracy’ has proliferated at many schools. UT employs nearly 100 people in its diversity department, some of whom are paid in the six figures. Unnecessary and overpaid administrators are responsible for much of the increased overhead borne by students in the form of tuition increases.”

Texas Public Policy Foundation’s Thomas Lindsay echoed Pulliams’ comments.

“Our research suggests that the bulk of the increases go to administration, a phenomenon dubbed ‘administrative bloat,’” Lindsay said in an email to The College Fix.

What’s more, Texas colleges and universities are not alone, he added, noting that while 40 years ago faculty outnumbered administration by roughly 2 to 1 nationwide, today the proportions are nearly equal.

Meanwhile, there is one state that bucked the national trend.

Self found that Nevada’s average tuition cost actually decreased 2.8 percent relative to inflation. In 2015, tuition in the state averaged $28,857. In 2019, that number had dropped slightly to $28,045.

“Inflation is a worry for many people but, for some students and their families, rises in inflation can be the difference between being able to afford to attend university and obtain a degree, and missing out entirely,” Garvey said.

The study incorporated the costs of tuition, room and board, and books and supplies to determine the average cost of a college education on College Tuition Compare. Inflation was calculated through US Inflation Calculator.

Erdogan: “Patriotic” Turks. Now Is The Time To “Leave The Dollar” And Buy Turkish Lira

President Tayyip Erdogan, on Tuesday, told Turks to ditch the dollar and convert their foreign currencies to Turkish lira as an act of “patriotism,” reported Reuters.

“Leave the dollar and the rest. Let’s turn to our money, the Turkish lira. The Turkish lira doesn’t lose value anymore. Let’s show our patriotism like this,” Erdogan told members of his Justice and Development Party (AK Party) in parliament.

Turkey is faced with a historic economic crisis. The Turkish lira has plunged over the last five years, international credit rating agencies have downgraded the country’s debt to junk, and a recession threat remains imminent.

Erdogan’s government published plans for de-dollarizing in July 2019 to build a central bank-issued digital currency.

The digital currency, named the ‘digital lira,’ will be part of a new economic development roadmap from the early 2020s to mid-2025, that will end the country’s dependence on the dollar.

Tests of the digital lira are expected at the end of 2020, and it will allow instantaneous transactions between Turkish citizens and offer decentralized financial instruments for the economy.

Once again Erdogan is demanding Turks to de-dollarize. Shown above, he’s made the call several times over the last five years as the lira has collapsed.

Maybe the lira is headed for another plunge and Erdogan wants Turks to buy the dip? But the call this time to buy the lira is coming ahead of the possible launch of the digital lira.

The latest news from Turkey indicates Russian S-400 missile defense systems are being tested in Ankara, which will certainly outrage the Trump administration and could force Washington to hit Turkey with new economic sanctions. The result would weigh on the currency, so maybe Erdogan is drumming up buying power before the next plunge.

FBI officials concerned that FBI lawyer Kevin Clinesmith’s tampered and altered documents to obtain Foreign Intelligence Surveillance Warrant will put into question all the evidence gathered to obtain the warrant.

Horowitz referred Clinesmith to DOJ Prosecutor John Durham appointed by Attorney General William Barr for further investigation.

Other FBI officials will be wrapped up into Clinesmith’s warrant tampering. Who approved the warrants?

Criminal Defense Attorney David Schoen says FBI failed to make immediate correction of any materially false statement or any material omission. “Clearly no such correcting submission was made here.”

FBI Lawyer Kevin Clinesmith led the interview on George Papadopolous in February, 2017.

Clinesmith was anti-Trump and removed from the Russia investigation.

Department of Justice Inspector General Michael Horowitz’s anticipated report will reveal that the Foreign Intelligence Surveillance Application warrant was tampered with but the significance of that cannot be understated. It means that Horowitz’s discovery will discredit the bureau’s handling of its investigation into President Donald Trump’s campaign and Russia during the 2016 presidential election and it could make any information discovered during the course of seeking approval for the FISA and after ‘fruit of the poisonous tree’,” according to numerous sources who spoke to SaraACarter.com.

“Based on what we know, Clinesmith’s tampering of documents appears to have been significant enough to have played a role in the FISA courts decision to grant a warrant to spy on an American, maybe more than one American,” said a U.S. official, who spoke on condition of anonymity due to the sensitivity of the matter.

“There is concern among the FBI that all the evidence will come into question, as it should – particularly the case of the ‘fruit of the poisonous tree’ that the evidence itself is tainted – if that’s true than anything gained from that evidence might also be tainted. This could be a problem for anyone who approved the FISA as well.”

What we now know is that FBI lawyer Kevin Clinesmith, allegedly altered an email that FBI officials used to prepare to seek court approval to renew the wiretaps on former Trump campaign advisor Carter Page, as first reported by the New York Times and verified by SaraACarter.com. The extent of the alterations in the FISA application is still unknown but it was significant enough for Horowitz to refer Clinesmith to Connecticut Federal Prosecutor John Durham, who was appointed by Attorney General William Barr to investigate the origins of the FBI’s handling of the probe. Durham’s probe has also expanded to the CIA, of which he has interviewed numerous officers and the Pentagon’s Office of Net Assessment, which paid FBI confidential informant Stephan Halper to collect information on several Trump campaign advisors, as first reported by this new site.

The DOJ obtained three FISA renewal orders on Page. According to the NYT “the paperwork associated with the renewal applications contained information that should have been left out, and vice versa, the people briefed on the draft report said.”

That’s a serious problem, stated the U.S. official. Why? Because Clinesmith’s alterations in the documents played a role in the ability for the FBI to continue to wiretap Page throughout the renewal process.

David Schoen, a criminal defense attorney, told SaraACarter.com that the FISA process requires absolute scrutiny as the defendant, the person targeted by the warrant, is not represented by anyone due to the extraordinary secrecy of the process.

Schoen noted, if an “agent falsifies, materially alters with false information, or makes a material omission in documents relied on to authorize surveillance – and here it was to authorize the most intrusive kind of surveillance by the most secretive court in the land – then any further step in the process and any material obtained by surveillance from the point of his illegal conduct forward is arguably poisoned by the initial illegal materially false alteration or material omission.”

“Moreover, while all courts rely completely on the integrity of the surveillance application and supporting documentation and on the agents presenting them, the FISC must by definition do so to an even greater degree because it is all presented ex parte and the entire process is shrouded in secrecy , but can impact on the privacy of American citizens to the greatest degree imaginable,” he added.

More importantly said Schoen, “the FISC has an express rule of procedure affirmatively requiring the immediate correction of any materially false statement or any material omission. Clearly no such correcting submission was made here.”

Making matters worse, Clinesmith was vehemently anti-Trump, raising significant questions of bias. He was removed in February, 2018, from the Russia investigation, in the same fashion former FBI Special Agent Peter Strzok, who headed the investigation into Trump’s campaign, was removed. Clinesmith’s anti-Trump text messages stated the “crazies have won” and “viva la resistance” in relation to Trump’s presidential victory.

Was Clinesmith a low level FBI attorney? Or did he play a significant role in the early investigation?

George Papadopolous, who was central to the FBI’s investigation into Trump and believes the FBI took a FISA out on him, said no.

On Monday, Papadopolous told Fox and Friends, that Clinesmith was the “attorney who interviewed me from the Department of Justice, I know the New York Times mentioned him as some sort of low level attorney for the DOJ, but I don’t think he was a low level attorney.”

“This individual brought an entire delegation from Washington D.C. to interview me in February, 2017 and we now know he, and some of the others who interviewed me are under criminal investigation,” Papadopolous added.

“So I think the report is not going to be as pleasant as many people think it’s going to be for the FBI and its probably going to lead into criminal prosecution that Durham is going to be taking over from him.”

Will the altered evidence collected by Clinesmith taint the rest of the evidence submitted to the court?

Clinesmith was caught. But what happens to the information the FBI collected and who else may have collected information regarding the targets:Papadopolous and Page both foreign policy advisors early on during the Trump campaign. Further, it would stand to reason that any information submitted on former Trump National Security Advisor Army Lt. Gen. Michael Flynn, would also come under scrutiny as well if it was used in any way during the investigation.

Another question that lingers is the FBI’s relationship with its alleged confidential informant Halper, who was a paid contractor for the DOD. He also apparently sent reports to the FBI and those reports would be significant in Durham’s investigation, according to sources.

Halper’s reports may or may not have been used in obtaining the FISA, on Page and whose reports may now come into question by the Justice Department, said several sources familiar with the Office of Net Assessment and the FBI.

Horowitz’s report is expected to be hundreds of pages long and mostly unredacted.

If that is the case, the majority of information that has been requested by Republican lawmakers but has remained classified on the Russia investigation may be declassified in an effort to get the report out to the American public, according to sources.

A crucial piece of the classified documents would be any exculpatory evidence that wasn’t presented to the FISA court, according to a senior lawmaker. It would in effect, be evidence that would say there was no collusion between Trump and the Russians and may very well be the evidence collected by Halper during his interactions with Trump’s advisors.

In May, Trump gave Barr the authority to declassify the documents, which have been described as four major buckets by Republicans.

On December 9, Horowitz, whose office has remained tight lipped on the matter, is expected to release the report and he will testify before Congress two days later on Dec. 11.

The index of property values increased 2.1% from September 2018, higher than the median estimate of 2%.

Source: Bloomberg

The 0.36% MoM jump is the biggest since March 2018.

Prices rose from the prior month in 17 cities, led by a 0.8% increase in Seattle and a 0.7% gain in Los Angeles.

Home prices fell in San Francisco, Chicago and Boston.

All 20 cities in the index, with the exception of San Francisco, showed annual gains, led by a 6% surge in Phoenix.

As S&P writes, home prices rose in September as lower mortgage rates and a solid labor market generated buyer interest in a market where supply remains lean.