AI Just Solved A 50-Year-Old Mystery That Could “Dramatically” Change How We Fight Cancer Tyler Durden

Wed, 12/02/2020 – 18:40

On the day our technological AI overlords decide to finally end the human race, we will be able to tout the feather in our cap that at one point they helped us solve some of the world’s toughest mysteries.

Such was the case with a science problem that the medical and scientific community has been struggling with for more than 5 decades. The problem of “mapping the three-dimensional shapes of the proteins that are responsible for diseases from cancer to Covid-19” appears to now have a solution – thanks to AI.

Google’s Deepmind now says it has created a program called AlphaFoldthat can solve the mapping problems in “a matter of days”, according to a new report from The Independent. If it works as claimed, the solution will have arrived “decades” before it was expected, the piece notes.

Of the 200 million known proteins, only a small amount are understood. The task of figuring out how each individual protein works is time consuming and expensive. This development could dramatically move our understanding forward further, and faster.

DeepMind claims that “AlphaFold determined the shape of around two-thirds of the proteins with accuracy comparable to laboratory experiments.”

The 14th Community Wide Experiment on the Critical Assessment of Techniques for Protein Structure Prediction (CASP14) partnered with Google for the project. The group is comprised of scientists who have been working on a solution for protein mapping since 1994, more than 25 years.

Dr John Moult, chair of CASP14, commented: “Proteins are extremely complicated molecules, and their precise three-dimensional structure is key to the many roles they perform, for example the insulin that regulates sugar levels in our blood and the antibodies that help us fight infections.”

He continued: “Even tiny rearrangements of these vital molecules can have catastrophic effects on our health, so one of the most efficient ways to understand disease and find new treatments is to study the proteins involved. There are tens of thousands of human proteins and many billions in other species, including bacteria and viruses, but working out the shape of just one requires expensive equipment and can take years.”

Nobel Laureate and Professor Venki Ramakrishnan said: “This computational work represents a stunning advance on the protein-folding problem, a 50-year-old grand challenge in biology. It has occurred decades before many people in the field would have predicted. It will be exciting to see the many ways in which it will fundamentally change biological research.”

The next step will be submitting a paper detailing the findings for peer-review.

via ZeroHedge News https://ift.tt/3qlSe4X Tyler Durden

Real Vision managing editor Ed Harrison joins editor Max Wiethe to discuss the potentially negative jobs data that Ed is watching out for later this week. Harrison also highlights the four fiscal cliffs between now and the inauguration that could potentially cause permanent economic damage and undermine the optimism surrounding the vaccine rotation trade. They also discuss the importance of perceived duration in how certain assets react to these surprises in real economic data. In the intro, Real Vision’s Peter Cooper discusses the new ADP numbers, the latest data on the spread of COVID-19 in the U.S., the U.K.’s emergency-use authorization of Pfizer and BioNTech SE’s vaccine, and president-elect Biden’s nominations for key economic positions in his administration.

via ZeroHedge News https://ift.tt/37vnu96 Tyler Durden

Creator Of The Bond VIX: It All Comes Crashing Down After 2025 Tyler Durden

Wed, 12/02/2020 – 18:20

By Harley Bassman, creator of the MOVE index, the “VIX for bonds”

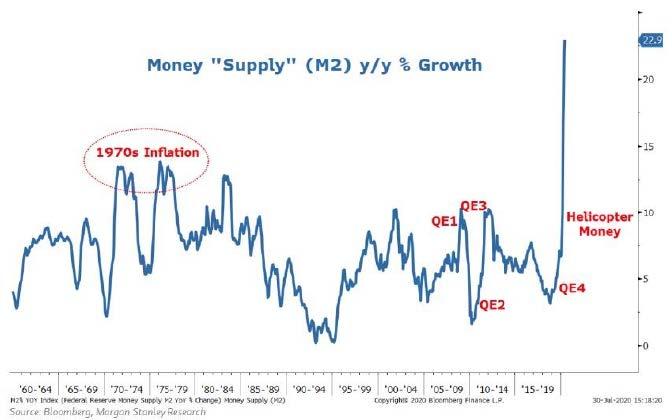

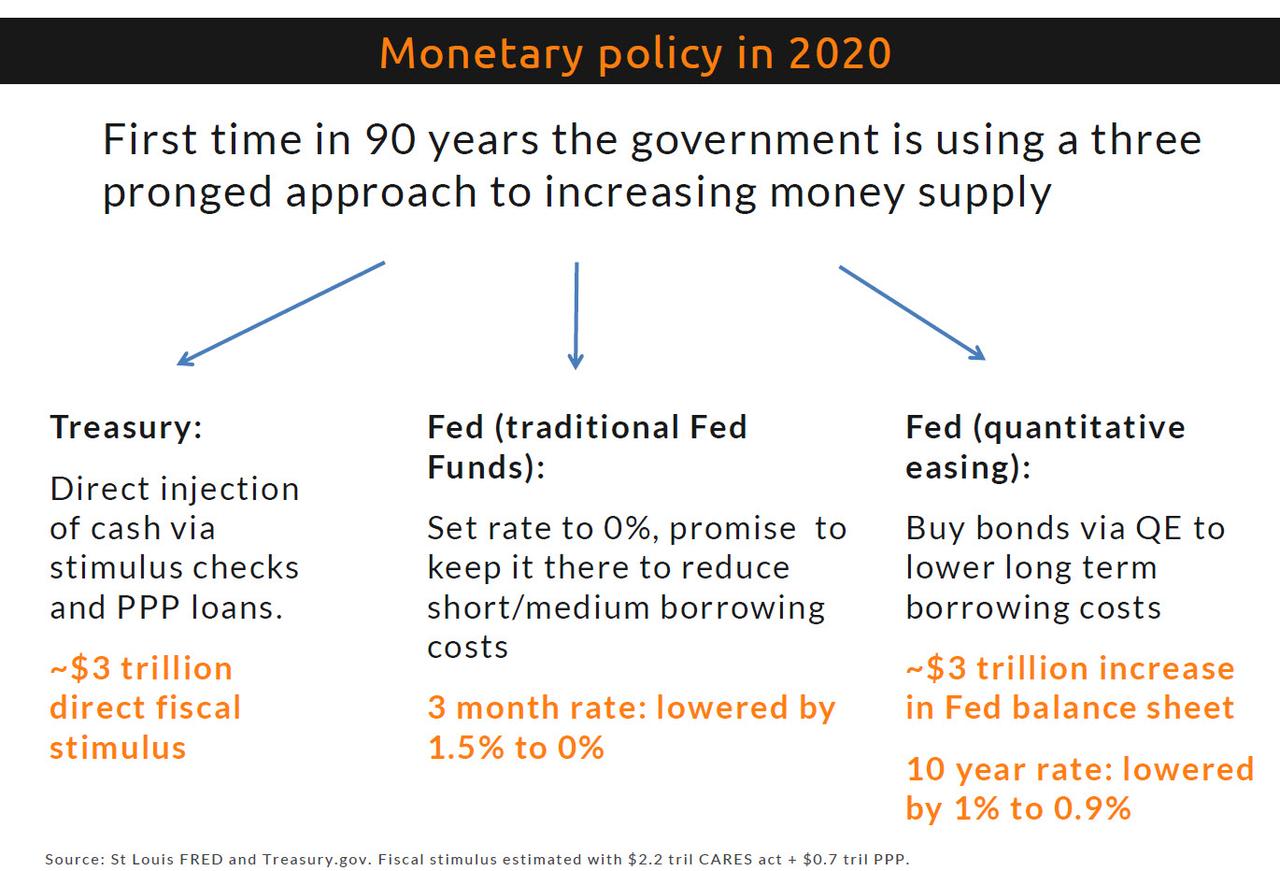

The lack of (CPI) inflation should not distract anyone from recognizing that our financial economy is presently overwhelmed by too much debt, both public and private; and it is beneath the cloak of systemic risk management that the Federal Reserve (FED) flipped on their printing press to support an alphabet soup of asset purchase programs.

And while I do not begrudge most of the FEDs actions to offer relief from both the Great Financial Crisis (GFC) and the COVID pandemic, what we all must recognize is that the financial remediation of these two crises have pulled forward the day of reckoning for how to fund the promise of Social Security and Medicare for the retiring Baby Boomer demographic.

The political game of “kick the can” for managing the two largest strands of our social safety net has reached an end; about a decade sooner than hoped. We are at a crossroads where one path is well trodden by financial history, and the other newly paved by an economic Pied Piper. But her siren song has been too sweet, and we are turning to the perfidy of Modern Monetary Theory (MMT).

Here we consider the reason and consequence of this dangerous road.

Only Congress can legally “spend” money (Fiscal Policy), and since they would not offer sufficient support in response to the GFC, the FED stepped in with (Monetary Policy) Large Scale Asset Purchases (LSAP), also known as Quantitative Easing (QE), as their most potent tool. These assets landed on the FED’s balance sheet.

While indeed much has changed over the past decade, sometimes to the point where facts do not exist, what has remained constant are the rules for double entry bookkeeping, where every asset must be paired with a liability.

Thus, the assets on the FED’s ledger are paid for by the creation of Money; an incongruity since by law the FED cannot “spend” money.

A Zero Interest Rate Policy (ZIRP) and QE were supposed to be interim measures that would be reversed upon an economic recovery; a progression always followed in the past. However, FED attempts at normalization were thwarted by the 2013 bond “taper tantrum” and the late 2018 equity tizzy.

The FED recognized that there are only two ways out of a debt crisis – either default or inflate with the caveat that inflation is simply a slow-motion default.

Since the market would not allow the FED to reduce its balance sheet via asset sales (or even the slow bleed of letting bonds mature), the alternate solution was to create inflation as a way to reduce the value of debt.

The FEDs dog-eared play book posited that if they increased the supply of Money (M2), and the economy held constant (Quantity), then Prices must rise (inflation) to keep the equation in balance.

GDP = Money * Velocity = Price * Quantity

Such a pity that Velocity collapsed, almost fully offsetting the increase (printing) of Money.

But do not toss out your economic textbooks just yet, as the seeming lack of inflation from the FEDs money-printing is a David Copperfield style illusion.

While CPI inflation barely registers a pulse, asset inflation is rampant. The Case-Shiller Index of residential housing is up 63% from its December 2011 low, and is 23% above its previous peak in June 2006. Gold kissed 2000 in August, an alltime high. And, of course, the S&P 500 is a five-bagger from early 2009.

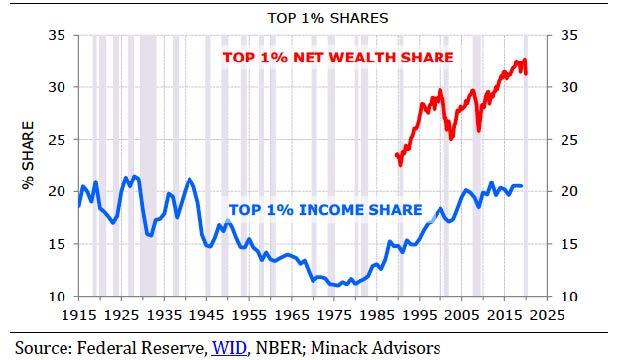

Notice how much of our national wealth is held by the Top 1%. While a 3%-point increase over the previous peaks may seem small, let me assure you that 3% of a huge number is an extremely large number. Strangely, income distribution held steady. If FED policies favored the wealthy, and their share of wealth increased, why did their share of income not rise in a similar fashion ?

Wealth concentration increased despite a static distribution of income because the affluent do not spend additional income. The Velocity of money declined because the dollars the FED created went into asset purchases instead of hourly wages where those funds would be recycled back into the economy.

A recent FED study reported that nearly 40% of US households do not have cash on hand to cover a $400 emergency expense (car repair or broken appliance). Surely funds directed to these households would soon be spent (recycled). Velocity is a measure of recycled spending; financial asset purchases are static.

I am loath to offer the topic of politics on these pages, if only because half my readers would soon use a hardcopy version for lining their bird cage.

But as a public policy comment, middle-class citizens should be mad as hell that Government resources were directed at policies that widened the wealth gap. I will stipulate this was NOT the intention of the FED; and that Fiscal policies by both parties have been grossly insufficient.

Thus, the trumpets have blared for the salve of Modern Monetary Theory.

As a reminder, Modern Monetary Theory (MMT) advocates suggest that Governments that create their own fiat currency can borrow so long as there is spare capacity in the economy. In a nutshell, deficits do not matter until debt capacity is reached, which will be signaled by rising inflation.

Never mind that nary an agency has created a predictive model for inflation; at best one can back test a few variables, but these models collapse in real time. Neither the FED, the CBO, nor the major Wall Street banks have successfully modeled inflation – as such, our policy makers will only dial back a debt binge after inflation occurs. This sort of risk management is akin to racing a car down a foggy lane and not hitting the brakes until after one slams into a tree.

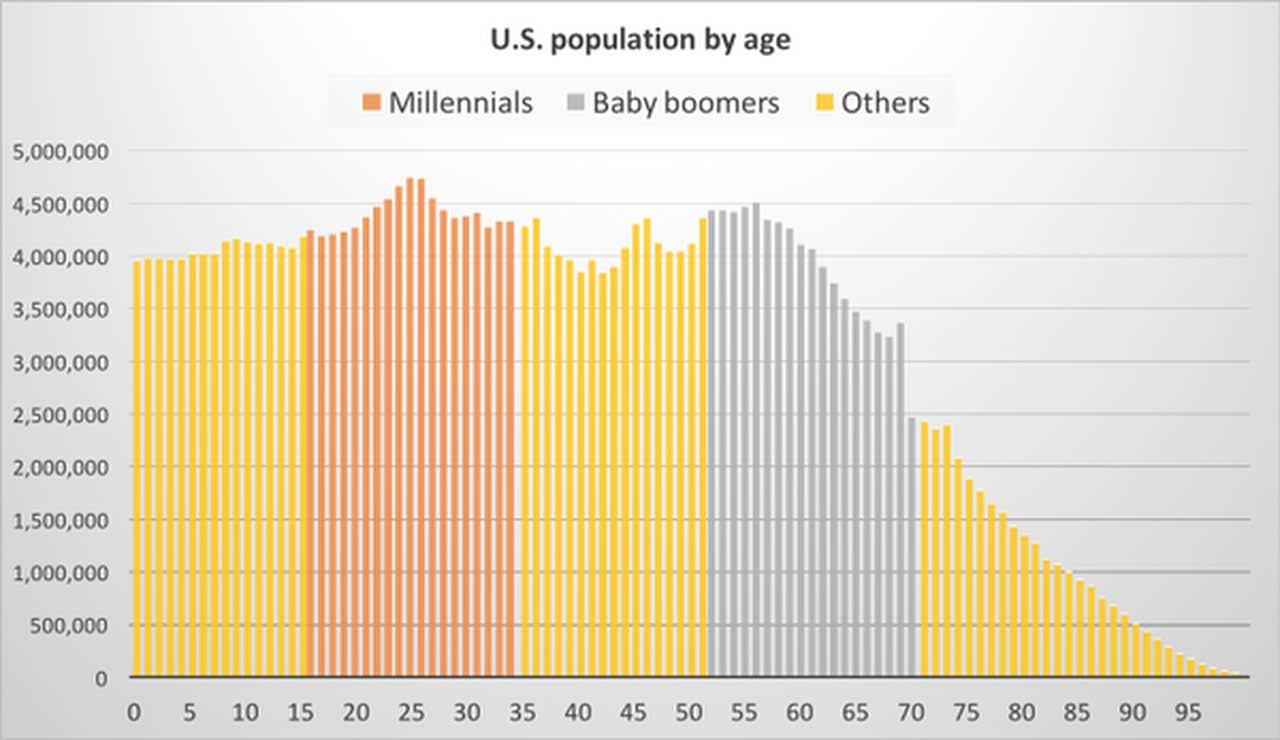

But MMT has arrived as a confluence of events are making economic demands on the Government that cannot be denied by a political class whose priority is reelection. The combination of a COVID support package, perhaps Millennial relief of college debt, and most important, the promise to Baby Boomers to fund Social Security (SS) will draw bipartisan votes in favor of a MMT-fiscal expansion.

Let’s be clear, MMT was coming with or without COVID, no matter who was elected President, but recent events have accelerated the process.

The high-end for a COVID relief package is tagged at $3Tn, and the notion of forgiving all college debt would cost $1.68Tn. But this is my bar bill at the club compared to the funding gap to support Social Security.

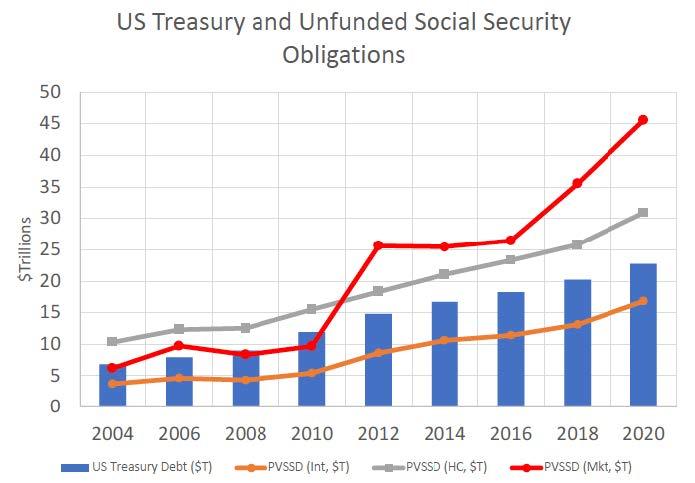

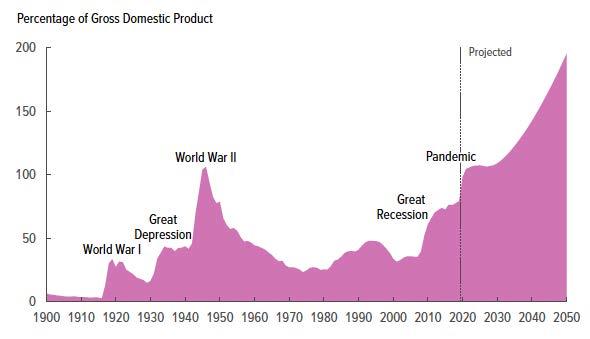

The chart above borrows from a scholarly report by James Moore, PhD. It shows the total US Treasury debt outstanding while the lines are the projected Social Security deficit. From the Social Security Trustees (SST), the orange line is their base-case while the gray line represents the SST’s high-risk scenario. Both were calculated using historical assumptions for interest rates, inflation, and economic growth.

The red line is the result of using current market-based inputs for interest rates and inflation. Notice how this estimate was between the SSTs base-case and high-risk scenarios until 2010, but impact of the Great Financial Crisis (GFC) exploded the future liability.

In case I was too coy, let’s link these thoughts. The US Government has run a cumulative deficit over the past 100 years of $22.7Tn; in contrast, to fully fund Social Security using current metrics would cost an additional $45.6Tn. Unless eligibility or benefits are significantly altered, some form of debt issuance that rhymes with MMT will be required.

The chart from the CBO offers a similar outlook as a percent of GDP. Notice the steep increase from 2030 to 2050 starts near 100% of GDP instead of closer to 40% of GDP before the GFC and COVID. These two events accelerated an already challenging decision process.

Here is the main point: This past decade’s money printing was used to purchase assets; this next decade’s money printing will be used to fund an expansive Fiscal policy which will funnel money into the hands of people who will spend it. Thus, the Velocity of money will increase and produce inflation.

By 2026 all of the Baby Boomers will qualify for Social Security, and the Millennials will be the largest voting cohort. Both will demand Fiscal support which can only be funded via MMT budgeted borrowing. The most prescient bond bulls (Lacy Hunt, David Rosenberg, Albert Edwards) have noted that the FED’s money creation has been a self-defeating process that may reduce rates further, with the caveat that direct monetization of fiscal spending could lead to inflation. In other words, direct funding the US Treasury.

This is a quibble that deserves a push. In the same way that one “borrows beer” at a party, having the Treasury wash their issuance through Wall Street dealers to the FED’s QE balance sheet is still “money printing”. The key difference is how those funds are used. Presently the FED’s asset purchases have coincided with reduced Velocity which dampened inflation; this will change when Fiscal money is directed toward those who will spend it upon receipt.

Modern Monetary Theory is nonsense; the excessive creation of a fiat currency (eventually) leads to inflation. If it did not, I can assure you there would be a shelf of books detailing such miracles over the past five thousand years of recorded history. “Stop eating when you are fat” is not a healthy diet.

Not to go native on you, but don’t you wonder why the Old Testament called for a trumpet to be sounded on the tenth day of the seventh month every 50 years for a Jubilee where all debts were cancelled ?

While it may take longer than I expect for the final denouement, mark this as the moment our political class shirked their duty to make the hard decisions.

Investment advice:

Don’t panic (yet) as MMT will be terrific for the first number of years. There will be a “sugar high” as expansive Fiscal policy transfuses money to those who will spend it. Similar to how corporate earnings expanded with the 2017 tax cut, so too should earnings enjoy the tailwind from Fiscal support to those who tend to spend.

College debt relief will initially increase retail sales, but will ultimately migrate towards home sales as this is the household formation demographic.

Developed Market (DM) Equities should do well, especially when the dividend yield for most DM Indices exceeds their Central Bank controlled rate.

I love Mortgage REITs despite a nice rally; their dividend yield is still ~9%. This payout should be stable if the FED keeps its promise of ZIRP until 2023.

Other ways of riding the FEDs rate suppression coattails can be sourced via well-managed BDCs and Muni CEFs that employ financial leverage. For CEFs, pay particular attention to the Undistributed Net Investment Income (UNII) as a deficit here usually presages a distribution cut.

I think it’s “safe in the pool” until 2023-25, then it will be adult swim only. This is why I own long-dated options to protect against rising interest rates – a product outlined in “Pigs Can Fly” – January 28, 2020, and I will detail again soon.

“If you tell a lie big enough and keep repeating it, people will eventually come to believe it…the truth is the mortal enemy of the lie.” – Joseph Goebbels

You know my rejoinder: “It’s never different this time.”

via ZeroHedge News https://ift.tt/33z3j8Y Tyler Durden

Iran To Boot Nuclear Inspectors Unless Access To Banking & Oil Markets Restored Tyler Durden

Wed, 12/02/2020 – 18:00

Critics of Trump and Pompeo’s maximum pressure campaign against Iran have argued that the sanctions strangulation and ‘dirty tricks’ actions which put the Islamic Republic on the extreme defensive and thus a militarized posture will only push it to pursue a nuclear bomb at all costs.

After all the mullahs see what happened to Libya and Iraq, and especially since the last January assassination of IRGC Quds Force chief Qassem Soleimani (and now the killing of its top nuclear scientist last Friday) consider that Iran is at war on multiple fronts against its enemies. As yet more proof, Iran is ready to take the most dramatic step yet pulling further away from prior designated restrictions on its nuclear energy development program:

A bill requiring Iran’s government to suspend nuclear inspections unless sanctions are lifted, and ignore other restraints on its nuclear program agreed with major powers, was passed by the hardline-led parliament on Tuesday.

IAEA inspectors at an Iranian facility, file image.

If this is done before Trump’s exit, it could serve as casus belli for military action. This after administration hawks – with Pompeo leading the way – have reportedly been given free reign to hammer Iran short of provoking major war.

A new report in The Daily Beast claims that “Trump has given some of his most hawkish administration officials, particularly his top diplomat, Mike Pompeo, carte blanche to squeeze and punish the Islamic Republic as aggressively as they wish in the coming weeks.”

The Iranians attached a timeline for the potential looming booting out of international inspectors: “Lawmakers later passed the full bill, including a provision requiring the government to suspend United Nations nuclear inspections if Western powers which are still part of the 2015 nuclear accords, as well as China and Russia, do no re-establish Iran’s access to world banking and oil markets within a month,” according to Reuters.

Iran will be asked for additional concessions for sanctions relief, says Biden’s new NSA head.

Opening gambit? Negotiations will be bumpy. Iran will ramp up refinement & and use China’s willingness to break sanctions as counter gambit. https://t.co/mNeteCki0l

This is also likely designed to give Iran greater leverage going into talks and negotiations with the new Biden administration. The President-Elect has vowed to try and get the US back into the 2015 nuclear deal brokered under Obama, but of course Iran has already blasted past nuclear enrichment level caps stipulated by the deal as a response to US sanctions.

The current US administration has also promised to derail any future Biden attempts to restore participation in the JCPOA. If Iran does move to end the nuclear inspections program, this could indeed seriously hinder any Biden initiative to restore peaceful relations.

via ZeroHedge News https://ift.tt/3qol70s Tyler Durden

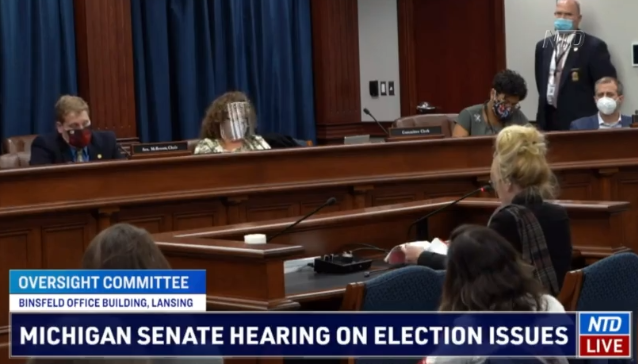

Dominion Whistleblower Testifies On “Complete Fraud” At Detroit Voting Center Tyler Durden

Wed, 12/02/2020 – 17:40

A contractor for Dominion Voting Systems who was present during the Nov. 3 election at Detroit’s TCF Center testified at a Senate Committee hearing on Tuesday, telling the panel that she saw fraud throughout the day, as well as on Nov. 4, according to the Epoch Times.

“What I witnessed at the TCF Center was complete fraud. The whole 27 hours I was there, there were batches of ballots being ran through the tabulating machines numerous times, being counted 8 to 10 times. I watched this with my own eyes; I was there to assist with IT,” said Melissa Carone, who added that there were ‘completely untrained’ people working night shift – including a friend she’s known for two decades.

“They were allowed to do whatever they wanted to do. I, Nick, and Samuel, that worked for Dominion, they were on the stage. They had a contract employee, me, and another one that was from Texas—I have his name right here, Miles Smiley, 90-year-old man, there to assist with IT work. And he did not have any kind of background in IT and lived in Tennessee. So this man was just walking around aimlessly. I was really the only one running around like crazy helping these people,” she said.

Carone also claims that batches of ballots were being scanned 8-10 times, and that ballots were able to be accessed by election workers after being scanned – when they are supposed to be dropped into a sealed box and preserved.

The boxes, she said, were moved across the room and used to block GOP observers. In addition, Carone said that one Dominion employee disappeared to a “warehouse” for several hours before there was a large ‘data dump for Biden.

Carone says the proper way to scan ballots when there’s a paper jam is to reset the count, in other words, discard the count, on the machine and rescan all of them with the jammed paper on top.

But, apparently, that didn’t happen and counters rescanned ballots without resetting the count.

In an interview with The Epoch Times, Carone says that Dominion hasn’t contacted her since she submitted her affidavit.

via ZeroHedge News https://ift.tt/3oi1C7T Tyler Durden

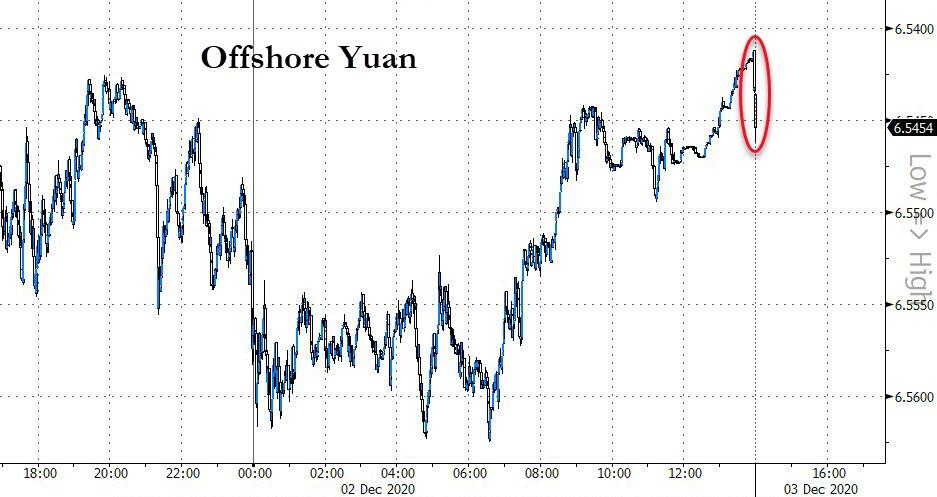

House Passes Bill Forcing Chinese Companies To Agree To Audit Oversight Or Delist From US Tyler Durden

Wed, 12/02/2020 – 17:22

Not long after a top US intelligence official unveiled the existence of a Chinese intelligence operation, the House passed a bill that, should it become law, would force Chinese companies listed in the US to either adhere to strict American accounting standards, or delist and go elsewhere.

We’ve reported on the push to pass the bill several times. Trump made the issue a high priority this fall as election day neared. The bill targets a loophole that allows Chinese companies to essentially write their own rules when it comes to auditing, something that has led to literally dozens of corporate frauds that have cost American and international investors billions of dollars.

The collapse of Luckin Coffee and the CCP’s bailout of Evergrande helped to underscore the fact that Chinese companies essentially play by their own rules, and if foreign investors get screwed, so be it.

But the Trump team made it a centerpiece of its late game push against China, and now the legislation has finally passed the Democrat-controlled House. It’s in Trump’s hands now, as GOP Sen John Kennedy, one of its authors, pointed out in a tweet. Though we suppose it’s possible the US could strike some kind of deal with Beijing in the mean time.

Communist China is right now using U.S. stock exchanges to exploit American workers and families—people who put their retirement and college savings in public companies.

Today, the House joined the Senate in rejecting that toxic status quo UNANIMOUSLY. https://t.co/Zv6ukt8wP2

The news has hit the offshore yuan; it has perhaps also stoked fears that the US might somehow miss out in the economic resurgence reportedly taking place in Asia, which has done a much better job of stamping out the virus than the rest of the world.

The surfeit of fraud-ridden Chinese firms created an atmosphere where short sellers like Citron Research and Muddy Waters Research minted reputations (and billions of dollars for themselves and their backers) as they rooted out evidence of fraud like a kind of hedfe fund blood sport.

These firms have collectively worked, along with others, to help expose innumerable frauds and misstatements from companies based in China. A movie, “The China Hustle”, was even made about this very topic.

The Public Company Accounting Oversight Board, an entity created by Sarbannes-Oxley to oversee accounting standards at US-listed companies, has been repeatedly unsucessful in its attempts to secure cooperation from China on a broad scale. The PCAOB has often had to sue Chinese audit firms and negotiate with Chinese regulators for more information. Now, new regulations could put the responsibility on the listing exchanges, like NASDAQ and NYSE, who choose to give credibility to China-based entities by accepting their listing fees and putting them on their well known exchanges.

It has been reported that the administration is trying to pass the new rules before outgoing SEC head Jay Clayton leaves at the end of the year. The Biden administration can then presumably “tweak” them to a degree.

These same exchanges have helped make Chinese businessmen like Alibaba founder Jack Ma into billionaires. But they never even managed to offer any kind of real oversight of companies like Alibaba.

Ma is now getting his comeuppance after publicly griping about some obscure regulatory feature in China, apparently angering China’s leaders to such a degree that they cancelled the spinoff of Alibaba’s Ant Financial.

via ZeroHedge News https://ift.tt/3fZLFQK Tyler Durden

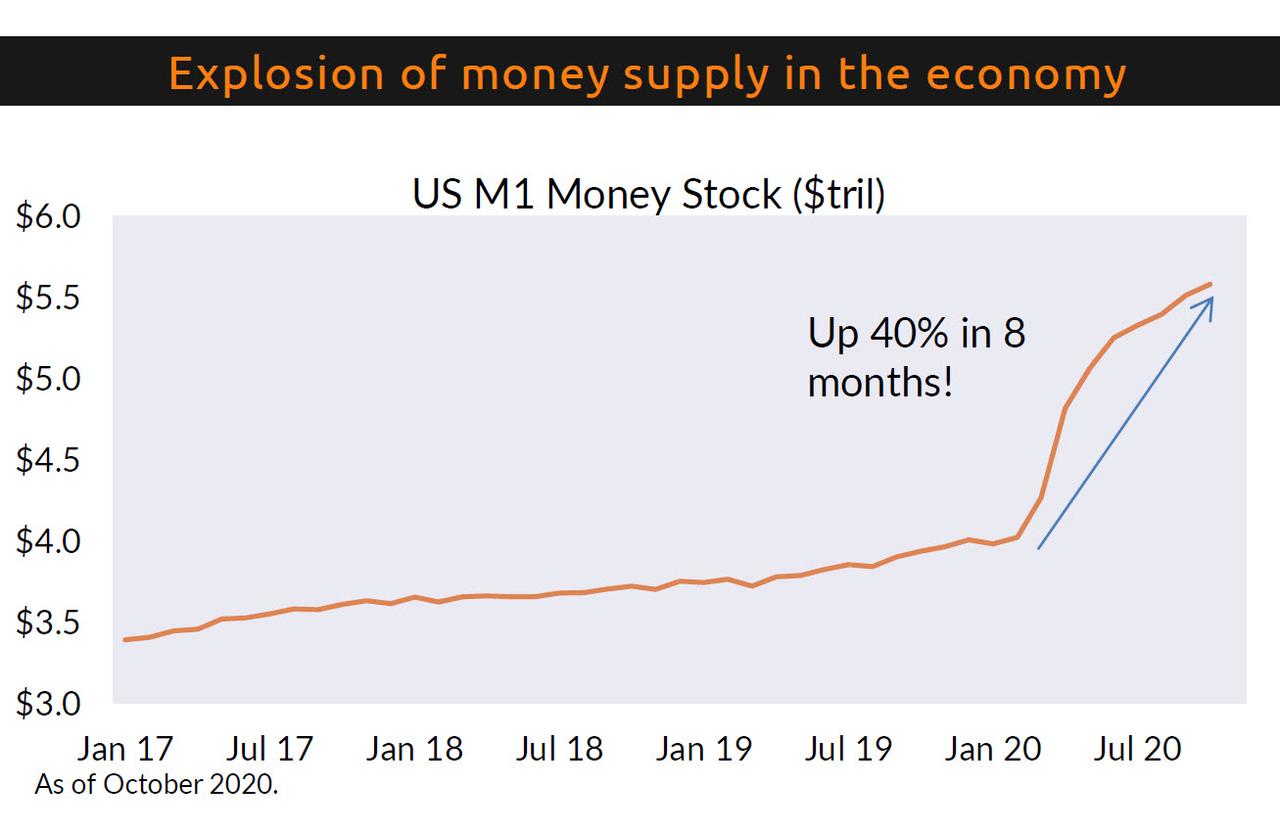

Print enough money and you can increase asset prices under any circumstance. The government has printed 40 cents for every dollar that existed in March.

All things equal, this would translate to 40% inflation as prices rise due to increased money supply. Of course, in reality inflation increased less than 1%…

… because economic activity slowed down so much and savings rates skyrocketed.

While it can seem like the lack of inflation gives the government a free pass to print, the printing is not without consequences. The money is flowing through to higher financial inflation and lowering the value of the dollar relative to other currencies and gold.

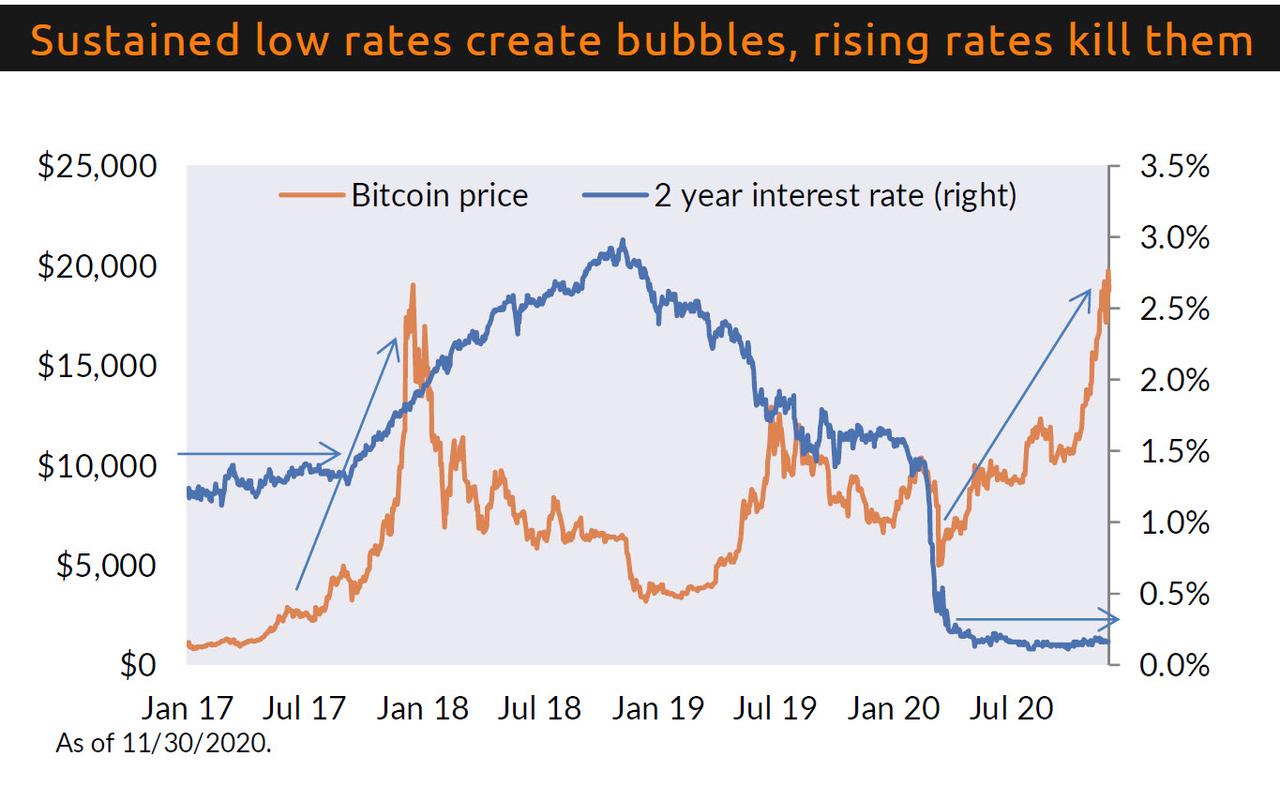

The combination of massive printing and historically low rates is producing bubble like behavior in many markets like crypto-currencies, much like in 2017. Of course in 2017, the Fed began to withdraw liquidity and crushed many of those asset bubbles.

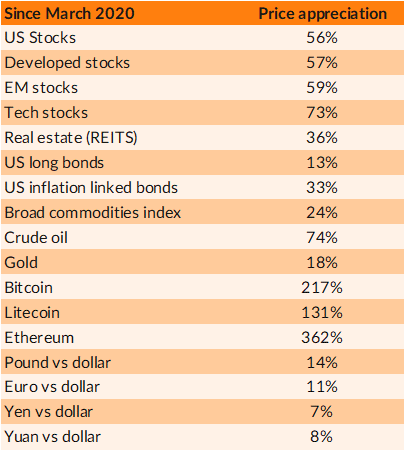

This time around we are also seeing a torrent of new casual day traders, reminiscent of stories you read about the Roaring Twenties. Below I show the indiscriminate price appreciation across the board since the government rescued the markets in March.

As you can see, the 40% increase in money supply didn’t go into the real economy, but sloshed all around the financial markets. The price of anything is measured in the form of dollars per unit whether it is $/share, $/bond, $/house, $/barrel, etc. So the price of everything comes down to those two things, supply of assets and the quantity of money chasing those assets. More money chasing fewer assets means higher prices, and vice versa. This year has been an extreme example of how if you print enough money, you can increase asset prices under virtually any circumstance.

Going forward, I believe the Fed and the Treasury’s top priority will continue to be the real economy. Asset bubbles are an unfortunate side effect of massive liquidity, high savings rate and low interest rates. They’ll need to carefully manage those bubbles as recover from COVID such that the bursting won’t topple the real economy. See the deck below for a more in-depth discussion.

via ZeroHedge News https://ift.tt/39zkL0O Tyler Durden

The comments come just days after Biden and his team announced their nominees for top foreign policy positions, along with key appointments like Janet Yellen to Treasury and other economic-policy posts. They have been sourced to Bill Evanina, the director of an obscure but critical intelligence agency known as the US NCSC. The comment was reportedly made during remarks at the Aspen Cyber Summit, which has reliably generated newsmaking comments and headlines in recent years.

That Evanina’s comments are even being picked up by the wires is almost surprising, considering that Bloomberg has a reputation for being soft on China for fear of compromising its terminal business.

But at second glance, it’s obvious why: Evanina also insisted that the 2020 election was flawlessly done.

A former Bloomberg editor attested a few years back that they were stopped from publishing stories about the accumulated, hidden wealth of President Xi and his family members. When Beijing launched its purge of Western reporters earlier this year, Bloomberg wasn’t hit nearly as hard as the NYT, WSJ and other American news organizations.

Continuing on the China theme, Evanina added that the world’s second-largest economy is now “the existential threat we face” in the US.

Indeed, as President Xi’s actions to punish foreign governments, as well as critics and dissidents both abroad and within its boarders, intensify, it’s more important than ever that an American president can stand up to the Politburo, and hold his ground.

When people become desperate enough, those in power can get most of them to do just about anything. The first wave of lockdowns knocked us into the worst economic downturn since the Great Depression of the 1930s, it sent suicide rates soaring all over the globe, and it plunged millions upon millions of ordinary citizens into a deep state of despair. Now another wave of lockdowns is being instituted all over the planet, and this is going to perfectly set the stage for the “solutions” that the elite plan to offer all of us in 2021.

It has been said that if you want people to be willing to accept a solution, first you have to make them realize that they have a problem.

And once this “dark winter” finally ends, almost everybody will be absolutely desperate to return to their “normal” lives.

With each passing day, more extremely harsh restrictions are being imposed. For example, a brand new “stay at home order” was just issued in Los Angeles County…

All public and private gatherings with anyone outside a single household are now banned in Los Angeles County, as most of the country grapples with an unprecedented surge of Covid-19.

The ban will last three weeks, starting Monday and ending December 20.

It would be nice if the lockdown actually does get lifted before the end of the year, but for at least the next three weeks all 10 million people living in L.A. County will be forced “to stay home as much as possible”…

All 10 million residents are asked to stay home as much as possible and wear face masks when outside — even when exercising at the beach and parks, said the Los Angeles County Department of Public Health, which issued the order last week.

On top of that, California Governor Gavin Newsom is warning that he may soon impose “much more dramatic, arguably drastic” restrictions for the entire state…

California Gov Gavin Newsom just warned that more drastic steps could be taken to contain the virus after the state reported another 15k+ new cases yesterday. The Golden State could be facing “much more dramatic, arguably drastic” measures to contain the spread of the virus. The state also broke its record for hospitalized patients yesterday: The state reported 7,415 coronavirus hospitalizations, with more than 1,700 of those patients in ICUs. The number of hospitalizations broke the state’s previous record of 7,170 in July.

Unfortunately, we are witnessing similar craziness all over the nation. In New Mexico, the new restrictions that were just instituted created so much panic that people were soon waiting for hours just to get into a supermarket to shop for food…

New Mexico Gov. Michelle Lujan Grisham (D) has put immense pressure on businesses with her “abrupt” lockdown order – forcing “nonessential” businesses to close and creating what has been dubbed “modern breadlines” — with people waiting 2-4 hours to enter essential retailers, former GOP Senate candidate Elisa Martinez explained during an appearance on Breitbart News Saturday.

After seeing what the first round of lockdowns did to our nation, why would these politicians want to do it again?

More than 70 million Americans have filed unemployment claims so far in 2020, more than 40 million could be facing eviction in 2021, and there has been a dramatic spike in suicides during this pandemic.

When a 90-year-old woman named Nancy Russell found out that another lockdown was happening in her area, she decided to opt for assisted suicide…

According to CTV News, a 90-year-old woman living in Toronto took her own life via medically assisted suicide, the choice made in large part due to the second surge of coronavirus cases and a looming period of increased restrictions.

As I keep reminding my readers, there is always hope if you look at the bigger picture and suicide is never the answer to anything.

Unfortunately, most people are not getting a message of hope from the mainstream media, and Russell decided that the months ahead were going to be too bleak in her nursing home for her to be able to handle…

Residents eat meals in their rooms, have activities and social gatherings cancelled, family visits curtailed or eliminated. Sometimes they are in isolation in their small rooms for days. These measures, aimed at saving lives, can sometimes be detrimental enough to the overall health of residents that they find themselves looking into other options.

Just as we are hitting a low point with this pandemic, authorities all over the globe are announcing that vaccines will soon be available.

In fact, it is being reported that as many as ten different vaccines could be available by the middle of 2021…

Ten COVID-19 vaccines could be available by the middle of next year if they win regulatory approval, but their inventors need patent protection, the head of the global pharmaceutical industry group said on Friday.

As soon as the public can get them, it is inevitable that millions upon millions of people will rush out to get their shots so that they can return to their “normal” lives.

But what they aren’t telling you is that these new vaccines are entirely different from vaccines that you may have gotten previously.

When Moderna was just finishing its Phase I trial, The Independent wrote about the vaccine and described it this way: “It uses a sequence of genetic RNA material produced in a lab that, when injected into your body, must invade your cells and hijack your cells’ protein-making machinery called ribosomes to produce the viral components that subsequently train your immune system to fight the virus.”

“In this case, Moderna’s mRNA-1273 is programmed to make your cells produce the coronavirus’ infamous coronavirus spike protein that gives the virus its crown-like appearance (corona is crown in Latin) for which it is named,” wrote The Independent.

Under normal circumstances, very few people would sign up to have their cells “hijacked”, but at this point millions upon millions of people will be so desperate for a “solution” that they will take a vaccine no matter what the long-term consequences might be.

The International Air Transport Association (IATA) announced this week it is in the final phase of development for what it hopes will be universally accepted documentation that in turn could boost confidence among wary travelers.

The digital health pass would include a passenger’s testing and vaccine information and would manage and verify information among governments, airlines, laboratories and travelers.

If these new “digital vaccine passports” are implemented for international travel, it is probably just a matter of time before they are required for domestic travel as well.

Of course there are lots of people out there that are trying to sound the alarm about all of this, but UN communications director Melissa Fleming says that her organization has already recruited an army of “110,000 information volunteers” to combat the spread of “misinformation”…

Fleming told the World Economic Forum that #PledgetoPause and Verified have “recruited 110,000 information volunteers” thus far. She said “we equip these information volunteers with the kind of knowledge about how misinformation spreads and ask them to serve as kind of ‘digital first-responders’.” Fleming has stated elsewhere that the UN has “reached out to Member States, UN media partners, celebrity supporters” and “businesses” “to help us disseminate to the millions we will need to reach” with the campaign.

They want to control what you think as they lead you into a dystopian future that will ultimately turn into a complete and utter nightmare.

The truth is that none of us will be going back to our “normal lives” ever again.

But the elite will continue to hold that carrot out there in order to get you to do what they want, and millions upon millions of people will fall for it.

* * *

Michael’s new book entitled “Lost Prophecies Of The Future Of America” is now available in paperback and for the Kindle on Amazon.

via ZeroHedge News https://ift.tt/36tHA4e Tyler Durden

{kind=link}