Watch House Democrats Hold Debate Before Vote On Formal Impeachment Procedures

House Democrats on Thursday will debate and then hold a vote on a formal roadmap for President Donald Trump’s impeachment, as several key witnesses have provided testimony this week supporting claims that the Trump administration withheld nearly $400 million in military aid to Ukraine unless they investigated allegations of corruption against former Vice President Joe Biden and his son Hunter.

One day after a decorated army officer told Congressional investigators he witnessed Trump and a senior diplomat pressure Ukraine, three other State Department officials on Wednesday offered more evidence in testimony that supported the allegations against the US leader.

And the inquiry testimony set dates for three more witnesses, including Trump’s estranged former National Security Advisor John Bolton, who would have had first-hand knowledge of the president’s alleged effort to leverage military aid to Ukraine in exchange for President Volodymyr Zelensky investigating his Democratic rival Joe Biden. –AFP via Yahoo

President Trump has blasted the investigation as a “witch hunt,” and has insisted that there was no “quid pro quo” proposed during his communications with Ukrainian President Volodomyr Zelensky.

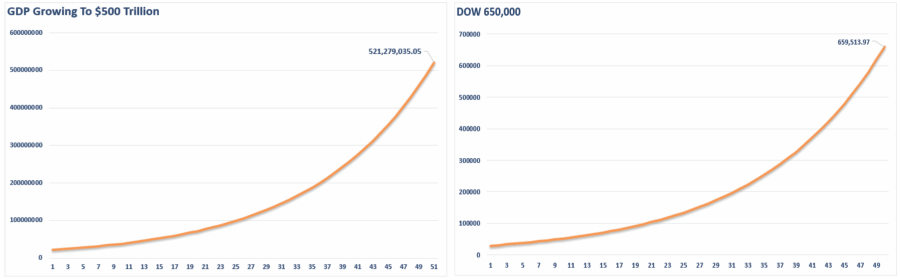

“Speaking from his annual investment conference in New York, Baron predicted the Dow Jones Industrial Average, based on historical moves over decades, will reach 650,000 in 50 years, with an over $500 trillion U.S. economy.”

Doing some quick math, that assumption is for a 6.6% annualized return on both the Dow and the U.S. economy, as noted by Ben Carlson.

This is roughly a 6.6% annual return to get to Dow 650k

Both are innocuous tweets, meant with the best of intentions to leave you with a sense of optimism about your financial future.

I get it. Really.

As Bob Farrell once quipped:

“Bull markets are more fun than bear markets.”

Here is the problem.

It’s complete bulls*** on both counts.

Mr. Baron, as noted, was speaking at his “buy and hold” conference, and the tweet was meant to both grab attention and headlines.

It worked.

The problem with being “bullish all the time” is that it is also very dangerous.

This is particularly the case in late-stage “bull markets,” where poor investment decisions, and excessive portfolio “risk,” are masked by seemingly ever-rising prices. Previously bad investment ideas, products, and strategies tend to resurface in a different form or package. Investment strategies like “buy and hold” and “dollar cost averaging” become popular even though they are absolutely guaranteed to leave you well short of your financial objectives in the future.

So, what does this have to do with CNBC’s article?

It has everything to do with one of my “pet peeves,” and the biggest fallacy pushed by Wall Street today – “compound returns.”

Markets/Economies Don’t Compound

Let’s start with the economy.

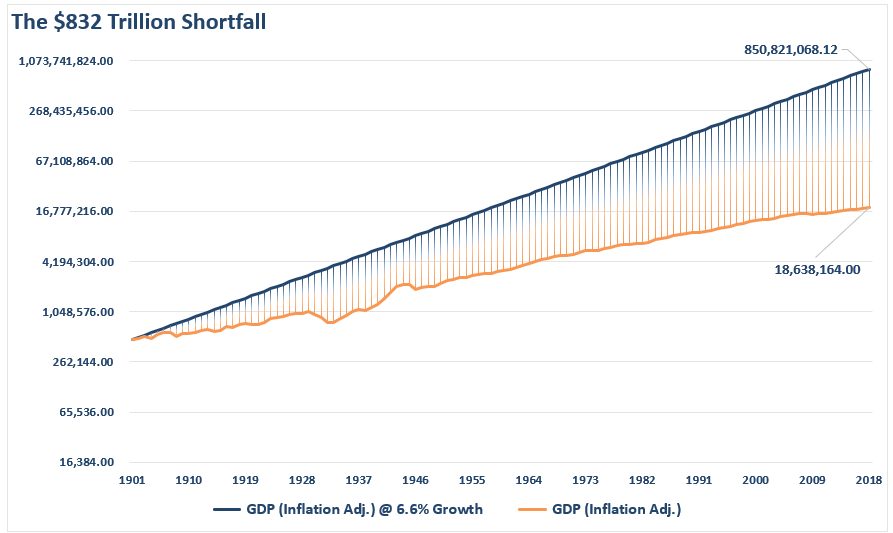

The economy hasn’t seen an annualized growth rate of 6% since the 1950’s when the U.S. was the manufacturing hub of the entire world. Following WWII, the majority of Europe, and Japan following two nuclear bombs, were devastated. Today, the U.S. is no longer a manufacturing hub, but a services provider for ever-lower costs. Services, as compared to manufacturing, has a very low economic multiplier effect. Given $22 Trillion in debt and climbing, the attainment of a 6% growth rate is not a possibility.

The chart below pretty much details the problem.

It is often stated the U.S. economy has grown by more than 6% on average over the long-term. (This is a true statement) However, it is also a very misleading statement. Average and actual growth are two very different things.

If we go back to 1901 and assume the economy grew at 6.6% annualized, as Mr. Baron suggests will happen in the future, the economy would currently be roughly $852 trillion in value, rather than just a paltry $19 trillion.

What happened?

A lot of years of very low, or negative, economic growth.

The same thing holds true with the Dow.

As noted, Mr. Baron suggests the Dow will be valued at 650,000 in the next 50-years. So clearly, as a young investor you should just sock all your hard-earned savings into an “index fund” and hang on.

“The stock market is literally the same thing as a high-yield savings account.” – Jim J. (names have been changed to protect the stupid.)

Here’s the thing.

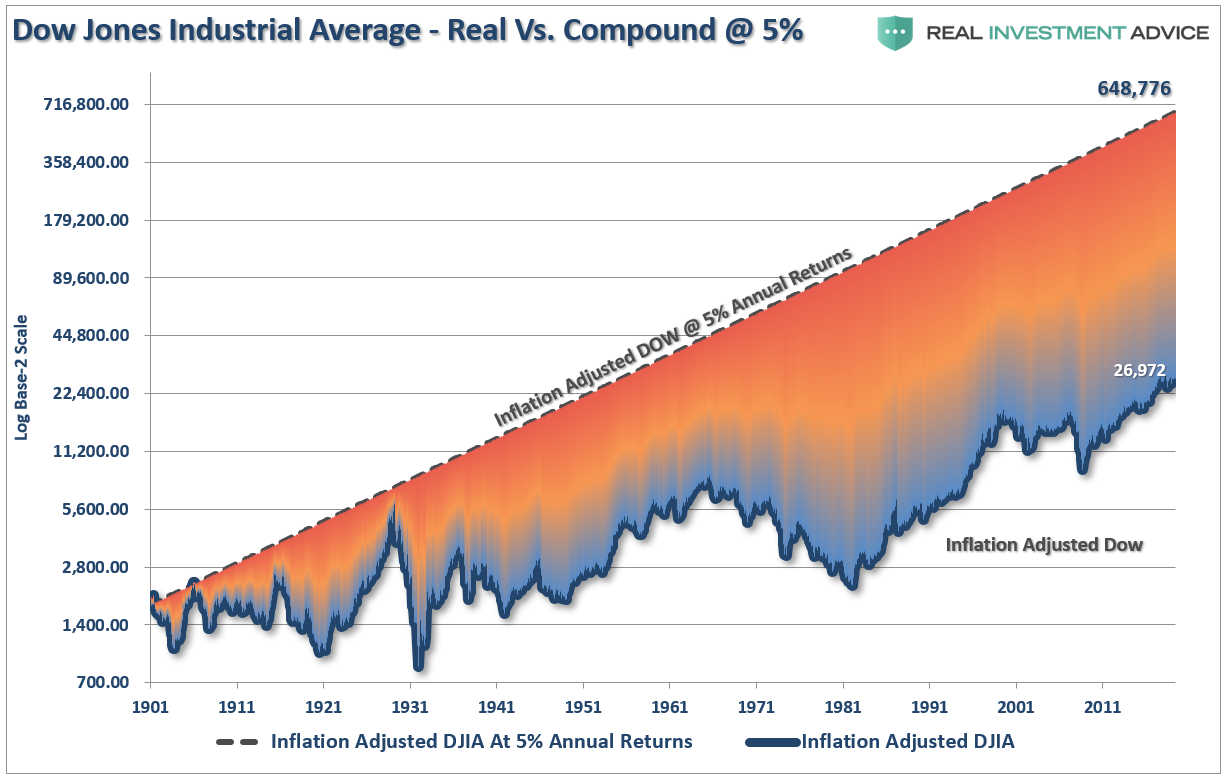

It has often been stated the markets have had an average annual return of 8-10% depending on who you ask. If we just assume the Dow had compounded at just 5% since 1901, we would already be at 650,000.

But it’s not.

We are just stuck here at a “crappy ole’ 27,000.”

There is a huge difference between compound returns and average returns. The historical performance of the markets since 1900, including dividends, has averaged a much higher rate of return than just 5% annually. Therefore, the Dow should actually be much closer to 1,000,000 than 650,000.

Again, it’s not.

Nope…we are just hanging out way down here at 27,000.

Why? Because crashes matter. This is particularly the case when it comes to your financial goals and investing time horizons.

Think about it this way.

If “buy and hold” investing worked the way that it is preached, then why are the financial statistics of 80% of Americans so poor?

The three biggest factors are:

Destruction of capital;

Lack of savings, and;

Time.

While lost capital gain be regained, the time lost “getting back to even,” cannot be. Unfortunately, we don’t live forever, and time is our ultimate enemy. This is also, after two major bear markets, the majority of “boomers” are simply unprepared financially for retirement.

It is also the reason why we are facing a massive “pension crisis”in the not so distant future as capital destruction, low contribution rates, and over-estimation of returns has led to massive shortfalls to meet required distributions in the future.

Who wouldn’t love a world where everyone just invests some money, the markets rise 6% annually, and everyone one’s a winner?

Unfortunately, there is a vast difference between an “index” which benefits from share buybacks, substitutions, and market capitalization weighting versus a portfolio invested in actual dollars. Yes, a “buy and hold” portfolio will grow in the financial markets over time, but it DOES NOT compound.

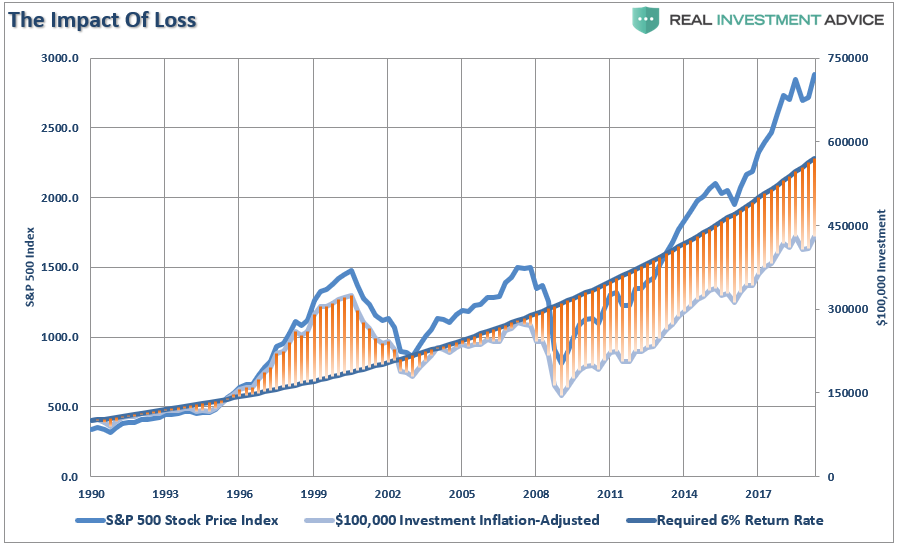

Read this carefully: “Compound returns assume no principal loss, ever.”

To visualize the importance of this statement, the chart below shows $100,000, adjusted for inflation, invested in 1990 versus a 6% annual compound rate of return. The shaded areas show whether the portfolio value exceeds the required rate of return to reach retirement goals. As noted, due to the impact of two bear markets, portfolios are well short of the targeted 6% annualized rate of return investors were told they would receive.

If your financial plan required 6% “compounded” annually to meet your retirement goals; you didn’t make it.

See the problem? People 30-years ago who were hoping to retire, simply can’t. It will likely be the case for individuals today looking to retire 30-years from now.

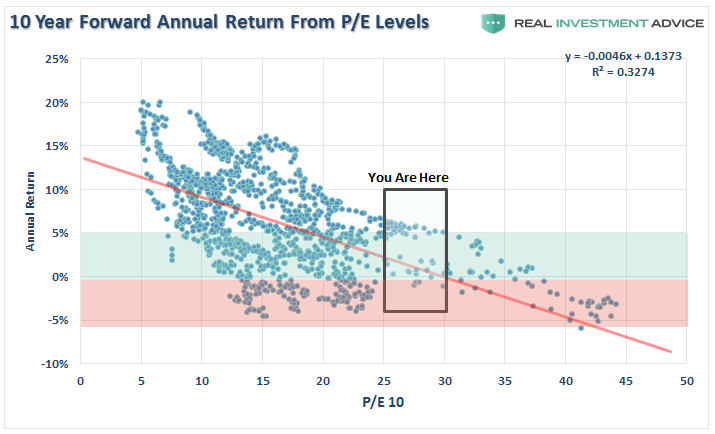

With markets now back to the second highest level of valuations on record, forward returns over the next 10-years are going to be substantially lower than they have been over the past 10-years.

That isn’t being bearish. That is just math.

Dr. John Hussman previously wrote the most salient point on this topic.

“Put simply, most apparent ‘opportunities’ to obtain investment returns above zero in conventional assets over the coming decade are based on a misunderstanding of valuations, total returns, and historical yield relationships. At current valuations, virtually everything is priced for a decade of zero.”

Throughout history, bull market cycles are only one-half of the“full market”cycle. This is because during every “bull market” cycle the markets, and economy, build up excesses which are “reverted” during the following “bear market.”

As Sir Issac Newton once stated:

“What goes up, must come down.”

Looking beyond the very short-term overly optimistic view of “this time is different,” the coming unwinding of current speculative extremes will occur with the completion of the current market cycle.

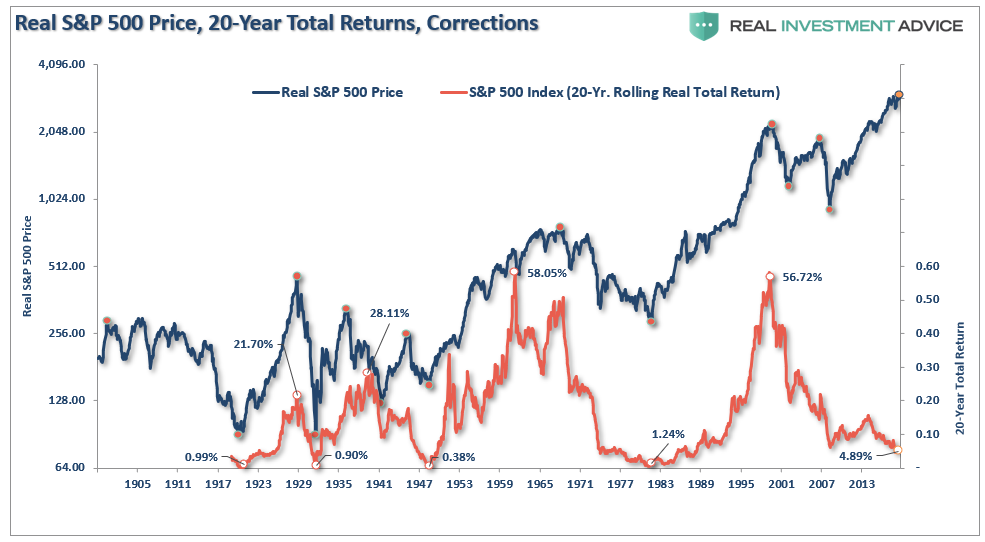

When we look at 20-year trailing returns, there is sufficient historical evidence to suggest total, real returns, will decline towards zero over the next 3-years from 7% annualized currently. (These are trailing 20-year total real returns, not forward)

Re-read that last sentence again and look closely at the chart above. From current valuation levels, the annualized return on stocks by the end of the current 20-year cycle will be close to 0%. A decline in the next 3-years of only 30%, the average drawdown during a recession, will achieve that goal.

The second-half of this current cycle will begin likely sooner, rather than later. As stated, it is a function of time (length of market cycles), math (valuations) and physics (price deviations for long-term means.)

I am not bullish or bearish.

My job as a portfolio manager is simple; invest money in a manner that creates returns on a short-term basis while reducing the possibility of catastrophic losses over the long-term.

While “bulls have more fun” while markets are rising, both “bulls” and “bears” are owned by the “broken clock” syndrome during the completion of the full-market cycle.

The biggest secret in achieving long-term investment success is not necessarily being “right” during the first half of the cycle, but by not being “wrong” during the second half.

This is a lesson that CNBC should have learned by now.

After a brief, hope-filled, bounce in August, October’s Chicago PMI is a shitshow, plunging from 50.4 in August to 43.2 (contraction) in October (well below the 48.0 expected).

Source: Bloomberg

This is the biggest 8-month drop since July 1980…

Source: Bloomberg

Under the hood:

Prices paid rose at a slower pace, signaling expansion

New orders fell at a faster pace, signaling contraction

Employment fell at a slower pace, signaling contraction

Inventories fell at a slower pace, signaling contraction

Supplier deliveries rose at a faster pace, signaling expansion

Production fell at a slower pace, signaling contraction

Order backlogs fell at a faster pace, signaling contraction

This is unpossible… haven’t the people living in Chicago looked at the stock market recently?

Rabobank: “Is It Getting Crazier Out There, Or Is It Just Me?”

Submitted by Michael Every of Rabobank

Happy Halloween! On what was supposed to be Brexit day we instead need to find other things to be scared of. Fortunately, there are plenty out there. Indeed, Halloween seemed an appropriate time for me to finally watch ‘Joker’ – and if there was ever a film oozing angry ‘Age of Rage’ populism this is it. It literally shouts “Kill the rich!” in places. Ironically, trying to watch Joker while several rows in of seats in front of me were illuminated by mobile phones held aloft like lighters during an 80’s hair-metal power ballad by a generation too young to even know what the 1980’s were almost produced the same violent reaction in me as one scissors-related scene: amazingly, even said scene did not prompt the guy in front of me to look up from his device. “Is it getting crazier out there, or is it just me?”

Meanwhile, a Joker-style uprising in Chile has seen the country forced to cancel hosting the 2020 APEC summit. That’s the kind of barbarians-getting-through-the-gates development that markets really don’t like; and unless a Trump resort is available(?) perhaps there will be no APEC at this year. In which case, where are Trump and Xi going to sit down and sign this ‘phase one’ trade deal? (The one that we think is an empty box rather than anything substantive.)

Anyway, checking after viewing I see that Joker currently has a 69% critics rating on the review-aggregator website Rotten Tomatoes vs. an 89% audience score. That’s an arbitrage opportunity–buy or sell it, depending on which score you trust–but not as large as for a new D.C.-Universe neighbour, the Batwoman TV show, which has a 71% critics rating but just a 12% audience score. Is it angry US culture wars or are Russians involved somewhere again?

The question is being asked in the real D.C. universe in the presidential impeachment process. With no irony, the latest bomb dropped is that John “Bomb ‘em” Bolton is to testify; a man alleged to be akin to a previous Joker iteration in that he “just wants to see the world burn” is now being looked at as a voice of reason by those same critics. Of course, as every step is taken members of the D.C. team will be checking audience vs. critics scores to see if impeachment really is a good idea or not politically – and that arbitrage is again important for markets.

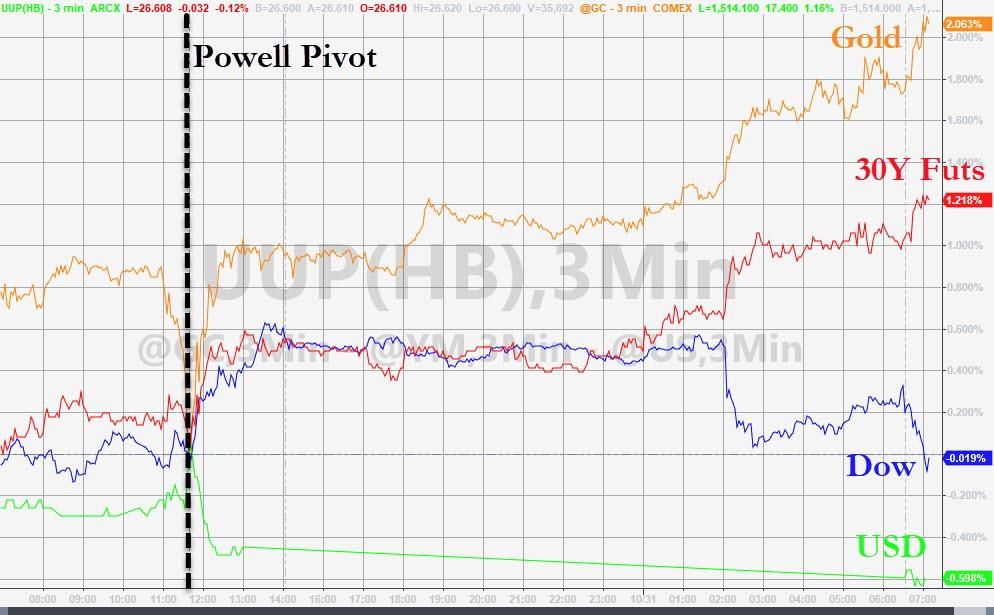

In the expanded D.C. universe yesterday we also had the outcome of the Fed meeting. Against the backdrop of GDP healthily beating expectations at 1.9% q/q annualized, driven by both household and state spending (a figure helpfully mocked by the editor of The Global Times for being far less than China’s “6% growth”), the Fed decided to cut rates 25bp for a third time this year to 1.75%. More importantly, the Fed made clear that this is it: the mid-cycle adjustment that it had absolutely no idea would be necessary back in January this year is now complete and they are on hold. Chairman (Ker)-Powell also added that it would require a major shift upwards in inflation to get them to raise rates again, or for geopolitics to go wrong for them to be forced to cut: otherwise they are done.

As our own D.C. hero Philip Marey makes clear here, we strongly disagree. Our view is that the economic data released in recent weeks have been outright alarming. They point to a sustained and significant contraction in manufacturing, a slowdown in the services sector and a slowdown in employment growth. There was even an unexpected decline in retail sales. As a result, we expect a recession in the second half of 2020 that will force the Fed to cut rates all the way back to zero. Oh, and we does not think the Repo issue is under control either. More to come there too.

Anyway, back to critics/audience arbitrage. In Joker the eponymous madman launches into an angry tirade at the world: “All of you, the system that knows so much, you decide what’s right or wrong. The same way that you decide what’s funny or not.” Given central-bank and central-government shepherding of asset prices, can we really say the same isn’t true if we substitute the word “funny” for “value”?

Where is the value of a bond or a stock if there were no central-bank backstop? Are we about to find out if the Fed are going to sit on their hands, as we don’t think they will? And isn’t it ironic that supervillains and banks end up together in my mind even when there is no bank-robbing going on in a Joker movie that was far more Taxi Driver than Batmobile?

Is that scary enough for you? No? Well how about Treasury Secretary Mnuchin proposing the removal of some of the post-crisis reporting requirements for RMBS to help the markets along? That should raise as many hairs on the back of the neck as it does champagne glasses near term. And want another Halloween scare? On the Brexit front it appears that the Lib Dems have struck an electoral Remain pact with the Green Party and Welsh nationalists and former Tory Dominic “General Grievous” Grieve….and the latest news on the other side is that the Brexit Party is prepared to stand down in Tory marginal seats and only attack key Leave-voting Labour constituencies. If true, that makes Remain the popular equivalent of the D.C. Universe before Wonder Woman vs. Leave’s Marvel Comics Universe ensemble – even if the latter is ironically led by BoJo(ker). Early days, but it looks like a potential power shift towards a strong Leave victory.

Yet Halloween has candy too. As Joker says, “All I have are negative thoughts.” Fortunately not all we have are negative yields – indeed there are a few trillion less today than a few months ago. And we can try to accentuate the positive further: sometimes real value slips through ‘the system’ anyway. As someone quipped regarding Greece issuing debt at negative yields, at least now we openly see those buying Greek bonds won’t be getting all their money back!

This morning also saw an enormous and unexpected surge in Aussie building approvals (up 7.6% m/m vs. flat consensus) as the market once again moves from outright gloom back to bubble territory, at least in Sydney and Melbourne. It’s a choppy series but this underlines: 1) RBA cuts are less likely near term; and 2) Australia has become like the Chinese economy on which it relies. There are fewer and fewer productive business opportunities to invest in, so one either goes all-in on property (when the RBA, APRA, and government give the thumbs up) or one goes all out (when the RBA, APRA, and government give the thumbs down). There is no moderate house-price inflation scenario: it’s dangerous bubble or dangerous bust. Which one do you think the Jokers at the RBA will want to lean towards, via Aussie QE if needed?

We also had China’s manufacturing PMI far weaker than expected at 49.3 and non-manufacturing PMI at 52.8, meaning a composite of 52.0, down from 53.1. So on top of all the other screams today, we can add a slowing Chinese economy.

Dems Hold Thursday Vote On Critical Impeachment Resolution: Here’s What You Need To Know

After weeks of private hearing involving employees from the White House and State Department, the Democrats’ impeachment investigation is about to move into a far more public phase, following what’s likely to be a historic vote on Thursday. The House will call a vote on a resolution setting the rules for public impeachment proceedings. And if the count comes back as expected (that is, straight down party lines), the Dems will prevail, and the next round of hearings (this time, public ones) will be scheduled, according to the New York Times.

The vote also marks the first time that lawmakers will go on the record with their support for the inquiry, or opposition.

Under the proposed rules, President Trump’s legal team would be allowed to present a formal defense of the president during the hearings. And they would have the power to cross-examine witnesses once debate over impeachment begins, and submit proposals calling for additional witnesses.

Sources on Capitol Hill told the NYT, BBG and other media outlets that the resolution would call for a public phase to begin in three weeks. Though it wouldn’t put an end to the private hearings. The public hearings will largely be led by the Intelligence Committee and its Chairman Adam Schiff, one of the leaders of the impeachment inquiry and a favorite target of President Trump.

The resolution also sets the stage for the material gathered during the investigation phase to be turned over to the Judiciary Committee and Chairman Jerrold Nadler, another favorite Trump antagonist, who would hold additional hearings where Trump and/or his lawyers would be allowed to participate. Ultimately, the Judiciary Committee will be responsible for drawing up articles of impeachment.

Though the Dems’ rules allow the president pretty much all of the rights demanded by his legal team, there’s likely to still be squabbling between the Dems and Republicans, particularly over whether to call certain witnesses, like the still-anonymous whistleblower who first filed a complaint about possible quid-pro-quo surrounding the July 25 call between Trump and Ukrainian leader Zelensky.

The White House slammed the Dems’ resolution, saying that it only proved that the investigation had been an “illegitimate sham.” Under the resolution’s rules, said White House Press Secretary Stephanie Grisham, Trump wouldn’t be afforded due process until the proceedings were nearly finished.

Those are pretty much the basics of the resolution. Here’s a guide to what comes next, courtesy of NPR:

Open hearings

The resolution designates House Intelligence Committee Chairman Adam Schiff, D-Calif., as the point person to preside over any public hearings.

“The American people will hear firsthand about the President’s misconduct,” Schiff said in a statement on Monday, but he has not indicated which witnesses he would call.

Schiff and the top Republican on the panel, Devin Nunes, R-Calif., are the two lawmakers who would lead the questioning in hearings — but they can yield to their staff counsels. The bulk of the questioning during closed-door depositions conducted to date has been done by Democratic and Republican committee lawyers.

Republicans can request witnesses to appear at the open hearings and can request that subpoenas be approved, but those need to be approved by the majority.

Democrats have said they would like William Taylor to testify in open session. He is the top U.S. diplomat in Ukraine, and he gave a detailed account of the parallel foreign policy effort led by Rudy Giuliani, the president’s personal attorney, to leverage military assistance for investigations into former Vice President Joe Biden and his son, Hunter.

Committee public report

The resolution directs the Intelligence Committee to issue a report on its findings and recommendations and send the report to the House Judiciary Committee, which will consider any potential articles of impeachment. It also has to be publicly released. The report will be made in consultation with the House Foreign Affairs and Oversight committees — the two other panels that have been participating in the witness interviews so far.

It is also up to Schiff to publicly release any transcripts of closed-door testimony — potentially removing or blocking sensitive information.

Pelosi and most House Democrats have stressed that the current impeachment probe be narrowly focused on the issues around the Ukraine matter. But all the House panels investigating any potential impeachment issues are directed to send their evidence to the Judiciary Committee.

Judiciary hearing on articles of impeachment

The House Judiciary Committee is the panel that has jurisdiction over impeachment proceedings. Once the Intelligence Committee sends its report to the panel, it can begin the process of drafting articles of impeachment.

Top Democrats argue that the president’s alleged push to withhold military assistance for Ukraine — which Congress had already authorized — in order to secure a commitment for an investigation for his own domestic political benefit is grounds for an article of impeachment. But it’s unclear what the specific charge in the article would be.

Articles of impeachment are compared to an indictment, and the standard set forth in the Constitution is broad and at the discretion of the majority: “high crimes and misdemeanors.”

Schiff has made it clear that he does not plan to go to court to enforce subpoenas for testimony and documents from those administration officials who have refused to comply. Instead, he has maintained that those Trump officials “will be building a very powerful case against the president for obstruction — an article of impeachment based on obstruction.”

Judiciary markup and vote on articles of impeachment

The Judiciary Committee released its own procedures on Tuesday for how it will consider any articles of impeachment, separate from the House resolution.

Chairman Jerry Nadler, D-N.Y., said in a written statement that the committee’s process confers “rights for the minority and for the President equal to those provided during the Nixon and Clinton inquiries.”

These include the ability of the president’s lawyers to receive copies of documents and evidence, to attend sessions and hearings when evidence is being presented, to question witnesses and to respond to the Democrats’ arguments.

Republicans have complained that the process allowed for the Judiciary Committee should also be allowed for the open Intelligence Committee hearings.

Full House vote on articles of impeachment

Once the Judiciary Committee completes its hearings and votes on any articles of impeachment, its report would go to the full House for a vote.

There is no timeline for these next steps in the House, but Democratic leaders have indicated that they would like to wrap up the process before the end of the year.

If the House passes the articles and votes to impeach, the process then heads to the Senate. Senate Majority Leader Mitch McConnell has said that if the House approves articles and transmits them to the Senate, he will begin the process of holding a trial and ultimately a vote on whether to acquit or remove the president.

* * *

The vote is expected later in the day on Thursday, exactly when is still unclear. Anybody who wants to read the resolution in its entirety can find the full draft here.

You don’t use up all of your ammunition before the battle even begins.

The U.S. economy has not even officially entered recession territory yet, although many experts are definitely anticipating one in 2020. When that recession arrives, the Federal Reserve is going to want as much ammunition to fight it as possible. So I was horrified to learn that the Federal Reserve announced on Wednesday that interest rates are being slashed once again. We have now had three interest rate cuts in 2019 as the Federal Reserve desperately attempts to revive the stalling U.S. economy. But what are they going to do during the next recession when they have already pushed interest rates all the way to the floor and they can’t push them any lower?

In addition, in recent days the Federal Reserve has decided to absolutely flood the financial system with new money in a desperate attempt to stabilize the repo market. In essence, the Federal Reserve has launched a massive new round of quantitative easing even before a major crisis has erupted on Wall Street. I can understand trying to be proactive, but in reality quantitative easing is an extreme emergency measure that should only be used in the most desperate of situations. If the Fed is creating this much new money now, what are they going to do once things really get bad? Are we destined to become the next Venezuela?

For a long time, the Federal Reserve has insisted that the U.S. economy is in good shape. If that is true, there is no way in the world that the Fed should be cutting interest rates. But that is exactly what happened on Wednesday…

In a vote widely anticipated by financial markets, the central bank’s Federal Open Market Committee lowered its benchmark funds rate by 25 basis points to a range of 1.5% to 1.75%. The rate sets what banks charge each other for overnight lending but is also tied to most forms of revolving consumer debt.

It was the third cut this year as part of what Fed Chairman Jerome Powell has characterized as a “midcycle adjustment” in a maturing economic expansion.

With rates now so close to zero, there isn’t going to be much that the Fed can do in that regard once the next recession strikes.

Powell said lowering the rate again was ‘insurance’, or protection needed because ‘weakness in global growth and trade developments have weighed on the economy and posed ongoing risks’.

If the U.S. economy doesn’t plunge into a deep recession next year, Powell and the other bureaucrats at the Fed will probably be applauded for these moves.

But if we do experience a significant economic downturn, they will be caught with their pants down.

1.9 percent is not good at all, and if honest numbers were being used it would show that our economy is actually contracting. But at least things are relatively stable for the moment, and as long as things are relatively stable the Federal Reserve should not be resorting to emergency measures.

Of course Wall Street was absolutely thrilled that the Fed cut rates again, and news of the rate cut pushed the S&P 500 to yet another all-time record high…

Stocks advanced Wednesday after the Federal Reserve cut interest rates for the third time this year, propelling the Standard & Poor’s 500 to a fresh record.

The S&P 500 index added 9.88 points, or 0.3%, to close at 3046.77. The Dow Jones industrial average climbed 115.27 points, or 0.4%, to end at 27,186.69. The Nasdaq added 27.12 points, or 0.3%, at 8,303.98.

And without a doubt, this rate cut is good for consumers. Rates on mortgages, auto loans and credit cards will go down, and that will save average Americans a lot of money…

These Fed interest rate cuts are starting to add up, lowering costs for many Americans who use credit cards or take out loans while squeezing savers.

The Federal Reserve lowered its benchmark interest rate Wednesday by a quarter percentage point for the third time in the past three months. The move is likely to further trim borrowing costs on credit cards, home equity lines, adjustable-rate mortgages and auto loans.

But this is yet another example of the short-term thinking that is plaguing our society.

When the next recession arrives, the Fed will be able to cut rates a handful of times, and then that will be the end of it.

The Fed should have also held off on buying more bonds until we really needed it as well. Even though a new financial crisis has not even started yet, the Fed has been creating money like crazy and their balance sheet has ballooned “by about $100 billion over the past month”…

The Fed has been buying bonds again, but officials insist it is an effort to stabilize the funds rate within the target range rather than a resurrection of QE. Still, the central bank balance sheet has expanded by about $100 billion over the past month and is back above the $4 trillion mark, $3.6 trillion of which is in Treasurys and mortage-backed securities.

So if the Fed is being this crazy now, what are they going to do when a real financial crisis erupts?

Perhaps they should just get it over with and create trillions of dollars right now and turn us into the Weimar Republic already.

Because that is where all of this craziness is eventually going to take us. Our dollar is eventually going to be absolutely worthless and we will become the next Venezuela.

I have always been highly critical of the Federal Reserve, but at least in other eras those running the Fed were at least mildly competent.

But now it appears that incompetence is running wild over at the Federal Reserve, and we will all pay a great price for their mistakes in the not too distant future.

Kudlow Tries To Rescue Markets After China Spoiled The Party

Dow futures were down a horrifying 90 points this morning, erasing all of Powell’s pumpathon after China poured cold water on US-China trade talks. So what does the administration do – to rescue stocks from a terrifying 0.3$ drop?

Unleashes The Kudlow:

*KUDLOW SAYS U.S.-CHINA TALKS GOING SMOOTHLY: WHITE HOUSE AIDE

And the result, reflexive buying by algos…

But it seems like the White House’s jawboning is losing its mojo.

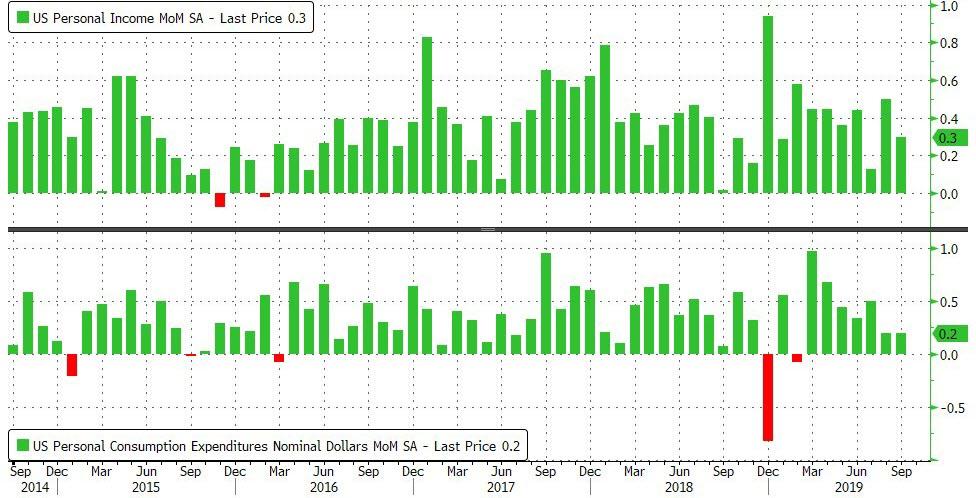

US Incomes, Spending Accelerated In September As Fed’s Favorite Inflation Signal Slowed

After August’s slowdown in annual growth for spending and income, analysts forecast a modest rebound in September but the data disappointed with personal income up 0.3% MoM (in line with expectations) but spending rose just 0.2% MoM (below the +0.3% MoM expected).

Source: Bloomberg

On a Year-over-year basis, both incomes and spending growth accelerated…

Source: Bloomberg

And one of The Fed’s most-watched inflation signals – core PCE deflator – slowed YoY, as real personal spending began to re-accelerate…