Saturday’s event was the “largest-ever” food giveaway as described by NTFB. As shown below, aerial photos reveal vehicle lines stretched miles down the street.

Samantha Woods, a Dallas, Texas resident who was waiting in line, told CBS, “I see blessings coming to us cause we all struggling. And I appreciate North Texas helping us out.”

Cynthia Culter, another Dallas resident, said, “I haven’t been working since December, can’t find a job, they cut my unemployment, it’s a real big deal.”

NTFB spokeswoman Anna Kurian told CNN that “forty percent of the folks coming through our partners’ doors are doing so for the first time.”

NTFB President Trisha Cunningham said she is proud of her team “for providing some hope and care during these extraordinary times.”

“It was quite a humbling scene to see so many in need,” Cunningham told CNN.

Internet searches for “drive thru food bank near me” is absolutely erupting.

While the virus-induced downturn may be over for the rich, as stocks and real estate prices catapult higher, working-poor folks have been financially ruined in the last eight-month.

Huge demand for food banks nationwide could result in a “meal shortage” within the next 12 months.

via ZeroHedge News https://ift.tt/35GGmC6 Tyler Durden

Study Warns That New Work-From-Home Trend is Making People More “Racist” Tyler Durden

Wed, 11/18/2020 – 09:25

Authored by Paul Joseph Watson via Summit News,

A new study being promoted by the mass media claims that working from home makes people more “racist” because they are less exposed to ‘diversity’ in the workplace.

The survey, conducted by polling company Survation for the Woolf Institute, “warns that without alternative settings to offices being set up, opportunities for social mixing between different religious and ethnic groups will be greatly reduced,” according to the BBC.

76 percent of those who work in shared offices in the UK are exposed to ethnic diversity, meaning those who work from home are isolated from such a setting and as a result more likely to be “prejudiced,” according to the study.

37 percent of unemployed people are also more likely to only have friends from their own ethnic group.

With huge numbers of people now working from home due to coronavirus restrictions, 44 percent of the workforce in the UK, this presents a conundrum for technocrats overseeing a “Great Reset” that seeks to restructure capitalism.

“Academia, long removed from scientific breakthrough and existential exploration, has seemingly become an industry dedicated to the relentless pursuit of racism, wherever it may dwell,” writes Graham Dockery.

“The Woolf Institute studies relations between faiths and ethnicities in the UK, and wouldn’t exist if it couldn’t root out ever more bizarre instances of prejudice to publicize.”

Interestingly enough, the study also concedes that people who live in more diverse communities were “more likely to be negative towards ethnic diversity.”

In other words, people who are actually exposed to ‘diversity’ don’t find it to be a “strength” and don’t like it.

This correlates with a 2019 peer reviewed study by Danish academics which found that ethnic diversity has a negative impact on communities because it erodes trust.

Seeking to answer whether “continued immigration and corresponding growing ethnic diversity” was having a positive impact on community cohesion, the study found the opposite to be the case.

So diversity really isn’t a strength after all, but our new technocratic overlords are going to force you to embrace it anyway.

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. I need you to sign up for my free newsletter here. Also, I urgently need your financial support here.

via ZeroHedge News https://ift.tt/2UAfiyl Tyler Durden

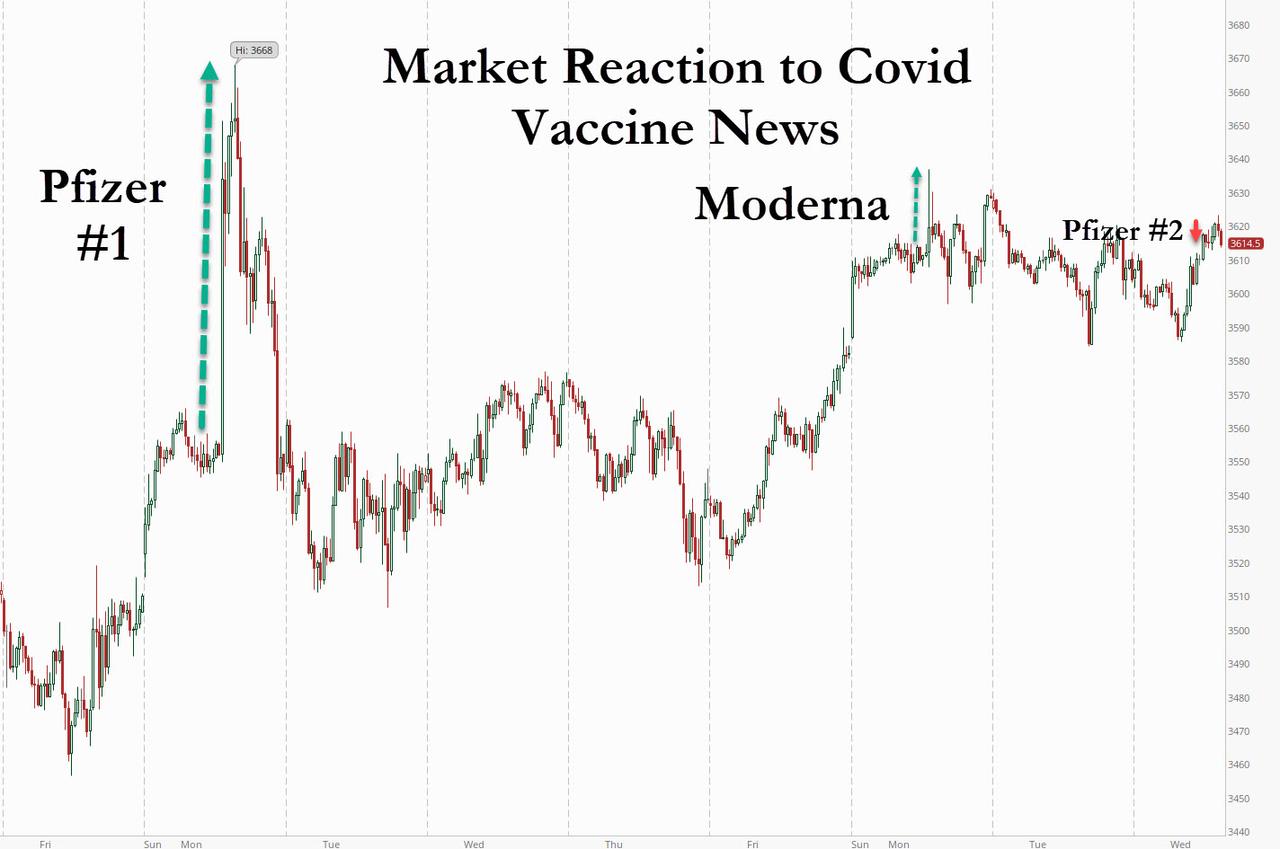

Is All The “COVID Vaccine Good News” Priced In? Tyler Durden

Wed, 11/18/2020 – 09:06

In discussing yesterday’s market action, overnight Rabobank’s Head of Macro Strategy Elwin de Groot, writes that following the vaccine-inspired rally, “the market seems to have reached a delicate balance now where on the one hand, many investors are willing to long beyond the temporary resurgence of the virus as there is ‘light at the end of the tunnel’, whilst others remain concerned that the upcoming months could still prove rather challenging. This balance was well-illustrated by the performance in the S&P 500 yesterday, where the market opened lower, then regained almost fully the opening losses but then slipped again towards the end of the trading session. Yes, with the S&P only a whisker from its all-time high it is obviously ‘risk-on’, but somehow if feels different.“

This point was on full display this morning when in the third consecutive good vaccine news released since Pfizer’s covid news last Monday, in which the company followed up with an increased effectiveness estimate (from 90% to 95%) which should make the company’s application for emergency US authorization be accepted smoothly, the stock response was lukewarm at best, with futures now having faded the entire post-update spike higher.

This same point was touched upon by Bloomberg’s market live blog, which points out that “the shock value from incremental progress on Pfizer’s vaccine is understandably less than last week’s initial announcement, and it seems reasonable to expect that the ultimate market impact today will be relatively limited. After all, views are already coalescing around the idea that a vaccine will be fairly widely available by next spring, so in a sense the capacity to surprise has started tilting towards bad news on that front.”

That said, and as we have warned repeatedly in recent months, a vaccine is one thing, widespread adoption – especially in a country where just 46% of Americans said they will be willing to take the first available vaccine without observing side effects first – is something entirely different. Here’s Bloomberg on this transition to actual implementation of the vaccine:

This being said, it is reasonable to think that a prospective return to normalcy has not yet been fully priced, particularly in the spreads that I have talked about in recent weeks — stuff like the Russell versus the NDX, etc. Moreover, I suspect at this juncture the public is going to be as interested in the safety aspect of a vaccine as its effectiveness; a straw poll of some friends suggested quite a bit of variance in the enthusiasm to be front-of-the-queue to get inoculated. As such, it’s nice to see headlines referring to the safety aspect of the Pfizer drug, though the CEO hinted as much at a conference yesterday.

This may explain why the market is now shrugging off any incremental vaccine – with both stocks and yields below pre-announcement levels – and why any incremental move higher in stocks will now be contingent on a credible plan of just how these multiple vaccines are actually administered to a skeptical population.

via ZeroHedge News https://ift.tt/32V5SSA Tyler Durden

US Sees Most COVID Deaths Since Spring, FDA Approves Rapid Home Test: Live Updates Tyler Durden

Wed, 11/18/2020 – 08:50

Summary:

US suffers most new deaths in months

Pfizer vaccine now 95% effective

Lucira home test approved

FDA panel to meet next month to discuss vaccines

Tokyo sees record jump in cases

PA orders new restrictions

India outbreak continues to weaken

LA County prepares new curfew orders

Sinovac appears to be safe per trial data

* * *

The biggest COVID-19 related news on Wednesday is the release of the final data from the Pfizer-BioNTech vaccine trial, which showed the vaccine to be 95% effective, on par with Moderna’s mRNA vaccine results, which were released earlier in the week. While we await Moderna’s “final” data showing its vaccine to be 96% effective, it’s worth noting that this wasn’t the only new development in the battle against the virus.

Following the announcement, it was reported that a critical FDA panel will meet on Dec. 8 to discuss the first wave of COVID-19 vaccines, raising the possibility that the first general-use approvals might come around then, or shortly after.

Lucira’s rapid home test for the virus was just approved for emergency use by the FDA on Wednesday, granting a powerful new tool that can allow exposed persons to text themselves without potentially putting others at risk. The test is the first that can be fully self-administered, and it can provide results at home in 30 minutes or less. The approval comes at a time when the US is reporting an average of 150,000 new coronavirus cases per day.

“This new testing option is an important diagnostic advancement to address the pandemic and reduce the public burden of disease transmission,” said FDA Commissioner Stephen Hahn in the statement.

In other news, after announcing early Wednesday (local time) that Tokyo would be placed on the highest new alert level to stop the spread of the virus, daily coronavirus cases in Tokyo hit a new record of 493 on Wednesday, topping the previous record of 472 set on Aug. 1.

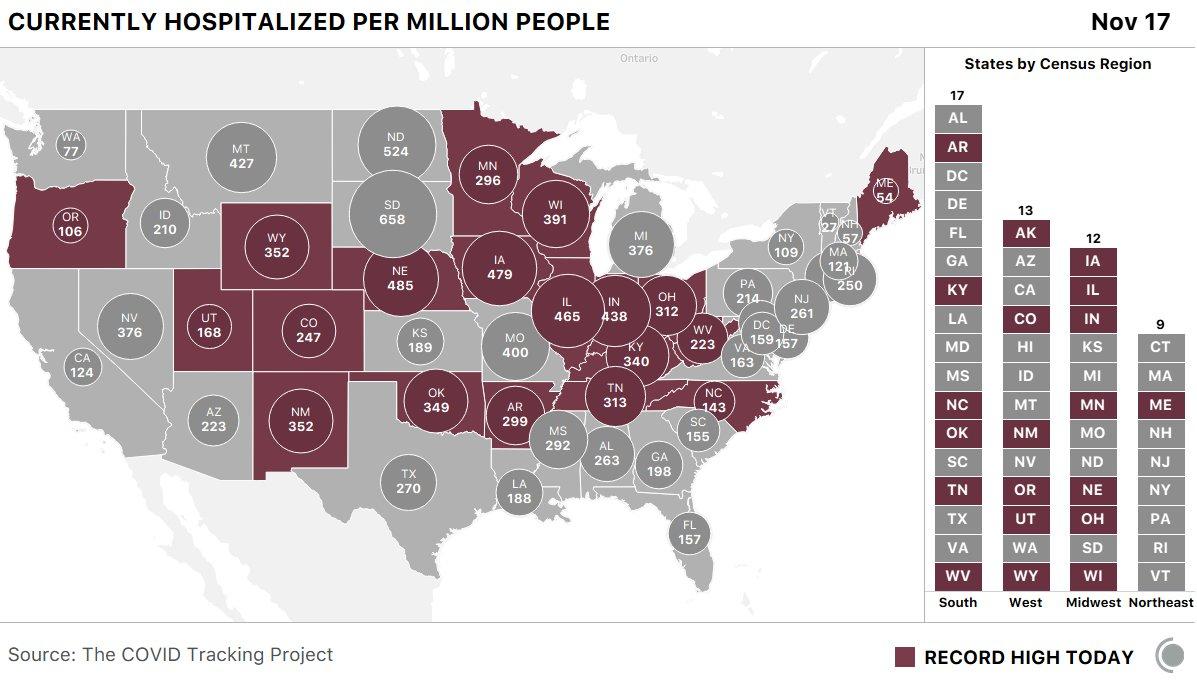

Across the US, 20 states are seeing hospitalizations reach peak levels.

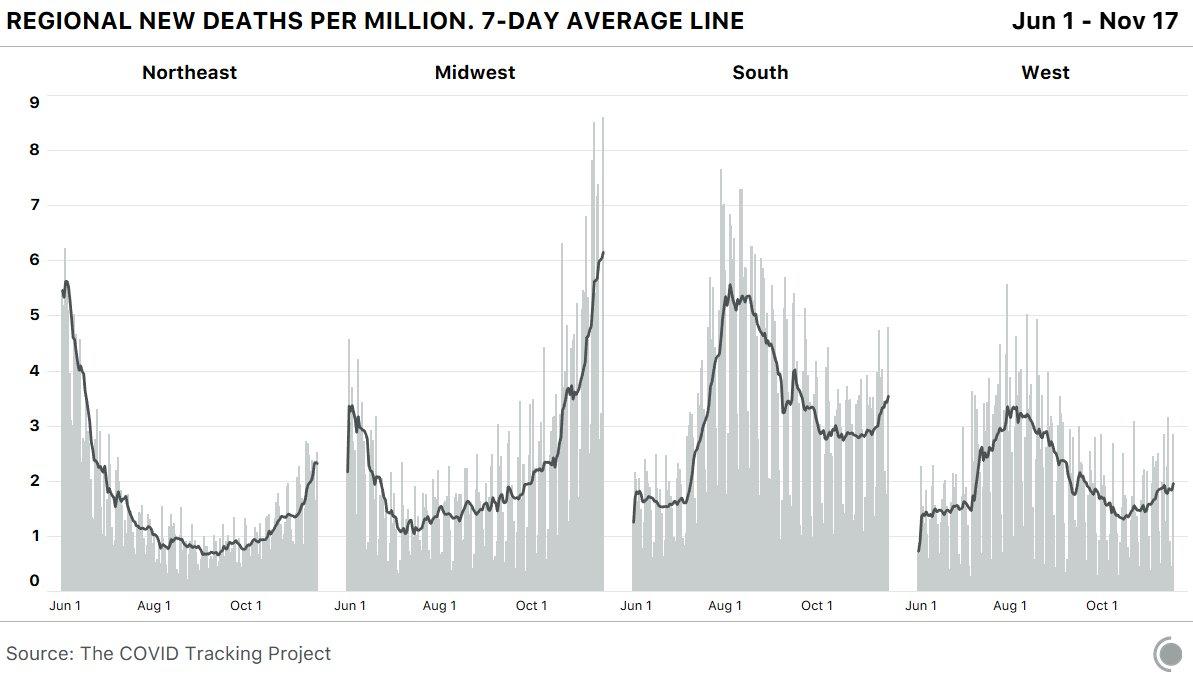

Deaths are surging higher in the Midwest to new record levels, though they’re also rising in other regions as well. The US reported more than 1,550 new deaths yesterday, its largest daily tally since the spring.

Here’s more COVID news from Wednesday morning and overnight:

Yesterday, Pennsylvania’s Secretary of Health announced new targeted efforts to slow the spread of the virus in the state, including strengthening a mandatory mask order, along with a new mandate for those traveling to PA from out of state (Source: WGAL).

Following this morning’s Pfizer news, the Indian government is reportedly in talks with Pfizer and Moderna for COVID-19 vaccine.

Los Angeles County plans to implement a curfew from 2200-0600 beginning on Friday night and restaurants with outdoor dining, breweries and wineries will be reduced to 50% capacity (Source: Newswires).

The US isn’t the only country with some helpful vaccine news: Sinovac’s vaccine CORONAVAC appeared to be safe and well tolerated at all doses according to Phase 1/2 study, while phase 3 will be crucial to determine the immune response according to researchers. Researchers also stated the vaccine is suitable for emergency use during the pandemic and noted that antibody levels induced by the vaccine were lower than those seen in people that have recovered from the virus.

Tokyo is preparing to raise its coronavirus infection alert status to the highest of level 4. Elsewhere, South Australia’s Premier announced mobility restrictions amid the ongoing outbreak in the state with all schools, universities, takeaway food, pubs and cafes to be shut for 6 days. (Source: Nikkei).

India reports 38,617 new cases, up from 29,163 the previous day, bringing the total to 8.91 million. The death toll jumped by 474 to 130,993 (Source: Nikkei).

South Australia Premier Steven Marshall announced a six-day lockdown to stamp out an outbreak that has now expanded to 22 new cases, warning that the strain of coronavirus detected was especially worrying.

via ZeroHedge News https://ift.tt/3fmPpf3 Tyler Durden

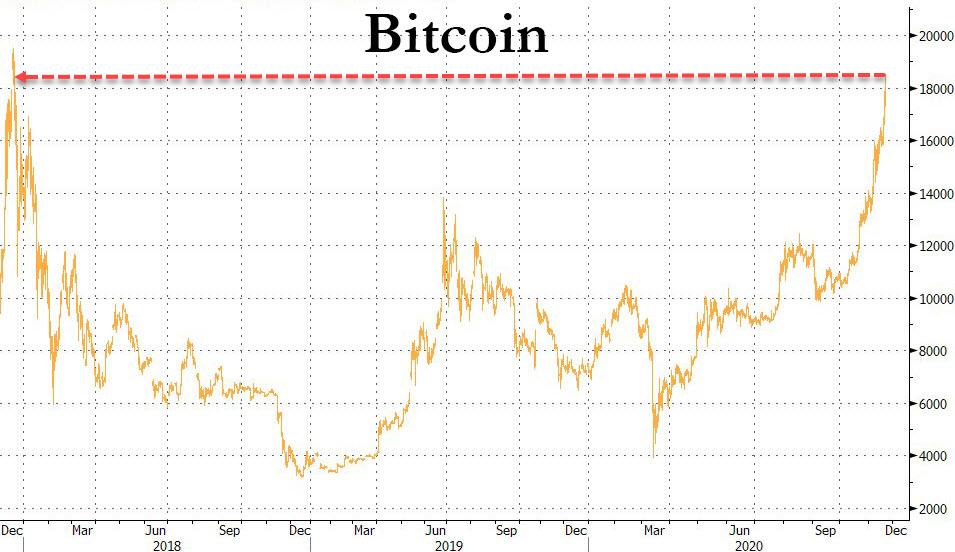

Dalio Admits “I Might Be Missing Something” As Bitcoin Surges Above $18,000 Tyler Durden

Wed, 11/18/2020 – 08:45

Since the US election, Bitcoin prices (in USD) have surged a stunning 40%, also lurching higher after each vaccine headline hit.

Source: Bloomberg

Getting ever closer to its all-time record high…

Source: Bloomberg

As crypto prices soared overnight, Bridgewater Associates founder Ray Dalio stepped back into the fray, saying in a Twitter thread that “I might be missing something about Bitcoin so I’d love to be corrected.”

… My problems with Bitcoin being an effective currency are simple. They are that:

1) Bitcoin is not very good as a medium of exchange because you can buy much with it (I presume that’s because it’s too volatile for most merchants to use, but correct me if I’m wrong)…

2) it’s not very good as a store-hold of wealth because it’s volatility is great and has little correlation with the prices of what I need to buy so owning it doesn’t protect my buying power, and…

3) if it becomes successful enough to compete and be threatening enough to currencies that governments control, the governments will outlaw it and make it too dangerous to use.

Also, unlike gold which is the third highest reserve assets that central banks own, I can’t imagine central banks, big Institutional investors, businesses or multinational companies using it. If I’m wrong about these things I would love to be corrected. Thank you.

This comes after Dalio’s comments last week that “I don’t think digital currencies will succeed in the way people hope they would,” citing those three main problems with bitcoin and other cryptocurrencies that will limit their future.

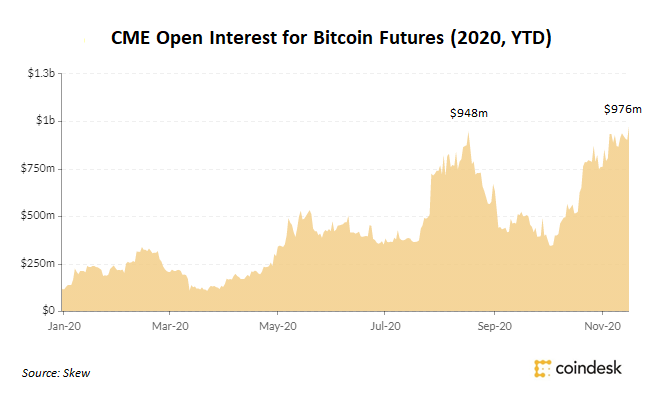

Dalio’s skepticism did not make it as far as Chicago whereopen interest for bitcoin futures traded on CME Group’s exchange has reached record highs of $976 million amid a surge of institutional capital inflows to the leading cryptocurrency and its derivative markets.

Hollywood is also chiming in with Game of Thrones actress Maisie Williams asked “Should I go long Bitcoin?”

I bought more $BTC last night at 15800. It’s going to 20k and the. To 65 k. The network effect has taken over. I see tons of new buyers and there is very little supply. It’s an easier trade here that at 11k. So YES, buy it.

Finally, we note that Bitcoin’s recent surge has pushed its market cap to a record high above $336 billion, outstripping the market cap of Nvidia — one of the world’s most well-known manufacturers of graphics cards (that incidentally are often used to mine cryptocurrencies).

via ZeroHedge News https://ift.tt/35HoerP Tyler Durden

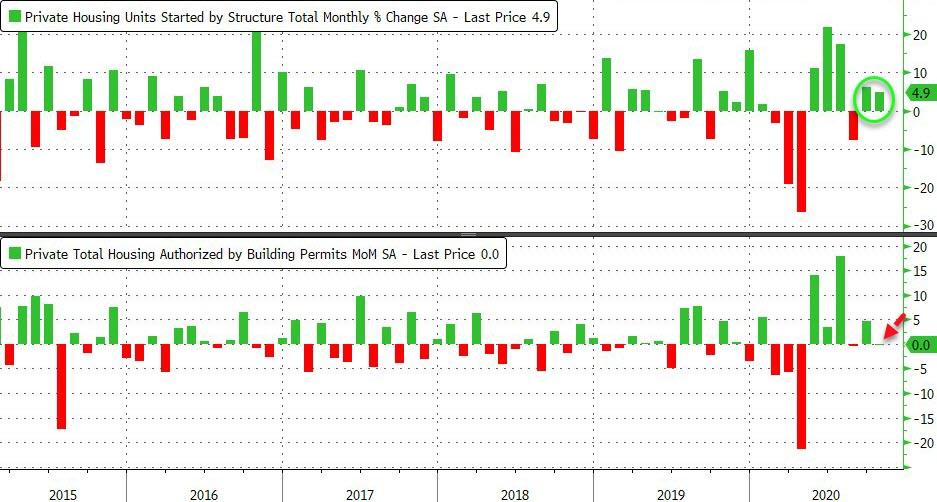

US Housing Market Stumble? Home Starts Rise But Rental Unit Permits Plunge In October Tyler Durden

Wed, 11/18/2020 – 08:40

With the US housing bubble reinflating, ‘expert’ analysts expected building starts and permits to continues their meteoric rise in October. However, the results were mixed.

Housing Starts beat expectations, rising 4.9% MoM (well above the 3.2% expectation) and also saw a major upward revision in September, from +1.9% MoM to +6.3% MoM.

Building Permits disappointed, unchanged in October versus expectations of a 1.4% rise MoM.

Source: Bloomberg

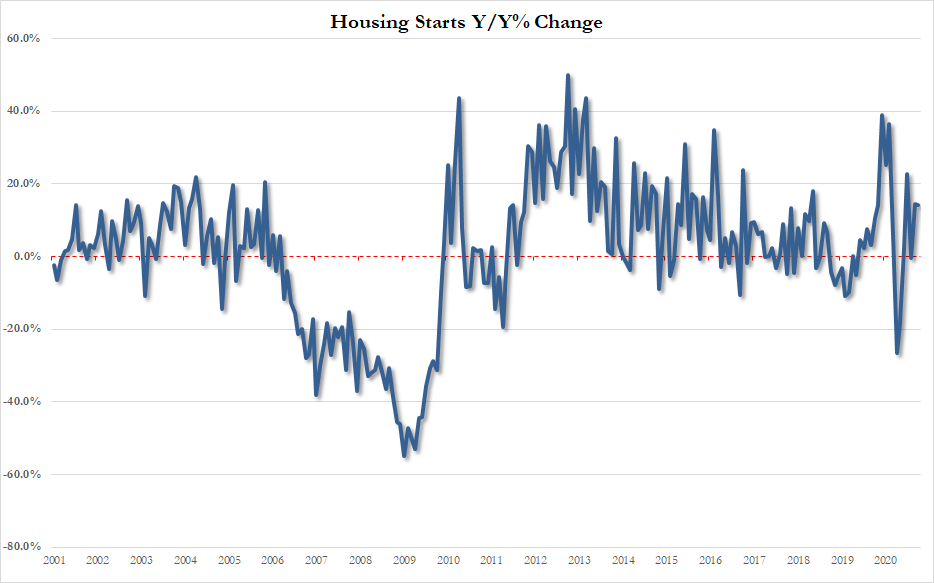

Overall Housing Starts are up significantly in 2020…

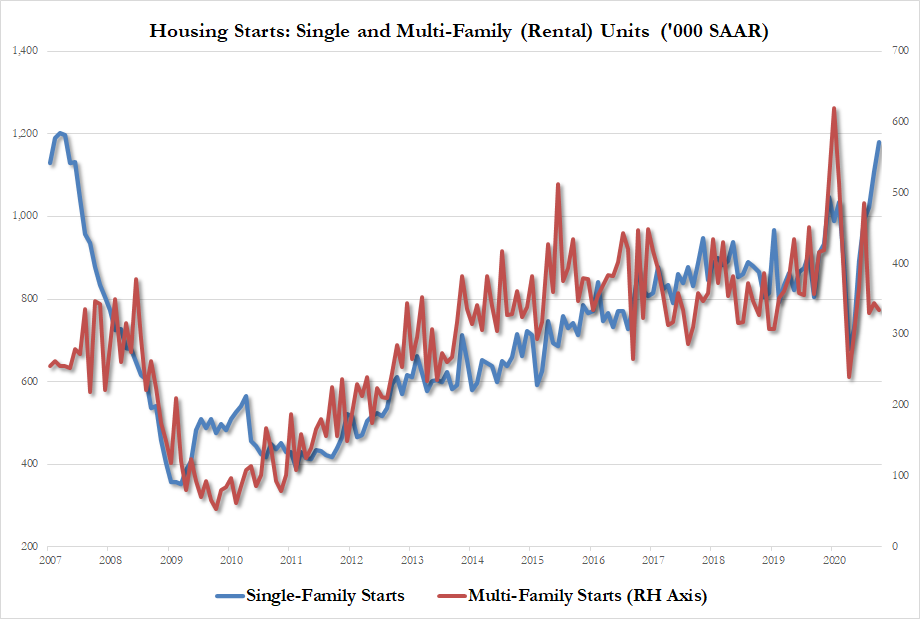

Single Family Starts surging to at 1.179MM, up 6.4% M/M, up 29.4% Y/Y, and highest since 2007 as multi-family starts remained flat (and notably lower than pre-COVID)…

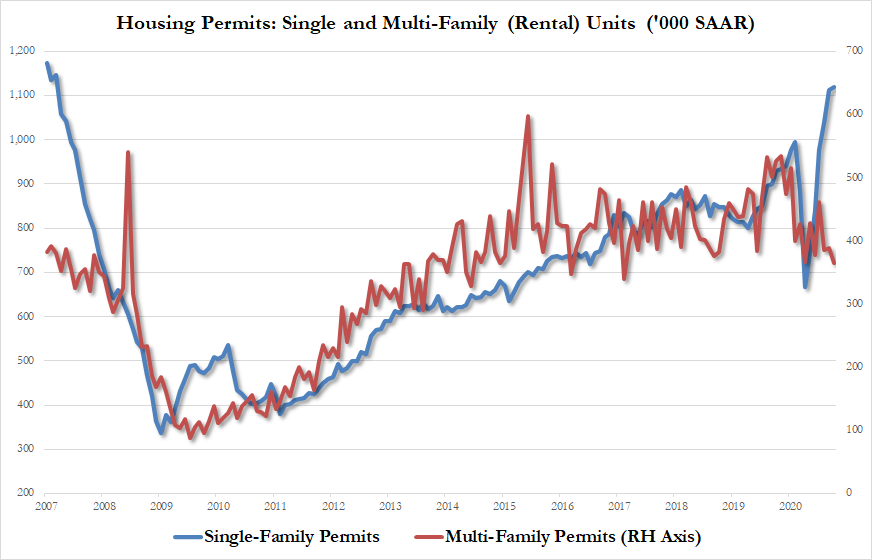

On the more forward-looking permits side, the picture was similar with multi-family (rental) units tumbling to 365K, down 5.9% M/M, down 30.6% Y/Y, and lowest since Feb 2017…

With NAHB sentiment at record highs, one wonders why homebuilders are not loading up on the forward-looking building permits?

…if we build it, they will come?

via ZeroHedge News https://ift.tt/38V7mQu Tyler Durden

In The Biggest App Store Overhaul Since 2008, Apple Cuts Fees For Most Developers By 15% Tyler Durden

Wed, 11/18/2020 – 08:19

In the biggest change to the Apple store’s revenue structure since the iPhone maker launched the service in 2008, and one which could have an adverse impact on its Services revenue at least over the short-term, Apple announced it would cut by half the fees charged to most developers who sell software and services on the App Store. Apple’s standard 30% fee will remain for developers that generate more than $1 million in a calendar year.

Since the beginning of the App Store, Apple generally has charged developers a 30% slice of revenue generated by their apps. In 2016, Apple lowered to 15% the cut it takes from subscriptions purchased through the apps for more than a year. Earlier this year, Apple also loosened restrictions on some cloud-gaming apps and email services, charging a fee to fewer developers.

The company is lowering the App Store fee to 15% from 30% for developers who produce as much as $1 million in annual revenue from their apps and those who are new to the store. The changes kick in Jan. 1 as part of an App Store Small Business Program, the world’s largest company said Wednesday in a statement. The company said the new structure will apply to the “vast majority” of developers who charge for apps and in-app purchases on Apple’s devices. The program won’t affect some major apps such as those from Netflix and Spotify Technology.

Apple said it’s making the change to help small developers financially and to provide a way for them to invest in their businesses amid the economic struggles caused by the Covid-19 pandemic.

“We’re launching this program to help small business owners write the next chapter of creativity and prosperity on the App Store, and to build the kind of quality apps our customers love,” Cook said in a statement. “The App Store has been an engine of economic growth like none other, creating millions of new jobs and a pathway to entrepreneurship accessible to anyone with a great idea.”

The company said that if a developer made $1 million or less in 2020, the fee will drop to 15% in 2021 until they reach the $1 million mark. If a developer doesn’t reach $1 million in revenue in 2021, they will retain that discount in 2022. If a developer tops $1 million in revenue in a calendar year, they won’t be eligible again for the 15% split until their revenue falls to less than $1 million for a full calendar year.

The change will take place across App Stores on the iPhone, iPad, Mac, Apple TV and Apple Watch. The company has said that 85% of apps found on the App Store are free and aren’t part of the revenue fee system.

The change comes as a result of ongoing scrutiny from government regulators and criticism from developers about the percentage of revenue Apple takes for App Store purchases. The company has also been engaged in a lawsuit with Epic Games, the maker of the video game Fortnite, over its App Store fees and payment rules. Alphabet’s Google also charges similar fees to developers on its Android app store. U.S. Justice Department lawyers have probed the rules that govern Apple’s App Store, and at least one developer was asked about the 30% fee. Spotify also has complained about the fees to the European Union’s antitrust agency.

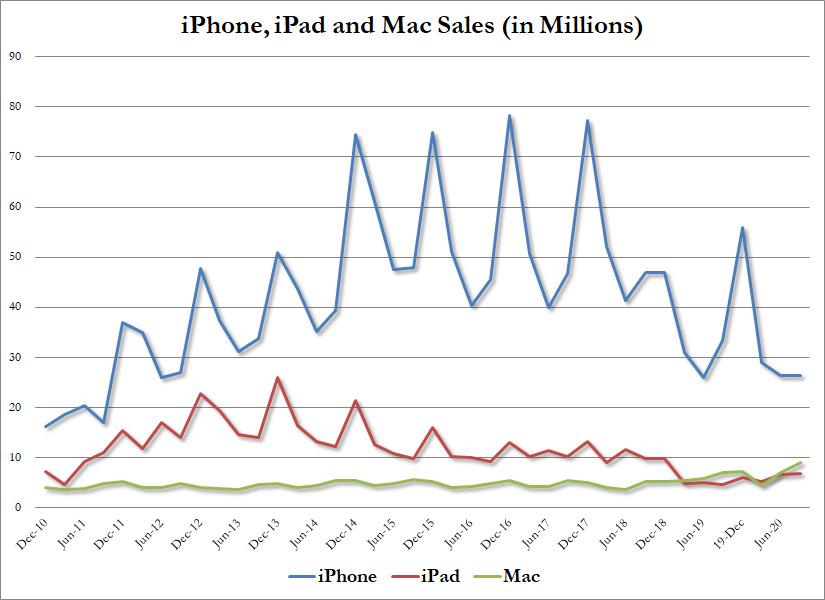

With iPhone sales having peaked in 2016/2017…

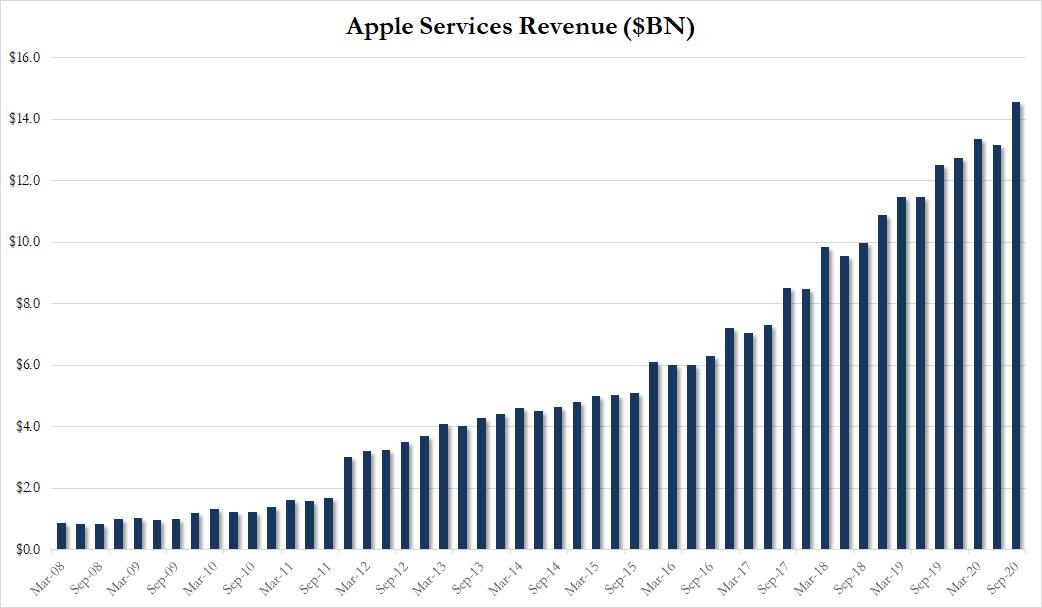

… income from app developers has been key to Apple’s growing services business, which reached almost $54 billion in revenue in fiscal 2020.

Quoted by Bloomberg, Toni Sacconaghi, an analyst at Sanford C Bernstein, said that the App Store is one of several products and offerings that make up the services unit, but is the biggest revenue driver. He estimates the App Store alone will bring in $18.7 billion in 2021, about a third of Apple’s total services revenue next year.

According to Apple, there are 1.8 million apps in the App Store across all of the company’s platforms and more than 28 million registered developers. The company said earlier this year the store has generated $155 billion for developers since it started.

Chief Executive Officer Tim Cook testified about the company’s App Store practices at a July hearing before U.S. lawmakers. In advance of Cook’s appearance, Apple published a study that claimed its 30% cut is normal for the industry or lower than some app stores.

Small developers make up the majority of App Store sellers. Some major apps, such as those offered by Netflix and Spotify, don’t let subscribers sign up through the App Store, avoiding the 30% charge. Apple’s new fee program reductions won’t lure those subscriptions back because the popular apps generate far more than $1 million annually.

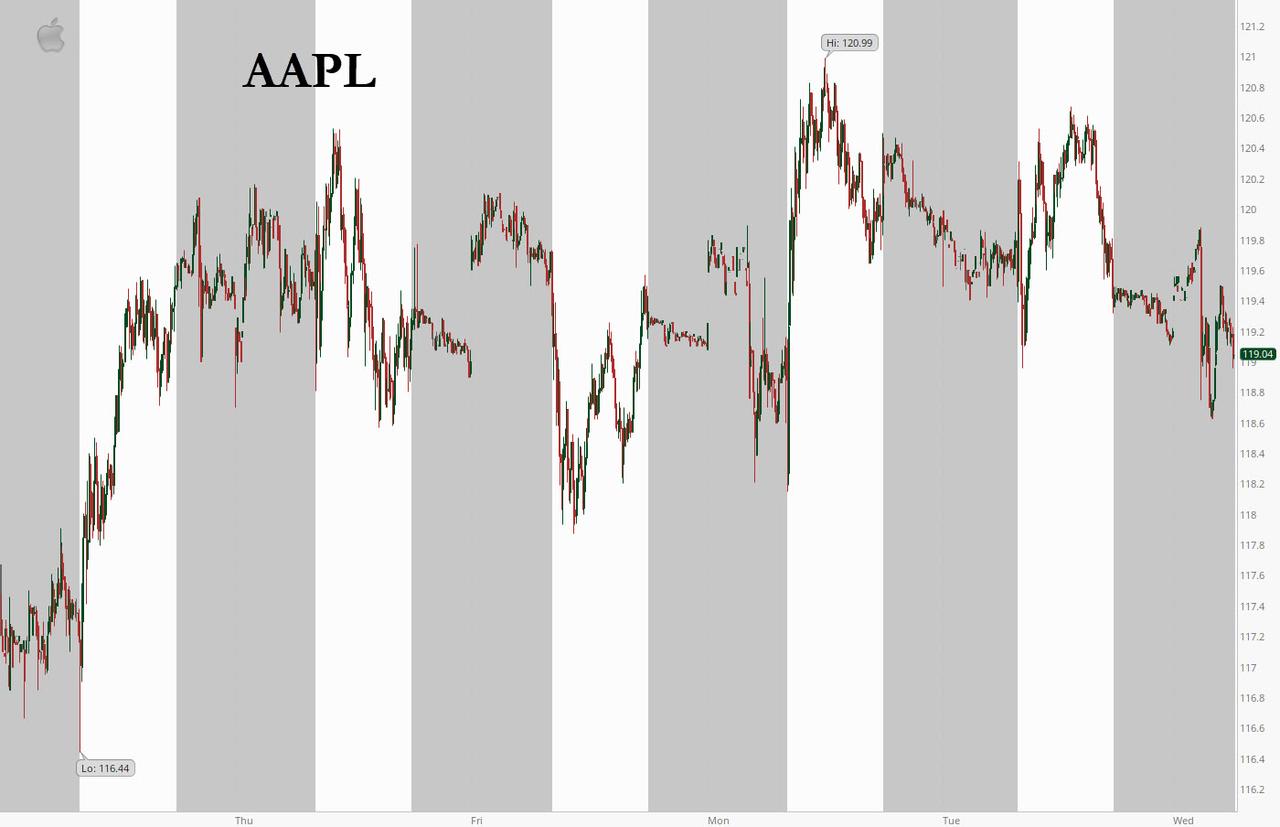

While the price cut will have an adverse near-term impact on Service revenue, Apple is betting that the fee change will result in developers creating more apps and sticking with the App Store, which will create enough new revenue to offset any potential financial negatives from the fee reductions. AAPL stock remains unsure what the outcome is, and after an initial kneejerk move lower, it has stabilized near Tuesday’s closing price.

via ZeroHedge News https://ift.tt/3fcEV1B Tyler Durden

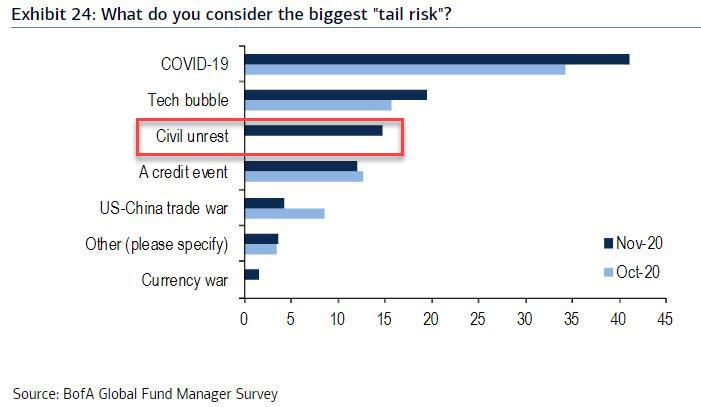

The most bullish Fund Manager Survey (FMS) of 2020 on the back of vaccine, election, macro; Nov FMS shows a big drop in cash, 20-year high in GDP expectations, big jump in equity, small cap & EM exposure; reopening rotation can continue in Q4 but we say “sell the vaccine” in coming weeks/months as we think we’re close to “full bull”.

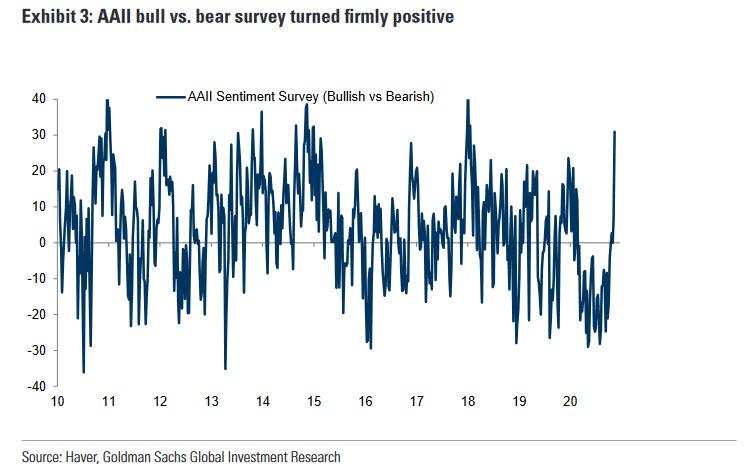

Yet while there were several other observations in the survey (the full report can be found here), all of which confirmed what we had previously seen in the latest AAII survey, namely that virtually every trader is now super bullish…

… what caught our attention was not among the list of euphoric superlatives, but was hidden deep inside the risk factors.

We are referring to what the survey respondents defined as the biggest threat: while at the top, for the 8th consecutive month, covid was seen as the biggest “tail risk”…

… what we found remarkable is that after “tech bubble” in 2nd place in the list of biggest tail risks, “Civil Unrest” suddenly popped into 3rd place, after not being cited as a notable risk in any of the previous BofA surveys.

So what’s going on here, is Wall Street really starting to worry about what we first said back in 2010 – much to Time Magazine’s mockery – that the Fed’s disastrous policies would eventually push US society to armed conflict and/or to civil war. While it may be easy to dismiss such fears as hyperbolic, consider what otherwise level-headed Bloomberg macro commentator (and former Lehman trader) Mark Cudmore wrote overnight in his latest lament that markets are so broken, that in the end it will all “end in tears”, either in the form of collapse of fiat currency or through “political revolution”, read armed conflict.

Which brings us back to square one. Because in a world where a handful of traders are the most bullish they have been in 20 years while the living standards of tens of millions of Americans are absolutely dismal with the economy on the verge of yet another depression-causing shutdown, the flashbacks to the days just before the French Revolution are all too real.

We leave you with Cudmore’s full dystopian comment on what comes next:

A Post-Truth World Is Easy Money for Some Investors: Macro View

It has paid off this year to just enjoy the forest rather than study the trees. More than ever before, markets are rewarding investors who have the ability to embrace a strong narrative over those who focus on analysis and details.

I have rarely experienced such a large gap between my confidence in the future of the largest market drivers and my lack of conviction in where the risk-reward trades lie. There’s a large cohort of the market suffering from the same dilemma but many others are thriving.

The winners are the people smart enough to recognize the reinvigorated power of an old market adage: “Don’t fight the Fed.” The influence of central banks is now pervasive in all markets — not just bonds, credit and stocks, but also cryptocurrencies and art.

Ironically, the incredible impact of central bank policies stems from their powerlessness to achieve a narrow mandate. With limited success in boosting inflation in the face of a global pandemic, they have resorted to fueling the only price gains they can guarantee: financial assets and investments.

Since March, Bloomberg’s Markets Live team has joked internally that the answer to any question is “Buy stonks!” (the typo an intentional reference to the “hodl” meme that successfully encapsulated a similarly unsophisticated winning strategy in crypto) and that any negative news is just a “dip-buying opportunity” in this post-truth world.

These comments were most often thrown out by the cynics on the team, but it’s the wise minority who realized their power. A month ago I highlighted that risk-reward analysis has become reward-analysis and yet I’ve struggled to embrace this new era myself.

I too often delve into whether a narrative has become over-priced in an asset class, when such an approach should now only be applied to a small subset of negative stories. For positive ones, there’s no such reason to question their longevity, as they will naturally morph into a fresh bullish narrative — one with different protagonists but a similar outcome, just like in The Neverending Story.

So where do we stand? Interest rates will stay low for a long time to come; any violent market selloff will be dealt with by extraordinary policy steps; the virus will ultimately be contained but not until after many more fatalities, lost livelihoods and corporate bankruptcies; e-commerce, telecommuting and cashless transactions have seen a permanent boost; the inequality gap grows ever larger and the political frustrations ever deeper.

What does that mean for investors? No idea! Well, that’s not true. Deep down I think we all know what this means but some are better at embracing this paradigm wholeheartedly.

The path will be volatile but selloffs are indeed dip-buying opportunities. It will end in tears at some point, maybe through political revolution or perhaps the collapse of fiat currency, but that time could be many years away and shouldn’t influence how you operate today.

To quote Charles Prince, the CEO of Citigroup until the eve of the financial crisis: “When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance.”

Sure, he soon resigned and was asked to testify before Congress about the millions of dollars in exit pay he received after the bank lost billions on subprime mortgages. But his words bring to mind this year’s winners who can dance in the forest without noticing the trees.

via ZeroHedge News https://ift.tt/2IKZO83 Tyler Durden

After yesterday’s modest selloff as covid optimism fizzled amid fresh daily record numbers of new cases, on Wednesday futures contracts on three major U.S. equities indexes rebounded sharply as vaccine optimism made a triumphal comeback after Pfizer Inc. said a final analysis of clinical-trial data showed its Covid-19 vaccine was 95% effective, paving the way for the company to apply for the first U.S. regulatory authorization for a coronavirus shot within days. The news propelled S&P 500 futures as much as 0.4% higher, erasing earlier decline of as much as 0.6% as the reflation trade appeared back in vogue, while futures on the Nasdaq 100 and Dow Jones rose 0.2% and 0.5%, respectively, as of 7am ET, while Russell 2000 index futures rose 0.6% as the small cap outperformance was set to continue.

Propping up the Dow was Boeing, which announced the crash-prone 737-MAX was cleared to returned to the skies as the FAA lifted its longest-ever US grounding.

The gains helped reverse Tuesday’s drop when US markets closed in the red after soft U.S. retail sales data, a rise in COVID-19 cases and uncertainty over fresh stimulus measures in the world’s largest economy had sapped sentiment. While the release of two successful coronavirus vaccine trial data over the last week had buoyed markets, the still-high infection rate globally had acted to trim gains, said Jane Shoemake, London-based fund manager at Janus Henderson.

“People can see light at the end of the tunnel now and the markets clearly responded to that, but it’s not going to go up in a straight line because we’ve still got to get through the winter… (and) that is going to continue to temper some of the exuberance people feel”, Shoemake said.

Cormac Weldon, Head of U.S. Equities at UK asset manager Artemis said while the overall picture for investors was brighter, the recovery was likely to be uneven. “Low inventories and the need to manufacture and distribute goods are likely to be the first drivers of the recovery, with the re-emergence of consumer demand adding a powerful second phase.”

The MSCI World index was up 0.1% at 1013 GMT, just shy of the previous session’s record high. After opening lower, European shares crawled back into the black tracking overnight gains in Asia where China stimulus hopes helped MSCI’s broadest regional gauge rise 0.7%, with the STOXX 600 index rising as much as 0.5% to an intraday high following the Pfizer news.

Earlier in the session, Asian stocks gained, led by the finance and IT sectors. Most markets in the region were up, with Taiwan’s Taiex advancing 1.3% and Australia’s S&P/ASX 200 rising 0.5%, while Japan’s Topix slid 0.8%. Trading volume for MSCI Asia Pacific Index members was 13% above the monthly average for this time of the day. The Topix lost 0.8%, with Toyota and Sony contributing the most to the move. The Nikkei 225 Stock Average lost 1.1% after Tokyo reported a record number of new Covid-19 infections. The Shanghai Composite Index rose 0.2%, driven by China Life and Industrial Bank.

Strong corporate earnings in the third quarter have also underpinned the positive stock market sentiment, said analysts at Barclays, with firms “confident on the outlook and in control of costs”, they said in a note to clients.

“This reinforces the case for a strong earnings rebound and pick-up in corporate activity in 2021, as the cyclical recovery unfolds.”

As risk sentiment returned, risk havens sold off and Treasuries dipped to session lows in early U.S. trading after Pfizer Inc.’s final analysis of clinical-trial data previewed last week showed its Covid-19 vaccine was 95% effective. Yields flipped to slightly cheaper on the day across belly, remaining within a basis point of Tuesday’s close across the curve. Treasury’s 20-year new-issue bond auction is ahead. 10-year yields, just above 0.86%, were slightly cheaper on the day vs bunds and gilts. On today’s calendar we have a sale of $27BN in 20Y Treasurys at 1pm which is $2b larger than previous new issue; the 20Y WI is trading around 1.397%, above all six previous 20-year stops and ~2.7bp cheaper than last month’s. In Europe’s debt markets, Germany saw its benchmark 10-year government bond yield fall to its lowest since Pfizer announced its COVID-19 vaccine update a week and a half ago.

“Yields continue to grind lower as more warning signs flash about the near-term outlook,” said Benjamin Schroeder, senior rates strategist at ING. “Euro zone spreads appear to have eyes only for QE (quantitative easing), shrugging off volatility and EU setbacks,” he said, referring to news this week that Hungary and Poland have blocked the adoption of the 2021-2027 budget and recovery fund by European Union governments.

The yield on China’s 10-year sovereign debt rose by 5.2bps to a new high for 2020 at 3.33% (the 2019 high yield is in the vicinity of 3.45%). The price response in onshore rates stands in contrast to the move in US debt with a similar maturity profile (-3.3bps in yield week-to-date).

In FX, the USD declined 0.2% in BBDXY terms, with the Index trading further below the 1,150 mark and on the verge of hitting a new low for 2020. Advisors from the incoming US administration have shied away from a national lockdown in early-2021, which has helped lift risk appetite alongside positive vaccine news. The dollar declined against all Group-of-10 currencies as it continued to be sold amid a more optimistic vaccine outlook and after Fed Chair Jerome Powell said the U.S. economy still has a “long way to go” before it fully recovers from the pandemic. The Bloomberg Dollar Spot Index fell as much as 0.3% in early trading, nearing the multi-year low recorded on Nov. 9, to take losses into a fourth day, before recovering some losses following the Pfizer news.

The Turkish lira extended a drop to as much as 1.1% after President Recep Tayyip Erdogan spoke against higher interest rates one day before central bank’s key rates meeting, sparking confusion whether the CBRT would hike rates by as much as 500 bps tomorrow as some banks now expect. Erdogan said high interest rates render production impossible, prevent improvement in exports: “We will solve our problems in line with free market economy practices” he said adding that “Turkey will accomplish price and financial stability, we are targeting lower inflation as soon as possible.” The Lira was trading 0.4% lower at 7.7076 per USD after dropping as low as 7.80; The Borsa Istanbul Banks Index pared gains of as much as 5.3% after Erdogan’s comments and was trading 2% higher.

In other markets, the Norway krone led G-10 advances; USD/NOK down 0.6% 9.017, as oil rose toward $42 a barrel in New York, as signs of a robust demand recovery in Asia offset a jump in U.S. crude stockpiles. USD/JPY fell 0.4% to 103.83, its lowest since Nov. 9. Cross is down a fifth day, the longest run in two months. AUD/USD rose 0.2% to 0.7318 as broad dollar weakness reverses an earlier decline. GBP/USD continued to be supported, rising as much as 0.4% to 1.3297. U.K. and European Union could strike a deal on their future trading and security relationship early next week. Media reports “suggesting a deal next week and the departure from government of high profile Brexit hardliners seems to have inspired fresh confidence in a deal and thus in sterling,” Sean Callow, senior currency strategist at Westpac Banking Corp.

With stocks still well supported, other risk markets also took heart, with U.S. crude futures and Brent crude futures both up just over 1%, bolstered by hopes OPEC will delay a planned increase in production.

But nowhere was the move more pronounced than in Bitcoin, where the cryptocurrency briefly traded above $18,000 for the first time since Dec 2017, extending its blistering 2020 rally driven by demand for its perceived quality as an inflation hedge and expectations of mainstream acceptance. The original and biggest cryptocurrency jumped as high as $18,483 and was last up 2%. It has soared about 160% this year and has jumped 17% in the last three days alone.

Bitcoin is now close to its all-time high of just under $20,000, which it touched at the peak of its retail investor-fuelled 2017 bubble. “It is not out of the question for the crypto to hit its all-time high of $20,000 this side of Christmas,” said Simon Peters, analyst at investment platform eToro.

“The crypto industry has consolidated, matured and is seeing real traction with institutional investors. Investors are using bitcoin as an inflationary hedge to combat the prospect of continued government stimulus.”

Meanwhile that “old school” bitcoin, gold, was weaker, trading $20 lower at $1871.

Looking at the day ahead now, data highlights include the UK CPI reading for October, along with new car registrations in the EU27 for that month. From the US, we’ll also get October’s housing starts and building permits. Central bank speakers include the Fed’s Williams, Bullard and Kaplan, along with BoE Chief Economist Haldane.

Market Snapshot

S&P 500 futures up 0.4% to 3,621

STOXX Europe 600 up 0.05% to 389.00

MXAP up 0.2% to 188.36

MXAPJ up 0.6% to 623.94

Nikkei down 1.1% to 25,728.14

Topix down 0.8% to 1,720.65

Hang Seng Index up 0.5% to 26,544.29

Shanghai Composite up 0.2% to 3,347.30

Sensex up 0.4% to 44,142.57

Australia S&P/ASX 200 up 0.5% to 6,531.10

Kospi up 0.3% to 2,545.64

Brent Futures up 1.3% to $44.70/bbl

Gold spot down 0.3% to $1,870.39

U.S. Dollar Index down 0.2% to 92.28

German 10Y yield fell 0.2 bps to -0.565%

Euro up 0.2% to $1.1880

Brent Futures up 0.9% to $44.12/bbl

Italian 10Y yield fell 1.3 bps to 0.528%

Spanish 10Y yield unchanged at 0.075%

Top Overnight News from Bloomberg

European Central Bank policy makers are trying to persuade investors not to focus too much on the size of their next dose of monetary stimulus, hoping they will instead look at its design

After a couple of big crashes that destroyed billions in value, the digital currency has rebounded to its highest value since January 2018, crossing $18,000 this week. The cause: a flurry of developments that suggest Bitcoin has taken some big steps toward going mainstream

Italy’s banks could face higher costs to sell bad loans as the government is set to scrap tax relief measures in next year’s budget. The government decided not to extend into 2021 a tax benefit introduced earlier this year to facilitate the disposal of non-performing loans held on the balance sheets of Italian banks. Lenders and customers have been severely hit by the pandemic crisis

U.K. Prime Minister Boris Johnson announced a 12 billion-pound ($15.9 billion) plan to boost green industries and tackle climate change, in a blueprint he says will create or support as many as 250,000 jobs

The U.K.’s entry to Europe’s booming green sovereign bond scene could prove a catalyst for broader corporate issuance, helping London’s ambitions of becoming the continent’s ethical investing hub

Investors in Europe are getting their once-a-year opportunity to snap up Chinese sovereign debt in volume as the nation returns with a euro bond sale that stands to benefit from ultra-low borrowing costs there

New Zealand’s central bank said it accidentally disclosed sensitive information from its latest Monetary Policy Statement to a group of financial services firms before the official publication time last week

Quick look at global markets courtesy of NewsSquawk

Asian equity markets traded mostly higher as the region attempted to pick up from the weak handover from Wall Street where all major indices finished a choppy session in the red amid mixed data and as the recent vaccine euphoria wore off. ASX 200 (+0.5%) was positive with the index underpinned by outperformance in its largest weighted financials sector but with upside limited in the broader market by softness in commodity-related stocks, while Nikkei 225 (-1.1%) lagged its peers on recent currency inflows and virus concerns with Tokyo preparing to shift to the highest virus alert level. Hang Seng (+0.5%) and Shanghai Comp. (+0.2%) were kept afloat despite a slow start as participants remained cautious following another liquidity drain by the PBoC and amid further tension-related headlines after US bombers entered China’s air defence identification zone on Tuesday and with US regulators drafting plans to require Chinese companies listed in the US, to use auditors overseen by US regulators or risk being removed from exchanges. Finally, 10yr JGBs eked mild gains amid recent upside in T-notes and underperformance in Tokyo stocks, but with upside capped by mixed results at the 20yr JGB auction.

Top Asian News

Copper Roars, Zinc Rallies as Chinese Demand, Dollar Spur Rally

China’s Credit Jitters Deepen a Selloff in Government Bonds

Bank of Thailand Shifts Focus to Baht Rally, Holds on Rates

Sharp to Return to Japan’s Blue Chip Index, Replacing Docomo

European equities trade modestly firmer after a softer start to the session (Eurostoxx 50 +0.1%) as prices continue to consolidate around recent levels in the absence of any further incremental newsflow. The picture remains the same for the region as optimism around the efficacy of COVID-19 vaccines is somewhat tempered by the nearer-term outlook which is one of mounting COVID cases, lockdown restrictions and ongoing disputes over the passage of the European recovery fund. Sectoral performance is relatively mixed with mild outperformance in the tech sector, something which recently has often been a sign of rotation in/out of growth momentum names and out/into value/cyclicals. However, the performance of the latter is relatively mixed, suggesting that this morning is not in-fitting with this theme. Additionally, the magnitude of moves thus far are relatively minor and as such there is the risk that any such discrepancies between groups could be subject to over-interpretation. The highlight of this morning’s earnings reports was Danish shipping giant Maersk (-2.1%) with the Co.’s report often viewed as a bellwether for global economic activity, on which, the Co. noted that it has recovered faster than initially anticipated as it benefits from firmer retail sales in the US. Elsewhere, RSA (+3.9%) are firmer on the session after the Co. accepted a GBP 7.2bln takeover approach from Intact and Tryg. Other deal activity has seen Deutsche Boerse (+3.4%) agree to acquire an 80% stake in Institutional Shareholder Services with an enterprise value of USD 2.3bln. To the downside, Air France-KLM (-3.3%) are lower on the session with reports noting the Co. are said to be in discussions over a EUR 6bln capital raise. Hargreaves Landsown (-1.5%) are another laggard for the session amid reports that Stephen Lansdown, the Co.’s founder has sold 6.7mln shares at a discount.

Top European News

Spain Raises Hurdle for Foreign Investments in Strategic Firms

Pimco Said to Take Office Space in Dublin in Boost to Market

British Land Hikes Asset Sales as Values Drop $1.1 Billion

Ubisoft Jumps on Positive Update for New Assassin’s Creed Game

In FX, the Dollar and index look increasingly destined to decline further as sellers continue to pounce on rebounds and the technical backdrop/momentum turns more bearish to the benefit of its major and EM counterparts. In fact, the Buck’s downfall may be due to relative strength elsewhere as much as negative US specifics, albeit the ongoing rise in COVID-19 infections and fatalities has dampened some vaccine optimism as stimulus remains gridlocked in the still uncertain Presidential Election aftermath. The DXY has faded after another tame and short-lived recovery petered out just above 92.500 and is just off 92.200 having fallen to 92.207 vs last week’s 92.129 trough ahead of housing data and another round of Fed speak.

NZD/GBP/AUD – In contrast to the Greenback, latest Kiwi and Aussie revivals appear more solid on the respective 0.6900 and 0.7300 handles following mixed NZ PPI data and appreciation in the YUAN from another higher PBoC Cny midpoint fix. Meanwhile, the Pound is inching closer to 1.3300 and back through 0.8950 against the Euro ahead of a potentially key update from EU chief Brexit negotiator Barnier on Friday and in wake of reports that France may have ‘accepted’ that there will less water to fish in post-UK transition. However, market contacts suggest there could be big offers into the next big figure in Cable and price action supports that theory, while Aud/Usd may be capped around 0.7350 in the run up to Aussie employment overnight.

JPY/CAD/EUR/CHF – The Yen has breached 104.00 again irrespective of somewhat conflicting Japanese trade impulses, as the surplus smashed consensus, but only by virtue of the fact that exports hardly fell and imports plunged much more than expected. Elsewhere, the Loonie is back above 1.3100 against the backdrop of firmer oil prices in advance of Canadian CPI again, while the Euro is still on track to test 1.1900 and in bullish mode above the 50 HMA (1.1856) given no big upside option expiry interest to hamper the pair today, unlike Usd/Cad that should be cushioned by a hefty 1.1 bn at the 1.3000 strike. In similar vein, the Franc is finding 0.9100 tough to overcome, and perhaps wary of more verbal intervention to compliment direct action via SNB’s Maechler who is scheduled to talk at some point.

SCANDI/EM – Choppy trade for the Sek and Nok due to fluctuations in risk sentiment, but the Try is bucking the overall trend of gains vs the Usd after yesterday’s brief interlude as the clock ticks down to Thursday’s eagerly anticipated CBRT policy meeting that comes with an aggressive median forecast of +475 bp in comparison to unchanged SARB expectations.

In commodities, WTI and Brent have continued to grind higher throughout the morning aided by the gradual pick-up in equity performance as well as tail-winds from the USD’s underperformance thus far. Fundamentally, little new has occurred since yesterday’s JMMC gathering and attention has now firmly turned to the full OPEC/OPEC+ gathering at month-end for further updates prior to the next JMMC on December 17th. Currently, the benchmarks are posting gains of around 1.0% and reside in relative proximity to session highs. For reference, last night’s private inventories printed a larger than expected build of 4.2mln vs. Exp. 1.7mln and did prompt some crude downside although this was relatively short-lived. Later today the EIA will release their inventory report with the headline expected at a build of 1.65mln. Moving to metals, spot gold is overall flat this morning but has been erring slightly lower in-spite of the USD’s downside with some desks attributing the mild pressure to Fed nominee Shelton’s nomination being blocked yesterday, though this does retain the scope for a re-vote at a later date; in the context of Shelton’s previously expressed interest in hard-money regimes.

US Event Calendar

7am: MBA Mortgage Applications -0.3%, prior -0.5%

8:30am: Housing Starts, est. 1.46m, prior 1.42m

8:30am: Housing Starts MoM, est. 3.18%, prior 1.9%

8:30am: Building Permits, est. 1.57m, prior 1.55m

8:30am: Building Permits MoM, est. 1.43%, prior 5.2%

DB’s Jim Reid concludes the overnight wrap

The rally in risk assets paused for breath yesterday as markets shifted their focus from Monday’s positive vaccine news to the near-term challenges of rising case growth and tighter restrictions. By the close, both the S&P 500 (-0.48%) and the Dow Jones (-0.56%) had fallen back from their record highs. 18 of the 24 industry groups in the S&P fell yesterday, led by defensives such as Utilities (-2.01%), Food & Staples (-1.49%) and Healthcare Equipment (-1.42%). However, the NASDAQ fell a lesser -0.21% thanks in part to a +8.21% advance for Tesla, which came on the back of the news that it’ll join the S&P 500. It added c.$31.8bn market cap on the day, which is around the same size as Yum! Brands ($31.4bn), Freeport-McMoRan Inc ($30.6bn) and notably near Ford ($34.8bn). As we mentioned yesterday, it will comfortably enter the top 10 of the S&P 500 when it arrives in December.

In other “is it a bubble or not news?” Bitcoin (+5.59%) traded back above $17,000 for the first time since 21 December 2017 – a level it has only closed above for 5 other days in history. It even briefly soared through $18,000 in Asia trading. This is even as gold (-0.45%) continues to slip, so the two have decoupled a bit of late. The precious metal is now down -8.88% from its early-August highs. The two have been correlated recently mostly due to their negative relationship to the dollar, which was down -0.24% yesterday and closed only +0.30% higher than its pandemic closing lows.

As we go to print Asian markets are taking a sudden dip lower as Japanese broadcaster FNN announced that Tokyo saw a record 493 Covid-19 cases. This follows earlier news from the Nikkei that the Tokyo Metropolitan Government is making final arrangements to raise its alert on the infection status to the highest of 4 levels. The Nikkei is down -1.13% as we type. Futures on the S&P 500 are down -0.34%. Elsewhere, markets are trying to hang onto earlier gains with the Hang Seng (+0.14%), Shanghai Comp (+0.34%), Kospi (+0.22%) and ASX (+0.51%) all still up.

Fed Chair Powell spoke yesterday at an online event hosted by the Bay Area Council and said that the economic recovery in the US would likely continue at a “solid” pace though he called rising coronavirus infection rates a “significant” downside risk “especially in the near term.” While Powell indicated that the recent spate of vaccine news is good for the medium-term outlook of the economy, a full recovery is a still a long way off and that the Fed “will stay here and be strongly committed to using all our tools.” He went on to indicate that he leaned towards keeping the Fed’s emergency lending facilities operation as is, given that the “recovery is incomplete” – this comes as all but one of those facilities are scheduled to expire at year-end. Regardless of the Fed’s position on the matter, the Treasury Secretary Mnuchin would have to agree to keep the facilities open and he has not yet made a decision. Elsewhere, Judy Shelton’s confirmation to the Federal Reserve Board was blocked yesterday in 47-50 vote after two Republican senators were unable to attend due to quarantining. Senate Majority leader McConnell voted no in order to be able to bring the vote back up once the two missing senators were again available. Given Democratic Senator-elect Mark Kelly is set to join the chamber as early as the first week of December, the schedule of the GOP to get Shelton confirmed is tightening.

On the Vaccine front, Pfizer’s CEO said overnight that a key safety milestone had been reached in the study of its vaccine, and the drug maker is now preparing to seek an emergency-use authorisation. Elsewhere, the Indonesian government is planning to kick-starts its vaccine inoculation program next month with an initial 3mn doses likely to be from China’s Sinovac. The country will prioritise health workers, police, military and public servants.

Back to markets and over in Europe it was a similar story to the US, as the STOXX 600 (-0.24%) and bourses across the continent also lost ground. The STOXX Travel & Leisure index (-1.06%) suffered in particular amidst fears of continued restrictions heading through the winter months, while Healthcare (-1.32%) was the worst-performing sector in Europe. Other cyclicals such as Energy (+0.71%) and Autos (+0.72%) continued to edge higher as the vaccine news kept them afloat.

With investors rotating out of risk assets, yesterday saw a strong performance in sovereign bond markets, where a number of new records were set. For example, yields on 10yr Italian BTPs fell -1.3bps to an all-time low of 0.639%. Meanwhile in Greece, the spread of 10yr yields over bunds fell another -3.0bps to 1.233%, which is their tightest level in over a decade. Core sovereign bonds also gained ground, with yields on 10yr Treasuries falling -4.9bps to 0.857%, as those on 10yr bunds (-1.8bps), gilts (-2.5bps) and OATs (-2.3bps) also fell.

Another asset that performed well yesterday was sterling, which strengthened +0.36% (up a further +0.13% overnight) against the US dollar thanks to headlines that suggested the Brexit negotiators could manage to agree a deal early next week, potentially as soon as Monday. Nevertheless, the same set of headlines also had officials cautioning that the talks could still fall apart, while a statement from Prime Minister Johnson’s office said that “it is far from certain that an agreement will prove possible”. It’s not clear when we’ll get any further news, but the Guardian’s Brexit correspondent, Lisa O’Carroll tweeted that UK government sources weren’t expecting a breakthrough this week and were looking to next week instead for a deal. If these reports are right, that means that a deal won’t have been reached in time for tomorrow’s video conference of EU leaders, in which they would have had the opportunity to discuss the issue.

In terms of the latest developments on the virus, in New York City, the 7-day average positivity rate was at 2.74%, which is below the important 3% threshold that would lead to school closures. Ohio’s Governor imposed a 10pm to 5am curfew for the next 21 days, though he has maintained that he is trying to keep businesses open outside of those hours as much as possible. In Scotland, a number of areas including Glasgow faced tougher Level 4 restrictions, which includes the closure of non-essential shops, along with pubs and restaurants. Elsewhere in Europe, the Netherlands extended their partial lockdown measures while also lifting some restrictions imposed two weeks ago. Libraries, theaters, cinemas, museums and swimming pools can reopen while bars and restaurants remain shut. Similarly in France, Prime Minister Castex announced that the country will not end the full lockdown but that some measures may be lifted. It is starting to look like late-spring again with the virus getting worse in the US as it plateaus in parts of Europe. Across the other side of world where the virus has been spreading less aggressively, South Australia announced a 6-day lockdown that would see even schools and universities close to help contain a growing cluster of Covid-19 infections in the state capital Adelaide. South Korea also reported the highest number of daily infections in almost 12 weeks.

Yesterday’s data saw a weaker-than-expected reading on US retail sales, which rose by just +0.3% in October (vs. +0.5% expected), while the previous month’s growth was also revised down to 1.6% (vs. 1.9% previously). That +0.3% growth is the slowest pace of growth since the sharp contractions when the pandemic first hit, and the soft reading will add to concerns with the coronavirus case numbers surging once again. One caveat is that YoY US retail sales are up a fairly remarkable +5.7%, which shows how much government and central bank stimulus has propped up spending.

In more positive real time data, industrial production rose +1.1% in October (vs. +1.0% expected), and September’s decline was revised to show a smaller contraction than expected. Lastly, the NAHB’s housing market index rose to a record 90 (vs. 85 expected).

To the day ahead now, and data highlights include the UK CPI reading for October, along with new car registrations in the EU27 for that month. From the US, we’ll also get October’s housing starts and building permits. Central bank speakers include the Fed’s Williams, Bullard and Kaplan, along with BoE Chief Economist Haldane.

via ZeroHedge News https://ift.tt/3kLWJS9 Tyler Durden

Final Results Show Pfizer COVID-19 Vaccine 95% Effective Tyler Durden

Wed, 11/18/2020 – 06:56

After confirming yesterday that its Phase 3 vaccine trial had finally recorded its last confirmed COVID-19 infection needed before applying for an emergency use approval from the FDA, Pfizer Wednesday morning has just released a summary of its “final” data which – as luck would have it – showed the Pfizer vaccine is actually 95% effective, leaving it on par with Moderna’s vaccine.

The final number is an improvement on the 90% effective preliminary finding released by Pfizer last week. What’s more, the new data answered a critical question posed by experts: how effective is the vaccine on older and more vulnerable patients? Pfizer and Biontech said Wednesday that the vaccine’s efficacy in people older than 65 was more than 94%.

According to WSJ, now that the final data is in, Pfizer expects to apply for the EUA within days, the company said Wednesday.

Shares were trading almost 4% higher in premarket on the news.

via ZeroHedge News https://ift.tt/3nBshfC Tyler Durden