Elon Musk Is Now Officially Going To Trial For Calling Vernon Unsworth “Pedo Guy”

Elon Musk is officially heading to trial after a federal judge declined his last request to toss out a defamation case brought by Vern Unsworth, the heroic cave diver that Musk famously referred to as “pedo guy” on Twitter.

U.S. District Judge Stephen Wilson ruled on Monday that a jury will have to decide whether or not Musk was negligent for failing to check the accuracy of his statements before he made them to his over 20 million Twitter followers and a journalist, according to the LA Times.

The judge tossed the idea of Musk having a free speech defense, ruling that the statements did not have any basis in any public controversy involving Unsworth. Unsworth’s lawyer, L. Lin Wood said after the hearing that “the burden of proof for negligence is lower than that for actual malice”.

This means that Unsworth will only have to convince the jury by a preponderance of the evidence, rather than clear and convincing evidence, making it easier for the panel to find Musk liable for defamation, Wood said.

Punitive damages could come as a result of the jury finding that Musk acted with malice, according to Wood.

Musk’s attorney, Alex Spiro, said: “We look forward to the trial. We understand that, while Musk has apologized, Unsworth would like to milk his 15 minutes of fame.”

Judge Wilson was not convinced that Musk’s allegations of pedophilia were relevant as to whether or not Musk’s submarine would have worked in the rescue, stating to Musk’s lawyer: “You’re saying his being a pedophile is germane to the issue whether Musk had sincere motivation. That seems a bit of a stretch.”

The judge is expected to issue a written ruling soon.

Musk’s spat with Unsworth started famously, after Unsworth referred to Musk’s proposed Thai cave rescue submarine as a “PR stunt” and told Musk, via a CNN interview, that he could stick his proposed solution “where it hurts”. Musk responded by calling Unsworth “pedo guy” in a Tweet, before referring to him as a “child rapist” in an email that Musk thought was “off the record” with a Buzzfeed reporter. The email was not off the record, and Buzzfeed subsequently released Musk’s e-mail to the public.

Recall, toward the beginning of the month, we wrote aboutMusk referring to himself as a “fucking idiot” for e-mailing his unverified information about Unsworth to Buzzfeed.

“Italy? Don’t be silly… its fixed, nothing can go wrong with the plan now….”

My telly lives a precarious life. It was nearly shot this morning as two political numpties whittered on about the necessity to prevent Brexit, how untrustworthy Boris is, how the best interests of the country are served by their diligence in endlessly debating the placement of a comma in the withdrawl agreement, and how its important the UK waits till it’s safe for pensioners to go to the polls when the weather is better, and students are back in their residencies. Argg.. Do these people ever stop to listen to themselves? Please make them stop! None of these things actually matter! Tis far better to get democracy done roughly, than to strangle and devalue it through pointless political posturing – but that’s what most MPs are determined to show off about…

Despite the Brexit gloom there is something curious going on in the UK. Parliament may be engaged in some curious self-flagellation game, but elsewhere the confidence level of the country is much better. Companies and Consumers see past the eejits being interviewed on College Green, and are getting on with it. They see a bright future once we’re through the present gloom. They are largely ready. The UK will face adversity as we usually do.. a frown, a shrug and get on with it.

Despite being a Scotsman, (which means I am genetically inclined to support whomever is playing England), the likelihood England are going to win the Rugby World Cup could actually confirm a sea change in the UK’s outlook. I was reading a very insightful article by my chum David Murrin yesterday – Brexit Lessons From The England Rugby World Cup Team. He draws parallels between England Coach Eddie Jones’ and the Brexit team’s goal driven approach. They are prone to reversals through the process, but in the long-term, they get there. Interesting stuff! Give it a read.. (And yes, I will be supporting England on Saturday! And singing a well known Spitting Image song..)

Meanwhile, back in the real world.

Stocks hit a record high! I am unconvinced by the arguments its due to greater confidence about a trade deal – its more likely about the Fed easing later this week. The sudden rise in any Chinese stocks with any connection, however tenuous, to Blockchain yesterday was funny – shows how close China is to US. Just a few years ago putting crypto in any business plan was a guarantee of success!

I am slightly worried much of the recent upside has come from Tech stocks. Some, like Apple and Microsoft are now establishment stocks – and key components of the Blain Pension plan, but so is Alphabet which took a slight tumble y’day. They all pass my fundamental test – stocks I see value in. Others, like Facebook and even Amazon (which I have formed an intense hatred of because of a delivery problem), have too much regulatory risk for my tastes. Despite the experience of the failed Unicorn IPOs this year, parts of the Tech market are still playing to a suspension of rational investing – and I am concerned a further tumble in unicorns could destabilise solid tech.

One of the big gainers was Spotify on the back of great numbers. I made a schoolboy error last year when I switched my streaming music service from Spotify to Apple. Spotify is simply a much much better service – I regret my switch. It’s now got 115 million paying subscribers and is growing faster than any of its rivals – but it still isn’t profitable, which at some point will impact the value. It is close to profit – and will likely get there.

The key issue about Spotify is how great it and streaming has been for the music industry – reinvigorating artist revenues, and driving more opportunities to monetise and get music out there. Streaming is important, but it’s Content that’s King!

It’s one of the key concepts behind a new music deal we’re putting together: the content value of music: 40 years ago, as CDs started to replace vinyl, the average music listener was limited to the radio, and personal and expensive music collections – and would have had access to less than 5% of recorded music. The streaming revolution has opened up immediate access to maybe 90% of recorded music- which not only has opened diversity and choice, but spawned greater value monetising music in films, advertising and wider markets. It’s created a Content Revolution. It’s happening, and its massively valuable.. but to the content providers rather than the streamers. (If you want to hear about our deal – join the queue.)

Bond Market worries

The Bond Market is causing me much more concern. After we get this week’s rate cut out the way, the downside momentum on bonds is likely to increase: less appetite for central bank easing and asset-purchase distortion, rising doubts about the long-term wisdom of ultra-low rates, rising concerns about credit quality and massive doubts about just how liquid bond markets will be in a changed outlook.

The reason bonds have performed so strongly through 2019 has largely been on the back of recession expectations and that central banks would continue to bail out markets. Recession can still happen, downturn is certainly a risk. China growth has been driving markets for the last 10-years and its clearly slowing on trade rifts and the economy internalising. Unfortunately, the corporate bond markets got well ahead of the curve:

Issuance has been massive – cheap rates stimulating a massive borrowing binge which wasn’t used to create new capacity, but largely spent on buyback stocks. Result: Overleverage.

Credit Quality has decreased – the hunt for yield has pushed investors down the credit curve to the point most corporate debt is poised a notch or two above junk. Easy money led to cuts in investor protections. Portfolio managers can kid themselves it’s still investment grade. Result: Increased Credit Risks.

Global economic downturn, or even a small rise in interest rates will create a shift in the credit threshold line – pushing many near junk issuers into junk territory as their credit outlook declines and interest rate costs accelerate. Result: Firesales of junk assets from IG holders.

Exit path – everyone is very aware there is no market making. It’s an agency market, and without buyers in a credit downturn there is no capacity to slow falling prices if everyone tries to exit. Result: Chronic Illiquidity risk.

FT carries a story this morning about bond giant PIMCO: Pimco shuns US Corporate Bonds, backing away from the US corporate bond market due to “concerns they could be a rapid decline in prices during an economic downturn”. There is one of my coveted No Sh*t Sherlock awards winging its way towards their California offices.

Great article on Green Bonds from Bloomberg’s Mark Gilbert y’day: The Explosion in Green Bonds Comes Without a Premium – pointing out the market to fund green projects has a puzzling price feature: if they are so virtuous, why don’t they trade at a premium? I suspect he was being rhetorical – and a highly experienced market journalist is well aware Green Bonds are largely a marketing gimmick. Although they have slightly outperformed the overall credit market, they are pretty much in line with Investment Grade Credits – so precious little price reward for investing in Green stuff. Yet. He predicts they will tighten. I predict a rise in company’s Greenwashing – using green labels to spend on not so green things!

Russian Patrol Comes Under Turkish Mortar Attack In Northern Syria

Turkey has attacked a Russian military police convoy patrolling a northern Syria border area near Turkey, according to local correspondents and video of the incident’s aftermath.

Unconfirmed Syrian Kurdish media reports say at least one Russian soldier who was part the military police (MP) patrol was injured after the convoy came under fire by Turkish artillery fired from Turkey’s side of the border in an area called Derbisiye. A senior foreign correspondent for the Telegraph also posted a video of the attack’s aftermath:

Video purports to show aftermath of a mortar attack on Russian Military Police at Dirbesiye border crossing w Turkey in NE Syria. pic.twitter.com/gr9OdqzVZh

Early unconfirmed reports say there may be other casualties including two journalists and four civilians possibly injured in the attack on the Russian police convoy.

Kurdistan24 News journalist Akram Salih described of the incident that the Turkish army entered the Syrian side of the border at which point the mortar was fired at the Russian side.

Local reports say Turkish sources are angered they were not informed about a Russian military police visit to the border, while Turkish media is denying that any mortar shelling took place altogether.

Following the White House’s ordered draw down of US forces from border areas where they were embedded with Syrian Kurdish forces earlier this month, Russian military patrols moved in, as part of a Turkish ‘safe zone’ agreement brokered between Putin and Erdogan.

Russian military police patrol in northern Syria. Image source: AP

Turkish forces now no doubt see the Russian patrols as ‘protecting’ the Kurdish militias, just as the US did before, resulting in high tensions – including this latest reported mortar attack – whether intentional or inadvertent.

Ankara is controversially pushing to carve out a 30km buffer zone in northeast Syria. Ironically, though Erdogan has claimed the Turkish military will root out ISIS, it must be remembered that this weekend ISIS terror leader Abu Bakr al-Baghdadi was killed merely 7km from the Turkish border in Idlib.

Pending Home Sales Surprise, Biggest Annual Gain Since 2015

Despite disappointing slowdowns in sales of new- and existing-homes, pending home sales were expected to show a small positive gain in September but surprised with a 1.5% MoM pop (0.9% exp).

This is the strongest pending home sales index since Dec 2017…

Source: Bloomberg

The National Association of Realtors’ Index of pending home sales increased 6.3% in September from a year earlier on an unadjusted basis, the biggest gain since August 2015

Source: Bloomberg

“Even though home prices are rising faster than income, national buying power has increased” with lower interest rates, Lawrence Yun, NAR’s chief economist, said in a statement.

“But home prices are rising too fast because of insufficient inventory.”

The monthly gains in contracts were concentrated in the Midwest and South, while the West and Northeast recorded declines.

US Confidence Tumbles To 7-Month Lows As ‘Hope’ Evaporates

After plunging in September, Conference Board confidence was expected to rebound but, thanks to a small upward revision, October confidence slipped to its lowest since March with expectations weakest since January.

Consumer confidence in October fell to 125.9 vs 126.3 in prior month – lowest since March

Present situation confidence rose to 172.3 vs 170.6 last month – small bounce

Consumer confidence expectations fell to 94.9 vs 96.8 last month – lowest since January

Source: Bloomberg

The labor differential (plentiful vs hard-to-get) rebounded modestly in October from 33.5 to 35.1.

Under-35s confidence tumbled in October with Over-55s improving modestly

While plans to buy a home ticked up in October, plans to buy a car slipped notably.

October 28, 1929 – 90 years ago this week – is known as ‘Black Monday’ in financial circles.

The US stock market had peaked the previous month, on September 3, 1929, with the Dow Jones stock index reaching a record high of 381.

But throughout September and October, nervous investors began pulling their money out of the market.

And over a three day period in late October (including Black Monday), the market lost more than 30% of its value.

Ninety years later, I thought it would be prudent to look at three key insights from that historic crash, starting with:

1) Stocks are more overvalued today than they were in 1929

Back in 1929, the price/earnings ratio of the average company trading on the New York Stock Exchange was about 15.

In other words, investors were willing to pay $15 per share for every $1 of the average company’s profit.

That’s not high at all. In fact, a Price/Earnings ratio of 15 is completely in line with historic averages.

Coca Cola’s Price/Earnings ratio back in 1929 ranged between 15 and 18. Today it’s 30… meaning that investors today are willing to pay roughly twice as much for each dollar of Coke’s annual profit.

Coca Cola is actually quite an interesting case study.

If we just go back a few years to 2010, Coca Cola’s annual revenue was $35 billion. By 2018 the company’s annual revenue had fallen to less than $32 billion.

In 2010, Coca Cola generated $5.06 in profit (earnings) per share. In 2018, just $1.50.

And Coca Cola’s total equity, i.e. the ‘net worth’ of the business, was $31 billion in 2010. By 2018, equity had fallen to $19 billion.

So over the past eight years, Coca Cola has lost nearly 40% of its equity, sales are down, and per-share earnings have fallen by 70%.

Clearly the company is in far worse shape today than it was eight years ago.

Yet Coke’s share price has nearly DOUBLED in that period.

Crazy, right?

It’s not just Coca Cola either; the Price/Earnings ratio of the typical company today is about 50% higher than historic averages.

(This means that the stock market would have to drop by 50% for these ratios to return to historic norms.)

It’s clear that investors are simply willing to pay much more for every dollar of a company’s earnings and assets than just about ever before, including even right before the crash of 1929.

2) Stocks fell by nearly 90% in 1929… and it took decades to recover.

The ‘crash’ wasn’t isolated to Black Monday.

From the peak in September 1929, stocks ultimately fell nearly 90% over the next three years. The Dow bottomed out in 1932 at just 42 points.

42 is lower than where the Dow was trading in 1885… so the crash wiped out DECADES of growth. And it took until November 1954 for the Dow to finally surpass its high from 1929.

If that were to happen today, it means the Dow would fall to just 2,700… a level it hasn’t seen since the early 1990s. And it wouldn’t return to today’s highs until the mid 2040s.

Most people think this is completely preposterous.

And to be fair, I think the government and central bank will do everything in their power to prevent a severe crash.

The Federal Reserve has already announced that it will print another $60+ billion per month, which should be favorable for the stock market in the short term.

But just because we can’t imagine something happening doesn’t mean it can’t happen. In fact it’s happening right now in Japan:

Japan’s stock market peaked in late 1989 with its Nikkei index reaching nearly 39,000.

Within a few years the Nikkei had lost half of its value and would ultimately fall by 80%.

Even today, thirty years later, the Nikkei index is still 40% below its all-time high.

There is no law that requires the stock market to go up. It can fall. And it can stay low for years… even decades.

3) Adjusted for inflation, stocks have returned just 1.7% per year since 1929.

It’s best to think long-term about any investment. Businesses take time to grow and expand, and patient investors who understand this tend to do well.

But when thinking about the long-term, it’s imperative to consider the extraordinary effects of inflation.

Every single year your money loses around 2% of its value. But over time those small bites of inflation fester into a major chunk of your investment gains.

Consider that, even according to the federal government’s monkey math, the US dollar has lost 94% of its value since 1929.

So even though the Dow is more than 70x higher than it was in mid-1929, when you consider the effects of inflation, stocks are only about 5x higher over the past 90 years.

That works out to be an average annualized return of just 1.7%.

Even over the past 20 years– if you go back to late 1999, the stock market has only returned about 2.2% per year when adjusted for inflation.

Think about all the risks and wild market swings that investors have had to deal with over the past 20 years– all for a measly 2.2%.

It’s interesting to note that, when adjusted for inflation, GOLD has outperformed stocks over the long run.

When adjusted for inflation, gold has averaged a 1.8% return since 1929 (slightly higher than stocks), and a 6.7% return since 1999– more than 3x as much as stocks.

But unlike stocks, people who own gold haven’t had to put up with the same risks. No shady brokers. No WeWork bullshit. No Enron scandal.

They earned 3x more than the stock market– with the added benefit of being able to hold their investment right in their own hands.

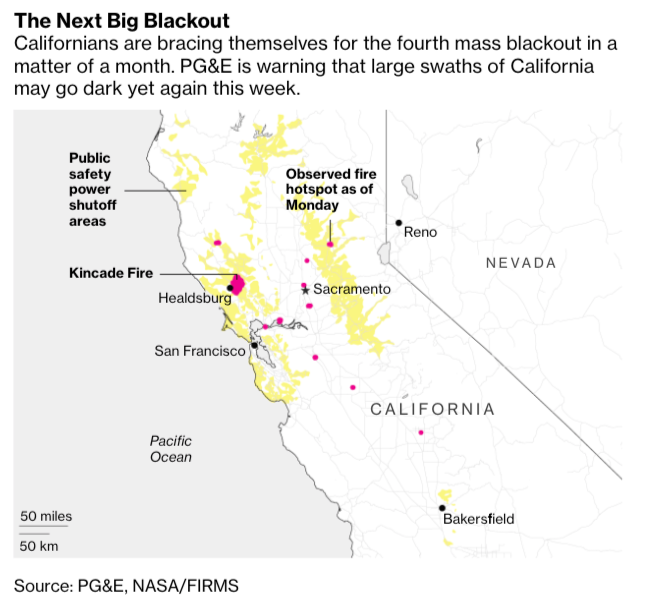

PG&E’s Rolling Blackouts Could Leave 1.8 Million Californians Without Power

Parts of California are seriously starting to behave like a third world country. No, we’re not talking about the poop, homeless, and opioid crisis on the streets of San Francisco, we’re talking about rolling blackouts from the state’s electric company, PG&E Corp.

The next round of blackouts are expected on Tuesday, as 1.8 million Californians will experience their fourth planned power shutoff this month.

The warning of the next big blackout came late Monday as PG&E restored electricity to nearly one million residents after the company cut power over the weekend to prevent windstorms from knocking over its powerlines and sparking fires, reported Bloomberg.

With another windstorm expected for Tuesday, PG&E will reduce power to 605,000 homes and businesses in the Bay Area, California’s wine country, and several regions around Sacramento to minimize powerline accidents that could spark wildfires.

The Kincade Fire, currently burning in Sonoma County, started last Wednesday after a PG&E high-voltage transmission line was blown over by a windstorm.

PG&E has been routinely criticized for its faulty equipment sparking a string of wildfires in 2017 and 2018 that killed dozens of people and destroyed hundreds of structures with estimated damage of $30 billion. PG&E has since filed for bankruptcy as its stock has crashed 95% in 25 months.

Bloomberg notes that 3 million Californians are still recovering from last week’s blackout, with at least half of those folks without power through Monday night. Most of these folks without power will likely remain in the dark as the next round of blackouts starts Tuesday morning.

“This event will start to impact the same people again in certain areas,” PG&E utility chief Andy Vesey told journalist Monday. “It is the weather — it’s not something we can control.”

Fires have also erupted in Southern California, affecting the ultra-wealthy in their upscale neighborhoods in Los Angeles.

“Leave,” Los Angeles Mayor Eric Garcetti told residents Monday. “The only thing you cannot replace is you and your family. So get your loved ones, your pets, and leave.”

*map

As fires rage across the state and power is shutoff to millions of residents and businesses, the loss of economic activity could start weighing down on the state’s GDP. The economic losses over the last several years are expected to be in hundreds of billions of dollars.

There have been many articles appearing in recent months suggesting that the economy might go into a recession within the next year. Many have focused on whether the Federal Reserve should cut interest rates to stop this from happening. There also has been a lot of speculation as to the effect that an economic downturn will have on the 2020 Presidential elections. I have not seen anyone talk about how today’s high stock prices will likely cause an economic collapse.

There have been numerous suggestions coming at things from the opposite direction, making the case that a recession will likely cause stock prices to fall hard. But I view that way of thinking about things as a holdover from the Buy-and-Hold Era. If stock price changes are caused by rational assessments of economic developments, it would make sense that economic bad times would cause stock prices to fall. But I believe that Shiller’s research showing that valuations affect long-term returns is legitimate research. If that is so, then high stock prices are caused by irrational exuberance and the inevitable disappearance of irrational exuberance causes trillions of dollars of consumer spending power to leave the economy, causing a contraction.

If that’s the way things work, the economic crisis of 2008 never came to an end. Employment numbers improved and businesses stopped going under. So, in a surface sense, economic conditions certainly improved. But the economic numbers improved only when CAPE levels returned to the dangerous levels that applied prior to the onset of the crisis. We pumped up stock prices to make people less fearful of spending but at the cost of insuring that a follow-up price crash would be coming in not too long a time.

So the economic crisis never really ended. It went into remission. If the economy was booming with stock prices at reasonable levels, we could take comfort that good times really had returned. But I don’t feel able to trust a recovery that is financed by an overpriced stock market. Overpriced stocks makes us feel that it is safe to spend again. But the financial security pushing spending forward is illusory. There is no “there” there when stock prices could fall to fair-value levels at any moment and trillions of dollars of spending power could be taken off the table again.

I am not a fan of illusory stock prices. I think that we all should be doing all that we can to keep stock prices at something close to fair-value levels at all times. All of our financial planning decisions depend on us knowing how much wealth we possess and it is not possible to know this for so long as stocks are priced at two times their real value, as they are today.

We cannot even form reasonable assessments of the merit of the actions of policymakers at times when high stock prices are causing the economic numbers to look better than they would look if stock prices were at reasonable levels. President Trump naturally says that it is his policies that have brought on good economic times. But how can we know how the economy would be doing if the entire stock market were priced at one-half of the level at which it is today priced. And I of course do not intend to make a partisan comment here. President Obama’s policies looked better because of the effect of high stock prices as well.

It is the Federal Reserve’s job to keep the economy from contracting too hard. Does that mean keeping stock prices from crashing? I get the sense that there are times when Federal Reserve members take this factor into consideration. But keeping irrational exuberance going at some point becomes a futile endeavor. We can’t just create money out of thin air by pushing stock prices upward. At some point the market insists that prices reflect real value (this is Shiller’s core finding). Pushing prices up is a holding action. Sooner or later we have to accept that fair-value prices will prevail again and that the economic pain that follows from a return to fair-value prices must be endured.

High stock prices are a lie. That’s what I am saying. They are not just a lie that affects stock investors. They are a lie that affects everyone who is living in our economic system. The Pretend Money that is created when stock prices rise above fair-value levels always disappears down the road a bit. And the net result is a negative because of the disruption experienced when businesses that appeared to be doing well go under and when workers who appeared to be headed for decent retirements find themselves far short of achieving their financial goals at a time in life when it is too late to do anything about it.

I reject the idea that we may be seeing a new economic crisis in the days ahead. To my way of thinking, we will be seeing a resumption of a crisis that we experienced for only a few months in late 2008 and early 2009 and then put off for another time. We put that crisis off because we did not look how out stock portfolios looked when fair-value price levels were restored. But the put-off was a temporary thing. To achieve more permanent solutions to the problems that received national attention in late 2008, we are going to have to come to terms with the primary cause of those problems — the high stock prices that still apply today.

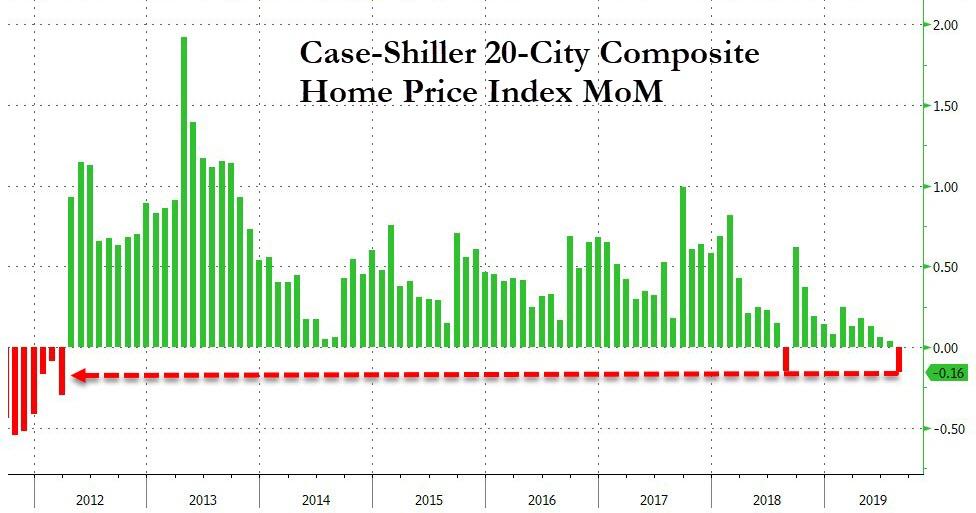

US Major City Home Price Growth Slumps To Weakest In 7 Years

For the 17th month in a row – the longest streak since 2008 – US home price growth (in 20 major cities) has been unable to re-accelerate.

S&P CoreLogic’s (Case-Shiller) 20-City Composite home price index rose 2.03% YoY in August and flat to a downward-revised July print…

Source: Bloomberg

This is the weakest growth since August 2012, and biggest MoM drop since March 2012…

Source: Bloomberg

All 20 cities in the index, with the exception of San Francisco, showed year-over-year gains. Prices there fell 0.1% from August 2018.

Prices in 17 cities rose from the prior month on a seasonally adjusted basis. In New York, home prices fell 0.4% from July, while in Las Vegas, they dropped 0.1%. In Detroit, prices were unchanged month over month.

As Bloomberg notes, although mortgage rates are hovering near a three-year low, tepid wage gains are limiting buyer enthusiasm in markets such as Las Vegas and New York. Meanwhile a shortage of affordable inventory is keeping prices elevated.

The latest in a growing line of witnesses in the Democrats’ impeachment probe has revealed himself: The New York Times reported last night that Lt. Col. Alexander Vindman, an Iraq War veteran and top Ukraine expert on the National Security Council, is planning to tell House impeachment investigators that he heard President Trump offer an explicit quid pro quo to the Ukrainian president.

It’s amazing that the Dems are calling more witnesses to testify to this fact – and, of course, leaking every “top secret” development to the New York Times – since the White House has already released a transcript of the July 25 call with Ukrainian President Volodymyr Zelensky. We can all determine for ourselves whether we thought Trump crossed the line, or not.We don’t need Witnesses to relay their opinion.

Alex Vindman

Already, many officials, including Zelensky himself, have said there was no quid pro quo.

But that apparently doesn’t matter to the NYT, or its MSM compatriots.

Vindman reportedly told the Times that he was on the call, and that he was so “sickened” by Trump’s behavior, he “twice registered internal objections about how Trump and his inner circle were treating Ukraine. He said he did this out of a sense of duty.

On Tuesday, he will become the first sitting White House official to testify in the impeach inquiry involving the country of his birth, as the NYT’s Sheryl Gay Stolberg points out.

In a draft of his opening statement before the top-secret impeachment committee that was leaked to the NYT, Vindman claims that he is a “patriot”, and that he didn’t think Trump’s conduct was “proper.”

“I am a patriot and it is my sacred duty and honor to advance and defend our country irrespective of party or politics,” Vindman said.

“I did not think it was proper to demand that a foreign government investigate a U.S. citizen, and I was worried about the implications for the U.S. government’s support of Ukraine,” Colonel Vindman said in his statement. “I realized that if Ukraine pursued an investigation into the Bidens and Burisma it would likely be interpreted as a partisan play which would undoubtedly result in Ukraine losing the bipartisan support it has thus far maintained.”

Vindman reportedly moved to the US as a child from Ukraine, and as a result speaks Russian, Ukrainian and English fluently. Arriving as a refugee, he eventually served in the military, rising through the ranks, then achieving a Master’s Degree from Harvard in Russian, Eastern Europe and Central Asian Studies. He has an identical twin brother, Yevgeny Vindman, who is also a Lieutenant Colonol.

But lower down in the story, NYT investigative reporter Danny Hakim includes an interesting, unexplained, detail.

“While Colonel Vindman’s concerns were shared by a number of other officials, some of whom have already testified, he was in a unique position. Because he emigrated from Ukraine along with his family when he was a child and is fluent in Ukrainian and Russian, Ukrainian officials sought advice from him about how to deal with Mr. Giuliani, though they typically communicated in English.”

It’s something that Fox News host Laura Ingraham first pointed out on her show Monday night.

Oh my God, look at the spin they are using right now, actually saying that Vindman is a Ukrainian double agent….this is so freaking bananas pic.twitter.com/Oxpju5W23N

Stanford Law Professor and former Bush Administration lawyer John Yoo agrees this is suspicious: It almost sounds as if Vindman is acting as a double-agent for the Ukrainians and advising them against his own boss’s interests?

{kind=link}