When I was growing up, my father, probably much like yours, had pearls of wisdom that he would drop along the way. It wasn’t until much later in life that I learned that such knowledge did not come from books but through experience. One of my favorite pieces of “wisdom” was:

“A sure-fire ‘no lose’ proposition is doing exactly the opposite of whatever ‘no lose’ proposition is being proposed.”

Of course, back then, he was mostly giving me “life advice” about not following along with my stupid-ass friends who were always up elbows deep in mischief.

However, that advice also holds true with the financial markets currently. As I have noted over the last couple of weeks (read this and this) the “bulls” certainly seem to regained control of the markets as new highs were reached on Monday. As I stated, between the Fed cutting rates, reigniting “not-QE,” and the President following our script of putting the “trade war” to rest, “what is there NOT to love if you are a bull.”

While we have begun to opportunistically increase our the equity exposures in our portfolios, we are cognizant there are currently several warning signs investors should consider before buying into the “bullish view.”

Here are four to consider.

Warning 1: Conflicting Confidence

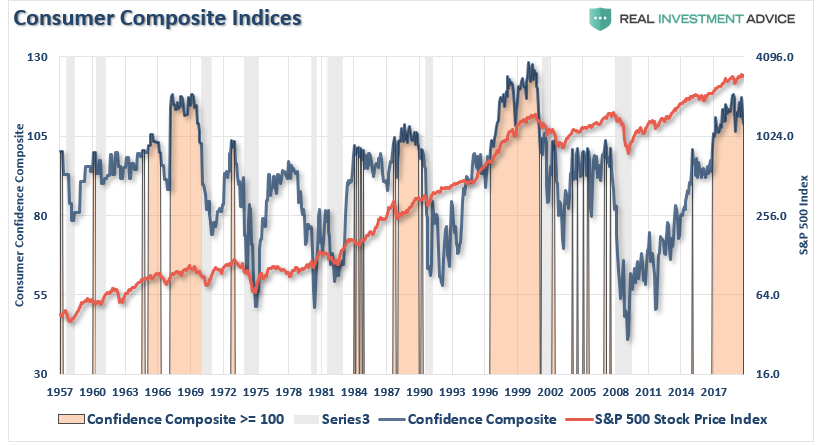

There are several different surveys of confidence, which all currently show the same thing. Individuals are extremely optimistic on just about everything. Recently, I discussed our composite confidence indicator:

“The latest release of the University of Michigan’s consumer sentiment survey rose to a three-month high of 96, beat consensus expectations, and remains near record levels. The chart below shows our composite confidence index, which combines both the University of Michigan and Conference Board measures. The chart compares the composite index to the S&P 500 index with the shaded areas representing when the composite index was above a reading of 100.”

“On the surface, this is bullish for investors. High levels of consumer confidence (above 100) have correlated with positive returns from the S&P 500.”

As I have discussed many times previously, the stock market rise has NOT lifted all boats equally. More importantly, the surge in confidence is a coincident indicator and more suggestive, historically, of market peaks as opposed to further advances.

As David Rosenberg, the chief economist at Gluskin Sheff previously wrote:

‘For an investment community that typically lives in the moment and extrapolates the most recent experience into the future, it would only fall on deaf ears to suggest that peak confidence like this and peak market pricing tend to coincide with each other.”

However, that confidence may be short-lived as “CEO Confidence” is near historic lows. As we covered in our previous analysis, this divergence should not be dismissed. A quick look at history shows this historical relationship between these two measures of confidence. The divergence is seen every time prior to the onset of a recession.

Notice that CEO confidence leads consumer confidence by a wide margin. This lures bullish investors, and the media, into believing that CEO’s really don’t know what they are doing. Unfortunately, consumer confidence tends to crash as it catches up with what CEO’s were already telling them.

What were CEO’s telling consumers that crushed their confidence?

“I’m sorry, we think you are really great, but I have to let you go.”

Warning 2 – All Hat, No Cattle

For those of you unfamiliar with Texas sayings, “all hat, no cattle” means that someone is acting the part without having the “stuff” to back it up. Just wearing a “cowboy hat,” doesn’t make you a “cowboy.”

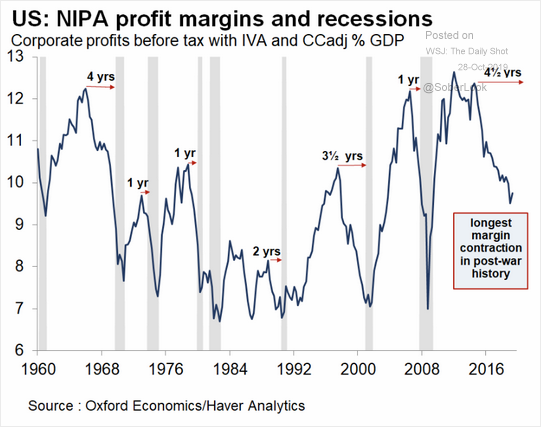

One of the problems for the “bulls” currently is that while asset prices are hitting record highs, profit margins aren’t.

In other words, investors, in their rush to “be long the market,” are paying ever-higher prices for each dollar of profit being produced. The problem, of course, is falling profit margins, not surprisingly, have preceded recessions and bear markets.

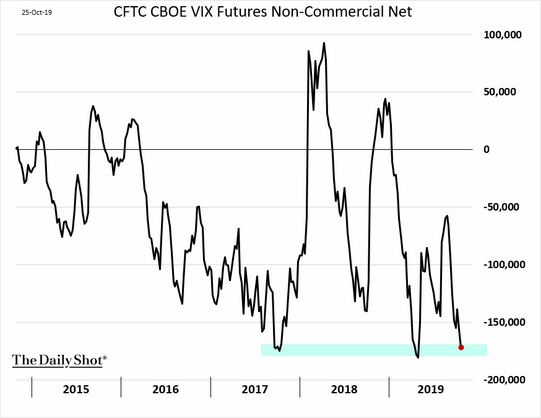

We will discuss valuations more in a moment, but the important point here is that investors are increasingly taking on “risk,” without consideration for the consequences. As shown, below speculators are now extremely “short volatility” which suggests there is no fear of a correction. Unfortunately, for the bulls, this has typically been a pretty reliable contrarian indicator.

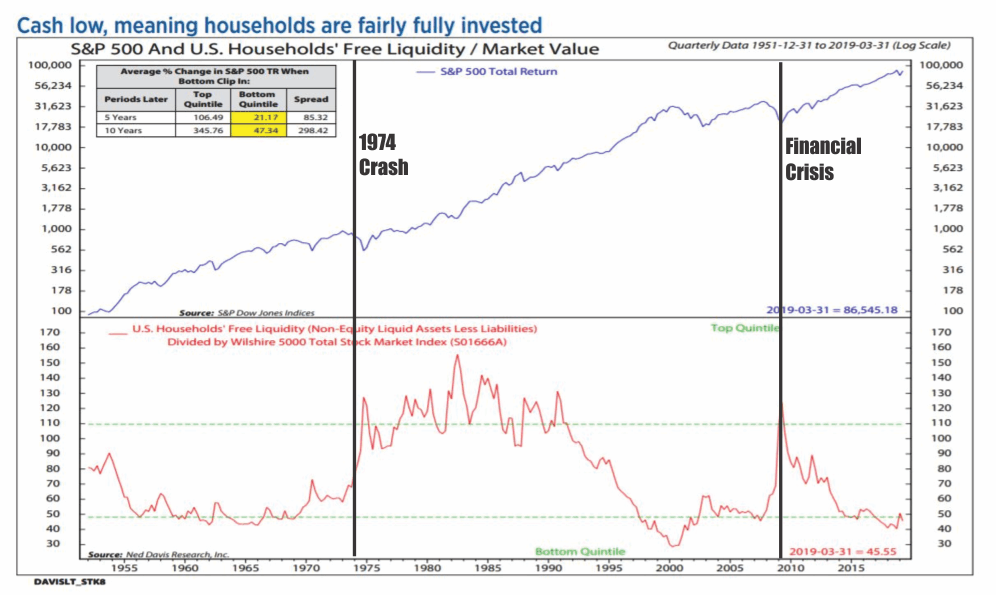

Much of the existing “complacency” stems from the belief the Fed will continue to lower interest rates and provide ongoing support for asset prices. After all, this is what happened as the Federal Reserve kept interest rates suppressed after the financial crisis. However, the difference between now and then is that individuals are currently fully invested in the financial markets.

“Cash is low, meaning households are fairly fully invested.” – Ned Davis

In other words, the “pent up” demand for equities is no longer available to the magnitude that existed following the financial crisis which supported the 300% rise in asset prices.

While investors may want to believe asset prices can only go higher, this is the very basis of the “Greater Fool Theory.” At some point, someone, is going to be left holding the bag.

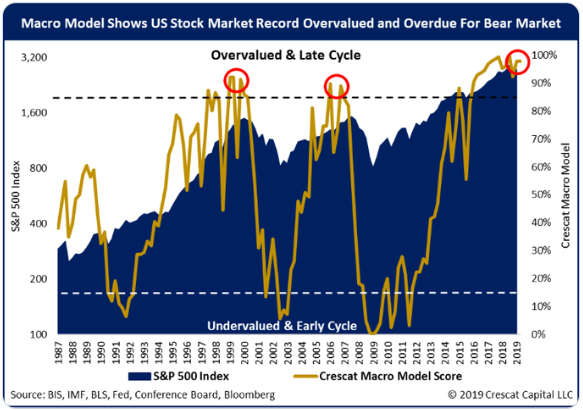

Warning 3 – Valuations

With the global levels of over-valuation of stocks and bonds, combined with excessive optimism, and leverage as noted above, such has set the stage for exceedingly low returns over the next decade, or longer. As our friends over at Crescat Capital recently noted, valuations are anything but “cheap.”

What happens next should be obvious: unless one assumes that the laws of economics and finance are irreparably broken; a deep recession and a market crash are inevitable, especially after the longest central bank-sponsored bull market in history.

However, in the short-term, valuations, as discussed previously, are a poor market timing device for investors. However, from a long-term investment perspective, valuations mean a great deal as it relates to expected returns.

With earnings estimates being revised lower, economic growth remaining weak, and high levels of complacency, the importance of valuations should not be readily dismissed.

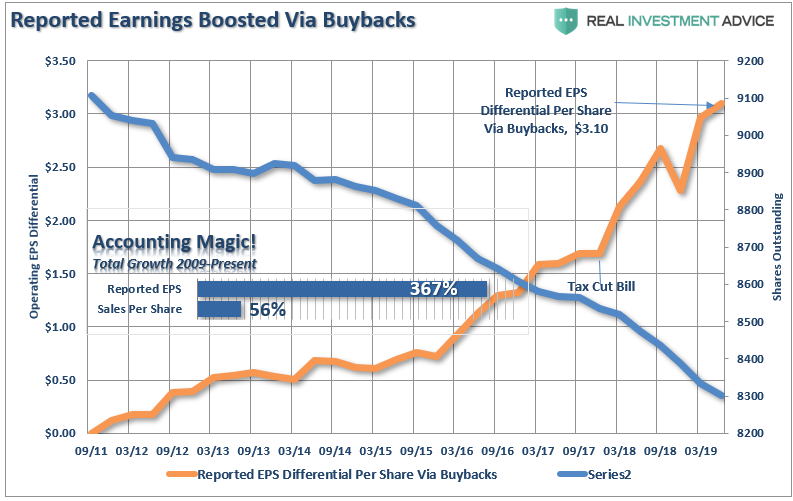

Warning 4 – Share Buy Backs

We have discussed the issue of “share buybacks” numerous times and the distortion caused by the use of corporate cash to lower shares outstanding to increase earnings per share.

“The reason companies spend billions on buybacks is to increase bottom-line earnings per share which provides the ‘illusion’ of increasing profitability to support higher share prices. Since revenue growth has remained extremely weak since the financial crisis, companies have become dependent on inflating earnings on a ‘per share’ basis by reducing the denominator.As the chart below shows, while earnings per share have risen by over 360% since the beginning of 2009; revenue growth has barely eclipsed 50%.”

The problem with this, of course, is that stock buybacks create an illusion of profitability. However, for investors, the real issue is that almost 100% of the net purchases of equities has come from corporations.

The problem is that corporate spending binge may be coming to an end. Via Goldman Sachs:

“Corporate buybacks are ‘plummeting’ as companies tighten their purse strings, and it could have a big impact on the market, Goldman Sachs warned in a note to clients.

In the second quarter, S&P 500 share buybacks totaled $161 billion, about 18% less than the first quarter, the firm found. The amount spent on buybacks this year is down 17% from a year earlier.

For 2019, total buybacks will drop 15% to $710 billion, and in 2020 they see a 5% decline to $675 billion.”

While this may not sound like much, it suggests that a primary support for higher asset prices is being removed. Of course, if a recession sets in, share repurchases could easily cease altogether.

If They Don’t “Buy & Hold” – Why Should You?

Of course, these are just “warning signs.” None them suggest that the markets, or the economy, are immediately plunging into the next recession-driven market reversion.

But they are warning signs nonetheless. Past experience suggests that future returns are likely to be far less than historical averages suggest. Furthermore, there is a dramatic difference between investing for 30 years, and whatever time you personally have left to your financial goals.

While much of the mainstream analysis suggests you should “invest for the long-term,” and “buy and hold” regardless of what the market brings, that is not what professional investors are doing.

The point here is simple. No professional, or successful investor, every bought and held for the long-term without regard, or respect, for the risks that are undertaken. If the professionals are looking at “risk,” and planning on how to protect their capital from losses when things go wrong, then why aren’t you?

“We Made Mistakes”: Boeing CEO’s Senate Testimony Released Before Today’s Hearing

Boeing’s CEO is set to appear before the Senate Commerce committee today to address the controversy surrounding the two fatal 737 Max crashes that took the lives of 346 people. According to Bloomberg, Chief Executive Officer Dennis Muilenburg will also address new allegations that the company withheld safety information from regulators subsequent to the crashes, a story we first reported on about two weeks ago.

He will be the first official from Boeing to testify publicly, and the company’s storied history and now-tarnished reputation (not to mention Muilenburg’s job) may hang in the balance.

Muilenberg’s upcoming testimony, released by the company on Monday, states: “We know we made mistakes and got some things wrong. We own that, and we are fixing them. We have developed improvements to the 737 Max to ensure that accidents like these never happen again.”

Notably absent from his testimony is elaboration on how the company’s design and testing broke down. However, lawmakers at a second hearing at the House of Representatives, scheduled for Wednesday, are expected to raise the issue.

Representative Peter DeFazio, an Oregon Democrat who is chairman of the Transportation Committee, said that Boeing engineers concluded that the 737 Max faced “potential catastrophe” if the safety feature implicated in the crashes activated for just 10 seconds without pilots taking notice.

DeFazio asked: “Now, that was never clearly communicated to the FAA, as far as we can tell. Was that intentional withholding or unintentional?” He made it clear that the embattled CEO will face “stern questioning”.

DeFazio asked: “How did you design an airplane with a single point of failure wired to a safety critical catastrophic system? How could that ever happen? Why did it happen? What happened to your company?”

The trip to Capitol Hill comes just about one year after the Lion Air crash that occurred in the Java Sea off the coast of Indonesia. Muilenburg visited the Indonesian embassy in Washington to meet with the ambassador and pay his “respects to those lost aboard,” the company said.

Of course, it was just months after the Lion Air crash that an Ethiopian Airlines plane also crashed, slamming into a field and causing a massive controversy around the 737 Max and the plane’s MCAS system, which was triggered by erroneous sensor readings in both crashes.

Muilenburg is expected to say of the 737 Max that: “…it will be one of the safest airplanes ever to fly…” when the flying ban on the model is lifted.

But Senators will have their chance at Muilenburg first.

Senator Ted Cruz is expected to focus on how the accidents happened to begin with. Cruz had previously asked: “What went wrong on the regulatory process? Why did they sign off on a training system where the pilots aren’t told about this new operation that could endanger the system? And how can we fix it? How can we make it better?”

Senator Roger Wicker, a Mississippi Republican and the Commerce Committee’s chairman, says he thinks there will be a legislative response to the testimony. He said: “I think there’ll be some statutory fixes. Is the plane ready to go, and then what mistakes were made and what’s to prevent them from happening in the future.”

Muilenburg, meanwhile, admits that Boeing did a “poor job” of explaining the flight control function to pilots after U.S. regulators had agreed to omit the MCAS system from the plane’s flight crew operations manual, at Boeing’s request.

Muilenburg will say: “Our airline customers and their pilots have told us they don’t believe we communicated enough about MCAS — and we’ve heard them. Boeing has worked with airlines and pilots to test its redesigned software and offer feedback on training and educational materials.”

U.S. lawmakers are considering changes to current laws that allows the FAA to deputize employees of aircraft manufacturers, like Boeing. Even though the FAA was involved in the early stages of approving Boeing’s MCAS system, the company was left to perform much of its own oversight. As the system evolved, the software became more capable of making “aggressive nose-down movements”, which was cited as the cause of the Lion Air crash by the Indonesian National Transportation Safety Committee.

DeFazio is also targeting legislation that would limit the ability of companies like Boeing to to make changes to existing aircraft without having to recertify them from scratch. This could wind up adding costs and time to the approval of new aircraft, like Boeing’s 777X, and addresses the fact that the 737 Max was certified as an “amended version” of earlier models dating back to the 1960’s.

Richard Aboulafia, an aviation consultant, blames the crashes on decades of deregulation and funding constraints.

He concluded: “The government has a lot to answer for, too. This is the close cousin of people who monitor water-quality in Flint. There needs to be a broader debate about providing resources to regulatory agencies.”

Record Rally Fizzles As Fed Meeting Begins, Investors Look For Reasons To Keep Buying

After the S&P hit a record on Monday – just as the Fed was set to cut rates for the 3rd consecutive time for reasons unknown – and world stocks hovering near a 15 month high underpinned by optimism over a U.S.-China trade deal after Trump said on Monday he expected to sign a significant part of a trade deal with China ahead of schedule but did not elaborate on the timing, S&P 500 futures edged lower, and European market slumped into a sea of red led by the FTSE 100 and telecom shares, while tech names dropped after Alphabet earnings missed.

Google parent Alphabet meanwhile slipped after missing analysts’ estimates for quarterly profit even though revenue growth topped expectations. A mixed bag of earnings also offset some of the chipper mood on European bourses, with the Stoxx 600 easing 0.4% after six straight sessions of gains, with energy producers among the biggest laggards. BP Plc shares declined as the driller said it’s unlikely to raise its dividend this year.

The European losses followed a mixed performance in Asia, where stocks gained for a fourth day, with materials and health care sectors advancing, following a rally in the U.S. equities that pushed the S&P 500 Index to a record. Japan’s Nikkei rose 0.4% to reach a 2019 high, while Shanghai stocks dropped after a warning against speculation on blockchain-related stocks depressed trading (one day after blockchain stocks soared). India’s Sensex Index rose the most and China’s Shanghai Composite Index being the laggard. India’s stock market reopened after a holiday and jumped on earnings optimism. Japan’s Topix Index closed at its highest level since Dec. 3. China shares retreated after a two-day gain, dragged by with Agricultural Bank of China and China Life Insurance Progress in U.S.-China trade talks helped boost risk-on sentiment in the region. U.S. President Donald Trump said the U.S. is ahead of schedule to sign a big portion of the China deal.

The U.S. trade representative also said Washington was studying whether to extend tariff suspensions on $34 billion of Chinese goods set to expire on Dec. 28, but analysts cautioned that trade tensions were far from over. “It isn’t yet clear that an interim deal that kicks trade worries down the road would be sufficient to allay concerns about the geopolitical, economic, earnings, and policy backdrop,” Mark Haefele, CIO at UBS Global Wealth Management.

“President Trump’s announcement of a Chinese commitment to buying $40–50 billion of U.S. agricultural products appears unrealistic – U.S. exports to China peaked at just $26 billion in 2012, when prices were much higher.”

With the S&P already at all time highs, investors are struggling to find new reasons to buy and extend the record-breaking rally in stocks. Optimism on the China trade front from President Donald Trump is aiding the bull case, and an anticipated Fed rate cut on Wednesday adds fuel. Still, recent data has come in mixed and while corporate earnings are topping estimates on average, the bar has been set low.

“What we’ve had happening in markets in the last few weeks is a lifting of that perceived uncertainty” about U.S.-China trade and Brexit, with central bank easing providing a lift, Sue Trinh, a global macro strategist at Manulife Investment Management, told Bloomberg TV. “The real risk is that we’re seeing a boost to asset prices but no real uptick in the real economy,” she said.

In rates, with markets in wait and see mode for Fed and trade developments, bond yields inched lower. Yields on Japanese 10-year bonds hit the highest since June and their Australian counterparts jumped almost nine basis points, while peers in the U.S. and Germany halted a surge that’s lasted several days. Germany’s benchmark 10-year bond yield hovered just below three-month highs hit on Monday, when yields across the single currency bloc rose sharply after the European Union granted Britain a Brexit extension.

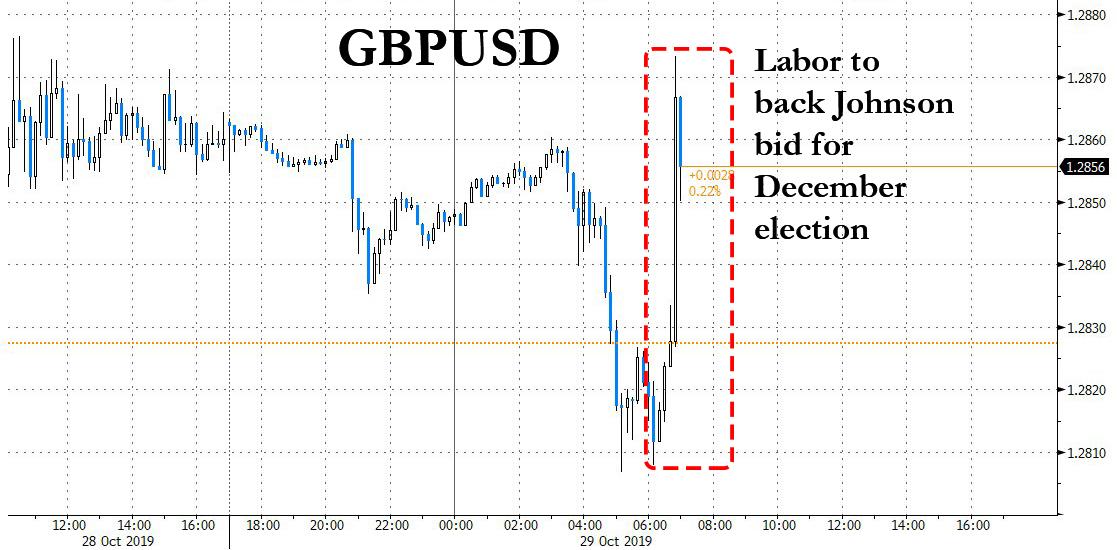

Bonds regained some of previous session’s losses, with Treasuries bull-flattening and European sovereigns firmer. Treasury futures retreated from near session highs as U.K. pound rallied on a report that opposition Labour party will support PM Johnson’s proposal for an early election; Yields on two-year Treasury notes were treading water after hitting four-week highs on Monday at 1.668%.

Investors are still looking forward to a likely rate cut from the Federal Reserve on Wednesday, though the outlook was less clear beyond that (and Jefferies expects the Fed to surprise markets by not cutting this week at all, instead saving its firepower for December). “We expect the Federal Reserve will cut rates this week and possibly once next year, as insurance against a broad economic slowdown,” BlackRock’s chief fixed income strategist, Scott Thiel, said in a note to clients. The futures market has another 50 basis points of cuts priced in by June. Central banks in Japan and Canada also meet this week, with talk the former might ease further if only to prevent an export-sapping bounce in its currency.

The shift from safe harbors saw the yen weaken slightly, with the dollar standing at 108.89 yen after having reached its highest in three months. It was eyeing a key technical level at 109.31. The euro edged up to $1.1095 and was little changed against a basket of currencies at 97.782. The Bloomberg Dollar Spot Index advanced in run-up to Fed decision and U.S. jobs data.

As shown above, the pound first extended losses vs. G-10 peers, with PM Boris Johnson still struggling to schedule a general election, before spiking on news Labour supports a December election.

Oil held below $56 a barrel after Russia said it’s too early to talk about deeper output cuts, casting doubt on the ability of OPEC and its allies to balance supply against a deteriorating demand outlook. Spot gold hovered at $1,493 per ounce after having pulled away from last week’s top around $1,517.

Expected data includes the August Case Shiller report, October consumer confidence and September pending home sales. Meanwhile the BoE’s Carney is due to speak while as for earnings, the highlights include MasterCard, Merck, Pfizer, BP, GM and Amgen.

Market Snapshot

S&P 500 futures little changed at 3,034.50

STOXX Europe 600 down 0.4% to 397.57

MXAP up 0.5% to 162.50

MXAPJ up 0.2% to 521.68

Nikkei up 0.5% to 22,974.13

Topix up 0.9% to 1,662.68

Hang Seng Index down 0.4% to 26,786.76

Shanghai Composite down 0.9% to 2,954.18

Sensex up 1.6% to 39,887.04

Australia S&P/ASX 200 up 0.07% to 6,745.42

Kospi down 0.04% to 2,092.69

German 10Y yield fell 1.4 bps to -0.346%

Euro down 0.2% to $1.1083

Italian 10Y yield rose 5.1 bps to 0.662%

Spanish 10Y yield fell 1.5 bps to 0.292%

Brent futures down 0.5% to $61.24/bbl

Gold spot up 0.1% to $1,494.36

U.S. Dollar Index up 0.1% to 97.84

Top Overnight News

Boris Johnson is pushing for an election to unlock Brexit after failing for a third time to trigger a snap poll. He remains doggedly determined to secure a third general election in a tumultuous four years. On Tuesday, he will try again to persuade reluctant members of Parliament

House Speaker Nancy Pelosi moved the Democrats’ impeachment inquiry of Trump into a new phase Monday that signals the public soon will get a look at the witnesses and evidence being assembled to build a case against the president

China’s third-quarter slowdown continued into October, with only a few signs of stabilization evident amid the weakest pace of expansion in almost 30 years

New Zealand’s Treasury Department warned the finance minister that S&P Global Ratings could remove its positive outlook on the country’s AA credit rating following the government’s so-called Wellbeing Budget, which ramped up social spending, a document obtained by Bloomberg shows

Consumer prices in Tokyo rose at the same pace in October even after a sales-tax hike, underscoring the challenge the Bank of Japan faces in stoking inflation as it prepares for a review of price strength later this week

Oil held below $56 a barrel after Russia said it’s too early to talk about deeper output cuts, casting doubt on the ability of OPEC and its allies to balance supply against a deteriorating demand outlook

PBOC skipped open-market operations again Tuesday, effectively draining 250 billion yuan from the financial system as funds come due. Fiscal spending at the end of the month will offset maturities, it said in a statement

Global finance and banking chiefs used an investment forum in Saudi Arabia to renew a warning that central banks have run out of firepower to fight the next economic downturn. Billionaire hedge-fund founder Ray Dalio said the global economy was facing a “scary situation”

Macquarie Group Ltd. is cutting about 100 equity research and sales jobs in London and New York, according to people familiar with the situation

Asian equity markets trade mixed as the region just about took impetus from Wall St where the S&P 500 and NASDAQ 100 notched record highs after US-China trade optimism was further fuelled by comments from US President Trump that suggested a signing of the phase 1 deal could be ahead of schedule. ASX 200 (U/C) was lifted at the open although some of the gains were later faded amid losses in commodity stocks due to lower oil prices and after the precious metal gave up the USD 1500/oz level, while Nikkei 225 (+0.5%) briefly reclaimed the 23000 milestone for the first time in over a year as it benefitted from a more favourable currency. Conversely, Hang Seng (-0.4%) and Shanghai Comp. (-0.9%) were the laggards despite the current backdrop of heightened trade optimism, as participants digested a slew of earnings and after the PBoC refrained from liquidity operations which resulted to a substantial CNY 250bln liquidity drain. Finally, 10yr JGBs tracked the losses in T-notes amid gains in stocks and with the Japanese benchmark at a yearly high, although some of the losses were recouped following a predominantly stronger than previous 2yr JGB auction results.

Top Asian News

Hedge Funds Fight for Asia Talent by Boosting Bonuses, Training

Aramco to Trade on Saudi Exchange on Dec. 11, Arabiya Says

Forget Zero Fees, Robots. One Broker Doubles Down on Humans

HSBC’s Quinn Says Economics of Europe ’Do Not Work’ for Banks

European equities have drifted lower after a relatively uninspiring open [Eurostoxx -0.3%] following on from a mixed APAC. Bourses are broadly in the red and remain choppy with no clear underperformer, albeit the region remains cautious ahead of this week’s risk events. Sectors are mostly in negative territory with the exception of Healthcare, which is buoyed by Fresenius SE (+4.5%) and Fresenius Medical Care (+5.8%) after earnings topped analyst estimates. On the flip side, the energy sector bears the brunt of softer energy prices coupled with overall downbeat numbers from oil-giant BP (-2.2%) who reported a 41% drop in Q3 net profits due to lower upstream earnings, softer oil prices, maintenance and weather impacts. Individual movers are largely earnings orientated, Grifols (+3.2%) benefit following firm earnings coupled with a EUR 5.3bln refinancing programme whilst to the downside, Stora Enso (-8%) shares plumbed the depths after disappointing earnings in which the Co. cited weak Q4 demand, thus peers Smurfit Kappa (-0.5%) and Mondi (-0.3%) initial fell in sympathy but has since trimmed losses. Finally, Swedbank (-3.8%) sunk after Estonian Financial Inspector and Sweden’s FSA opened sanctioning cases regarding the Co’s alleged money laundering. Looking ahead to US earnings, Dow listed Merck & Co (2.1% weighting) and Pfzier (0.9% weighting) which may have follow-through effects to European peers.

Top European News

MorphoSys Drops Most Since January On Trial Discontinuation

Swedbank Faces Bigger Risk of Fines as Watchdog Weighs Sanctions

Salvini Could Be Back to Shake Up Italy Sooner Than You Think

LVMH’s Bid For Tiffany Puts Pressure on Rivals to Respond

In FX, GBP – The Pound was initially precarious after the latest Parliament rejection of a motion to hold a GE on December 12 and ongoing wrangle to find an alternative date that might garner enough backing between Downing Street and those opposition parties that are likely to vote in favour of a snap poll. However, Labour subsequently giving their support to a December General Election has generated Sterling strength with Cable now firmer on the day with a high circa 1.2870 thus far.

USD – Sterling weakness and some contagion has nudged the DXY a tad closer to 98.000 ahead of more US data and day 1 of the October FOMC meeting that is widely expected to culminate in a 3rd 25 bp rate cut, but probably highlight ongoing divergence between Fed policy-makers resulting in less clarity over forward guidance.

EUR/CHF/NZD/CAD – All softer vs the Greenback, as the single currency remains top heavy around 1.1100, but underpinned ahead of Fib support at 1.1065, while the Franc continues to pivot 0.9950, Kiwi straddles 0.6350 and Loonie meander either side of 1.3050.

AUD/JPY – Bucking the overall trend, albeit marginally and also largely rangebound awaiting this week’s big events that kick off from Wednesday. The Aussie is still outpacing is US and NZ peers as Aud/Usd hovers around 0.6850 and Aud/Nzd just shy of 1.0800, but not deriving much impetus via comments from RBA Governor Lowe broadly reaffirming the on hold for now with an easing bias stance. However, looming CPI data could well be influential ahead of housing metrics on Thursday and PPI the following day. Elsewhere, the Yen has pared some losses from a test of 200 DMA support at 109.06 and decent option expiry interest from 109.00 to 109.10 (1.6 bn) even though Japan Post Insurance is eyeing less JGB holdings in the October-March period.

NOK – The Norwegian Crown is underperforming and only just holding off fresh record lows vs the Euro circa 10.2575 amidst softer crude prices and Norges Bank rhetoric underlining that rates are likely to remain unchanged for the entire forecast horizon, or coming period to quote Nicolaisen verbatim.

EM – The Rand has rapidly depreciated in wake of outlines of the SA Government’s plan for Eskom that did not include debt restructuring and propelled Usd/Zar up sharply towards 14.7200 vs near 14.5300 at one stage.

In commodities, WTI and Brent are softer this morning but once again not by any significant magnitude trading with losses of less that USD 1/bbl at present. News flow for the session thus far has again been light though this is likely to pick up from tomorrow via data and Central Bank meetings, including FOMC. For the rest of the session the main highlight will be tonight’s APIs which previously printed a build of 4.51mln and was notably not corroborated by the subsequent EIA metrics showing a draw of 1.69mln. Elsewhere, source reports note that Saudi Aramco is to announce the price range on November 17th and begin an IPO subscription on December 4th, aiming to trade on the Saudi Market from December 11th. Further, Nigeria’s new Energy Minister was on the wires this morning, albeit provided little by way of new substance. Elsewhere, gold prices remain tentative within a tight range, as is usually the case ahead of the Fed’s monetary policy meeting; however, the metal has just seen a modest sell off. Meanwhile, copper trimmed some of yesterday’s losses, again on the lookout for risk events. Finally, Dalian iron ore futures ended the day lower by 1.7% amid China demand woes.

US Event Calendar

9am: S&P CoreLogic CS 20-City MoM SA, est. -0.1%, prior 0.02%; 20-City YoY NSA, est. 2.1%, prior 2.0%

10am: Pending Home Sales MoM, est. 0.8%, prior 1.6%; NSA YoY, est. 3.55%, prior 1.1%

DB’s Jim Reid concludes the overnight wrap

I got home last night to watch the latest big U.K. Parliamentary vote and found my 4yr old daughter hogging the TV and watching “Frozen”. Given the gridlock at Westminster at the moment this seemed pretty apt. There is a reasonable chance the ice will melt today though as the U.K. government reacted to not getting the necessary 2/3rds of Parliament vote for a General Election on December 12th under the FTPA by suggesting they will propose a single line bill today for an election on the same date. This will only require a simple majority.

The Lib Dems and SNP have already indicated that they would support a vote for December 9, so it seems like the two groups are just haggling over the exact date and details at this point. The opposition parties prefer an earlier poll to ensure that students are more readily able to vote and to further ensure against Johnson bringing his WAB to another vote before the election. The Government conceded last night that they wouldn’t progress the WAB before an election but trust is so low that there might need to be a way of guaranteeing this before the two smaller opposition parties agree to it. The main opposition Labour Party are seemingly opposed to the election but it wouldn’t surprise me if they voted for it if the other two parties found a way to support it. It would be bad optics to be opposed when all other main parties backed it. Even though Labour’s official position was to abstain last night 38 MPs still voted against it. So by this time tomorrow we could have an election date…. but then again it’s easily possible we don’t.

Away from Westminster and over in markets, with the distraction of the big macro events of the week not kicking in until tomorrow onwards, there was a new record high for the S&P 500 to get excited about. Indeed the index took out the previous July high to close 0.45% above it and +0.56% higher on the day – the fifth positive day in the last six. Actually since the October 8th close we’ve had 10 positive days out of 14, including each of the last four sessions. At the start of this three-week rally, three positive catalysts coincided: Johnson and Varadkar held their positive bilateral meeting; Chair Powell announced that the Fed would resume securities purchases to grow its balance sheet; and the US and China agreed on “phase one” of their trade deal. That trifecta of positive developments has certainly underpinned the recent rally. We certainly need the data to catch up now to justify the strength.

Back to yesterday and it was the tech sector which really led the charge after the NASDAQ rose +1.01%. It’s not quite back at the July record highs just yet but yesterday’s move puts it within 0.05%. Meanwhile, the NYSE FANG index nudged up +1.02 % and the trade-sensitive semiconductor index rose +1.75%. That is a +6.41% move over the last 3 sessions for semiconductors, the best stretch since July. Prior to this, the STOXX 600 closed up +0.25% which means the index has closed higher for 6 consecutive sessions. The last time it did that was back in July as well.

Credit markets also had a decent day with US HY spreads -3.5bps tighter. The flip side of the risk off move was a decent selloff across sovereign bond markets. Indeed 10y Treasuries sold-off +5.1bps to close at 1.846% while 10y Bunds closed up +3.0bps at -0.332%. It was the end of July that we last saw Bunds back at these ‘lofty’ levels, which was also the last time that 20-year bond yields were positive, though the whole curve is still currently negative out to the 20 year tenor. Similarly, gold was down -0.82% while safe haven currencies also broadly underperformed, with the yen down -0.29% to its weakest level since June. Argentinian assets were pressured following the weekend election results, with the benchmark MERVAL index down -3.90% while yields on 10-year international bonds rose +95.0bps. Finally, bitcoin rose another +10.02% to take its two-day move to +26.52%, the most since May after the China blockchain headlines we mentioned this time yesterday.

Dictating the US tempo once again were trade headlines, this time the positive snippets from President Trump about the US being “ahead of schedule” to sign a deal. Some more idiosyncratic stock specific news also played a part. Of note was a +4.28% gain for AT&T following a board reshuffle and announcement to pay down debt. Microsoft climbed +2.46% after it won a $10 billion government contract to provide cloud computing services to the defense department. Its main competitor for the contact, Amazon, saw shares gain +0.89%, lagging the broader tech move.

Back in Europe, ECB President Draghi’s last week at the helm started with his final scheduled remarks at an honorary farewell ceremony in Frankfurt. He once again call for coordinated fiscal stimulus in the euro area. In front of the heads of government from Germany, France, and Italy, Draghi said that “we need a euro-area fiscal capacity of adequate size and design: large enough to stabilize the monetary union (…) uncoordinated policies are not enough.” By the end of the week he will handoff the institution to Christine Lagarde, who has also called for fiscal policy to support monetary efforts in recent years.

Meanwhile, after yesterday’s surge in China’s blockchain related stocks after comments by Chinese President Xi Jinping, the People’s Daily is carrying a commentary this morning saying that “The future is here for blockchain, but we need to stay rational.” This came as more than 70 tech shares surged yesterday by the daily limit in Shanghai and Shenzhen.

This has perhaps helped Chinese and Hong Kong’s bourses to trade lower this morning with the Shanghai Comp (-0.43%), Shenzhen Comp (-0.27%) and Hang Seng (-0.46%) all down. The Nikkei (+0.43%) is trading higher while the Kospi (-0.11%) is lower. As for FX, most Asian emerging market currencies are trading up this morning on trade deal optimism with the Chinese yuan up +0.14% to 7.0584 while the South Korean won is leading the advances by gaining +0.51%. 10y USTs yields are up +1.2bps, with 10y JGBs also up +1.6bps to -0.124% – the highest level since June this year. Elsewhere, futures on the S&P 500 are trading flattish.

Meanwhile, after markets closed last night, Alphabet shares fell -1.63% after profits fell year-on-year and missed expectations by around 10%. Much of the miss was due to higher capital spending, as the company focuses on expanding its cloud computing and machine learning business lines.

Switching play and coming back to the elections in Germany over the weekend, our economists highlighted in their note yesterday that the results have increased the probability of an early GroKo demise, but the team still think that the status quo forces are more likely to prevail; meaning that the GroKo treaty will be the ultimate arbiter in case of (more likely) conflicts. Calls from within the SPD to move to the opposition will not fall silent, but the SPD does not really have strong incentives to leave the coalition and trigger new elections, given their weakness in current polls. See our colleagues’ full summary here .

In other news, with the big data releases reserved mostly from tomorrow onwards – including payrolls on Friday – the warm up prints yesterday didn’t really move the dial. That said the advance goods trade balance in the US did provide a bit of food for thought following a narrowing in the deficit to $70.4bn in September from $73.1bn in August. That included drops in both imports and exports, with the latter down around 3% yoy. This should be a small negative for the FOMC statement on Wednesday given weakness in exports growth. Elsewhere, wholesale inventories were down surprisingly last month (-0.3% mom vs. +0.2% expected) while finally the Dallas Fed manufacturing survey was weak in October, printing at -5.1 (vs. +1.0 expected). That’s the weakest since July although it’s worth noting that the future expectations index did improve.

Prior to this, in Europe the September M3 money supply data showed a slowdown of money creation from 5.8% to 5.5% yoy. Credit growth also slowed and our economists noted that this resulted in the credit impulse turning negative for September having been in positive territory since April 2019.

To the day ahead now, which this morning includes October consumer confidence in France and September money and credit aggregates data in the UK. This afternoon in the US we have the August S&P CoreLogic house price index data, October consumer confidence and September pending home sales. Meanwhile the BoE’s Carney is due to speak while as for earnings, the highlights include MasterCard, Merck, Pfizer, BP, GM and Amgen.

Cable Spikes As Labour Backs Johnson’s Bid For December Election

After weeks of uncertainty surrounding whether the opposition would join with Boris Johnson to end the Brexit impasse by calling for a general election this year, a deal has finally been reached, and it looks like Johnson will get the 2/3rds majority he needs to dissolve Parliament and call for elections.

Cable, which had been under pressure Tuesday morning as the greenback rallied, spiked on the news, to trade at $1.2840, compared with $1.2807 earlier in the session.

Labour finally capitulated and agreed to back Johnson, with leader Jeremy Corbyn agreeing to another embarrassing U-turn. Corbyn said his No. 1 condition was that a no-deal Brexit be off the table (this is already the case thanks to the Benn Act), Bloomberg reports.

Does this mean the election is a sure thing? Not quite. Rather, a period of squabbling over the timing of the vote is about to begin, as different parties have expressed support for different dates.

There’s also the issue of opposition support for keeping settled EU citizens on the electoral register.

Is a December GE now locked on? Not quite yet. I’m told Labour will back amendments to put settled EU citizens on the electoral register. IF SNP/LDS do too, the Govt could yet pull the bill… so they may not.

A marathon session of debate in Parliament is now about to begin. Cabinet minister Jacob Rees-Mogg said the government wants the election bill to pass all House of Commons stages on Tuesday, meaning that the debate over the bill could continue “until any hour.”

Beijing Bars Student Activist Leader Joshua Wong From District Council Race

In the latest Beijing-backed crackdown on the Hong Kong pro-democracy movement and its leaders, many of whom have increasingly faced arrest and rumors about lengthy prison terms, Joshua Wong, the student activist who emerged as a leader with international profile back in 2014, has been barred from running for Hong Kong’s District Council.

In a Tuesday letter, Wong was informed that his candidacy in the District Council elections had been declared invalid in accordance with the Basic Law, Hong Kong’s constitution. In a separate statement, which didn’t name Wong, officials said support for Hong Kong self-determination was inconsistent with the law.

This is how Joshua Wong is disqualified to be elected today, 29th, Oct, 2019.

The Hong Kong government just don’t care the world seeing how brutal they stripe the right of being elected from a ordinary citizen. pic.twitter.com/S9sZNzWSez

In a response, Wong blamed the Hong Kong government for kowtowing to Beijing. He slammed the “politically driven” decision, another example of the government curbing the liberties of every-day Hong Kongers, according to SCMP.

“The ban is clearly political driven,” he said. “The so-called reason is judging subjectively on my intention to uphold the Basic Law. But everyone knows the true reason is my identity – Joshua Wong is a crime in their mind.”

“I have never actively advocated independence as an option, but she twisted and wrongly interpreted my remark,” he said, adding that Beijing had clearly exerted great pressure on Hong Kong officials, demonstrated by the original returning officer taking sick leave and its mouthpiece People’s Daily calling him an “independence leader”.

Wong believed his advocacy of the Hong Kong Human Rights and Democracy Act in the United States was probably the core reason of the ban in Beijing’s mind.

“But they have to pay the price in the international community…my disqualification will only trigger more people to take to the streets and vote in the coming elections,” he said.

Wong also said he would consider challenging the decision after November’s district council elections.

“Under the Basic Law, the allegiance requirement does not mention district council in the legislation,” Wong said. “So how much power or legal basis does a returning officer of the district council – which is a consultative body – have to carry out political vetting? This is critical.”

According to WSJ, this year, the district council seats up for election make up almost all of the city’s 18 local councils. Wong is part of a wave of pro-democracy candidates who are challenging establishment members, hoping the anti-government atmosphere will help them win big gains.

District council members effectively act as liaisons between the community and the legislature. They act as representatives on issues of government programs and public facilities. But they don’t make laws, or have any kind of veto power. The HK legislature isn’t due to hold an election until next year.

District councilors also hold close to 10% of the seats on the 1,200-member election committee that chooses Hong Kong’s leader.

Wong has been intensely persecuted since emerging as the leader of the 2014 Umbrella Movement protests. Like the contemporary pro-democracy fever, the 2014 movement also began as something else: Wong and several of his classmates took to the streets to hand out flyers objecting to new classes in Hong Kong’s public schools intended to indoctrinate students about the Communist Party. That later merged with the backlash to Beijing’s election tampering, and Wong, still in high school at the time, found himself the leader of a student army of protesters.

He has been refused passage in several Asian countries, including Malaysia, as local governments were wary of angering Beijing. He has been repeatedly arrested – recently by a gang of plainclothes-wearing police, who grabbed him and hurried him into an unmarked police van.

Interestingly, not all of the pro-democracy activists were banned from the race. Eddie Chu Hoi-dick, a pro-democracy lawmaker previously barred from running in a village representative election due to his support for “separatism” (something that Wong is also now being accused of) was given the all-clear to run in the elections.

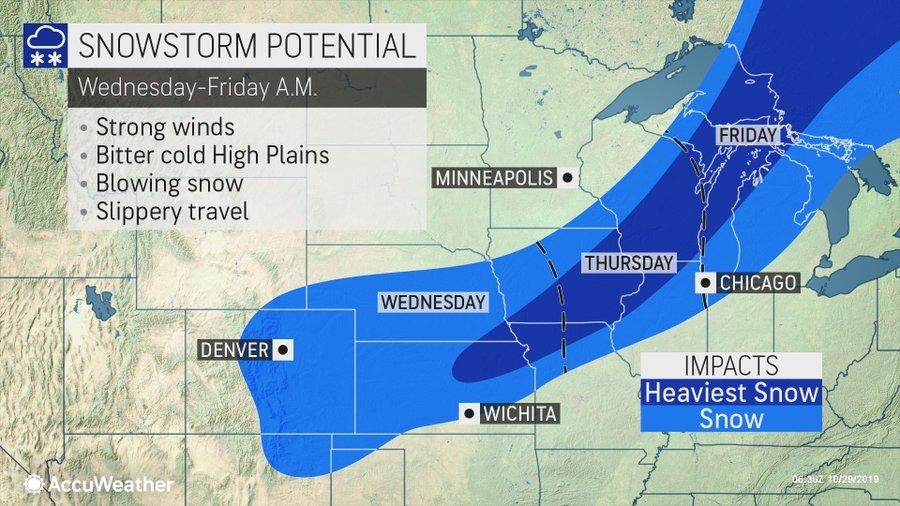

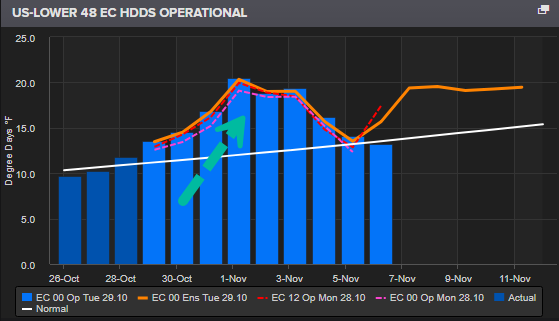

Winter Blast To Dump Heavy Snow Across Rockies, Plains, Midwest This Week

Several major snowstorms are expected to dump heavy snow across the Rockies, the Plains, and into the Midwest this week as cold Arctic air blankets those regions in the last days of October.

The potential for cold into November? It’s complicated.

The Weather Channel is reporting “a southward plunge of the jet stream from the Rockies into the central US has entrenched a pipeline of arctic air over those regions. Two weather systems tapping into that cold air are producing snowfall as they track from the Rockies to the Plains and into Midwest.”

The National Weather Service (NWS) has issued winter weather alerts across the northern and central Rockies and central High Plains.

Denver-Boulder corridor, located in northern Colorado, has been placed under a winter storm warning through Wednesday morning. The region could see 6 to 12 inches of snow on through Tuesday night.

From Tuesday evening into Wednesday, snow will be seen in the Central Plains, Midwest, and the Rockies.

The Weather Channel said an area of low pressure will form near the Great Lakes on Thursday, could produce the first accumulating snow for northeastern Missouri into eastern Iowa, western and northern Illinois, and southern Wisconsin.

With a plunge in the jetstream, Central and Midwest heating degree day (HDD) indexes, a measurement designed to quantify the demand for heating a building, have moved above trend through the end of the month into the first week of November.

A similar pattern in HDD is also seen in the lower-48, suggests that energy demand is increasing as the winter season begins.

NatGas spot prices have soared nearly 14% in six sessions.

The former CEO of trucking company Scania has warned that Sweden is heading towards civil war due to uncontrolled mass immigration.

In an interview with Swebbtv, businessman Leif Östling said that the arrival of so many new migrants who have failed to integrate into Swedish society is creating a fertile ground for violent unrest.

“We’ve taken in far too many people from outside. And we have. Those who come from the Middle East and Africa live in a society that we left almost a hundred years ago,” he said.

Explosions and grenade attacks have skyrocketed in many Swedish cities, with much of the unrest being blamed on migrant gangs. Sexual assaults and violent crime is also on the rise.

Östling underscored problems with integration by highlighting his own experience running Scania, where around 90 out of a hundred Somali migrants hired to work for the company were fired or left because they were unable to arrive on time or work in teams.

Östling believes that the “knowledge transfer” necessary for migrants to cope in Swedish society could take a generation to accomplish.

The businessman said he hoped that the country’s problems could be fixed within 10 years but if not, civil war could ensue, necessitating that the military be called out to deal with violent unrest in migrant areas.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

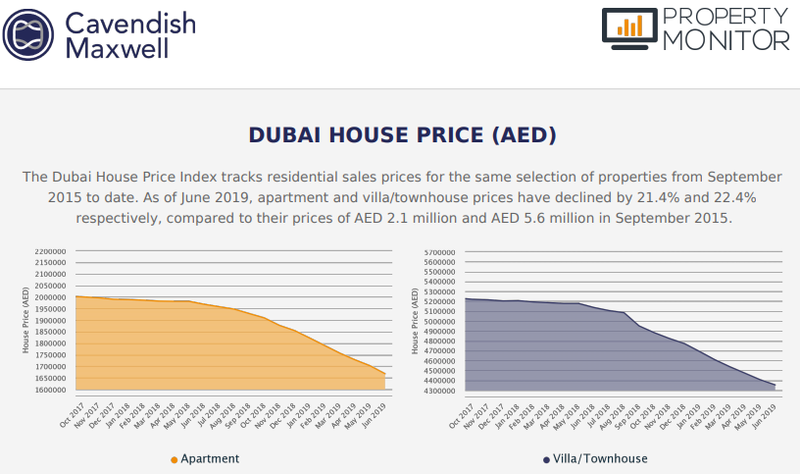

Halt All New Home Construction In Dubai Or Face Economic Disaster, Top Builder Warns

Damac Properties, one of the largest property developers in Dubai, warned over the weekend about an imminent economic crisis, festering in Dubai’s real estate market.

Damac Chairman Hussain Sajwani told Bloomberg that a collapse in the housing market is nearing unless new home construction is halted for several years. “Either we fix this problem, and we can grow from here, or we are going to see a disaster,” Sajwani said.

Sajwani is the latest real estate executive to voice his concern that Dubai’s housing market is on the brink of disaster.

The slump in the city’s housing market has been underway for the last five years. Prices have tumbled by more than 30% in the same timeframe.

Property broker JLL estimates 30,000 new homes will be constructed this year, which is more than twice the demand.

Despite the requests to halt all new home sales, Sajwani said Damac would complete 4,000 homes in 2019 and another 6,000 in 2020. The developer is expected to reduce new builds and concentrate on selling inventory next year.

“All we need is just to freeze the supply,” Sajwani said. “Reduce it for a year, maybe 18 months, maybe two years,” he said.

Sajwani predicted oversupplied markets would crash home prices.

He said if prices drop further, then it would trigger a tsunami in non-performing loans that would cause contagion in the banking industry.

“The domino effect is ridiculous because Dubai’s economy relies on property heavily,” he said.

Standard and Poor’s warned last month that economic growth in Dubai will trend lower through 2022 due to depressed oil prices, a global synchronized slowdown, turmoil from the US and China trade war, and geopolitical uncertainties in the Middle East.

The international rating agency said deterioration in real estate and tourism sectors had weighed heavily on the domestic economy.

Housing data from Cavendish Maxwell’s Dubai House Price Index via Property Monitor showed home prices plunged to their lowest levels in June, not seen since the 2008 financial meltdown.

Damac’s shares have crashed more than 77% in the last 26 months, mirroring the downturn in the overall housing market.

If oversupplied conditions aren’t corrected in the coming quarters, Sajwani’s prediction of a market crash could unfold in Dubai in 2H20.

A long night of suffering has kept one of the richest continents on the globe in a state of virtual dark age for over a century. Although the age of science has given humanity the means to access the highest standards of living in world history, 2019 has seen 15 000 children die of preventable deaths every day (illness, starvation and murder) with half occurring in Sub Saharan Africa. In a world of advanced energy technology, only five of 54 African countries have access to 100% electrification and all are North African.

Africa’s dark situation was never due to simplistic terms like “corruption” or “incompetence”, nor was Africa ever “culturally incompatible” with western technology as some racists have taught in social science classes. The truth is that Africa was never given true independence as is popularly believed. Sure there was nominal independence, but the economic independence needed to become a sovereign country was never granted by the empire.

This is why the growing presence of nations such as China and Russia on the continent are increasingly seen as beacons of hope for a new generation of Africans who recognise in this Eurasian alliance an opportunity to capture the future they were robbed of over half a century ago.

The Russian African Summit in Sochi

A watershed moment in this systemic change has occurred with the first Russia-Africa Economic and Security Summit in Sochi (Oct. 23-24) co-chaired by President Putin and Egypt’s President el-Sisi, featuring 50 African heads of State alongside 3000 representatives of business, government, and finance. This summit was the first of its kind, and followed hot off the heels of China’s first China-Africa Economic and Security Summit which was held in July 2019. In the past two years,40 African states have signed onto China’s Belt and Road Initiative which has scared many imperially minded technocrats in the west.

“We are not going to participate in a new ‘repartition’ of the continent’s wealth; rather, we are ready to engage in competition for cooperation with Africa, provided that this competition is civilized and develops in compliance with the law. We have a lot to offer to our African friends.”

While it does not have the same level of investments as China (which leads the world with $200 billion/year), Russia’s investments have quadrupled since 2009 now clocking it at $20 billion/year and growing with a focus on rail, energy diplomacy, education, culture sharing and military assistance. Russia is currently building Egypt’s first nuclear reactor in El Dabaa, and is negotiating with several other nations such as Ethiopia, Nigeria and Kenya to go nuclear which will end the policy of technological apartheid imposed onto Africa for decades. Russia has announced the construction of an Africa Center of Excellence and Nuclear Power in Ethiopia and the Russian Academy of Sciences announced branches opening up across Africa. A vital driver for development, Russian Railways is working to construct trans-border and intra-border rail in Ghana, Burkina Faso, Nigeria, Libya, Egypt and East Africa (just to name a few). During the summit, Russia announced a cancellation of a $20 billion African debt as an act of goodwill.

President Putin pointed out the elephant in the room when he said:

“We see a number of Western states resorting to pressure, intimidation, and blackmail against governments of sovereign African countries. They hope it will help them win back their lost influence and dominant positions in former colonies and seek—this time in a ‘new wrapper’—to reap excess profits and exploit the continent’s resources without any regard for its population, environmental or other risks. They are also hampering the establishment of closer relations between Russia and Africa—apparently, so that nobody would interfere with their plans”

Unlike the west, Russia has the advantage of having encouraged African development during the dark days of the Cold War and is thus infinitely more trusted than the west, whose positive attempts to genuinely help Africa develop (as seen under the leadership of John F. Kennedy, Italian Industrialist Enrico Mattei or President de Gaulle) ended with either assassinations or coups.

Some may call Putin’s words anti-west hyperbole, but a comparison of the quality of investments Russian vs American into Africa demonstrates the two opposing intentions referenced by Putin.

The Trap of Conditionalities

Where US Aid, the World Bank and IMF have poured billions of dollars into Africa over decades, standards of living, and stability of those recipient nations have only plummeted. This is the opposite result one would expect from such “generous” behaviour. Why?

The answer can be partly be found in the shift towards IMF/World Bank conditionalities which grew out of a monstrous paradigm shift that occurred in the 1950s-1970s. Where leaders such as Franklin Roosevelt and his ally Henry Wallace envisioned an industrialized Africa liberated from colonialism, the Bretton Woods instruments they created to provide long term low interest loans internationally were cleansed of anti-colonial leaders and replaced with deep state tools early in the Cold War ensuring that any credit issued would be tied to deadly conditionalities as exposed by John Perkins in his book Confessions of an Economic Hitman.

Under this neo-colonial formula, Africa was allowed to get money. But those dollars would no longer be “permitted” to be invested into genuine nation building or advanced technological progress as Patrice Lumumba, Kwame Nkrumah or Thomas Sankara intended. Only “appropriate technologies” such as windmills or solar panels were permitted. Small wells were ok, but major water/energy projects like hydroelectric dams or Great Manmade Rivers were not allowed. Certainly no nuclear power was permitted (unless you happened to be an apartheid state run by white racists of course). Oil drilling and mining investments were ok, but only if foreign companies like Barak Gold or Standard Oil did the work and none of the revenue or electricity benefited the people. Without the means of producing real wealth (defined as combination of material, intellectual and spiritual growth), Africa’s productive powers of labor collapsed with their sovereignty and the debts only grew.

Hysterical Neocons Lash out

It is no secret that just as China began outpacing the Americans in African investment in 2007. Rather than acting intelligently to increase genuine infrastructure funding as the Chinese had done, the US Deep State not only continued its outdated debt-slavery practices, but created AFRICOM as a military arm across the continent. Ironically AFRICOM’s presence coincided with a doubling of militant Islamist activities since 2010 with 24 groups now identified (up from only 5 in 2010) and a 960% increase in violent attacks from 2009-2018. Just as western lending has caused a pandemic of slavery, so too has western security forces only spread mass insecurity.

The fact is that the neo cons infesting the Military Industrial Complex have openly identified both countries as co-equal enemies to the USA and understand that this alliance represents an existential threat to their hegemony. Speaking at the Heritage Foundation last year, former National Security Advisor John Bolton said (without blushing):

“The predatory practices pursued by China and Russia stunt economic growth in Africa; threaten the financial independence of African Nations; inhibit opportunities for US investment… and pose a threat to US national security interests.”

His words were bolstered by acting head of AFRICOM Thomas Waldauser in Feb. 2019 “To thwart Russian exploitative efforts, USA AFRICOM continues to work with a host of partners to be the military partner of choice in Africa.”

Luckily for the world, Bolton and Waldauser were both flushed from their posts by an American President who has chosen to ally with Russia and China rather than risk World War III. However, the dangerous ideology and deep state power structure they represent is not yet defeated, and with Trump’s intention to pull troops out of Syria, these psychotic forces are as dangerous as ever.

Dio Mio! ‘Corruption-Fighting’ Italian PM Linked To Rogue Vatican Fund

Italy is hardly a stranger to financial horrorshows. Whether it’s fiscal mismanagement, blundering centuries-old banks loaded down with bad loans, a federal government too deep in the red, fears of a populist-backed parallel currency or the shadowy tendrils of the mafia tainting the country’s agri-export business.

And now, what appears to be serious financial corruption scandal has found a direct line to the Quirinal Palace.

So, what exactly is going on? Well, yesterday, the FT reported that a Vatican-backed investment fund that is under investigation by the Vatican authorities had hired Italian PM Giuseppe Conte to negotiate a deal.

Just weeks before Conte took office (for the first time), Conte, then a little-known Florence-based academic, was hired in May 2018 to provide a legal opinion in favour of Fiber 4.0, a shareholder group involved in a fight for control of Retelit, an Italian telecoms company.

The biggest investor in Fiber 4.0 was the Athena Global Opportunities Fund, which was constituted entirely by $200 million from the Vatican Secretariat. The Fund was owned and operated by Raffaele Mincione, an Italian financier.

The news of Conte’s involvement will likely attract more scrutiny of the Fiber 4 deal from the Vatican police. In fact, Conte’s involvement wasn’t widely known until the police raided the all-powerful Vatican’s Secretariat of State, the Church’s most powerful centralized bureaucracy and the source of all the financing for the Fiber 4.0 deal.

Conte

The Secretariat is currently under investigation over its involvement in several suspicious transactions, allegedly including this property deal, which inspired the initial raid mentioned above, according to the FT on Mondy.

In the property deal the Secretariat invested in a $143 million building deal in London’s Chelsea with money it held away from central Papal State funds in several Swiss bank accounts. The deal has raised concerns from Vatican investigators that the Secretariat may have been misusing hundreds of millions of dollars under its control, which have been donated to the poor by Catholics around the world.

Now, investigators that Conte, either unwillingly or willingly, helped paper over something similar.

In Conte’s deal, the fund was part of a consortium (Fiber 4.0) hoping to win control of a small Italian telecoms company called Retelit. Fiber 4.0 hired Conte in May 2018 as a “freelance legal expert” after the consortium lost a vote in April over a proposal to take over Retelit. It lost the vote to a rival company controlled by German and Libyan interests, which Conte apparently believed gave the, an opening.

Conte argued in the memo that the Italian government could step in and annul the vote using rules intended to protest “strategically important assets” (not dissimilar to the CFIUS deal review board in the board).

Once he finally took office, in June 2018, he did just that. However, a few months later, his maneuverings were reversed and he was fined for his conduct.

Conte is now trying his hardest to distance himself from that deal.

“Regarding the new facts reported by the Financial Times, it should be noted that Mr Conte only gave a legal opinion and was not aware of, and was not required to know, the fact that some investors were connected to an investment fund supported by the Vatican and now at the centre of an investigation,” Conte’s office told the FT.

This would be a most delicious irony: For Conte, whose reputation as an honest politician helped save his career when the Five Star-League coalition collapsed, to instead be felled by suspicions surrounding a possibly corrupt act mostly committed while he was still a civilian.