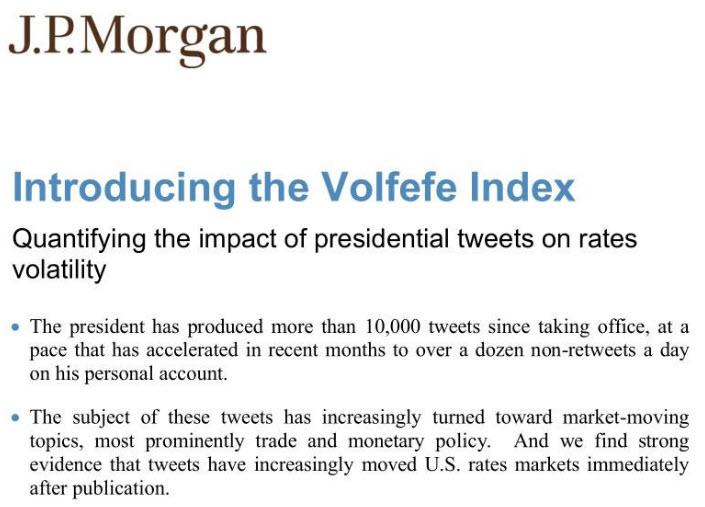

JPMorgan Launches “Volfefe Index” To Track Impact Of Trump’s Tweets On Market Volatility

Some time in the past 3 years, US capital markets – already rigged and broken beyond comprehension by central banks and HFTs – crossed over into the realm of absurdity, but it wasn’t until this Friday that we got official confirmation. That’s when JPMorgan came up with the “Volfefe Index” (remember Covfefe) to quantify Trump’s impact on rate volatility.

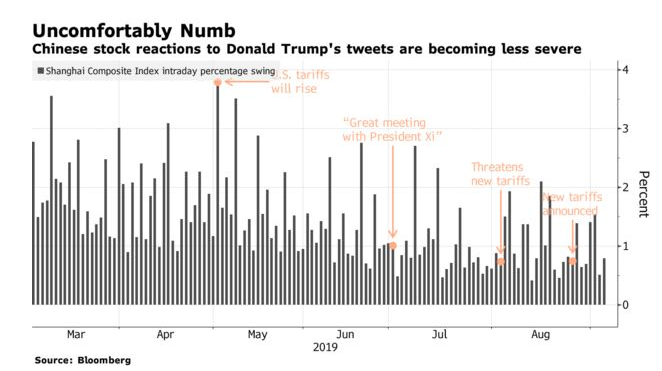

When it comes to Trump’s tweeting habit, there are two approaches. One can ignore them, as Asia is increasingly doing, or one can obsess over them and use them as the springboard for violent daily market reversals.

Commenting on the former, last week we said that is starting to ignore Trump’s tweets, for three reasons: First, China doesn’t have easy access to them, since the social media service is banned there; second, the President’s tweets often occur outside of Chinese trading hours, causing them to have less of an effect on Chinese markets than U.S. markets; Finally, the novelty simply seems to be wearing off.

Zhang Haidong, a fund manager at Jinkuang Investment Management in Shanghai said: “It’s pointless following him too closely — he might say something today and it will be a whole different story tomorrow. Trading off his tweets alone would be too volatile.”

Indeed, as the next chart shows, the Chinese stock market is becoming immune to anything the Trump twitter feed unleashes on the world.

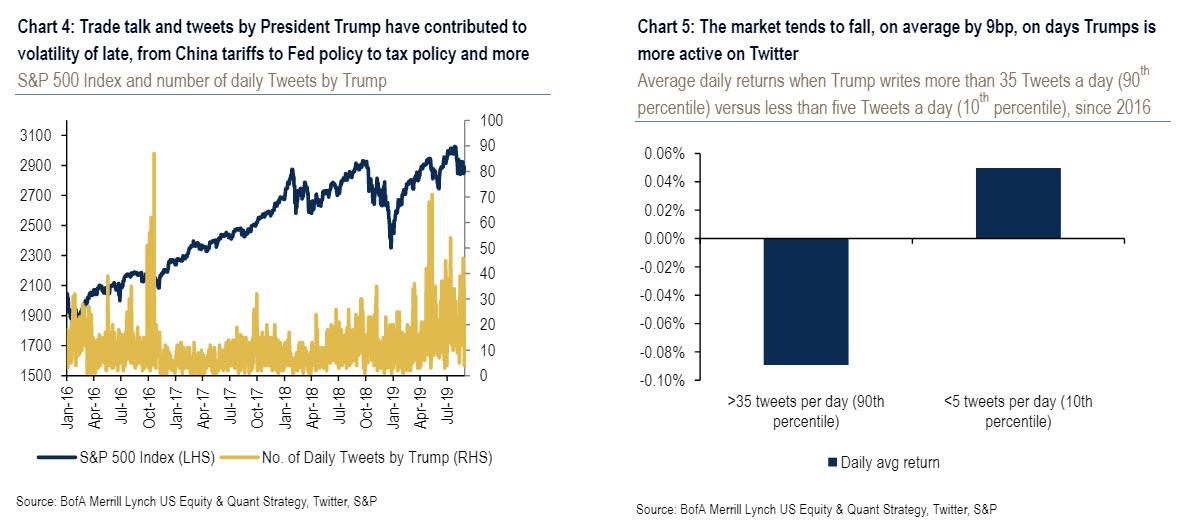

In the US however, it’s a different story, and Trump’s tweets carry as potent a punch on market volatility and stock prices as ever, especially since twitter is the venue where the president has announced two of his last trade escalations against China. Or perhaps it’s just reflexivity, as Trump tends to tweet up a storm whenever the market is dropping, in hopes of “tweeting” the market higher.

Whatever the arrow of causality, last week Bank of America found that since 2016, on days with more than 35 tweets (90th percentile) by President Trump, the market has seen seen negative returns (-9bp), whereas on days when Trump keeps it to less than 5 tweets (10th percentile), the market has posted positive returns (+5bp), both of which are statistically significant.

Fast forward to Friday when JPMorgan’s rates strategists decided to actually quantify the impact of Trump’s tweets on volatility in the bond market, and so the Volfefe Index was born.

Not surprisingly, JPM found that the index explains a measurable fraction of the moves in implied rate volatility for 2-year and 5-year Treasurys.

“This makes rough sense as much of the president’s tweets have been focused on the Federal Reserve, and as trade tensions are broadly seen as, first and foremost, impactful on near-term economic performance and, likewise, the Fed’s reaction to such developments,” wrote JPM’s analysts led by Munier Salem.

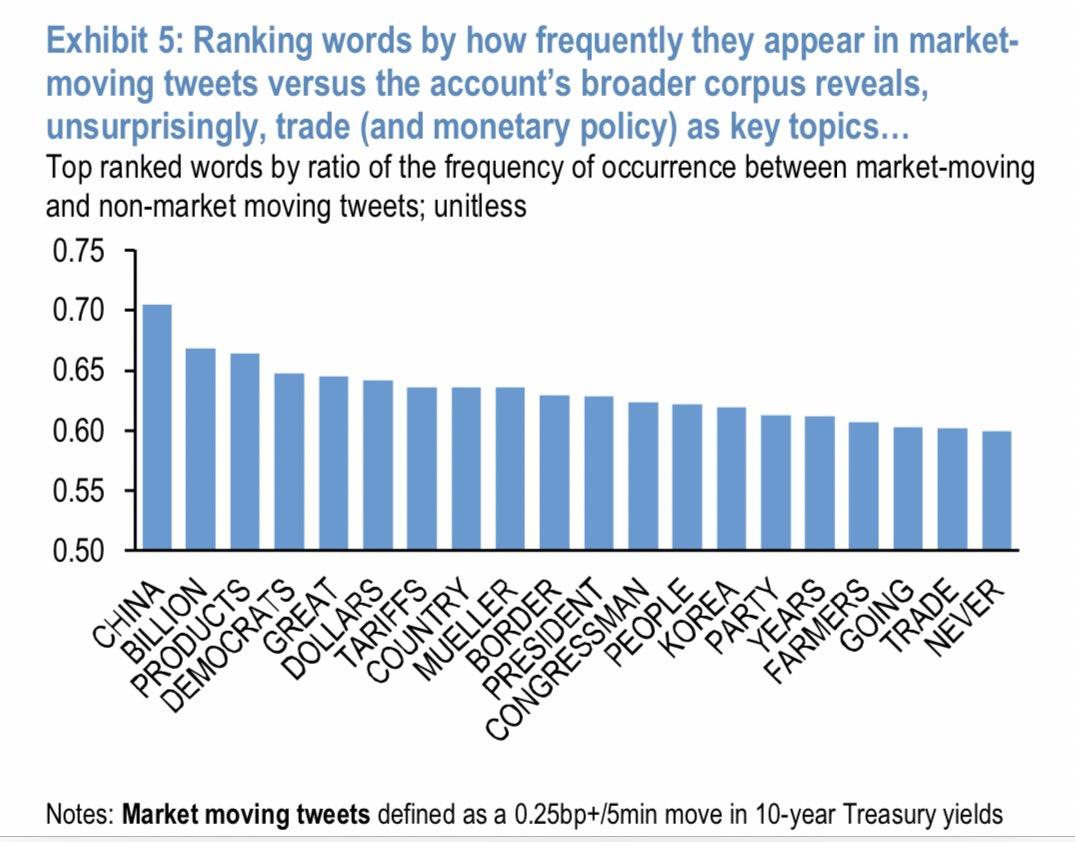

Besides his pet peeve, the Fed, which Trump believes is out to get him by not cutting rates faster (an assumption that was merely cast away as merely paranoia until Bill Dudley, like a total idiot, decided to insert his foot in his mouth and confirm that the Fed does indeed pick US presidents and monetary policy is used to influence presidential elections) Trump’s market-moving messages have also addressed trade and monetary policy, with key words including “China,” “billion,” “products”, “Democrats”, “great” and “dollars”…

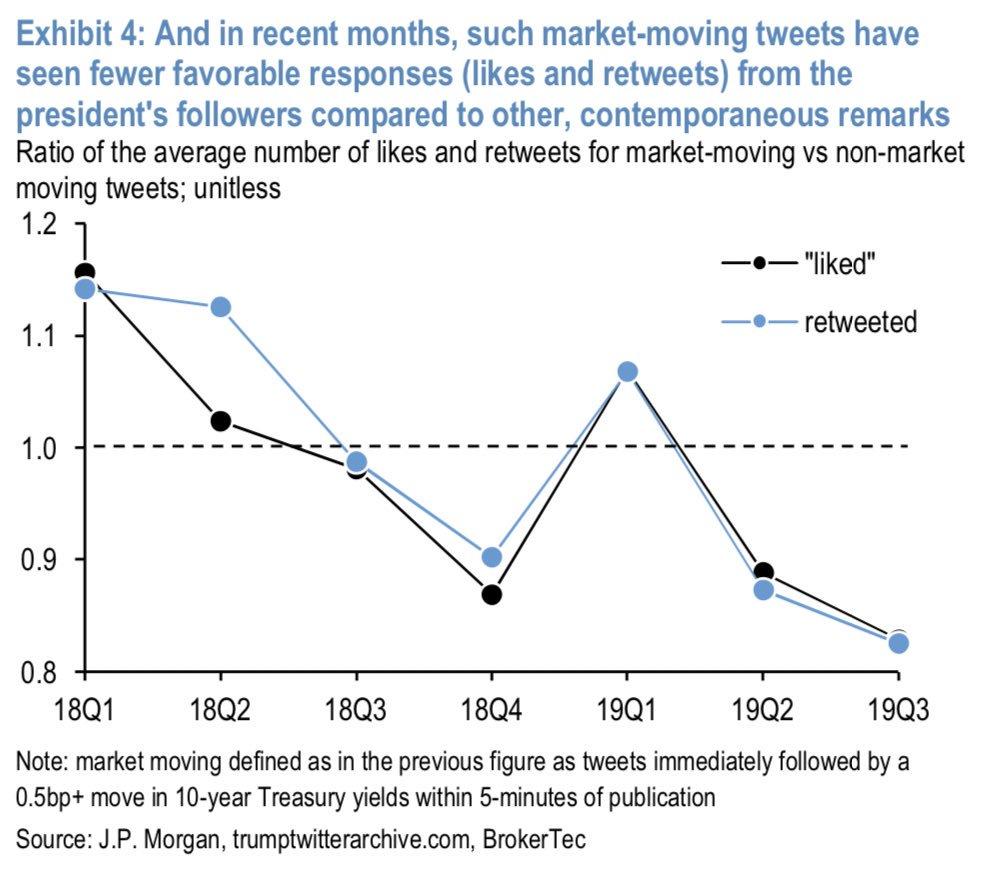

… although as JPM points out, these tweets are increasingly less likely to see “fewer favorable responses (likes and retweets) from the president’s followers compared to other, contemporaneous remarks.”

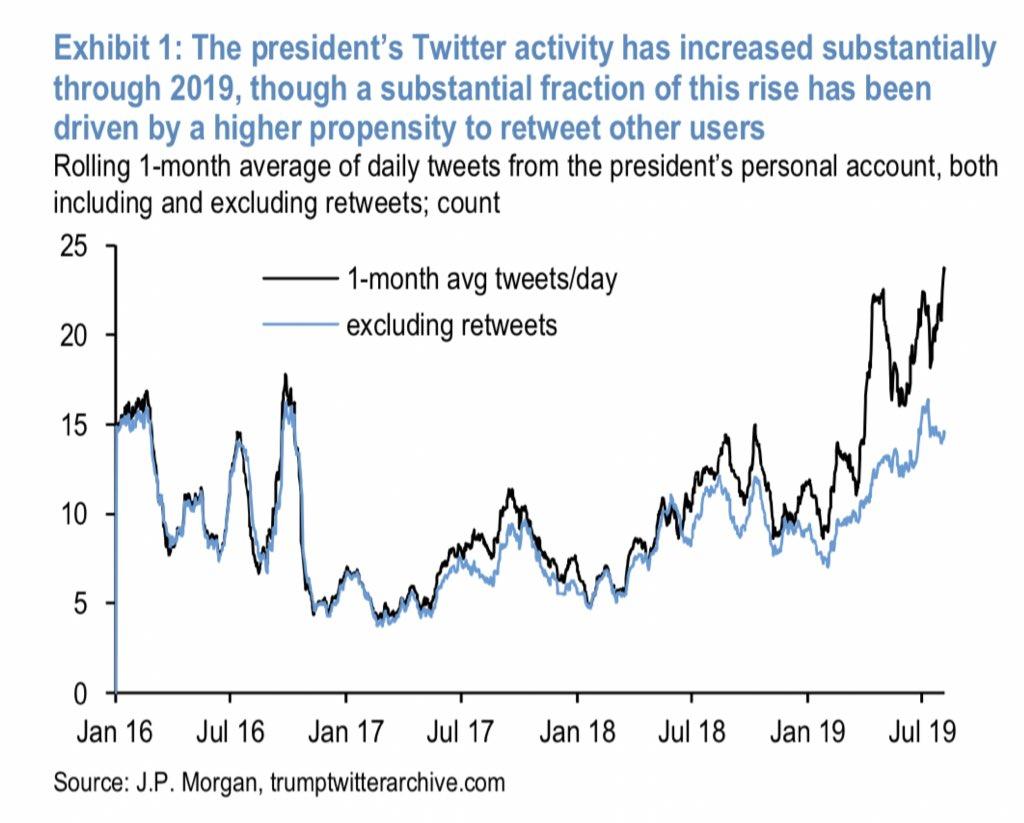

The good news is that there is more than enough data for any statistical model as over the past three years, since his election in 2016, Trump has averaged more than 10 tweets a day to some 64 million followers — roughly 14,000 total over that period associated with his personal account, of which more than 10,000 since taking office, a pace that has continued to accelerate and in recent months has peaked at over a dozen non-retweets per day.

Yet, as JPMorgan found, out of the roughly 4,000 non-retweets that have taken place during market hours from 2018 to the present, only 146 moved the market, although Trump’s market moving tweets have seen an increase in “dramatic fashion” of late, coinciding with a spike in volatility, JPM found.

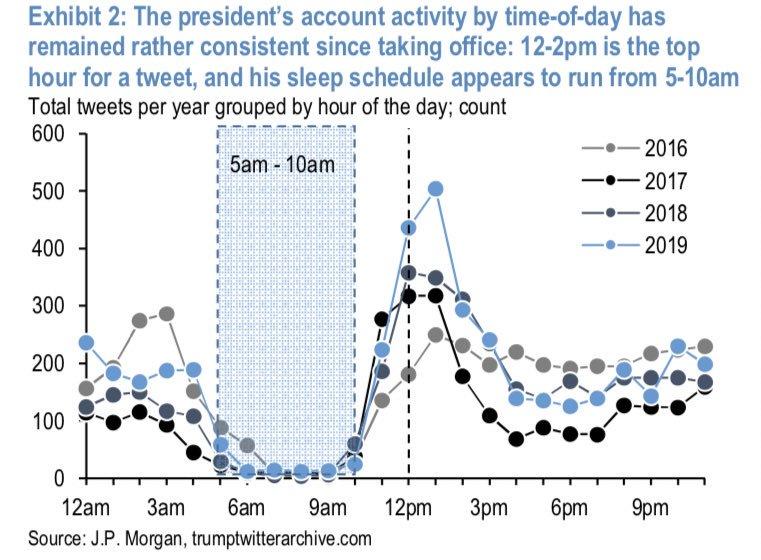

JPM also found that most of Trump’s tweets come in the two-hour block from noon to 2:00 pm, with a 1:00 pm tweet roughly three times as likely to arrive at any other hour of the afternoon or evening. One bizarre observation is that Trump’s 3:00 am tweets were more common than his 3:00 pm tweets, which is a pain for both US rates and equity futures markets, as overnight liquidity is especially dismal. And an interesting finding from Trump’s tweeting pattern: the president is presumably sleeping from 5:00 am to 10:00 as there’s a lull in tweeting activity during that time.

Finally, while there has clearly been a surge in overall twitter activity by the president, “a substantial fraction of this rise in activity comes from an increased propensity to retweet others”, JPM finds. Excluding these non-original tweets, the recent surge in presidential tweeting is far more timid.

JPMorgan’s conclusion: “the president’s remarks on this social medial platform have played a statistically significant in elevating implied volatility.“

Yet while a cottage industry of Trump Twitter experts has emerged in recent months, the reality is that even if Trump has elevated market volatility, it has yet to adversely impact the overall market, which remains 40% higher since Trump’s election, and roughly 30% since his inauguration, even if the S&P has gone almost nowhere in the past 12 months.

Tyler Durden

Sun, 09/08/2019 – 19:30

via ZeroHedge News https://ift.tt/2A4l40R Tyler Durden

{kind=link}