The pandemic has been devastating for the oil industry globally. Explorers suspended drilling, producers, idled wells, Big Oil majors put up assets for sale. But the world continues to need oil, albeit lower amounts of it than a year ago, and it will continue to need it.

Exploration is not dead. It is especially not dead in Africa – a hot spot in oil and gas before the pandemic.

The East Africa Crude Oil Pipeline

Earlier this month, French Total and the Uganda government signed an important deal, for the construction of a pipeline that will carry Ugandan oil to the Kenyan coast. Two weeks later, the presidents of the two countries signed their own deal about the $3.5-billion infrastructure.

The final investment decision on the pipeline is expected by the end of the year in a rare good sign about the future of oil demand. Uganda and Kenya are both newcomers on the oil scene with hopes to join the oil exporting community soon. If the construction of a $3.5-billion oil pipeline still makes economic sense for countries that are not among the wealthiest in the world, there may be some hope for oil demand.

The South African oil discovery

Africa Energy, a Canadian exploration company, said last week it expected to strike a lot of oil in an offshore block in South Africa with reserves that could exceed those of an earlier discovery made by Africa Energy and Total in the same block. Earlier this year, Africa Energy doubled its stake in the consortium exploring the block to 10 percent. Total is the operator. Africa Energy should announce the results of the drilling project by the end of next month.

The Luiperd prospect is the largest of five prospects in the offshore block 11B/12B in South African waters that have attracted explorers’ attention. Consortium members estimate the resources of Luiperd alone to be in excess of 500 million barrels.

What’s more important is that, according to Africa Energy, the Luiperd prospect offers as much as 80 percent of success—”unheard of in frontier exploration today,” the company’s chief executive Garrett Sodden told an industry conference. The entire offshore block has potential reserves of several billion barrels.

Drilling in Zimbabwe

An Australian company, Invictus, is meanwhile preparing to start drilling exploration wells in Zimbabwe, with the start date scheduled for October 2021. These would be the first oil and gas wells to be drilled in South Africa’s neighbour to the north—another country hopeful it will strike oil, which will boost its energy self-sufficiency.

The drilling project is seen to cot some $15 million, Africa Oil and Power reported last week, adding that it builds on promising results from earlier exploration conducted by Exxon. In the 1990s, Exxon identified an area that was highly likely to contain hydrocarbons but dropped the project because it was after oil and the area was more likely to contain gas. The government of the country, which is currently 100-percent dependent on exports for its energy needs, seems fine with gas, too. It is currently putting the finishing touches to a production sharing agreement with Invictus in case oil and gas are found.

The Gambian license

UK-based explorer PetroNor earlier this month received a 30-year drilling license from the Gambian government after an arbitration process concerning two offshore blocks. After the successful completion of the arbitration, PetroNor will have rights to explore just one of the blocks, with the other passing to an unnamed “major oil company”.

The new license is based on a new production-sharing framework developed by the Gambian government, which, according to PetroNor, is more favourable for explorers and producers. The company now has a year to decide if it wants to proceed with drilling in the offshore block.

Pandemic delays

Despite all the positive news from frontier regions in Africa, the continent has not been spared the fallout of the pandemic that destroyed a lot of oil and gas demand. Kenya’s government, for instance, said recently that Covid-19 had slowed down exploration in the Turkana region, which would delay Kenya’s ambitions to become an oil exporter until 2024, from an earlier plan to start shipping oil abroad in 2022.

The pandemic has also delayed exploratory drilling in Mozambique following the distribution of new blocks in a government tender. It was supposed to begin this year but “some adjustments” the pandemic necessitated have pushed the schedule to 2021-2022.

One of the biggest producers on the continent, meanwhile, is working on a new exploration strategy to boost its oil and gas reserves. Angola’s government earlier this month approved a plan, to take effect by 2025, that would see the country boost its exploration activities to increase recoverable reserves and make sure it produces at least 1 million bpd by 2040.

South Africa, on the other hand, has delayed a new oil and gas exploration and production bill that was supposed to be passed this year, again because of the pandemic. Now, the deadline for the approval of the bill has been moved to the end of the third quarter of 2021.

Overall, however, the picture appears to be better in Africa’s frontier oil regions than in legacy producing parts of the world.

via ZeroHedge News https://ift.tt/3i1ldFT Tyler Durden

French Officials Considering “Absurd” New Tax On Vehicles Based On Weight Tyler Durden

Fri, 09/25/2020 – 02:45

Pretty soon, there’s going to be no cars left to drive. Between California looking to phase out internal combustion engines by 2035 and France apparently now considering another tax on vehicles based on how much they weigh, it seems like the world is hell bent on assuring a future that’s replete with Ubers and public transit.

But regardless, the press to “save the planet” much push on. That’s why at the Convention Citoyenne sur le Climat (the Citizens’ Climate Convention) in June 2020, the idea of taxing vehicles by how much they weigh was raised. It is currently being considered by the French government, according to The Connexion.

Meanwhile – as is usual with government – the left hand doesn’t know what the right hand is doing. In May 2020, just one month earlier, the government was doling out an aid package of 8 billion Euros for the French car industry trying to boost production. The taxes by weight would have just the opposite effect.

The future of French automobiles

Luc Chatel, president of automobile association la Plateforme de la Filière Automobile (PFA) pointed out that the two policies obviously contradict each other and has asked for “stability” in decisions being made by government. Good luck with that.

He stated on French TV last week: “We cannot, three months after [the government announced its support plan], put in place a tax that will go against what we’ve been told.”

Taxe sur le poids des véhicules: “On ne peut pas mettre en place une taxe qui va à l’encontre de ce qui s’est dit il y a 3 mois” selon le président de la plateforme automobile

He called the tax “absurd” and continued: “The cars will benefit from a bonus for reduced CO2 emissions and a penalty [for their weight] at the same time. It’s ridiculous.”

Chatel predicts that 70% of vehicles in France will be affected by the tax.

And for France, it looks like the environmentalist agenda doesn’t stop with vehicles. “As well as taxing vehicles according to their weight,” the Connexion article says, “the 150 measures proposed by the citizens’ Climate Convention include changing the French constitution to highlight the importance of environmental protection, and introducing a new environmental crime called ‘ecocide’.”

via ZeroHedge News https://ift.tt/2RVhhvx Tyler Durden

When I last posted an article about Brexit in May I discussed how the convergence of a possible world trade organisation scenario with the EU and the Covid-19 lockdown measures would serve to exacerbate the economic strain that the UK is currently being subjected to. I argued that as the devastation brought about by the self imposed lockdown became more profound, not only would a WTO Brexit compound matters but it would also put further downward pressure on sterling and prove a harbinger for a significant spike in inflation over the coming years.

Four months on and a number of developments have since occurred. As I predicted, the transition period was not extended, meaning it will come to an end on the 31st December 2020. Shortly afterwards a cabinet office document of ‘worst case scenarios‘ was revealed that detailed what may happen should a no deal Brexit coincide with a ‘second wave‘ of Covid-19. One possibility raised was how the government could decide to deploy the military on the streets of Britain in the event of public disorder.

Earlier this month, with trade negotiations floundering, Boris Johnson announced that if a deal cannot be agreed by October 15th the UK will walk away and revert to WTO tariffs. Following on from this was his latest intervention came just days ago when he unveiled renewed Covid-19 restrictions on the population after a rise in those testing positive for the virus, just as the final rounds of Brexit negotiations are due to begin.

One aspect to pick up on here is how when addressing the nation this week, Johnson made clear that he would be prepared to authorise using the military to ‘backfill when necessary‘ should the police require more support to enforce restrictions. Johnson also told the House of Commons that he had the option to ‘draw on military support where required to free up the police.’

Johnson’s official spokesman had this to say on the matter:

This would involve the military backfilling certain duties, such as office roles and guarding protected sites, so police officers can be out enforcing the virus response.

This is not about providing any additional powers to the military, or them replacing the police in enforcement roles, and they will not be handing out fines. It is about freeing up more police officers.

So here we have both Brexit and Covid-19 being talked about as potentially escalating to the stage where the military could be called upon under the guise of helping to maintain social order.

From my perspective here’s why I think this should be taken seriously:

Before the original lockdown was implemented on March 24th, I saw first hand in my role as a supermarket worker how the usual lucid nature of shoppers rapidly gave way to palpable fear and hysteria. After weeks of wall to wall coverage on Covid-19 in the media, the threat of a national lockdown began to enter the narrative. People responded by rushing to buy up food and medical supplies. As a consequence supply chains were severely impacted with shelves lying empty for weeks on end.

This demonstrated to me one inescapable fact. As much as people claim to distrust the mainstream media, what it actually showed was just how many continue to rely on outlets like Sky, the BBC and daily newspapers in guiding their perceptions. Their relentless messaging was undoubtedly a driving influence over the behaviour of people leading into the lockdown.

What I witnessed was how the threat of being deprived of essentials triggered within people a survival instinct. After weeks of preparatory propaganda, they knew what was coming and were inspired to act. The UK’s ceremonial exit from the EU on January 31st was now no longer part of the news agenda. Months of discord over Brexit was consigned to history.

But here’s the problem – the UK did not leave the European Union in any meaningful way on January 31st. Nothing materially changed in terms of the relationship. When those in support of Brexit declared on the morning of February 1st 2020 that the sky had not fallen in, they were at best being disingenuous. This is primarily because the country remains a member of the single market and the customs union. The real point of exit, when the UK is due to vacate the institutions that make up the EU, is not set to happen until the end of 2020 when the transition period expires.

The arrival of Covid-19 rendered Brexit an afterthought. But with the end of the transition period less than 100 days away, this is no longer the case. People are beginning to think about Brexit again.

My worry is that the public response to a likely no deal scenario will be met in a similar manner to how fears over a national lockdown were met. Boris Johnson’s deadline of October 15th for a trade deal, which coincides with a European Council meeting, is quickly approaching, as is the threat of a second lockdown.

If Johnson keeps to his word and the 15th passes without agreement, the UK will declare their intention to move onto WTO tariffs come January 1st 2021. That would leave exactly eleven weeks before this became a reality. Plenty of time for the media to begin a campaign of fear based propaganda – centred around stories of food and medicine shortages – and for the government to promote a nationwide communications programme urging people to prepare for potential disruption.

Irrespective of the outcome of negotiations between the UK and EU, traders will face new customs controls and processes. Simply put, if traders, both in the UK and EU, have not completed the right paperwork, their goods will be stopped when entering the EU and disruption will occur. It is essential that traders act now and get ready for new formalities.

With Christmas approaching, I suspect that warnings such as this will once again trigger within people the same fear that they felt back in March. There are already some signs, albeit isolated, of people starting to stockpile.

But unlike six months ago, the British public now have more than Covid-19 to consider. On the one hand you have people observing social distancing rules, which were not a requirement during the first bout of panic buying. On the other are increasing concerns that supermarkets may soon see an upsurge in customer demand off the back of a potential second lockdown, supply chain disruption following a no deal Brexit and the yearly onslaught of Christmas shopping.

It seems obvious to me that the media would portray a ‘second wave‘ of Covid-19 and a disorderly Brexit as a two pronged threat to the public.

You can probably tell where I am going with this. If a second lockdown is implemented, I suspect it would occur in the weeks leading up to Christmas. As fears would mount over access to supplies and people began to pile into supermarkets to stock up, warnings would be abound that because of the uptake in custom people are failing to social distance resulting in the spread of the virus, which in turn would create a rationale within the media for a second lockdown. A economically ruinous lockdown that would largely be blamed on Brexit. And, of course, running beneath Brexit is the narrative of a rise in nationalism and protectionism, which global planners have cited as dangers to the post World War Two ‘rules based global order.’

If you put aside any ideological bias you may have over Brexit, you begin to see how a chaotic separation from the EU is beneficial to global planners. This is something I have discussed in numerous articles over the past couple of years. Central bankers speak of the ‘post Brexit architecture‘ in terms of the the future make-up of the global economic system. Most recently the World Economic Forum launched their ‘Great Reset‘ initiative, which includes plans for a global economic reset that would likely encompass the recomposition of currencies, the introduction of central bank digital currency and a desire to replace ‘failed institutions, processes and rules with new ones that are better suited to current and future needs‘.

One of those institutions just happens to be the World Trade Organisation, which was earmarked for reform back in 2018. The WTO would play the leading role in a no deal Brexit outcome, and if it is shown as being not up to the job then this strengthens the hand of global planners to either remodel or replace it entirely.

As I have long argued, the most vulnerable aspect to Brexit is pound sterling, both in terms of its value and its role as a global reserve currency. Brexit can and I think will play a part in global planners attempting to reconstruct the economic system in their own image. In that sense it is why I believe they want Brexit to happen and in as disorderly a way as possible. Chaos is often advantageous to globalists, not detrimental. Especially when they have already laid out their solutions through Sustainable Development and the Great Reset. All they need is a sufficient number of crises in order to position themselves as the benefactors.

via ZeroHedge News https://ift.tt/33Xrqxp Tyler Durden

A reader recently wrote me a long letter on how he feels about all this ‘Plandemic’ stuff. I thought it would be good to share it as there is so much in it which rings bells of truth for me…

[emphasis ours]

I’ve just woken up after reading ZeroHedge late into the night. I awoke with the conviction that Covid is being used to roll out a police state:

They know it’s not deadly, it’s no longer spreading and Lockdown is killing off the few small businesses which remain viable. Yet Boris now insists upon banning the assembly of more than 6 people. He has recalled some petty bureaucrats to act as street enforcers and requested people become snitches who report on their neighbours for any breaches of these guidelines. This automatically means we must now all fear our neighbours, or strangers who take our car number. How better to destroy the mutual trust upon which society is built?

Just think if one were to refuse to bend the knee. In Australia and Spain the police have been caught using excessive force against those not wearing masks. Intimidating isn’t it? I’m thinking I may have to start using one. Yet the science is clear – masks offer no protection.

So we know these new restrictions are not being driven by the authority’s concern for our health. And what is the difference between where we are now and making it normal for the police to come to your door and arrest you for a breach of their protocols? What is the difference between where we are now and an oppressive police state?

There is only one difference between now and full-on state oppression: A change in the Zeitgeist.

They need an event that will change the mood of the people – an event or a series of events that make us afraid of ‘them’. A psychological shock that will give the police the conviction that things are so bad ‘a little force is necessary’ to ensure things don’t get out of control. And then, magically, the current ‘temporary restrictions’ become state oppression. What could that game changer be?

Imagine this November: The US has 100 cities descending into what looks like the start of civil war as patriots turn out to stop Antifa burning down Middle America. Kamala Harris is calling for the army to ‘evict’ Trump because he refuses to leave the White House on the grounds that he won the popular vote while the mail-in ballots were fraudulent.

For the Brits, Brexit has caused problems at the ports – among other things some foodstuffs are not getting through. Germany’s economy has cratered after the EU stopped them exporting cars to the UK (Trumps already tariffed them), and the EU’s bank has insisted Germany let the 500 non-viable, medium sized biz (currently kept alive with emergency funding) go bankrupt.

Deutsche Bank collapses and this initiates a global banking crisis. Europe has no way of saving its banks as all the European economies are so damaged and 20% of workers have already been laid off. It’s a Greek style banking crisis on steroids. People are pulling out cash in the expectation of daily cash limits. Physical gold will have already disappeared from the market place. So any biz with money in the bank is frantically buying bitcoin in an attempt to avoid their working capital being ‘bailed in’.

The banks will have already pulled the plug on their most vulnerable customers – the airlines – so virtually no planes are flying. Dover is jammed up with lorries lining the approach roads. So no one can leave Blighty. And if you did, the emergency measures intended to pre-empt Covid’s Second Wave require you to be kept in quarantine at your destination. Locked down in a hotel, under military guard (as in NZ), for 4 weeks at your own expense and with frequent testing to ensure you are not a carrier. With full bio-metric data being collected and filed on an EU wide register. In practice this means that travel becomes so fraught that escape from your homeland is just about impossible.

You get the gist? November could be the end of world as we know it’ (TEOTWAWKI). But my point is this: Why are we looking at such a catastrophe if their goal is not a police state? No one destroys the globe’s economy and creates the conditions for a 10 year Greater Depression by accident. This has to be a planned, intentional destruction of much of global civilization.

The evidence is overwhelming. This civilization has been purposefully destroyed. Right now we’re in an unreal time (like the beautiful summer just before WW1’s carnage). It’s like Wiley E Coyote who has gone over the cliff, is still running but not yet started to fall. But when we fall, how will people react as they realize that they will never work again, never pay off the mortgage, never collect their pensions? If we have state oppression and economic chaos by Christmas then what will be the next stage of their takeover?

The world’s economy is already doomed. The already broken supply chains ensure it can only get worse. Once the derivative market goes, and banks can no longer fund the credit lines crucial for importers and exporters, then trade will collapse and thus food supplies cease.

It would seem to be inevitable that America is going to see more conflict as the Dems & Soros show no signs of wishing to abort their colour revolution. Maybe in 2021, maybe a year or two later, but there will come a time when a credit shortage leads to deflation. So the banks will print more and then rain down helicopter money which will lead to inflation. And then the currencies will start collapsing. Many people understand that this is inevitable. But what happens when people come to accept that money isn’t go to be worth the paper it’s printed on? And thus keeping a job may not be worth the danger of leaving your house or of leaving safety.

I summarise one of last night’s articles:

“the beasts of burden don’t rebel, they just no longer show up. Not showing up can take a number of forms: early retirement, sick leave, a demand to work halftime, a workers’ compensation stress leave, and of course, resignation and quitting as in: “take this job and shove it”. They slip noiselessly into the cracks and crevasses and once they’re gone, there’s nobody left to replace them.”

“As the Vital Few 4% realize the system no longer works for them and opt out, this will have an out-sized effect on the 64%, most likely urban dwellers, highly dependent on increasingly brittle, fragile services that depend on the Vital Few for their functionality. Think of London’s tube train drivers phoning in sick – ideology won’t matter.

Those dropping out may be Conservative or Progressive or they may have lost interest entirely in politics and all the other circuses that serve to distract the populace from the crises dissolving the glue that held the system together. “So I won’t get rich, that dream died a long time ago.” What I’m interested in now is getting my life back and getting the heck out of Dodge as things fall apart.”

The rich will escape to their holiday cottages. The poor will riot – but what then? As the social facade cracks, and the economic system breaks, there is neither a society nor an economy to fall back on. By Christmas it will be obvious that normality has gone for ever.

So what will ‘they’ do with millions of unemployed, frightened people? If ‘they’ leave the internet on then the people will start to organize – first politically – but when that doesn’t work, riots and then finally revolution. Turn it off and they will riot without being organized. Turn off phones and all hell will break out. Don’t turn them off and the kids will organize against the state – trash cars or burn down the local police station. Have you noticed how some police stations look like forts?

My point is that it’s very hard not to see ‘events’ hitting the fan this November. And once they do it’s very hard to see life ever going back to stability, let alone ‘normality’. Rather, there will be an overwhelming need to control {oppress} the population before they take over the state. But what do you do with millions of unemployed in a failed economy who are doomed to losing their currency, long term poverty and probably food shortages. There is only one thing ‘they’ can do. Kill them.

Ideally, for the elite, Covid’s Second Wave will have a higher morbidity rate. Enough to steadily reduce the population but not so fast they can’t be buried in plague pits. It would have to be bad enough to justify a harsh Lockdown but it’s difficult to see that being feasible without giving the people electricity, internet & food and the money to pay for it. And even then it’s only a temporary fix as Lockdown can’t last for ever. Permanent Lockdown would soon destroy the currency which will mean no electricity or food.

Maybe Covid-19 v1.0 was supposed to kill off more people but it failed. Or maybe it worked as intended – they didn’t want to risk killing off too many in case the Lockdown failed and we revolted. But I don’t see they have much choice now. ‘The Fourth Turning’ will be turbulent until 2025 and things won’t really be resolved until 2030. How are they going to manage us for another 10 years? How will they control us? Feed us?

They can start a war but no one is going to turn up. Fight a war for the elite? Use a gun to kill people you don’t know? That’s not going to happen. And they need to preserve the professional soldiers to ‘maintain the peace’ in the cities. So what options do they have but to release a more potent bio-weapon – nuclear war perhaps?

One of the scary things about working through ‘their’ options is that they don’t have many. Things have gone too far – they’ve destroyed the world’s economy. The system is stuffed. What are ‘they’ going to do with 2bn unemployed people. Even if there is enough food but the US has a developing dust bowl, Africa’s suffered huge locust devastation, and China’s preparing for food shortages. How do unemployed people pay for it? Who can give them money without destroying the currency or if the currency is already destroyed?

A simple thing like the current fall in the number of sunspots is indicating an immediate future of colder weather and lower crop yields. Add into that, fuel shortages for agricultural machinery, lack of fertilizer – Nitrogen is made by burning lots of oil, lack of supply lines, and loss of credit lines. With people in Lockdown ‘they’ would be relying on a planned economy (not a free market) which is going to be inefficient. A planned economy is completely incapable of ensuring a stable food supply when there are shortages and the world is chaotic.

It’s not even feeding our cities that will be prime problem. It will be feeding the cities in Mexico and North Africa. They can’t cope with food price inflation. But they won’t starve – they’ll flood into the USA or cross the Mediterranean – lucky us! And what will Erdogan in Turkey do to feed his people – nothing good! If there are real food shortages then note that there are huge Muslim populations in France & Sweden, Turks and refugees in Germany, Pakistani ghettos in UK and plenty more where they all came from.

I’m feeling concerned. The problem is I can’t see Brexit solving our problems. Sure, it may not exacerbate them as much as I fear. November’s events may not trigger us into a state of oppression. But do you see my point? Things have got so bad, they can only get worse. November is bound to see some changes and they may well trigger a change in the Zeitgeist, though how significant depends on ‘events, dear boy, events’.

But whatever happens I think it’s virtually guaranteed that both the economy and society will keep on deteriorating.

Do you think I’m right?

Will November be the tipping point?

Is there any way back?

Will there be anything to go ‘back’ to?

Or else, is it a case of: “we’re doomed, I tell ya, doomed”. And what happens when more people work out that the elites have created a situation where their only option is to rapidly reduce the population! Famine will lead to uncontrollable social conflict, perhaps with Muslims massacring whites in general or the local Jewish populations in particular. I think that much conflict could see ‘them‘ lose control.

Thus it’s hard to see any other viable method than a bio-weapon. Agenda 21 could be implemented on schedule. And if not, the solution will need to be applied within a few years, certainly before 2025. Timing may depend on vaccine production as there will have to be at least enough vaccine for essential workers, the police, the military and the management class if the elite are to retain control.

via ZeroHedge News https://ift.tt/303rGdc Tyler Durden

“The Constitution is not neutral. It was designed to take the government off the backs of the people.”

– Justice William O. Douglas

The U.S. Supreme Court will not save us.

It doesn’t matter which party gets to pick the replacement to fill Justice Ruth Bader Ginsberg’s seat on the U.S. Supreme Court. The battle that is gearing up right now is yet more distraction and spin to keep us oblivious to the steady encroachment on our rights by the architects of the American Police State.

Americans can no longer rely on the courts to mete out justice.

Although the courts were established to serve as Courts of Justice, what we have been saddled with, instead, are Courts of Order. This is true at all levels of the judiciary, but especially so in the highest court of the land, the U.S. Supreme Court, which is seemingly more concerned with establishing order and protecting government interests than with upholding the rights of the people enshrined in the U.S. Constitution.

As a result, the police and other government agents have been generally empowered to probe, poke, pinch, taser, search, seize, strip and generally manhandle anyone they see fit in almost any circumstance, all with the general blessing of the courts.

Rarely do the concerns of the populace prevail.

When presented with an opportunity to loosen the government’s noose that keeps getting cinched tighter and tighter around the necks of the American people, what does our current Supreme Court usually do?

It ducks. Prevaricates. Remains silent. Speaks to the narrowest possible concern.

More often than not, it gives the government and its corporate sponsors the benefit of the doubt, which leaves “we the people” hanging by a thread.

Rarely do the justices of the U.S. Supreme Court— preoccupied with their personal politics, cocooned in a world of privilege, partial to those with power, money and influence, and narrowly focused on a shrinking docket (the court accepts on average 80 cases out of 8,000 each year)—venture beyond their rarefied comfort zones.

Every so often, the justices toss a bone to those who fear they have abdicated their allegiance to the Constitution. Too often, however, the Supreme Court tends to march in lockstep with the police state.

In recent years, for example, the Court has ruled that police officers can use lethal force in car chases without fear of lawsuits; police officers can stop cars based only on “anonymous” tips; Secret Service agents are not accountable for their actions, as long as they’re done in the name of “security”; citizens only have a right to remain silent if they assert it; police have free reign to use drug-sniffing dogs as “search warrants on leashes,” justifying any and all police searches of vehicles stopped on the roadside; police can forcibly take your DNA, whether or not you’ve been convicted of a crime; police can stop, search, question and profile citizens and non-citizens alike; police can subject Americans to virtual strip searches, no matter the “offense”; police can break into homes without a warrant, even if it’s the wrong home; and it’s a crime to not identify yourself when a policeman asks your name.

The cases the Supreme Court refuses to hear, allowing lower court judgments to stand, are almost as critical as the ones they rule on. Some of these cases have delivered devastating blows to the lives and rights enshrined in the Constitution. By remaining silent, the Court has affirmed that: legally owning a firearm is enough to justify a no-knock raid by police; the military can arrest and detain American citizens; students can be subjected to random lockdowns and mass searches at school; and police officers who don’t know their actions violate the law aren’t guilty of breaking the law.

You think you’ve got rights? Think again.

All of those freedoms we cherish—the ones enshrined in the Constitution, the ones that affirm our right to free speech and assembly, due process, privacy, bodily integrity, the right to not have police seize our property without a warrant, or search and detain us without probable cause—amount to nothing when the government and its agents are allowed to disregard those prohibitions on government overreach at will.

This is the grim reality of life in the American police state.

In fact, our so-called rights have been reduced to technicalities in the face of the government’s ongoing power grabs.

In the police state being erected around us, the police can probe, poke, pinch, taser, search, seize, strip and generally manhandle anyone they see fit in almost any circumstance, all with the general blessing of the courts.

This is what one would call a slow death by a thousand cuts, only it’s the Fourth Amendment being inexorably bled to death by the very institution that is supposed to be protecting it (and us) from government abuse.

These are the hallmarks of the emerging American police state, where police officers, no longer mere servants of the people entrusted with keeping the peace, are part of an elite ruling class dependent on keeping the masses corralled, under control, and treated like suspects and enemies rather than citizens.

Whether it’s police officers breaking through people’s front doors and shooting them dead in their homes or strip searching motorists on the side of the road, in a police state such as ours, these instances of abuse are not condemned by the government. Rather, they are continually validated by a judicial system that kowtows to every police demand, no matter how unjust, no matter how in opposition to the Constitution.

The system is rigged.

Because the system is rigged and the U.S. Supreme Court—the so-called “people’s court”—has exchanged its appointed role as a gatekeeper of justice for its new role as maintainer of the status quo, the police state will keep winning and “we the people” will keep losing.

By refusing to accept any of the eight or so qualified immunity cases before it this past term that strove to hold police accountable for official misconduct, the Supreme Court delivered a chilling reminder that in the American police state, ‘we the people’ are at the mercy of law enforcement officers who have almost absolute discretion to decide who is a threat, what constitutes resistance, and how harshly they can deal with the citizens they were appointed to ‘serve and protect.”

This is how qualified immunity keeps the police state in power.

Lawyers tend to offer a lot of complicated, convoluted explanations for the doctrine of qualified immunity, which was intended to insulate government officials from frivolous lawsuits, but the real purpose of qualified immunity is to rig the system, ensuring that abusive agents of the government almost always win and the victims of government abuse almost always lose.

How else do you explain a doctrine that requires victims of police violence to prove that their abusers knew their behavior was illegal because it had been deemed so in a nearly identical case at some prior time?

It’s a setup for failure.

A review of critical court rulings over the past several decades, including rulings affirming qualified immunity protections for government agents by the U.S. Supreme Court, reveals a startling and steady trend towards pro-police state rulings by an institution concerned more with establishing order, protecting the ruling class, and insulating government agents from charges of wrongdoing than with upholding the rights enshrined in the Constitution.

Worse, as Reuters concluded, “the Supreme Court has built qualified immunity into an often insurmountable police defense by intervening in cases mostly to favor the police.”

For those in need of a reminder of all the ways in which the Supreme Court has made us sitting ducks at the mercy of the American police state, let me offer the following.

To sum it up, we are dealing with a nationwide epidemic of court-sanctioned police violence carried out with impunity against individuals posing little or no real threat. In this way, the justices of the United States Supreme Court—through their deference to police power, preference for security over freedom, and evisceration of our most basic rights for the sake of order and expediency—have become the architects of the American police state.

So where does that leave us?

For those deluded enough to believe that they’re living the American dream—where the government represents the people, where the people are equal in the eyes of the law, where the courts are arbiters of justice, where the police are keepers of the peace, and where the law is applied equally as a means of protecting the rights of the people—it’s time to wake up.

We no longer have a representative government, a rule of law, or justice.

Liberty has fallen to legalism. Freedom has fallen to fascism.

Justice has become jaded, jaundiced and just plain unjust.

And for too many, the American dream of freedom and opportunity has turned into a living nightmare.

Given the turbulence of our age, with its police overreach, military training drills on American soil, domestic surveillance, SWAT team raids, asset forfeiture, wrongful convictions, profit-driven prisons, and corporate corruption, the need for a guardian of the people’s rights has never been greater.

Yet as I make clear in my book Battlefield America: The War on the American People, neither the president, nor the legislatures, nor the courts will save us from the police state that holds us in its clutches.

So we can waste our strength over the next few weeks and months raging over the makeup of the Supreme Court or we can stand united against the tyrant in our midst.

After all, the president, the legislatures, and the courts are all on the government’s payroll.

They are the police state.

via ZeroHedge News https://ift.tt/3mSXTO0 Tyler Durden

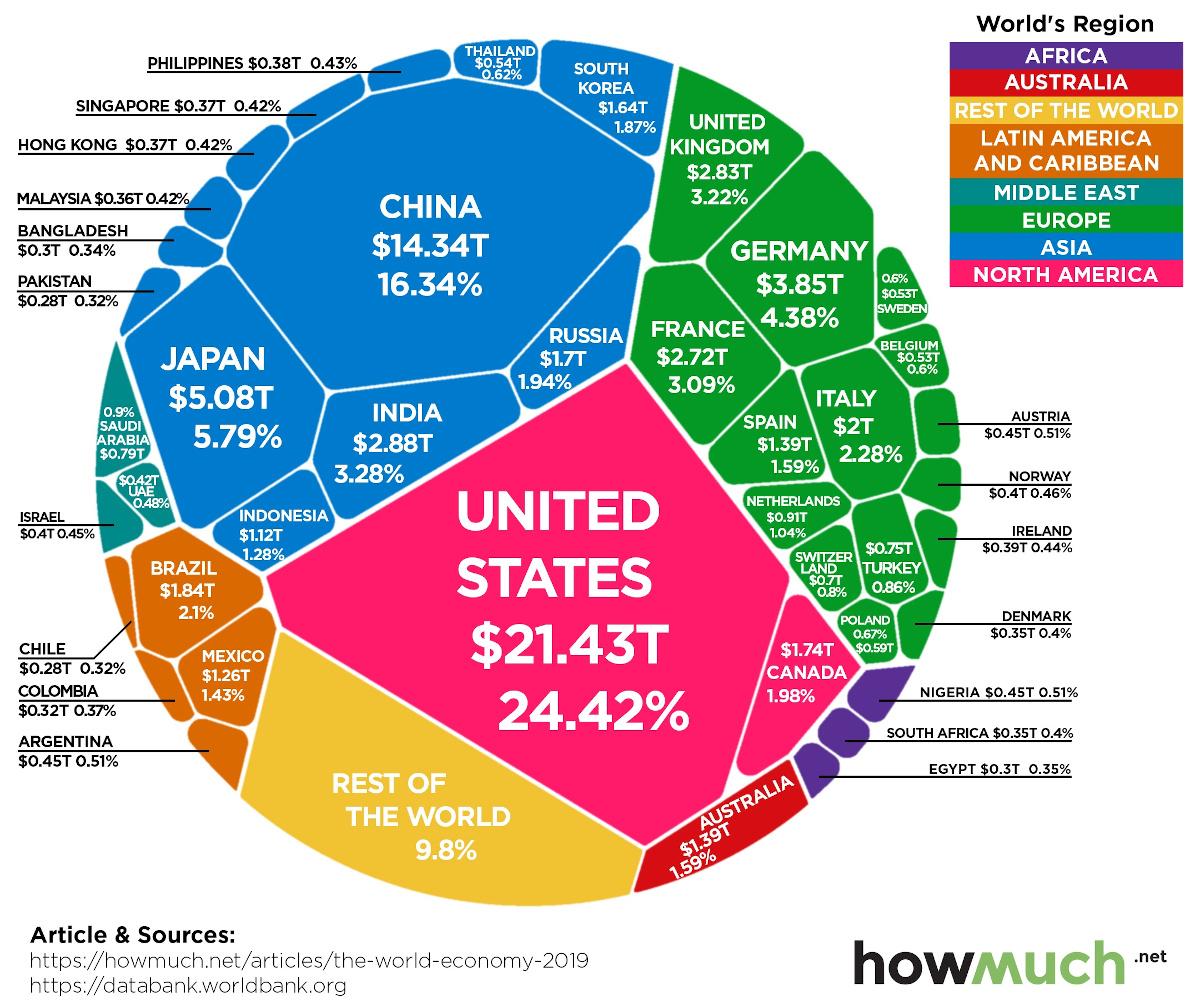

The $88 Trillion World Economy In One Chart Tyler Durden

Thu, 09/24/2020 – 23:40

The global economy can seem like an abstract concept, yet, as Visual Capitalist’s Iman Ghosh notes, it influences our everyday lives in both obvious and subtle ways. Nowhere is this clearer than in the current economic state amid the throes of the pandemic.

This voronoi-style visualization from HowMuch relies on gross domestic product (GDP) data from the World Bank to paint a picture of the global economy – which crested $87.8 trillion in 2019.

Editor’s note: Annual data on economic output is a lagging indicator, and is released the following year by organizations such as the World Bank. The figures in this diagram provide a snapshot of the global economy in 2019, but do not necessarily represent the impact of recent developments such as COVID-19.

Top 10 Countries by GDP (2019)

In the one-year period since the last release of official data in 2018, the global economy grew approximately $2 trillion in size—or about 2.3%.

The United States continues to have the top GDP, accounting for nearly one-quarter of the world economy. China also continued to grow its share of global GDP, going from 15.9% to 16.3%.

In recent years, the Indian economy has continued to have an upward trajectory—now pulling ahead of both the UK and France—to become one of the world’s top five economies.

In aggregate, these top 10 countries combine for over two-thirds of total global GDP.

2020 Economic Contractions

So far this year, multiple countries have experienced temporary economic contractions, including many of the top 10 countries listed above.

The following interactive chart from Our World in Data helps to give us some perspective on this turbulence, comparing Q2 economic figures against those from the same quarter last year.

One of the hardest hit economies has been Peru. The Latin American country, which is about the 50th largest in terms of GDP globally, saw its economy contract by 30.2% in Q2 despite efforts to curb the virus early.

Spain and the UK are also feeling the impact, posting quarterly GDP numbers that are 22.1% and 21.7% smaller respectively.

Meanwhile, Taiwan and South Korea are two countries that may have done the best at weathering the COVID-19 storm. Both saw minuscule contractions in a quarter where the global economy seemed to grind to a halt.

Projections Going Forward

According to the World Bank, the global economy could ultimately shrink 5.2% in 2020 – the deepest cut since WWII.

See below for World Bank projections on GDP in 2020 for when the dust settles, as well as the subsequent potential for recovery in 2021.

Source: World Bank Global Economic Prospects, released June 2020

via ZeroHedge News https://ift.tt/2FROwOe Tyler Durden

Former CIA Director John Brennan personally edited a crucial section of the intelligence report on Russian interference in the 2016 election and assigned a political ally to take a lead role in writing it after career analysts disputed Brennan’s take that Russian leader Vladimir Putin intervened in the 2016 election to help Donald Trump clinch the White House, according to two senior U.S. intelligence officials who have seen classified materials detailing Brennan’s role in drafting the document.

John Brennan, left, with Robert Mueller in 2013: The CIA director’s explosive conclusion in the ICA helped justify continuing Trump-Russia “collusion” investigations, notably Mueller’s probe as special counsel. AP Photo/Bebeto Matthews

The explosive conclusion Brennan inserted into the report was used to help justify continuing the Trump-Russia “collusion” investigation, which had been launched by the FBI in 2016. It was picked up after the election by Special Counsel Robert Mueller, who in the end found no proof that Trump or his campaign conspired with Moscow.

The Obama administration publicly released a declassified version of the report — known as the “Intelligence Community Assessment on Russian Activities and Intentions in Recent Elections (ICA)” — just two weeks before Trump took office, casting a cloud of suspicion over his presidency. Democrats and national media have cited the report to suggest Russia influenced the 2016 outcome and warn that Putin is likely meddling again to reelect Trump.

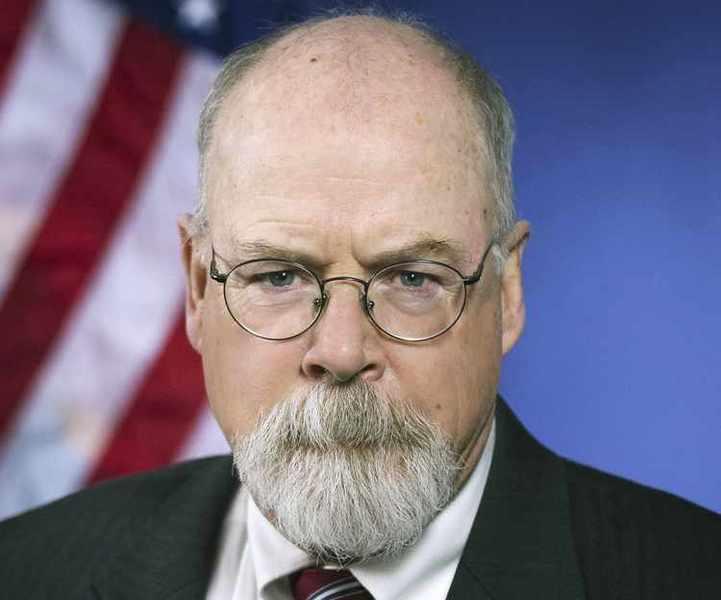

The ICA is a key focus of U.S. Attorney John Durham’s ongoing investigation into the origins of the “collusion” probe. He wants to know if the intelligence findings were juiced for political purposes.

RealClearInvestigations has learned that one of the CIA operatives who helped Brennan draft the ICA, Andrea Kendall-Taylor, financially supported Hillary Clinton during the campaign and is a close colleague of Eric Ciaramella, identified last year by RCI as the Democratic national security “whistleblower” whose complaint led to Trump’s impeachment, ending in Senate acquittal in January.

John Durham: He is said to be using the long-hidden report on the drafting of the ICA as a road map in his investigation of whether the Obama administration politicized intelligence. Department of Justice via AP

The two officials said Brennan, who openly supported Clinton during the campaign, excluded conflicting evidence about Putin’s motives from the report, despite objections from some intelligence analysts who argued Putin counted on Clinton winning the election and viewed Trump as a “wild card.”

The dissenting analysts found that Moscow preferred Clinton because it judged she would work with its leaders, whereas it worried Trump would be too unpredictable. As secretary of state, Clinton tried to “reset” relations with Moscow to move them to a more positive and cooperative stage, while Trump campaigned on expanding the U.S. military, which Moscow perceived as a threat.

These same analysts argued the Kremlin was generally trying to sow discord and disrupt the American democratic process during the 2016 election cycle. They also noted that Russia tried to interfere in the 2008 and 2012 races, many years before Trump threw his hat in the ring.

“They complained Brennan took a thesis [that Putin supported Trump] and decided he was going to ignore dissenting data and exaggerate the importance of that conclusion, even though they said it didn’t have any real substance behind it,” said a senior U.S intelligence official who participated in a 2018 review of the spycraft behind the assessment, which President Obama ordered after the 2016 election.

He elaborated that the analysts said they also came under political pressure to back Brennan’s judgment that Putin personally ordered “active measures” against the Clinton campaign to throw the election to Trump, even though the underlying intelligence was “weak.”

Adam Schiff: Soon after the Democrat took control of the House Intelligence Committee, its review of the drafting of the intelligence community assessment was classified and locked in a Capitol basement safe. AP Photo/J. Scott Applewhite

The review, conducted by the House Intelligence Committee, culminated in a lengthy report that was classified and locked in a Capitol basement safe soon after Democratic Rep. Adam Schiff took control of the committee in January 2019.

The official said the committee spent more than 1,200 hours reviewing the ICA and interviewing analysts involved in crafting it, including the chief of Brennan’s so-called “fusion cell,” which was the interagency analytical group Obama’s top spook stood up to look into Russian influence operations during the 2016 election.

Durham is said to be using the long-hidden report, which runs 50-plus pages, as a road map in his investigation of whether the Obama administration politicized intelligence while targeting the Trump campaign and presidential transition in an unprecedented investigation involving wiretapping and other secret surveillance.

The special prosecutor recently interviewed Brennan for several hours at CIA headquarters after obtaining his emails, call logs and other documents from the agency. Durham has also quizzed analysts and supervisors who worked on the ICA.

A spokesman for Brennan said that, according to Durham, he is not the target of a criminal investigation and “only a witness to events that are under review.” Durham’s office did not respond to requests for comment.

The senior intelligence official, who spoke on the condition of anonymity to discuss intelligence matters, said former senior CIA political analyst Kendall-Taylor was a key member of the team that worked on the ICA. A Brennan protégé, she donated hundreds of dollars to Clinton’s 2016 campaign, federal records show. In June, she gave $250 to the Biden Victory Fund.

Andrea Kendall-Taylor: A Brennan protégé, she donated hundreds of dollars to Hillary Clinton’s 2016 campaign, and recently defended the ICA in a “60 Minutes” interview. “60 Minutes”/YouTube

Kendall-Taylor and Ciaramella entered the CIA as junior analysts around the same time and worked the Russia beat together at CIA headquarters in Langley, Va. From 2015 to 2018, Kendall-Taylor was detailed to the National Intelligence Council, where she was deputy national intelligence officer for Russia and Eurasia. Ciaramella succeeded her in that position at NIC, a unit of the Office of the Director of National Intelligence that oversees the CIA and the other intelligence agencies.

It’s not clear if Ciaramella also played a role in the drafting of the January 2017 assessment. He was working in the White House as a CIA detailee at the time. The CIA declined comment.

Kendall-Taylor did not respond to requests for comment, but she recently defended the ICA as a national security expert in a CBS “60 Minutes” interview on Russia’s election activities, arguing it was a slam-dunk case “based on a large body of evidence that demonstrated not only what Russia was doing, but also its intent. And it’s based on a number of different sources, collected human intelligence, technical intelligence.”

But the secret congressional review details how the ICA, which was hastily put together over 30 days at the direction of Obama intelligence czar James Clapper, did not follow longstanding rules for crafting such assessments. It was not farmed out to other key intelligence agencies for their input, and did not include an annex for dissent, among other extraordinary departures from past tradecraft.

Eric Ciaramella: The Democratic national security “whistleblower,” whose complaint led to President Trump’s impeachment, was a close colleague of Kendall-Taylor. It’s not clear if Ciaramella also played a role in the drafting of the January 2017 assessment. whitehouse.gov

It did, however, include a two-page annex summarizing allegations from a dossier compiled by former British intelligence officer Christopher Steele. His claim that Putin had personally ordered cyberattacks on the Clinton campaign to help Trump win happened to echo the key finding of the ICA that Brennan supported. Brennan had briefed Democratic senators about allegations from the dossier on Capitol Hill.

“Some of the FBI source’s [Steele’s] reporting is consistent with the judgment in the assessment,” stated the appended summary, which the two intelligence sources say was written by Brennan loyalists.

“The FBI source claimed, for example, that Putin ordered the influence effort with the aim of defeating Secretary Clinton, whom Putin ‘feared and hated.’ “

Steele’s reporting has since been discredited by the Justice Department’s inspector general as rumor-based opposition research on Trump paid for by the Clinton campaign. Several allegations have been debunked, even by Steele’s own primary source, who confessed to the FBI that he ginned the rumors up with some of his Russian drinking buddies to earn money from Steele.

Former FBI Director James Comey told the Justice Department’s watchdog that the Steele material, which he referred to as the “Crown material,” was incorporated with the ICA because it was “corroborative of the central thesis of the assessment “The IC analysts found it credible on its face,” Comey said.

Christopher Steele: His dossier allegations were summarized in a two-page annex to the ICA, but dissenting views about the Kremlin’s favoring Hillary Clinton over Trump were excluded. Victoria Jones/PA via AP

The officials who have read the secret congressional report on the ICA dispute that. They say a number of analysts objected to including the dossier, arguing it was political innuendo and not sound intelligence.

“The staff report makes it fairly clear the assessment was politicized and skewed to discredit Trump’s election,” said the second U.S. intelligence source, who also requested anonymity.

Kendall-Taylor denied any political bias factored into the intelligence.

“To suggest that there was political interference in that process is ridiculous,” she recently told NBC News.

Her boss during the ICA’s drafting was CIA officer Julia Gurganus. Clapper tasked Gurganus, then detailed to NIC as its national intelligence officer for Russia and Eurasia, with coordinating the production of the ICA with Kendall-Taylor.

They, in turn, worked closely with NIC’s cybersecurity expert Vinh Nguyen, who had been consulting with Democratic National Committee cybersecurity contractor CrowdStrike to gather intelligence on the alleged Russian hacking of the Democratic National Committee computer system. (CrowdStrike’s president has testified he couldn’t say for sure Russian intelligence stole DNC emails, according to recently declassified transcripts.)

Durham’s investigators have focused on people who worked at NIC during the drafting of the ICA, according to recent published reports.

No Input From CIA’s ‘Russia House’

The senior official who identified Kendall-Taylor said Brennan did not seek input from experts from CIA’s so-called Russia House, a department within Langley officially called the Center for Europe and Eurasia, before arriving at the conclusion that Putin meddled in the election to benefit Trump.

“It was not an intelligence assessment. It was not coordinated in the [intelligence] community or even with experts in Russia House,” the official said. “It was just a small group of people selected and driven by Brennan himself … and Brennan did the editing.”

The official noted that National Security Agency analysts also dissented from the conclusion that Putin personally sought to tilt the scale for Trump. One of only three agencies from the 17-agency intelligence community invited to participate in the ICA, the NSA had a lower level of confidence than the CIA and FBI, specifically on that bombshell conclusion.

The official said the NSA’s departure was significant because the agency monitors the communications of Russian officials overseas. Yet it could not corroborate Brennan’s preferred conclusion through its signals intelligence. Former NSA Director Michael Rogers, who has testified that the conclusion about Putin and Trump “didn’t have the same level of sourcing and the same level of multiple sources,” reportedly has been cooperating with Durham’s probe.

The second senior intelligence official, who has read a draft of the still-classified House Intelligence Committee review, confirmed that career intelligence analysts complained that the ICA was tightly controlled and manipulated by Brennan, who previously worked in the Obama White House.

“It wasn’t 17 agencies and it wasn’t even a dozen analysts from the three agencies who wrote the assessment,” as has been widely reported in the media, he said.

“It was just five officers of the CIA who wrote it, and Brennan hand-picked all five. And the lead writer was a good friend of Brennan’s.”

Brennan’s tight control over the process of drafting the ICA belies public claims the assessment reflected the “consensus of the entire intelligence community.” His unilateral role also raises doubts about the objectivity of the intelligence.

In his defense, Brennan has pointed to a recent Senate Intelligence Committee report that found “no reason to dispute the Intelligence Community’s conclusions.”

“The ICA correctly found the Russians interfered in our 2016 election to hurt Secretary Clinton and help the candidacy of Donald Trump,” argued committee Vice Chairman Mark Warner, D-Va.

“Our review of the highly classified ICA and underlying intelligence found that this and other conclusions were well-supported,” Warner added.

“There is certainly no reason to doubt that the Russians’ success in 2016 is leading them to try again in 2020, and we must not be caught unprepared.”

Brennan, ex-Obama homeland security adviser Lisa Monaco and ex-national intelligence director James Clapper, interviewed by Nicolle Wallace of MSNBC, right, at a 2018 Aspen Instutute event. Aspen Institute

However, the report completely blacks out a review of the underlying evidence to support the Brennan-inserted conclusion, including an entire section labeled “Putin Ordered Campaign to Influence U.S. Election.” Still, it suggests elsewhere that conclusions are supported by intelligence with “varying substantiation” and with “differing confidence levels.” It also notes “concerns about the use of specific sources.”

Adding to doubts, the committee relied heavily on the closed-door testimony of former Obama homeland security adviser Lisa Monaco, a close Brennan ally who met with Brennan and his “fusion team” at the White House before and after the election. The extent of Monaco’s role in the ICA is unclear.

Brennan last week pledged he would cooperate with two other Senate committees investigating the origins of the Russia “collusion” investigation. The Senate judiciary and governmental affairs panels recently gained authority to subpoena Brennan and other witnesses to testify.

Several Republican lawmakers and former Trump officials are clamoring for the declassification and release of the secret House staff report on the ICA.

“It’s dynamite,” said former CIA analyst Fred Fleitz, who reviewed the staff report while serving as chief of staff to then-National Security Adviser John Bolton.

“There are things in there that people don’t know,” he told RCI.

“It will change the dynamic of our understanding of Russian meddling in the election.”

However, according to the intelligence official who worked on the ICA review, Brennan ensured that it would be next to impossible to declassify his sourcing for the key judgment on Putin. He said Brennan hid all sources and references to the underlying intelligence behind a highly sensitive and compartmented wall of classification.

He explained that he and Clapper created two classified versions of the ICA – a highly restricted Top Secret/Sensitive Compartmented Information version that reveals the sourcing, and a more accessible Top Secret version that omits details about the sourcing.

Unless the classification of compartmented findings can be downgraded, access to Brennan’s questionable sourcing will remain highly restricted, leaving the underlying evidence conveniently opaque, the official said.

via ZeroHedge News https://ift.tt/3kNh7TC Tyler Durden

US School Districts Abandon Online-Curriculum Provider Over ‘Racially Insensitive & Inaccurate’ Content Tyler Durden

Thu, 09/24/2020 – 23:00

As children prepare for online learning to continue being part of their life for at least another 6 months to a year (ultimately, it will depend on when a vaccine can be distributed), embarrassing stories of incompetence by the companies who are running these programs have whipped up a firestorm of controversy in the media.

Complaints about the Acellus Learning Accelerator, the program picked by the Alameda School District in California, and many others around the country, have piled up in local press reports.

Earlier this month, the controversy was sparked by “racist” or “sexist” questions, including one that asked young students what’s the proper definition of a “family”, before showing several options, including a black single mother, and a traditional white family with a mom and a father.

The answer was ‘the white family’. California’s liberals were apoplectic, and Alameda’s school district immediately severed its relationship with the program’s owner. One couple who said they paid the massively inflated home prices in Alameda in part for the schools. The fact that the district is spending money on programs with such obvious flaws is “frankly depressing”.

“We bought a home here so our kids could enroll in these schools and to have them roll out something like that,” Eckman said. “It’s very disappointing.”

Now, WSJ is reporting on more examples of the Acellus software’s egregious mistakes, including this error: ‘that Rosa Parks was arrested because she didn’t sit in the Blacks only section on a bus, instead of the correct answer, which is ‘she refused to give up her seat to a white ma’.

Teachers have at times rebelled, telling supervisors that the content simply “isn’t suitable” and ceasing to use it in their classes.

Over the past few weeks, Hawaii has emerged as a locus of complaints about the software, as thousands of parents signed a petition condemning the company’s content as racist, sexist and low quality. This fall, Acellus, which had previously only been used by some home schooled students in the state, had become the primary remote learning tool for 80k students across the state.

While school districts in Hawaii confessed that they didn’t thoroughly vet the product, one school district in Ohio rejected the software after finding several examples of “racially insensitive” content. The Delaware City School District in Ohio told parents it reviewed Acellus in greater depth after receiving complaints, and that the “racially and culturally insensitive material” had been evident.

In one particularly startling example, a history lesson the southern plantations said that slavery was “important” to keep them going.

As it turns out, while Acellus’s founders tout the software as “magical” and unlike anything else on the market, WSJ has discovered that three of the “PhDs” in charge of the company got their degrees from non-accredited institutions.

Later on in the story, Acellus’s biggest backers admitted that the software’s main competitive advantage was its price: It cost just $100 per student for the school year, compared with $300 or $400 for competing products. Previously, districts mostly used it sparingly for kids who needed to catch up on course credits. The WSJ story also hinted at strange “religious” ties in the founder’s “background”.

It’s almost hard to believe that America’s schools would make the mistake of contracting an “education” company run by three pseudo-“PhDs” who got their credentials from what’s effectively a diploma mill. But with the fiscal pinch and general chaos of the pandemic, school districts are finding it difficult to adapt.

via ZeroHedge News https://ift.tt/2FQnwPb Tyler Durden

In 2016 I told the few people who were listening to me then that I thought Trump would win Florida by around seven points depending on the level of cheating in Broward and Dade counties by now deposed and disgraced Broward Supervisor of Election, Brenda Snipes.

He wound up winning by three, so to me that says there was likely a fair amount of it going on. Argue with me all you want but I operate, normally, under the principle that U.S. elections of any import are determined by the maxim:

He who cheats best, wins.

Call it the Luongo Rule of Electoral Politics if you will.

This year we know that the cheating will be systemic and of a kind that we’ve not experienced before.

There is no more decorum about it. Only those truly naive or in the media will tell you otherwise.

In this election the ideologues have been radicalized on all sides to view the threat of the other side winning as existential to their future. And, far be it from me to tell them they’re wrong, because when I’m being honest with myself, they aren’t.

So that gives them not only motive, means and opportunity to cheat but also the fervent belief that they have to in order to save society itself. Well, at least, that’s what they are telling themselves as they go about doing it.

What’s also very clear is that the oligarch class which animates the establishment wing of the Republican party is working with the whole of the Democratic party and the media to remove Trump from power by any and all means necessary.

And while they are certainly signaling that they will use any and all means necessary to achieve this end, they would prefer for their actions to have the veneer of respectability, through some form of electoral mandate, even if that mandate is patent fiction.

Now any political neophyte knows Florida is the most important state in the union today from an electoral college perspective. Without Florida both Trump and Biden have a very difficult path to victory.

Those 29 (soon to be 31) electoral votes represent the pivot on which the entire election rests. I spent an hour recently with Joe Cotto of the Cotto/Gottfried Show talking about this from a uniquely Florida perspective which I think should give anyone pause who thinks Florida is actually up for grabs, because it isn’t.

Caption: They even got mah Trump Face… must love YouTube!

Looking back on the whole Coronapocalypse a tremendous amount of attention and pressure was placed on Governor Ron DeSantis to destroy the state economy.

It seemed every five days or so I’d log into Twitter to see some version of #DeSantisMustDie trending. After six months of it it’s a little tiring.

Then again, after a four-year temper tantrum electoral politics is pretty much tiresome.

For most of this year the polls have all told us that Joe Biden was winning in Florida. And that may have been the case six months ago, you know, when no one gave a crap about the presidential election except people who make their living covering it.

Guilty as charged.

But in the wake of almost surreal violence and scenes of looting and, frankly, animal-like behavior all that was ever going to do was push the moderate voter in a state like Florida towards Donald Trump, not away from him.

And now the polls, as flawed and dishonest as most of them are, have begun to reflect this basic truth. At no time in 2016 did Trump lead the polls in Florida. On election night I watched the faces of shitlibs from across the socio-economic spectrum of Alachua county go into paroxysms of despair as the results came in.

I almost, for a minute, felt bad for them.

So, this years, in my analysis, it doesn’t help that even the die-hard Democrat midwits I’ve known for most of my life are holding their nose to vote for Biden, not because he’s any good but because their own sense of self would be tarnished forever by voting Republican.

That level of disgust is a not a motivator to vote, it’s a motivator to stay home and drink heavily. And it will not play well for Biden here, nor will it help him win Democratic strongholds by the same majorities Democrats usually win by in places like Broward, Leon (Tallahassee), Alachua (Gainesville) and even Miami-Dade.

Honestly, they should worry more about pushing him to the teleprompter lucid at this point.

Now, don’t get me wrong, felons who have paid their way back to make restitution to their victims should be allowed to decide who rules over them. I think they should have their right to self-defense restored as well, especially non-violent felons.

But what’s happening here is blatant electioneering and an in-kind contribution to the Biden campaign. It’s indicative of what happens when you invest too much power in the political process, the power corrupts everyone and incentivizes them to skirt the rules.

Given that the entire political, legal and monetary system is designed to roll wealth up to oligarchs like Bloomberg it seriously distorts their power to alter the course of elections at a fundamental level.

All libertarian critiques of why handing these people money, guns and laws is a truly terrible idea apply here.

The problem with money in politics is that there is money in politics.

And that won’t change until the systems themselves are decentralized and stripped of their power.

That’s what is so seductively dangerous about the whole “Defund the Police” movement, it is highlighting a real inequity in our society. Police and prosecutors have too much power and too much immunity from the consequences of their actions and the use of their power.

And I’m happy to have a real conversation about how to alter the path we’re on – End the Drug War, get rid of income taxes, tort reform, strengthen home rule of states, etc. But that’s not what Antifa and BLM are offering. It isn’t what the Democrats’ silent assent for their subhuman behavior will offer us if they return to power.

And as far as I can tell very few people here in the state of Florida disagree with me on this.

Woke liberal absurdity has taken over St. Petersburg, FL & the mayor Rick Kriseman is to blame. His city defunded the police in July. @ GovRonDeSantis should suspend him immediately and restore the police department. BLM thugs harassing pic.twitter.com/Ixb5RGWvGz@rockpsychologst

And if anyone in that video had two operating brain cells to rub together to make a spark they’d realize this isn’t going to win them an election. And then the Soros/Brock bucks will vanish and they’ll just be more grist for the mill of oligarchs like Mini Mike.

They have gone all-in on this strategy. Men like George Soros have spent billions in support of this push for the World Economic Forum’s Great Reset. They aren’t going to allow such a little thing like the passing of a supreme court justice at the wrong time deter them from their goal.

You don’t need to have a dog’s keen nose to smell the fear and desperation that clings to these people, however. It is palpable in their behavior, their rhetoric and their over-reaction to everything Trump does or might do.

And their act is tiresome.

The American people have fear porn fatigue. It’s showing up in the polls and its showing up in their hysterics.

Regardless of how the election turns out, there will be no rest from the violence unleashed and the violence yet to come when millions of Americans come to the uncomfortable conclusion that they will never hold power again in their lifetimes.

No matter how they try to buy our obedience in Florida. Because this is the Florida I know.

According to Bloomberg, a flood of hedge funds are planning to expand their presence in the Sunshine State, as wealthy residents from northern states contend with the threat of higher taxes.

Paul Singer’s Elliott Management Corp. is reportedly considering opening a Florida office, as is Chicago-based Balyasny Asset Management, which has approximately $8 billion in AUM and plans to open an outpost in MIami, according to people familiar with the matter.

Adding to the list of firms which have already made the move is Bluecrest Capital Management, which just opened a Miami office for approximately 10 portfolio managers. Notably, Miami is offering companies up to $50,000 if they relocate downtown and employ at least 10 high-wage workers as part of their “Follow the Sun” campaign.

The moves to Florida, which has no state income tax, come as locales with the highest number of hedge funds weigh tax increases on the rich. Last week, New Jersey adopted a millionaires tax, and a ballot measure in Illinois calls for raising taxes on the wealthy. New York Governor Andrew Cuomo has said such a tax could be possible if the U.S. government fails to step in with aid, and Connecticut’s legislature also has discussed a tax hike.

“Every firm like Elliott is in the process of evaluating choices in how and where they work, including working from home and opening additional offices, but Elliott has not made any decisions,” said Stephen Spruiell, a spokesman for the New York-based firm. –Bloomberg

According to Palm Beach Hedge Fund Association head David Goodboy, two or three hedge funds per week are asking him about making the move, vs. one or two per month during the normal times. 90% of them are from Manhattan and Greenwich, Connecticut – with popular destinations including Miami, Palm Beach and Boca Raton – the latter of which Verition Fund Management set up shop two years ago for a couple of portfolio managers.

In 2015, David Tepper moved from New Jersey to Miami, relocating Appaloosa Management there the following year.

As Bloomberg also notes, wealthy individuals have been drawn to Florida’s favorable tax laws for years – with the GOP-backed 2017 law capping deductions for state and local taxes on federal returns undoubtedly contributing to newcomers. Meanwhile, real estate in Miami and Palm Beach has been on fire – with sellers deluged by offers.

via ZeroHedge News https://ift.tt/2Eute8q Tyler Durden

{kind=link}