For those who are considering a career in communications, a key question to understand is how much money you’ll be making when you graduate. Furthermore, will that salary be sufficient to pay for the debt involved with getting your degree?

While predicting one’s future income is subject to uncertainty, especially in the current economic climate, there is luckily a lot of data out there. Along with Priceonomics customer MastersInCommunications.org, we analyzed and collected data by the US Department of Education about how much money communications majors earn.

Using data from the College Scorecard, a data resource about the earnings and debt of graduates of US colleges, we looked at which undergraduate communications programs produced the graduates with the best and worst financial prospects.

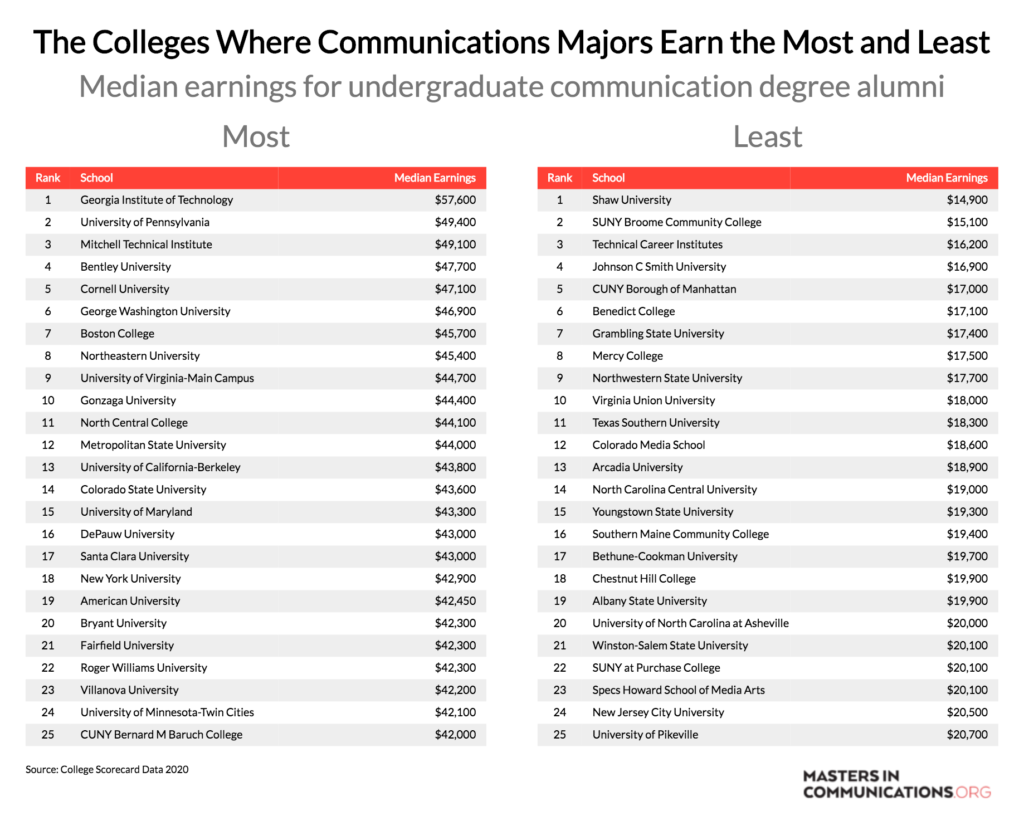

We found that communications majors from Georgia Tech and the University of Pennsylvania have the highest earnings while Shaw University has the lowest-earning graduates. Colleges like Devry and Grambling State University produce communications graduates with the highest debt while the City University of New York (CUNY) has graduated with the lowest levels of debt.

***

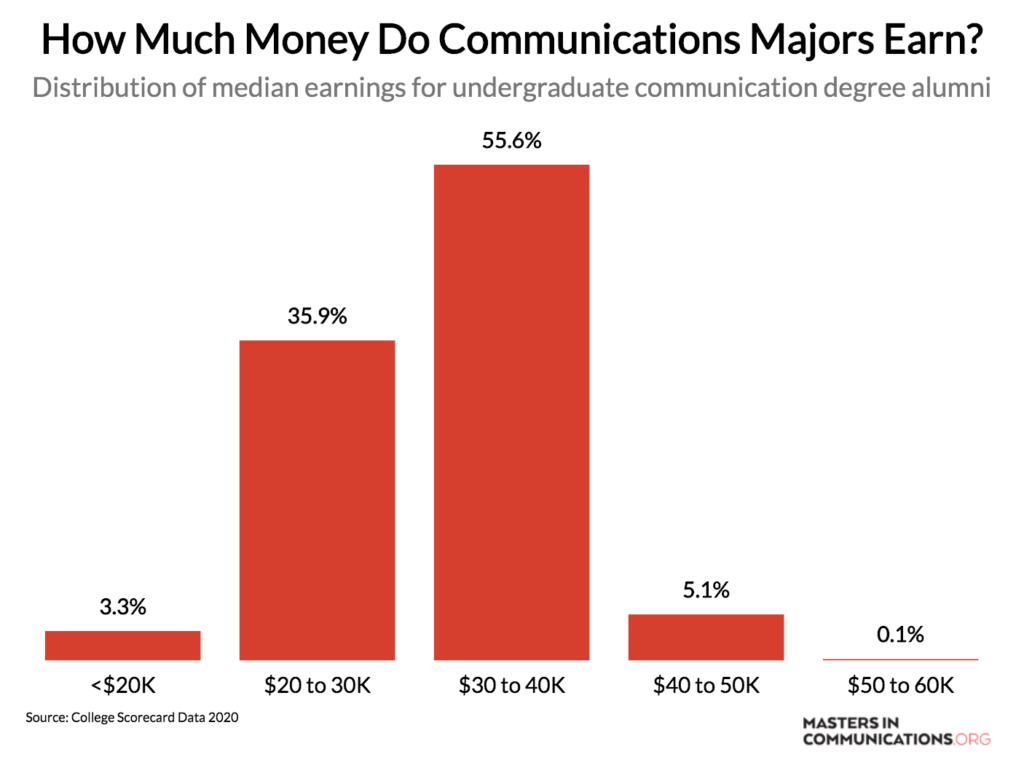

Before beginning the analysis of colleges where communications graduates earn the most and least, let’s look at the overall data. According to the most recent data from the US Department of Education College Scorecard, the median college graduate with a communications degree earns $31,400, approximately the same as the median US worker.

Not all communications programs are created equal, however. And you have ample reason to consider an online masters in communication program. Below shows the distribution of undergraduate communications programs segmented by median annual salary:

55.6% of graduates from college communications programs earn between $30K and $40K per year. In total, nearly 95% of communications majors earn under $40K per year. No undergraduate institution reported communications majors earning above $60K per year. Which colleges produce communications majors that earn the most and least? The following chart shows the schools reporting the highest median earnings among their undergraduates who studied communication:

Communications majors from Georgia Institute of Technology earn the most in the country with a median salary of $57,600 per year. In second place is the University of Pennsylvania, an Ivy League school where graduates earn just under $50,000 per year. In third place is the Mitchell Technical Institute, a technical college in South Dakota.

Communication graduates from Shaw University in Raleigh, North Carolina earn just $14,900 per year, the lowest in the country. SUNY Broome and Technical Career Institute graduates earn the second and third lowest salaries respectively.

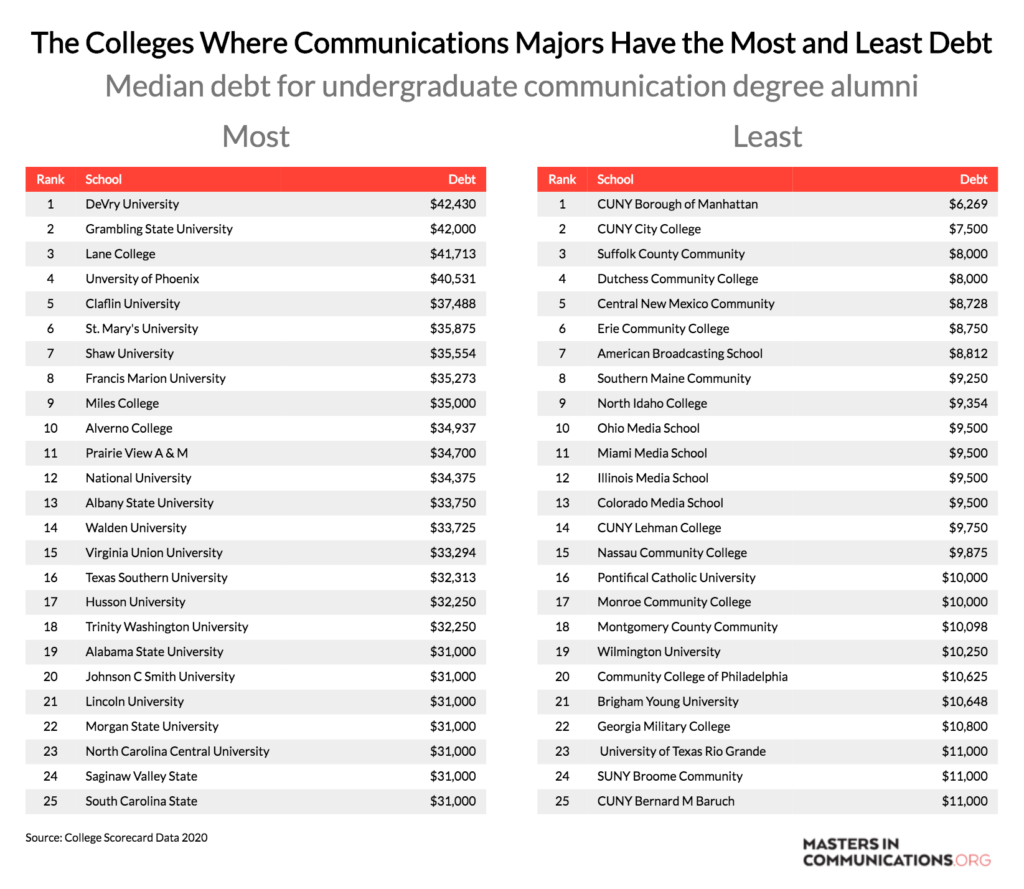

When it comes to debt, which schools communication graduates emerge with the highest and lowest burdens?

Communications majors from Devry University emerge with $42,430 in debt, the highest in the country. Grambling State and Lane College communications majors also graduate with more than $40,000 in debt. On the other hand, a number of community colleges graduate communications majors with less than $10,000 in debt.

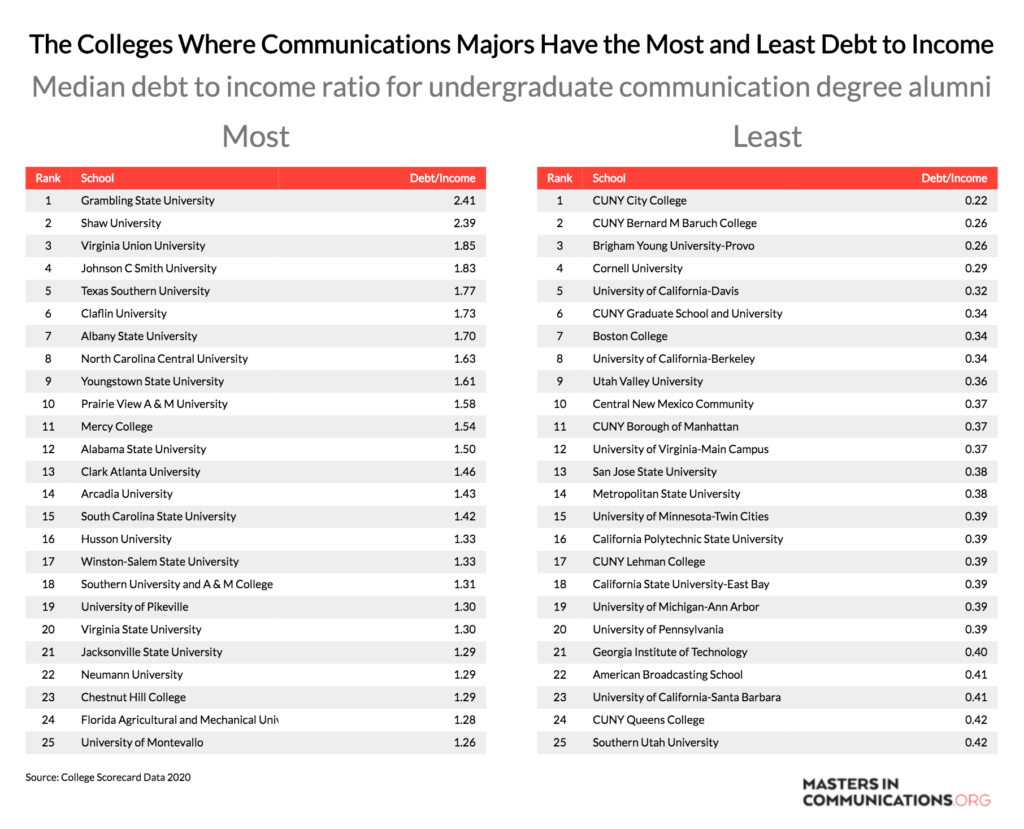

Having high levels of debt can be a problem, but that can be made up for with having a high income. Which colleges produce communications majors with high debt to income ratios and which ones come out with high incomes relative to their debt? The chart below shows the schools with the best and worst debt to income ratios (Total Debt / Annual Income):

Some of the schools whose students graduate with debt also have the least favorable debt to income ratios. Grambling State University and Shaw University produce communications graduates with the highest debt to income ratios by a considerable margin. On the other hand, schools that produce graduates with low debt relative to their income are a mix of community colleges (CUNY), lower-priced private schools (Brigham Young), higher-priced private schools (Cornell), and state schools (University of California). For a communication major who looks to graduate with a strong income relative to debt, all types of schools may fit the bill.

via ZeroHedge News https://ift.tt/33Btifa Tyler Durden

Soybean Futures Hit 27-Month High On Increased Chinese Demand Tyler Durden

Thu, 09/17/2020 – 21:40

CBoT soybean futures entered a new bull market in September, soaring 21% in the last five months, with most of the gains (+18%) over the previous 23 sessions as strong demand from China comes online.

According to Reuters, there’s a lot to be excited about in soybean fundamentals as the demand outlook story brightens with China increasing soybean purchases:

The U.S. Department of Agriculture confirmed private sales of 327,000 tonnes of U.S. soybeans to China. The USDA has announced U.S. soy sales to China in each of the last nine business days.

A Farm Futures producers’ survey conducted in late July and released on Wednesday projected a 4.9% rise in U.S. 2021 soybean seedings and a 0.3% drop in corn acres.

Agriculture leaders, including Jim Sutter, CEO of the U.S. Soybean Export Council, told CNBC’s “Street Signs Asia” on Sept. 10 that “outlook demand for the next six months or so is pretty good.”

Sutter said, “U.S. farmers are feeling much more optimistic than they said, a year or even six months ago,” adding that China has been buying U.S. soybeans as part of the phase one trade deal signed between both countries in January.

“Now, as we get into the time of the year, when China is more typically purchasing soybeans from the northern hemisphere — the United States in particular — we are seeing them make significant purchases … we have a record amount of new crop sales open to China at this time, so we are thinking that it is a successful trade deal,” Sutter said.

China is committed to buying $12.5 billion of U.S. farm products under phase one agreement, with another $19.5 billion in 2021.

“I continue to believe that the phase one agreement is very important and is being executed well,” said Sutter.

We noted, in late August, the “prospects of strong Chinese demand pushed Chicago soybean futures prices to a seven-month high this week.”

“China has been stepping up purchases of American agricultural goods since the end of April, with soybean sales for delivery next season currently running at their highest level for this time of year since 2013.”

And of particular note is the fact that this surge in prices – on apparent demand – is against the typical seasonal pattern in soybean price action…

While China’s demand for U.S. soybeans appears to be increasing, partly because the country’s hog herd numbers are recovering from the African swine fever outbreak, overall trade deal commitments under the phase one deal will likely not be met this year.

China’s increased soybean purchases is good news for President Trump ahead of the presidential elections on Nov. 03.

via ZeroHedge News https://ift.tt/3kwDe0v Tyler Durden

“Everyone Involved Should Face Jail Time”: Trump Jr. Slams Nashville Officials For Concealing Low COVID-19 Numbers Tyler Durden

Thu, 09/17/2020 – 20:44

Donald Trump Jr. has weighed in over Nashville officials concealing the low number of COVID-19 cases in bars and restaurants.

In a Thursday tweet, the president’s son said “The Dem Mayor of Nashville KNOWINGLY LIED ABOUT COVID DATA to justify shutting down bars & restaurants, killing countless jobs & small businesses in the process,” adding “Everyone involved should face jail time. How many other Dem run cities is this happening in?”

The Dem Mayor of Nashville KNOWINGLY LIED ABOUT COVID DATA to justify shutting down bars & restaurants, killing countless jobs & small businesses in the process.

Everyone involved should face jail time. How many other Dem run cities is this happening in?https://t.co/8anzs5Jgba

Leaked emails between the senior adviser to Nashville’s Mayor and a health department official reveal a disturbing effort to conceal extremely low coronavirus cases emanating from bars and restaurants, while the lion’s share of infections occurred in nursing homes and construction workers, according to WZTV Nashville.

On June 30th, contact tracing was giving a small view of coronavirus clusters. Construction and nursing homes causing problems more than a thousand cases traced to each category, but bars and restaurants reported just 22 cases.

Leslie Waller from the health department asks “This isn’t going to be publicly released, right? Just info for Mayor’s Office?“

“Correct, not for public consumption.” Writes senior advisor Benjamin Eagles. –WZTV

Four weeks later, Tennessean reporter Nate Rau asked the health department: “the figure you gave of “more than 80” does lead to a natural question: If there have been over 20,000 positive cases of COVID-19 in Davidson and only 80 or so are traced to restaurants and bars, doesn’t that mean restaurants and bars aren’t a very big problem?“

To which health department official Brian Todd scrambled for an answer – asking five health department officials: “Please advise how you respond. BT.”

The response – from an official whose name was omitted from the leaked email: “My two cents. We have certainly refused to give counts per bar because those numbers are low per site,” adding “We could still release the total though, and then a response to the over 80 could be “because that number is increasing all the time and we don’t want to say a specific number.””

According to a metro staff attorney asked by city councilmember Steve Glover to verify the authenticity of the emails, “I was able to get verification from the Mayor’s Office and the Department of Health that these emails are real.”

Glover told WZTV: “They are fabricating information. They’ve blown there entire credibility Dennis. Its gone i don’t trust a thing they say going forward …nothing.”

Glover says he has been contacted by an endless stream of downtown bartenders, waitresses, and restaurant owners. Why would they not release these numbers?

“We raised taxes 34 percent and put hundreds literally thousands of people out of work that are now worried about losing their homes their apartments etcetera and we did it on bogus data. That should be illegal!” he says.

Again, we weren’t told by the mayor’s office this wasn’t true. We were told to file a freedom of information act request. –WZTV

via ZeroHedge News https://ift.tt/35KUrPG Tyler Durden

After two Los Angeles sheriff’s deputies were shot and critically wounded on Saturday, Joe Biden warned, “Weapons of war have no place in our communities.” And within just hours of the attack, Biden tweeted in praise of the original bans on assault weapons and high-capacity magazines, which lasted from 1994 to 2004. “These bans saved lives, and Congress should never have let them expire,” he wrote.

A handgun, not an assault rifle, was used to shoot the deputies. But it seems that Biden never misses an opportunity to deceptively complain about “weapons of war.”

In the past, Biden and vice presidential nominee Kamala Harris have applied this label to AR-15 semi-automatic rifles. But these guns function exactly as small-game, semi-automatic hunting rifles. Though it looks like the M16 machine gun made famous in the Vietnam War, no military in the world uses the AR-15.

Gun control advocates commonly pose the question:

“Why do people need a semi-automatic AR-15 to go out and kill deer?”

The answer is simple: It is a hunting rifle. It has just been made to look like a military weapon. Semi-automatic weapons are also used to protect people and save lives. Single-shot rifles that require you to physically reload the gun may not do people a lot of good when their first shot misses or fails to stop an attacker. Or, for that matter, if they are facing multiple assailants.

What about Biden’s claims that the assault weapons ban saved lives?

Since the ban expired in September 2004, murder and overall violent crime rates have fallen. In 2003, the last full year before the law expired, the U.S. murder rate was 5.7 per 100,000 people. The murder rate never returned to that level, and fell to 5.0 per 100,000 people by 2018.

If the ban had any effect, one would think that it would reduce the number of murders committed with rifles. But the percentage of firearm murders that were committed with rifles was at 4.8% prior to the ban starting in September 1994, and averaged 4.9% from 1995 to 2004. In the 10 years after the ban, the figure averaged just 3.9%. This pattern is the opposite of what gun control advocates predicted.

Many academic studies have examined the original federal assault weapons ban.

They consistently found no statistically significant impact on mass public shootings or any other type of crime. Clinton administration-funded research by criminology professors Chris Koper and Jeff Roth confirmed as much in a 1997 report for the National Institute of Justice.

“The evidence is not strong enough for us to conclude that there was any meaningful effect (i.e., that the effect was different from zero),” they wrote.

Koper and Roth suggested at the time that it might be possible to find a benefit after the ban had been in effect for more years. In 2004, they published a follow-up NIJ study with fellow criminologist Dan Woods.

“We cannot clearly credit the ban with any of the nation’s recent drop in gun violence,” they concluded.

“And, indeed, there has been no discernible reduction in the lethality and injuriousness of gun violence.”

Gun control advocates often cite work by Louis Klarevas, but his non-peer-reviewed methodologies are highly flawed. For one thing, Klarevas looks only at the total number of mass public shootings, whether they were committed with assault weapons or with other types of guns. While the share of mass public shootings that utilized assault weapons fell during the ban, it fell even more sharply in the 10 years after the ban ended in 2004. And any reduction that the ban caused in attacks with assault weapons may simply have meant more attacks with other types of guns.

Biden’s tweet also touted large-capacity ammunition magazine bans. Contrary to common perception, ordinary hunting rifles can hold just as large a magazine as “assault weapons.” Any gun that can hold a magazine can hold one of any size. That is true for handguns as well as rifles. Magazines are basically metal boxes with springs, and are easy to make and virtually impossible to stop criminals from obtaining. The 1994 legislation banned magazines that could hold more than 10 bullets, yet had no effect on crime rates.

Biden is making it clear that gun control is near the top of his agenda. So it’s little wonder that gun control zealot Michael Bloomberg just pledged to spend at least $100 million in Florida alone on behalf of the Biden campaign. But no matter how much Biden wishes it were true, guns bans won’t make American’s safer. With Democrats promising to eliminate the Senate filibuster if they win, gun bans will be an integral part of the radical agenda that they will quickly enact. To his credit, Biden is not hiding it.

via ZeroHedge News https://ift.tt/3c9BJ59 Tyler Durden

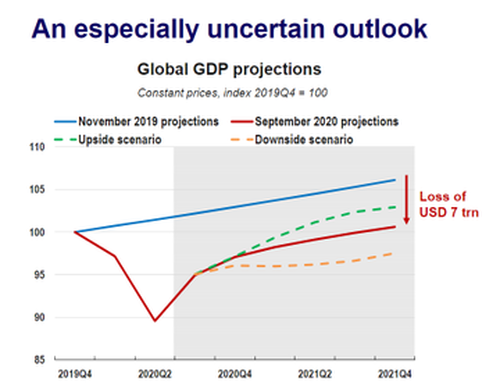

World Bank Warns Recovery Could Take “Five Years” Tyler Durden

Thu, 09/17/2020 – 21:00

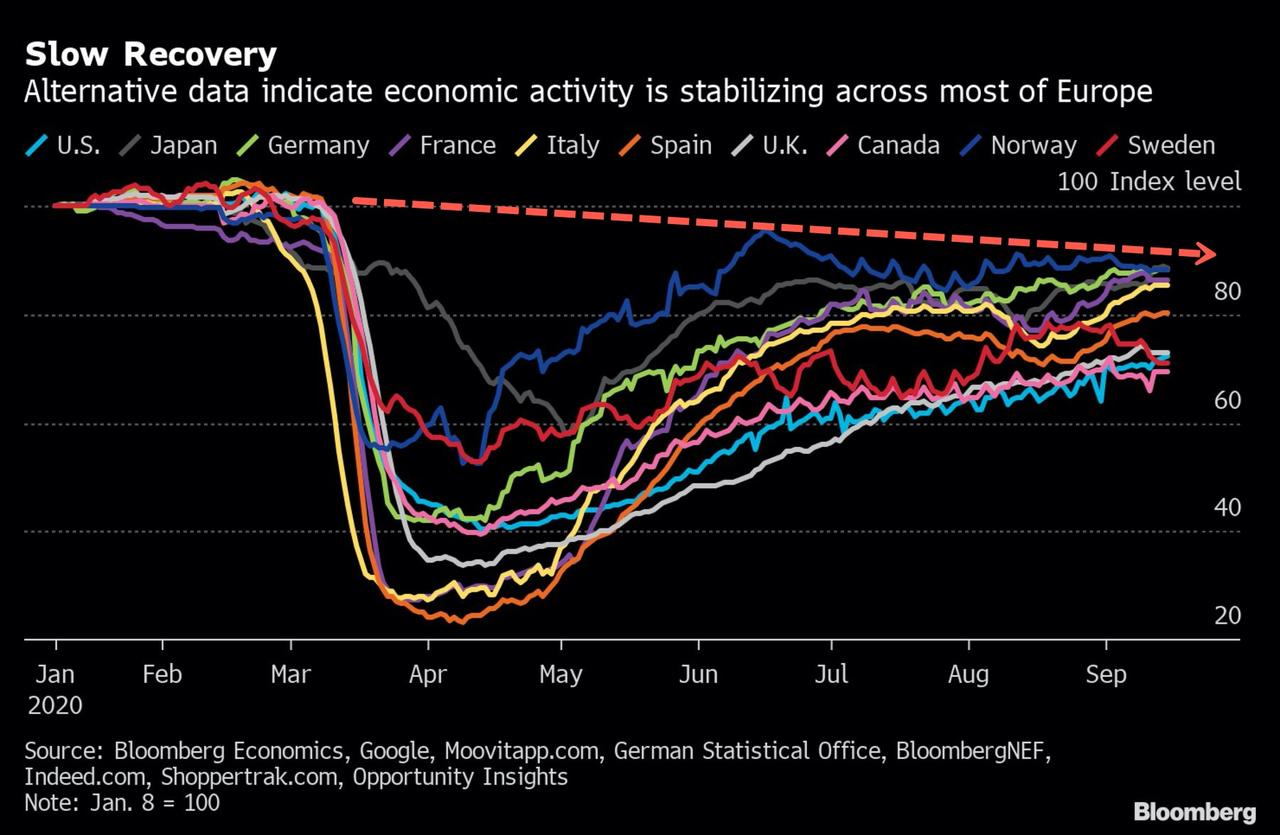

Global economic activity around the world has stabilized in mid-September, though far below pre-COVID-19 levels as recoveries risk reversing if monetary and fiscal stimulus is not continued at rates seen in the first half of 2020. We noted Wednesday, a new OECD report offered some hope the global downturn is not as severe as previously thought but is still viewed as an “unprecedented” decline.

We also noted the OECD report is problematic for policy-makers who have unleashed easy-money policies during the pandemic to artificially inflate economies and boost risk assets, as policy support in the second half of the year might not be as great as what was seen earlier in the year (as is currently playing out in Washington with the prospect of a slimmed-down stimulus bill getting slimmer).

So with waning support from central banks and fiscal stimulus from governments, the quick rebound seen in the global economy has likely stalled, and the shape of the recovery will no longer resemble a “V” but more of a “W” or “U” or “L.”

For more color on the shape of the global recovery, or rather perhaps how long the recovery will last, chief economist of the World Bank, Carmen Reinhart, warned Thursday, a full recovery could take upwards of five years, reported El País.

“There will probably be a quick rebound as all the restriction measures linked to lockdowns are lifted, but a full recovery will take as much as five years,” Reinhart said, while speaking at a conference in Madrid, Spain.

Carmen Reinhardt, Chief Economist at the World Bank

Reinhart said (as quoted by Reuters), “the pandemic-caused recession will last longer in some countries than in others and will increase inequalities as the poorest will be harder hit by the crisis in rich countries and the poorest countries will be harder hit than richer countries.”

“Central banks have tried to provide liquidity to avoid affecting more households. But as much as central banks give support, there are businesses that will not return, there are closed restaurants or stores that will not reopen, there are homes that will take a long time to find employment, there are airlines or hotels that will not survive a long period without normal mobility. There are going to be a lot of bankruptcies: if you look at the credit rating agencies, S&P, Moody’s, Fitch, the amount of reduction in credit quality that has been seen since the beginning of the year, both at the corporate and sovereign levels, has been a record. And central banks are not all-powerful either: no matter how much credit support is given, at some point you have to face the deterioration in the financial system, and that is not a criticism: it is inevitable because of the deep drop in the economy. Under these conditions, we have to think about cuts that allow new credits for recovery,” she said.

She added, “this crisis did not start as a financial crisis. But given the depth of this decline we are experiencing, it is turning into a financial crisis. For very obvious reasons: many households have lost a job that they will not get back, they have difficulties in paying their debts, many businesses have closed their doors and will not reopen them, the shopping centers are paralyzed and half empty.”

This comes as 29.7 million people around the world have been infected with COVID-19 and 938,820 have died, according to the latest Johns Hopkins University figures. High frequency data (via Bloomberg) is showing the recovery around the world has stabilized but risks a reversal if more policy support, if that is from central banks or governments is not seen.

Readers should be asking: What happens when Wall Street misreads the shape of the recovery?

To answer that, Gary Shilling, the president of A. Gary Shilling & Co., told CNBC’s Elizabeth Schulze in a July interview that once investors realize the shape of the recovery is an “L” rather than the overhyped “V,” it would trigger a 1930s stock market decline.

via ZeroHedge News https://ift.tt/3hEzOXG Tyler Durden

The upcoming election may be the most important in US history. At least as important as that of 1860, which led directly to the War Between the States.

In 2016 I believed Trump would win and placed a money bet on him.

This time I’m not so sure, despite Trump’s “incumbent advantage” and the fact the Democrats could hardly have picked two worse candidates.

I see at least six reasons why this is true, namely:

The Virus

The economy

Demographics

Moral collapse of the old order

The Deep State

Cheating

The consequences of a Democrat victory will be momentous.

Let’s look at why it’s likely.

1. The Virus

Despite the fact COVID is only marginally more deadly than the annual flu, and the fact it’s only a danger to the very old (median death age 80), the hysteria around it is changing the nature of life itself. It’s proven much less serious than the Asian flu of the late ’60s or the Hong Kong flu of the late ’50s. And not even remotely comparable to the Spanish flu of 1918-19. None of those had any discernable effect on the economy or politics. COVID is a trivial medical event but has created a gigantic psychological hysteria.

The virus hysteria is, however, a disaster from Trump’s point of view for several reasons. None of them have anything to do with his “handling” of the virus—apart from the fact that medical issues should be a matter between a patient and his doctor, not bureaucrats and politicians.

First, the virus hysteria is severely limiting the number and size of Trump’s rallies, which he relies on to keep enthusiasm up.

Second, more people are staying at home and watching television than ever before. However, unless they glue their dial to Fox, they’ll gravitate towards the mainstream media, which is stridently anti-Trump. People who are on the fence (and most voters are always in the wishy-washy middle) will mostly hear authoritative-sounding anti-Trump talking heads on television, and they’ll be influenced away from Trump.

Third, older people have by far the heaviest voter turnout, but roughly 80% of the casualties of the virus are elderly. And over 90% of those deaths are related to some other condition. Be that as it may, fear will make older people less likely to vote in this election. The COVID hysteria will still be with us in November. Older people tend to be culturally conservative and are most likely Trumpers.

Fourth, in today’s highly politicized world, the government is supposed to be in charge of everything. Despite the fact there are thousands of viruses, and they’ve been with us thousands of years, this one is blamed on the current government. Boobus americanus will tend to vote accordingly.

2. The Economy

Keeping his voters at home is one thing. But the effects the hysteria is having on the economy are even more important. The effect of COVID on the economy should be trivial since only a small fraction of the relatively few Covid deaths are among people who are economically active.

Presidents always take credit when the economy is good and are berated when it’s bad on their watch, regardless of whether they had anything to do with it. If the economy is still bad in November—and I’ll wager it’s going to be much worse, despite the Fed creating trillions of new dollars, and the government handouts—many people will reflexively vote against Trump.

In February, before the lockdown, there were about 3.2 million people collecting unemployment. Now, there are about 30 million. So it seems we have over 30 million working-age people who are . . . displaced. That doesn’t count part-time workers, who aren’t eligible for unemployment but are no longer working.

The supplementary benefits have ended. If they return, it will be at lower levels. The artificial good times brought on by free money will end too. It will be blamed on the Republicans.

Worse, the public has come to the conclusion that a guaranteed annual income works. This virus hysteria has provided a kind of test for both Universal Basic Income and Modern Monetary Theory—helicopter money. So far, anyway, it seems you really can get something for nothing.

An important note here: Trump—whatever his virtues—is an economic ignoramus. He’s supported both helicopter money and artificially low-interest rates since he’s been in office. But especially now, because he knows it’s all over if today’s financial house of cards collapses on his watch.

I’ll wager that, out of the 160 million work-force Americans, 30 million will still be out of work by voting day. The recognition that the country is in a depression will sink in. The virus hysteria was just the pin—or sledgehammer, perhaps—that broke the bubble. But that’s another story. What’s for sure is that the average American will look for somebody to blame. As things get seriously bad, people will want to change the system itself, as was true in the 1930s.

The only economic bright spot for Trump is the stock market. But it’s at bubble levels. Not because the economy is doing well, but because of the avalanche of money being printed. Where it is in November is a question of how much more money the Fed will print, and how much of it flows into the stock market. Even then, there’s an excellent chance it could collapse between now and the election.

For reasons I’ve detailed in the past, the economy is now entering the trailing edge of a gigantic financial and economic hurricane. The Greater Depression will be much different, longer-lasting, and nastier than the unpleasantness of 1929-1946. And people vote their pocketbook. Bill Clinton was right when he said, “It’s the economy, stupid.” If stocks fall, it will compound this effect. A high stock market just gives the illusion of prosperity. And, at least while stocks are up, contributes to the atmosphere of class warfare. Poor people don’t own stocks.

3. Demographics

Since the gigantic political, economic, and social crisis we’re in will be even more obvious come November, people will want a radical change. Since that—plus lots of free stuff—is what the Democrats are promising, they’re likely to win. But there are other factors.

The last election was close enough, but now, four years later, there are four more cohorts of kids that have gone through high school and college and have been indoctrinated by their uniformly left-wing teachers. They’re going to vote Democrat overwhelmingly.

Alexandria Ocasio-Cortez (AOC), and people like her, are both the current reality and the future of the Democratic Party—and of the US itself. She knows how to capitalize on envy and resentment. The Black Lives Matter and Antifa movements have added the flavor of a race war to the mix. Racial antagonism will become more pronounced as whites lose their majority status over the next 30 years.

Nobody, except for a few libertarians and conservatives, is countering the purposefully destructive ideas AOC represents. But they have a very limited audience and not much of a platform. Arguing for sound money and limited government makes them seem like Old Testament prophets to Millenials. Collectivism and statism are overwhelming the values of individualism and liberty.

It’s exactly the type of thing the Founders tried to guard against by restricting the vote to property owners over 21, going through the Electoral College. Now, welfare recipients who are only 18 can vote, and the Electoral College is toothless.

For the last couple of generations, everybody who’s gone to college has been indoctrinated with leftist ideas. Almost all of the professors hold these ideas—as well as high school and grade school instructors. They place an intellectual patina on top of emotional, fantasy-driven leftist ideas.

When the economy collapses in earnest, everybody will blame capitalism. Because Trump is rich, he’s incorrectly associated with capitalism. The country—especially the young, the poor, and the non-white—will look to the government to “do something.” They see the government as a cornucopia.

A majority of Millennials are in favor of socialism, as are so-called People of Color. By 2050, whites will be a minority in the US. A straw in the wind is that a large majority of the people who commit suicide each year are middle-class white males—essentially, Trump supporters. The demographic handwriting is on the wall. Trump’s election in 2016 was an anomaly. No more than a Last Hurrah.

4. Moral Collapse

There’s now a lot of antagonism toward both free minds and free markets. A majority of Americans appear to actually support BLM, an openly Marxist movement. Forget about free minds—someone might be offended, and you’ll be pilloried by the mob. Forget about free markets—they’re blamed for all the economic problems, even though it’s the lack of them that caused the problem. The idea of capitalism is now considered undefendable.

Widespread dissatisfaction with the system is obviously bad for the Republicans and good for the Democrats, who promote themselves as the party of change.

It used to be pretty simple—the Republicans and the Democrats were just two sides of the same coin, like Tweedledee and Tweedledum. Traditionally, one promoted the warfare state more, the other the welfare state. But it was mostly rhetoric; they were pretty collegial. Now, both the welfare and the warfare state have been accepted as part of the cosmic firmament by both parties. The difference between them is now about cultural issues. Except that polite disagreement has turned into visceral hatred.

The Dems at least stand for some ideas—although they’re all bad ideas. The Republicans have never stood for any principles; they just said the Dems wanted too much socialism, too fast, which is why they were always perceived—correctly—as hypocrites. Antagonism between the right and the left is no longer political or economic—it’s cultural. That’s much more serious.

Look at the 20 Democratic candidates that were in the primary debates last summer. They were all radical collectivists, dedicated statists. The Republicans were all—with one exception—mealy-mouthed nonentities.

Unlike Trump and the Reps, the Dems actually have a core of philosophical beliefs—and that counts during chaos. It doesn’t matter that they’re irrational or evil. People want to believe in something. The Dems give them a secular religion that promises a better world. The Reps only represent the withering status quo—which is not very appealing.

There’s no political salvation coming from the Republican party. Like Trump himself, it doesn’t have any core principles. It just reacts to the Dems and proposes similar, but less radical alternatives to their ideas. It doesn’t stand for anything. It’s only capable of putting forward empty suits, pure establishment figures like Bob Dole, Mitt Romney, or Bush. Or a nobody like Pence. That’s a formula for disaster in today’s demographic and cultural environment.

Incidentally, I’m not a fan of Trump, per se. He’s an opportunist who flies by the seat of his pants. He’s essentially an American Peron, whose economic policies are disjointed and inconsistent. His foreign policies are dangerous, provoking the Iranians and the Russians and starting a cold war with China that could easily spin out of control and turn into a major hot war.

But on the bright side, he’s a cultural conservative. And that’s why people support him. He wants to see the US return to the golden days of yesteryear, the world of Leave it to Beaver, Ozzie, and Harriet, and Father Knows Best. We’d all like to see domestic tranquility and rising prosperity. But that’s not the world we’re going to be living in, not just for 2020, but the whole decade.

For years, I’ve joked that I planned on watching riots on my widescreen from a secure location, not out my front window. Things have now become so predictable that when I turn on the news, I kill the audio and just put the Stone’s “Street Fighting Man” on a continuous loop.

Anyway, conservatives are completely demoralized. They’re grasping at cultural and moral straws from a bygone era. It’s impossible to defend being a white person anymore; propaganda has made it shameful to be white. If you object to the race-baiters, you’ll be shouted down in the media—especially by white “liberals.” Everything you grew up with and thought was part of the cosmic firmament is being washed away as unworthy.

As an example, recently, in Stone Mountain, Georgia, 1,000 uniformed, armed black men went out of their way to say that they were looking for a fight. “Where are the rednecks that want to fight with us?”

It would have been out of the question at any time in the past, but no rednecks showed up to the party. That’s partially because they’ve been psychologically cowed, and partially because they recognize that if they did when law enforcement arrived, they’d be the ones that were prosecuted, not the black men.

It’s a complete inversion of what would have been the case only a generation ago. Then the blacks would have been too psychologically cowed to turn up for a fight, and the legal system would have railroaded them.

Just to be clear, I’m opposed to any kind of identity politics, regardless of the group. The point is that there’s been a sea change in mass psychology.

The demoralization of the ancien regime is why the destroyers of scores of statues of national heroes, from Columbus on down, are not being prosecuted. Nor do any citizens come out to oppose them. It’s a matter of psychology. Whites and conservatives no longer believe in themselves. When that’s true, it’s game over. Yes, I know it’s not true of all of them—but I believe it’s a fair generalization.

This was spelled out very presciently by late Soviet defector Yuri Bezmenov, a KGB agent who fled to Canada in 1970. Bezmenov stated in the mid-1980s that there were four stages of collapse: Demoralization, Destabilization, Crisis, and Normalization. Demoralization takes decades. Bezemov said in 1985 that the process of demoralization—an undermining of a target nation’s values that makes it ripe for revolutionary takeover—was “basically completed already” in the United States. Destabilization, which we’ve seen, especially since the crisis of 2008, is now reaching a climax. I believe a Crisis that changes everything is coming in November.

5. The Deep State

The president is important. But the fact of the matter is that the Deep State—which is to say the top senators and congressmen, heads of the Praetorian agencies, generals, top corporate guys, top academic guys, top media people—really runs the country.

Since the Deep State supports Biden and despises Trump, they’ll do everything in their power to defeat him. You’ve seen this with numerous commercials that don’t sell products so much as promote Woke and SJW ideology. Almost all corporations, universities, sports franchises, and media now make diversity hiring and social activism high priorities.

The 2016 election took them by surprise; they didn’t think it was possible. This time they’re going to be organized, and the Deep State is going to be working actively against Trump’s reelection. Whether it’s through active “de-platforming” by Google, Twitter, and Facebook, or the more subtle influence of how they present things, this time, they’re going all out to derail Trump. They have immense power and can use it in many ways.

They didn’t do much in 2016 because it hardly seemed worth the trouble; the election was thought to be in the bag for Hillary. This time it’s going to be different.

6. Cheating

The first five factors are important; they represent megatrends, tidal size influences. But let’s be candid. This election is going to hinge on who cheats the best. And the Democrats have, over the years, developed far greater expertise in cheating than the Republicans. I grew up in Chicago, and it was a joke even then. Saul Alinsky’s “Rules for Radicals” wasn’t written for the kind of people who vote Republican.

For one thing, there’s now an emphasis on mail-in votes, which makes it easier to cheat. You can register dead people as voters. You can register your dog as a voter. You could probably register 50 million Nigerian princes and get away with it. If the fraud is ever even discovered, it won’t be until long after the election. Which means it’s likely to be a contested election long after Nov 3rd.

That’s only part of it, though. A high percentage of voting machines are computerized. Fraud by hacking voting machines is apparently easy to do—and it’s pretty untraceable. It’s just a matter of planning and boldness.

One of the consequences of these widely acknowledged dysfunctions is to delegitimize the whole idea of voting. That’s possibly not a bad thing. Mass democracy inevitably degrades into a system where the poorer citizens vote themselves benefits at the expense of the middle class. Basically, mass democracy is mob rule dressed in a coat and tie. But if the populace loses faith in “democracy” during a serious economic crisis—like this one—they’re going to look for a strong man to straighten things out. The US will look more and more like Argentina. Or worse.

Remember what Stalin said: “Who votes doesn’t count. What counts is who counts the votes.”

But what about the idea of democracy itself? What does it matter the US starts to resemble a Third World country if that’s the will of the people? I’ve got to say that I don’t believe in democracy as a method of government. I understand how shocking that is to hear. Let me explain.

There’s something to be said for a few people who share traditions and culture and generally agree on how the world works, voting on who will speak for them when it’s appropriate. That’s one thing—and it can make sense. But it’s very different from a gigantic agglomeration of very different, even antagonistic, people fighting for control and power.

Winston Churchill said two things about democracy that are apposite.

One is that “Democracy is the worst form of government, except for all the others.” I would argue that’s simply not true. The alternatives are worth discussing.

The other thing that he said was, “The best argument against Democracy is a five-minute conversation with the average voter.” He’s absolutely right in that quip.

Getting back to cheating: Will foreign interference in US elections be part of the cheating? Kind of. There already are millions of foreign citizens—illegal aliens orchestrated by the left—interfering directly in the outcome by voting. That’s much more of a change than some random Russians making political comments on Facebook allegedly during 2016. Although the Russian thing isn’t even a tempest in a toilet bowl. So what if some Russian kids played around on their computers to see what they could do? It was totally trivial and meaningless.

In a way, it just proves the old saying, turnabout is fair play. For many years, the US government has cultivated regime change in foreign countries by interfering very overtly in their elections.

Why should Americans act surprised if it happens in the US?

A Counter Argument

What are the chances Trump could win, despite the six points I’ve just mentioned? There are two factors I can think of.

One is that the Dems may have overplayed their hand by first supporting, and now not denouncing the “mostly peaceful protest” (aka, riots), Defund the Police, Black Lives Matter, Antifa, and the like. People can approve or not—but they don’t want to be scared or have their lives disrupted. It may send the silent majority to the Republicans.

Second is the immense enthusiasm of Trump’s supporters. When he goes somewhere, they disrupt their lives and line-up, waiting for hours to get into the venue. It seems Biden and Harris can barely fill a coffee shop. Millions of middle Americans support Trump as if their lives depended on it. And in a way, they do.

If Trump loses the election—or more exactly, if the Democrats win—it is, in fact, going to change the nature of the US drastically and permanently. Unfortunately, that’s going to be the case even if Trump wins.

Next week I’ll follow up with what’s going to happen after the election. Stay tuned.

* * *

Disturbing economic, political, and social trends are already in motion and now accelerating at breathtaking speed. The risks that lie ahead are too big and dangerous to ignore. That’s exactly why bestselling author Doug Casey and his team just released a free report with all the details on how to survive an economic collapse. It will help you understand what is unfolding right before our eyes and what you should do so you don’t get caught in the crosshairs. Click here to download the PDF now.

via ZeroHedge News https://ift.tt/2Fx35ql Tyler Durden

Black Lives Matter Protesters In Pittsburgh Charged After Harassing, Cursing Out Diners Tyler Durden

Thu, 09/17/2020 – 20:20

Three Black Lives Matter protesters in Pittsburgh are now facing charges from police after they were identified as people involved in viral videos that showed them cursing out diners at an outdoor restaurant. One protester even chugged a person’s beer, according to Fox News.

Pittsburgh police brought the charges on Monday against Shawn Green, Kenneth McDowell and Monique Craft for the incident that took place at a restaurant called Sienna Mercato.

In video of the incident, Craft can be seen wearing a shirt that says “Nazi Lives Don’t Matter”, walking up to an older white couple, grabbing their beer off the table, and chugging it. That should help move along race relations in the country! Great thinking, Monique.

For his/her efforts (Craft is non-binary), Monique was issued a summons for theft, conspiracy and simple trespass. Craft told the Pittsburgh Post-Gazette that the video “only shows one side of the story”.

McDowell – who screamed obscenities at diners using a megaphone – was charged with possessing instruments of a crime, conspiracy, harassment and two counts of disorderly conduct. A complaint against McDowell says he swore at diners and gave them the middle finger.

You can watch video of the “protest” from CBS here:

via ZeroHedge News https://ift.tt/33DDR1d Tyler Durden

The IMF predicts that the global economy will contract by 4.9% this year, down from growth of 2.9% in 2019, while the World Bank has forecast a fall of 5.2%, the worst contraction since the Second World War.

With national economies suffering from revenue shortages, and populations in need of additional government support to mitigate the impacts of the crisis, SWFs have in many cases seen their roles transformed.

As a result of reduced income, many governments have been tapping SWFs to help balance budgets and provide stimulus to businesses or households.

This development has changed the conventional wisdom surrounding SWFs, which have combined assets estimated of around $6trn globally.

Before the pandemic the funds were seen as having limited – or a total lack of – liabilities. However, Covid-19 has seen SWFs called on to meet the implicit liabilities associated with economic shocks.

Among some SWFs, there is a growing realisation that they are no longer standalone institutions, but rather fiscal policy tools that are fully integrated into the macroeconomic management of their respective countries.

This shift has also brought about significant challenges for SWFs as they adapt to the new economic environment.

For commodity-based funds, many of which are underpinned by significant hydrocarbons exposure, the reduction in economic activity associated with Covid-19 has combined with persistently low oil prices to create twin challenges.

Meanwhile, for funds primarily based on trade surpluses, the deceleration in global trade and subsequent logistical and transport challenges have created similar hurdles.

Asset sell-off

Covid-19 has forced many of the less liquid SWFs to offload assets to generate cash.

The trend is expected to be particularly prevalent in countries with a heavy reliance on oil revenue.

For example, in Norway, where the government expects net cash flows from petroleum activities to fall by 62% this year to the lowest level since 1999, the country is expected to withdraw some $37bn in assets from its SWF, more than four times the previous record of $9.7bn in 2016.

This development is also expected to affect the Middle East, where funds will be called on to bridge fiscal deficits, which international credit ratings agency Fitch expects to constitute between 10% and 20% of GDP this year.

In Abu Dhabi, where the deficit is forecast to total 12% of GDP, the agency expects a $20bn drawdown on sovereign savings, while in Oman, tipped for a 19% fiscal deficit, analysts say as much as $8bn could be withdrawn from its SWFs.

In light of this, JP Morgan estimates that SWFs in the MENA region could dump up to $225bn in equities this year.

In addition to selling off assets to pay for budgetary spending, some SWFs have been called on to make other forms of investment.

In June Temasek, Singapore’s SWF, recapitalised domestic shipbuilding and repair conglomerate Sembcorp Marine with $1.5bn. This came after the fund channelled $13bn into flag carrier Singapore Airlines.

Such investment is a prime example of the increasing attention SWFs are paying to their home markets since the outbreak of the pandemic. While most investments remain international, domestic deals are increasing in size and frequency.

According to the International Forum of SWFs (IFSWF), domestic deals accounted for 21% of the total value of SWF investment in 2019, with this trend increasing over the past six months.

Opportunities amid disruption

While some funds have sought to offload assets, others are looking to take advantage of lower share prices during the pandemic.

Among them is Saudi Arabia’s Public Investment Fund (PIF), which – despite the downturn in the global hydrocarbons industry and its stated goal of spurring diversification – has recently made investments in international energy giants.

In April the PIF acquired around $1bn worth of stakes in European energy majors Royal Dutch Shell, Eni and Total, which was followed by a $200m investment in Norway’s Equinor.

The fund also acquired stakes in other sectors affected by the pandemic, including an 8.2% stake, valued at $369m, in US cruise ship operator Carnival, and a $300m investment in events company Live Nation.

The PIF is not the only active investor among SWFs in this difficult environment. According to data from capital markets data company PitchBook, SWFs poured $17bn into venture capital companies in the first half of the year, exceeding the 2019 full-year levels.

Chinese tech companies Tencent and Kuaishou were both significant beneficiaries, while Abu Dhabi’s Mubadala Investment Company put $3bn into Waymo, Alphabet’s self-driving technology arm.

Among some funds, there has been a broader shift towards tackling issues related to the pandemic.

“We reshuffled our priorities based on Covid-19,” Ayman Soliman, CEO of the Sovereign Fund of Egypt, told OBG.

“We looked at the issues that were emerging in the region – food security, medical security and medical supplies – and realised that these should be our top priority.”

Looking ahead

Although it can be difficult to assess the losses accrued by SWF portfolios since the outbreak of the pandemic given the opaque nature of their investments, in April JP Morgan estimated that funds would suffer total equity losses of around $1trn.

However, this recent contraction seems to be accelerating a pre-existing trend that has seen the amount of equity invested by SWFs fall from $54.3bn in 2017 to $35bn in 2019, according to the IFSWF.

In a report released in August, Bernardo Bortolotti and Veljko Fotak from the Sovereign Investment Lab, along with Chloe Hogg from the London School of Economics, wrote that “the golden age of SWFs is over”.

“Declining oil prices, mounting protectionism and increasing barriers to international capital flows have halted the spectacular rise of SWFs of the last two decades. The double whammy of the Covid-19 shock and of the new macroeconomic reality represents a quintessential challenge for an industry,” the trio wrote.

“Yet, with $6trn under management, SWFs remain major players in global finance and have the potential to mitigate some of the worst financial consequences of the current crisis.”

As countries recover from the economic recession, recent developments suggest the funds will be seen as a key tools in building resilience against future economic shocks.

via ZeroHedge News https://ift.tt/3mug2Sd Tyler Durden

“Alone In The World”: US Vows “Full” Iran Sanctions Snapback Begins Saturday Morning Tyler Durden

Thu, 09/17/2020 – 19:40

Another Iran showdown is coming at the United Nations at the end of this week after the United States finds itself isolated in claiming authority to impose ‘snapback’ sanctions on Iran:

Virtually alone in the world, the Trump administration will announce on Saturday that U.N. sanctions on Iran eased under the 2015 nuclear deal are back in force. But the other members of the U.N. Security Council, including U.S. allies, disagree and have vowed to ignore the step. That sets the stage for ugly confrontations as the world body prepares to celebrate its 75th anniversary at a coronavirus-restricted General Assembly session next week.

On Wednesday the Trump administration pledged it will move to impose “full” US sanctions on any international entity or arms company doing deals with Iran.

Per the terms of the 2015 nuclear deal brokered under Obama, a 13-year old arms embargo on Iran is set to expire October 18 of this year.

The US failed in a recent bid weeks ago to get the UN Security Council to back its efforts to extend the embargo. On Aug. 20 Secretary of State Mike Pompeo announced at UN headquarters that the US will activate snap back sanctions, which even US allies say it has no authority to do, given Trump withdrew from the deal in May 2018.

“These will be valid U.N. Security Council (actions) and the United States will do what it always does, it will do its share as part of its responsibilities to enable peace,” Pompeo said Wednesday. “We’ll do all the things we need to do to ensure that those sanctions are enforced.”

The White House is ready to go it alone, promising that all prior UN sanctions will“snap back” at 8 p.m. EDT on Saturday, according to remarks this week by newly appointed special envoy for Iran Elliott Abrams.

“We expect all U.N. member states to implement their member state responsibilities and respect their obligations to uphold these sanctions,” Abrams said at a Wednesday press briefing.

“If other nations do not follow it… I think they should be asked … whether they do not think they are weakening the structure of U.N. sanctions,” he added.

via ZeroHedge News https://ift.tt/2FJvclQ Tyler Durden

Does Critical Race Theory promote racial harmony or does it “sow division” as the Trump administration claims? And what is its relation, if any, to Marxism?

With the November election just around the corner, it’s only to be expected that President Trump would seek to rally conservative voters and drive his supporters to the polls. So, when his administration, on September 4, instructed the federal government to eliminate all training in “Critical Race Theory,” some thought it was just a red-meat stunt to excite the Republican base. Others saw it as an act of right-wing censorship and an obstruction of racial progress.

In truth, there’s much more to this development than mere politicization and censorship.

Here’s a breakdown of what the administration is doing and why it’s a welcome move.

The Executive Memo

“It has come to the President’s attention that Executive Branch agencies have spent millions of taxpayer dollars to date ‘training’ government workers to believe divisive, anti-American propaganda,” Office of Management and Budget Director Russ Vought wrote in the executive memorandum.

“Employees across the Executive Branch have been required to attend trainings where they are told that ‘virtually all White people contribute to racism’ or where they are required to say that they ‘benefit from racism,’” Vought explained.

“According to press reports, in some cases these training [sic] have further claimed that there is racism embedded in the belief that America is the land of opportunity or the belief that the most qualified person should receive a job.”

The order instructed federal agencies to identify and eliminate any contracts or spending that train employees in “critical race theory,” “white privilege,” “or any other training or propaganda effort that teaches or suggests either that the United States is an inherently racist or evil country or that any race or ethnicity is inherently racist or evil.”

The days of taxpayer funded indoctrination trainings that sow division and racism are over. Under the direction of @POTUS we are directing agencies to halt critical race theory trainings immediately.https://t.co/dyMeJka9rt

How did it “come to the President’s attention,” and what press reports is Vought referring to?

Well, President Trump is known to watch Tucker Carlson’s show on Fox News. And days before the memo was issued, Carlson had on journalist Christopher Rufo to discuss his multiple reports uncovering the extent to which Critical Race Theory (CRT) was being used in federal training programs.

“For example, Rufo claimed, the Treasury Department recently hired a diversity trainer who said the U.S. was a fundamentally White supremacist country,”wrote Sam Dorman for the Fox News web site, “and that White people upheld the system of racism in the nation. In another case, which Rufo discussed with Carlson last month, Sandia National Laboratories, which designs nuclear weapons, sent its white male executives to a mandatory training in which they, according to Rufo, wrote letters apologizing to women and people of color.”

Rufo challenged President Trump to use his executive authority to extirpate CRT from the federal government.

As I told @TuckerCarlson tonight: I call on President @realDonaldTrump to immediately issue an executive order abolishing critical race theory from the federal government.

There is no place for this toxic, divisive, pseudoscientific ideology in our public institutions. pic.twitter.com/78J0CwNjfh

CNN’s Brian Stelter (as well as Rufo himself) traced Trump’s decision directly to the independent investigative journalist’s self-proclaimed “one-man war” on CRT, of which the recent Carlson appearance was only the latest salvo.

“It has come to the President’s attention that Executive Branch agencies have spent millions of taxpayer dollars to date ‘training’ government workers to believe divisive, anti-American propaganda.”

Selter characterized Trump’s move as a reactionary attack on the current national “reckoning” on race. He cited the Washington Post’s claim that, “racial and diversity awareness trainings are essential steps in helping rectify the pervasive racial inequities in American society, including those perpetuated by the federal government.”

So which is it? Is CRT “divisive” and “toxic” or is it “rectifying” and “anti-racist”?

Intellectual Ancestry

To answer that, it would help to trace CRT to its roots. Critical Race Theory is a branch of Critical Theory, which began as an academic movement in the 1930s. Critical Theory emphasizes the “critique of society and culture in order to reveal and challenge power structures,” as Wikipedia states. Critical Race Theory does the same, with a focus on racial power structures, especially white supremacy and the oppression of people of color.

The “power structure” prism stems largely from Critical Theory’s own roots in Marxism—Critical Theory was developed by members of the Marxist “Frankfurt School.” Traditional Marxism emphasized economic power structures, especially the supremacy of capital over labor under capitalism. Marxism interpreted most of human history as a zero-sum class war for economic power.

“According to the Marxian view,” wrote the economist Ludwig von Mises, “human society is organized into classes whose interests stand in irreconcilable opposition.”

Mises called this view a “conflict doctrine,” which opposed the “harmony doctrine” of classical liberalism. According to the classical liberals, in a free market economy, capitalists and workers were natural allies, not enemies. Indeed, in a free society all rights-respecting individuals were natural allies.

A Bitter Inheritance

Critical Race Theory arose as a distinct movement in law schools in the late 1980s. CRT inherited many of its premises and perspectives from its Marxist ancestry.

The pre-CRT Civil Rights Movement had emphasized equal rights and treating people as individuals, as opposed to as members of a racial collective. “I look to a day when people will not be judged by the color of their skin, but by the content of their character,” Martin Luther King famously said.

In contrast, CRT dwells on inequalities of outcome, which it generally attributes to racial power structures. And, as we’ve seen from the government training curricula, modern CRT forthrightly judges white people by the color of their skin, prejudging them as racist by virtue of their race. This race-based “pre-trial guilty verdict” of racism is itself, by definition, racist.

The classical liberal “harmony doctrine” was deeply influential in the movements to abolish all forms of inequality under the law: from feudal serfdom, to race-based slavery, to Jim Crow.

But, with the rise of Critical Race Theory, the cause of racial justice became more influenced by the fixations on conflict, discord, and domination that CRT inherited from Marxism.

Social life was predominantly cast as a zero-sum struggle between collectives: capital vs. labor for Marxism, whites vs. people of color for CRT.

A huge portion of society’s ills were attributed to one particular collective’s diabolical domination: capitalist hegemony for Marxism, white supremacy for CRT.

Just as Marxism demonized capitalists, CRT vilifies white people. Both try to foment resentment, envy, and a victimhood complex among the oppressed class it claims to champion.

Traditional Marxists claimed that all capitalists benefit from the zero-sum exploitation of workers. Similarly, CRT “diversity trainers” require white trainees to admit that they “benefit from racism.”

Traditional Marxists insisted that bourgeois thoughts were inescapably conditioned by “class interest.” In the same way, CRT trainers push the notion that “virtually all White people contribute to racism” as a result of their whiteness.

Given the above, it should be no wonder that CRT has been criticized as “racist” and “divisive.”

Reckoning or Retrogression?

Supporters of CRT cast it as a force for good in today’s “rectifying reckoning” over race.

But CRT’s neo-Marxist orientation only damages race relations and harms the interests of those it claims to serve.

In practice, the class war rhetoric of Marxism was divisive and toxic for economic relations. And, far from advancing the interests of the working classes, it led to mass poverty and devastating famines, not to mention staggering inequality between the elites and the masses.

Today, the CRT-informed philosophy, rhetoric, and strategy of the Black Lives Matter organization (whose leadership professed to be “trained Marxists”) is leading to mass riots, looting, vandalism, and assault. The divisive violence has arrested progress for the cause of police reform, destroyed countless black-owned small businesses, and economically devastated many black communities.

Those who truly wish to see racial harmony should dump the neo-Marxists and learn more about classical liberalism. FEE.org is the perfect place to start.

Is Trump’s Ban a Form of Censorship?

So much for CRT being a force for good. Of course, even horrible ideas are protected by the First Amendment. The government should never use force to suppress people from expressing ideas, speech, or theories it dislikes.

Critics insist that President Trump is engaged in this kind of censorship by targeting CRT.

Not so.

No one is banning White Fragility, the blockbuster CRT manifesto. No one is locking up those who preach CRT or ordering mentions of it stripped from the internet.

The memo simply says that taxpayer dollars will no longer be spent promulgating this theory to federal government employees. As heads of the executive branch, presidents have wide latitude to make the rules for federal agencies under their control. Deciding how money is spent certainly falls under their proper discretion—and it is always done with political preferences in mind, one way or the other.

It is not censorship for Trump to eliminate funding for CRT, anymore than it was “censorship” for the Obama administration to choose to tie federal contracts to a business’s embrace of LGBT rights.

Elections have consequences, one of the most obvious being that the president gets to run the executive branch. If we don’t want the president’s political preferences to be so significant in training programs, then we should simply reduce the size of government and the number of bureaucrats.

In the meantime, stripping the federal government of the divisive, toxic, and neo-Marxist ideology of Critical Race Theory is a positive development for the sake of racial justice and harmony.

{kind=link}

{kind=link}