Following what many have described as the most violent weekend yet after 86 days, or 13 weeks of pro-Democracy protests in Hong Kong, which have led to the arrest of at least 1,117 residents, where the local police is now deploying water cannon in response to “rioters” using petrol bombs, China appears to have finally had enough and on Sunday, Beijing issued a stern ultimatum to not only Hong Kong protesters, but also the West on Sunday, reiterating that it will not tolerate any attempt to undermine Chinese sovereignty over the city.

“The end is coming for those attempting to disrupt Hong Kong and antagonize China,” stated a commentary piece published by the state’s Xinhua News Agency.

According to the Nikkei, the ultimatum was directed at “the rioters and their behind-the-scene supporters” – which should be interpreted as China’s latest accusation of Western meddling, with the article warning that “their attempt to ‘kidnap Hong Kong’ and press the central authorities is just a delusion,” adding, “No concession should be expected concerning such principle issues.”

The commentary said three red lines must not be crossed:

no one should harm Chinese sovereignty,

challenge the power of the central authorities

use Hong Kong to infiltrate and undermine the mainland.

“Anyone who dares to infringe upon these bottom lines and interfere in or damage the ‘one country, two systems’ principle will face nothing but failure,” the piece declared. “They should never misjudge the determination and ability of the central government… to safeguard the nation’s sovereignty, security and core interests.”

With the protests attracting global attention, the demonstrators and the authorities are also fighting a PR battle. On Saturday, the Chinese Foreign Ministry took an unusual step of distributing images of alleged protester vandalism to the international press, in an apparent attempt to discredit the movement.

The warning came just hours after tens of thousands of people blocked roads and public transport links to Hong Kong’s airport. The demonstrations, which started in response to a proposed bill that would have allowed extradition to the mainland, have mutated into a broader rejection of Beijing’s growing control over the semi-autonomous city, with China – and even Russia – accusing the CIA of being behind the ongoing protests.

Despite recently linking his view of the trade war with Beijing to the ongoing Hong Kong protests, Trump has refused to sternly condemn the growing possibility of a Chinese crackdown, leading some to suggest that China has cobbled a behind the scenes deal with Trump, whereby it lets the US president give the impression of a modest win in the trade war in exchange for being given a carte blanche to deal with the HK protesters as it sees fit when the time comes, and with the Chinese National Day holiday coming on Oct. 1, it is almost certain that Beijing will have to regain control over Hong Kong in the coming weeks if not days.

via ZeroHedge News https://ift.tt/2MN5m2F Tyler Durden

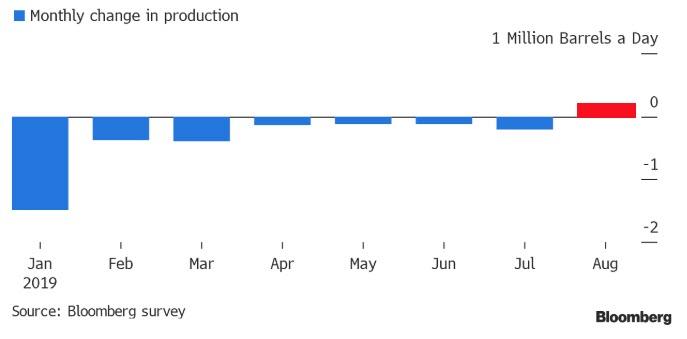

OPEC’s production increased in August thanks to Iraq and Nigeria a Reuters survey found on Friday.

OPEC’s August production has been estimated at 29.61 million barrels per day, which is 80,000 barrels per day over July’s production level.

The production increase is surprising, given that Iran and Venezuela are producing less not by choice, and continue to face uphill battles when it comes to maintaining their oil production. Saudi Arabia, too, over complied with the production cut deal again as expected, but it raised production for August slightly over July. Overall, the group is still over complying with the production quotas.

OPEC’s compliance for August is now estimated at 136%, no thanks to Iraq and Nigeria, who lifted production by 80,000 barrels per day and 60,000 barrels per day, respectively. And even though Saudi Arabia is still over complying, it lifted production in August to produce 9.63 million barrels per day.

While Iraq, Nigeria, and Saudi Arabia increased production in August, Iran’s production fell further—experiencing a 50,000 barrels per day loss for the month. US Secretary of State Mike Pompeo last week said it had successfully removed 2.7 million barrels of oil per day off the oil market since it first sanctioned the country.

Iran’s July oil and condensates exports for July fell to 120,000 barrels per day, Reuters said last week. Iran’s production for July was 2.21 million bpd. This compares to an average daily production rate of 3.55 million barrels for all of 2018.

Oil prices fell sharply on Friday, and news that OPEC’s production increased this month may press further down on prices.

And extended losses in late Sunday, early Monday trading.

via ZeroHedge News https://ift.tt/2zGfktU Tyler Durden

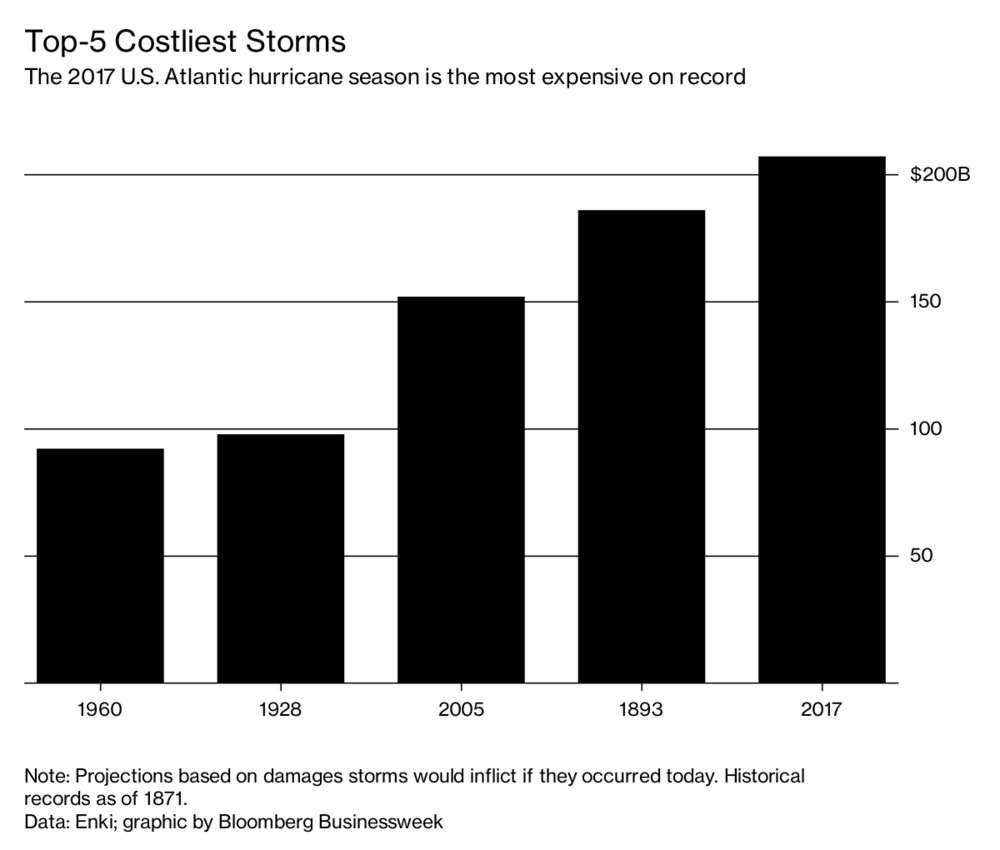

Insurances companies could be in serious trouble now that Hurricane Dorian has spent a full day dragging across the Bahamas, according to a team of analysts at UBS. After battering the Caribbean island nation with gusts of up to 220 mph, the unprecedented Category 5 storm looks to be one of the most damaging storms in recent memory.

Now that Dorian has officially cemented its position as the second-strongest storm to form in the Atlantic in modern history, UBS analysts have updated their models to reflect a broader swath of losses. It’s now believed the storm could cause total insured losses in the range of $5 billion to $40 billion, with a ‘base case’ of $25 billion, up from $15 billion a few days ago.

This could put solvency capital at risk for some firms, the team of analysts said, according to Sputnik.

The analysts estimate the 2019 hurricane season could cause about $70 billion of natural catastrophe losses, which could erode excess capital and lead to higher premiums.

Though they got some relief last year, insurers faced record bills from hurricanes, earthquakes and wildfires in 2017, as Hurricanes Maria, Harvey and Irma hammered Puerto Rico and the Continental US…

…and wildfires in California led to the most destructive season on record.

Of the big reinsurance names, UBS named Swiss Re as its least preferred stock to hold during the 2019 hurricane season, adding that a second buyback was unlikely. Meanwhile, Lancashire, Beazley and SCOR were set to see the biggest gains from an increase in premiums across the industry.

Fortunately, as of Monday morning, a ‘direct’ hit in Florida was seen as less likely, thought it’s impossible to say with any degree of certainty how the storm will make landfall in the US.

via ZeroHedge News https://ift.tt/2ZCLlS7 Tyler Durden

Germany held the first two of three important state elections over the weekend. And the results were striking. Leading up to the elections polls had the current opposition party in the Bundestag, Alternative for Germany (AfD), neck and neck with the ruling parties in both Saxony and Brandenburg.

Chancellor Angela Merkel’s ruling coalition was battered by the results but not beaten.In Brandenburg, her partners, the Social Democrats (SPD), beat AfD by 5 points, 26.3% to 23.5%, while in Saxony Merkel’s Christian Democratic Union (CDU) held onto 32% of the vote while AfD took 27.5%.

Both of these results represent more than a doubling of support for AfD in these states and bodes very well for a party that is was only formed in 2013.

And both of these results portend very well for the election in Thuringia at the end of October as well as the next general election in 2021.

So while AfD failed to win either Saxony or Brandenburg and both states will put together cartel-style governments standing for nothing, it wasn’t going to rule if they had anyway.

None of the other parties would form a coalition with them on principle and pathetic virtue signaling. And that leaves AfD’s hands clean for the future.

The preliminary seat projections in Saxony have the CDU having to partner with at least two other parties to form a government which excludes AfD.

Being the official opposition party in the Bundestag and having strong but neutered representation in these important states puts AfD exactly where it needs to be on the eve of a political and financial crisis in Europe, especially as Germany slides further into recession.

It further highlights the undemocratic means by which people like Merkel hold onto power. For a clear example of that, simply cross the Alps to Italy.

It is those in power that get the blame, and rightly so, for economic downturns and social upheaval. They’ve had the gavel and the bully pulpit and they failed to use them wisely to govern with an eye ahead on the real problems rather than their pet agendas.

In Merkel’s case that is further EU integration. She’s had sincere struggles passing on power within the CDU as she tries to exit the scene. So have the SPD.

It’s clear that both the CDU and the SPD have future leadership vacuums that will not be able to 1) hold their parties together and 2) navigate what will be the most tumultuous period of German history since the end of World War II.

So, today, if I’m Drs. Jorge Meuthen or Alice Weidel, the leadership of AfD, I’m ecstatic at the vote totals, which were in line with projections, but I’m even happier not to be in charge when the worst of the financial crisis hits the European Union next year.

Being the opposition when the world comes crashing down around your political opponents is the best position to be in.

And AfD are that today. Slowly, they are rebranding themselves as the solution for all of Germany. It’s a slower process than in, say, Italy, where the cultural identity and its relationship to political ideologies are less fraught with guilt.

Speaking of Italy. With last week’s coup, Matteo Salvini and The League are in now in the same position in Italy. Having won the battle to push Salvini out of government the Brussels’ loyal technocrats and weak-willed reformers in Five Star Movement will now bear the full wrath of the Italian people as their sell out occurs and the incipient financial crisis engulfs them.

Many Germans today are loathe to identify with anything seen as fascist. And this has hampered the growth of AfD as the wholly subservient German press has done nothing but hound them as Neo-Nazis and the rest.

But it isn’t working. Here’s the demographic breakdown of the Saxony vote.

Germany (Saxony regional election): Green GRÜNE-G/EFA; strong among young people, right-wing AfD (ID) strong among middle-aged people and CDU (EPP) strong among older generations. #ltwsn19#ltwsachsen#Sachsenwahlpic.twitter.com/76PsT6xxKh

Note even EuropeElects can’t write a tweet without lying for the establishment. The Greens are not the most popular with young people, AfD is (black bars). In fact, this chart right here is what will have Merkel shaking uncontrollably this morning.

The post-WWII social-democratic state is under severe attack at a generational level and it won’t change. There has been a break in the generational identity along party lines across most of Europe. The Brexit Party’s vote in the U.K. in May is a prime example of that. A party five weeks old beat parties entrenched at the top of British politics for more than a century.

FYI, the same dynamic is occurring in Greece with Golden Dawn. If not for the patently absurd ballot access laws here in the U.S. we would see a similar shift away from the Repuglicans and Demoncrats.

German politics will not change tomorrow with these results. But they will change. Be it in 2021 or later.

The trend is in motion. The older generation, the Baby Boomers, have failed to make their case to the younger ones. They have lost the moral legitimacy to rule and the thread of history.

They have simply grasped onto the reins of power and will hold on to the bitter end because their lack of humanity, being post-modernist, secular humanist Marxist scum, tells them to.

The best way to beat them is to hand them the rope they so willingly grasp for while drowning and let them tie it around their own neck. They created the mess that’s in motion.

They should be in power when the bills come due.

* * *

Join my Patreon and join those that see the failure in motion and Install Brave to ensure we can still talk to each other while it happens.

via ZeroHedge News https://ift.tt/2ZrDzLP Tyler Durden

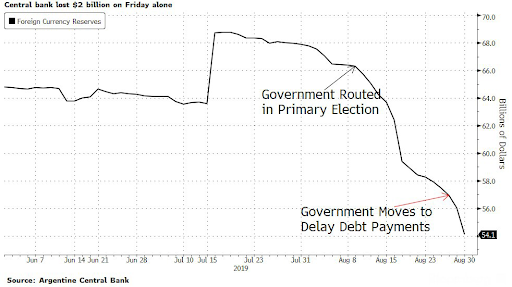

Thanks to zero liquidity (US holiday) and some repo’d reserves, the Argentine Peso has exploded higher this morning (biggest jump in over 17 years) after unveiling a new capital control plan over the weekend to stall its collapsing…everything.

As Bloomberg’s Jorgelina do Rosario and Philip Sanders note, Sunday’s move shows how the crisis has moved beyond international bond investors to affect ordinary Argentines, who may choose to save in dollar bank accounts.

In the aftermath of the Aug. 11 primary elections that showed Fernandez on course for victory in October, Argentine depositors withdrew hundreds of millions of dollars from their accounts – cash the central bank counts as part of its gross foreign reserves. These withdrawals, coupled with policy makers’ sale of dollars to shore up the peso, has led to a dramatic fall in the country’s stock of reserves.

Around $3 billion drained out of the foreign-currency reserves on Thursday and Friday alone after the government changed the terms for its short-term debt. The country risks exhausting its net reserves, which stand at under $15 billion, within weeks if it keeps losing money at this pace.

Source: Bloomberg

Having lost so much last week trying to stabilize the currency, we wonder how much today’s move took…

Source: Bloomberg

But while the currency is panic-bid, bonds are getting dumped… The 2022 bonds are down another 5 points in early trading!

Source: Bloomberg

The return of populism in Argentina is scaring the “dickens out of emerging-market investors,” said Stephen Innes, an Asia-Pacific market strategist at AxiTrader in Bangkok.

If the resurgent currency surprises you, you’re not alone as insiders tell us that black-market USDARS is trading around 64/USD – a new collapse to a new record low.

via ZeroHedge News https://ift.tt/2HGAaxF Tyler Durden

I’m wondering if the political breakdown we’re currently seeing develop across nation states is something inevitable in terms of economic evolution – a response to new technology and the changing demands societal change creates. It’s not necessarily a disastrous outlook… but its challenging to find the right investment responses to how our economies are developing.

In terms of global markets, I’ve come to the conclusion we’re currently passing through the end of one cycle – the Era of Globalisation. We’re likely to see more turmoil as the current economic and political foundations continue to crumble. The next cycle is going to be very different in terms of implications of trade, growth, utility, and the way in which society works – or doesn’t. A new form of capitalism perhaps? A new society? I have some ideas – which make me some kind of Neo-Keynsian… Happy to discuss anytime.

What did I miss in markets? For a whole week I didn’t open the FT, trawl Bloomberg, sneak a look at Zerohedge, or open any emails with attachments. I’ll spend today playing catch up – but the main issues remain the same:

Where does China vs US Trade War take us in the short-term?

What are the long-term implications of the end of the Globalisation Era – who will be winners and losers? (This is a massive topic – I will put some thots out later this week.)

What is the outlook for Europe – and is it relevant?

When does the UK become investible again?

What’s the right portfolio mix for a market is flux?

And, most immediately – How noisy will be the bursting of the current bond bubble be? (Some of the recent central bank comments surprised me, and inflation is on the horizon.)

Answers to these questions and a billion more will be written on the cold dead pages of financial history, but today we can only guess and offer opinions on what they might be.

I suspect the China story is about to become more complex because of Hong Kong. I reckon we’re heading towards a tragedy that will only widen the divisions between East and West. If the UK was truly smart we’d be offering the 170,000 Hong Kong people hold British Overseas passports UK residency rights.

Realistically, the protestors have zero chance of achieving democracy, and they must know that. The protests are impressive, but poking a hornet’s nest is never smart. Eventually China will clamp down or the Hong Kong economy becomes irrelevant. The cynical position for the US is a win/win: Pro-democracy protests will ultimately undermine Xi’s authority, while precipitous action by China will allow the US to claim the moral high-ground. But the protestors will be very mistaken if they expect the US to bail them out. Hong Kong isn’t on the US list. But is full of smart, well educated UK passport holders who could be of great use here in the UK. (Years ago someone proposed the UK gives Hong Kong 100 square miles of otherwise empty land, and 50 years later it would be the richest city in Europe!)

I have no opinion on Boris’s constitutional shenanigans – if we have to destroy democracy to achieve it, well I guess that’s what it takes. It looks to be more of the same. Let’s wait and see what happens.

via ZeroHedge News https://ift.tt/32kGRNL Tyler Durden

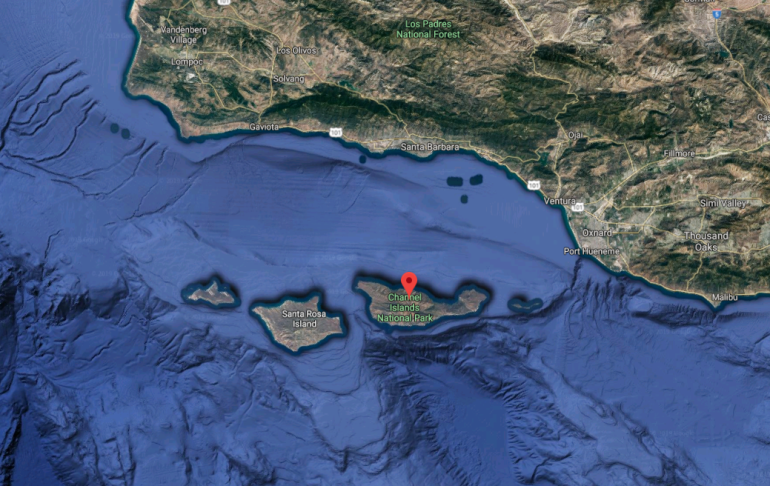

A boat fire off the Ventura County coast in California has left 34 people dead, according to KTLA, citing Ventura County fire department officials.

A Google Maps satellite image shows Santa Cruz Island. Via KTLA

According to the US Coast Guard, a rescue operation on the 75-foot boat near Santa Cruz island was still underway as of 5:43 a.m., however they did not confirm any fatalities.

In a Monday morning tweet, the USCG Los Angelessaid that “a group of crew members has been rescued (one with minor injuries) and efforts continue to evacuate the remaining passengers.”

The vessel was reported as being on fire. The a group of crew members has been rescued (one with minor injuries) and efforts continue to evacuate the remaining passengers. https://t.co/ojaSdUTHXd

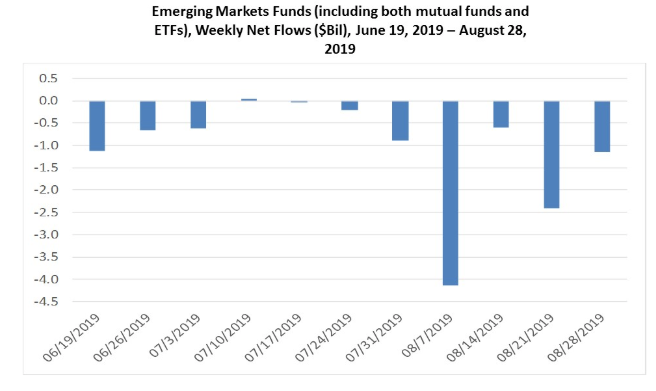

Lipper’s Emerging Markets Funds have experienced their worst-ever net outflows during 3Q19. The mass exodus is due to a combination of factors, likely caused by an escalation of the trade war between the U.S. and China this summer, a global synchronized slowdown that is wreaking havoc on emerging market countries, and a strong dollar that has sent emerging market currencies into a tailspin.

“Lipper’s Emerging Markets Funds peer group (including both mutual funds and ETFs) experienced net outflows of $1.1 billion for the fund-flows trading week ended Wednesday, Aug. 28. This negative net flow marked the tenth net outflow in the last eleven weeks for the peer group during which over $11.8 billion has left the group’s coffers. As part of this slump, the emerging markets funds group suffered the worst weekly net outflow in its history (Lipper began tracking fund flows data for this group in 1993) as $4.1 billion left during the fund-flows week ended Aug. 7. The group has recorded a net negative flow of $10.2 billion for the quarter to date putting it on pace to surpass the second quarter of 2013 (-$13.7 billion) for its worst quarterly fund flows result ever,” as per a new report via Refinitiv.

Most of the -$8.6 billion net outflow during 3Q19 for emerging market funds have been seen in ETFs as opposed to mutual funds (-$1.6 billion): iShares MSCI Emerging Markets ETF (EEM, -$5.6 billion) and iShares Core MSCI Emerging Markets ETF (IEMG, -$2.6 billion) were the two largest individual negative net flows for ETFs. GMO Emerging Domestic Opportunities Fund(-$292 million) was the largest net outflow amongst mutual funds.

Emerging markets are at the mercy of the U.S.-China trade war after investors spent an exhausting summer pivoting between disappointment and optimism for a possible trade truce.

Last week, President Trump told reporters that he held “high-level talks” with China about the trade war, adding “this is the first time I’ve seen them where they really want to make a deal.”

China countered by saying there were never any talks. And CNN reported that: “Instead, two officials said Trump was eager to project optimism that might boost markets and conflated comments from China’s vice premier with direct communication from the Chinese.”

With no trade deal in sight, at midnight on Saturday, the Trump administration slapped tariffs on $112 billion in Chinese imports. One minute later, at 12:01 am EDT, China retaliated with higher tariffs being rolled out in stages on a total of about $75 billion of U.S. goods.

The whipsaw in sentiment in the last week of August into early Septemeber will weigh on emerging markets in the weeks ahead. Investors will be watching the Federal Reserve for more hints of rate cuts ahead of the next meeting on Sept. 18.

“For EM prospects to improve, we would need to see the Fed turning more proactively dovish and/or trade tensions abating,” Morgan Stanley strategist James Lord wrote in a note. “Neither of these outcomes seem likely for now.”

The emerging market trade has been stuck in a rut for the last 82 weeks, with severe headwinds from a strengthening dollar and a trade war that has amplified the global downturn in growth.

September could be another painful month, with more outflows expected in emerging market ETFs and mutual funds.

via ZeroHedge News https://ift.tt/2PCzxeZ Tyler Durden

What happens when these monstrous speculative bubbles pop?

Let’s start by stipulating that if I’d taken a gummit job right out of college, I could have retired 19 years ago. Instead, I’ve been self-employed for most of the 49 years I’ve been working, and I’m still grinding it out at 65.

By the standards of the FIRE movement (financial independence, retire early), I’ve blown it. The basic idea of FIRE is to live frugally and save up a hefty nestegg to fund an early comfortable retirement. As near as I can make out, the nestegg should be around $2.6 million–or if inflation kicks in, maybe it’ll be $26 million. Let’s just say it’s a lot.

You’ve probably seen articles discussing how much money you’ll need to “retire comfortably.” The trick of course is the definition of comfortable. The conventional idea of comfortable (as I understand it) appears to be an income which enables the retiree to enjoy leisurely vacations on cruise ships, own a boat and well-appointed RV for tooling around the countryside, and spend as much time golfing or boating as he/she might want.

FIRE retirees might opt for socially aware volunteer work or hiking trips in remote regions. Whatever the activities, the basic idea here is: retirement = no work = enough cash to do whatever I please.

Needless to say, Social Security isn’t going to fund a comfortable retirement, unless the definition is watching TV with an box of kibble to snack on.

Where do you put your expanding nestegg so it earns a positive yield? In the good old days, regular savings accounts earned 5.25% annually by federal law. Buying a house was not a way to get rich quick, it was more like a forced savings plan, as over time real estate earned about 1% above the core inflation rate.

But all the safe ways of securing a return have been eradicated by the Federal Reserve. The Fed’s “fix” for economic stagnation was to financialize the U.S. economy, effectively eliminating low-risk returns and forcing everyone to become a speculator in high-risk financial casinos.

As a result, the saver seeking a yield above zero is gambling that all the asset bubbles don’t all pop before he/she cashes out. If the bubbles keep inflating steadily for another decade, making assets ever-more overvalued and unaffordable, then maybe the saver can exit the asset bubbles with the desired nestegg. But what if the bubbles in stocks, bonds, real estate, etc. pop?

What are the chances that monumental bubbles in stocks, bonds and real estate will continue inflating for another decade? Most gigantic asset bubbles pop after five years of expansion. The current bubbles are in Year Ten of their speculative expansion, and it seems highly unlikely that they will be the only bubbles in the history of humanity to never pop.

If the current bubbles follow the pattern of all other speculative credit-driven bubbles, they will pop, without much warning and with devastating consequences for all those who believed the bubbles couldn’t possibly pop.

Which leads to another strategy entirely: focus not on retiring comfortably, but on working comfortably. Line up work you enjoy that can be performed in old age. That’s a much safer bet than counting on the bubble-blowing machinery of the Fed to keep inflating speculative bubbles that magically never pop.

Although nobody wants to talk about it, state and local government pensioners are dependent on bubbles never popping, too–not just asset bubbles like stocks but bubbles in the sales, income and property taxes that fund their pension plans.

What happens when these monstrous speculative bubbles pop? Trillions in phantom wealth vanish, pension funds go broke, states, cities and counties are insolvent, and nesteggs invested in speculative assets dry up and blow away.

To quote Jackson Browne: “Don’t think it won’t happen just because it hasn’t happened yet.”

After futures tumbled sharply lower when they re-opened for trading on Sunday night, following a weekend in which the US and China did in fact activate a fresh round of reciprocal tariffs contrary to the market’s whisper expectations for a delay, stocks have staged another remarkable comeback with futures now virtually unchanged from their Friday close…

… as Europe’s Stoxx 600 Index rose 0.7% to session highs as of noon London time, climbing to the highest level in a month and extending its winning streak to a third session, as health care and utility stocks are the best sector performers, each rising 1.2%, closely followed by telecoms and financial services.

Earlier in the session, Asian stocks were mixed, with Singapore and the Philippines leading declines. The Topix slipped 0.4%, dragged down by Daiichi Sankyo and SoftBank Group. The Bank of Japan cut bond purchases for a second time in two days in a bid to stop benchmark yields from falling to record lows. Meanwhile, despite the escalation in trade war, the Shanghai Composite Index advanced 1.3%, with Ping An Insurance Group and China Shenhua Energy among the biggest boosts. The catalyst for the Chinese rebound: the Chinese government said it will maintain “reasonably ample” liquidity and “reasonable growth” in aggregate financing, while the latest monthly Caixin PMI gave investors hope that China’s manufacturing sector may finally be bottoming after it printed at 50.4, its first expansion in two months, and beating expectations of a 49.8 print, even as the official NBS Mfg PMI dropped again, earlier in the weekend, sliding to 49.5, and just barely missing expectations. Needless to say, the algos focused on the good news, and ignored the bad.

As Goldman wrote, “in contrast to the fall in NBS manufacturing PMI in August, the Caixin manufcturing PMI implied stronger growth momentum in the manufacturing sector” even though according to its analysis, the “NBS manufacturing PMI in general has a higher correlation with industrial production growth, compared with the Caixin manufacturing PMI (although both PMIs’ correlation with industrial production appeared to have weakened in recent months). The Caixin manufacturing PMI appeared to be more closely correlated with concurrent export growth.” As a result, “the better August reading could also reflect support from trade front-loading ahead of higher tariffs on exports to the US”, according to Goldman. Not only that, but the production shutdown ahead of October 1st National day might have also front-loaded production activities to August. If so, don’t tell that to the algos, who used the Caixin print as the basis for what has now turned into a worldwide rally, even though for yet another day the yuan refused to rebound and the jaws between the Chinese currency and equity futures have continued to grow.

Naturally, with US markets closed for labor day holiday, volumes are dismal, and US equity markets and cash Treasuries won’t trade even though treasury futures edged lower while the Bloomberg dollar rose for the sixth consecutive day, hitting a fresh two year high (as a reminder, the broad trade-weighted dollar remains at all time highs).

“Broad market activity and trading volume are likely to be somewhat muted today,” Simon Ballard, a macro strategist at First Abu Dhabi Bank, wrote in a note. While it should mean a quiet start to the week, “the net cautious tone seems set to dominate investor sentiment,” he said.

In the U.K., the pound fell and gilts rose a day before Parliament re-convenes in a potential showdown over a possible no-deal Brexit, while a barometer of the country’s manufacturing dipped to its lowest level in seven years.

As we enter the historically most volatile month of the year, investors are still reeling from the August rollercoaster that saw a collapse in Treasury yields and declines for equities globally which however were largely recovered on hope that a trade deal will emerge (narrator: it won’t).

Meanwhile, in commodities, crude oil struggled for traction after its first monthly drop since May amid fears that the fading global economic growth will hurt fuel demand. Also keeping a lid on sentiment are demonstrations in Hong Kong, where a senior official said he won’t rule out imposing an emergency law in a bid to wrestle back control after protesters caused major disruptions to the city’s international airport over the weekend.

Elsewhere, America’s southeastern coast braced for Hurricane Dorian, tied as the most powerful storm to hit land anywhere in the Atlantic, after it inflicted colossal damage to the Bahamas. Also notably over the weekend, Argentina’s troubled government imposed currency controls to halt the flight of dollars out of the country as it teeters on the brink of default. Turkey’s lira rose after data showed the economy shrank less than expected in the second quarter.

Top Overnight Headlines from Bloomberg

Trump administration slapped tariffs on $110 billion of Chinese imports Sunday, marking the latest escalation in a trade war. China’s retaliated with higher tariffs being rolled out in stages on a total of about $75 billion of U.S. goods

Argentina’s government imposed capital controls to halt a slump in FX reserves and the peso that has pushed the country to the brink of default

Boris Johnson’s summer is over. The week that could determine how long he remains prime minister — and how or whether Britain leaves the European Union — is about to begin

Bank of Japan cut bond purchases for a second time in two days as the benchmark yield hovers near record lows. The central bank offered to buy 140 billion yen of 10-to-25y securities, down from 160 billion yen at its prior operation

Italy’s premier-designate Giuseppe Conte said he plans to present a list of key ministers and a new government program to President Sergio Mattarella between Tuesday and Wednesday as he seeks to hold together a ruling coalition

Angela Merkel’s ruling coalition stemmed a surge by Germany’s far-right populists in two elections in the former communist east. The anti-immigration Alternative for Germany trailed the incumbent Social Democrats by 2 to 3 percentage points in the state of Brandenburg, according to TV projections

Riot police patrolled key subway stations on Monday morning ahead of a planned strike that threatens to disrupt transportation in Hong Kong after another weekend of chaos left travelers stranded at the airport

Major European indices are firmer [Euro Stoxx 50 +0.4%], as markets initially struggled for clear direction, after the downbeat Asia-Pac session as the additional US levy on Chinese goods and China’s retaliatory tariffs came into effect alongside today’s US market holiday; before taking a positive line. Notably, the FTSE 100 (+1.5%) is outperforming its peers, as exporters benefit from the subdued Sterling due to the ongoing Brexit narrative over PM Johnson’s prorogation and the increasing likelihood of a no-deal outcome, whilst downbeat UK manufacturing PMI further weighed on the currency. Sectors opened the session all in the green but have since deteriorated somewhat to a mixed performance. In terms of individual movers, AstraZeneca (+3.3%) are topping the FTSE 100 after positive Phase III trial results; just below the Co. on the Stoxx 600 this morning is Adecco (+2.2%) after being upgraded to outperform from neutral at Credit Suisse. At the other end of the spectrum, Thyssenkrupp (-0.8%) shares are lower ahead of Wednesday’s DAX 30 reshuffle, during which the Co. are expected to be demoted from the index and German listed MTU Aero Engines (+2.1%) is seen as a strong contender for the empty spot.

In FX, sterling was already looking shaky in the run up to the UK manufacturing PMI amidst reports of RHS demand in Eur/Gbp for the 9.00 am fix (perhaps residual or belated month end orders), with Cable slipping towards and just through 1.2100 amidst heightened jitters ahead of tomorrow’s new and potentially truncated Parliament term. However, the Pound briefly regrouped even though the headline print was worse than forecast and sub-components were bleak before succumbing to more selling pressure as Tory rebels continued their condemnation of PM Johnson’s move to suspend the upcoming session in an attempt to head off a no deal Brexit motion. On that note, latest reports suggest that a cross-party group will launch a bill aimed at blocking no deal within hours, and Cable is hovering just above 1.2075 awaiting further developments/news, while Eur/Gbp is holding near the top of a circa 0.9025-85 range. From a chart perspective, 1.2065 is next on the downside for Cable (August 20 low) ahead of 1.2015 (2019 base) and hefty option/barrier interest at the 1.2000 strike

USD – The Dollar is firmer almost across the board, as the DXY inches a bit further above the 99.000 handle to a marginal new ytd peak (99.109) and closer to the next line of chart resistance (99.262) in wake of additional/higher US tariffs on around 1/3 of the remaining Usd300 bn Chinese goods and Usd75 bn US exports to China in return. However, the Greenback is also gaining at the expense of rival currencies that continue to weaken of their own accord, as noted above.

EUR/CHF/CAD/AUD/NZD/JPY – The single currency derived some indirect support via the aforementioned Sterling cross activity through the run of Eurozone manufacturing PMIs, but Eur/Usd has subsequently retreated from a circa 1.1000 recovery high to print a fresh, albeit slender, yearly low at 1.0958, not far from supposed expiries at 1.0950, but away from a hefty 1.8 bn rolling off at the big figure. Meanwhile, the Franc is closer to the base of a 0.9918-0.9890 band, but outperforming vs the Euro within 1.0866-99 parameters and the Loonie has lost impetus between 1.3310-1.3340 vs its US counterpart. Elsewhere, the Aussie is meandering from 0.6715 to 0.6735 on the back of mixed Chinese PMIs overnight and a shock drop in Q2 Australian business inventories vs the Kiwi that is just keeping its head above 0.6300 following improved NZ Q2 terms of trade that has nudged Anz/Nzd down towards 1.0650 from 1.0685. The Yen has drifted towards 106.40 from just over 106.00 at one stage with Japanese PM Abe due to announce a cabinet reshuffle next week and Q2 Capex a bit better than expected.

SEK/NOK – The Scandi Crowns have both been boosted by encouraging manufacturing PMIs, and especially from Norway where the headline rebounded above 50.0 again, with Eur/Sek eyeing 10.7500 and Eur/Nok sub-10.0000.

EM – The Turkish Lira has also rebounded from worst levels with the aid of a better manufacturing PMI, but also as Q2 GDP data revealed less contraction. Usd/Try has tested 5.8000 bids/support vs a high just a few pips shy of 5.8400, but Usd/Ars may see more upside if capital controls fail to stop the rot.

In commodities, WTI and Brent futures are slightly softer, with prices just above the 55/bbl and 59/bbl levels with little by way of specific catalysts thus far, although gains in the complex are somewhat capped by the latest imposition of US and China tariffs in which China slapped a 5% levy on US crude oil exports. Despite demand woes outweighing supply concerns, it is worth keeping an eye on Hurricane Dorian which, according to the NHC’s latest update, is drifting westward with life-threatening storm surges and dangerous hurricane-force winds expected along the Florida east coast through mid-week. As it stands, production in the Gulf of Mexico has not been affected. On the geopolitical front, UK is said to be considering sending drones to near the Gulf of Oman amid its crisis with Iran, which follows comments from the UK’s Royal Navy Captain who stated that its warship has faced 115 confrontations with the IRGC since the start of July. Elsewhere, gold prices are marginally firmer, in-spite of the weaker Buck, albeit the yellow metal remains above the USD 1500/oz handle. Copper prices are lacklustre today as trade woes weighed on the red metal with little impetus derived from mixed China PMIs. Meanwhile, China’s iron ore futures rose around 6% at a point to a two-week high with desks citing robust short-term demand with Beijing rolling out more support measures to the Chinese economy. Finally, nickel prices gained in excess of 8% after the Indonesian Finance Ministry said nickel ore export ban will take effect as of January 1st 2020 (as touted), and new mineral ore export ban is only to be implemented for all Nickel Ore grades.

via ZeroHedge News https://ift.tt/2PBwC6s Tyler Durden

{kind=link}