Everyone is already stopped out and it’s not even 8am.

Barely 90 minutes after markets tanked after China vowed it retaliate imminently to Trump’s imposition of new tariffs, futures exploded higher on what was interpreted as a conciliatory headline from China that apparently reversed all the negative sentiment.

CHINA HOPES U.S. CAN MEET HALF WAY WITH IT ON TRADE ISSUE: HUA

How this was indicative of anything more than what it meant, namely tacit hope that the US would concede further without making any concessions of its own, is unclear but to algos the headline was all they needed to activate the afterburners on the BTFD program and the result was the following:

European stocks similarly pared their drop on the headline, after benchmarks had dropped as much as 1.4% earlier.

That said, suggesting that the bounce will fizzle was the response in the yuan which was barely noticeable:

Whether optimism persists is unclear, but what is clear is that for now, the pattern of futures surging after a CNBC “Markets in Turmoil” episode remains unbroken.

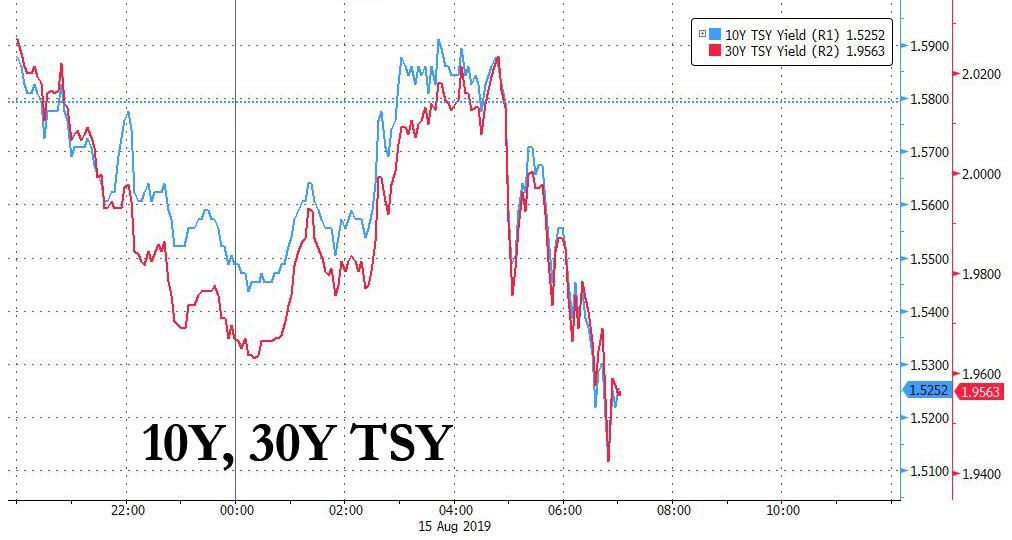

For the 4th day in a row the pattern of a stronger risk open following by a sharp drift lower in both asset prices and yields has re-emerged, much to the frustration of BTFDers.

Global stocks opened for trading on the right foot, with US equity futures initially rising despite 30Y yields falling to all time lows below 2.00% late on Thursday, after several late evening tweets by Trump seemed to indicate further conciliation between the US and China in the ongoing trade war while the PBOC finally fixed the yuan slightly stronger at 7.0268, vs 7.0312 one day before, if slightly weaker than expected 7.0236. However, it all ended with a bang, with S&P futures falling hard, and signaling another weak open for U.S. stocks, which fell 3% on Wednesday on rising recession fears …

… and European stocks slumping after China stepped up its trade-war rhetoric, vowing imminent retaliation against the US, and roiling markets that had been starting to calm. The result: US traders walking in to another sea of red.

Treasuries and European bonds rallied, with the 10Y yield sliding further, and dropping as low as 1.51% while the 30Y dropped deeper into record territory, sliding as low as 1.95%, a new all time low.

“The only game in town is the central banks, hence the bond markets are rallying,” said Peter Schaffrik, global macro strategist at RBC Capital Markets. “We have regional bonfires in Hong Kong, Argentina, Japan against South Korea, and none of these are going away easily; each and every one is not necessarily strong enough to cause trouble.“

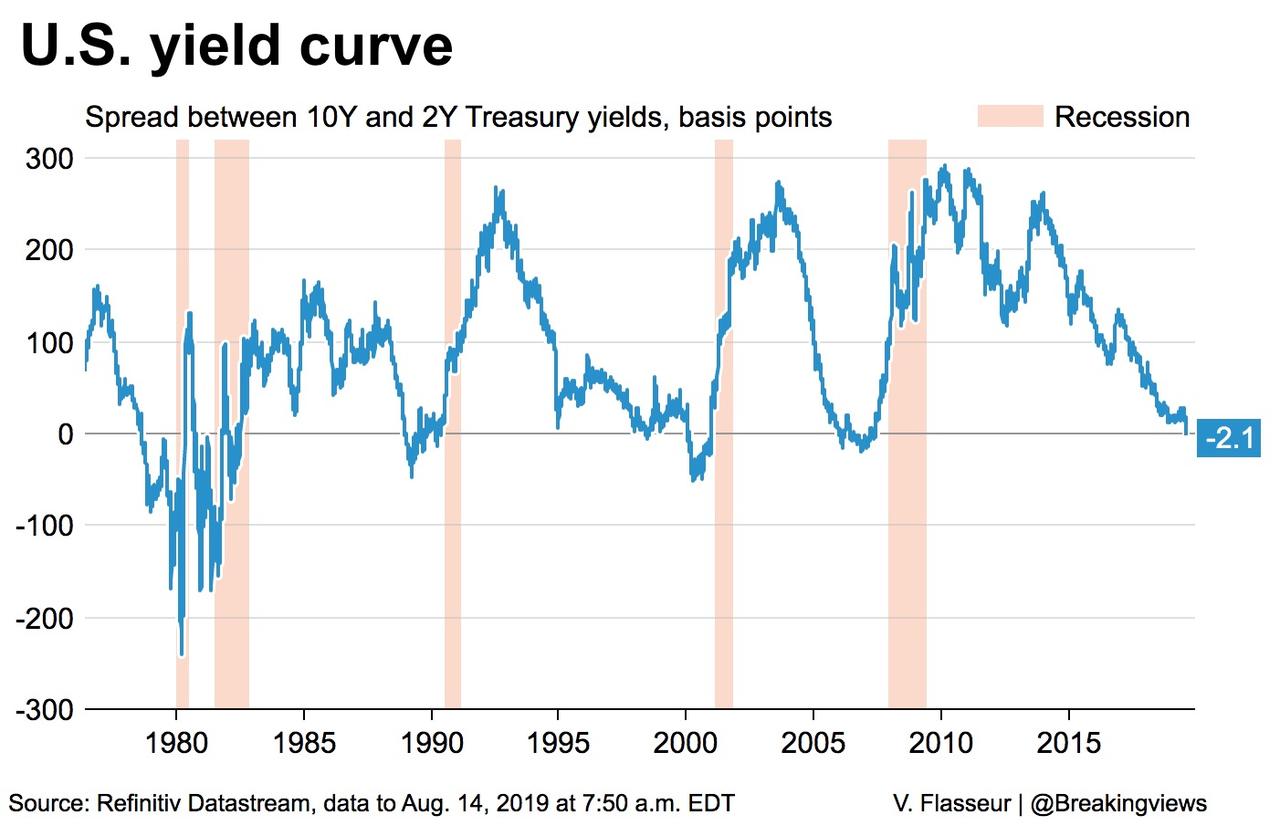

As widely discussed on Wednesday, recession fears grew on Wednesday after the 2s10s TSY spread inverted for the first time in 12 years, when the same yield curve inversion presaged the 2008 recession, and pretty much every other recession in the past 50 years.

“We have seen stocks trading very poorly as a result of the yield curve inversion, so that will be flashing some additional warning lights for the Fed that they have to do more,” said Andrea Iannelli, investment director at Fidelity International. “The only question is, can the Fed out-dove the market? At the very least they will have to match market expectations in the short term.”

So far the Fed is failing to out-dove the market, and the MSCI Asia Pacific Index declined, led by energy and health-care firms, after an inverted Treasury yield curve spurred worries over a possible recession. Country benchmarks were mixed, with Australia falling and Hong Kong advancing, while trading volume jumped across the region. Japan’s Topix retreated 1% to a seven-month low, as electronic firms and retail giants weighed on the gauge. The Shanghai Composite Index reversed earlier losses to close 0.3% higher, with Ping An Insurance and Foxconn Industrial Internet among the biggest boosts. China’s central bank added liquidity to the financial system amid prolonged trade tensions with the U.S.

After initially trading higher, Europe’s Stoxx 600 slumped as much as 0.5%, erasing earlier gains, after China’s surprise warning it would have to take countermeasures after the latest trade war salvo. The Chinese comments sent London and Frankfurt lost over 1%.

Meanwhile, in rates German 30-year yields dipped below minus 0.2% for the first time. Ten-year yields touched a record low of minus 0.67% with Sept. bund futures rising +25 ticks to 178.56; France 10y -1bp to -0.38%; Italy 10y +1bps to 1.51% Also notable: Europe’s 50Y swap rate turned negative for the first time ever.

Meanwhile, across the Atlantic, and as noted above, Treasuries outperformed bunds, while core bonds lead gains over semi-core peers and curves flatten. Italian bonds are steady with futures volumes running at less than half the 10-day average. Gilts rose amid haven buying even as U.K. retail sales for July beat the median estimate.

What sent the U.S. curve over the brink into inversion was German data on Wednesday that showed the economy had contracted in the quarter to June. That came on the heels of dire Chinese data for July. The British yield curve also inverted. The German curve is at its flattest since 2008.

The growth panic comes amid economic stress in Argentina and some other emerging markets, fears of Chinese military intervention in Hong Kong and trade tensions that show no sign of abating.

“Hoping for the best on the policy front but positioning for the worst on the economic backdrop seems to be the flavor of the day,” said Stephen Innes, a managing partner at Valour Markets. “The Fed, now out of necessity alone, will need to adjust policy much more profoundly than they expected.”

In FX, the dollar index .DXY was down at 97.862, with the euro – which has now emerged a carry funding and safe haven currency just like the yen – up at $1.1155; and speaking of the yen, it was flat at 105.8 to the dollar having earlier traded at 106.74. The currency has gained against the dollar for eight of the past 10 sessions. Excluding a mini-crash episode in January, it recently hit 17-month highs. The pound traded near the day’s high as U.K. retail sales data for July unexpectedly rose; Australia’s dollar bounced back from Wednesday’s sell-off after employment beat forecasts and damped bets on a central bank rate cut next month

In commodities, oil prices plunged with Brent crude LCOc1 losing another 2% to $58.4 a barrel, after shedding 3% overnight. Safe-haven gold was up 0.3% at $1,520 per ounce XAU=, just off recent six-year highs.

Market Snapshot

S&P 500 futures up 0.8% to 2,863.25

STOXX Europe 600 up 0.07% to 366.41

MXAP down 0.9% to 149.84

MXAPJ down 0.5% to 483.27

Nikkei down 1.2% to 20,405.65

Topix down 1% to 1,483.85

Hang Seng Index up 0.8% to 25,495.46

Shanghai Composite up 0.3% to 2,815.80

Sensex up 1% to 37,311.53

Australia S&P/ASX 200 down 2.9% to 6,408.09

Kospi up 0.7% to 1,938.37

German 10Y yield fell 0.5 bps to -0.655%

Euro up 0.06% to $1.1146

Italian 10Y yield fell 10.9 bps to 1.156%

Spanish 10Y yield rose 0.4 bps to 0.147%

Brent futures down 1.5% to $58.60/bbl

Gold spot up 0.2% to $1,519.56

U.S. Dollar Index little changed at 97.94

Top Overnight News from Bloomberg

China called planned U.S. tariffs on an additional $300 billion in Chinese goods a violation of accords reached by Presidents Donald Trump and Xi Jinping, signaling its intention to impose retaliatory measures

The recession alarm bell ringing in U.S. government bond markets sent investors rushing once more to haven assets, pushing the world’s stockpile of negative-yielding bonds to another record

The inverted yield curve looks set to be a global phenomenon, with major Asian debt markets primed to mirror the moves in Treasuries as fears grow that the world economy is teetering on the brink of a recession

Germany Inc.’s outlook for the rest of the year is filled with gloom, suggesting a recession could be in the cards. Companies from Europe’s largest economy lead the list of profit warnings issued in the region during the latest earnings season

Asian equity markets conformed to the rout seen on Wall St. where all major indices fell around 3% and the DJIA slumped 800 points in its worst performance YTD after recent weak data from China and Germany, with recession fears also stoked after the US 2s/10s curve inverted for the first time since 2007. ASX 200 (-2.9%) and Nikkei 225 (-1.2%) were lower in which the energy sector led the declines in both indices after similar underperformance stateside following a near-5% drop in crude prices and with Australia mulling over a slew of earnings releases, although gold stocks have bucked the trend as the stock sell-off spurred safe-haven appeal. Hang Seng (+0.7%) and Shanghai Comp. (+0.3%) were heavily pressured at the open but with downside later stemmed after continued PBoC liquidity efforts in which it injected CNY 30bln through reverse repos and CNY 400bln through 1yr MLF, while reports that Hong Kong Airport resumed normal operations and with strength in China Unicom post-earnings helped soften the blow for Hong Kong which briefly turned positive. However, the recovery in the Hang Seng was short-lived due to the broad risk averse tone and with losses in index heavyweight Tencent following mixed earnings and a cautious outlook. Finally, 10yr JGBs printed fresh highs as the global recession fears spurred a safe-haven bid, which saw the 10yr, 20yr and 30yr JGB yields at their lowest in more than 3 years. This coincided with the US 2s/10s yields winding in and out of inversion and the US 30yr yield dropping below 2% for the first time on record, while mild support was also seen following stronger results at the 5yr JGB auction.

Top Asian News

Hong Kong and China Stocks Rise in Shadow of Global Growth Fears

China Border Agents Probe Hong Kong Travelers’ Personal Devices

Chinese Champion Huawei Under Fire for Calling Taiwan a Country

Major European indices were initially firmer at the open but following negative updates on the US-China trade front, a further bout of risk off swept through markets [Euro Stoxx 50 -1.5%], on reports that China’s Finance Ministry say China will have to take countermeasures on US moves and their actions violate the consensus achieved at the Osaka G20 meeting. No notable over/under performers amongst indices which are all firmly in negative territory following the aforementioned US-China update, but as a reminder Italy’s equity markets are closed due to Assumption Day. Sectors are posting a slightly mixed performance but have also dropped firmly into negative territory, Energy names are lagging as oil prices remain under pressure with the added factor of Iran’s Grace 1 tanker reportedly to be released today; though the US Department of Justice are trying to seize the tanker. Also factoring on the complex is underperformance from Vestas Wind Systems (-3.5%), who represent 3.5% of the Stoxx 600 Oil & Gas index, after missing on Q2 metrics and narrowing revenue guidance. Elsewhere, RBS (-10.0%) are at the bottom of the Stoxx 600 weighed on by a downgrade at HSBC; note, the Co. are trading ex-dividend today. Returning to earnings, and at the other end of the Stoxx spectrum, are both GVC (+2.3%) and Carlsberg (+3.5%) after stating that FY outlook is ahead of expectations and confirming FY guidance with organic beer volume higher by 1.4% YY respectively.

Top European News

Vestas Profit Misses Forecasts as Wind Turbine Revenue Falls

German Profit Warnings Signal Trade Woes May Trigger Recession

In FX, the upbeat jobs data has helped the Aussie withstand another bout of risk aversion prompted by an official blast from China on the trade front and reiteration that Beijing will retaliate with countermeasures against the additional Usd300 bn tariffs that contravene the G20 truce agreement. Aud/Usd is holding firmly above 0.6750, albeit off 0.6790 overnight highs spurred by a significant beat in the payroll count vs expectations, and mainly due to full time workers. Similarly, Sterling got an unexpected lift from UK retail sales data confounding consensus for some payback after previous excesses, but Cable continues to meet resistance around 1.2100.

JPY – The Yen is back to roughly flat vs the Dollar and most other currency counterparts after a sudden slide in early EU trade that is still baffling market participants and pundits given no clear catalyst for the move. For the record, factors ranging from in incorrect order to official intervention have been touted, and clearly the speed of the sell-off did trigger stops and chart-based transactions, while a more macro or fundamental motive could have been a back-up in US Treasury yields and curve dis-inversion. However, risk aversion has resurfaced amidst the latest Chinese sabre-rattling and Usd/Jpy is back below 106.00 from circa 106.80 at one stage.

NOK – The Norwegian Crown has also been volatile within 10.0470-9.9720 parameters against the Euro, as the Norges Bank removed specific reference to next month when maintaining guidance for further policy normalisation this year due to heightened external risks and uncertainty. Nevertheless, it remains on track for more divergence in terms of benchmark rates compared to G10 and many if not all other global Central Bank peers, bar the Riksbank.

EUR/CAD/CHF/NZD – All relatively rangebound vs the Greenback even though overall sentiment has taken another turn for the worse after tentative signs of stability. The single currency is stuck between 1.1155-35, the Loonie is pivoting 1.3300, while the Franc has tracked its safe-haven Yen peer to a degree from around 0.9755 to 0.9725, and the Kiwi is straddling 0.6450, albeit largely on the downside towards 0.6425.

EM – Amidst widespread deviation for global/general and more specific or unique reasons, perhaps the rebound in Usd/Cnh from circa 7.0305 lows to 7.0630 is telling/ominous after 7.0268 Usd/Cny fix. Note also, Hong Kong has slashed its 2019 GDP projection to exacerbate global growth concerns, though the Government has injected Hkd 19.1bn via economic measures to try and ward off recession.

In commodities, Brent and WTI prices are firmly in negative territory, post the US-China updates, and have dipped below the USD 59.00/bbl and USD 55.00/bbl levels respectively which had been somewhat of a base for the benchmarks overnight after yesterdays significant downside for the complex, which saw Brent settle lower by around 3% on the day. On the supply/geopolitical front reports indicate that it is likely Iranian tanker Grace 1 will be permitted to leave Gibraltar as Chief Minister Picardo will not renew the vessels detention order which expires on Saturday; after which a court is to decide on the next steps. However, reports indicate that the US Department of Justice has applied to seize the tanker, which casts some doubt over the likelihood of the vessels near-term release. As a reminder prior to the vessel’s seizure reports indicated that it had loaded a 2mln/bbl cargo in Iranian waters around mid-April. Elsewhere, tomorrow sees the delayed release of OPEC’s monthly oil market report, focus will be on whether it takes a similar stance to the IEA and EIA reports in cutting 2019 world oil demand growth forecast. Turning to metals, where spot gold (+0.4%) remains above the USD 1500/oz mark as the market has settled somewhat from yesterday’s significant risk-off moves, but didn’t benefit much from the aforementioned trade headlines; the data slate ahead includes a number of notable US data points, which may spark further bouts of global growth worry if the prints are weak. Separately, copper prices are similarly little changed in-line with the largely tentative market sentiment thus far.

US event calendar

8:30am: U.S. Initial Jobless Claims, Aug. 10, est. 212k, prior 209k

8:30am: U.S. Retail Sales Advance MoM, July, est. 0.3%, prior 0.4%

8:30am: U.S. Empire Manufacturing, Aug., est. 2.0, prior 4.3

8:30am: U.S. Philadelphia Fed Business Outl, Aug., est. 9.5, prior 21.8

9:15am: U.S. Industrial Production MoM, July, est. 0.1%, prior 0.0%

4pm: U.S. Net Foreign Security Purchases, June, no est., prior $3.5b

DB’s Craig Nicol concludes the overnight wrap

A mere 4,453 days had passed since the last time the US 2s10s curve was negative. That was until yesterday morning when the curve struck a low of -1.9bps. It ebbed and flowed around 0 for most of the day after that before closing the US session at +0.1bps. Still, the symbolic nature of the curve inverting is not to be underestimated. In fairness all of the other frequent measures of the yield curve have already inverted, namely the 3m10s (-37.8bps), 3s5s (-2.8bps), 2s5s (-8.0bps), and 18m3m-3m (-58.0bps). However, as we’ve discussed on many occasions, the 2s10s curve has the greatest power as a recession indicator in our view.

In fact, Jim must have had a dull day on holiday as he kept on emailing us about the 2s10s inversion. In the end he asked us to put this para in this morning to reflect his view. “Although other measures of the US yield curve have progressively inverted over the last few quarters, for me yesterday’s 2s10s inversion is the one that worries me most. In my opinion, it has the best track record for predicting an upcoming recession over more cycles than any of the others. Indeed, every inversion since 1956 has seen a recession follow. Although the median length of time to a recession is 17 months, credit spreads have pretty much exclusively widened from the point of inversion onwards (see p7 of Yield Curve 101 here ). Of those 2 of the 9 recessions since the 1950s took more than 2 years to materialise after the first inversion though. The first in the mid-1960s (took nearly 4 years) was due to a Fed policy error where the Fed didn’t raise rates as expected (they actually cut) with inflation rising. The curve re-steepened and only inverted again as the Fed reversed course and hiked a few quarters later. The recession soon followed the subsequent inversion. The second, following the May 1998 inversion, took 34 months until a recession arose but the inversion was relatively brief and occurred just prior to the Russian/LTCM crisis where the Fed rapidly cut 75bps thus re-steepening the curve. The Fed then raised rates again from 1999 and the curve re-inverted in early 2000, around a year before the actual recession. So, the conclusion is that the Fed has successfully acted before to delay the inversion turning into a recession but only on 2/9 occasions. Given that the market already prices in 65bps of cuts before year end it feels like they might need to out-pace that to make it 3 out of 10 where they’ve delayed the recession. I should say that our analysis uses closing prices, and we actually closed at 0.1bps last night so I have to be a bit careful here. But having spent most of my career suggesting that this was the most reliable indicator that the US cycle is entering its last act, I have to become far more negative now it looks likely to be triggered, especially given the history of credit spreads immediately after. As an aside, I don’t think this time is different because of term premium being much lower and global QE etc. as we think the causality is through animal spirits. In an inverted yield curve environment, this gets increasingly drained and thus impacts financial and economic activity. So I really don’t care why the curve inverts, just that it does. Anyway, see our “Yield Curve 101” link above for more and I’ll go back to steeper and steeper mountains in the Alps (no flat bits here) and hand you back to Craig and Quinn.”

That move for the curve included a 12.5bps rally for 10y Treasuries which saw them break below 1.60% to close at 1.580%, although this morning they’ve pushed on further to 1.549%. That puts them just 18.9bps above the 2016 lows now. In addition to that, the 10y real yield turned negative yesterday for the first time since October 2016. As for 30y yields, they have dipped below 2% for the first time ever overnight, currently trading at 1.966%, while 2y yields are trading at 1.557% which compares to a closing level on Tuesday of 1.669%. It’s quite amazing to think that 30y yields are also now below the effective Fed Funds rate. It was a similar story in Europe too yesterday, where 10y Bunds dropped -4.1bps and to a new low of -0.654%. Spain and Portugal are now within 14bps and 16bps of being negative at the 10y, while that Austrian 100y bond is now trading at a cash price of over 200. That corresponds to a yield of 0.689%. Not to be outdone also, the 2s10s Gilt curve also briefly turned negative yesterday.

While the 2s10s curve turning negative no doubt compounded the risk-off yesterday, the reality is that sentiment was already hit hard by that weak China data and then later by confirmation that Germany’s economy contracted in Q2 (more on that below). The trade rhetoric didn’t help at the margin too with commerce secretary Wilbur Ross telling CNBC that there is no date set for US-China trade talks while later on White House trade advisor Peter Navarro said in an interview with Fox that the US “can’t meet China halfway” and that “seven structural issues” still remain. Interestingly one of those was a reference to “hacking,” which hasn’t been a clear part of the trade talks so far and is likely to present an additional hurdle to a deal. Nevertheless, President Trump later tweeted overnight that “Good things were stated on the call with China the other day.” He also said that the tariff postponement to December “actually helps China more than us, but will be reciprocated.

Unsurprisingly, equity markets had a day to forget. The S&P 500, DOW and NASDAQ tumbled -2.93%, -3.05% and -3.02%, respectively, with the move for the S&P 500 the second worst since December. Sector wise, energy and financials fell the most with the S&P 500 banks index actually tumbling -4.29% for the biggest daily loss since 4 December. That index has now fallen on 8 of the last 11 days and is back to trading at the lowest since March. The moves were incredibly broad-based, with 99.4% of S&P 500 companies trading lower, which was the worst ratio since February 2018. Other risk assets also struggled mightily yesterday too. In Europe the STOXX 600 closed down -1.68%. EM equities shed -2.88% and currencies retreated, highlighted by the South African rand (-1.83%), the Brazilian real (-2.10%), and the Argentine peso (-7.36%). In commodities oil fell -3.27%, while gold gained +0.99% to reach $1,516, its highest level since 2013. Meanwhile HY credit spreads in the US and Europe were +24bps and +3bps wider, respectively. On that, yesterday we published a short note which makes six observations about recent price action in the US IG and HY credit market. See the link here for the full report.

Overnight, markets are mostly trading lower in Asia too, however the good news at least is that most bourses have pared back heavier declines at the open. As we go to print the Nikkei (-1.29%), Shanghai Comp (-0.62%) and Hang Seng (-0.17%) are all in the red along with the ASX (-2.61%) following the latest employment data in Australia. Meanwhile, S&P 500 futures are up +0.19% as we type. In rates, with the US 2s10s curve hovering near where it closed last night, bond markets have rallied through much of Asia too with 10y JGBs in particular now down to -0.247% and approaching the 2016 low of -0.295%.

Meanwhile, and in some non-curve related news, with 11 weeks to go until the UK’s scheduled departure from the EU on October 31st, Labour leader Jeremy Corbyn has written to other MPs who oppose a no-deal Brexit, calling on them to support a “strictly time-limited temporary government” led by Corbyn as Prime Minister, with the purpose of getting an Article 50 extension and calling a general election. However, with a number of MPs in other parties, including the anti-Brexit Liberal Democrats, opposing Corbyn as PM, this may prove a difficult vision to actually realise. Corbyn’s letter also said that he would call a no-confidence vote “at the earliest opportunity when we can be confident of success.” The House of Commons won’t be sitting again until September 3rd though, so there’ll be at least a couple of weeks before any moves like this could take place.

In other news, the data highlight was the negative GDP print in Germany, which showed the economy contracted -0.1% qoq as expected, which certainly did not help sentiment. Our economists have lowered their full-year 2019 German growth forecasts to 0.3% from 0.7%, see their full note here . Elsewhere, French CPI was confirmed at 1.3% yoy and -0.2% mom, though UK CPI came in higher than expected at 2.1% yoy versus expected 1.9%. The UK’s core CPI metric printed at 1.9%, 0.1pp stronger than expected.

On the Fedspeak front, the only notable comments from St. Louis President Bullard, who said that “macroeconomic outcomes are quite good for the US.” He talked about the ongoing Fed policy review, saying that the key question is how to avoid getting “stuck at an inflation rate that’s lower than your inflation target.” He included negative interest rates as a potential tool, which may have contributed to the marked selloff in bank stocks, though other Fed officials have downplayed the likelihood of that tool. Next week is the Fed’s annual Jackson Hole conference, where it is possible that Powell and other senior officials could speak. We are likely to get the schedule of speeches this evening.

Looking at the day ahead, this morning the only data out in Europe is the July retail sales report in the UK. However it’s busy for data in the US this afternoon. We’ll get August manufacturing surveys from the NY and Philly Fed, while preliminary Q2 nonfarm productivity and unit labour costs data is due. Perhaps the most significant will be the July retail sales report however where the core and control groups readings are expected to show +0.4% mom and +0.5% mom, respectively. We’ll also get the latest jobless claims reading, July industrial and manufacturing production, August NAHB housing market index print and June business inventories. Central bank policy meetings are also due in Norway and Mexico, and in the evening, likely around 7:30pm, we should get the programme for the Fed’s Jackson Hole conference next week, which could see Powell speak.

via ZeroHedge News https://ift.tt/33xowyp Tyler Durden

With markets looking to open in the red following Wednesday’s stunning drop, the infamous Madoff Whistleblower (who was ignored for years) Harry Markopolos has picked Thursday to publish a report about GE’s accounting strategies, claiming that the company’s ‘cash situation’ is a lot worse than the company’s filings would suggest.

Harry Markopolos

GE, for its part, has said Markopolos’s allegations are ‘Entirely False and Misleading’, of course, that didn’t stop shares from plunging 7% in pre-market trading.

Markopolos told WSJ ahead of the report’s release, his group found GE’s insurance unit will need to bolster its reserves by $18.5 billion in cash and faulted the way the company is accounting for its oil-and-gas business. All told, he said, the accounting problems amount to $38 billion, or 40% of the conglomerate’s market value.

GE shares were off 7% in premarket trade thanks to Markopolos’s report, even though he’s not saying anything that JPM’s Tusa hasn’t said already.

via ZeroHedge News https://ift.tt/2OWFrak Tyler Durden

One day after the Chinese press roundly mockedTrump’s unsolicited tariff delay as proof the US was losing the trade war with China, with the Global Times saying that “Chinese experts said the sudden postponing of impending tariffs showed that the maximum pressure tactics of the US are losing their bite when it comes to China”, a suddenly emboldened Beijing – perhaps sensing that it is indeed dealing with a weaker opponent – called planned U.S. tariffs on an additional $300 billion in Chinese goods a violation of accords reached by Presidents Donald Trump and Xi Jinping, and warned it would take all necessary measures to impose new tariffs on its own.

Echoing what Global Times editor in chief Hu Xijin said overnight, a short Thursday statement from the State Council Tariff Committee said the new 10% tariffs have taken the U.S. and China off the track of resolving their dispute through negotiation, and noted that China “has no choice but to take necessary measures to retaliate,” without specifying what the nation would do. The committee has overseen tit-for-tat retaliatory tariffs on American products.

That said, according to an analysis by twitter China watcher, Trinh Nguyen, the amount China has left under tariffs is about USD10bn (already imposed 110bn) “so not much ammunition & will need curb investment/FX deval/UST/rare earth curb. Chart below 👇🏻 US has plenty left & reflects trade diff w/ China.”

China: Will have to take all necessary measures to impose new tariffs.

The amount China has left is ~USD10bn (already imposed 110bn) so not much ammunition & will need curb investment/FX deval/UST/rare earth curb. Chart below 👇🏻 US has plenty left & reflects trade diff w/ China. pic.twitter.com/eieW5WF2MM

But what is far more troubling, is that contrary to Trump’s implied expectation that China would respond with an olive branch of its own and according to Steven Englander, “will expect China to reciprocate by buying US agricultural products in the coming weeks”, not only does China not plan on doing so but – as we warned yesterday – will send relations between the two nations into even greater turmoil with escalation of its own.

As far as I know, the Chinese side requests that both sides respect the consensus reached at Osaka summit, which is removing all additional tariffs, not delaying some. I doubt Chinese side will resume large-scale purchase of US farm products under current circumstances. pic.twitter.com/74vf9PrKXo

In kneejerk response to the apparent escalation, European stocks declined and U.S. equity futures pared a gain of almost 1%. The Stoxx Europe 600 index fell while the three main American equity contracts trimmed an earlier jump after China’s move.

And with the ball no longer in China’s court now that Beijing has spat at Trump’s coy attempt at quasi-appeasement, all eyes are back on Trump’s twitter feed where the US president has two options: either offer even more concessions to China and be seen as even weaker and more desperate to get some concessions out of Beijing (unlikely), or go back to square one and/or escalate tensions even more and potentially eliminate the proposed tariff delay, sending stocks plunging (and the Fed that much closer to the coveted emergency rate cut).

via ZeroHedge News https://ift.tt/2YWQ69X Tyler Durden

As the public carries on with the great debate about what really happened (or didn’t happen) to Jeffrey Epstein early Saturday morning in the hours before he was found dead in his cell at MCC in an apparent suicide, the Washington Post has unleashed a bombshell.

First, remember how some witnesses claimed they had heard horrifying shrieking coming from Epstein’s cell in the hours before his death? Well, here’s one explanation for that: An autopsy report found that Epstein had endured multiple breaks in his neck bones, deepening the mystery surrounding his death last week.

Among the bones broken in Epstein’s neck was the hyoid bone, which in men is near the Adam’s apple. These breaks can occur in those who hang themselves, particularly if they are older, according to forensics experts and studies on the subject.

But they are more common in victims of homicide by strangulation.

Even Jonathan L. Arden, president of the National Association of Medical Examiners, admitted that a hyoid break is more commonly associated with homicidal strangulation than suicidal hanging.

The hyoid bone played a pivotal role in another critical New York City case: The death of Eric Garner.

The hyoid bone played a central role in a heated dispute last year over another high-profile death in New York, that of Eric Garner. A New York police officer was accused of using an improper chokehold while trying to arrest Garner and of causing his death. A police officers’ association claimed that an autopsy from Sampson’s office found there was no break of Garner’s hyoid bone, and that this proved that the officer could not have strangled Garner and caused his death.

These details, according to WaPo, are the first to emerge from Epstein’s autopsy, something that will undoubtedly be closely watched by the legions of Epstein conspiracists who have emerged since his death.

While AG William Barr has described Epstein’s death as “an apparent suicide,” but DoJ officials have refused to comment on the latest findings from Epstein’s autopsy.

The office of New York City’s chief medical examiner, Barbara Sampson, completed an autopsy of Epstein’s body Sunday. But Sampson listed the cause of his death as pending. Asked about the neck injuries Sampson said in a statement that no single factor in an autopsy can alone provide a conclusive answer about what happened.

“In all forensic investigations, all information must be synthesized to determine the cause and manner of death. Everything must be consistent; no single finding can be evaluated in a vacuum.”

The reports about Epstein’s neck injuries followed revelations that the two guards responsible for guarding him had fallen asleep during the hours before his death, then falsified paper work to try and cover their tracks. And dozens of veteran prosecutors and prison officials were shocked that one of the most high-profile inmates in the country wasn’t more closely watched.

Sure, plenty of details remain to be revealed from Epstein’s autopsy, but his jailhouse death is beginning to sound like something out of ‘the Wire’.

via ZeroHedge News https://ift.tt/2N5dElF Tyler Durden

ExxonMobil has recently discussed with operators selling part or all of its assets in the UK North Sea in a move that could raise up to US$2 billion for Exxon and mark another major U.S. exit from the area, Reuters reported this week, quoting three industry sources familiar with the matter.

Exxon has been a major investor in the UK North Sea since 1964, when the first exploration drilling in the area began. The U.S. major holds interests in 40 producing oil and gas fields and produces around five percent of UK oil and gas production, with an average 80,000 barrels of oil and 441 million cubic feet of gas a day. Exxon’s investment in the North Sea is managed through a 50/50 joint operation with Shell.

If Exxon sells some or part of its assets in the UK North Sea, it will be yet another major U.S. oil and gas firm to divest interests in this mature area to focus on their current key growth areas, which for Exxon right now are the Permian in Texas and conventional oil production offshore Guyana.

While European supermajors Shell, BP, and Total continue to view the North Sea as one of their core assets, U.S. majors have been selling North Sea stakes as many of them are now focused on U.S. shale.

Marathon Oil said in February that it would be exiting the UK North Sea as it continues to focus on high-return U.S. shale oil operations.

In April, ConocoPhillips sold its UK oil and gas business to Chrysaor Holdings for US$2.675 billion in a deal which Wood Mackenzie described as “another story of the changing corporate landscape in the North Sea – for the first time, a non major is the number one producer in the UK.”

Chevron also sold in May its North Sea assets—except for a non-operated stake in the Clair field—for US$2 billion to Ithaca Energy.

A sale of assets in the UK would add to Exxon’s plan to sell its assets offshore Norway in what could be a major withdrawal from European offshore production.

In Norway, ExxonMobil sold in 2017 its ownership interests in its operated fields Balder, Jotun Ringhorne, and Ringhorne East to Point Resources, but continued to hold ownership interests in fields that it doesn’t operate.

In June, an Exxon spokesman told a Norwegian newspaper that the company is weighing the sale of its assets in Norway. Rystad Energy has estimated that Exxon’s portfolio of Norwegian upstream assets has a value of US$3.1 billion. As of 1 January 2019, Exxon controlled 530 million barrels of oil equivalent on the Norwegian Continental Shelf, the most valuable asset being a stake in the Snorre field, worth nearly US$700 million, according to Rystad.

via ZeroHedge News https://ift.tt/2YQ87Xo Tyler Durden

Eurostat has released new statistics highlighting the level of electronic waste generated in EU Member States and some EFTA countries.

While much of Scandinavia has earned plaudits for its high standards of living, excellent heathcare and low unemployment levels, Statista’s Niall McCarthy notes that the region is actually Europe’s worst electronic waste offender.

19.6 kg of electronic waste was collected per inhabitant in Norway in 2016, the highest level of any country in Eurostat’s analysis.

Likewise, Sweden came second with 16.4 kg per inhabitant and it had the highest level of any EU Member State.

The United Kingdom followed with 14.8 kg while Denmark had 12.kg – the third-highest level recorded across the EU. The principality of Liechtenstein was third overall with 13.9 kg.

via ZeroHedge News https://ift.tt/2KBDlsx Tyler Durden

Former 3 star General Joachim Wundrak says that Angela Merkel is so politically correct, she cannot even bring herself to talk about the “German people”.

Wundrak announced that he’s going to run for mayor of Hanover as a member of Alternative for Germany (AfD) party.

He slammed Merkel for being the front person for enacting “anti-German” pro-mass migration policies and refusing to even acknowledge the existence of German people as a group.

“Merkel has sworn an oath to Germany, but she already has a problem talking about a German people. She prefers to speak of ‘population’. Many German politicians struggle to profess their own nation,” said Wundrak.

“The protection of one’s own borders is no longer a priority goal,” he added.

“Germany is giving more and more sovereignty to the EU, the European Central Bank, to supranational organisations. I do not agree with this. The nation-state is the primary form of organisation for Germany. Where structures become too big, an undemocratic spirit quickly arises.”

Merkel’s paranoia about displaying any form of patriotism is notorious.

During an event in 2015, Merkel was handed a small German flag only for her to appear embarrassed and hand it back. She then flashed a disapproving shake of the head to someone else on the stage.

* * *

There is a war on free speech. Without your support, my voice will be silenced. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

via ZeroHedge News https://ift.tt/2OVI0K0 Tyler Durden

It’s being proposed as prostitution with the safety and convenience of an Uber. A historic airport in Berlin is the proposed site of “Verichtungsboxen” — orpublicly available prostitution booths where sex workers can meet clients at what’s considered a relatively safe and regulated venue.

The mayor of Berlin’s central Mitte district is leading the initiative to turn the city’s former Tempelhof airport, which was famous for being a Nazi airfield in WWII and afterwards site of the Berlin airlift during the Cold War, into a “drive-in” prostitution site.

The historic Tempelhof airport. Image source: Cairns Post

According to CNN, the plans will include“drive-in booths, where customers can meet sex workers in their own vehicles.”

Since going out of service in 2008, Tempelhof has since been turned into a sprawling public park and recreation area, but previously claimed the title of the world’s oldest operating commercial airport.

The Green party mayor leading the initiative, Stephan von Dassel, says he wants to not only clean up Berlin’s streets, but provide a safer environment for sex workers, ultimately in a bid to improve the lives of “residents and sex workers” alike.

Via The Daily Mail

“Residents and businesses have been calling for a ban on street prostitution for many years,” he said in a statement.

He further described as the Berlin Senate refusing to take any regulatory action “because it fears a deterioration of the overall situation.”

The historic Tempelhof airport turned public park area. Image source: Getty via CNN.

Tempelhof airport has often been referenced as “Hitler’s Airport” but has since 2008 been a popular public park and recreation area.

Dassel also noted that providing Kurfürstenstrasse at the well-known and popular city site would hopefully prevent men “seeking sexual services at such a low price”. One of the problems, he explained, is that sex workers increasingly had to operate as a “bulk business in order to earn a basic income.”

Germany legalized street prostitution in the early 2000’s, and especially over the last decade has seen the sex industry boom, with prostitutes enjoying “worker’s rights” the same as if they were in transportation or the food industry. Berlin has long been known as having among the world’s most liberal prostitution laws.

Verrichtungsboxen in Zürich-Altstetten, August 2013

But similar to the situation the The Netherlands recently, there’s been a slow public backlash given the simultaneous sex worker health crisis, influx of drugs, pimps, human trafficking, and rampant unreported abuse of women.

One classic line of Mitte district’s mayor quoted by CNN is as follows:

The visibility of pimps is having a “negative impact on the safety of residents,” he says.

Another example of regulated sex booths. Source:Uwe Weiser (Express)

The drive-in sex booths idea has actually been implemented on a limited bases in places like Cologne, Zurich, and in The Netherlands.

In practice they ideally include security features like cameras outside the booths and alarm buttons that a sex worker can push if they are under threat.

But one significant roadblock the plan may run into is the fact that as a centrally located public park, where families can often be seen rollerblading or picnicking or having an early evening stroll, is that families may react angrily at the idea that Tempelhof could be partially transformed into a drive-in sex service.

This would of course, simply take the pimps and prostitutes off the streets and bring them to the recreation and “play” area of the landmark airport.

via ZeroHedge News https://ift.tt/31xY1qW Tyler Durden

Fifty years ago, the Battle of the Bogside in Derry between Catholics and police, combined with the attacks on Catholic areas of Belfast by Protestants, led to two crucial developments that were to define the political landscape for decades: the arrival of the British army and the creation of the Provisional IRA.

An eruption in Northern Ireland was always likely after half a century of undiluted Protestant and unionist party hegemony over the Catholics. But its extreme militarisation and length was largely determined by what happened in August 1969.

An exact rerun of this violent past is improbable, but the next few months could be equally decisive in determining the political direction of Northern Ireland. The Brexit crisis is reopening all the old questions about the balance of power between Catholics and Protestants and relations with Britain and the Irish Republic that the Good Friday Agreement (GFA) of 1998 had provided answers with which everybody could live.

The occasion which led to the battle of the Bogside came on 12 August when the Apprentice Boys, a fraternity memorialising the successful Protestant defence of Derry against Catholic besiegers in the 17th century, held their annual march. Tensions were already high in Derry and Belfast because the unionist government and its overwhelmingly Protestant police force was trying to reassert its authority, battered and under threat since the first civil rights marches in 1968.

What followed was closer to an unarmed uprising than a riot as the people of the Bogside barricaded their streets and threw stones and petrol bombs to drive back attacks by hundreds of policemen using batons and CS gas. In 48 hours of fighting, a thousand rioters were treated for injuries and the police suffered unsustainable casualties, but they had failed to gain control of the Bogside.

Its defenders called for protests in other parts of the North to show solidarity with their struggle and to overstretch the depleted Royal Ulster Constabulary (RUC). In Belfast, Protestants stormed into the main Catholic enclave in the west of the city, burning houses and forcing Catholics to flee. The RUC stood by or actively aided the attacks. The local MP Paddy Devlin estimated that 650 families were burned out in a single night, many taking refuge in the Irish Republic

I was in Bombay Street, where all the houses were burned on the night of 14-15 August, earlier this year. The street was long ago rebuilt but still has a feeling of abnormality and menace because it is only a few feet from the “peace line” with its high wall and higher wire mesh to stop missiles being thrown over the top from the Protestant district next door.

The most striking feature of Bombay Street is the large memorial garden, though it is more like a religious shrine, to martyrs both military and civilian from the district who have been killed by political violence since 1916. A high proportion of these were members of the Provisional IRA who died in the fighting during the 30 years of warfare after Bombay Street was burned.

The memorial is a reminder of the connection between what many local people see as an anti-Catholic pogrom in 1969 and the rise of the Provisional IRA. It split away from what became known as the official IRA because the latter had failed to defend Catholic districts.

Pictures of the ruins of Bombay Street on the morning of 15 August show local people giving British soldiers cups of tea. But this brief amity was never going to last because the unionist government in Stormont had asked the prime minister of day, Harold Wilson, to send in the troops not to defend Catholics but to reinforce its authority.

It was the role the British army were to play in one way or another for the next 30 years. It was one which was bound not only to fail but to be counterproductive. So long as the soldiers were there in support of a Protestant and unionist political and military establishment, the IRA were always going to have enough popular support to stay in business.

British governments at the time never got a grip on the political realities of the North. Soon after the troops were first sent there, the cabinet minister Richard Crossman blithely recorded in his diary that “we have now got ourselves into something which we can hardly mismanage”. But mismanage it they did and on a grotesque scale. The Provisionals were initially thin on the ground, but army raids and arrests acted as their constant recruiting sergeant. Internment without trial introduced on 9 August 1971, the anniversary of which falls today, was another boost as were the hunger strikes of 1981 which turned Sinn Fein into a significant political force.

What are the similarities between the situation today and 50 years ago? In many respects, it is transformed because there is no Protestant unionist state backed by the British army. The Provisional IRA no longer exists. The GFA has worked astonishingly well in allowing Protestants and Catholics to have their separate identities and, on occasion though less effectively, to share power.

Brexit and the Conservative Party dependence on the Democratic Unionist Party (DUP) for its parliamentary majority since 2017 has thrown all these gains into the air. DUP activists admit privately that they want a hard border between Northern Ireland and the Republic because they have never liked the GFA and would like to gut it. Sinn Fein, which gets about 70 per cent of the Catholic/nationalist vote these days, is pleased that the partition of Ireland is once again at the top of the political agenda.

“I am grappling with the idea of a hard border which I would call a Second Partition of Ireland,” Tom Hartley, a Sinn Fein veteran and former lord mayor of Belfast, told me. He is baffled by British actions that appear so much against their interests, saying that “they had parked the Irish problem, but now Ireland has moved once again into the centre of British politics”.

Would Boris Johnson’s enthusiasm to get rid of “the backstop” evaporate if he wins or loses a general election and the Conservatives are no longer dependent on the DUP for their majority? Possibly, but his right-wing government has plenty of members who never liked the GFA and their speeches show them to be even more ignorant about Northern Ireland politics than their predecessors in Harold Wilson’s cabinet half a century ago.

An example of this is their oft-declared belief that some magical gadget will be found to monitor the border by remote means. But any such device will be rapidly torn down and smashed where the border runs through nationalist majority parts of the border.

Northern Ireland may be at peace, but in a border area like strongly Republican South Armagh, the police only move in convoys of three vehicles and carry rifles, even if they are only delivering a parking ticket.

Catholics are no longer the victims of economic discrimination, though Derry still has the highest unemployment of any city in the UK. There has been levelling down as well as levelling up: Harland and Wolff, the great shipyard that once employed much of the population of Protestant east Belfast, went into administration this week.

Irish unity is being discussed as a practical, though highly polarising, proposition once again. Political and economic turmoil is back in a deeply divided and fragile society in which the binds holding it together are easily unstitched.

via ZeroHedge News https://ift.tt/2Z6WOoS Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}