Two weeks ago, when we observed the flush in markets as a result of technical selling following the breach of key CTA levels which in turn precipitated a selling feedback loop as extensive negative gamma positions had to be unwound, as selling forced more selling, Nomura’s Charlie McElligott cautioned that a similar snapback is possible to the upside if only there was sufficient bullish sentiment to push US equity futures above key selling levels.

So following this morning’s newsless meltup, this morning McElligott is out with a note declaring “mission accomplished” as said feedback loop has indeed emerged, and as he writes “the knock-on bleeding-out of Equities Vol Dealers’ crash hedges is accelerating into this morning’s VIX expiry, with unwinds now helping further accelerate the move higher Equities futures overnight (S&P futs +0.8% overnight)—“mission accomplished” ; )

The catalyst behind said hedge unwind is the previously noted recent re-emergence of the infamous “50-cent” VIX trader, who forced dealers to take opposing positions to his/her Call Wing positions, which due to positive gamma and dealer vega balancing, were forced to keep buying stocks the higher the market rose, and the lower VIX dropped, to wit:

These “crash” hedges are so “outsized” simply due to the massive scale of the “50 Cent” August VIX Call Wing positions, which Dealers are short—and thus they have been forced to get long a lot of S&P Vega via VIX futs, S&P downside or just “shorts” in Spooz to offset this exposure

As McElligott also reminds us, prior to the July return of “50 Cent,” this massive “lottery ticket” demand in the VIX “Call Wing” had disappeared after Feb ’18 saw the effective extinction of the leveraged VIX ETNs’ “Short Vol” position, which thereafter drove a broad collapse in VIX futs / options volumes. However, as the Nomura quant notes, “now after the Summer ’19 return of the entity’s hedging program to the VIX options space, the implications of this flow are particularly outsized, especially in-light-of Dealer VaR constraints / risk limits specifically into this peak of Summer illiquidity and thus, low market capacity to digest it all.”

Which brings us to today’s meltup: as the “50 Cent” call wing decays with all of the strikes looking to be out of the money into this morning’s expiry, Dealer hedges need to be unwound and / or covered, particularly noting their “short gamma” position in VIX futures options.

And, in a repeat of the insane move by we observed back in February 2017 when the Catalyst Fund’s Hedge Futures Strategy Fund almost singlehandedly moved the entire market higher by several percent when it was caught in a “gamma trap”, in classically-perverse “negative convexity” style, dealers are now forced to sell more Vega (VIX futs) the lower VIX goes; and “BOOM,” that in McElligott’s eyes is largely why we’ve seen a “TWAP seller” look over the past 3.5 sessions in UX contract, losing ~5 vols in the process:

DEALER “SHORT GAMMA” IN NOW-DECAYING AUG VIX CALL WING MEANS TWAP-LIKE SELLING OF FUTURES OVER THE PAST 3.5 SESSIONS INTO THIS MORNING’S EXPIRY

There’s more. As McElligott repeats what he warned just yesterday, the implications of the “mechanical melt” in the VIX complex have then not just acted as catalysts for “Higher Stocks” since last week, but potentially too, near-term going-forward as well. Here are the details as per the Nomura quant:

This grinding move lower in VIX futs will too further incentivize monetization of “long vol” positions (particularly the still-massive net long Vega position from VIX ETNs) as an additional catapult/amplifier for “Higher US Equities” near-term

The normalization of front-VIX contracts LOWER too means that a re-steepening of the VIX futs curve (out of the recent inversion) which will gradually signal for the return of Systematic “Roll-Down” strategies as an additional “Volatility Seller” flow to the market with bullish second-order impact upon Equities

And as we like to focus-upon here, these “short VIX / short vol” flows will increasingly too then drag trailing realized vols lower, which as a critical “allocation- / leverage-” input to Systematic “Target Vol / Risk-Control” strategies will ultimately drive further re-leveraging and / or “short covering” into their Equities positions

Speaking of CTAs going long again, while Charlie did note yesterday that his CTA model’s Eurostoxx position re-leverage from the prior +56% signal all the way back-up to +100%, joining SPX, NDX, CAC and ASX, today he points out that remaining CTA model shorts at “risk” of covering locally from here, and sending risk even higher, include:

Russell 2k (currently -100% Short, would begin to cover at 1542),

Nikkei (-100% Short, would begin to cover at 21053),

DAX (-73% Short, would begin to cover at 12085),

FTSE (-73% Short, would begin to cover at 7226),

Hang Seng (-100% Short, would begin to cover at 26991),

Hang Seng CH (-100% Short, would begin to cover at 10345)

KOPSI (-100% Short, would begin to cover at 266)

Finally, with this morning’s Spooz bounce, Nomura sees SPX options Dealer Gamma elevate back in a very “neutral to long” status, thus acting to stabilize and insulate Spooz into a “less chase-y” trading environment which can then further engender restoration of sentiment. Indeed, as shown in the chart below, the higher we move above the SPX spot breakeven of 2918, the faster the meltup will become.

Of course, this near-term meltup does not mean “all clear”, and as we described yesterday, and as McElligott cautions today, “September poses its own set of challenges and should continue to keep directional trading “tactical” in nature.”

The biggest risk here remain both the Fed and ECB where “dovish expectations” remain exceedingly high and thus risk a perceived “hawkish disappointment,” which could then dictate US Rates (higher yields) and USD (higher) price-action all acting to “TIGHTEN” financial conditions. Together with the resumption of the corporate “buyback blackout” around mid- September into Q3 EPS season (~75% of S&P 500 corporates will see their purchase windows close by 9/17/19), any “macro shock as catalyst for lower Equities” (e.g. September Fed or ECB disappointment) scenario risks the following sequencing:

a drop in spot back into Dealer “Short Gamma” zone, which too then could converge with…

the increased potential for recently / currently RE-leveraged “Long Equities” positions (or at least covering “Shorts”) from Target Vol / CTA Trend accounts which could then too see a forced DE-leveraging upon a large enough drop—ESPECIALLY in-light of…

the mid-Sept gradual loss of the “Buyback Bid” and…

VIX September seasonality, which is the 2nd best avg monthly return for the volatility index in its history

via ZeroHedge News https://ift.tt/2KWNWgy Tyler Durden

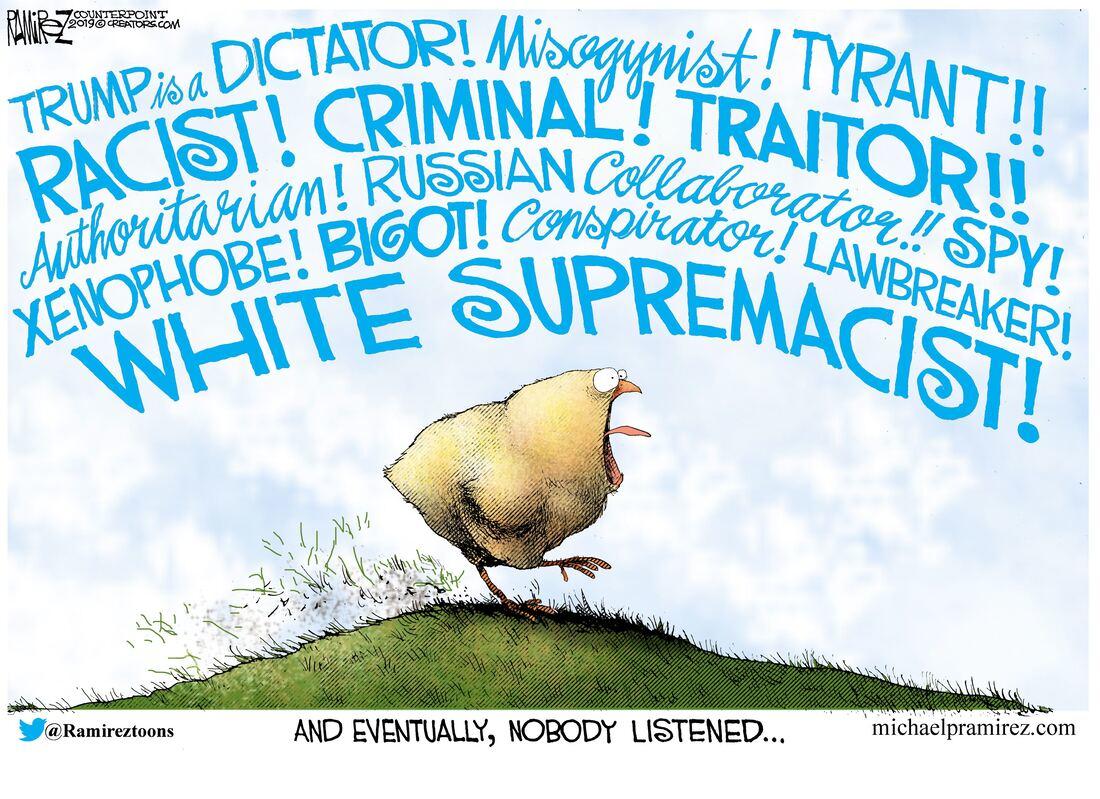

As the Russiagate circus attempts to quietly disappear over the horizon, with Democrats preferring to shift the anti-Trump narrative back to “racist”, “white supremacist”, “xenophobe”, and the mainstream media ready to squawk “recession”; the Trump administration may have a few more cards up its sleeve before anyone claims the higher ground in this farce we call an election campaign.

As The Hill’s John Solomon details, in September 2018 that President Trump told my Hill.TV colleague Buck Sexton and me that he would order the release of all classified documents showing what the FBI, the Department of Justice (DOJ) and other U.S. intelligence agencies may have done wrong in the Russia probe.

And while it’s been almost a year since then, of feet-dragging and cajoling and deep-state-fighting, we wonder, given Solomon’s revelations below, if the president is getting ready to play his ‘Trump’ card.

Here are the documents that Solomon believes have the greatest chance of rocking Washington, if declassified:

1.) Christopher Steele’s confidential human source reports at the FBI. These documents, known in bureau parlance as 1023 reports, show exactly what transpired each time Steele and his FBI handlers met in the summer and fall of 2016 to discuss his anti-Trump dossier. The big reveal, my sources say, could be the first evidence that the FBI shared sensitive information with Steele, such as the existence of the classified Crossfire Hurricane operation targeting the Trump campaign. It would be a huge discovery if the FBI fed Trump-Russia intel to Steele in the midst of an election, especially when his ultimate opposition-research client was Hillary Clinton and the Democratic National Committee (DNC). The FBI has released only one or two of these reports under FOIA lawsuits and they were 100 percent redacted. The American public deserves better.

2.) The 53 House Intel interviews. House Intelligence interviewed many key players in the Russia probe and asked the DNI to declassify those interviews nearly a year ago, after sending the transcripts for review last November. There are several big reveals, I’m told, including the first evidence that a lawyer tied to the Democratic National Committee had Russia-related contacts at the CIA.

3.) The Stefan Halper documents. It has been widely reported that European-based American academic Stefan Halper and a young assistant, Azra Turk, worked as FBI sources. We know for sure that one or both had contact with targeted Trump aides like Carter Page and George Papadopoulos at the end of the election. My sources tell me there may be other documents showing Halper continued working his way to the top of Trump’s transition and administration, eventually reaching senior advisers like Peter Navarro inside the White House in summer 2017. These documents would show what intelligence agencies worked with Halper, who directed his activity, how much he was paid and how long his contacts with Trump officials were directed by the U.S. government’s Russia probe.

4.) The October 2016 FBI email chain. This is a key document identified by Rep. Nunes and his investigators. My sources say it will show exactly what concerns the FBI knew about and discussed with DOJ about using Steele’s dossier and other evidence to support a Foreign Intelligence Surveillance Act (FISA) warrant targeting the Trump campaign in October 2016. If those concerns weren’t shared with FISA judges who approved the warrant, there could be major repercussions.

5.) Page/Papadopoulos exculpatory statements. Another of Nunes’ five buckets, these documents purport to show what the two Trump aides were recorded telling undercover assets or captured in intercepts insisting on their innocence. Papadopoulos told me he told an FBI undercover source in September 2016 that the Trump campaign was not trying to obtain hacked Clinton documents from Russia and considered doing so to be treason. If he made that statement with the FBI monitoring, and it was not disclosed to the FISA court, it could be another case of FBI or DOJ misconduct.

6.) The ‘Gang of Eight’ briefing materials. These were a series of classified briefings and briefing books the FBI and DOJ provided key leaders in Congress in the summer of 2018 that identify shortcomings in the Russia collusion narrative. Of all the documents congressional leaders were shown, this is most frequently cited to me in private as having changed the minds of lawmakers who weren’t initially convinced of FISA abuses or FBI irregularities.

7.) The Steele spreadsheet. I wrote recently that the FBI kept a spreadsheet on the accuracy and reliability of every claim in the Steele dossier. According to my sources, it showed as much as 90 percent of the claims could not be corroborated, were debunked or turned out to be open-source internet rumors. Given Steele’s own effort to leak intel in his dossier to the media before Election Day, the public deserves to see the FBI’s final analysis of his credibility. A document I reviewed recently showed the FBI described Steele’s information as only “minimally corroborated” and the bureau’s confidence in him as “medium.”

9.) The redacted sections of the third FISA renewal application. This was the last of four FISA warrants targeting the Trump campaign; it was renewed in June 2017 after special counsel Robert Mueller’s probe had started, and signed by then-Deputy Attorney General Rod Rosenstein. It is the one FISA application that House Republicans have repeatedly asked to be released, and I’m told the big reveal in the currently redacted sections of the application is that it contained both misleading information and evidence of intrusive tactics used by the U.S. government to infiltrate Trump’s orbit.

10.) Records of allies’ assistance. Multiple sources have said a handful of U.S. allies overseas – possibly Great Britain, Australia and Italy – were asked to assist FBI efforts to check on Trump connections to Russia. Members of Congress have searched recently for some key contact documents with British intelligence. My sources say these documents might help explain Attorney General Bill Barr’s recent comments that “the use of foreign intelligence capabilities and counterintelligence capabilities against an American political campaign, to me, is unprecedented and it’s a serious red line that’s been crossed.”

These documents, when declassified, would show more completely how a routine counterintelligence probe was hijacked to turn the most awesome spy powers in America against a presidential nominee in what was essentially a political dirty trick orchestrated by Democrats.

via ZeroHedge News https://ift.tt/2KJJz9D Tyler Durden

One day after China warned the US that it won’t make trade concessions if the US “plays the Hong Kong card“, the famous twitter troll Hu Xijin, editor in chief of the nationalist, state owned Chinese newspaper Global Times, amplified the sentiment tweeting moments ago that “China is making arrangements on scenario of no deal” as a result of Trump’s recent shift in strategy that links trade talks with the situation in Hong Kong. “The deterrence of the US not signing the deal on China is close to zero.”

As for Washington’s threat to link trade talks with the situation in Hong Kong, what I heard on various occasions is scorn on this idea. China is making arrangements on scenario of no deal. The deterrence of the US not signing the deal on China is close to zero.

As a reminder, yesterday we reported that in a short commentary published by Communist Party mouthpiece People’s Daily late on Monday, the author said that events in Hong Kong were the internal affairs of China, and linking them with trade negotiations was a “dirty” aim.

“Making a fuss about Hong Kong will not be helpful to economic and trade negotiations between China and the US,” the commentary said. “They would be naive in thinking China would make concessions if they played the Hong Kong card” the oped cautioned. Chinese diplomatic observers also said Beijing considered the worsening situation in Hong Kong a sovereignty issue and would be highly unlikely to cave to Washington’s pressure.

The remarks followed a statement by US Vice-President Mike Pence on Monday which reiterated President Donald Trump’s demand to tie the largely stalled trade talks with Hong Kong’s deepening crisis, a day after hundreds of thousands of people marched peacefully in defiance of repeated intimidation from Beijing. In an address at the Detroit Economic Club on Monday, Pence said the Trump administration would continue to urge Beijing to resolve differences with the protesters peacefully and warned that it would be harder for Washington to make a trade deal with Beijing if there was violence in the former British territory. Separately, Mike Pompeo said that China should allow Hong Kong protesters the freedom to express themselves, in what China saw as clear interference in its own internal matters.

The Chinese article countered by saying that the top priority for Hong Kong was to stop violence and restore order, adding that US politicians should not send the wrong message to people creating chaos in the city. “In the face of political intimidation, we not only dare to say no, but also take countermeasures,” it warned.

Hu Xijin’s Global Times also warned in an editorial on Monday that American political and public opinion elites should not harbour the illusion they could influence China’s decisions on Hong Kong.

“Because of the trade war, the US has lost the ability to impose additional pressure on China,” it said. “The US should stop its meaningless threat of linking the China-US trade talks with the Hong Kong problem. Beijing did not expect to quickly reach a trade deal with Washington. More Chinese people are prepared that China and the US may not reach a deal for a long time.”

Chinese analysts noted Trump appeared to have hardened his stance on Hong Kong in the past week or so, under growing pressure from US lawmakers and extensive media coverage of the increasingly violent protests. Indeed, it was only a month ago when we reported that “Trump Abandoned Support For Hong Kong Protests To Revive Trade Talks With Beijing.” Now that trade war is once again front and center, with Trump using it as leverage for further Fed rate cuts, the US president is once again refocusing his attention on Hong Kong.

As the SCMP writes, Trump initially focused on making a deal with China ahead of his 2020 re-election bid and adopted a hands-off approach by characterizing the protests as “riots” which were a matter for China to handle. Over the past few days, he suggested Chinese President Xi Jinping should resolve the situation by meeting with protest leaders and warned that any violence in the handling of the Hong Kong crisis would exacerbate difficulties for attempts to bring an early end to the trade war.

“Trump’s about-face on Hong Kong, from being neutral to piling pressure on Beijing, is largely due to domestic political pressure ahead of the presidential elections,” said Shi Yinhong, an international relations expert at Renmin University and an adviser to the State Council which is China’s cabinet.

“But the Hong Kong issue concerns China’s sovereignty and the government’s ability to maintain stability, which in Beijing’s view is of superior priority. China cannot afford to make much compromise and will do everything to fend off interventions from abroad, in spite of all the risks and ramifications,” he said.

Shi also said none of the flashpoints in the bilateral ties – from Hong Kong, Taiwan, to the South China Sea and the denuclearisation of North Korea – had any easy solution in sight, with both sides showing little willingness to cooperate and accommodate the other’s interests. He said the increasingly hardline, confrontational approach on China by Trump – who faced mounting pressure in his bid for re-election, especially amid signs of a looming global economic recession – would only make a trade deal increasingly unattainable.

“Even if there were no Hong Kong crisis, could the US and China reach a trade deal? Even if Beijing caved into Washington’s pressure on Hong Kong, would it make it easier for them to bridge their glaring differences in the trade talks and cut a deal?”

Of course not, and since Trump is far more interested in keeping trade war simmering and on the verge of a substantial escalation if only to keep the Fed on its toes and ready for far more aggressive rate cuts, and even “some quantitative easing”, that’s precisely what the US president wants.

via ZeroHedge News https://ift.tt/2P7A4FG Tyler Durden

President Trump’s polls show that the issue that voters most trust him on is the economy. But on Wednesday, Politico reported that Trump and his team have been quietly prepping donors, other key Republican power brokers and members of the GOP elite for a mild downturn between now and the election, something that economists believe to be increasingly likely.

According to Politico, Trump and his aides are aware that his biggest selling point heading into 2020 is the economy. But now that he’s gotten drawn in to this trade war with Beijing, Trump needs to find a way to prepare people for a mild or moderate recession as a matter of course, to ensure that his reputation as a businessman and as a populist who puts the economy first isn’t tarnished.

But without control of the House, the administration is examining its limited options to shore up the economy or assuage voters’ concerns if a recession arrives soon than economists expect. President Trump’s attacks on the Fed have worked so far, but whether the central bank delivers the 2-3 more cuts that markets are pricing in remains to be seen. And those reports about a payroll tax cut and shaving another few points off the corporate rate represent serious policy considerations. Trump famously said he’s been behind payroll tax cuts “for a long time.”

Then, there’s the trade war.

The administration is also urging the Federal Reserve to cut interest rates sharply, a move Trump has long sought in his public attacks on the central bank, and it is pursuing a trade deal with China amid various tariffs that some businesses say are posing substantial economic risks.

“The only thing they have in their control is China and putting out regulatory rules,” said one former senior administration official. “Beyond that, there is very little that they can do – but that does not mean people are not brainstorming options.”

The White House has dedicated itself to promoting its economic narrative, with Larry Kudlow and other economic advisors hopping on calls with donors and interest groups.

The White House spent Tuesday selling its happy economic message. Top economic adviser Larry Kudlow hosted two calls with local and state officials and conservative groups to offer his own analysis and assurances, discussions that one White House official said had been planned for several weeks. Officials also reached out to business groups with a message that included stressing the stock market‘s resilience.

The president is intent on convincing voters that the economy is in fine shape because he knows voters often cast ballots based on how they feel at the time of the election about their own economic situation.

Because if there’s anything Trump does understand about the 2020 vote, it’s that people are going to decide whether to give him another term based on how they feel. So he’s deployed all of his people to get out there and talk about the economy.

“People do not vote on numbers. They vote on whether they feel good, and the president understands that. He is selling the feeling,” a second White House adviser said. “It is like any other sales pitch: He is constantly trying to play off people’s feelings and emotions on the economy.”

He’s not the only one. Kudlow, counselor to the president Kellyanne Conway and deputy White House press secretary Hogan Gidley all appeared on TV over the past few days to deliver the administration’s upbeat, public-facing message, while Vice President Mike Pence spoke to the Detroit Economic Club on Monday to tout the administration’s record featuring low unemployment and healthy wage growth.

“Despite the irresponsible rhetoric of many in the mainstream media, the American economy is strong, and the U.S. economic outlook remains strong as well,” Pence said in Detroit. “Last week, despite some volatility in global markets, leading retailers also reported strong sales and earnings, and consumer spending posted its strongest reading since March.”

There’s definitely more than a little truth in Trump saying that his life would be a lot easier if he hadn’t picked a fight with China.

Trump spent Tuesday stridently defending his administration’s trade standoff with China, which many economic experts and Republicans pinpoint as the main driver of any U.S. economic troubles.

“You should be happy that I’m fighting this battle, because somebody has to do it. We couldn’t let this go. I don’t even think it’s sustainable to let go on what was happening,” Trump told reporters as he detailed the way China steals U.S. intellectual property and argued none of his presidential predecessors were willing to confront China as he has.

“My life would be a lot easier if I didn’t take China on. But I like doing it because I have to do it. And we’re getting great help. China’s had the worst year they’ve had in 27 years, and a lot of people saying the worst year they’ve had in 54 years,” he added.

And if the economy does worsen, Trump has already lined up scapegoats: Jerome Powell, the media, Democrats, Europe, China – the list goes on.

via ZeroHedge News https://ift.tt/2KKp2lq Tyler Durden

On August 15, 2019 the Washington Post led with a story entitled Markets sink on recession signal. The recession signal the Post refers to is the U.S. Treasury yield curve which had just inverted for the first time in over ten years.

We have been highlighting the flattening yield curve for the past six months. As we have discussed, every time the ten-year Treasury yield has fallen below the two-year Treasury yield, thus inverting the yield curve, a recession has eventually developed.

Blaming the yield curve for market losses because it inverted by a couple of basis points is a nonsensical narrative for talking heads on business television. This article is about a different concern, a second-order effect caused by headlines like the one shown below. The story in the Post and similar ones in many major publications have awoken the public to the real possibility that a recession may be coming. It is a dog whistle that may cause the public to alter their behavior, and even slight changes in consumption habits can produce outsized effects on economic activity.

Reality

The 2s/10s yield curve stood at 265 basis points on January 1, 2014, meaning the ten-year yield was 2.65% higher than the two-year yield. From that date forward, as shown below, it has steadily declined. Like the changing of the seasons, as the days passed, that spread steadily fell. Unlike the seasons, investors are somehow now suddenly shocked to learn that economic winter follows fall. Since the beginning of 2019, the curve has been as steep as 25 basis points but has flirted with inversion on numerous occasions.

Given that the shape of the yield curve has been steadily flattening for five years, its current inversion ought not to be news. From an economic perspective, who cares, nothing has changed. The difference in a few basis points on the yield curve is truly meaningless. What has changed is investors’ behavioral instincts.

Explanation Bias

Blaming the yield curve for a market downturn is a narrative designed to fill the public need for an explanation on equity market losses. We talked to Peter Atwater, a behavioral specialist and guest on the Lance Roberts Show, to help us understand human behavior.

Per Peter: Confidence requires perceptions of certainty and control. Easily grasped narratives – even when they are woefully incorrect – fulfill both needs. Not sure that there is a formal name to the bias, but I would call it “Explanation Bias” – we need an easy story to fight against the anxiety that would arise from what would otherwise be randomness. And randomness is untenable.

We highly recommend following Peter on Twitter at @peter_atwater

In our need to explain and attempt to understand randomness, the public is now aware of a real and growing threat that was ignored just days prior. The sudden drop in the stock market and a potential catalyst for a much steeper decline is not necessarily about finance and economics; behavioral instincts are now in play.

Over the past several months we have said the window for a potential recession is open. By this, we meant that economic stimulus was waning, global growth was slowing, and the potential for a recession has increased as a result. The hard part of our forecast was to name the catalyst that could tip the economy into recession.

We postulated that it might be the brewing trade war, Iran, slowing global growth, or any number of other topics in the media at the time. The problem, as we pointed out in naming a single catalyst or narrative, was that it really could be something inconsequential or something we have not pondered.

This concept is akin to avalanches. The structure of the hill, weather, and the way the snow is perched determine whether an avalanche will occur. The catalyst, however, is but one snowflake that causes a chain reaction.

It is possible the snowflake in our case is the media and the public’s awareness of the relationship between yield curve inversions and recessions.

If the headlines do spark new concern and even slightly modifies consumption patterns, a recession may come sooner than we think. If you harbor concerns that a recession is coming, aren’t you more likely to eat in or put off buying a new TV? These little and seemingly inconsequential decisions made by a minority of consumers can tip the scale and create negative economic growth.

Here is another way to think about it. Picture your favorite restaurant, one that is always packed and has a waiting list. One day you arrive on a Saturday night expecting to wait an hour for a table, but to your delight, the hostess says you can sit immediately. You look around and the restaurant is crowded, but uncharacteristically there are a few empty tables. Those empty tables, while seemingly insignificant, may mean the restaurant’s sales are down a few percent from the norm.

A few percent may not seem like a big deal, but consider that the average annual recessionary growth low point was only -1.88% for the last five recessions. If economic growth is weak, then small negative changes in output can take an economy from expansion to contraction quicker than if growth rates were stronger. This seems to exemplify the current situation as growth has been fairly tepid post-financial crisis.

Summary

We can follow all the economic data and trends diligently, but consumption accounts for over 70% of U.S. economic growth. Therefore, recessions ultimately tend to be the effect of changes in consumer behavior. If the narrative du jour is enough to trouble even a small percentage of consumers, the likelihood of a recession increases. The evidence of such a change will eventually turn up in sentiment surveys, and when it does, the problem has already taken root. This is not a dire warning of recession but rather offers consideration of a legitimate second-order effect that potentially threatens this record-long economic expansion.

While the media focuses on the inversion narrative, alerting the public to recession warnings and driving consumers to re-think their planned purchases, we care more about when the yield curve will steepen. The steepening curve caused by aggressive Fed action after a curve inversion is the tried and true recession warning.For more, please read Yesterday’s Perfect Recession Warning May Be Failing You.

via ZeroHedge News https://ift.tt/2Z3hlj0 Tyler Durden

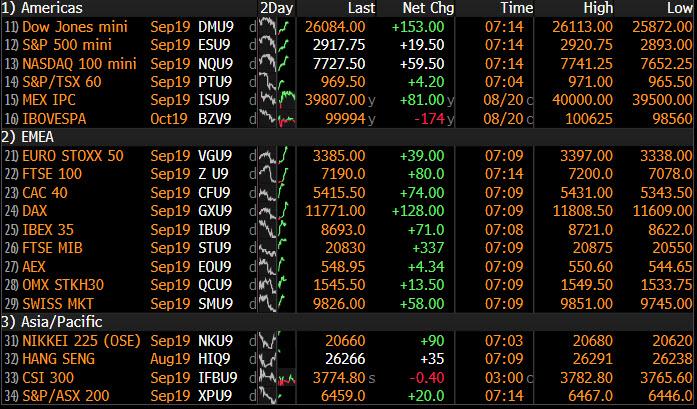

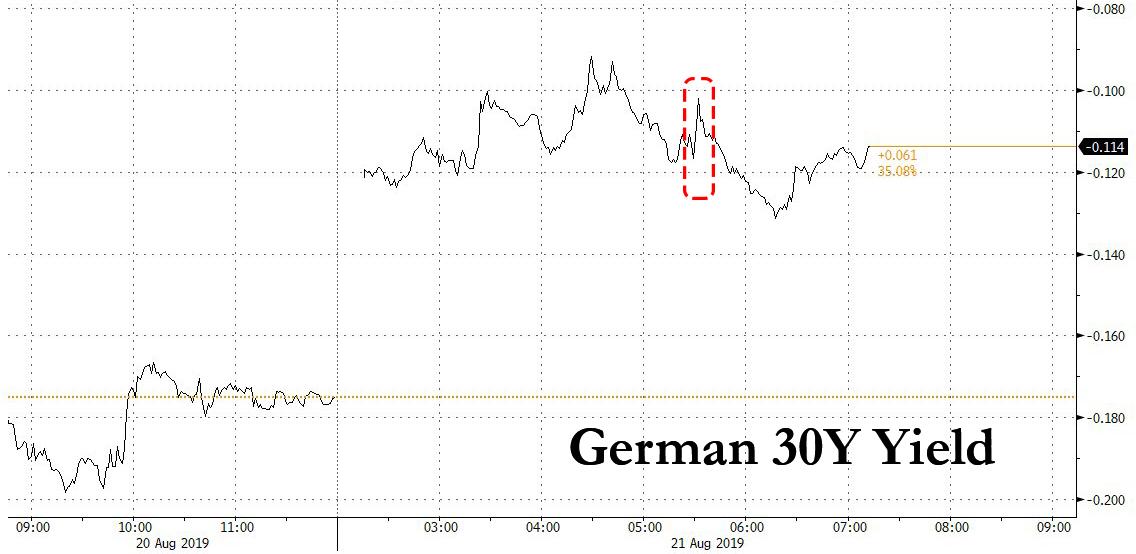

Yesterday’s market selloff is a distant memory this morning, with US equity futures sharply higher tracking European stocks which rose as much as 1%, and ignoring earlier weakness in Asian markets as hopes for more monetary and fiscal stimulus helped ease fears about global recession, political turmoil in Italy and endless trade wars. Treasury yields ticked higher after retreating Tuesday, while the sharp move higher in German 30Y bonds resulted in the failure of a much anticipated 30Y bond auction with a negative yield, a historic first.

Still, with key Fed announcements looming, in the form of today’s FOMC minutes and Friday’s Jackson Hole meeting, volumes subdued. The Euro STOXX 600 was 0.8% higher, rising earlier as much as 1.1%, while the FTSE MIB rises as much as 1.8% following a rout on Tuesday after the resignation of Italian Prime Minister Giuseppe Conte. The Stoxx autos sector index lead gains, up 2.2%, with Renault surging 4.2% and Fiat Chrysler up 4% after Italian daily Il Sole 24 Ore cited people familiar with the matter as saying the carmakers remain in contact on potential tie-up after publicly abandoning efforts. That put the STOXX 600 Autos Index on track for its best day in a month.

GEA Group, a German food-processing-machinery company, and outsourcing group Capita gained more than 5% after Goldman Sachs upgraded its rating on the stocks.

Asian stocks were fractionally lower, with Japanese and Australian stocks down, while shares rose in Hong Kong and Seoul and were little changed in Shanghai. Chinese shares were effectively unchanged even though the yuan rose for the first time a week after a “friendly fix” by the central bank which set the daily reference rate slightly stronger than expected, and higher than yesterday. After a “market-friendly fixing,” the bias has been to sell dollars Wednesday morning, Stephen Innes, managing director for VM Markets Ltd. in Singapore, wrote in a note. “With small volumes going through, it’s beginning to feel more like your typical August as the markets don’t seem to have much of an axe to grind one way or the other.” Innes added that there’s some pre-risk event position-squaring ahead of PMI data and Federal Reserve Chairman Jerome Powell’s speech in Jackson Hole later this week. “We could be back in the frying pan quickly if the yield curve inverts or Jay Powell reiterates his mid-cycle view of things,” he wrote.

The yield on 10-year government bonds edged higher for a second day, hitting its highest in two weeks. Treasuries underperformed bunds and gilts, while German bonds pared declines after the country sells new 30-year debt at negative yields for the first time. Italian bonds rise amid optimism that fresh elections will be averted. Bunds trimed declines as 30-year sale sees underbidding of 6c and tail of 3c; these are similar to the July sale of benchmark long bond that met underbidding of 5c and tail of 1c; this is even as oversubscription falls on Wednesday to 1.05x from 1.07x prior and is technically undersubscribed at 0.43x versus 0.86x previously after accounting for retentions.

Italian bond yields steadied after falling on Tuesday, as Italian President Sergio Mattarella begins two days of talks that will lead either to formation of the country’s 67th government since World War Two or to early elections.

Investors will be watching policy makers and world leaders as they convene at the latest G7 meeting to consider the weakest global growth since the financial crisis. The Group of Seven leaders, with Trump among them, will gather in France from the weekend as the ECB prepares to cut interest rate.

And while the Fed minutes due Wednesday may provide some clarity on officials’ views, they’re likely to be overshadowed by Chairman Jerome Powell’s address at Jackson Hole in Wyoming on Friday in the wake of Trump’s latest attack on the central bank according to Bloomberg. Much depends on what the Fed does with U.S. interest rates, making markets hyper-sensitive to the minutes – due later on Wednesday – of its last meeting.

“People are looking ahead to Jackson Hole later this week and the message that Jerome Powell may or may not give us on the direction of monetary policy. That is the highlight of the week and we are waiting with baited breath,” said Andrew Milligan, head of global strategy at Aberdeen Standard Investments.

The sentiment was confirmed by Tuuli McCully, head of Asia-Pac at Scotiabank, who told Bloomberg that “the key thing this week is the Jackson Hole speech by Fed Chair Powell. It will be interesting to hear if he sticks to the mid-cycle adjustment tone or if he will promise more.”

Futures are fully priced for a quarter-point cut in rates next month and cuts of more than 100 basis points by the end of next year. Morgan Stanley economist Ellen Zentner advised clients to watch for the use of the word “somewhat” when Powell describes future policy. “Acknowledgment that downside risks have increased with no characterization of ‘somewhat’ could be taken as confirmation that it is likely the Fed makes a larger cut in September,”Zentner wrote in a note.

Meanwhile, President Donald Trump showed no signs of backing down in his tussle with China, declaring on Tuesday a confrontation was necessary even if it hurt the U.S. economy in the short term.

Currency markets were mostly subdued as the euro struggled and was last down 0.1% at $1.1092. The dollar index initially rose 0.1% to 98.265, but has since given up gains. Sterling failed to overcome technical resistance and met leveraged selling while the yen came under pressure from Japanese names; it was down 0.3% at $1.2134 and 0.2% against the euro at 91.405 pence.

In commodities markets, U.S. crude rose 17 cents to$56.30 per barrel. Brent added 23 cents to $60.26. Spot gold was weaker at $1,498.15 an ounce.

Market Snapshot

S&P 500 futures up 0.7% to 2,918.75

STOXX Europe 600 up 0.8% to 374.23

MXAP down 0.3% to 152.50

MXAPJ down 0.07% to 495.15

Nikkei down 0.3% to 20,618.57

Topix down 0.6% to 1,497.51

Hang Seng Index up 0.2% to 26,270.04

Shanghai Composite up 0.01% to 2,880.33

Sensex down 0.5% to 37,133.03

Australia S&P/ASX 200 down 0.9% to 6,483.27

Kospi up 0.2% to 1,964.65

German 10Y yield rose 3.1 bps to -0.659%

Euro up 0.04% to $1.1104

Italian 10Y yield fell 6.4 bps to 1.024%

Spanish 10Y yield rose 3.3 bps to 0.129%

Brent futures up 1.2% to $60.76/bbl

Gold spot down 0.5% to $1,500.18

U.S. Dollar Index little changed at 98.22

Top Overnight News from Bloomberg

EU poured cold water on Boris Johnson’s attempt to renegotiate the Brexit deal, saying the so-called backstop to prevent a hard Irish border was a vital part of the divorce agreement

Trump said he would be putting off a planned meeting with Denmark’s prime minister because she didn’t want to talk about a possible U.S. property deal to buy the island of Greenland. In Denmark, members of parliament responded with bewilderment and disbelief

Central bankers and Group of Seven leaders will convene this week 8,000 kilometers apart with the same thing on their mind: What more stimulus do they need to support the weakest global growth since the financial crisis?

China detained an employee of the U.K. consulate in Hong Kong under local law, the Foreign Ministry said, confirming earlier reports he was being held. The issue was an internal Chinese matter and not a diplomatic dispute, the ministry said, adding that detainee Simon Cheng is a Hong Kong citizen

Germany saw weak demand for the world’s first 30-year bond offering a zero coupon, after a global debt rally that has pushed yields across Europe into negative territory

British exporters are to be enrolled in a key customs system so they can trade with the EU after the scheduled Brexit deadline on Oct. 31. The U.K. tax authority will automatically issue more than 88,000 companies with an Economic Operator Registration and Identification number over the next two weeks, the Treasury said in a statement on Wednesday

Norway’s $1 trillion wealth fund, Norges Bank Investment Management, rose $28.5 billion in the second quarter ahead of market turmoil that drove equities lower over the past month and saw bond yields plunge further below zero

Chancellor of the Exchequer Sajid Javid may wait to name a successor to BOE Governor Mark Carney until after Britain’s planned Oct. 31 departure from the EU, according to a person familiar with the process

U.K. now plans to only participate in EU meetings where it has “significant national interests involved,” according to a letter signed by PM Boris Johnson’s EU Adviser David Frost

U.S. economy doesn’t appear to be headed toward a recession, San Francisco Fed President Mary Daly said. “When I look at the data coming in, I see solid domestic momentum,” Daly she wrote in a post on Quora.com

Just over a year after agreeing to front Italy’s oddball coalition as its prime minister, Giuseppe Conte handed his resignation in to President Sergio Mattarella Tuesday night, leaving his brief political career up in the air

U.S. President Donald Trump said he can cut taxes by indexing capital gains to inflation without congressional approval, a move the White House has been considering for months

Wall Street watchdogs handpicked by President Trump eased the Volcker Rule’s controversial ban on banks making speculative investment

Asian equity markets traded subdued as the region conformed to the dampened global risk tone with markets cautious ahead of the looming FOMC minutes and the Jackson Hole Symposium. ASX 200 (-1.0%) underperformed with broad pressure across its sectors. Nikkei 225 (-0.3%) was also lower but with downside stemmed as exporters found some solace from a gradually weakening currency, while Hang Seng (+0.1%) and Shanghai Comp. (Unch.) traded indecisively after the PBoC’s quasi liquidity efforts resulted to another net daily drain and amid ongoing trade uncertainty as US President reiterated he is currently not ready to make a trade deal with China but suggested something will happen maybe sooner later. In addition, reports noted that outflows from funds focused on China investments recently widened to its highest since early 2017. Finally, 10yr JGBs returned flat as the initial upside from the cautious risk tone later faded after hitting resistance at the 155.00 level and near its record highs, while the BoJ were only in the market today for Treasury Discount Bills.

Top Asian News

Hong Kong Protests Enter Crucial Period Before China Anniversary

Cigarette Maker ITC Is Said to Mull Bid for India’s Coffee Day

Yemen Vows to Confront U.A.E.-Backed ’Coup’ as Infighting Rages

China Traders Bet Big on a Lagging Bank Stock in Hong Kong

European equities are higher across the board [Eurostoxx 50 +1.2%] despite a subdued Asia-Pac handover with some citing a possible market squeeze. Market participants note that stocks are driven by a couple factors: 1) Today’s session commenced at a low base as stocks yesterday were pressured by Italian concerns. 2) low volumes heading into key risk events including FOMC/ECB Minutes (full previews available in the Research Suite) and the annual Jackson Hole Symposium, US volumes have also been low. Sectors are all in the green, with underperformance seen in defensive stocks as investors seek riskier equities. Consumer discretionary is the marked outperformer with gains led by Pandora (+13.6%) as its earning-led optimism continues, whilst Fiat Chrysler (+3.5%) and Renault (+4.9%) shares rebounded amid reports on continuing merger talks. In terms of other individual movers, GEA group (+5.1%) rests closer to the top of the Stoxx 600. On the flip side, Alcon (-2.5%) shares fell following earnings after-hours yesterday.

Top European News

U.K. Steps Up Brexit Preparedness for Firms as Deadline Looms; U.K. Budget Deficit Soars as Britain Prepares for Brexit

Norway’s Wealth Fund Delivers $28.5 Billion Gain Ahead of Plunge

Eastern Europe Domestic Swine Fever Cases Climb Fivefold in July

Berlin’s Fintech Wealth Is Attracting at Least One Private Bank

In FX, the Greenback has waned again, with the DXY fading just ahead of 98.500 and the more significant pinnacle reached at the start of the month when the index scaled fresh ytd highs (98.932). Usd/major pairings remain relatively mixed and rangebound in advance of potentially market-moving and game-changing events to come in the form of FOMC minutes, preliminary PMIs, ECB minutes and then the JC gathering that kicks off tomorrow and runs through to Saturday. In the interim, US existing home sales may provide some impetus as the DXY meanders between 98.302-145.

JPY/NZD/CHF/GBP – Another upturn in broad risk sentiment has pushed the safe-haven Yen, Franc and Gold back down from yesterday’s peaks towards 106.60, through 0.9800 and 1500 respectively, but the Kiwi and Pound have also lost ground against the Buck, with Nzd/Usd retesting 0.6400 and Cable retreating from circa 1.2175 to 1.2130. Note, technical resistance at the 21 DMA (1.2172) and ahead of 1.2200 (1.2197 Fib retracement) could have stymied Sterling again along with more clarification from EU officials that any alternatives to the Irish backstop would be facilitated via the PD not the WA.

AUD/CAD/EUR – The G10 outperformers, or at least holding up better than the rest as the Aussie retains sight of the 0.6800 handle, Loonie pivots 1.3300 and Euro continues to straddle 1.1100, awaiting aforementioned highlights for the week (on paper at least). Aud/Usd remains supported in wake of RBA minutes underlining a wait-and-see approach after recent rate cuts, while Usd/Cad has retreated from Tuesday’s apex amidst a rebound in crude prices and looking for further direction from Canadian CPI data and the single currency is still showing resilience in the face of Eurozone political instability in Italy and Spain.

NOK/SEK – The Scandi Crowns are benefiting from the latest revival in risk appetite and Eur/Nok has topped out ahead of 10.0000 despite weaker than forecast Norwegian unemployment, while Eur/Sek is drifting down from 10.7600+ towards 10.7100 in tandem.

EM – A generally firmer tone across the region, with the Rand drawing encouragement from soft SA inflation even though this may prompt more SARB easing, as Usd/Zar breached key chart support around 15.2800 to probe under 15.2200 before returning to 15.2500 and consolidating.

WTI and Brent prices are firmer amid the improvement in risk appetite coupled with support from a larger-than-forecast drawdown in API crude stocks (-3.5mln vs. Exp. -1.9mln). Elsewhere, reports stated that Canada’s Alberta has decided to extend it current production curbs by a year, until the end of 2020 amid slow pipeline progress. Due to the extension, the base limit will increase to 20k BPD from 10k BPD per producers (effective Oct 1st), thus helping out the smaller producers as the first 20k BPD of production will be exempt from cuts. Turning to geopolitics where Fox News, citing sources, reported that an Iranian oil tanker (Bonita Queen) is heading to Syria and carrying around 600k barrels of crude, which would violate Western Sanctions. This comes just days after Iranian tanker Adrian Darya 1 (formerly Grace 1) was released from Gibraltar after being seized regarding suspected exports to Syria. On today’s docket, participants will be eyeing the widely followed weekly DoE inventory data for an immediate catalyst ahead of the FOMC minutes, with headline crude expected to drawdown of 1.889mln. Elsewhere, gold is lacklustre and trades around the 1500/oz mark amid a seemingly improved risk tone and some potential profit taking ahead of the FOMC minutes later. Meanwhile copper moves in tandem with the current risk sentiment and trades higher on the day, albeit prices remain below 2.6/lb. Finally, Dalian iron ore futures declined to 10-week lows amid the ongoing supply/demand imbalance, with traders citing further downside in light of BHP’s bleak outlook for the base metal.

US Event Calendar

7am: MBA Mortgage Applications, prior 21.7%

10am: Existing Home Sales, est. 5.39m, prior 5.27m; MoM, est. 2.3%, prior -1.7%

2pm: FOMC Meeting Minutes

2pm: FOMC Meeting Minutes

6:30pm: Fed’s Kashkari Speaks at Economic Conference in Minneapolis

DB’s Craig Nicol concludes the overnight wrap

There may have been a slight lull in newsflow over the last 24 hours however the few scraps of news that we have been fed have left markets somewhat uninspired. By the close of play last night the S&P 500 ended -0.79%, with similar moves for the NASDAQ (-0.68%) and DOW (-0.66%). There was more political volatility in Italy and reports of new tax cuts in the US, but the dominant factor was again trade. US Secretary of State Pompeo told CNBC that Huawei remains a national security threat and also that he is concerned about “other Chinese companies.” That could portend expanded sanctions, though Pompeo did go on to say that he expects the US and China teams to resume trade talks in the short term. Later in the day, President Trump said that he’s “not ready to make a deal with China” and said that Europe would meet any demand if faced with the threat of tariffs on car imports. In sympathy, safe havens were well bid with 10y Treasury yields down -5.1bps and thus reversing Monday’s move, while Gold closed up +0.75%. The yield curve also flattened another 2.0bps to 3.9bps having started the day closer to 7.0bps.

As for those developments in Italy, as expected Conte confirmed his resignation. Conte made it clear that the populist coalition of the League and 5-Star was over, calling Salvini’s decision to spark a political crisis “irresponsible’, although Salvini did try to make a last ditch attempt to smooth things over with 5-Star in order to pass the 2020 budget before heading to the polls. The question now is what will be President Mattarella’s next move. Mattarella needs to assess if a new coalition is viable or whether elections need to go ahead, most likely in October. Of the outcomes it’s likely that the market would view a PD/5-Star coalition as most favourable with 5-Star having adopted a less confrontational stance on Europe and a more responsible stance on public finances in recent times. Plus, if Mattarella allowed them to form a government, it’s likely that he would require assurances on the budget beforehand. However, the medium term risk is that such a coalition is unstable and falls apart leading to an outright victory for the League.

In terms of markets, BTPs outperformed all other sovereigns yesterday, rallying -6.4bps to 1.367%. Bunds fell -4.2bps to -0.694% and while we’re on them, it’s worth noting that we will likely see the first ever 30y Bund sold at a 0% coupon today when the auction is held this morning. Meanwhile the FTSE MIB dropped -1.11% yesterday, slightly underperforming drops for the STOXX 600 (-0.68%) and DAX (-0.55%). Despite the selloff in equities, European HY credit spreads tightened -6bps, while they widened +2bps in the US.

Overnight, markets appear to be struggling for direction with the Nikkei (-0.33%), Hang Seng (+0.11%), Kospi (+0.33%) and Shanghai Comp (+0.02%) pulling in different directions but on fairly low volumes. Futures on the S&P 500 are up +0.30% while there’s not much to report in FX or bond markets.

Moving on and looking ahead to today we’ve got the FOMC minutes from the July meeting out tonight. It’s worth noting that there will be an element of staleness to these now given the tariff developments since then however our economists made the point that they may provide an important benchmark for Fed officials’ outlooks prior to the escalation of trade tensions. They note for example, if the minutes indicate officials’ existing economic views were largely predicated on a flare-up in trade tensions, as St. Louis Fed President Bullard (dove/voter) mentioned last week, this would be relatively hawkish as it would imply officials think they do not need to do much more easing than they have already foreshadowed. However, if trade tensions returning to a boil a day after the July meeting was actually a surprise, which would be implied by Powell saying they had “returned to a simmer” in his prepared remarks to open the press conference, this would be consistent with our economists’ call that more monetary policy easing than was built into the June dot plot is to be expected.

In other news, there was some focus on a NY Times article in markets yesterday which suggested that President Trump could abandon some of his tariffs if the US economy threatens to go into recession. It also mentioned a cut to payroll taxes, which would directly boost labour income. That is a somewhat progressive form of tax cut, so it could tempt Democrats into supporting it, but it remains to be seen if the House will want to hand Trump any legislate wins in an election year. Later in the day, President Trump acknowledged that there have been discussions about payroll tax cuts, though he emphasised “whether or not we do it now, it’s not being done because of recession.” He also mentioned indexing capital gains taxes to inflation as another possible form of tax relief, which could be done with executive action, thus avoiding Congress, though legal experts are undecided on if that measure would survive court challenges.

Finally, there were a few Brexit headlines to digest yesterday, with the UK doing nothing to signal a change in their policy of insisting that the backstop be scrapped. Media outlets reported that Chancellor Merkel said “we will think about practical solutions,” which was viewed as a possible signal that the EU may be more willing to negotiate. We’re sceptical that her remarks signalled any change in policy, but the pound nevertheless gained +0.36% and +0.86% from the lows.

To the day ahead now, which this morning includes July public finances and net borrowing data in the UK, while this afternoon in the US we’ll get July existing home sales before the FOMC minutes are released. Away from that the EIA crude oil inventory report will also be released.

via ZeroHedge News https://ift.tt/2ZfDV7b Tyler Durden

Last night, when we previewed Germany’s sale this morning of what would be the world’s first ultra-long (30 Year) auction with a negative yield, we said that “traders will closely following the oversubscription rate on the sale, which neared a record low in the July after falling for the last three auctions.” And sure enough that turned out to be a rather thorny issue as the bond sale was technically a failure.

Here’s what happened: on Wednesday morning, with its entire yield curve below zero and the yield on the 30Y auction assured to be below zero, a reflection of dwindling expectations for inflation and growth over the coming years and ahead of the ECB’s relaunch of QE next month – Germany was hoping to sell some €2 billion in bonds maturing 2050. However, with bond yields rising sharply into the auction, with the yield on the German 30Y rising from -0.18% to as high as -0.10%, demand suddenly slumped.

And so, when the dust settled, it turned out that Germany had managed to sell just €824 million of the total €2 billion target at a record low yield of -0.11%, with the Bundesbank forced to retain almost two-thirds of the entire issue as demand plunged. In other words, this was basically a failed auction.

Thanks to the central bank’s intervention, the bid-to-cover ratio was just barely above one, or 1.05 times, versus 1.07 times for the previous sale of similar maturity bonds on July 17, while the real subscription rate – which accounts for retentions by the Bundesbank – fell to 0.43 times against 0.86 times at the previous auction. Anything below 1 indicates that there is no real market demand for the entire issuje.

“It is technically a failed auction,” said Jens Peter Sorensen, chief analyst at Danske Bank AS. “I am not all worried about this — as investors can always just buy in the future and do not need to participate in auctions.”

He may not be worried, but the optics are certainly not pleasant. Worse, it means that a disconnect may be forming between the primary (auction) and secondary market, where foreign investors are willing to send yields to record lows in the open market but stay quiet at auction, resulting in a potential air pocket between market and auction prices.

As Bloomberg adds, Commerzbank AG had expected demand to come from life insurers and macro investors before the sale. It failed to materialize.

Which begs the question: will this mini buyers strike for the historic auction be the catalyst that sends yields sharply higher? So far, it has not – despite the poor demand, the yield on the bonds dropped as low as -.13% after the auction, and was trading at -.117% last, suggesting that buyers are less worried about the failure and more worried about what happens to the European economy in the future.

via ZeroHedge News https://ift.tt/2Zkh1Ym Tyler Durden

As we pointed out yesterday, migration from Hong Kong to Taiwan has surged this year – but not solely because the streets of Hong Kong have been clogged with protesters since June. Young Hong Kongers, like their American counterparts living in San Francisco and Brooklyn, are struggling with the twin burdens of managing rent in one of the world’s most unaffordable cities. But unlike young Americans, Hong Kongers are also struggling against the creeping authoritarianism from Beijing.

This prompted Bloomberg to name Hong Kong’s millennials “the generation with no hope.”

And its latest profile begins with the story of Billy Tung, a 28-year-old accountant who regularly works weekends, but barely makes enough to share a small apartment that’s been partitioned into six bedrooms.

Billy Tung

Like many young workers in his situation, Tung is contemplating a move to Taiwan, where housing is more affordable, and which has a much lower cost of living.

Like many Hong Kongers of his generation, Tung finds it hard to save even while he carefully watches his spending on a day-to-day basis, which is why he’s been toying with the idea of moving to Taiwan. “I don’t want to spend the next 10 years working just to give it all away to Hong Kong real estate developers,” he said.

In a description that, probably intentionally, reflects the US, BBG writes about the “cardboard grannies” – elderly poor who have been reduced to picking through trash and recyclables – and a sense of aspirational living that has given way to hopelessness.

And this has been facilitated by a growing lack of economic and political self-determination felt by Hong Kongers.

Hong Kong has long been a land of contrasts in which glittering skyscrapers and chauffeur-driven Rolls-Royces are juxtaposed with decrepit apartment blocks and “cardboard grannies” picking through rubbish in search of recyclables. An aspiration for a share of those riches has been replaced by a growing sense of hopelessness.

Ho-Fung Hung, a professor in political economics who’s a China expert at Johns Hopkins University, says the economic malaise, combined with a perceived loss of cultural identity and frustration at a lack of political voice, is driving young people into the streets. “Participants come from all economic backgrounds,” says Hung. “What binds them together is a shared sense that there is no future for them in Hong Kong. Compared with their parents, they will live a lower quality of life.”

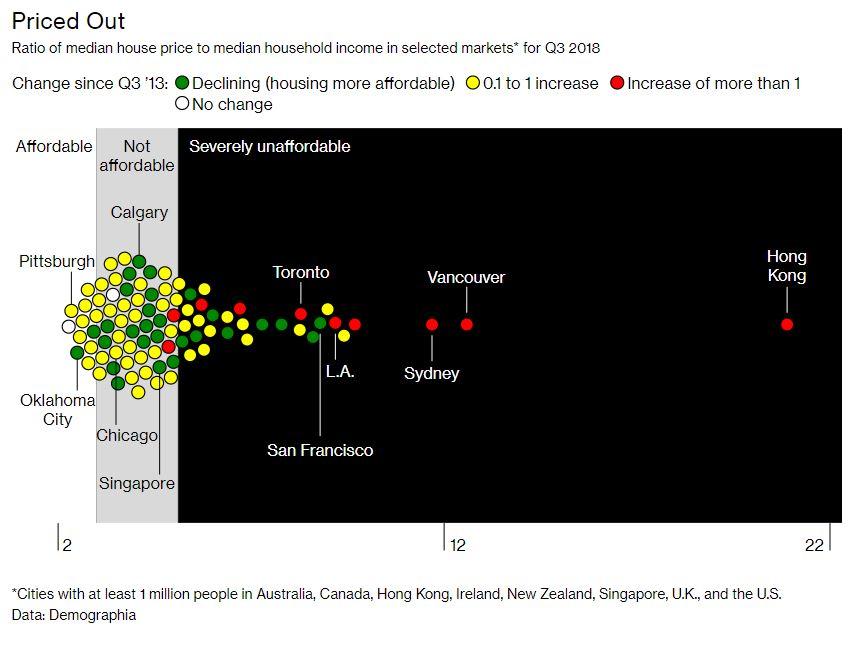

Median property prices in Hong Kong are roughly 21x median household incomes, which is more than Vancouver and Sydney, which come in around 13x and 11%. Meanwhile, wage growth in HK has slowed, while wage growth on the mainland has accelerated.

Huge demand, coupled with constrained supply in a market dominated by a handful of developers and cashed-up buyers from the mainland, has acted as a powerful cocktail to drive up house prices.

Wealthy shoppers from the mainland also drive up the prices of goods, as 1 in 5 Hong Kongers lives in poverty. Young people don’t have much trouble finding work, but too many jobs simply don’t pay a living wage.

As another young freelance worker complained, it’s impossible to survive in HK without support from her family. She’s worried that, when she finally marries, she “won’t have enough for a decent wedding banquet.”

Sze Chan, a 20-year-old who designs menus for restaurants on a freelance basis, has been on the front lines of the protests in recent weeks as police fired tear gas. “Young people in Hong Kong are very confused about the future,” she says. “Unless you get support from your family, it’s impossible for one to live. And with so little left every month, you can’t even have a decent wedding banquet when you marry, let alone buy a home.”

Chan at least has the option of still living at home, without which things would be much tougher. “The young people go on the streets not just because of the political situation—the government’s inability to address social issues plays a role, too. If it’s just about the extradition bill, there wouldn’t be so many people out protesting,” she says.

Yet, unlike their counterparts in the US, Hong Kongers haven’t embraced Communism and Socialism…despite having the world’s largest socialist power breathing down their necks.

via ZeroHedge News https://ift.tt/2NlW50T Tyler Durden

China confirmed that it has detained an employee of the UK consulate in Hong Kong, according to BBC and Bloomberg.

Nearly two weeks after Simon Cheng failed to return from a conference over the border in Shenzen, prompting his girlfriend, with whom he’d purportedly been texting at the time he was seized, to finally go to the press, Chinese Foreign Ministry spokesman Geng Shuang said Wednesday that Cheng was being held under a 15-day administrative detention process in the mainland city of Shenzhen. Geng said the issue was “a domestic matter” and not a “diplomatic dispute.”

If he’s only being held for 2 weeks, Cheng should be nearing the end of his time in custody, presumably unless Beijing wants to move ahead with formal charges.

Simon Cheng

The UK’s foreign office said Tuesday that it was “extremely concerned” about Cheng’s disappearance, and was seeking information from authorities in Hong Kong and the southern Chinese province of Guangdong.

In a sign that Cheng’s detention could be retaliation for UK lawmakers’ support for the pro-democracy protesters in HK, Geng cited China’s Public Security Administration Punishment Law, a statute pertaining to minor violations.

Geng warned the UK against meddling in the affairs of its former colony. “The British side has made a lot of erroneous remarks on Hong Kong,” Geng said, urging the UK “to stop pointing fingers and making accusations.”

Cheng’s disappearance has upset the UK consulate (though its reasons for not going public remain a mystery) given Beijing’s tendency to retaliate against diplomatic personnel. Chinese police have charged a former Canadian diplomat and a Canadian businessman with espionage, purportedly as retaliation for the decision to arrest Huawei CFO Meng Wanzhou.

via ZeroHedge News https://ift.tt/2Hi9HpX Tyler Durden

The toxic tide of anti-Russian propaganda and misinformation continues to surge, and it is depressing for those who wish that relations between Russia and Western Europe could be improved. The state of affairs seems even more disheartening when we consider what’s being going on in the skies, because recently there have been some interesting incidents.

First, the matter of harassment of a Russian passenger aircraft, a Tu-154 airliner for which a flight plan had been filed to fly over the Baltic and was en route from Kaliningrad to Moscow on August 13 when it was intercepted in international airspace by a NATO F-18 based in Lithuania. Russia’s defence minister, Sergey Shoygu, was a passenger, and this was the second time that an aircraft on which he was travelling has been buzzed by NATO fighters. According to Stars and Stripes, “A similar incident occurred in 2017, when a Polish F-16 fighter approached Shoygu’s plane over the Baltic Sea and a Russian jet pushed it away.”

Reporting this episode of NATO irresponsibility, Fox News quoted a NATO official as saying that “a Russian aircraft, escorted by at least one Russian fighter jet, was tracked over the Baltic Sea earlier today. Jets from NATO’s Baltic Air Policing mission scrambled to identify the aircraft which flew close to Allied airspace. Once identification of the aircraft had taken place, the NATO jets returned to base. NATO has no information as to who was on board.”

This statement contains a blatant lie — the claim that the aircraft had to be identified, when in fact it had filed a flight plan and its transponder was functioning. Then there was an allegation that is sheer nonsense, because if NATO doesn’t know the movements of Russia’s defence minister, then its intelligence services should all pack up. The contention that there was “no information as to who was on board” is utterly absurd. Mr Shoygu had been attending a ceremony for the construction of a new military academy in Kaliningrad, and this had been widely reported.

Two days after NATO’s absurd fandango in international airspace, there was another incident involving a Russian airliner. This time a Ural Airlines Airbus 321 hit a flock of birds while taking off from Moscow. The engines died, and the pilot most skilfully landed his aircraft in a field.

There seems to be something outstanding about airline pilots. Sure, one hears from time to time that one of them has been disciplined or even sacked for over-indulging in alcohol — but when you think of their vast responsibility, week in, week out, flying these enormous machines all round the world, you might agree that the occasional tipple is understandable. But the stories of how they react when they’re faced with a dire and potentially fatal situation are most heartening, and I am a wholehearted admirer of these dedicated professionals. They are usually the subjects of approving reports in western media outlets, which in such instances take a rare opportunity to be in general complimentary.

The New York Times, however, while not bothering to write a report of its own, carried an Associated Press item quoting an aeronautics professor at the Massachusetts Institute of Technology, John Hansman, as saying that in the skilful Moscow crash-landing “The pilot did a good job, but that’s why he was there.” Does this man hear himself? And what were the AP and NYT thinking of, retailing such condescending garbage from an academic who, although qualified to fly aircraft, isn’t fit to lick the boots of such as Ural Airlines Captain Damir Yusupov who saved the lives of 233 people by exercising cool professional skill.

Some western media reports were grudgingly complimentary. The UK’s Guardian newspaper set the tone by headlining that “The Kremlin lauds ‘heroes’ who landed plane in cornfield after gull strike” which was positive, although use of the word “Kremlin” is always intended to inject a sinister undertone. It reported that the aircraft “came down in a field south-east of Moscow with its landing gear up after colliding with a passing flock of gulls, which disrupted the plane’s engines . . . Some compared the landing to that of US Airways Flight 1549 on the Hudson River in New York in 2009 after it struck a flock of geese.”

The aircraft “came down”? Well, certainly it did, but it didn’t just pancake into the ground. It was skilfully guided down by a pilot like the one who, according to the same newspaper, “managed to avoid disaster and save the lives of all 155 people on board his stricken plane when he ditched into the icy waters of the Hudson river moments after taking off from New York’s LaGuardia airport” when his aircraft was similarly struck. The difference in tone is intriguing, just as is the Guardian’s snide aside that “Safety concerns have plagued Russia’s airline industry since the 1991 collapse of the Soviet Union, though standards are widely recognised to have risen sharply in recent years, particularly on international routes.”

What on earth have “safety concerns” got to do with an aircraft flying into a flock of birds? These sorts of mishaps are certainly a matter of concern, but are totally irrelevant to international standards of aviation safety. It wasn’t a rerun of the Boeing 737 Max affair, after all.

Then came the widely circulated Reuters news agency observation that “The plane was due to fly to Simferopol in Crimea, the peninsula annexed by Russia from Ukraine in 2014.”

The western media can never resist an opportunity to bring up the alleged “annexation” of Crimea, in spite of it being obvious that, as the BBC reported, the vast majority of Crimean citizens indicated in a referendum that they supported joining Russia. There was no surprise about the result, as most of these people are Russian-speaking, Russian-cultured and were liable to persecution by the Kiev administration that came to power following the US-assisted coup in 2014. (It is almost forgotten that, as revealed in mysterious circumstances, the US “lead point person for the Ukrainian crisis” Victoria Nuland was recorded before the coup as saying to the US Ambassador in Kiev that “Yats [Arseniy Yatseniuk, an anti-Russia activist] is the guy… Why don’t you reach out to him and see if he wants to talk before or after?”)

But President Obama claimed that the referendum was “illegal” and declared it would never be accepted by Washington. The story to be spread was that the people of Crimea were victims of a massive Russian invasion, which is now firmly believed in the West, demonstrating that, as stated by Nazi propaganda meister Joseph Goebbels, “If you tell a lie big enough and keep repeating it, people will eventually come to believe it.”

Consistent with Goebbels’ advice, it is a basic tactic of psychological operations to inject such snippets in a seemingly relevant context — hence inclusion in an international news agency report about the bird-strike on a Russian Airbus 321.

From menacing a Russian airliner in international airspace, to manipulating a news item about a Russian aircraft accident, the western establishment is demonstrating its taste for confrontation rather than conciliation. But it is time to think more positively. Russia and Western Europe need to work together to improve their economies and benefit their citizens. Rapprochement and harmony are the way ahead. The pointless air fandangos and derisive slanting of news items should cease, otherwise we’ll all be up in the air forever.

via ZeroHedge News https://ift.tt/2TR5yyh Tyler Durden

{kind=link}