The Days Of Tracking Robinhood Data Are Now Officially Over Tyler Durden

Mon, 08/10/2020 – 05:30

For years, the website RobinTrack.net has been doing a great job of mining RobinHood’s data to provide raw data and a visualization of which stocks the users of the retail brokerage have been holding and disposing of on a daily basis.

RobinTrack.net has been a wonderful way to keep an eye on exactly what stocks the bagholder crowd have been rushing into on a daily basis, providing insight into the hysteria of retail daytraders, allowing hedge funds to likely frontrun the data and providing opportunities for short sellers looking for ideas.

But those days appear to be all but over.

On Friday, CNBC reported that the brokerage will no longer display how many of its users hold a certain stock. In addition it is going to be taking down its public API data that allows other sites, like RobinTrack.net, to source its data for visualization and analysis purposes.

“The data has been used to show booms in retail stocks,” a CNBC report said on Friday. “You guys know RobinTrack well. A lot of financial news outlets use it for reporting, including CNBC.”

Robinhood has said in a statement that even thought it is restricting third party access to its API data, it still has “many other tools” that its users can offer.

“Trends and data are often misconstrued and misunderstood,” Robinhood said. “The majority of its users” are buy and hold users, not daytraders, the brokerage said.

Yeah, right. Aside from the PR spin of trying to position itself as a serious brokerage and not a casino app for unemployed daytraders, we’re guessing there is another angle to Robinhood removing this data: if you want it in the future, you’re going to have to pay.

Like its order flow, we’re guessing “everything’s for sale” at Robinhood and wouldn’t be surprised if the brokerage creates a hedge fund “product” with this data moving forward. Here’s CNBC’s report from Friday:

Robinhood says it will stop showing how many customers hold a certain stock on its website👀

Also restricting access to its API.. (that public data is how RobinTrack & other third parties show what Robinhood retail traders are buying and selling) pic.twitter.com/ZjX4DMykZ4

The EU is facing a crisis like never before. Even its own fanatic supporters are talking about an end game after recent concessions over a corona rescue plan have exposed how little grip Brussels has left. It’s all hidden in the small print.

Failed talks with the UK over a Brexit deal are just one of a handful of examples of why now pro-EU experts are all sounding the alarm over the EU’s stability. Along with the Corona bailout, there is a new impetus of ‘euro-scepticism’ from many member states signalling the end of the EU as we know it.

Talks between EU negotiators and Britain’s Brexiteers might as well have collapsed. In fact, they haven’t, but in so many ways it would be better if they did. The EU is taking its largest gamble ever by playing a ‘last minute’ game of chance with Boris Johnson – a leader who has proven that he is determined not to be drawn into such a charade and will firmly stick to the December 2020 deadline of pulling the UK out, with or without a deal.

A big sticking point is fisheries of course. France is putting huge pressure on Michel Barnier to negotiate something for the French. Before joining the EU, Britain had more or less a monopoly of the seas surrounding its shores – which it lost when it joined the European Union with now other countries fishing six times more fish than the UK. The trade deal itself also has a number of difficult areas which neither side wants to concede.

Given the EU’s track record and what we know about its own style, everything points to a last-minute drama at the end of November this year when Barnier and his officials wake up to the reality that Britain really is going to adopt WTO rules and get out of the EU altogether with no deal.

Many hardcore Brexiteers even prefer this option to a present deal now – a point that Barnier seems to have not grasped – as they believe a second round of negotiations will put Britain in a much stronger position to cut a deal.

Italy’s hangover

But in many respects a no deal Brexit is being shadowed now by an even bigger threat to the EU’s existence, which is how it has failed to nail a 2 trillion euro rescue package for its member states affected the most by the Covid-19 virus. In July, the EU agreed to a much smaller package which was a mixed bag of loans and grants. While Italy has been given a grant of 80bn euros and Greece 23bn, both these countries will be expected to pay part of a 750bn euro debt which is what some analysts like Yanis Varoufakis are calling a ‘Eurosceptic’s dream’. The recalcitrant former Greek finance minister reckons that Italy will only end up with 30bn euros after it has contributed to the bigger EU corona recovery debt, which guarantees that this country will become even more Eurosceptic in the future once Italians understand the small print of the ‘deal’.

Less money to go around

But the deal itself has driven a wedge between a number of northern European countries like Sweden and the Netherlands – and the rest – and, according to a number of pro-EU experts, is signalling the beginning of the end for the EU, which in reality is going to operate from 2021 with less money in its coffers than before, with Britain no longer contributing. Even BBC experts who are staunchly pro-EU, to the point of being fanatical, are pointing this out. Lyce Doucet, the BBC’s top international correspondent, speaking on a talk show, talked about the ‘breath-taking’ compromises which have been made in Brussels for the deal to get the green light and that break-away EU states like Hungary going rogue and new political/financial problems with Italy will play a real role in possibly the EU institutions having real difficulties in remaining in power of the European Union project.

With less money to go around, a big part of the EU breathing new life into itself – bigger projects like the environment, defence and even health funds – will all have to remain fanciful ideas on paper in Brussels.

And yet there’s no sign of the EU tightening its own belt on its own spending. Brussels simply doesn’t do austerity, unlike member states, which support it. What it prefers is to borrow money on international markets so that future generations are saddled with the debt and it can give off a veneer of normality and even stability. There is another cunning reason why it likes to always talk big figures. While talking hundreds of billions of euros, it makes it more or less impossible for any journalist in Brussels to suggest that the EU cuts its own operating costs – which by comparison to the huge numbers bandied about, looks very modest.

The EU’s entire operating budget for the last seven years – each year – is a modest 165 bn euros. No journalists in the Belgian capital like to point out that this figure has gone up every six years.

And no Brussels-based journalists like to admit that for the first time, despite appearances to the contrary, the actual EU budget for the next six years (2021 – 2027) is to remain the same at around a trillion euros.

This is because, in reality, no one has worked out how to paper over the cracks of the UK no longer sending 9bn euros to Brussels, which has to be paid by the larger contributors like France and Germany.

What is harder to grasp is how the EU is going to get much bigger funding for its international aid program, which it wants to boost by a massive 30%.

A good laugh

The EU has big plans to punch above its weight around the world in how much money it pumps into “developing economies”. It currently spends from its annual budget around 13bn euros in total propping up dictators who are happy to plaster EU aid boards all over the country and show mock reverence to Brussels’ artificially created hegemony. Some EU websites, although not mentioning the total new budget for the EU itself, refer to pumping this up by 30%. Given that the EU has a funding crisis, it’s hard to see how it will shuffle its present arrangements to meet this.

What the EU could do is scrap this entire aid project altogether and use the money for start up businesses in Europe as a way of offsetting crippling unemployment. But that’s unlikely to happen.

If you still have a sense of humour after leading EU supporters of the project talk about the beginning of the end, then here’s a howler for you. Buried deep in euro jargon is one minor detail which will indeed back up Varoufakis’ claim that the new blueprint is written by a eurosceptic who wants to bring the house down. Outside of the EU budget is the 750bn euro corona rescue package, which, wait for it, isn’t going to be paid back to its lenders, until the NEXT, EU budget period, starting 2028.

This is unprecedented as is the new rogue state of Hungary which is setting a new norm in how it regards Brussels’ so-called leadership. But the fact that most EU leaders or even Brussels officials may not be in employment in 2028 (or some may not even be alive) says a lot about how much confidence the EU has in itself as a serious long-term project. Expect biographies in years to come which claim corona was “killed” the EU by pensioners sitting in high-backed chairs talking to BBC journalists with softly spoken voice overs referring to Ursula and Angela and their care home tantrums. Will Angela Merkel in 2028 even be able to give TV interviews?

via ZeroHedge News https://ift.tt/2DCbWG6 Tyler Durden

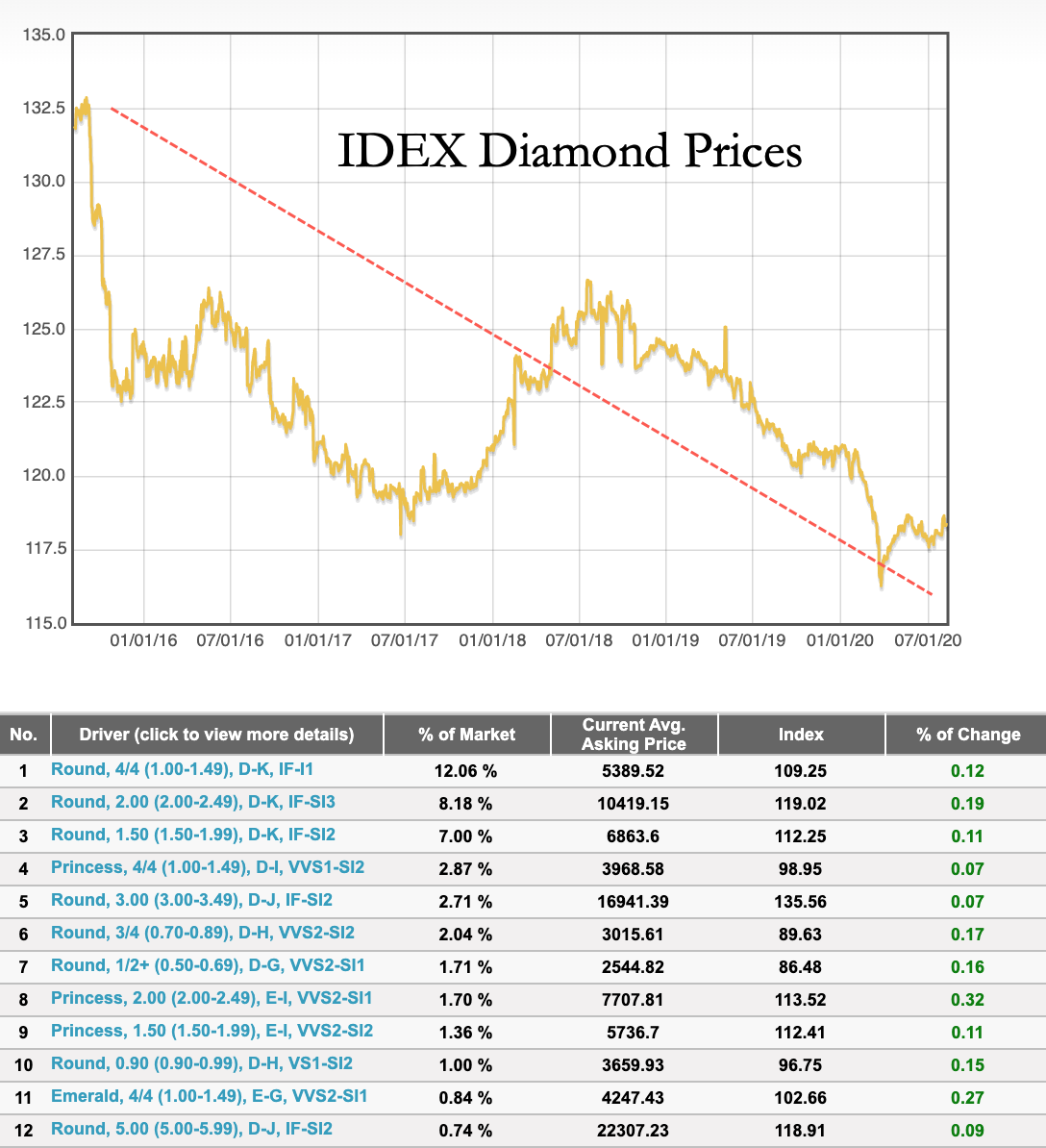

Botswana’s rough diamond exports crashed 68% in 2Q20, Reuters said, citing data from the Bank of Botswana.

De Beers Group, the world’s largest diamond company, received about 70% of its supply from Botswana, warned last month it was “paralyzed by the pandemic” as diamond demand slumped worldwide.

Rough Diamonds

Exports of diamonds from Debswana Diamond Company Limited, a joint venture mining operation between Botswana and De Beers, was approximately $293 million in 2Q20, down from $916 million in the previous quarter.

Bank of Botswana’s data showed no diamonds were exported in May, while only $20 million worth were shipped in June.

De Beers first realized waning diamond demand before the virus pandemic, was accelerated during lockdowns, and is now having a ripple effect that is set to wreak havoc on Botswana’s finances.

IDEX Diamond Prices

Plunging diamond exports will hurt Botswana’s balance of payments deficit, as diamonds are about 70% of the country’s exports. A fiscal crisis could be brewing in the country as 30% of the country’s revenues are derived from diamonds.

Diamonds may be forever, though demand for the diamonds is not. De Beers will have to slash production to balance the oversupplied market. What’s different about this recession is that consumer demand will not bounce back in a “V” as a virus pandemic keeps people out of jewelry shops, postpones weddings, and or simply consumers worldwide are just too broke to spend on luxury items.

via ZeroHedge News https://ift.tt/2DJM2zT Tyler Durden

It’s been a wild and bumpy ride for OPEC+ this year. The consortium, consisting of the traditional members of the Organization of the Petroleum Exporting Countries plus oil and gas superpower Russia, was largely responsible for the huge collapse in oil prices toward the end of April. After a huge drop in oil demand corresponding with the devastating spread of the novel coronavirus around the world, an OPEC+ strategy meeting turned into a spat between Russia and Saudi Arabia which then turned into an all-out oil price war and massive global oil glut. The oil storage shortage created by this glut would go on to push the West Texas Intermediate crude benchmark into previously-unthinkable negative territory, closing out the day on April 30th at nearly $40 below zero per barrel.

OPEC+ has since reconciled and once again banded together to address the oil market crisis, making myriad pledges and severe production cuts to bolster crude oil prices. But many of the countries that made those pledges have fallen far short of their promises.

“OPEC reached a historic deal to cut output by 9.7 million barrels per day in April, but a number of countries fell significantly short in meeting their production targets,” reports Markets Insider.

But, just this week Iraq, OPEC’s second-biggest member just made a huge commitment to cut its oil production in the coming months. After a Thursday night conversation between Iraqi and Saudi leadership, Baghdad “made a commitment to cut oil production by 400,000 barrels per day in August and September,” a massive uptick from the nation’s relatively paltry July production cut of 11,000 barrels per day.

But while the oil market is now recovering and countries like Iraq are starting to fall in line, this may not indicate smooth sailing for the international oil consortium.

“Rebounding oil prices have the potential to show the cracks that already exist in the delicate cooperation between the powerful oil-producing nations,” the Wall Street Journal reported this week in an article entitled “How a Tenuous Saudi-Russia Oil Alliance Could Melt Down.”

The article recounts OPEC’s rough, tough year(s), remarking that “Saudi Arabia, the dominant force of OPEC, might as well have been herding cats in recent years trying to bring order to the unruly cartel.” At first, the addition of Russia to bring the “+” to OPEC+ was a godsend for the group and a boon to oil markets, but now Riyadh and Moscow’s extremely different ambitions could spell doom for the cartel.

In light of the fact that many OPEC+ members have been complying with production cuts and that these cuts seem to be working, in mid-July, the cartel actually agreed to let OPEC members’ overall production to increase by a considerable 1.6 million barrels a day.

“The latest adjustment was a reflection of a demand picture that seems to be improving,” reports the Wall Street Journal.

“Yet that very development could hobble cooperation between Saudi Arabia and Russia going forward.”

As history has taught us over and over, alliances more often than not require a common enemy–in this case a floundering oil market.

“Under $40 [a barrel], they were able to come together. The higher the price, the harder it will be to get Russia to go along with continued production cuts – especially once you get to $50 a barrel for Brent Crude,” Gary Ross, Chief Executive Officer of Black Gold Investors told the Wall Street Journal.

And now, there’s not enough to keep Saudi Arabia and Russia’s diverging visions from, well, diverging. The two nations at the helm of OPEC+ publicly claim vastly different break-even prices and the recent easing of austere production measures could be the harbinger of doom for the already delicately-balanced cartel. And a dramatic failure for OPEC and its consortium of precarious oil autocracies could spell serious geopolitical turmoil for the Middle East, and by extension, for all of us in this global village.

via ZeroHedge News https://ift.tt/2Dup7sN Tyler Durden

Defiant Erdogan Says Turkey Has Resumed Mediterranean Gas Exploration & Drilling Tyler Durden

Mon, 08/10/2020 – 02:45

While over a week ago it was looking as if Turkey might back down on its ambitious oil and gas exploration aims in the eastern Mediterranean amidst global pressure, especially coming from the EU and US, President Erdogan is defiant once again, announcing Friday the resumption of energy exploration work that Greece and Cyprus says violates their territorial waters.

Emerging from Friday prayers at Hagia Sophia – which Turkey recently declared a mosque (in another shot aimed at Greece) – Erdogan said: “We have started drilling work again,” and added, “I don’t think we are obligated to talk to those who do not have rights in the areas of maritime powers.”

Via Reuters

Erdogan said a seismic survey ship is currently en route to the disputed region to continue its energy exploration.

The Turkish president’s comments were also seen as a firm rejected of a recent Greece and Egyptian deal defining their exclusive economic zones in contradiction to Ankara’s interpretation.

Turkey denied the agreement as “null and void” — which means Turkey’s expansionist claims are being contested by pretty much every Mediterranean country, also including Israel. The exception of course, is the Tripoli-based Libyan Government of National Accord (GNA), which lately inked its own agreement with Turkey defining broad swathes of the Mediterranean as within Turkey’s rights.

Turkey has sought to argue that the so-called Turkish Republic of Cyprus, which remains unrecognized internationally, gives it expansive rights encompassing the whole of Cyprus.

Via Anadolu Agency

Meanwhile Greece has complained of weekly illegal Turkish military incursions of its airspace, in a situation that is becoming militarized by the week.

Lately Greek forces have been on ‘high alert’ after Athens promised it would never let Turkish ships encroach of Greek maritime territory. The EU has also threatened sanctions over the past month as the crisis has grown.

via ZeroHedge News https://ift.tt/30G34YE Tyler Durden

General Dwight Eisenhower was the first NATO supreme allied commander.

After assuming that post in 1951, General Eisenhower wrote about NATO’s goal:

“If in 10 years, all American troops stationed in Europe for national defense purposes have not been returned to the United States, then this whole project will have failed.”

It did fail because seven decades later, long after the Soviet Union dissolved, NATO still exists with thousands of American troops deployed throughout Europe.

The Warsaw Pact was disbanded in 1991 as Soviet troops withdrew from Eastern Europe. The American empire exploited this peace to expand NATO and absorb former Warsaw Pact nations and even former Soviet republics while deploying NATO forces to Russia’s borders.

Watched the linked video for details:

via ZeroHedge News https://ift.tt/3fFScOJ Tyler Durden

So now we don’t have to listen to what those doctors said in front of the US Supreme Court, because it turns out that one of them has some whacky beliefs about sex with demons causing reproductive disorders. What a relief.

I’m not going to pretend that the things Dr. Stella Immanuel has said don’t sound just a little crazy to me. They do.

But I’ve been observing this game long enough to have a pretty good idea of how this works:

Someone says something that contradicts the dominant narrative (in this case, the narrative about medical science), and the machine that supports that narrative goes into overdrive to discredit them, with whatever information they can dig up–as long as it doesn’t involve discussing the actual substance of what the person has said.

I understand that for some people, maybe even for a great many, that is the end of the conversation.

So for everyone who is satisfied with the “fringe doctors promoting hydroxychloroquine also believe demon sex causes fybroids” narrative–please, stop here. Your ride is over, and you may go on believing that this group of doctors and other professionals has been thoroughly discredited by these statements.

For everyone else, if you are at all interested in why such a coordinated effort has been launched to silence and discredit this group, why – even before the sex demon stuff was uncovered – videos of the group’s press conference were quickly yanked from YouTube, and why their own website was taken down without warning by its host, SquareSpace, (their new website can now be found here) then please keep reading.

WHAT THE AMERICA’S FRONTLINE DOCTORS GROUP SAID:

What follows is a brief summary of the key points made by the group America’s Frontline Doctors at their press conference last week. I will not comment on the validity of their claims, however founder Dr. Simone Gold has provided support for much of what the group said, in a white paper that can be found here.

1. They believe that hydroxychloroquine is an effective treatment for Covid-19.

This is the claim made by several of the speakers, including Dr. Immanuel, based on their own clinical experience, as well as on multiple published studies. Many of those studies are listed here, and here.

2. State licensing boards are using their power to forcibly prevent people from having access to this drug.

According to Dr. Gold, many states have empowered their pharmacists to not honor prescriptions for hydroxychloroquine to be used in treating Covid-19. This, she says, is unprecedented:

“It has never happened that a state has threatened a doctor for prescribing a universally accepted safe generic cheap drug off-label.”

Meanwhile, says Gold, the drug is available over the counter in many other countries, including Iran and Indonesia, where it can be found “in the vitamin section”.

3. There is a coordinated campaign to discredit and suppress information about the drug hydroxychloroquine as a possible treatment for Covid-19:

“If it seems like there is an orchestrated attack going on against hydroxychloroquine,” said Dr. James Todaro, “it’s because there is.”

Dr. Todaro is speaking from experience. He was the co-author of a March 13 white paper arguing for the use of hydroxychloroquine against Covid-19. The paper was made public on Google Docs, received a lot of attention, and was then removed–without warning–by Google. (It has since been put back up.)

4. The World Health Organization halted its trials of hydroxychloroquine based on a blatantly fraudulent study that relied on data that it appears never even existed.

Bear in mind that this is the authority upon which YouTube CEO Susan Wojcickihas said she bases her company’s policy on “misinformation”.

The WHO later resumed trials after independent investigators discovered the problems and the study’s authors retracted it.

5. We should be able to have a free and open discussion about this.

Dr. Dr. Joseph Lapado from UCLA, sums it up:

“We’ve been using (hydroxychloroquine) for a long time. But all of a sudden it’s been escalated to this area of looking like some poisonous drug. That just doesn’t make sense… At the very least, we can live in a world where there are differences of opinion about the effectiveness of hydroxychloroquine, but still allow more data to come, still allow physicians who feel they have expertise with it to use that medication, and still, you know, talk and learn and get better at helping people with Covid-19.”

WHY THE ALL-OUT MEDIA ASSAULT ON THE FRONTLINE DOCTORS?:

The influence that the pharmaceutical industry wields over media outlets is no secret. As of 2018, an estimated 70% of all news advertising in the US came from pharmaceutical companies. I have written elsewhere about how “reporting” on medical issues can be difficult to distinguish from outright marketing for drug companies.

Social-media platforms are not immune to this influence, whether it comes via advertising dollars; “partnerships” such as that between the CDC Foundation and MailChimp (which like many other platforms, has an explicit policy of censoring content about vaccines that does not align with the positions of the CDC and the WHO); direct investment, such as that of Google’s parent company Alphabet; or indeed at the behest of politicians such as Congressman Adam Schiff, who last year wrote to the CEOs of Amazon, Facebook and Google, requesting that those companies censor information and products that did not conform to the officially sanctioned position on vaccines. All three complied.

So it should come as small surprise that both Google and YouTube have now taken to removing content supportive of hydroxychloroquine, a drug that is no longer covered by patent, and can be made and sold by any generic producer, for a fraction of the price that Gilead, for example, might charge for its still-patented Remdesivir.

Twitter and Facebook have likewise removed posts about the drug, most notably–and with no visible sense of irony–removing posts of the video in which the Frontline Doctors speak out about widespread media censorship of the topic. (You can now see those videos on Bitchute.)

One need not have an opinion on the merits of the drug hydroxychloroquine in order to recognize that something very odd is happening here. Something that doesn’t seem to have anything to do with free and open inquiry or honest scientific discourse.

Many argue that the politicization of this drug is founded in a desire to unseat President Trump, that the opposition to it is primarily because it was endorsed by Trump, and if it is deemed to be a failure (or even better, dangerous to patients) it will be a powerful strike against the president. That may well be part of what has motivated this. But there is another motivation, having to do with the desire to push a more expensive medication onto the market, and to push a new vaccine on the world’s population.

More broadly, it has to do with the narrative that those in the business of selling drugs demand we believe: that we are all in desperate need of their products (but only the ones still under patent) if we are to be healthy–or indeed, if we are to survive at all.

If it turns out that this “new” virus is easily treatable, with hydroxychloroquine or anything else, then the industry’s dreams go up in smoke. If hydroxychloroquine turns out to be a safe and effective way of treating Covid-19 (as multiplestudies and the experience in many other countriesoutside of the US indicate it may be) then there is much less reason for anyone to receive a vaccine for it, let alone the entire world’s population. Likewise, there is no pressing need to develop a new, more expensive treatment.

But even more than that: If it turns out that hydroxychloroquine is after all a safe and effective treatment for Covid-19, then this whole episode – the silencing of dissenting voices, the “fact-checking” on social media, the campaigns against “misinformation” – will be revealed in plain sight, for what it has always been: Nothing more than a well-funded marketing campaign and damage-control effort on behalf of the industry that wants you to believe that you need to use its expensive products in order to go on living.

So when a group of doctors took to the steps of the US Supreme Court and told the world how they were having success using a cheap anti-malarial that had been in use for 65 years to treat the most deadly contagion of our generation, it was a massive blow to the narrative upon which the pharmaceutical purveyors’ success depends. And over the next few days, as viewers engaged in a race with the censors, quickly downloading videos before they were removed, to post them on other platforms… it became clear that the censors and the gatekeepers had lost control of the conversation.

This is not only about hydroxychloroquine. Every time media outlets or social-media platforms engage in outright censorship of content, in a way that happens to benefit pharmaceutical companies, both parties lose just a little more credibility. The actions we are witnessing now are not the actions of an industry confident in the value of what it provides to the world. They are the actions of a desperate, threatened creature. They are the actions of an entity that is not strengthened by the truth, but weakened by it. That is what these (increasingly obvious) acts of censorship tell us. What we are witnessing are the pangs of a lumbering, wounded, behemoth.

via ZeroHedge News https://ift.tt/2F9sPID Tyler Durden

California Will Soon Be Paying $1,250 To People Who Test Positive For Coronavirus Tyler Durden

Sun, 08/09/2020 – 23:15

Always looking for ways to one-up its own failed welfare state and run the Covid score up on President Trump, California has now approved a pilot plan to pay $1,250 to anyone who tests positive for coronavirus to encourage them to “stay at home and self isolate”.

Alameda County’s Board of Supervisors has set aside $10 million for the program, which will allow payments to 7,500 people, according to the Daily Mail. The program was approved as the county hit a new high in daily coronavirus cases and as California continues to “struggle” to contain the outbreak in its state.

The program is being “welcomed” by local healthcare providers, who say it’ll help those in working class areas stay at home and not spread the virus by leaving the house.

Andrea Schwab-Galindo, CEO of Tiburcio Vasquez Health Center in Hayward commented: “Literally every single person that we have spoken to through our contract tracing program, they have all asked for either food, help with rent, or access to be enrolled in healthcare. Most people that test positive are usually the members that are out there working and able to do that.”

She continued: “You know, they are construction workers, they are grocery workers, so they are more exposed compared to some of the other family members they are trying to support, including their children.”

Resident Robert Mangrobang also embraced the program, stating: “Yeah, whatever makes it a lot easier for people to deal with this pandemic would be great. Twelve hundred dollars or even more would be ideal for comforting a lot of families.”

In order to qualify for the assistance, people who test positive must not be receiving unemployment or sick leave. Approval for the program will require a referral from one of the five approved clinics in the county. The board hopes the program will assist independent contractors, “people who are paid under the table” and “undocumented workers”.

Alameda County saw a large spike in cases on Wednesday, with 321 new cases reported. This was a new daily record for the county.

The area has a 28% positivity testing rate. For some reason, we bet that number rises.

via ZeroHedge News https://ift.tt/2DOoPMW Tyler Durden

The narrative that the Beirut explosion was an exclusive consequence of negligence and corruption by the current Lebanese government is now set in stone, at least in the Atlanticist sphere.

And yet, digging deeper, we find that negligence and corruption may have been fully exploited, via sabotage, to engineer it.

Lebanon is prime John Le Carré territory. A multinational den of spies of all shades – House of Saud agents, Zionist operatives, “moderate rebel” weaponizers, Hezbollah intellectuals, debauched Arab “royalty,” self-glorified smugglers – in a context of full spectrum economic disaster afflicting a member of the Axis of Resistance, a perennial target of Israel alongside Syria and Iran.

As if this were not volcanic enough, into the tragedy stepped President Trump to muddy the – already contaminated – Eastern Mediterranean waters. Briefed by “our great generals,” Trump on Tuesday said:

“According to them – they would know better than I would – but they seem to think it was an attack.”

Trump added, “it was a bomb of some kind.”

Was this incandescent remark letting the cat out of the bag by revealing classified information? Or was the President launching another non sequitur?

Trump eventually walked his comments back after the Pentagon declined to confirm his claim about what the “generals” had said and his defense secretary, Mark Esper, supported the accident explanation for the blast.

It’s yet another graphic illustration of the war engulfing the Beltway. Trump: attack. Pentagon: accident.

“I don’t think anybody can say right now,” Trump said on Wednesday. “I’ve heard it both ways.”

Still, it’s worth noting a report by Iran’s Mehr News Agency that four US Navy reconnaissance planes were spotted near Beirut at the time of the blasts.

Is US intel aware of what really happened all along the spectrum of possibilities?

That ammonium nitrate

Security at Beirut’s port – the nation’s prime economic hub – would have to be considered a top priority. But to adapt a line from Roman Polanski’s Chinatown: “Forget it, Jake. It’s Beirut.”

Those by now iconic 2,750 tons of ammonium nitrate arrived in Beirut in September 2013 on board the Rhosus, a ship under Moldovan flag sailing from Batumi in Georgia to Mozambique. Rhosus ended up being impounded by Beirut’s Port State Control.

Subsequently the ship was de facto abandoned by its owner, shady businessman Igor Grechushkin, born in Russia and a resident of Cyprus, who suspiciously “lost interest” in his relatively precious cargo, not even trying to sell it, dumping style, to pay off his debts.

Grechushkin never paid his crew, who barely survived for several months before being repatriated on humanitarian grounds. The Cypriot government confirmed there was no request to Interpol from Lebanon to arrest him. The whole op feels like a cover – with the real recipients of the ammonium nitrate possibly being “moderate rebels” in Syria who use it to make IEDs and equip suicide trucks, such as the one that demolished the Al Kindi hospital in Aleppo.

The 2,750 tons – packed in 1-ton bags labeled “Nitroprill HD” – were transferred to the Hangar 12 warehouse by the quayside. What followed was an astonishing case of serial negligence.

From 2014 to 2017 letters from customs officials – a series of them – as well as proposed options to get rid of the dangerous cargo, exporting it or otherwise selling it, were simply ignored. Every time they tried to get a legal decision to dispose of the cargo, they got no answer from the Lebanese judiciary.

When Lebanese Prime Minister Hassan Diab now proclaims, “Those responsible will pay the price,” context is absolutely essential.

Neither the prime minister nor the president nor any of the cabinet ministers knew that the ammonium nitrate was stored in Hangar 12, former Iranian diplomat Amir Mousavi, the director of the Center for Strategic Studies and International Relations in Tehran, confirms. We’re talking about a massive IED, placed mid-city.

The bureaucracy at Beirut’s port and the mafias who are actually in charge are closely linked to, among others, the al-Mostaqbal faction, which is led by former Prime Minister Saad al-Hariri, himself fully backed by the House of Saud.

The immensely corrupt Hariri was removed from power in October 2019 amid serious protests. His cronies “disappeared” at least $20 billion from Lebanon’s treasury – which seriously aggravated the nation’s currency crisis.

No wonder the current government – where we have Prime Minister Diab backed by Hezbollah – had not been informed about the ammonium nitrate.

Ammonium nitrate is quite stable, making it one of the safest explosives used in mining. Fire normally won’t set it off. It becomes highly explosive only if contaminated – for instance by oil – or heated to a point where it undergoes chemical changes that produce a sort of impermeable cocoon around it in which oxygen can build up to a dangerous level where an ignition can cause an explosion.

Why, after sleeping in Hangar 12 for seven years, did this pile suddenly feel an itch to explode?

So far, the prime straight to the point explanation, by Middle East expert Elijah Magnier, points to the tragedy being “sparked” – literally – by a clueless blacksmith with a blowtorch operating quite close to the unsecured ammonium nitrate. Unsecured due, once again, to negligence and corruption – or as part of an intentional “mistake” anticipating the possibility of a future blast.

This scenario, though, does not explain the initial “fireworks” explosion. And certainly does not explain what no one – at least in the West – is talking about: the deliberate fires set to an Iranian market in Ajam in the UAE, and also to a series of food/agricultural warehouses in Najaf, Iraq, immediately after the Beirut tragedy.

Follow the money

Lebanon – boasting assets and real estate worth trillions of dollars – is a juicy peach for global finance vultures. To grab these assets at rock bottom prices, in the middle of the New Great Depression, is simply irresistible. In parallel, the IMF vulture would embark on full shakedown mode and finally “forgive” some of Beirut’s debts as long as a harsh variation of “structural adjustment” is imposed.

Who profits, in this case, are the geopolitical and geoeconomic interests of US, Saudi Arabia and France. It’s no accident that President Macron, a dutifulRothschild servant, arrived in Beirut Thursday to pledge Paris neocolonial “support” and all but impose, like a Viceroy, a comprehensive set of “reforms”. A Monty Python-infused dialogue, complete with heavy French accent, might have followed along these lines: “We want to buy your port.” “It’s not for sale.” “Oh, what a pity, an accident just happened.”

Already a month ago the IMF was “warning” that “implosion” in Lebanon was “accelerating.” Prime Minister Diab had to accept the proverbial “offer you can’t refuse” and thus “unlock billions of dollars in donor funds.” Or else. The non-stop run on the Lebanese currency, for over a year now, was just a – relatively polite – warning.

This is happening amid a massive global asset grab characterized in the larger context by American GDP down by almost 40%, arrays of bankruptcies, a handful of billionaires amassing unbelievable profits and too-big-to-fail megabanks duly bailed out with a tsunami of free money.

Dag Detter, a Swedish financier, and Nasser Saidi, a former Lebanese minister and central bank vice governor, suggest that the nation’s assets be placed in a national wealth fund. Juicy assets include Electricité du Liban (EDL), water utilities, airports, the MEA airline , telecom company OGERO, the Casino du Liban.

EDL, for instance, is responsible for 30% of Beirut’s budget deficit.

That’s not nearly enough for the IMF and Western mega banks. They want to gobble up the whole thing, plus a lot of real estate.

“The economic value of public real estate can be worth at least as much as GDP and often several times the value of the operational part of any portfolio,” say Detter and Saidi.

Who’s feeling the shockwaves?

Once again, Israel is the proverbial elephant in a room now widely depicted by Western corporate media as “Lebanon’s Chernobyl.”

Israel did admit that Hangar 12 was not a Hezbollah weapons storage unit. Yet, crucially, on the same day of the Beirut blast, and following a series of suspicious explosions in Iran and high tension in the Syria-Israeli border, Prime Minister Netanyahu tweeted , in the present tense:

“We hit a cell and now we hit the dispatchers. We will do what is necessary in order to defend ourselves. I suggest to all of them, including Hezbollah, to consider this.”

That ties in with the intent, openly proclaimed late last week, to bomb Lebanese infrastructure if Hezbollah harms Israeli Defense Forces soldiers or Israeli civilians.

A headline – “Beirut Blast Shockwaves Will Be Felt by Hezbollah for a Long Time” – confirms that the only thing that matters for Tel Aviv is to profit from the tragedy to demonize Hezbollah, and by association, Iran. That ties in with the US Congress “Countering Hezbollah in Lebanon’s Military Act of 2019” {S.1886}, which all but orders Beirut to expel Hezbollah from Lebanon.

And yet Israel has been strangely subdued.

Muddying the waters even more, Saudi intel – which has access to Mossad, and demonizes Hezbollah way more than Israel – steps in. All the intel ops I talked to refuse to go on the record, considering the extreme sensitivity of the subject.

Still, it must be stressed that a Saudi intel source whose stock in trade is frequent information exchanges with the Mossad, asserts that the original target was Hezbollah missiles stored in Beirut’s port. His story is that Prime Minister Netanyahu was about to take credit for the strike – following up on his tweet. But then the Mossad realized the op had turned horribly wrong and metastasized into a major catastrophe.

The problem starts with the fact this was not a Hezbollah weapons depot – as even Israel admitted. When weapons depots are blown up, there’s a primary explosion followed by several smaller explosions, something that could last for days. That’s not what happened in Beirut. The initial explosion was followed by a massive second blast – almost certainly a major chemical explosion – and then there was silence.

Thierry Meyssan, very close to Syrian intel, advances the possibility that the “attack” was carried out with an unknown weapon, a missile -– and not a nuclear bomb – tested in Syria in January 2020. (The test is shown in an attached video.) Neither Syria nor Iran ever made a reference to this unknown weapon, and I got no confirmation about its existence.

Assuming Beirut port was hit by an “unknown weapon,” President Trump may have told the truth: It was an “attack”. And that would explain why Netanyahu, contemplating the devastation in Beirut, decided that Israel would need to maintain a very low profile.

Watch that camel in motion

The Beirut explosion at first sight might be seen as a deadly blow against the Belt and Road Initiative, considering that China regards the connectivity between Iran, Iraq, Syria and Lebanon as the cornerstone of the Southwest Asia Belt and Road corridor.

Yet that may backfire – badly. China and Iran are already positioning themselves as the go-to investors post-blast, in sharp contrast with the IMF hit men, and as advised by Hezbollah Secretary-General Nasrallah only a few weeks ago.

Syria and Iran are in the forefront of providing aid to Lebanon. Tehran is sending an emergency hospital, food packages, medicine and medical equipment. Syria opened its borders with Lebanon, dispatched medical teams and is receiving patients from Beirut’s hospitals.

It’s always important to keep in mind that the “attack” (Trump) on Beirut’s port destroyed Lebanon’s main grain silo, apart from engineering the total destruction of the port – the nation’s key trade lifeline.

That would fit into a strategy of starving Lebanon. On the same day Lebanon became to a great extent dependent on Syria for food – as it now carries only a month’s supply of wheat – the US attacked silos in Syria.

Syria is a huge exporter of organic wheat. And that’s why the US routinely targets Syrian silos and burns its crops – attempting also to starve Syria and force Damascus, already under harsh sanctions, to spend badly needed funds to buy food

In stark contrast to the interests of the US/France/Saudi axis, Plan A for Lebanon would be to progressively drop out of the US-France stranglehold and head straight into Belt and Road as well as the Shanghai Cooperation Organization. Go East, the Eurasian way. The port and even a great deal of the devastated city, in the medium term, can be quickly and professionally rebuilt by Chinese investment. The Chinese are specialists in port construction and management.

This avowedly optimistic scenario would imply a purge of the hyper-wealthy, corrupt weapons/drugs/real estate scoundrels of Lebanon’s plutocracy – which in any case scurry away to their tony Paris apartments at the first sign of trouble.

Couple that with Hezbollah’s very successful social welfare system – which I saw for myself at work last year – having a shot at winning the confidence of the impoverished middle classes and thus becoming the core of the reconstruction.

It will be a Sisyphean struggle. But compare this situation with the Empire of Chaos – which needs chaos everywhere, especially across Eurasia, to cover for the coming, Mad Max chaos inside the US.

General Wesley Clark’s notorious 7 countries in 5 years once again come to mind – and Lebanon remains one of those 7 countries. The Lebanese lira may have collapsed; most Lebanese may be completely broke; and now Beirut is semi-devastated. That may be the straw breaking the camel’s back – releasing the camel to the freedom of finally retracing its steps back to Asia along the New Silk Roads.

via ZeroHedge News https://ift.tt/3imGU3G Tyler Durden

“Somebody Needs To Go To Jail”: Graham Erupts After Document Reveals FBI Lied To Congress Tyler Durden

Sun, 08/09/2020 – 22:15

Senate Judiciary Committee Chairman Lindsey Graham (R-SC) was furious during a Sunday appearance with Fox News’ “Sunday Futures with Maria Bartiromo,” after his committee released a document revealing that the FBI misled the Intelligence Committee during the Russia probe when it claimed that Christopher Steele’s salacious dossier was backed up by one of its primary sources.

“Somebody needs to go to jail for this,” Graham told Bartiromo, adding “This is a second lie. This is a second crime. They lied to the FISA court. They got rebuked, the FBI did, in 2019 by the FISA court, putting in doubt all FISA applications.”

“A year before, they’re lying to the Senate Intel Committee. It’s just amazing the compounding of the lies,” he added.

The document in question contains the draft talking points the FBI used to brief the Senate Intelligence Committee in February 2018, including an assessment that the primary sub-source of the information contained in the Steele dossier had backed up the former MI-6 agent’s reporting.

The primary sub-source “did not cite any significant concerns with the way his reporting was characterized in the dossier to the extent he could identify it,” the FBI memo claimed. “…At minimum, our discussions with [the Primary Sub-source] confirm that the dossier was not fabricated by Steele.”

What’s more, FBI agents were told by Steele’s primary sub-source that much of the content attributed to him in the dossier was in “jest” or uncorroborated.

The agency was also warned by the CIA that the memos contained Kremlin disinformation – and had even assembled a spreadsheet which debunked, or could not corroborate most of the claims.

And according to Graham, the document is so misleading that he wants FBI Director Christopher Wray to identify those involved in the congressional briefing.

There is widespread evidence released by the Judiciary Committee and the DOJ inspector general contradicting the February 2018 FBI briefing memo including that the primary sub-source:

told the FBI that he “has no idea” where some of the language attributed to him came from or that his contacts and “never mentioned” some information attributed to him.

told the FBI he “did not know the origins” or “did not recall” other information contained in the dossier that was supposedly from his contacts

alleged that Steele used “incorrect source characterization” for one of his contacts. told the FBI that the corroboration for the dossier was “zero” and that he takes what the sources for the dossier told him with “a grain of salt.”

claimed much of what he told Steele was second-hand or even in jest and never intended it to be treated as intelligence because if was “word of mouth and hearsay” and “conversation that [he] had with friends over beers.”

via ZeroHedge News https://ift.tt/3iqRVkE Tyler Durden

{kind=link}

{kind=link}