The Consumer Financial Protection Bureau (CFPB) under the Trump administration, has published a Notice of Proposed Rulemaking (NPRM) to amend the Fair Debt Collection Practices Act (FDCPA). The CFPB’s proposal would change Regulation F to direct Federal rules overseeing the activities of debt collectors. The CFPB’s new proposal would allow debt collectors to call consumers as frequently as seven times per week and be permitted to start sending emails and texts.

When debt collectors call consumers, the Federal Trade Commission (FTC) enforces FDCPA, which established rules for debt collection in 1977. Now the Trump administration wants to bring FDCPA into the 21st century, by allowing debt collectors to spam deadbeat consumers with email and text, and on a more frequent basis.

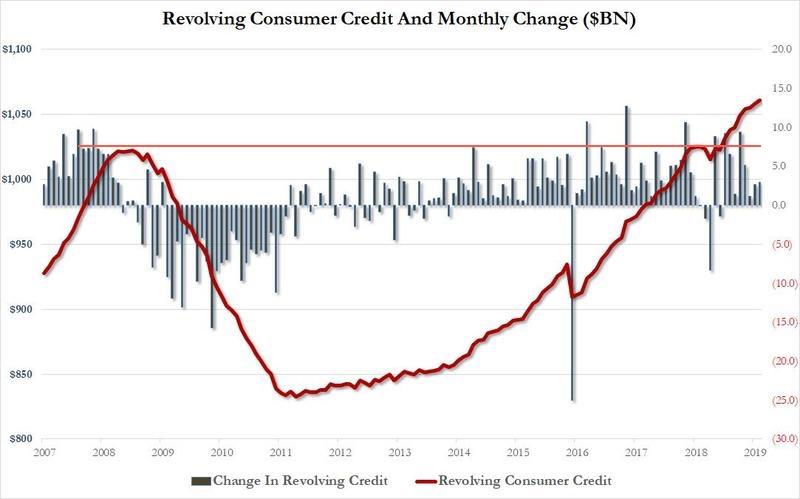

Revolving credit (credit cards) surpasses 2008 high

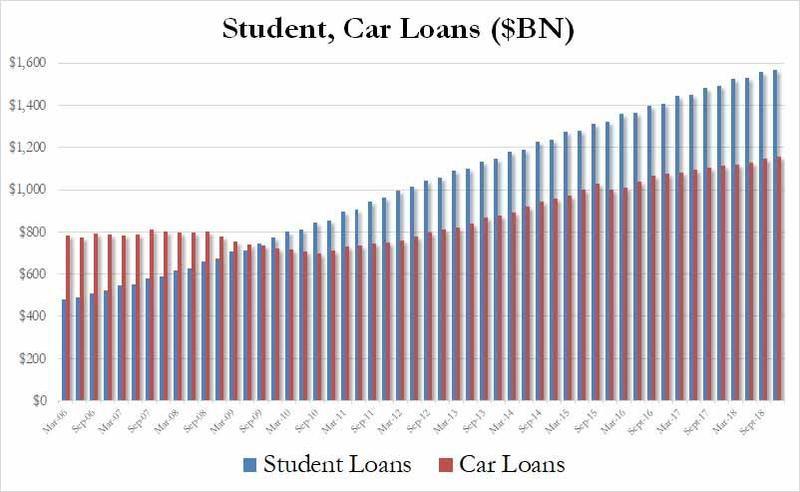

Student loans and auto loans more than double from prior cycle lows

Under the new proposal, consumers can opt out of receiving collection notices through email and text, the CFPB said in a Tuesday statement, adding that debt collectors would be expected to send disclosures with information for consumers on how to respond.

“The CFPB is taking the next step in the rulemaking process to ensure we have clear rules of the road where consumers know their rights and debt collectors know their limitations,” said CFPB Director Kathleen L. Kraninger. “As the CFPB moves to modernize the legal regime for debt collection, we are keenly interested in hearing all views so that we can develop a final rule that takes into account the feedback received.”

Once a debt collector makes contact with the consumer, the collector would have to wait seven days before contacting again. The statement said the proposal would “establish a clear, bright-line rule limiting call attempts and telephone conversations.”

The new proposal comes as the Trump administration is attempting to dismantle the federal government’s top consumer watchdog that proactively supervises banks, credit card companies, and other lenders – making sure they’re not committing fraud or abusing consumers

.

These major changes at the CFPB have led to cases filed against financial companies to plummet in the last year, as the CFPB has rolled back regulations that would generally protect consumers.

Kraninger said she has laid out a business-friendly vision for the CFPB, including more programs on educating consumers about their financial well-being.

The latest CFPB Debt Collection Consumer Survey shows 140 million debt collection notices were sent out last year, based on an estimated 49 million consumers contacted by debt collectors. This comes out to about 15% of the total American population is in collections, which in the coming quarters, these deadbeat consumers could be bombarded with calls, emails, and texts from collectors in the “greatest economy ever.”

via ZeroHedge News http://bit.ly/2Vf9XKy Tyler Durden

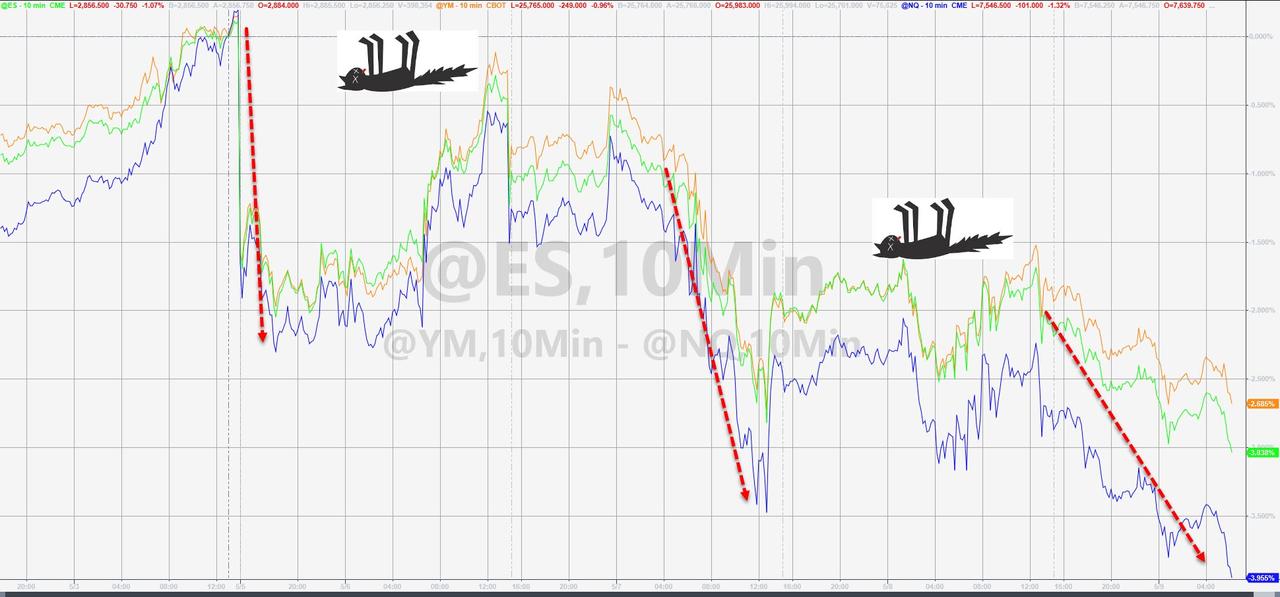

For months on end, world stocks rallied each and every day on the constant and familiar drumbeat, not to mention flashing red headlines, of “optimistic” trade news, favorable “leaks” by officials and predictions by the media citing “sources familiar” that a trade deal with China was imminent… Instead, as we reminded readers periodically, it was all a lie and absent a last minute miracle, Trump is set to hike tariffs on Chinese imports from 10% to 25% in roughly 12 hours.

And as Wall Street, which until this weekend was naively convinced that the trade war with China is now a thing of the past (only yesterday did Goldman make a Friday tariff hike its base case), faces the stark reality that it was embarrassingly unprepared for what happens next, Wall Street analysts – who by and large failed to predict the events of this week – are now confident that what has until now been a painful if orderly retreat in U.S. stocks, will mutate into something worse and much more painful if and when all-out “nuclear” trade war erupt between the U.S. and China, threatening the entire 2019 recovery, according to a Bloomberg compilation of sellside predictions, which note that “as Thursday’s ugly open in equities shows, Wall Street is coming to terms with the prospect of higher tariffs being imposed after midnight. Equities that rallied as much as 17.5% this year are down four straight days and headed for the worst week of 2019. Damage estimates are swirling.”

As Bloomberg adds, “all bets are” off as a Chinese delegation arrives in Washington on the heels of President Donald Trump’s fiery rhetoric, just hours before Friday’s deadline on fresh tariffs looming. As a result many money managers are dusting off their safety playbook in earnest, with echoes of tumult in 2018. “We tactically added to Treasuries on the back of trade wobbles,” said TwentyFour Asset Management CEO Mark Holman. He’s “holding off credit” and sticking to less volatile, short-term debt.

So just how is Wall Street preparing for what comes next?

As a new, and much more painful phase, of intercontinental trade war set to break out, Wall Street analysts are building up hedges in everything from Treasuries to deep out of the money options, while advising clients to get out of carmakers, and resist credit and emerging markets ahead of what many expect to be a rout , which has already wiped out some $2 trillion in market cap from global stocks, while halting the bubbling melt-up across risk assets along the way (so much for Larry Fink’s predictions).

As compiled by Bloomberg, here are some other ways in which Wall Street’s analysts are preparing for what comes next.

Derivatives

One strategy is that that a worst case scenario would generally spare U.S. small caps (even though the Russell just entered a correction) while Chinese stocks tumble more, and there’s a trade to front-run just that. According to Wall Fargo’s Pravit Chintawongvanich, one should buy puts on the China Large-Cap ETF, FXI, while selling them on the Russell 2000 ETF, the IWM.

Selling protective puts on IWM while buying them on FXI can help investors weather brewing tensions in global commerce, according to the strategist.

ETFs

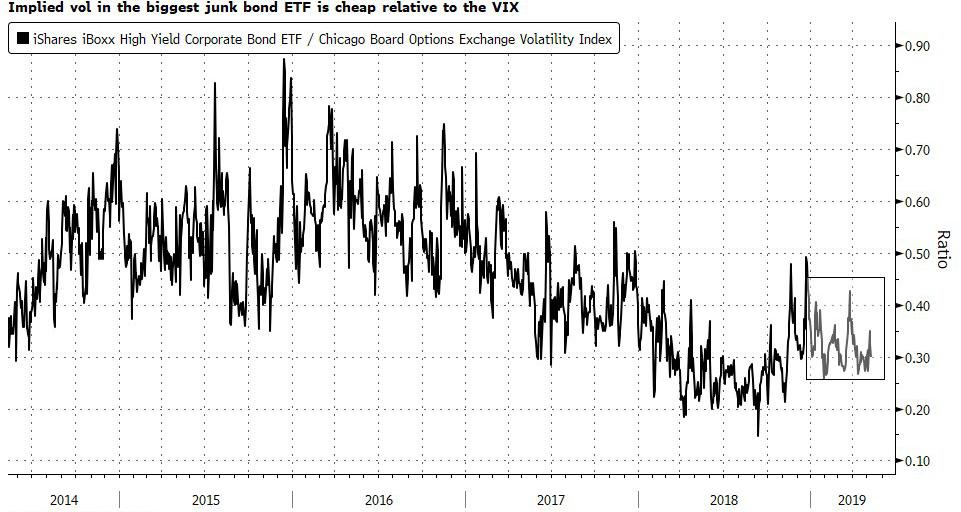

Others focus on cross-asset arbs, and note that the first asset which will likely get hammered is anything with a high beta which tracked stocks higher, namely junkbonds, which would be first on the firing line “should the latest jawboning over commerce assume a more insidious posture.” Yet consider that the implied vol tracking the biggest junk-bond ETF, HYG, which is decidedly lower compared to the VIX, also making it a cheap hedge. As a result, Macro Risk Advisors recommends buying put options on BlackRock’s benchmark product, with the investing strategy reaping fruit if the price of the ETF dips or price swings break out.

Safe Havens

Others are keeping it far simpler, and instead of dealing in derivatives or ETFs – both of which expose you to counteparty risk, something which should not be ignored should trade war go nuclear – are simply buying historical safe havens, such as Treasurys. Indeed, longer-dated bonds have traditionally made the most money during dashes to safety like the current one. Furthermore, in recent months bonds have tended to rally a lot more when risk appetite nose-dives, and they have a canny propensity to stay relatively firm when equities advance.

“For now, our worst-case scenario is a modest correction in global risk assets rather than a full-fledged meltdown,” according to Gaurav Saroliya, head of macro strategy at Oxford Economics. “Even so, the case for maintaining portfolio hedges remains.” TwentyFour asset’s Holman agrees: “We initially thought UST had the chance to creep higher in yield so we sold some 10-year notes,” he said. “But after the U.S.-China talks wobble we bought them back.”

Geographic Safety

An even simpler strategy is to focus on those regions which are relative immune to a global trade war. According to SocGen, while it is still too early to go all-in on America First trades, that may soon change: “The protection for now is back to the U.S.,” said Alain Bokobza, head of global asset allocation at Societe Generale in an interview with Bloomberg TV Wednesday. “These are periods where you go back into U.S., you go back into the dollar, you go back into U.S. equities, which are outperforming the rest. They are falling, but in a lower manner than what happens in China or Japan.”

Crashing Cars

With Europe once again dead center in the firing line if trade war escalates, carmakers in the region, a favorite Trump target, look especially vulnerable. The Stoxx 600 Automobiles & Parts Index has outperformed the broader benchmark by around 3 percentage points this year. That may not last however, according to Citigroup, which suggests buying a put spread on Europe’s automotive sector, in which buyers simultaneously purchase protective options at a strike price of 490 euros while selling contracts with a 460 strike. The structure helps offset the cost of the bearish bet and limits losses. The trade makes sense for investors who expect the index to fall, but not too far. “With the Trump administration in a hawkish mood, we believe SXAP remains vulnerable” Citi concluded.

Submerging Markets

In a replay of mid-2018, when we say various EM indices crumble, Evercore has recommended a put on the iShares MSCI Emerging Markets ETF to hedge against event risk, especially as China now takes up more than a quarter of the index. The trade gains with limited downside risk as long as the price of the fund drops, though returns are capped. And while Evercore still thinks an agreement can be reached – curbing the allure of the investing style – it says the $34 billion ETF remains a hedge-worthy vehicle for trade bears.

Services Good, Goods Bad

Another hedge comes from Goldman, which recommends exposure to services, while shunning goods sectors. Referring to trading last year, Goldman strategist David Kostin writes that”“services-providing stocks will outperform goods-producing stocks as long as the trade dispute continues.” Among the service providers cited are Microsoft, Amazon.com and Berkshire Hathaway; while goods producers include Apple, Johnson & Johnson and Exxon Mobil.

* * *

Finally, courtesy of Bloomberg, here are several snapshots from specific analysts, who while especially bullish until recently, have suddenly turned quite bearish, starting with Ameriprise Financial’s Anthony Saglimbene, who says that the S&P 500 at 2,900 is fair based on the current state of earnings and the economy, but all that could “quickly” go away.

“If we have this global flare up in trade tensions and we actually see more tariffs put on, then I think markets could very quickly give back 5 to 10% very easily,” he said in an interview at Bloomberg’s New York headquarters. “If we get to a point in the escalation where we’re actually slapping tariffs on all Chinese imports and you have China coming back and retaliating through various measures, then I think as quickly as we’ve seen the last four months be positive, we could quickly see that go away. However, the U.S. economy is fairly isolated, it’s a closed economy. We should continue to do OK, but it’s just not a great environment. And really it comes down to profits — profit margins, sales trends, those could all be more serious.”

Beware the Profit Hit: UBS estimates that with higher tariffs and a breakdown in talks, profits for U.S. companies could contract by 5%. With analysts currently forecasting earnings growth of 4.6% for the year, that number would be wiped out. In turn, equities could fall as much as 15%, said Mark Haefele, CIO of UBS Global Wealth Management. Worse, with a 25% tariff rate instead of the current 10% level, gross margins for S&P 500 companies could shrink by 23 basis points, according to Bloomberg Intelligence. If the U.S. administration slaps the tax on all goods from China, the hit to margins could be an even larger 50 basis points.

“China-trade risks have largely been priced out of U.S. equities this year, suggesting any tariff-policy shift is likely to trouble stocks’ bullish trend, in our view,” wrote Bloomberg Intelligence’s Gina Martin Adams and Michael Casper. “Share values of the median S&P 500 companies with China exposure have rallied twice as much as the index this year. While valuations imply investor awareness of complications of selling into China — perhaps a result of slower growth in the region in the past year — trade tension should pressure stocks of companies exposed to higher input costs.”

Beware the downside if no deal is reached: Bank of America estimates that the S&P 500 should end the year around 2,900 and has the potential to rally as high as 3,000 throughout the course of the year. If a deal is reached and some of the existing tariffs are dropped, that could provide a positive catalyst, says Jill Carey Hall, a U.S. equity strategist for Bank of America Merrill Lynch. But if we don’t get a deal, volatility could move higher.

“Bottom line is this is a market where we’ve been expecting higher volatility this year given geopolitics, given the trade backdrop, given the flattening of the yield curve cutting into this year that typically precedes a higher VIX,” she said on Bloomberg Television. “There’s certainly been a healthy amount of optimism priced in around a trade deal, so if we don’t get a deal, we do expect that the market could pull back. We’ve written that we could see a 5 to 10% pullback if trade tensions do escalate into an all out war and the tariffs rise or if we see tariffs on the remaining goods and China retaliates. There’s certainly downside risk that the market may not be fully pricing in.”

Beware a 7% Pullback if support is breached: Miller Tabak + Co.’s Matt Maley is keeping his eyes glued on the technical levels. If one breaks, then the S&P 500 could be headed even lower to the next stop. The result? A minimum of a 7% pullback. As noted earlier, on Thursday morning the S&P already tumbled some 20 points below the 50-day average, although it has since stabilized.

“The odds I suppose are still good that they’ll get some sort of a deal eventually, but the problem is that the market had been pricing in that they would get one signed certainly by June, if not by this week,” he said on Bloomberg Radio. “Since we’re not going to get that, the market was a little bit priced for perfection, I think it’s got more to pull back. If we get through this week and the tariffs do get placed on, the minimum I think is down — everybody’s been talking about the 50-day moving average on the S&P, which it looks like we’ll be testing this morning — I think it could take us down to at least the 200-day moving average, which is at 2,740ish. That would be down about 7% from the highs. I think that’s the minimum we’d see.”

GDP Smash: according to JPMorgan’s chief U.S. economist, Michael Feroli, estimates a higher tariff rate of 25% could reduce 2019 GDP growth by about two-tenths of a percentage point; the real number will certainly be far worse.

“Most economists agree that the trade war is likely to have limited impact on global economic growth, but a large impact on company earnings,” said Dennis Debusschere, head of portfolio strategy at Evercore ISI. “We wouldn’t take comfort in the idea that a limited impact on economic growth would also limit the downside risk to equities.

In any case, if “tariffs are increased at 12:01 AM Friday, the decline in risk assets is likely to intensify and we would not take comfort that it would take two weeks for tariffs to have an impact. The signal of continued escalation is what’s important” the gloomy Evercore prediction concluded.

via ZeroHedge News http://bit.ly/2HaFr0M Tyler Durden

Speaking ahead of China VP Liu’s arrival, President Trump told reporters that he had received a lettere from Chinese President Xi and suggested the two may speak on the phone. Additionally, Trump claimed he has “an excellent alternative” to the China deal.

That seemed positive to the machines and so the reaction was swift algo buying…

via ZeroHedge News http://bit.ly/2YhcjKT Tyler Durden

A 31-year-old Tennessee man was arrested on Thursday over allegations that he illegally obtained and then leaked classified national defense information to a reporter, according to the Department of Justice (DOJ).

Daniel Everette Hale of Nashville worked as a NSA intelligence analyst while deployed to Afghanistan, after which he worked for the National Geospatial-Intelligence Agency (NGA) – where he worked as a political geography analyst between December 2013 and August 2014.

While assigned to the NSA during active duty for the Air Force, Hale allegedly began communicating with a reporter for an unknown news outlet – meeting with them “on multiple occasions,” while also communicating via an encrypted messaging platform.

After his shift from the NSA to the NGA, Hale is accused of printing six classified documents unrelated to his work in February 2014, which were later published by the reporter’s news outlet.

According to allegations in the indictment, while employed as a cleared defense contractor for NGA, Hale printed from his Top Secret computer 36 documents, including 23 documents unrelated to his work at NGA. Of the 23 documents unrelated to his work at NGA, Hale provided at least 17 to the reporter and/or the reporter’s online news outlet, which published the documents in whole or in part. Eleven of the published documents were classified as Top Secret or Secret and marked as such. -DOJ

According to the indictment, the reporter was listed in Hale’s cell phone contact list, and he possessed two thumb drives – one of which contained a page marked “SECRET” from a classified document that he had printed in February, 2014, and later attempted to delete from the drive.

The other thumb drive contained Tor software – commonly used to access or exchange information on the ‘dark web’ – which were recommended by the reporter’s news website in an article notifying people how to leak documents.

Hale has been charged with obtaining national defense information, retention and transmission of national defense information, causing the communication of national defense information, disclosure of classified communications intelligence information, and theft of government property, according to the DOJ.

Each charge carries a maximum penalty of 10 years in prison, however the DOJ notes that actual sentences for such crimes are typically less than the maximum.

via ZeroHedge News http://bit.ly/2JsKaMM Tyler Durden

“So, if the housing market isn’t going to affect the economy, and low interest rates are now a permanent fixture in our society, and there is NO risk in doing anything because we can financially engineer our way out it – then why are all these companies building up departments betting on what could be the biggest crash the world has ever seen?

What is more evident is what isn’t being said. Banks aren’t saying “we are gearing up just in case something bad happens.” Quite the contrary – they are gearing up for WHEN it happens.

When the turn does come, it will be unlike anything we have ever seen before. The scale of it could be considerable because of the size of some of these leveraged deals.” – Lance Roberts, June 2007

It is often said that no one saw the crash coming. Many did, but since it was “bearish” to discuss such things, the warnings were readily dismissed.

Of course, what came next was the worst financial crisis since the “Great Depression.”

But that was a decade ago, the pain is a relic of history, and the surging asset prices due to monetary policies has once again lured both Wall Street and Main Street into the warm bath of complacency.

It should not be surprising warnings are once again falling on “deaf ears.”

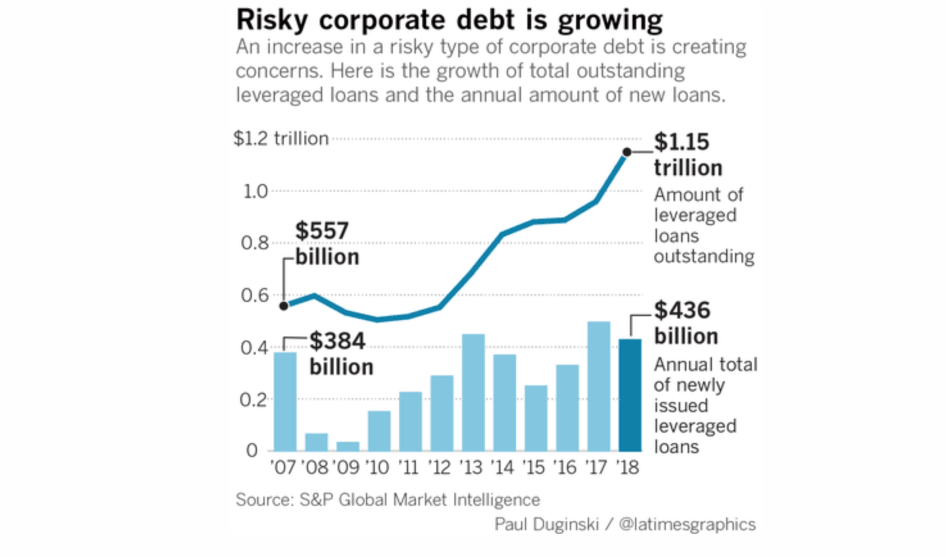

The latest warning came from the Federal Reserve who identified rising sales of risky corporate debt as a top vulnerability facing the U.S. financial system in their latest financial stability report. Via WSJ:

“Officials, for the second time in six months, cited potential risks tied to nonfinancial corporate borrowing, particularly leveraged loans—a $1.1 trillion market that the Fed said grew by 20% last year amid declining credit standards. They also flagged possible concerns in elevated asset prices and historically high debt owned by U.S. businesses.

Monday’s report also identified potential economic shocks that could test the stability of the U.S. financial system, including trade tensions, potential spillover effects to the U.S. from a messy exit of Britain from the European Union and slowing economic growth globally.

Specifically, the Fed warned a downturn could expose vulnerabilities in U.S. corporate debt markets, ‘including the rapid growth of less-regulated private credit and a weakening of underwriting standards for leveraged loans.’”

It has become quite commonplace to dismiss the current environment under the thesis of “this time is different.”This was also the case in 2007 where the general beliefs were exactly the same:

Low interest rates are expected to persist indefinitely into the future,

A pervasive belief that Central Banks have everything under control, and;

The economy is strong and there is “no recession” in sight.

Remember, even though no one knew it at the time, the recessions officially started just 5-months later.

The issue of “zombie corporations,” or companies that would be bankrupt already if not for ongoing low interest rates and loose lending standards, is not a recent issue. Via Zerohedge:

“As Bloomberg reports, in a particularly striking sign, the Fed said the businesses with the biggest existing debt loads are also the ones taking on the riskiest loans. And protections that lenders include in loan documents in case borrowers default are eroding, the U.S. central bank said in its twice-a-year financial stability report. The Fed board voted unanimously to approve the document.

‘Credit standards for new leveraged loans appear to have deteriorated further over the past six months,’ the Fed said, adding that the loans to firms with especially high debt now exceed earlier peaks in 2007 and 2014.

‘The historically high level of business debt and the recent concentration of debt growth among the riskiest firms could pose a risk to those firms and, potentially, their creditors.’

Leveraged loans are routinely packaged into collateralized loan obligations, or CLOs. Investors in those securities — including insurance companies and banks — face a risk that strains in the underlying loans will deliver ‘unexpected losses,’ the Fed said Monday, adding that the secondary market isn’t very liquid, “even in normal times.”

‘It is hard to know with certainty how today’s CLO structures and investors would fare in a prolonged period of stress,’ the Fed added.”

Yes. CLO’s are back.

And it was the Central Bank’s largesse that led to the latest bubble. As noted by WSJ:

“Financial stability has remained a central focus at the Fed because of the easy-money policies employed to nurse the economy back to health in the years following the financial crisis. Critics have warned that the Fed’s large bond-buying campaigns and years of near-zero interest rates risked new bubbles.”

One of the common misconceptions in the market currently, is that the “subprime mortgage” issue was vastly larger than what we are talking about currently.

Not by a long shot.

Combined, there is about $1.15 trillion in outstanding U.S. leveraged loans — a record that is double the level five years ago — and, as noted, these loans increasingly are being made with less protection for lenders and investors.

Just to put this into some context, the amount of sub-prime mortgages peaked slightly above $600 billion or about 50% less than the current leveraged loan market.

Of course, that didn’t end so well.

Currently, the same explosion in low-quality debt is happening in another corner of the US debt market as well.

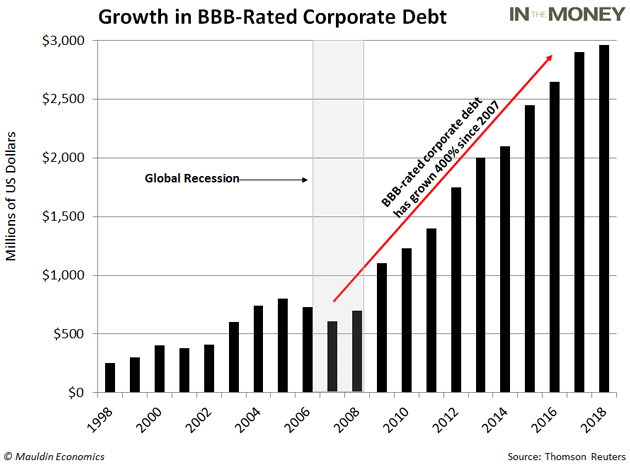

“In just the last 10 years, the triple-B bond market has exploded from $686 billion to $2.5 trillion—an all-time high.

To put that in perspective, 50% of the investment-grade bond market now sits on the lowest rung of the quality ladder.

And there’s a reason BBB-rated debt is so plentiful. Ultra-low interest rates have seduced companies to pile into the bond market and corporate debt has surged to heights not seen since the global financial crisis.”

As the Fed noted a downturn in the economy, signs of which we are already seeing, a significant correction in the stock market, or a rise in interest rates could quickly cause problems in the corporate bond market. The biggest risk currently is refinancing the debt. As Frank Holmes noted in a recent Forbes article, the outlook is rather grim.

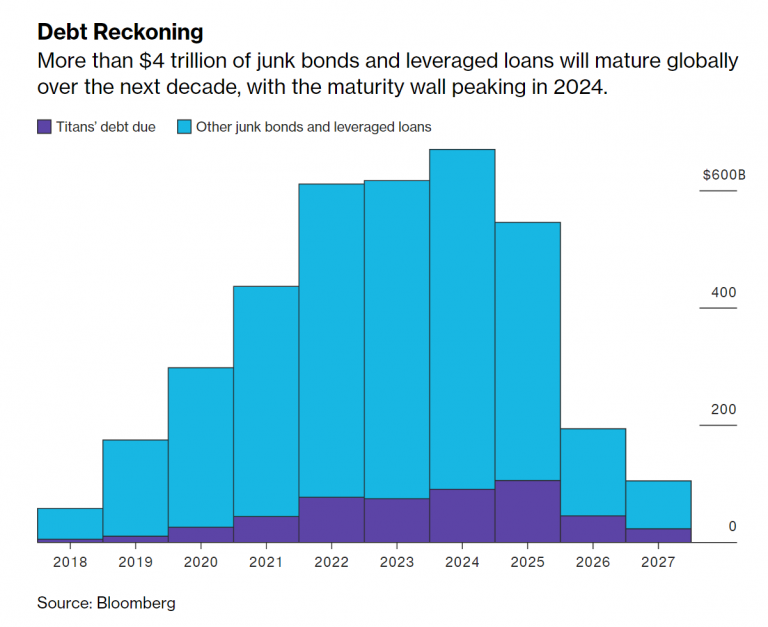

“Through 2023, as much as $4.88 trillion of this debt is scheduled to mature. And because of higher rates, many companies are increasingly having difficulty making interest payments on their debt, which is growing faster than the U.S. economy, according to the Institute of International Finance (IIF).

“On top of that, the very fastest-growing type of debt is riskier BBB-rated bonds — just one step up from ‘junk.’ This is literally the junkiest corporate bond environment we’ve ever seen. Combine this with tighter monetary policy, and it could be a recipe for trouble in the coming months.”

Let that sink in for a minute.

Over the next 5-years, more than 50% of the debt is maturing.

As noted, a weaker economy, recession risk, falling asset prices, or rising rates could well lock many corporations out of refinancing their share of this $4.88 trillion debt. Defaults will move significantly higher, and much of this debt will be downgraded to junk.

“Many companies will get into trouble if the real interest rate on ten-year treasuries rises over 1%. These businesses are so leveraged that they can’t cover their debt payments at levels even as humble and as low as a 1% real interest rate on ten-year treasuries as it translates into corporate borrowing. Just look at the growth in the herd of listed zombies; companies whose average operating income has fallen short of covering the average interest rate expense over three consecutive years. As it turns out, the corporate living dead, as a share of the broad S&P 1500 index, are close to 14%. Former Fed-Chairman Ben Bernanke once tried to reassure everyone that the Fed could raise rates in 15 minutes if it wanted to. Well, it turns out the Fed cannot do that. So, it’s a brave new world we’re living in.”

Not Just Corporate Debt

While subprime and CDO’s blew up the markets in 2008. It isn’t just corporate debt that has ballooned to problematic levels in recent years.

There is another financial risk of epic proportions brewing currently. If you are not familiar with “shadow banking,”you should learn about it quick.

Nonbank lending, an industry that played a central role in the financial crisis, has been expanding rapidly and is still posing risks should credit conditions deteriorate.

Often called ‘shadow banking’ — a term the industry does not embrace — these institutions helped fuel the crisis by providing lending to underqualified borrowers and by financing some of the exotic investment instruments that collapsed when subprime mortgages fell apart.

This kind of lending has absolutely exploded all over the globe since the last recession, and it has now become a $52 trillion dollar bubble.

In the years since the crisis, global shadow banks have seen their assets grow to $52 trillion, a 75% jump from the level in 2010, the year after the crisis ended. The asset level is through 2017, according to bond ratings agency DBRS, citing data from the Financial Stability Board.

The real crisis comes when there is a “run on pensions.” With a large number of pensioners already eligible for their pension, and a $5 trillion dollar funding gap, the next decline in the markets will likely spur the “fear” that benefits will be lost entirely.

The combined run on the system, which is grossly underfunded, at a time when asset prices are dropping, credit is collapsing, and shadow-banking freezes, the ensuing debacle will make 2008 look like mild recession.

It is unlikely Central Banks are prepared for, or have the monetary capacity, to substantially deal with the fallout.

As David Rosenberg noted:

“There is no way you ever emerge from eight years of free money without a debt bubble. If it’s not a LatAm cycle, then it’s energy the next, commercial real estate after that, a tech mania years after, and then the mother of all of them, housing over a decade ago. This time there is a huge bubble on corporate balance sheets and a price will be paid. It’s just a matter of when, not if.”

Never before in human history have we seen so much debt. Government debt, corporate debt, shadow-banking debt, and consumer debt are all at record levels. Not just in the U.S., but all over the world.

If you are thinking this is a “Goldilocks economy,” “there is no recession in sight,” “Central Banks have this under control,” and that “I am just being bearish,” you would be right.

But that is also what everyone thought in 2007.

via ZeroHedge News http://bit.ly/30c5FaL Tyler Durden

More than 168,000 illegal immigrants have been released into the US this fiscal year – a number sure to surge as the border crisis worsens, according to Nathalie R. Asher, acting chief of US Immigration and Customs Enforcement’s deportation branch.

In Wednesday comments to Congress, Asher added that according to the results of a pilot program, 87% of released immigrants fail to show up for their court hearings, resulting in judges ordering them deported in absentia, according to the Washington Times, which adds that tracking them down has been a daunting task for officials.

Nearly 110,000 were nabbed at the southwestern border in April, including nearly 100,000 caught by the Border Patrol trying to sneak into the U.S. The other 10,000 were encountered when they showed up at ports of entry demanding to be let in, despite lacking permission. –Washington Times

“Family units are not appearing in great numbers,” said Asher, who revealed the figures to Senators amid a request for more money and legal tools to try and stem the surge of illegal immigrants.

Arrests highest in 12 years

In addition to the staggering number of border crossers detained in April alone, monthly arrests have reached their highest level since 2007, according to the Washington Post.

Unauthorized border crossings have more than doubled in the past year, and they are on pace to exceed 1 million on an annual basis, as Guatemalan and Honduran families continue streaming north in record numbers with the expectation they will be quickly processed and released from custody. –Washington Post

“Our apprehension numbers are off the charts,” said Border Patrol chief Carla Provost in Wednesday comments to senators in Washington. “We cannot address this crisis by shifting more resources. It’s like holding a bucket under a faucet. It doesn’t matter how many buckets we have if we can’t turn off the flow.”

“My greatest concern is that we will no longer be able to deliver consequences and we will lose control of the border,” she added.

Sick kids stuffed in tractor-trailer rigs

According to Fox5, Mexico authorities intercepted and detained 289 Central American migrants traveling in tractor-trailer rigs, including children with measles, chickenpox and other illnesses.

Authorities had to punch a hole in one of the freight containers to free the migrants, who had been transported from the Gulf coast state of Tabasco toward the U.S. border.

…

The state said Monday the migrants were given food, water and medical attention and turned over to immigration authorities. –Fox5

Back in the US, the Trump administration has attempted to crack down in illegal immigration amid constant battles with Congress over funding President Trump’s long-promised border wall, although enough has still been allocated for hundreds of miles of barriers.

Along with physical measures such as the deployment of razor wire and thousands of US soldiers – White House officials have tightened the asylum claim process, making it more difficult for migrants to come to the US and be allowed to stay. Unfortunately, these measures haven’t worked – given the surge in apprehensions and overcrowded ICE facilities.

DHS officials for the first time this week said the agency is running out of space to jail single adult migrants, who arrived in April at the highest level in five years. One DHS official warned of a complete border breakdown if single adults who cross illegally can no longer be detained and deported.

DHS officials already have declared a “breaking point” for U.S. border agents and infrastructure, with court rulings and a crunch of detention space forcing them to release the vast majority of migrant family members and children into the interior of the United States. Border officials view single adult migrants as the one remaining demographic they can deter by “applying consequences.” –Washington Post

One DHS official told the Post: “If we were forced to release single adults, our prediction is you would see a draw or a flow that we’ve never seen before in our history.”

via ZeroHedge News http://bit.ly/2HcHdhX Tyler Durden

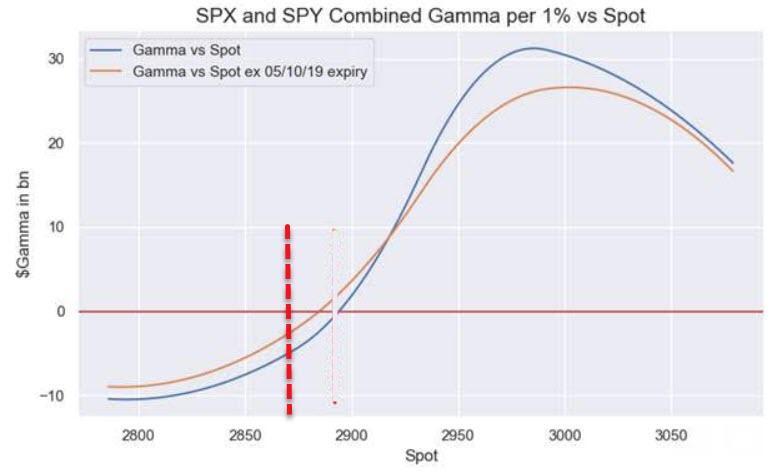

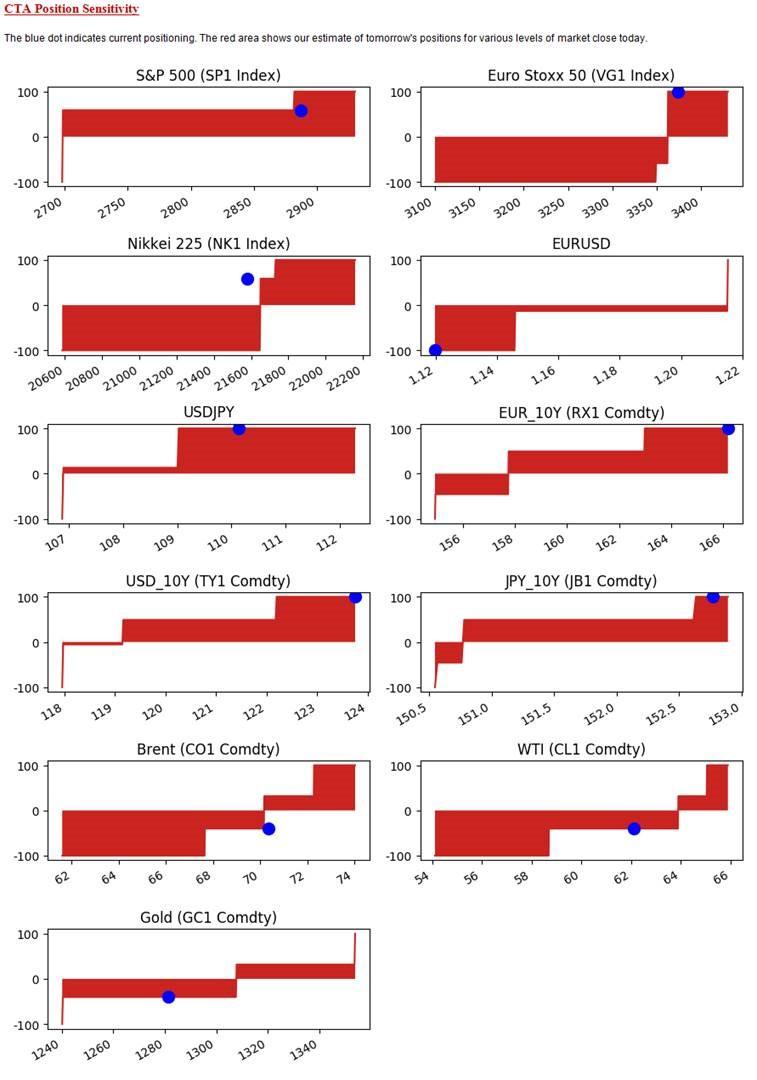

Yesterday, we summarized the violent action in volatility as follows: “If Feb 5, 2018 was the infamous inverse VIX ETF “volmageddon“, then May 7, 2019 was the “VVIXtermination” event“, following the recent explosion in the vol of vol, or VVIX, and as Nomura’s Charlie McElligott writes today, “the trade yesterday certainly was short delta, short VVIX, long front VIX.”

Then, as McElligott elaborates this morning, the “consistent dynamic” – which we first previewed over the weekend in “Is The VIX About To Explode Higher Thanks To A Record Short Squeeze ” – across the last few bouts of market turmoil have seemingly first evidenced-themselves in vol of vol—or “VVIX never lies”; As the Nomura strategist also notes, “since that initial “VVIX as ground zero” theme, we thereafter witnessed the VIX curve turmoil with systematic short vol covering, and thereafter, said issues then-showed in Delta One –type products (Risk Premia strategies, Notes etc as we begun seeing more “Yield Enhancement”- / Carry- / Momentum- strategy stop-outs on short vol positions).”

Meanwhile, as stocks slide ever deeper into “negative gamma” territory, which we first discussed late on Sunday, the lower the S&P drops the greater the risk of a sudden repricing lower in risk.

It’s not just this feedback loop of selling begetting more selling that is notable, but as the Nomura strategist also notes, CTAs are sharply losing faith in the rally and accelerating their deleveraging, most notably the Russell 2000, where trend-followers are now -100% max short, to wit:

the Russell’s notable momentum breakdown since February is showing in the trend lookback windows, as the overall model has again pivoted back outright “-100% Short”—FWIW, the model would begin covering-back on a close above 1563 (signal goes to -79%), so this price-signal remains very volatile.

Meanwhile, outside of Equities and the rising deleveraging risk, McElligott asks ‘where else is “Trend”,’ and answers:

Still “+100% Long” in Global DM Bonds / Rates, as not just “end-of-cycle slowing” and global CB “dovish pivot” are dictating, but now too just the obvious risk-aversion with the trade-war / tariff re-escalation

“+100% Long” signal in USD remains vs nearly all G10 as well as USDCNH

The Commodities view is hyper-bearish, with Shorts across 21 of 22 assets the model trades (11 of those 21 are “-100%” signals as well); the only “Long” is in Gasoline)

Summarizing this, McElligott writes that the “position sensitivity” optic is particularly powerful right now, as the highlighted Equities- and Commodities- visuals capture the proximity of recent inflection points / deleveraging; “however, the Global Bonds- and USD FX crosses- capture still how deeply “in the money” the signals are, with little current threat of deleveraging said positions.”

In short, the biggest sensitivity to marginal news is smack in the middle of equities, which judging by the continued slide in the S&P suggests that not only is the bad news nowhere near close to priced in, but depending on what happens tonight, the real pain may be yet to come.

via ZeroHedge News http://bit.ly/2HcDAHj Tyler Durden

The last thing the market needed this week was another wrench in the works of the US-China trade talks, which were already on the brink of collapse. But that’s exactly what they got when, at around 11 am ET on Thursday, the news broke that the FCC has the votes to block China Mobile from entering the US market.

Beijing won’t like that, as it now seems the Trump administration’s war against Huawei has expanded to the entire Chinese telecoms sector.

Though, to be sure, the FCC is reportedly still weighing its final decision.

FCC HAS VOTES TO BAR CHINA MOBILE FROM U.S. MARKET

FCC CONSIDERING REJECTION OF CHINA MOBILE APPLICATION

Stocks are nearing LoD on the news.

We feel this tweet adequately captures the spirit of this news.

Starting in stocks, spreading to bonds, and now leaking across other asset-classes, volatility expectations are starting to surge everywhere this week since President Trump and China’s various media outlets play headline hockey over the trade-deal-endgame.

But, as former fund manager, Richard Breslow, notes, the largest canary in the coalmine appears to be in Emerging Market assets.

via Bloomberg,

Without a doubt the best headline from yesterday came late in the day. The S&P 500 had rallied to be up “as much as” one-half percent. It pointed out that there was “Potential resistance between 2900 and 2909”. That is true and the hint at optimism was admirable. The story was published before the market gave up all of its gains into the close. Traders often talk about buying the rumor and selling the fact. The problem here is they can’t figure out what is the rumor and what is the fact.

What has been interesting about today’s price action hasn’t been the latest set-back for equities. It seems like they have garnered more than 100% of the attention. And they do indeed look like they are on the defensive. But they haven’t yet done anything that says it’s all over. We know what those levels are. And we have a pretty good sense of what will or won’t get us there in the near future.

Of more immediate concern is what is beginning to show up in other markets.

If you look at the Dollar Index, it’s fair to say it remains comatose. It just can’t get away from its big pivot level of 97.70. Uncertainty has bred uncertainty.

But currencies that will suffer should the tariff issue escalate are beginning to show signs of giving up the ghost. The Korean won has been steadily getting caned by the Japanese yen.

Granted the news from the North hasn’t been constructive. Just today, there were reports about the firing of two short-range missiles. But the cross is also an important measure of how relative levels of exposure to China are being evaluated. And the flashing warning signs turned a much deeper shade of red when the cross blew through what was supposed to be a ridiculous extreme from the yen’s January flash crash.

And between reliance on China and out-sized dependence on commodity demand, it is advisable to start watching and perhaps fretting about the Australian dollar. This double whammy is really starting to bite. Earlier this week, the RBA held rates steady. But the central bank and the market still have a dovish bias. Same issue as elsewhere. Good labor market, low inflation. Despite the RBA having issued a statement so recently, tonight’s Statement on Monetary Policy is likely to get extra attention and reaction.

The Bloomberg Commodity Index is really struggling. It is also approaching major league support. Failure down here will have reverberating repercussions. Catching a bid would also. On the positive side it has WTI, which has so far held the important $60 level. On the flip-side, it isn’t possible to look at copper and not be concerned.

What just might be the most important thing to watch, however, may be emerging markets. Being long remains a very well-subscribed trade. To say the least. Well, EM equities are having a really bad day, without much more room at all to fall before critical support.

Of more immediate import, this morning the MSCI EM currency index slipped below multiple-bottom support that has mattered all year. Those promised gains from what may have been the most popular year-ahead trade recommendations set last December are rapidly disappearing.

This could all end with sighs of relief and discussions about who bought the dip. But we are getting close to where that needs to kick in.

via ZeroHedge News http://bit.ly/2VnUAEB Tyler Durden

Starting in stocks, spreading to bonds, and now leaking across other asset-classes, volatility expectations are starting to surge everywhere this week since President Trump and China’s various media outlets play headline hockey over the trade-deal-endgame.

But, as former fund manager, Richard Breslow, notes, the largest canary in the coalmine appears to be in Emerging Market assets.

via Bloomberg,

Without a doubt the best headline from yesterday came late in the day. The S&P 500 had rallied to be up “as much as” one-half percent. It pointed out that there was “Potential resistance between 2900 and 2909”. That is true and the hint at optimism was admirable. The story was published before the market gave up all of its gains into the close. Traders often talk about buying the rumor and selling the fact. The problem here is they can’t figure out what is the rumor and what is the fact.

What has been interesting about today’s price action hasn’t been the latest set-back for equities. It seems like they have garnered more than 100% of the attention. And they do indeed look like they are on the defensive. But they haven’t yet done anything that says it’s all over. We know what those levels are. And we have a pretty good sense of what will or won’t get us there in the near future.

Of more immediate concern is what is beginning to show up in other markets.

If you look at the Dollar Index, it’s fair to say it remains comatose. It just can’t get away from its big pivot level of 97.70. Uncertainty has bred uncertainty.

But currencies that will suffer should the tariff issue escalate are beginning to show signs of giving up the ghost. The Korean won has been steadily getting caned by the Japanese yen.

Granted the news from the North hasn’t been constructive. Just today, there were reports about the firing of two short-range missiles. But the cross is also an important measure of how relative levels of exposure to China are being evaluated. And the flashing warning signs turned a much deeper shade of red when the cross blew through what was supposed to be a ridiculous extreme from the yen’s January flash crash.

And between reliance on China and out-sized dependence on commodity demand, it is advisable to start watching and perhaps fretting about the Australian dollar. This double whammy is really starting to bite. Earlier this week, the RBA held rates steady. But the central bank and the market still have a dovish bias. Same issue as elsewhere. Good labor market, low inflation. Despite the RBA having issued a statement so recently, tonight’s Statement on Monetary Policy is likely to get extra attention and reaction.

The Bloomberg Commodity Index is really struggling. It is also approaching major league support. Failure down here will have reverberating repercussions. Catching a bid would also. On the positive side it has WTI, which has so far held the important $60 level. On the flip-side, it isn’t possible to look at copper and not be concerned.

What just might be the most important thing to watch, however, may be emerging markets. Being long remains a very well-subscribed trade. To say the least. Well, EM equities are having a really bad day, without much more room at all to fall before critical support.

Of more immediate import, this morning the MSCI EM currency index slipped below multiple-bottom support that has mattered all year. Those promised gains from what may have been the most popular year-ahead trade recommendations set last December are rapidly disappearing.

This could all end with sighs of relief and discussions about who bought the dip. But we are getting close to where that needs to kick in.

via ZeroHedge News http://bit.ly/2VnUAEB Tyler Durden