Apple Demands UK Retail Landlords To Slash Rents By Half Tyler Durden

Tue, 08/04/2020 – 03:45

Apple Inc. soared 10% Friday after a blowout earnings report, adding $171 billion to its market capitalization, making it the world’s most valuable company, at $1.817 trillion (surpassing Saudi Aramco). Despite positive earnings during coronavirus lockdowns, Apple has requested UK retail store landlords to slash rent by as much as 50%.

Apple’s is up $170BN today, more than the market cap of Oracle, more than the GDP of Hungary; Apple’s value increase today would be the 33rd biggest company in the S&P500

The Sunday Times reports Apple is pushing for substantial rent reductions across 38 of its UK retail stores and asking for a “rent-free period.” In return, the iPhone maker is expected to extend leases by a couple of years, something desperate landlords might have to agree too, considering the implosion of CRE.

“Apple is seeking to bring its rents into line with other retailers, many of which are benefiting from cut-price deals as landlords struggle to keep their shopping centers occupied,” The Times said.

Apple said that, while its stores were closed, online demand for iPhones and iPads was “phenomenal” during the lockdown.

Its outlets are among the most profitable in the industry, and their popularity means that landlords are desperate to keep the Silicon Valley titan as a tenant.

The company’s proposals are understood to relate to stores with several years left to run on their leases, meaning that landlords are not yet obliged to make a decision. Apple declined to comment. – The Times

Apple is asking for rent reductions at a time when the UK has put the brakes on reopenings due to rising coronavirus infections in Europe. This means foot traffic of retail spaces are set to slump once more, will pressure brick and mortar shops, including Apple stores.

via ZeroHedge News https://ift.tt/3frZqFO Tyler Durden

The United States is showing resiliency and strength compared with other leading economies worldwide.

The impact of the Covid-19 forced shutdown crisis is lower in the United States than in Japan, Germany, France, the average of the European Union 27 and the Euro-Area countries.

The recovery is also stronger and more sustainable. This does not mean that the economic impact is small. Recession is severe and its impact on jobs and growth cannot be underestimated, but it is important to show how other economies with larger government spending plans and important entitlement programs are showing a much weaker performance.

The second quarter GDP was much better than in the euro area (-9.5% quarterly compared to -12.1% in the eurozone), although it reflects a notable quarterly drop, and well below the one seen in 2008.

This comparison is important because most mainstream economists believe that higher government spending and public sector help offset the blow of a recession. They do not. The United States quarterly GDP fall, at -9.5%, is small compared to Germany’s -10.1%, France -13.8%, Italy -12.4%, Spain -18.5% and the European Union 27 at -11.9%.

You may have read the quarterly annualized -32.9% figure for the United States, but it is misleading to compare it with the European published figures which are not annualized. Annualized rate estimates how much the economy would grow or shrink if the rate of change seen in the quarter continued at the same pace for four consecutive quarters. If we compared apples with apples, the -32.9% United States quarterly annualized GDP collapse would be from -40% in Germany to -55% in Spain.

In any case, it seems relevant to insist on three points:

1) The United States GDP decline was smaller than consensus estimates;

2) It is notably lower than the Eurozone figure, which was worse than consensus expected; and

3) The advanced U.S. data points to one of the strongest recoveries in the world.

The improvement in domestic demand that we already began to observe in the month of May has been confirmed in June. Retail sales registered an increase of +7.5% per month, the second highest number in the historical series after the May data, and this time with a less relevant “base effect”. In year-on-year terms, retail sales are already growing at +1.1% and, eliminating vehicle sales, this increase amounts to + 7.3% year-on-year. Still a lot to improve, though.

Advanced and leading indicators in the United States point to a third-quarter GDP rise of 18% to 20% in annualized terms, recovering more than half of the first half of the year decline in three months.

There is a lot to do and no one can be complacent. The U.S. economy could close the year at flat growth and 6% unemployment in the most optimistic scenario if consumption and investment progressed within potential. However, it is more likely that the economy may end down 5% and unemployment at 8.5%, all according to our estimates. This compares with a eurozone that may likely fall more than 9% in 2020 with official unemployment and furloughed jobs reaching an average of 12.5% according to Bloomberg.

There are important warning signs to consider. Consumer confidence continues weak at 73.2 basis points in July 2020, a decrease of 5 points compared to June of this year and far from levels above 100 showed during the month of February.

Leading indicators are encouraging but not optimistic. The composite purchasing managers index (PMI) for the month of July has managed to reach the economic expansion zone, at 50. The main engine continues to be the industry, at 51.3 compared to 49.8 in June, reflecting a positive evolution into expansion but with numerous challenges ahead, including investment and hiring plans. Services, a critical sector for the United States economy, remains in contraction.

The United States industrial production has shown two months with positive monthly growth (+ 5.4% in June), although low year-on-year (-10.8% in June 2020).

Employment is improving, but admittedly at a slower pace than would be desired. Jobless claims remain stubbornly above one million, and continuing jobless claims are falling at a slower pace than expected. Still, continuing jobless claims have fallen from a record 25 million to 17 million in two months. These need to fall faster, and decisive supply-side measures are needed to attract new jobs and investment.

Debt in the United States is a big challenge, but -again- metrics show a better situation than the eurozone. The accumulated deficit through June already exceeds $ 2.74 trillion, more than 10% of US GDP. Interestingly, debt to GDP in the United States is likely to rise to 98.5% according to Bloomberg consensus, but not even close to the levels of the Euro-area, at 103%, according to the ECB.

These figures contradict the calls for a stronger Euro vs the US Dollar. Despite the headline-grabbing U.S. figures, growth, debt, and employment are likely to show a better evolution than in the Euro-Area, and monetary metrics also show a stronger situation. The European Central Bank already has negative real rates and its balance sheet exceeds 53% of GDP compared to the Federal Reserve balance sheet of 33% of GDP. The US Dollar global demand is high and rising, and the world still has a US dollar shortage. That is not the case of the Euro, where demand is stable but much smaller, according to the Bank of International Settlements, and supply is rising much faster than the US dollar.

A stable and solid recovery will only be achieved with the right policies. Copying the European Union will only lead the United States to stagnation. The poor performance of the European economies in this crisis is also a reminder of why the United States should not implement similar policies.

If the United States government decides to raise taxes and increase intervention, the recovery will be slower and more painful than it is.

via ZeroHedge News https://ift.tt/3ftoXi5 Tyler Durden

Spanish Stocks Break Support As Virus Concerns Reemerge Tyler Durden

Tue, 08/04/2020 – 02:35

Spain’s IBEX 35 Index futures have slumped 11% in 9 trading sessions “as fears of new lockdowns coupled with weaker than expected macro data soured investors’ sentiment,” said Reuters‘ Stefano Rebaudo.

“There is a combination of factors,” said James McKenzie, head of research of Fidentiis in Madrid.

“Worries about possible new lockdowns as coronavirus cases keep rising, recent bad numbers for Q2 GDP and probably even worse data ahead as the UK quarantine for travelers to Spain will put under further pressure the tourism industry,” McKenzie said.

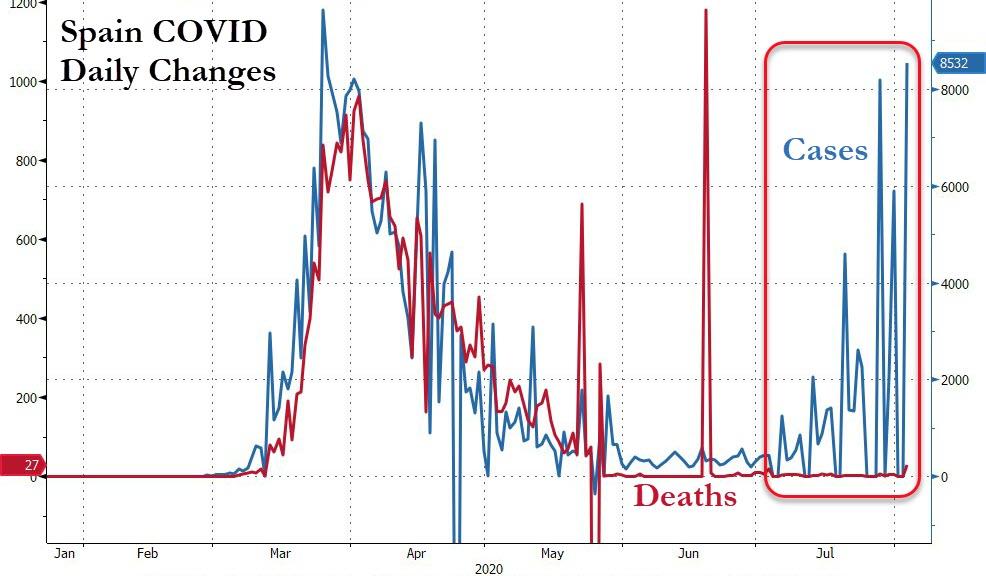

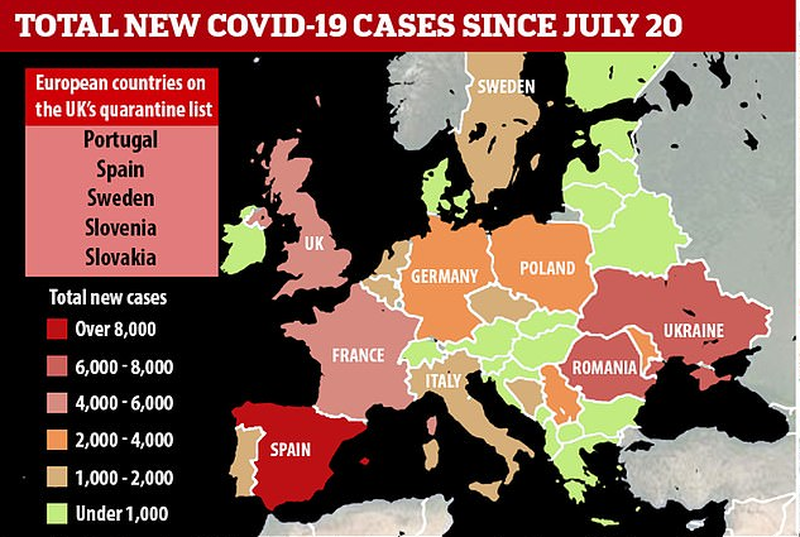

Spain reported 1,525 new COVID-19 cases on Friday, making it the most significant increase in cases since June, which was around the time national lockdown was lifted. Countries in Europe are now advising citizens against travel to Spain.

Virus cases have surged across Europe

Spain’s GDP, like Germany and France, reported last week some of the biggest crashes ever for the second quarter. The eurozone economy contracted by 12.1% in 2Q YoY.

Depressing data in the eurozone, more importantly, Spain, highlights the collapse in the travel and tourism industry, fading any hopes a quick rebound will be seen.

The selloff in Spanish stocks is an eye-opener for world stocks, currently powered by a bubble in US technology stocks.

The virus is re-emerging across the world, maybe the souring of investors’ mood in Spanish stocks is a precursor to a much broader sell-off.

via ZeroHedge News https://ift.tt/2XpcHck Tyler Durden

The continued presence of tens of thousands of American military personnel in Europe seventy-five years after the end of the Second World War is rarely questioned either by politicians or the mainstream media. Currently there is little recollection of how, after the war ended, soldiers from Britain, France, the U.S. and the Soviet Union occupied Germany, each in a designated zone. Germany’s capital Berlin was divided into four sectors, each with a foreign military occupying force. I was a part of that occupation force from 1968 through 1971, serving in the U.S. Army’s Berlin Brigade as part of the 430th Military Intelligence Detachment.

The initial intention to keep postwar Germany in check morphed into the Cold War with the Soviets. The Soviet sector of Berlin became the capital of communist East Germany while the U.S. led efforts to create a military union based in Western Europe that would resist further Russian expansion. That alliance became the North Atlantic Treaty Organization (NATO) in 1949, a structure that incorporated the newly minted Federal Republic of Germany, and the Soviets countered with the Warsaw Pact that included nearly all of Eastern Europe. Both the Organization and Pact were ostensibly defensive alliances and the U.S. active participation was intended to demonstrate American resolve to come to the aid of the Europeans. The Cold War between the two alliances continued until 1991 when the Soviet Union collapsed. Germany was reunited, the Berlin wall was torn down, the foreign troops went home and the city again became the country’s capital.

During my time in Germany the Cold War was decidedly hot, having relatively recently witnessed the Russian denial of Berlin’s occupied city status shared among the four victorious nations by building a wall and confronting U.S. forces at the new border crossing points. My recollection is that in 1970 there were more than 10,000 GIs in Berlin alone and about 200,000 more stationed in West Germany.

Today there are approximately 36,000 American soldiers and airmen based in a reunited Germany but President Donald Trump decided in early June to withdraw 9,500 of them and to also cap the total U.S. military presence in that country at 24,000, which would involve 2,500 more cuts and might go even deeper depending on what is eventually included in the numbers. Preliminary planning suggests that about 5,600 will be repositioned to other NATO countries, including Italy, Belgium and Poland, while 6,400 will be returned to the U.S., from which point they might go on to the Pacific theater to confront “Chinese ambitions.” Unlike previous Trump pronouncements on reductions in force in Afghanistan and Syria, neither of which has actually been achieved, this latest move regarding Germany appears to be serious.

As some of the soldiers that are being re-positioned elsewhere in Europe will undoubtedly be closer to the border with Russia, there should be no doubt but that the Kremlin is still the designated enemy. Whether Russia is an actual threat is questionable and many observers privately believe that NATO is an anachronism, kept going by the many statesmen and military establishments of the various countries that have a vested interest in maintaining the status quo.

In spite of the clearly diminished threat in Europe, NATO has expanded to 30 members, including most of the former communist states that made up the Warsaw Pact. The most recent acquisition was Montenegro in 2016, which contributed 2,400 soldiers to the NATO force. Since the demise of the Warsaw Pact, NATO has found work in bombing Serbia, destroying Libya and in helping in the unending task to train an Afghan army, tasks which were not envisioned when the treaty was signed in 1949.

Trump has also stated his intention to move the European Headquarters of U.S. forces from Stuttgart in Germany to Mons, near Brussels in Belgium. The move would seem to make some limited sense as NATO headquarters is also in Brussels, but there is also a political dimension to it. Trump has been sending the not unreasonable message that if the Europeans want more defense, they should pay for it themselves, though he has wrapped his proposal in his usual insulting and derogatory language. A wealthy Germany currently spends 1.1% of GDP on its military, far less than the 2% that NATO has declared to be a target to meet alliance commitments. That compares with the nearly 5% that the U.S. has been spending globally, inclusive of intelligence and national security costs.

Trump might actually have a reasonable U.S. perspective on the burden sharing issue, but the European concern is more focused on how Trump does what he does. For example, he announced the downsizing in June without informing any of America’s NATO partners. The Germans were surprised and pushed back immediately. German Foreign Minister Heiko Maas regretted the planned withdrawal, describing Berlin’s relationship with the Washington as “complicated.” Chancellor Angela Merkel was reportedly shocked. And Trump made matters worse last week when he tweeted “Germany pays Russia billions of dollars a year for Energy, and we are supposed to protect Germany from Russia” before maladroitly observing that “The United States has been taken advantage of for 25 years, both on trade and on the military. We are protecting Germany. So we’re reducing the force because they’re not paying their bill. It’s very simple: They’re delinquent. Very simple.”

The timing of the decision has also been questioned, with many observers believing that Trump deliberately staged the announcement to punish Merkel for refusing to attend a planned G-7 Summit in the U.S. that the president had been trying to arrange. Merkel argued that dealing with the consequences of the coronavirus made it difficult for her to leave home and the G-7 planning never got off the ground, which angered Trump, who wanted to demonstrate his global leadership in an election year.

Predictably, the Democrats and also some Republicans are piling on Trump over the decision.

Joe Biden sees a “profound problem” in the withdrawal while

Senator Bob Menendez of the Senate Foreign Relations Committee quipped “Champagne must be flowing freely this evening at the Kremlin.”

Republican Mitt Romney declared the move to be “grave error…a slap in the face at a friend and ally when we should instead be drawing closer in our mutual commitment to deter Russian and Chinese aggression. The move may temporarily play well in domestic politics, but its consequences will be lasting and harmful to American interests.”

The limited reduction in force actually makes no sense if one believes that NATO itself should instead be terminated due to its lacking any credible threat from Russia or from anyone else. A recent opinion poll suggests that keeping U.S. troops in Germany is not considered desirable by the Germans themselves, only 15% of whom support their remaining on national security grounds. And moving troops to Belgium and Italy is going in the wrong direction if one actually considers that there is an active threat from Moscow.

Nor does moving soldiers from one country that is behind on its 2% “dues” to NATO to other countries that are likewise in arrears make any practical sense but for a president who feels personally affronted by a foreign leader and is choosing to react petulantly as punishment. The disruption to U.S. military facilities that currently provide support to elements in Africa and the Middle East will be considerable, and the move will also not be cost-free. According to the New York Times, “Repositioning the troops will cost several billion dollars. The withdrawal and shifting of forces is likely to take months, if not years.”

And, of course, the real kicker is that if Joe Biden is elected president in a little less than three months the whole planned move will be scrapped by the victorious and persistently warlike Democrats.

No wonder Americans’ trust in the rationality of their government is at an all time low.

via ZeroHedge News https://ift.tt/2XrC4tV Tyler Durden

Parts Of France Impose Outdoor Mask Mandate In Controversial First Tyler Durden

Tue, 08/04/2020 – 01:20

The global pandemic lockdowns and social distancing regulations have produced many new controversial firsts, leading to both disputes between citizens and law enforcement, and among people often wrangling with each other over things like mask wearing or proximity, or even the ability to have gatherings at a park.

Though we thought we’d seen everything, here’s yet another true first: municipal governments in France have begun mandating the wearing of masks outdoors.

“Beach resorts along France’s Atlantic coast, picturesque promenades on the Loire River, farmers markets in the Alps — they’re among scores of spots around France where everyone is now required to wear a mask outdoors,” the Associated Press reports.

Mask at the beach? Image via Newsweek

The sure to be controversial policy in parts of the country comes as a national mask law goes into effect Monday; however, the mask law only mandates the wearing of a face covering indoors.

Currently, there are fears of a virus resurgence, with the French health authorities reporting 7,000 new cases over the course of the past week.

This second wave fear, such as the United States has been at the forefront of experiencing, is reportedly putting pressure on the government to go to the extreme of mandating the wearing of masks even outside.

Several sites around France have started requiring masks outdoors in recent days. Starting Monday, 69 towns in the Mayenne region of western France imposed outdoor mask rules, as did parts of the northern city of Lille and coastal city of Biarritz in French Basque country.

Thus far there’s been a clear scientific consensus that coronavirus is more easily spreadable indoors, while there’s less danger for it’s spread in the outside open air.

Mask while jogging? Getty Images

The idea that France could soon see a nationwide “outdoor” mask law would prove to be hugely controversial, given that it would require everyone from hikers to joggers to people just walking even in isolation to be masked up.

via ZeroHedge News https://ift.tt/2PozIrg Tyler Durden

Indian Stocks Break Critical Support As Pandemic Accelerates Tyler Durden

Tue, 08/04/2020 – 00:40

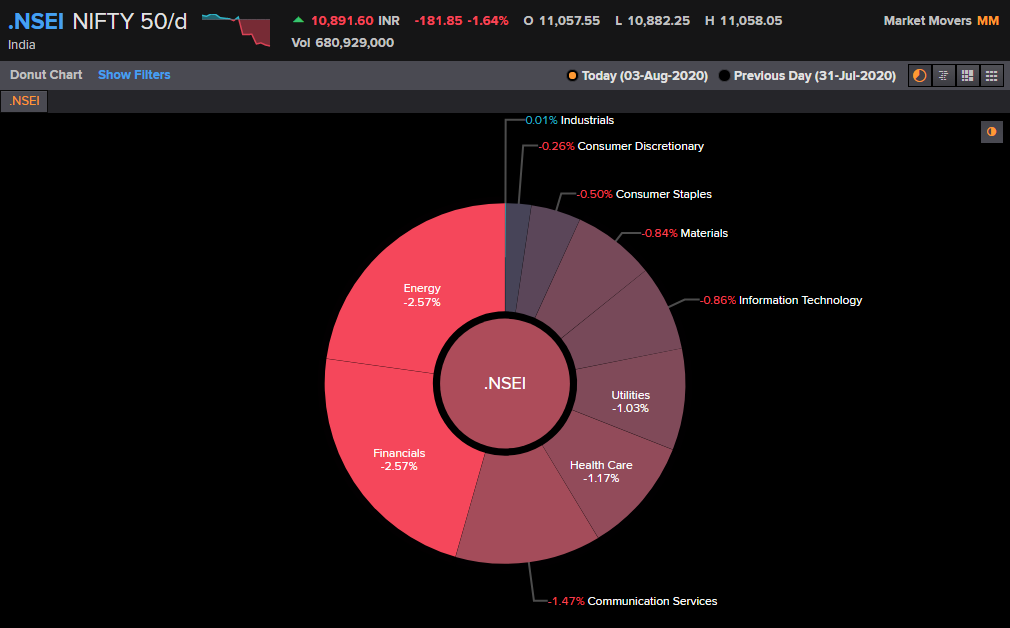

Indian shares have reversed in the last four sessions, breaking critical support, following financials, energy, healthcare, and telecommunication services pressuring the NIFTY 50 lower on Monday.

Ahead of the interest rate decision this week, investors have been souring over the prospects of rising coronavirus cases.

NIFTY 50 has fallen 4% since late last week, and this comes after a 50% increase in India’s main equity index since mid-March after it plunged 38% on the eruption of the virus pandemic.

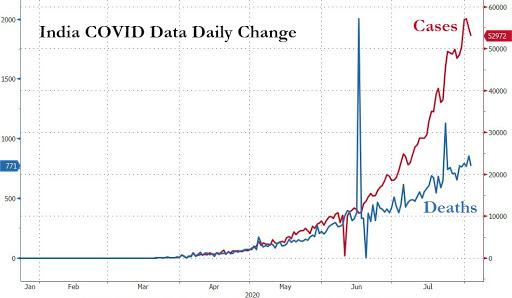

India’s interior minister said hospitalization with COVID-19 is surging as cases soared Monday above 50,000 for the fifth consecutive day.

India’s Ministry of Health and Family Welfare reported 52,972 new confirmed infections on Monday, pushing up the total to 1.8 million, just behind the US and Brazil.

With 771 new deaths, the virus pandemic has killed 38,135 people in the country, including that of a minister on Sunday.

Zee Business financial analyst Anil Singhvi warned NIFTY 50 downside could be seen if the ₹11,000-level support is violated. The index closed ₹10,891, indicating further downside is ahead.

Singhvi said investors should sell stocks if NIFTY 50 trends below ₹11,000. After the correction, he believes stocks could zoom higher.

“11000 most important level … Anil Singhvi said – do not be afraid of a few digit correction after the boom … If the market trades below 11000-10950, neutralize the position of the bull, said – for a big boom beyond 11300 Stay ready,” tweeted Zee Business (translated into English).

In my last few articles, I have found myself writing on the theme of the emerging new system and the battle between two paradigms (multipolar vs unipolar).

Within that theme, the important issue of psy ops, false solutions and epistemological warfare which is a part of everyone’s’ daily life (whether they know it or not) arose as well. Recent events and announcements have caused me to tackle another aspect of psychological warfare in the modern age.

UFOs and You

What would you do if the American and British governments both revealed that their secret UFO programs would declassify material from each nations’ respective National Archives?

What if you found out that leading politicians like former House Majority speaker Harry Reid had allocated $22 millions of tax payer dollars to UFO research and that Obama’s former chief counsellor (and rampant pedophile) John Podesta has openly called for UFO disclosure on several public occasions since 2002 or that Hillary Clinton herself called for UFO disclosure during her presidential campaign pledges of 2015?

Would you believe these claims or would you remain skeptical? How would you decide what to do?

With the July 23 public statement from the Pentagon that “off world vehicles not made on this earth” have been kept secret for decades, this question has become extremely important.

Major opinion-shapers like Joe Rogan, Tucker Carlson, and even Russia Today have promoted the cause of alien disclosure for the past few years and with the most recent Pentagon announcement, fascination in little grey men has spread like wildfire.

Who’s Playing this Game?

For the past several decades, government-sponsored UFO research has largely been driven by the work of private subcontractors like Bigelow Aerospace which was founded by billionaire real estate speculator Robert Bigelow who allocated large swaths of his fortunes to the creation of organizations like the National Institute for Discovery Science which have always worked in a private capacity with governments and academia. One of Bigelow’s biggest tools was Sen. Harry Reid who not only received generous campaign funds from the billionaire between 1998-2009 but also allocated tens of millions in national defense funds to his company starting in 2007.

In 2014, the creative force driving the “UFO-disclosure cause” has taken the form of a weird organization called To the Stars Academy of Arts and Science run by high level intelligence operatives and using a cardboard cut-out Tom Delonge (former lead singer of the punk band Blink 182). To the Stars has poured millions of dollars into cultural/educational and lobbying projects driven by books, movies, film and documentaries in the cause of “elevating global consciousness” in preparation for a new age of UFO disclosure.

“through a series of meetings I was soon connected to a large group of U.S. government officials. From the CIA, to the Department of Defense to Lockheed Martin Skunkworks. These were the guys involved in the secretive government programs that dealt with these subjects.”

Some of the shadowy figures affiliated with To the Stars include a former CIA director of operations, former Deputy Assistant secretary for Defense Intelligence, former Director of Information for White House Technology, and former chief of the CIA’s counter-biological weapons program. Both Podesta and Bigelow’s Aerospace have also worked closely with Delonge’s strange group over the past six years.

Bigelow is not the only billionaire who has allocated their vast fortunes to the cause of “UFO truth”.

The Rockefeller Project

In 1993, the Disclosure Initiative was created by none other than financier Laurence Rockefeller (4th son of Standard Oil Founder John D. Rockefeller) which had a two-fold purpose:

Unite all of the largest UFO research organizations in America under one umbrella organization which was promptly accomplished within one year and

Massively lobby the Clinton Administration to declassify millions of documents which was done in 1994, revealing little more than mountains of anecdotal testimonies and correspondences.

During the heyday of the Rockefeller UFO Disclosure Initiative, the Clintons stayed at the Laurence Rockefeller ranch in Wyoming, during which time an early recruit to the “disclosure mission” was Clinton Chief of Staff John Podesta. Podesta started going public with calls for UFO disclosure in 2002 and has continued to work with figures like Bigelow and To the Stars Academy over the next 18 years.

A fuller overview of Laurence Rockefeller’s “other” civilization-shifting programs from the 1950s-1990s can be seen here.

During the Clinton White House years, Laurence Rockefeller recruited a bodybuilding biologist named Stephen Greer to become the controller of the Disclosure Project which has provided his meal ticket to this very day. Greer has given thousands of interviews promoting the narrative that NASA’s Apollo Lunar projects were stopped in 1972 merely because the aliens who have been stationed on the Moon for eons didn’t want the truth to leak out (but were at least kind enough to let U.S. keep the technology they gave U.S. earlier in Roswell in the 1950s). If you believe in Greer’s narrative (which gets much crazier I promise), then human creative thought is actually not as special as “the shadowy forces controlling the government” wanted you to believe since space technology only existed because we stole stuff from ETs. Pretty much any inspired awe in universal creation and the power of the human mind to discover this creation with the effect of making life better through scientific and technological progress would easily be killed from this outlook.

The questions an intelligent person should now ask are:

Why would a leading figure of the Rockefeller dynasty devote the last decades of his life to the cause of “UFO truth”?

Did Laurence Rockefeller or those on his payroll or those in the CIA actually care about the right of the people to know hidden truths, or is the plan just designed to mis-direct the minds of credulous and jaded citizens into an invisible cage?

Might such a mis-direction prevent people from dealing with issues of America’s conversion into Nazism and accelerating disintegration?

Is it possible that these pedophiles, globalists, and Malthusian billionaires care less about the truth and more about inducing Americans to fixate on aliens while the republic is destroyed under economic collapse and war?

Squaring the Crop Circle

A large portion of the Disclosure Project’s work has gone into the investigation of crop circles which were first recorded in the early 1970s in Britain, and which have the peculiar characteristic of becoming increasingly well executed and complex over the course of five decades. Live Science reported that “the first real crop circles didn’t appear until the 1970s, when simple circles began appearing in the English countryside. The number and complexity of the circles increased dramatically, reaching a peak in the 1980s and 1990s when increasingly elaborate circles were produced”.

My question is: If transcendental alien races travelling at faster-than light speed, have been leaving encoded messages to U.S., then why would their artistic skills have improved so dramatically over a few years? Just a question.

MK Ultra & UFOs

Most people know of the CIA/MI6-funded mass brainwashing operation known as MK Ultra which was launched in 1953. Very few people have recognized the connection between MK Ultra and the rise of the UFO movement that grew in spades throughout the Cold War.

While U.S. and UK government UFO investigations did occur in piece meal starting in 1947 under Project Sign (1947), and Project Grudge (1949), it wasn’t until 1950 that official tax payer-funded departments were created in both nations to pursue “UFO research”. These took the form of the USA’s Project Blue Book (1952) which itself was modelled on the work conducted by Britain’s 1950 “Flying Saucer Working Party” spear-headed by Sir Henry Tizard (Chief Science Advisor to the Ministry of Defense and Chairman of Britain’s Defense Research Policy Committee).

Journalist Naomi Klein stated in her book The Shock Doctrine that Tizard played a leading role in the creation and funding of MK Ultra during a high level meeting in Montreal and Tizard’s Wikipedia entry notes that:

“One of the most controversial meetings he had to attend in his capacity as chair of the National Research Commission would only emerge many years later with the de-classification of CIA documents, namely a meeting on June 1st, 1951 at the Ritz-Carlton Hotel in Montreal Canada, between Tizard, Omond Solandt (chairman of Defence Research and Development Canada) and representatives of the CIA to discuss “brainwashing”.

This Ritz-Carleton meeting would lay the seeds for MK Ultra that was not only designed to deal with brainwashing, but created LSD, and explored the matter of breaking down a human mind into a blank slate with the explicit intention of reconstructing minds from scratch. As Klein’s book eloquently showcases, the intention was to use these discoveries on a national scale in order to conduct “shock therapy” on nations in order to break cultures and nations from their historic memories and traditions with the purpose of reconstructing them under a post-nation state (and post truth) neo liberal world order. While MK Ultra was funded by the Americans, the guidance for this operation were always driven by London’s Tavistock Clinic. A bone chilling expose of this clinic was produced by EIR’s Jeffrey Steinberg in 1993 which may keep you up at night.

As one can imagine, the very act of providing government funds to investigate flying saucers was itself sufficient to legitimize the existence of aliens in the minds of millions of Europeans and Americans during the Cold War years. During these dark years, faith in honest government collapsed under the imperial wars of Korea, Vietnam abroad and the growth of the Military Industrial Complex and McCarthyism at home. The world of secret patents, secret weapons, secret R&D that developed during this period in facilities like Area 51 made the frequent sightings by civilians and even un-vetted military pilots of “unidentified flying aircraft” an expected occurrence.

Flying Saucers and Area 51

In her 2012 book Area 51 Uncensored, journalist Annie Jacobson provided lengthy detail of the Cold War experiments, aerospace technology and nuclear bomb testing that took place at Area 51 during this period which largely fed off the earlier social engineering experiment of H.G. Wells’ War of the Worlds emergency broadcast read aloud in 1938. The mass panic that ensued the broadcast provided an insight into the levers of mass psychology that certain social engineers drooled over.

“The UFO craze began in the summer of 1947. Several months later, the G2 intelligence, which was the Army intelligence corps at the time, spent an enormous amount of time and treasure seeking out two former Third Reich aerospace designers named Walter and Reimar Horten who had allegedly created [a] flying disc.

…American intelligence agents fanned out across Europe seeking the Horton brothers to find out if, in fact, they had made this flying disc.”

During WWII, the Horten brothers were associated with the Austrian scientist Viktor Shauberger whose innovative designs for implosion (vs explosion) flying technology utilized water currents, and electromagnetism to generate flying machines that by all surviving accounts flew faster than the speed of sound. While much of his research was confiscated and classified by victor nations after WWII, Schauberger was promised government sponsorship in America which induced the inventor to move across the Ocean where Canada’s Avro Arrow program sought his designs for supersonic nuclear missile delivery aircraft. When he discovered that his work would only be used for military purposes, Schauberger pushed back and over the course of several months, his patents were essentially stolen, and he returned to Austria to die broke and depressed in 1958.

The Strategic Importance of Space

It was never a secret that the post-1971 globalized world order championed by the likes of Sir Henry Kissinger, David and Laurence Rockefeller and other Malthusians throughout the 20th century was always designed to collapse. With the mass shock therapy that such a collapse would impose upon the world, it was believed that a deconstruction of the Abrahamic traditions that governed western society for 2000 years could be accomplished and a new society could be socially engineered in the image of the Brave New (depopulated) World that would live like happy sheep forever under the grip of a hereditary alpha class and their technocratic managers.

The only problem which these social engineers have encountered in recent years is the re-emergence of actual statesmen who are unwilling to sacrifice their people and traditions on the altar of a new global Gaia cult. Such defenders of humanity’s better traditions have launched the multipolar alliance and have driven a policy of long-term growth and advance scientific and technological progress which is embodied brilliantly by the New Silk Road, and its extensions to the Arctic. The most exciting aspect of this New Silk Road/Multipolar Paradigm is the leap into space exploration as the new frontier of human self-development which has not been seen since the days of President Kennedy.

With China and Russia signing a pact to jointly develop lunar bases and the NASA Artemis Accords calling for international cooperation on Lunar and Mars resource development/industrialization, the age of unlimited growth that was lost with the LSD-driven mass psychosis of 1968’s “live in the now” paradigm shift may finally be recaptured. Programs designed to put humanity’s focus on real objective threats like Asteroid collisions, and solar-induced new ice ages are seriously being discussed by leaders of Russia, China and the USA.

There are billions of suns and potentially billions of galaxies, and chances are there is indeed life on many of the planets orbiting some of the stars within our growing, creative universe… and there is also a fair chance that cognitive life has also emerged on some of those planets. The best way to find out however is not to sit at home while the world economic system collapses under a controlled disintegration thinking about Rockefeller-funded conspiracy theories, but rather to fight to revive humanity’s open system destiny starting with a cooperative space program to extend human culture and economy to the Moon and Mars, and then onto other planetary bodies followed by missions to deep space.

If other civilizations exist, maybe it is our duty to take up the torch left to U.S. by JFK and go find them.

via ZeroHedge News https://ift.tt/2DkkDEG Tyler Durden

Shootings, Murders Spike By Record In Portland After Disbanding ‘Gun Violence Reduction Team’ Tyler Durden

Mon, 08/03/2020 – 23:45

Violent crime in US metro areas surged this summer amid the pandemic, recession, and social unrest: A perfect storm of distress that is unraveling society.

From Atlanta to Baltimore to New York City to Chicago to Houston to some major Californian metro areas, many of these democratically-controlled cities are facing an eruption in violent crime, including murders and thefts.

Readers may recall some of the cities listed above are the usual suspects when referring to metros with the most out of control crime in the US. Now Portland’s liberal utopia appears to be imploding, as murders in July jump.

Portland Police Bureau has responded to 15 homicides in July, which is a three-decade high, reported The Oregonian. The Portland Metropolitan Area has seen approximately 24 homicides this year. Besides homicides – assaults, burglaries, and vandalism are also increasing over last year’s figures.

Verified Non-Suicide Shootings In Portland

Police Chief Chuck Lovell is concerned by the increase in violent crime. He’s shifted officers from patrols to aid in ongoing homicide investigations.

“That’s very concerning. I mean, to know that that many people have been killed in such a short period of time,” Lovell said at a recent virtual press conference.

At the same time, Lovell said Portland City Hall slashed its budget, which resulted in the massive defunding wave in early July that forced a sizeable cut in its Gun Violence Reduction Team. Also, there’s been at least a month of lawless anarchists destroying property in the area. The federal government sent in personnel to squash the uprising.

Since the Gun Violence Reduction Team was disbanded on July 1, Lovell has repeatedly linked it with the struggle to police the city.

The loss “forced us into a position where we have to really look at what resources we can bring to bear, absent that structure that we had with the Gun Violence Reduction Team,” he said.

In another recent press conference about the rise in homicides, Portland Mayor Ted Wheeler admitted the city had seen “an unprecedented escalation of gun violence.”

In the first 12 days of the month, officials witnessed an over 380 percent spike in such violence, compared to the same time period in 2019.

“This is the city we live. Portlanders, our neighbors, are being hurt by this violence. They’re being killed. The violence and the loss of life are unacceptable,” Wheeler added.

Liberal cities, ones that have defunded police and allowed anarchists to run wild, are seeing a perfect storm of distress flare up as the virus-induced downturn has unleashed a social-economic bomb.

via ZeroHedge News https://ift.tt/33ppO12 Tyler Durden

As commentators focus on the hospitalisations of two Gulf monarchs, and permutate likely succession issues, they may miss the wood for the succession trees: Of course, the death of either the Emir of Kuwait (91 years old) or King Salman of Saudi Arabia (84 years old) is a serious political matter. King Salman’s particularly has the potential to upturn the region (or not).

Yet Gulf stability today rests less on who succeeds, but rather on tectonic shifts in geo-finance and politics that are just becoming visible. Time to move on from stale ruminations about who’s ‘up and coming’, and who’s ‘down and out’ in these dysfunctional families.

The stark fact is that Gulf stability rests on selling enough energy to buy-off internal discontents, and to pay for supersized surveillance and security set-ups.

For the moment, times are hard, but the States’ financial ‘cushions’ are just about holding-up (albeit only for the big three: Saudi Arabia, Abu Dhabi and Qatar). For others the situation is dire. The question is, will this present status quo persist? This is where the warnings of shifts in certain global tectonic plates becomes salient.

The Kuwaiti succession struggle is emblematic of the Gulf rift: One candidate for Emir, (the brother), stands with Saudi Arabia and its Wahhabi-led ‘war’ on Sunni Islamists (the Muslim Brotherhood). Whereas the other, (the eldest son), is actively backed by the Muslim Brotherhood, Qatar and Turkey. Thus, Kuwait sits on firmly on the Gulf abyss – a region with significant, but disempowered Shi’a minorities, and a Sunni camp divided and ‘at war’ with itself over support for the Muslim Brotherhood; or what is (politely called) ‘autocratic secular stability’.

Interesting though this is, is this really still so relevant?

The Gulf, perhaps more significantly, is held hostage to two huge financial bubbles. The real risk to these States may prove to come from these bubbles, which are the very devil to prick-down into any gentle, expelling of gas. They are sustained by mass psychology – which can pivot on a dime – and usually end catastrophically in a market ‘tantrum’, or a ‘bust’ – and with consequent risk of depression, should Central Banks ever try to lift the foot off the monetary accelerator.

The U.S. ubiquitous ‘asset bubble’ is famous. Central Bankers have been worrying about it for years. And the Fed is throwing money at it – with abandon – to keep it from popping. But as indicated earlier, such bubbles are highly vulnerable to psychology – and that may be turning, as the celebrated V-shaped, expected economic recovery recedes into the virus-induced distance. But for now, investors believe that the Fed daren’t let it implode – that the Fed has absolutely no option but go on throwing more and more money at it (at least until November elections … & then what?).

Less visible is that other vast ‘asset bubble’: The Chinese domestic property market. With its closed capital account, China has a huge sum (some $40 trillion) sloshing around in collective bank accounts. That money can’t go abroad (at least legally), so it rotates around between three asset markets: apartments, stocks, and commodities somewhat whimsically. But investing in apartments is absolutely king! 96% of urban Chinese own more than one: 75% of private wealth is represented by investments in condos – albeit with 21% standing empty in urban China, for lack of a tenant.

Long story, short, the Chinese massively chase property valuations. Indeed, as the WSJ has noted “the central problem in China is that buyers have figured out the government doesn’t appear to be willing to let the market fall. If home prices did drop significantly, it would wipe out most citizens’ primary source of wealth, and potentially trigger unrest”. Even during the pandemic – or, perhaps because of it as the Chinese piled-in – prices rose 4.9% in June, year on year. The total value of Chinese homes and developers’ inventory hit $52 trillion in 2019, according to Goldman Sachs; i.e. twice the size of the U.S. residential market, and outstripping even the entire U.S. bond market.

If it sounds just like America’s QE-inflated asset markets, that’s because it is. As things stand, both the Chinese residential and the U.S. equity bubbles are unstable. Which might fracture fist? Who knows … but bubbles are also vulnerable to pop on geo-political events (such as a U.S. naval landing on one of China’s disputed South Sea islands, to which China is promising, absolutely, a military response).

No one has any idea how Chinese officials can manage the property bubble, without destabilizing the broader economy. And even should the market stay strong, it creates headaches for policy makers, who have had to hold off on more aggressive economic stimulus this year – which some analysts say is needed, partly because of fears it will inflate housing further.

Ah … there it is: Out in plain view – the risk. The condo-trade has hijacked the entire Chinese economy, tying officials’ hands. This, at the moment when Trump’s trade war has turned into a new ideological cold war targeting the Chinese Communist Party. What if the Chinese economy, under further U.S. sanctions, slides further, or if Covid 19 resurges (as it is in Hong Kong)? Will then the housing market break, causing recession or depression? It is, after all, China and Asia that buy the bulk of Gulf energy: Demand shrinks, and price falls. The fate of the Gulf States’ economies – and stability – is tied to these mega-bubbles not popping.

Bubbles are one factor, but there are also signs of the tectonic plates drifting apart in a different way, but no less threatening.

Bankers Goldman Sachs sits at the very heart of the western financial system – and incidentally staffs much of Team Trump, as well as the Federal Reserve.

And Goldman wrote something this week that one might not expect from such a system stalwart: Its commodity strategist Jeffrey Currie, wrote that “real concerns around the longevity of the U.S. dollar as a reserve currency have started to emerge”.

What? Goldman says the dollar might lose its reserve currency status. Unthinkable? Well that would be the standard view. Dollar hegemony and sanctions have long been seen as Washington’s stranglehold on the world through which to preserve U.S. primacy. America’s ‘hidden war’, as it were. Trump clearly views the dollar as the bludgeon that can make America Great Again. Furthermore, as Trump and Mnuchin – and now Congress – have taken control of the Treasury arsenal, the roll-out of new sanctions bludgeoning has turned into a deluge.

But there has also been within certain U.S. circles, a contrarian view. Which is that the U.S. needs to ‘re-boot’ its economic model with a Tech-led, ‘supply-side’ miracle to end growth stagnation. Too much debt suffocates an economy, and populates it with zombie enterprises.

In 2014, Jared Bernstein, Obama’s former chief economist said that the U.S. Dollar must lose its reserve status, if such a re-boot were to be done. He explained why, in a New York Times op-ed:

“There are few truisms about the world economy, but for decades, one has been the role of the United States dollar as the world’s reserve currency. It’s a core principle of American economic policy. After all, who wouldn’t want their currency to be the one that foreign banks and governments want to hold in reserve?

“But new research reveals that what was once a privilege is now a burden, undermining job growth, pumping up budget and trade deficits and inflating financial bubbles. To get the American economy on track, the government needs to drop its commitment to maintaining the dollar’s reserve-currency status.”

In essence, this is the Davos Great Reset line. Christine Lagarde, in the same year, called too for a ‘reset’ (or re-boot) of monetary policy (in the face of “bubbles growing here and there) – and to deal with stagnant growth and unemployment. And this week, the U.S. Council on Foreign Relations issued a paper entitled: It is Time to Abandon Dollar Hegemony.

That, we repeat, is the globalist line. The CFR has been a progenitor of both the European and Davos projects. It is not Trump’s. He is fighting to keep America as the seat of western power, and not to accede that role to Merkel’s European project – or to China.

So why would Goldman Sachs say such a thing? Attend carefully to Goldman’s framing: It is not the Davos line.

Instead, Currie writes that the soaring disconnect between spiking gold price and a weakening dollar “is being driven by a potential shift in the U.S. Fed towards an inflationary bias, against a backdrop of rising geopolitical tensions, elevated U.S. domestic political and social uncertainty, and a growing second wave of covid-19 related infections”.

Translation:

It is about U.S. explosive debt accumulation, on account of the Coronavirus lockdown. In a world where there is already over $100 trillion in dollar-denominated debt, on which the U.S. cannot default; nor will it ever be repaid. It can therefore only be inflated away. That is to say the debt can only be managed through debasing the currency. (Debt jubilees are viewed as beyond the pale.)

That is to say, Goldman’s man says dollar debasement is firmly on the Fed agenda. And that means that “real concerns around the longevity of the U.S. dollar as a reserve currency, have started to emerge”.

It is a nuanced message: It hints that the monetary experiment, which began in 1971, is ending. Currie is telling U.S. that the U.S. is no longer able to manage an economy with this much debt – simply by printing new currency, and with its hands tied on other options. The debt situation already is unprecedented – and the pandemic is accelerating the process.

In short, things are starting to spin out of control, which is not the same as advocating a re-boot. And the debasement of money is inevitable. That’s why Currie points to the disconnect between the gold price (which usually governments like to repress), and a weakening dollar. If it is out of the Fed’s control, it is ultimately (post-November) out of Trump’s hands, too.

Should confidence in the dollar begin to evaporate, all fiat currencies will sink in tandem – as G20 Central Banks are bound by the same policies as the U.S.. China’s situation is complicated. It would in one way be harmed by dollar debasement, but in another way, a general debasement of fiat currency would offer China and Russia the crisis (i.e. the opportunity), to escape the dollar’s knee pressed onto their throats.

And for Gulf States? The slump in oil prices this year already has prompted some investors to bet against Gulf nations’ currencies, putting longstanding currency pegs with the dollar under pressure. GCC states have kept their currencies glued to the dollar since the 1970s, but low oil demand, combined with dollar weakness would exacerbate the threat to Gulf ‘pegs’, as their trade deficits blow out. Were a peg to break, it is not clear there would be any obvious floor to that currency, in present circumstances.

Against such a backdrop, the royal successions underway in Gulf States might perhaps be regarded a sideshow.

via ZeroHedge News https://ift.tt/3i5uhtL Tyler Durden

It’s Now Virtually Impossible To Get A Bank Loan As Lending Standards Soar Tyler Durden

Mon, 08/03/2020 – 23:05

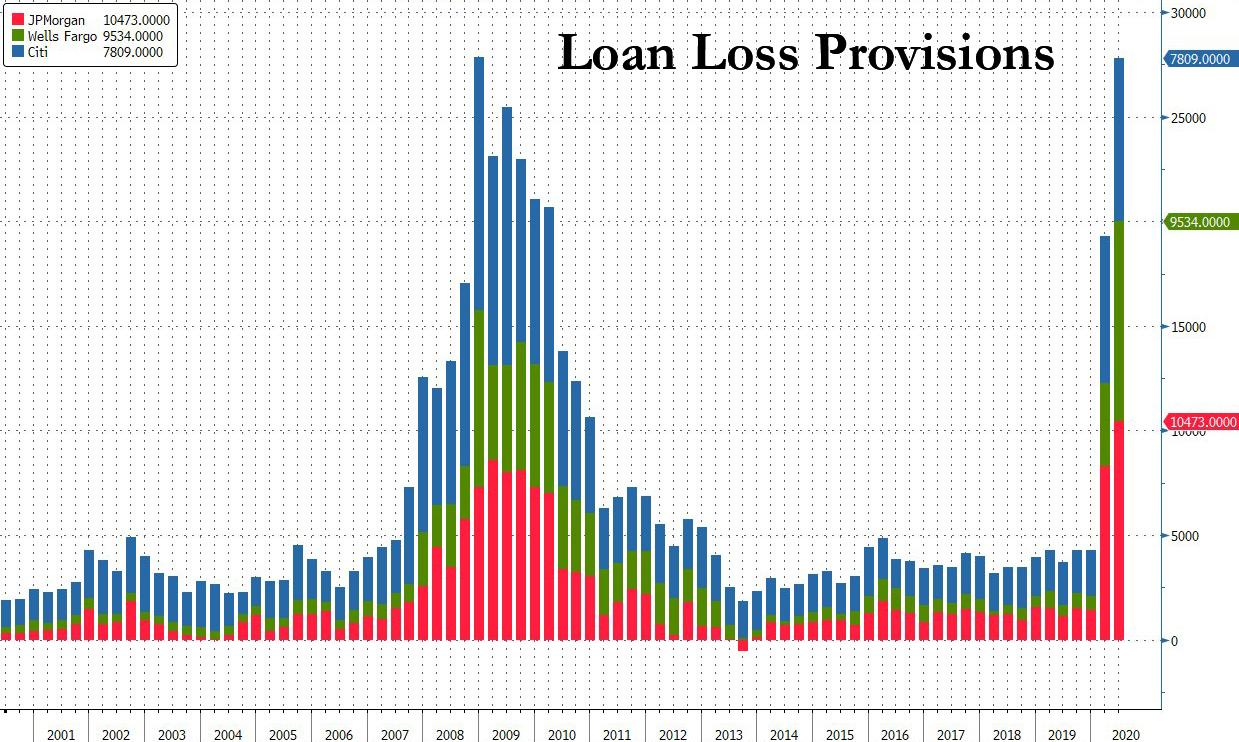

One quarter ago we pointed out something concerning: shortly after JPMorgan reported that its loan loss provision surged five fold to over $8.2 billion for the first quarter, the biggest quarterly increase since the financial crisis, in preparation for the biggest wave of commercial loan defaults since the financial crisis (a number which in the latest quarter surged to $10.5 billion along with all other banks’ loan loss provisions)…

… the bank hinted that things are about to get much worse when it first halted all non-Paycheck Protection Program based loan issuance for the foreseeable future (i.e., all non-government guaranteed loans) because as we said “the only reason why JPMorgan would “temporarily suspend” all non-government backstopped loans such as PPP, is if the bank expects a default tsunami to hit coupled with a full-blown depression that wipes out the value of any and all assets pledged to collateralize the loans.”

Shortly after, the bank also said it would raise its mortgage standards, stating that customers applying for a new mortgage will need a credit score of at least 700, and will be required to make a down payment equal to 20% of the home’s value, a dramatic tightening since the typical minimum requirement for a conventional mortgage is a 620 FICO score and as little as 5% down. Reuters echoed our gloomy take, stating that “the change highlights how banks are quickly shifting gears to respond to the darkening U.S. economic outlook and stress in the housing market, after measures to contain the virus put 16 million people out of work and plunged the country into recession.”

Finally, just days later, JPM also exited yet another loan product, when it announced that it has stopped accepting new home equity line of credit, or HELOC, applications. The bank confirmed that this change was made due to the uncertainty in the economy, and didn’t give an end date to the pause.

In short, JPM appeared to be quietly exiting the origination of all interest income generating revenue streams over fears of the coming recession, which prompted us to ask “just how bad will the US depression get over the next few months if JPMorgan has just put up a “closed indefinitely” sign on its window.“

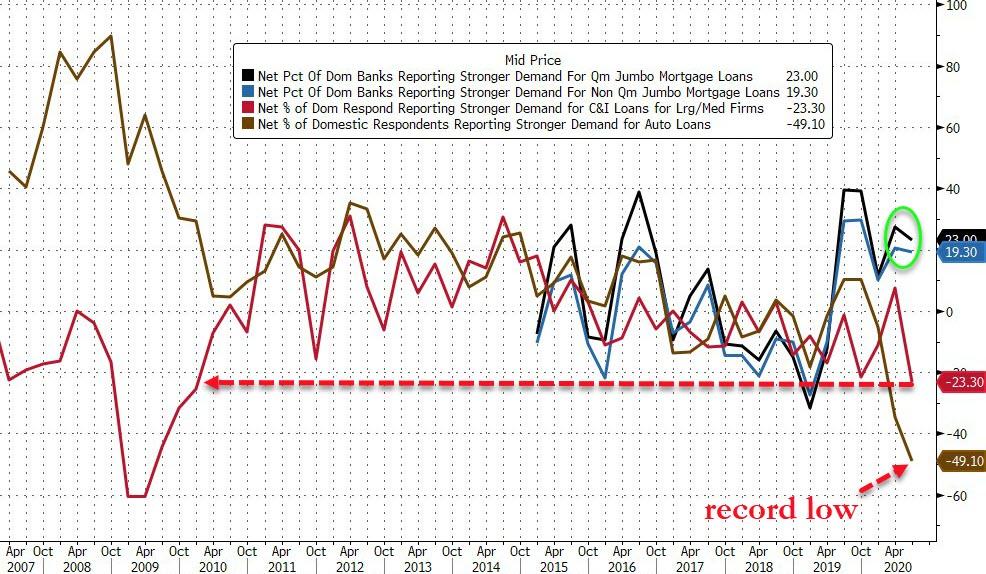

On Monday, we got confirmation that it was not just JPMorgan but all US commercial banks that are making the issuance of almost all new credit (with one notable exception) virtually impossible, when the Fed’s July senior loan officer survey showed that banks tightened lending standards across the board for C&I (commercial and industrial loans), CRE (commercial real estate), consumer (credit card and auto loans) and residential real estate (RRE) loans. The loan standards for most products – such as C&I loans, residential mortgages and credit cards – were hiked so much they nearly matched the standards during the financial crisis when it was virtually impossible to get any new loans.

This was the second quarter in a row in which loan officers reported sharply tighter financial conditions.

Just as concerning, demand for many loan products also slumped, and in the case of auto loans to record lows, with the exception of jumbo (both conforming and non-confirming) loans, which were roughly flat with demand boosted by record low interest rates.

Here are the details:

According to the July Fed’s Senior Loan Officer Opinion Survey (SLOOS), lending standards for commercial and industrial (C&I) loans tightened in the second quarter with a near record 71% of banks on net tightened lending standards for large and medium-market firms (vs. only 42% on net in the previous quarter), while 70% of banks on net tightened lending standards for small firms (vs. 40% on net in the previous quarter). 59% of banks on net increased spreads of loan rates over the cost of funds for large firms, while 54% on net increased spreads for small firms. In short, anything that is not explicitly guaranteed by the government such as PPP loans, banks won’t go near with a ten foot pole for one simple reason: they have zero visibility if and when they will get repaid.

For banks that tightened credit standards or terms for C&I loans or credit lines:

22% cited a deterioration in the bank’s capital position as playing a role,

97% cited a less favorable or more uncertain economic outlook,

85% cited a reduced tolerance for risk,

31% cited decreased liquidity in the secondary market for loans,

7% cited a deterioration in the bank’s own liquidity position,

26% cited increased concerns about the effects of legislative changes, supervisory actions, or changes in accounting standards.

More ominously for a consumer driven economy, demand for C&I loans from large- and medium-sized firms weakened after strengthening in Q1. 23% of banks on net reported weaker demand for C&I loans for large and medium-market firms, compared to 8% on net reporting stronger demand in the previous survey.

The biggest hit was for commercial real estate (CRE) loans, where standard tightened significantly in Q2. 81% (+29pp) of banks on net reported tightening credit standards for construction and land development loans, 78% (+26pp) on net reported tightening standards for loans secured by nonfarm nonresidential properties, and 64% (+15pp) on net reported tightening lending standards for loans secured by multifamily residential properties. Demand for CRE loans fell significantly across all three categories.

While demand for mortgages rose modestly, banks made it more difficult to get a mortgage by significantly tightening lending standards for mortgage loans. Lending standards for GSE-eligible (+53pp to +55%), non-jumbo, non-GSE eligible (+48pp to 59%), Qualified Mortgage jumbo (+50pp to 69%), non-Qualified Mortgage jumbo (+55pp to 70%), non-Qualified Mortgage non-jumbo (+49pp to +64%), and subprime (+29pp to t43%) mortgages all tightened. In other words, all those pleading the case that housing is exploding due to surging loan demand, are forgetting that there is also supply they need to consider, and contrary to conventional wisdom, banks have rarely been less willing to hand out mortgage loans.

Finally, banks’ willingness to make consumer installment loans declined significantly in Q2 (-41% on net vs. -20% on net previously). At the same time, credit standards for approving credit card applications tightened (+72% on net vs. +39% previously), while a modest share of banks also tightened standards for auto loans (+55% vs. +16% previously). Demand for credit card loans declined (-65% on net vs. -23% previously), as did demand for auto loans (-49% vs. -35% previously).

via ZeroHedge News https://ift.tt/33o9BsX Tyler Durden

{kind=link}

{kind=link}