A video clip posted to TikTok shows a woman holding a tape measure screeching hysterically as she appears to be upset with beachgoers for not adhering to proper social distancing.

The woman screams something unintelligible before shouting “Fuck you! Get out of here!” at other people who appear to have gathered near a lake or a beach.

The protagonist is wildly flailing around a tape measure she is holding as a man tries to restrain her.

“It’s people like you that are ruining it for all of us!” she yells.

According to respondents on Twitter who translated comments made by the woman filming the video, the screeching lady is upset at the others for being too close and not properly social distancing.

Others suggested that the woman was upset because she was trying to “measure something” and loud music was preventing her from concentrating.

Either way, the woman filming the video says that she just wanted to have a “tranquil” day with her family.

This looks like another case of a social distancing Karens gone wild.

* * *

There is a war on free speech. Without your support, my voice will be silenced. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

via ZeroHedge News https://ift.tt/2CnpvZy Tyler Durden

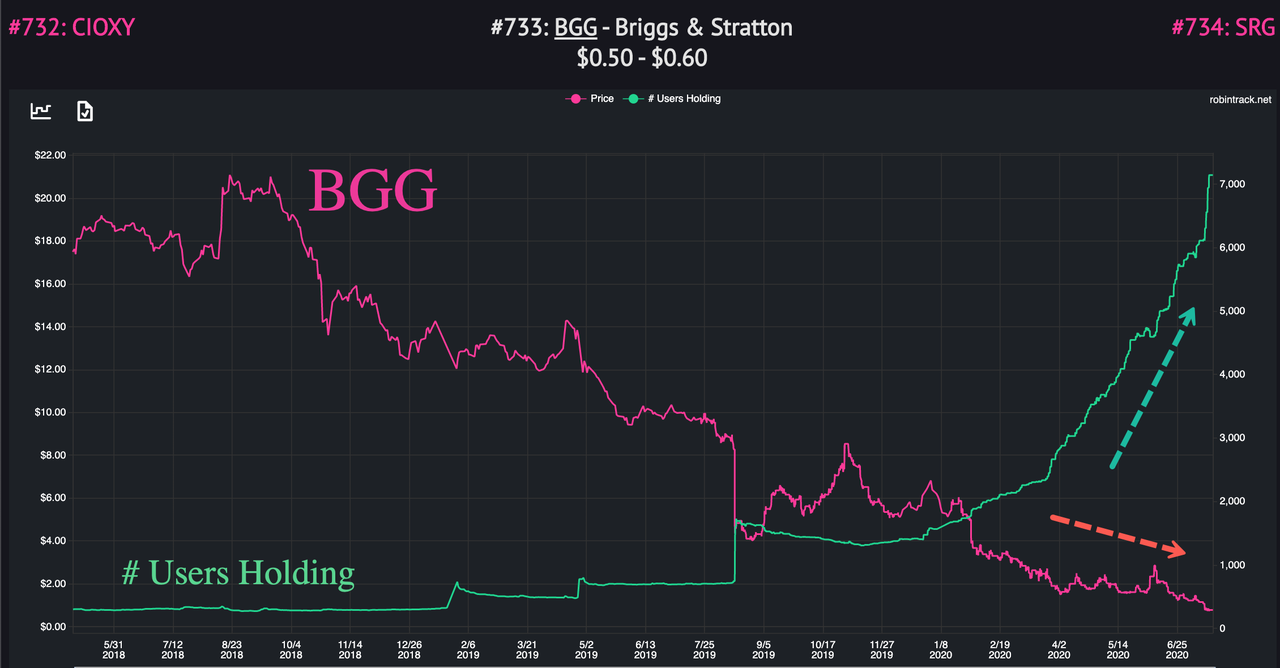

World’s Largest Producer Of Small Gasoline Engines Files For Bankruptcy Tyler Durden

Mon, 07/20/2020 – 22:30

Briggs & Stratton Corporation, the world’s largest manufacturer of small gasoline engines with headquarters in Wauwatosa, Wisconsin, filed petitions on Monday morning for a court-supervised voluntary reorganization under Chapter 11, along with plans to sell “all the company’s assets” to KPS Capital Partners.

The Fortune 1000 manufacturer of gasoline engines was able to secure a $677.5 million in Debtor-In-Possession (DIP) financing to support operations through reorganization efforts. The Company also said it “entered into a definitive stock and asset purchase agreement with KPS.”

To facilitate the sale process and address its debt obligations, the Company has filed petitions for a court-supervised voluntary reorganization under Chapter 11 of the U.S. Bankruptcy Code. The Company has also obtained $677.5 million in DIP financing, with $265 million committed by KPS and the remaining $412.5 from the Company’s existing group of ABL lenders. Following court approval, the DIP facility will ensure that the Company has sufficient liquidity to continue normal operations and to meet its financial obligations during the Chapter 11 process, including the timely payment of employee wages and health benefits, continued servicing of customer orders and shipments, and other obligations.

This process will allow the Company to ensure the viability of its business while providing sufficient liquidity to fully support operations through the closing of the transaction. Briggs & Stratton believes this process will benefit its employees, customers, channel partners, and suppliers, and best positions the Company for long-term success. This filing does not include any of Briggs & Stratton’s international subsidiaries. – Briggs & Stratton’s press release states

Todd Teske, Briggs & Stratton’s CEO, stated the Company faced “challenges” during the virus pandemic that made reorganization “necessary and appropriate” for the survivability of the Company.

“Over the past several months, we have explored multiple options with our advisors to strengthen our financial position and flexibility. The challenges we have faced during the COVID-19 pandemic have made reorganization the difficult but necessary and appropriate path forward to secure our business. It also gives us support to execute on our strategic plans to bring greater value to our customers and channel partners. Throughout this process, Briggs & Stratton products will continue to be produced, distributed, sold and fully backed by our dedicated team,” said Teske.

Briggs & Stratton is the world’s top engine designer and manufacturer for outdoor power equipment, with 85% of the small engines produced in the U.S. The pandemic and resulting virus-induced recession have been brutal for the Company, with declining engine sales, resulting in a reduction in the US workforce.

Financial Times noted, in June, the Company had difficulty refinancing a $175 million bond that matured in September. Sources told FT the Company’s deteriorating position made it impossible to obtain refinancing funds in the bond market.

Add Briggs & Stratton to the list of bankrupted companies as an avalanche of bankruptcies is expected in the second half of the year.

Not surprising whatsoever, Robinhood daytraders have panic bought collapsing Briggs & Stratton shares.

The bankruptcy wave is not over, it’s only getting started as the virus-induced recession will be more prolonged than previously thought.

via ZeroHedge News https://ift.tt/2OHkj57 Tyler Durden

Citadel Fined For Frontrunning Of Client Orders After Threatening To Sue Zerohedge Tyler Durden

Mon, 07/20/2020 – 22:17

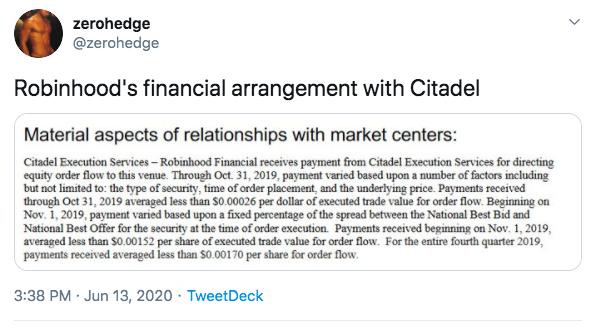

One month ago, shortly after our return to twitter from “permanent banishment”, when so much public attention had suddenly shifted to the retail daytrading platform Robinhood, we explained just how it is that Robinhood was so efficient at moving markets, and it had nothing to do with Robinhood or its small but dedicated army of 10-year-old daytrading fanatics. Instead, it had everything to do with various High Frequency Trading platforms buying up the retail orderflow that Robinhood was so generously packaging and reselling to the highest bidder, effectively giving HFTs a riskfree way of making pennies from every trade, which would then propagate like wildfire across various trading vanues, massively accentuating every small move thanks to the momentum-ignition capabilities of HFT algos.

We then also pointed out that Robinhood engages in a practice called payment-for-order-flow…

… for reasons that will become known very shortly.

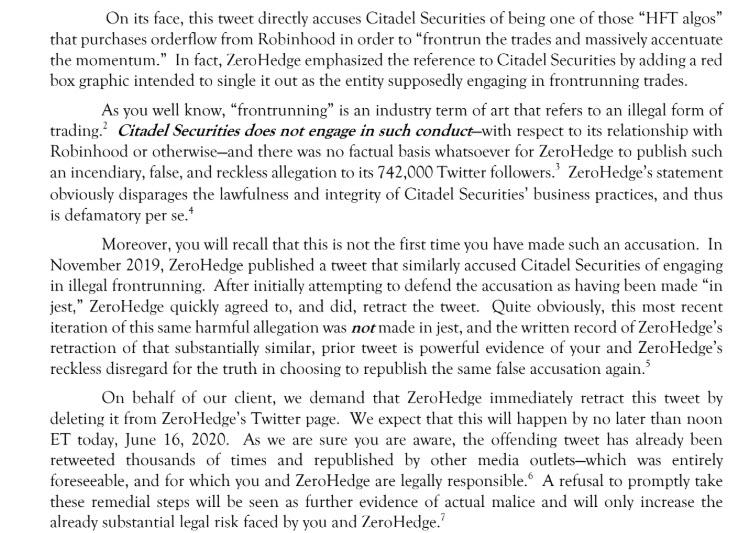

Unfortunately, both of those tweets no longer exist for the simple reason that just days after they were published, we received an angry letter from Citadel’s lawyers at Clare Locke threatening to sue us into oblivion if we did not immediately retract and delete said tweets.

Some key phrases of note from the above text:

“Citadel Securites does not engage in such conduct [i.e., frontrunning] and there was no factual basis whatsoever for ZeroHedge to publish such an incendiary, false, and reckless allegation to its 742,000 Twitter followers” [it’s 771,000 now].

“ZeroHedge’s statement obviously disparages the lawfulness and integrity of Citadel Securities’ business pratices.”

“Quite obviously, this most recent iteration of this same harmful allegation was not made in jest.”

“We demand that ZeroHedge immediately retract this tweet by deleting it from ZeroHedge’s Twitter page… A refusal to promptly take down these remedial steps will be seen as further evidence of actual malice and will only increase the already substantial legal risk faced by you and ZeroHedge.”

As the letter correctly notes, this was not the first time Citadel Securities (which is majority-owned by Ken Griffin, the billionaire investor, and is the sister firm to Citadel, the hedge fund he runs) threatened legal action against Zero Hedge for accusing the trading giant of frontrunning orders. On November 22, just hours if not minutes after a tweet of a similar nature, we got a similar legal threat from the same law firm representing Citadel Securities. Again, some of the highlights from that particular letter:

“ZeroHedge’s statement obviously disparages the lawfulness and integrity of Mr. Griffin and Citadel Securites’s business practices, and thus is defamatory per se.[sic]”

“As you well know, “frontrunning” is an unethical and illegal trading practice.”

Needless to say, instead of engaging in a legal battle with the world’s richest and most powerful trader and his army of lawyers, we decided to simply comply with their demand. That said, dear gentlemen from ClareLocke – we do know very well that frontrunning is an unethical and illegal trading practice. But we wonder: does your client know that?

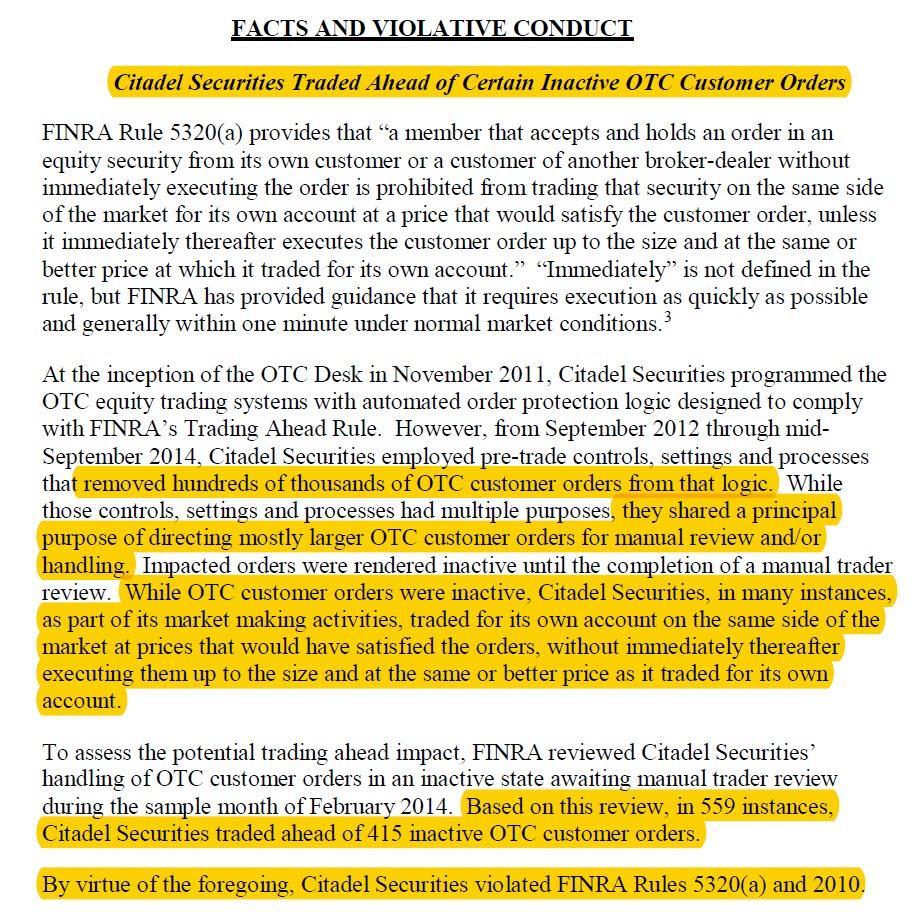

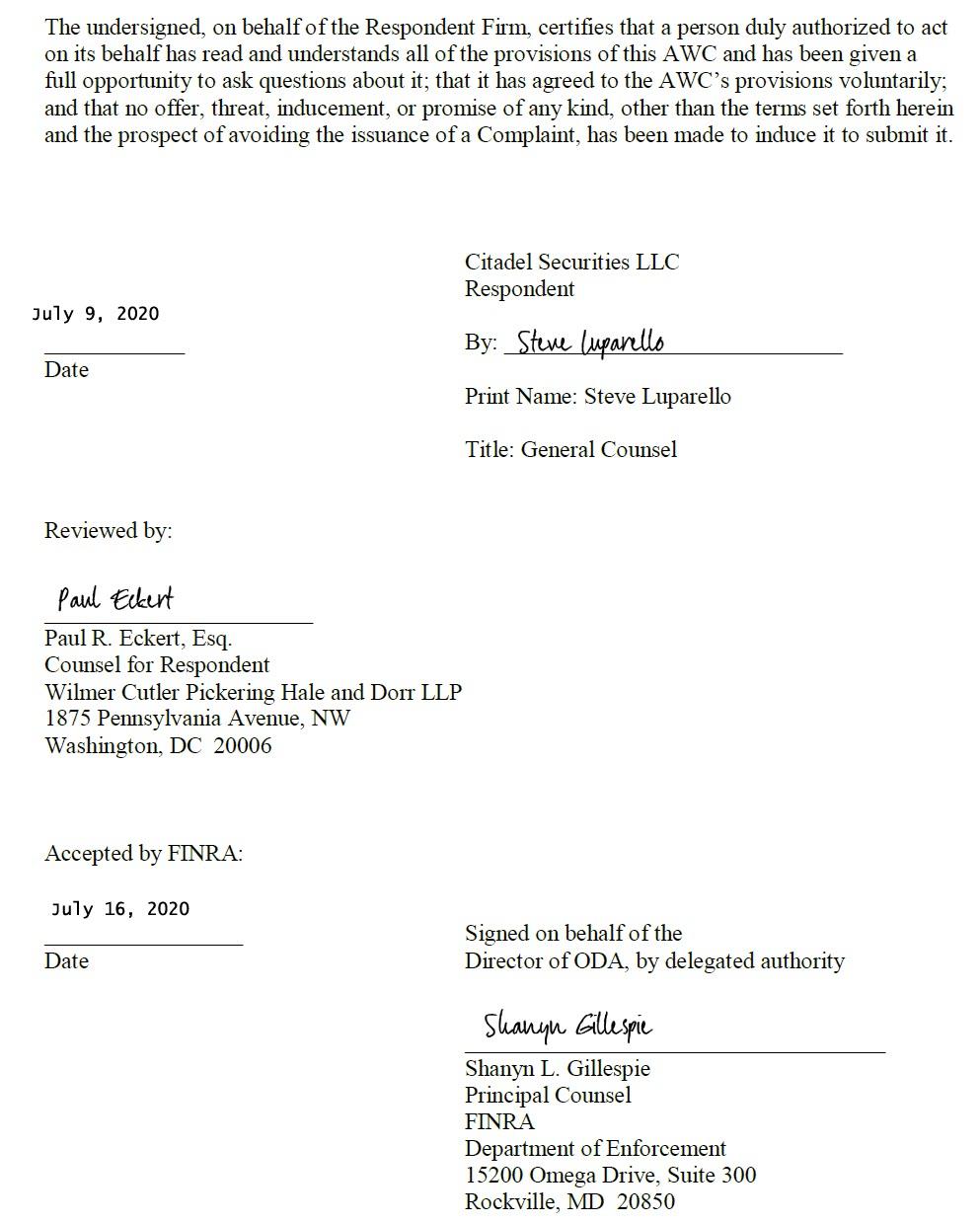

The reason why we ask is very simple. According to a Letter of Acceptance (No. 2014041859401), Waiver and Consent published by financial regulator FINRA, none other than Citadel Securities was censured and fined for engaging in – drumroll – “trading ahead of customer orders.”

Now we admit that our financial jargon is a bit rusty these days, but “trading ahead of customer orders” sounds awfully similar to another far more popular world, oh yes, frontrunning!

Jargon aside, some of the other highlighted words we are very familiar with, such as “hundreds of thousands”… and “559 instances” in which Citadel traded ahead of customer orders.

Now, we may be getting a little ahead of ourselves here, but it was Citadel’s own lawyers that informed us on more than one occasion that:

“frontrunning” is an unethical and illegal trading practice.”

So, what are we to make of this? Could it be that Citadel was engaging in at least 559 instance of what its lawyer called “unethical and illegal trading practice.” Surely not: after all the lawyers would surely know very well how ridiculous and laughable their letter and threats would look if it ever emerged that Citadel was indeed frontrunning its customers.

But then we read that Finra censured and fined Citadel $700,000 – or as twitter user @KennethDread puts it 0.70% Basquiats…

What a time to be alive when front running retail order flow only sets you back 0.70% Basquiats pic.twitter.com/LQ7sXGXtyJ

… and it appears that Citadel may indeed have engaged in some of what its own lawyers called “unethical and illegal” trading practice, especially since Citadel Securities’ own General Counsel, Steve Luparello signed the Finra AWC:

Well that’s… awkward.

And lest someone ignores all of the above – after all it was published in a fringe, tinfoil conspiracy theory website which according to glorious liberal wizards at Wikipedia is somehow both “far right” and “libertarian” at the same time – here is the far more “erudite” Financial Times explaining what happened:

Over a two-year period until September 2014, the market-maker removed hundreds of thousands of large OTC orders from its automated trading processes, according to Finra. That rendered the orders “inactive” and so they had to be handled manually by human traders.

Citadel Securities then “traded for its own account on the same side of the market at prices that would have satisfied the orders,” without immediately filling the inactive orders at the same or better prices as required by Finra rules, the regulator said.

In February 2014, a sample month reviewed by Finra, the market-maker traded ahead in nearly three-quarters of the inactive orders. “Based on this review, in 559 instances, Citadel Securities traded ahead of 415 inactive OTC customer orders,” the regulator said.

Of course, since the action was launched by Finra and not the SEC – probably for a reason – Citadel was allowed to put the whole sordid affair without admitting or denying the claims. Just one glitch: the company was required to make whole any customers affected, not something a market maker does if they “denying” claims.

The good news is that neither Citadel nor its lawyers can go after us again for merely reporting what Finra already found because on page 11 of the AWC we read the following:

The Firm may not take any action or make or permit to be made any public statement, including in regulatory filings or otherwise, denying, directly or indirectly, any finding in this AWC or create the impression that the AWC is without factual basis.

Which means that going forward, allegations about Citadel frontrunning clients – on at least 559 instances no less – are fair game. That said, Citadel did make a statement to the FT:

“We have addressed all of Finra’s concerns and take very seriously our obligations to comply fully with its rules. The issue relates to a limited number of manually handled orders, most of which occurred in 2012-2014.”

Which is a succinct way of summarizing precisely what Finra said. Our own request for comments was not returned by the publication time.

But wait, there’s more!

Finra also said Citadel Securities fell short of supervisory requirements and failed to display certain OTC customers’ limit orders: instructions to buy or sell at a specific price, or better. As the FT notes, “nearly half of the 467 limit orders reviewed by the regulator in the six years until September 2018 were found to violate Finra’s requirements to display orders. The bulk of the violations were for failing to execute trades against existing quotations in a timely manner, Finra said.”

What does the above mean for clients? Well, they are welcome to sue Citadel Securities and get their money back. As Finra writes, “the imposition of a restitution order or any other monetary sanction herein, and the timing of such ordered payments, does not preclude customers from pursuing their own actions to obtain restitution or other remedies.“

What does the above mean for Ken Griffin? Well, as noted above, the penalty is about 0.7% of what the CEO recently paid for a Basquiat painting.

It’s also clear that the size of the “penalty” will certainly not force Griffin to mortgage one or more of his extensive properties located in New York, London, Chicago, or Palm Beach and countless others:

One thing that is certain is that trading clearly pays, even if it means occasionally and purely unaccidentally “removing hundreds of thousands of mostly larger customer orders” from mandatory Trading Ahead and Limit Order Display Rules and customer protections.

In fact the only confusion we have at this moment is who is more ironically named: Citadel or Robinhood?

via ZeroHedge News https://ift.tt/2Bl6PZO Tyler Durden

Much of the Crossfire Hurricane investigation into Donald Trump was built on the premise that Christopher Steele and his dossier were to be believed. This even though, early on, Steele’s claims failed to bear scrutiny. Just how far off the claims were became clear when the FBI interviewed Steele’s “Primary Subsource” over three days beginning on Feb. 9, 2017. Notes taken by FBI agents of those interviews were released by the Senate Judiciary Committee Friday afternoon.

The Primary Subsource was in reality Steele’s sole source, a long-time Russian-speaking contractor for the former British spy’s company, Orbis Business Intelligence. In turn, the Primary Subsource had a group of friends in Russia. All of their names remain redacted. From the FBI interviews it becomes clear that the Primary Subsource and his friends peddled warmed-over rumors and laughable gossip that Steele dressed up as formal intelligence memos.

Paul Manafort: The Steele dossier’s “Primary Subsource” admitted to the FBI “that he was ‘clueless’ about who Manafort was, and that this was a ‘strange task’ to have been given.” AP Photo/Seth Wenig, File

Steele’s operation didn’t rely on great expertise, to judge from the Primary Subsource’s account. He described to the FBI the instructions Steele had given him sometime in the spring of 2016 regarding Paul Manafort: “Do you know [about] Manafort? Find out about Manafort’s dealings with Ukraine, his dealings with other countries, and any corrupt schemes.” The Primary Subsource admitted to the FBI “that he was ‘clueless’ about who Manafort was, and that this was a ‘strange task’ to have been given.”

The Primary Subsource said at first that maybe he had asked some of his friends in Russia – he didn’t have a network of sources, according to his lawyer, but instead just a “social circle.” And a boozy one at that: When the Primary Subsource would get together with his old friend Source 4, the two would drink heavily. But his social circle was no help with the Manafort question and so the Primary Subsource scrounged up a few old news clippings about Manafort and fed them back to Steele.

Also in his “social circle” was Primary Subsource’s friend “Source 2,” a character who was always on the make. “He often tries to monetize his relationship with [the Primary Subsource], suggesting that the two of them should try and do projects together for money,” the Primary Subsource told the FBI (a caution that the Primary Subsource would repeat again and again.) It was Source 2 who “told [the Primary Subsource] that there was compromising material on Trump.”

And then there was Source 3, a very special friend. Over a redacted number of years, the Primary Subsource has “helped out [Source 3] financially.” She stayed with him when visiting the United States. The Primary Subsource told the FBI that in the midst of their conversations about Trump, they would also talk about “a private subject.” (The FBI agents, for all their hardnosed reputation, were too delicate to intrude by asking what that “private subject” was).

Michael Cohen: The bogus story of the Trump fixer’s trip to Prague seems to have originated with “Source 3,” a woman friend of the Primary Subsource, who was “not sure if Source 3 was brainstorming here.” AP Photo/J. Scott Applewhite, File

One day Steele told his lead contractor to get dirt on five individuals. By the time he got around to it, the Primary Subsource had forgotten two of the names, but seemed to recall Carter Page, Paul Manafort and Trump lawyer Michael Cohen. The Primary Subsource said he asked his special friend Source 3 if she knew any of them. At first she didn’t. But within minutes she seemed to recall having heard of Cohen, according to the FBI notes. Indeed, before long it came back to her that she had heard Cohen and three henchmen had gone to Prague to meet with Russians.

Source 3 kept spinning yarns about Michael Cohen in Prague. For example, she claimed Cohen was delivering “deniable cash payments” to hackers. But come to think of it, the Primary Subsource was “not sure if Source 3 was brainstorming here,” the FBI notes say.

The Steele Dossier would end up having authoritative-sounding reports of hackers who had been “recruited under duress by the FSB” — the Russian security service — and how they “had been using botnets and porn traffic to transmit viruses, plant bugs, steal data and conduct ‘altering operations’ against the the Democratic Party.” What exactly, the FBI asked the subject, were “altering operations?” The Primary Subsource wouldn’t be much help there, as he told the FBI “that his understanding of this topic (i.e. cyber) was ‘zero.’” But what about his girlfriend whom he had known since they were in eighth grade together? The Primary Subsource admitted to the FBI that Source 3 “is not an IT specialist herself.”

And then there was Source 6. Or at least the Primary Subsource thinks it was Source 6.

Ritz-Carlton Moscow: The Primary Subsource admitted to the FBI “he had not been able to confirm the story” about Trump and prostitutes at the hotel. But he did check with someone who supposedly asked a hotel manager, who said that with celebrities, “one never knows what they’re doing.” Moscowjob.net/Wikimedia

While he was doing his research on Manafort, the Primary Subsource met a U.S. journalist “at a Thai restaurant.” The Primary Subsource didn’t want to ask “revealing questions” but managed to go so far as to ask, “Do you [redacted] know anyone who can talk about all of this Trump/Manafort stuff, or Trump and Russia?” According to the FBI notes, the journalist told Primary Subsource “that he was skeptical and nothing substantive had turned up.” But the journalist put the Primary Subsource in touch with a “colleague” who in turn gave him an email of “this guy” journalist 2 had interviewed and “that he should talk to.”

With the email address of “this guy” in hand, the Primary Subsource sent him a message “in either June or July 2016.” Some weeks later the Primary Subsource “received a telephone call from an unidentified Russia guy.” He “thought” but had no evidence that the mystery “Russian guy” was “that guy.” The mystery caller “never identified himself.” The Primary Subsource labeled the anonymous caller “Source 6.” The Primary Subsource and Source 6 talked for a total of “about 10 minutes.” During that brief conversation they spoke about the Primary Subsource traveling to meet the anonymous caller, but the hook-up never happened.

Nonetheless, the Primary Subsource labeled the unknown Russian voice “Source 6” and gave Christopher Steele the rundown on their brief conversation – how they had “a general discussion about Trump and the Kremlin” and “that it was an ongoing relationship.” For use in the dossier, Steele named the voice Source E.

When Steele was done putting this utterly unsourced claim into the style of the dossier, here’s how the mystery call from the unknown guy was presented: “Speaking in confidence to a compatriot in late July 2016, Source E, an ethnic Russian close associate of Republican US presidential candidate Donald TRUMP, admitted that there was a well-developed conspiracy of co-operation between them and the Russian leadership.” Steele writes “Inter alia,” – yes, he really does deploy the Latin formulation for “among other things” – “Source E acknowledged that the Russian regime had been behind the recent leak of embarrassing e-mail messages, emanating from the Democratic National Committee [DNC], to the WikiLeaks platform.”

All that and more is presented as the testimony of a “close associate” of Trump, when it was just the disembodied voice of an unknown guy.

Perhaps even more perplexing is that the FBI interviewers, knowing that Source E was just an anonymous caller, didn’t compare that admission to the fantastical Steele bluster and declare the dossier a fabrication on the spot.

But perhaps it might be argued that Christopher Steele was bringing crack investigative skills of his own to bear. For something as rich in detail and powerful in effect as the dossier, Steele must have been researching these questions himself as well, using his hard-earned spy savvy to pry closely held secrets away from the Russians. Or at the very least he must have relied on a team of intelligence operatives who could have gone far beyond the obvious limitations the Primary Subsource and his group of drinking buddies.

But no. As we learned in December from Inspector General Michael Horowitz, Steele “was not the originating source of any of the factual information in his reporting.” Steele, the IG reported “relied on a primary sub-source (Primary Sub-source) for information, and this Primary Sub-source used a network of [further] sub-sources to gather the information that was relayed to Steele.” The inspector general’s report noted that “neither Steele nor the Primary Sub-source had direct access to the information being reported.”

One might, by now, harbor some skepticism about the dossier. One might even be inclined to doubt the story that Trump was “into water sports” as the Primary Subsource so delicately described the tale of Trump and Moscow prostitutes. But, in this account, there was an effort, however feeble, to nail down the “rumor and speculation” that Trump engaged in “unorthodox sexual activity at the Ritz.”

While the Primary Subsource admitted to the FBI “he had not been able to confirm the story,” Source 2 (who will be remembered as the hustler always looking for a lucrative score) supposedly asked a hotel manager about Trump and the manager said that with celebrities, “one never knows what they’re doing.” One never knows – not exactly a robust proof of something that smacks of urban myth. But the Primary Subsource makes the best of it, declaring that at least “it wasn’t a denial.”

If there was any denial going on it was the FBI’s, an agency in denial that its extraordinary investigation was crumbling.

via ZeroHedge News https://ift.tt/39fIukx Tyler Durden

The Four Horsemen Of Disinflation: The Coming Rent-pocalypse Tyler Durden

Mon, 07/20/2020 – 21:50

One month ago, we discussed “The Most Important Question In Finance Today“, namely whether in the aftermath of the covid pandemic the world ends up with runaway inflation or price-crushing deflation. Today, Bank of America provides some additional perspective on what it calls the “inflation rollercoaster.”

Separating the inflation stories

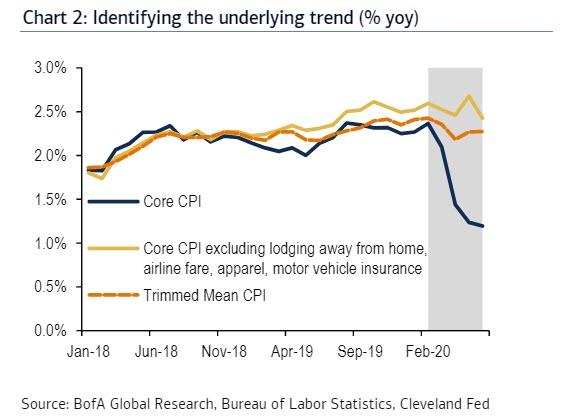

As BofA notes, the pandemic has created significant disinflationary shock to the US economy, with the latest CPI report showing core inflation running at a meager 1.2% yoy clip and core PCE later this month likely to come in at 1.1%. That said, it is important to note that current inflation readings are suggesting conditions are much worse than they actually are. Indeed, most of the deceleration can be attributed to a handful of idiosyncratic components. The underlying trend is stickier and has slowed more modestly.

Looking ahead, the underlying trend slows with rental inflation holding the key. This means that the rollercoaster will eventually turn-the base effects will turn positive in March 2021-and accelerate before settling at a higher, although still likely below target. Consistent with this thinking, Bank of America expects core CPI to trough at 0.8% yoy in 1Q 2021 before rising to 1.6% by the end of next year.

Four horsemen of disinflation

From March through May, the months when the covid shutdowns unleashed unprecedented damage on the US economy, core CPI declined by a cumulative 0.6% resulting in the % yoy rate collapsing to 1.2% from 2.4% in February. The deterioration owed largely to four main areas of weakness: lodging away from home, airline fares, apparel, and motor vehicle insurance. Despite these categories amounting to 6%-7% of CPI, each experienced a record drop in prices.

The first three fell as nonessential travel and businesses activity were shut down, and followed the same pattern of April being the worst month, followed by March and then May. Motor vehicle insurance dropped after insurers began an assortment of COVID-19 relief programs that provided temporary discounts or credits on auto premiums, for April and May for the most part.

According to BofA, these components have added significant noise to the data and should be largely faded when thinking about the underlying inflation trend. They are extreme idiosyncratic moves and are likely to prove transitory (unless there is a second wave of shutdowns of course). Moreover, we have already started to see stabilization in June as all four components posted an increase. With prices so low still, further positive payback seems more likely going forward than another major leg down. If excluded from core CPI, then inflation has slowed more modestly through June to 2.42% from a February reading of 2.59%.

Another more standard inflation metric that paints a similar picture of stickier underlying inflation is the Cleveland Fed’s Trimmed Mean CPI-an index that excludes the 8% of components with the most extreme moves to the upside and the 8% to the downside. TM CPI has also seen modest slowing to 2.27% yoy from 2.42% in February. But the risks are skewed to the downside going forward. Given the stickiness of underlying inflation, it takes some time for the demand shock to percolate and pull down prices.

The coming rent-pocalypse?

The key for underlying inflation will be what happens to owners’ equivalent rent (OER) and rent of primary residence, since the two comprise more than 40% of core CPI inflation. The housing data have been particularly resilient relative to the broader economic data, with the NAHB housing index just recently popping up to 72 in July from 58 and existing and new home sales likely to rise in June. Indeed, homebuying demand has been surprisingly firm during the pandemic as lower interest rates have raised affordability and preferences have increasingly shifted towards suburban living where homeownership is more feasible. However, the resilience of the homeownership market is likely to come at the expense of the rental market. While owners’ equivalent rent is meant to reflect housing costs borne by owner-occupied households, it is estimated using rent data and will therefore be sensitive to rental market dynamics.

So where do rents go from here? According to BofA, the labor market conditions will be a major driver of the rent trajectory. The early data have surprised expectations with the unemployment rate peaking at “only” 14.7% in April and falling to 11.1% in June. However, job gains going forward will not be quite so easy to come by. The virus is not under control as several hotspots have emerged in the last month, and most states have either put a pause on or reversed the reopening process. The real-time labor data are ominous as well as the Census Bureau’s Household Pulse survey have shown declining employment since the week of June 16th.

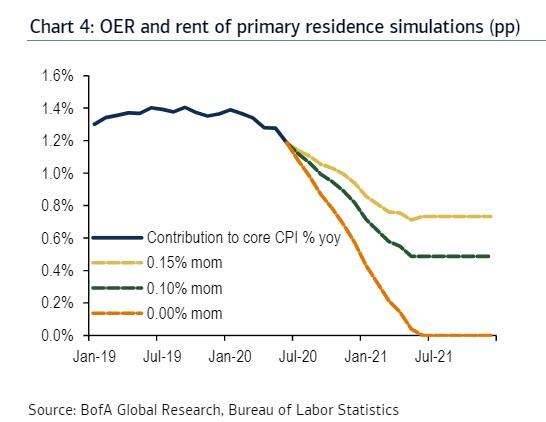

Meanwhile, BofA notes that it has started to see weakness register in CPI in the latest June report: both owners’ equivalent rent and rent of primary residence increased by only 0.1% mom-the softest readings since early 2011. This resulted in the % yoy rates for OER falling to 2.8% yoy from 3.3% in February and for rent of primary residence to 3.2% yoy from 3.8%. And while it may be premature to read into one month of data, BofA’s economists believe that this could be the beginning of a downtrend.

The regional OER data reveal that the soft June data were largely driven by the South and West. Weakness was also relatively broad in these two regions as rent inflation in both large (A, > 2.5mn people) and small (B/C, < 2.5mn people) urban areas were 0-0.1% mom. Meanwhile, the Northeast and Midwest posted trend-like rent gains in June. These two regions have not been immune to the deterioration in labor conditions, so that does pose a bit of a disconnect in terms of the labor-rent response. The June print would be more convincing if all four regions had softened-should this happen clearly there is scope for even weaker monthly readings in broad OER and rent of primary residence.

Even if June ends up being slightly fluky, the risks ahead are clearly skewed to the downside. It is worth reiterating that the CPI methodology allows for significant deflation to materialize in the rent components. If there is a missed payment and the landlord does not expect or is uncertain they will receive it, then that will register as a 95% decline in rents. Therefore, even a small share of missed rent payments can exert a noticeable drag. This is a tail risk though: Janson and Verbrugge (July 2020) found that the incidence of nonpayment in the CPI sample was quite low during the Great Recession. However, given the speed and severity of the current downturn, it could prove to be different this time.

What will slowing rents mean for underlying inflation? We can proxy the impact by simulating the effects of rent on core CPI. If OER and rents average a 0.15% mom clip from now until the end of 2021, then core CPI % yoy would slow by roughly 0.5pp.

If a softer average 0.1% mom reading, then it would be a 0.7pp deceleration. FWIW, BofA believes the underlying trend could slow by an amount within this range, although they can’t eliminate the risk of an even worse outcome as labor market slack will remain elevated with the unemployment rate ending next year close to 8%.

Stuck in purgatory

Putting it all together, BofA expects core CPI to continue to be biased lower through early next year, with core CPI settling below the pre-COVID trend-1.6%. After this point, the special factors will start to fade allowing for acceleration.

via ZeroHedge News https://ift.tt/3hiRnMX Tyler Durden

There is a lot of discussion about the low levels of inventory for sale, as potential sellers have pulled their homes off the market or are not wanting to list their homes at the moment, waiting for the Pandemic to blow over, or waiting for more certainty or whatever; or their mortgage is now in forbearance and they don’t want to make a move.

These discussions cite buyers who, after being kept out of the housing market for a couple of months due to the lockdowns, are now swarming around out there, stumbling all over each other, looking for homes to buy, jostling for position, and engaging in bidding wars with each other.

And then there is the widely reported move to the suburbs, or to small towns, and away from big densely populated cities, by those who have shifted to work-from-home, to work-from-anywhere, which blatantly contradicts some of the other stories of big cities being overrun by buyers engaging in bidding wars.

Those are some of the narratives we’re hearing, and they all make some intuitive sense. But this is not the case everywhere. So we’re going to look at San Francisco, one of the most expensive housing markets in the US, based on weekly data that was compiled by real-estate brokerage Redfin, from local multiple listing service (MLS) and Redfin’s own data, updated at the end of the week.

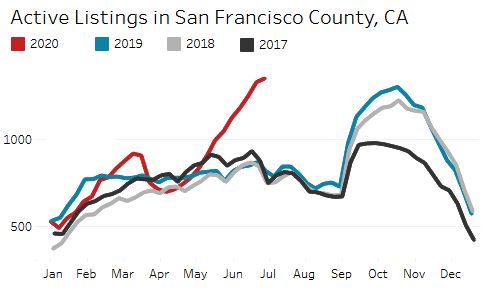

San Francisco is now flooded with homes for sale. “Active listings” surged to 1,344 homes in the week ended July 5, up 65% from the same week last year, and the highest number since the housing bust, amid a 145% year-over-year surge in “new listings.”

There normally is a seasonal surge in active listings after Labor Day that peaks in late October. But this month, the surge of active listings (1,344) has already blown by those peaks in October, including the multi-year peak of 1,296 in October 2019. This is “pent-up supply” coming on the market at the wrong time of the year when supply normally declines (chart via Redfin):

Redfin’s data doesn’t go back that far. But the 1,344 active listings would be the highest since 2011, during the final stretch of the San Francisco Housing Bust, based on MLS data provided by local real-estate site, SocketSite.

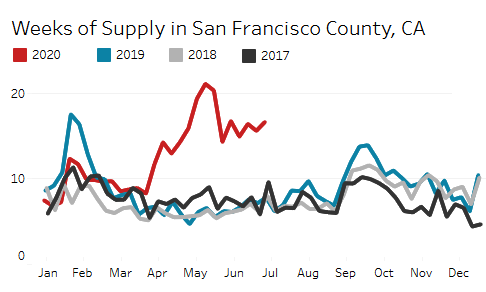

Supply of homes for sales has more than doubled, from 7.8 weeks last year at this time to 16.6 weeks now, at the current rate of sales. Note the spike of supply in May, a function of sales that had collapsed (chart via Redfin).

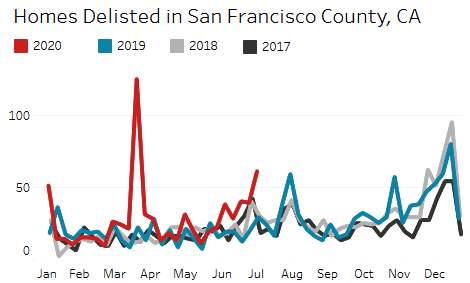

Homes are being pulled off the market again: 61 homes were delisted, over double the number in the same week last year. The chart below shows the spike in delisted homes that started in mid-March during the early phases of the lockdown. It also shows the normal seasonal spike of delistings ahead of the holidays in December – yes, inventory is low because sellers pull their unsold property off the market. But now, with the flood of inventory for sale on the market, the surge in delisted homes has started again (chart via Redfin):

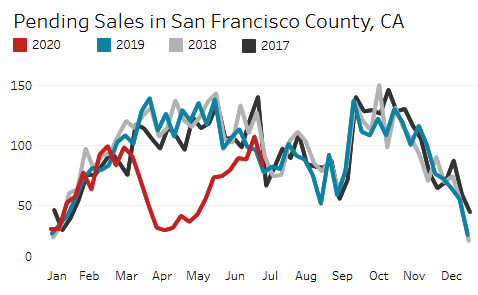

Pending sales lack pent-up demand. Pending sales had collapsed 77% by early April compared to the same time last year, but then started digging out of that trough. In early July, pending sales were still down 8% from last year and now are following the seasonal downtrend and appear to be back on track, just slightly lower.

In terms of the recovery, that was pretty good. But there is no sign of pent-up demand, and the home sales that didn’t happen during the collapse in March, April, and May have not created a surge in deals, and there is no sign of pent-up demand (chart via Redfin).

Buyers now have the largest choice of homes for sale since the Housing Bust nearly a decade ago. And there is no need to engage in bidding wars or other foolishness.

Sellers might be motivated, as they say. Among the sellers might be those who – given the issues of the Pandemic, or future Pandemics – are itching to leave the second most densely populated city in the US, and one of the most expensive, and head to cheaper pastures inland in California, or to other states, or to smaller towns with big price tags along the California coast.

There is lots of anecdotal reporting on these trends, including housing markets that have caught fire in places such as Carmel-by-the-Sea, a beach town on California’s Monterey Peninsula, on Highway 1, about 110 miles south of San Francisco and about 75 miles south of Silicon Valley.

And with work-from-home in place, it might be convenient too. It doesn’t take very long to drive to San Francisco and less long to Silicon Valley for the twice-a-month meeting, especially now, with work-from-home having cleared up some of the previously infernal congestion.

There are all kinds of anecdotal observations and theories people are spinning at the moment, trying to come to grips with the changes underway. But one thing we can now see: The sellers have come out of the woodwork in San Francisco. Just don’t look for the usual thicket of open-house signs on the sidewalk. The process has gone digital and by appointment only.

Do As I Say, Not As I Do: Well Known Tech Antitrust Critic Works For Apple And Amazon On The Side Tyler Durden

Mon, 07/20/2020 – 21:10

One of the country’s most well known antitrust critics, Fiona Scott Morton, happens to be advising two of the biggest tech names in the country, Amazon and Apple, on the side. Morton was labeled a “antitrust crusader” in 2019 by the New Republic.

Scott Morton has consistently said that tech giants are stifling competition and innovation in the country, but failed to recently disclose relationships with Amazon and Apple in papers she recently co-authored, according to Bloomberg. The papers laid out how the U.S. could bring antitrust cases against both Google and Facebook.

She claims that she usually discloses conflicts and that lack of disclosure on the papers shouldn’t be an issue because “Apple and Amazon didn’t pay her to write them” and because they “didn’t focus” on either company. She failed to address the obvious, however: that those companies are competitors of both Google and Facebook.

“I work for companies that I’m comfortable are not breaking the law. So you’re articulating what is making the market work well and how the company’s conduct is pro-competitive or efficient,” she said.

The consulting work she is doing raises obvious ethics questions, especially as antitrust probes are starting to broaden. Amazon, Apple, Facebook and Google are all expected to face significant government scrutiny when they testify July 27 before a House panel.

Scott Morton’s past includes serving for the Justice Department’s anti-trust division from 2011 to 2012. She claims that consulting is “important to her research and teaching” (and wallet) and declined to offer further details about her work.

George DeMartino, a professor at the University of Denver who specializes in ethic says that Scott Morton “should have disclosed her work for Amazon and Apple in the papers”. American Economic Association principles dictate that “economists disclose real and potential conflicts that might influence their work”.

DeMartino said: “Professionals have a duty to maintain trust, which as we now know is a fragile thing. That requires disclosing any actual conflict of interest or any entanglement that might reasonably be interpreted by others as a conflict.”

Gene Kimmelman, a senior adviser at Public Knowledge, who worked with Scott Morton on the Google and Facebook reports said that “conflicts are rife in the antitrust field”. He defended Scott Morton and said that she disclosed her work to him. “I wish all antitrust economists and lawyers had the level of integrity and consistency in analysis she has demonstrated over and over again,” he said.

He also says he hired an outside lawyer to navigate potential conflicts regarding 10 different advisors he asked for help. Almost all of them had conflicts, he said. “Part of the game is to hire them to prevent your opponents from being able to hire them. It’s a large investment that can pay off enormously.”

Economists are “among the most important” hires for companies facing anti-trust violations, Carl Shapiro, an economist at the University of California-Berkeley, said. Google specifically has hired tons of economists, who have cranked out a total of about 330 research papers between 2005 and 2017 that the company supported directly or indirectly. Recipients failed to disclose the funding source in 65% of cases.

Scott Morton stands out, however, because she has been such a high profile name: she has appeared on panel discussions and has testified in front of congress. Last year she helped pen a paper about the “immense power of tech platforms”.

And the names funding her have also come under scrutiny. Amazon has specifically been the target of Elizabeth Warren, who Tweeted in 2019: “Giant tech companies have too much power. My plan to #BreakUpBigTech prevents corporations like Amazon from knocking out the rest of the competition. You can be an umpire, or you can be a player — but you can’t be both.”

At the time, Scott Morton retweeted the Tweet and said: “This is the most articulate explanation of this Amazon theory of harm I have heard so far.”

She has since deleted the Tweet.

via ZeroHedge News https://ift.tt/32CJr5a Tyler Durden

On March 20, 2017, then-FBI Director James Comey told Congress that the FBI was formally investigating whether there were contacts between the Trump campaign and the Kremlin. We later learned that the alleged basis for this investigation was the Steele Dossier. Since then, we’ve also learned that the information in the Steele Dossier was fake.

The big question now is when did the FBI know that the whole investigation, which severely handicapped Trump’s first term, was baloney?

The answer, based upon newly released documents from the Senate Judiciary Committee, is that by mid-February 2017 Comey knew or should have known that the Steele Dossier was a hoax perpetrated by the Hillary campaign.

To go back a step, we know from Inspector General Michael Horowitz’s December 2019 report that the FBI relied upon the Steele Dossier both to spy on Carter Page and to investigate the Trump campaign. The same report establishes that the FBI’s investigation revealed that Steele’s information came from a source who, in turn, got his information from yet another source. By March 20, when Comey announced that the FBI was looking into the Trump campaign, FBI agents on the ground had already stated that the primary source had no credibility.

What the Horowitz Report did not address was when Comey personally learned about the credibility problem. Comey refused to cooperate with the IG investigation, so Horowitz glossed over Comey’s knowledge or lack thereof. One of the problems (see pp. 370-371 of the report) was that the FBI agents who interviewed the sub-source wrote documents falsely implying that he was reliable, even as their notes said otherwise.

That confusion held Horowitz back from imputing knowledge to Comey. The two newly declassified documents, however, practically cry out that, when Comey announced the Trump investigation, he knew or should have known that it had no basis.

The first document, which is heavily redacted, establishes that the primary source was not (as many speculated) a highly placed Russian. Contacts with the Kremlin would have militated in favor of believing him or her. But when the FBI identified Steele’s primary source, they found that he was not a Russian official, nor was he even based in Russia. That should have been a huge red flag that there was a problem.

The second document poses an even bigger problem for Comey. On February 14, 2017, the New York Times published an article entitled, “Trump Campaign Aides Had Repeated Contact With Russian Intelligence.” Peter Strzok, who headed the Trump investigation (aka Operation Crossfire Hurricane), read the article and made notes establishing that the FBI had no basis for investigating Trump. Sharyl Attkisson quoted the notes:

Claim in NYT article: “Phone records and intercepted calls show that members of Donald J. Trump’s presidential campaign and other Trump associates had repeated contacts with senior Russian intelligence officials in the year before the election, according to four current and former American officials.”

Note by Strzok: “This statement is misleading and inaccurate as written. We have not seen evidence of any individuals in contact with Russians (both Governmental and non-Governmental)” and “There is no known intel affiliation, and little if any [government of Russia] affiliation[.] FBI investigation has shown past contact between [Trump campaign volunteer Carter] Page and the SVR [Foreign Intelligence Service of the Russian Federation], but not during his association with the Trump campaign.”

[snip]

Claim in NYT article: “Officials would not disclose many details, including what was discussed on the calls, and how many of Trump’s advisers were talking to the Russians.”

Note by Strzok: “Again, we are unaware of ANY Trump advisers engaging in conversations with Russian intel officials” and “Our coverage has not revealed contact between Russian intelligence officers and the Trump team.”

[snip]

Claim by NYT: “Senior FBI officials believe … Christopher Steele … has a credible track record.”

Note by Strzok: “Recent interviews and investigation, however, reveal Steele may not be in a position to judge the reliability of subsource network.”

The FBI’s decision to investigate a duly elected president was arguably the most consequential investigation the FBI has ever undertaken. The man leading the investigation, who was only two levels below Director Comey, wrote notes that strongly imply that, five weeks before Comey announced the investigation (and after the FBI had engaged in months of intensive work), the FBI had nothing.

These documents make it more likely than not that Comey knew that the investigation was baseless. If he did know, and he nevertheless continued the investigation and publicly announced it, thereby deliberately and severely damaging a duly elected president, what he did was nothing less than sedition.

The fact that Comey still walks free is a troubling indication that it’s business as usual in the Swamp. When swamp rats who support Democrats break the law, they go free.

via ZeroHedge News https://ift.tt/2WEWTBD Tyler Durden

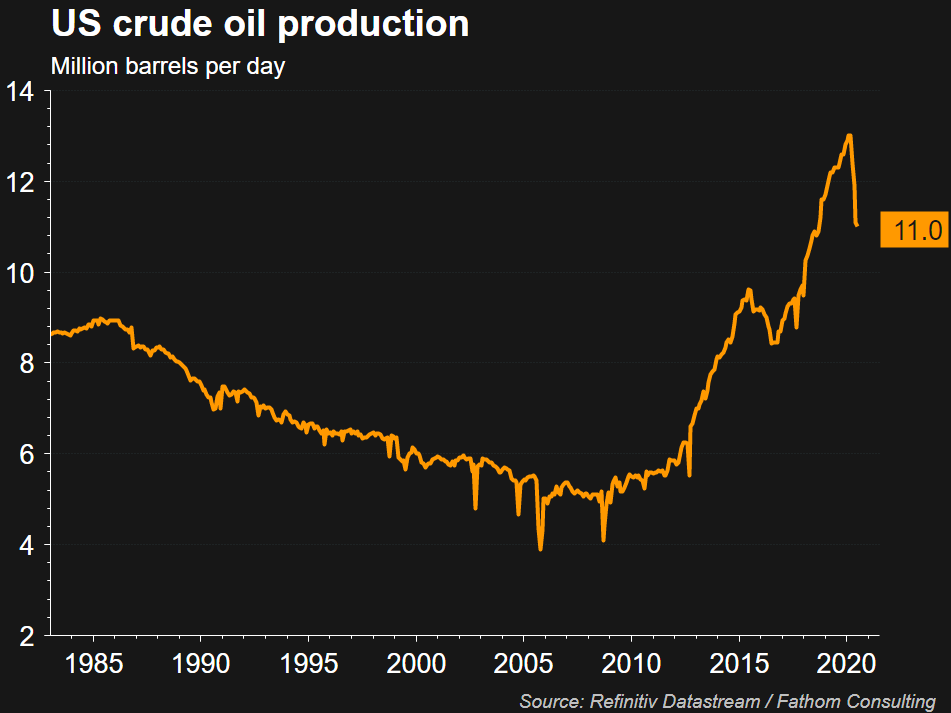

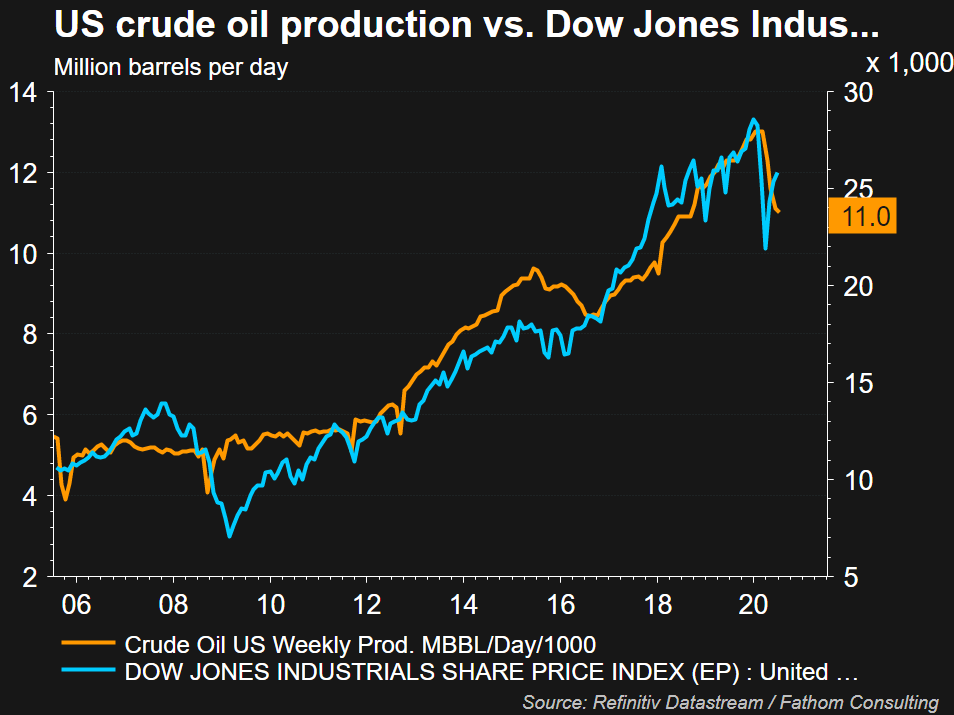

Top Shale Boss Warns US Production Won’t Revisit 2019 Levels “In My Lifetime” Tyler Durden

Mon, 07/20/2020 – 20:30

America’s energy dominance could be coming to an end as the country’s shale industry is experiencing steep production declines. Rarely do we hear President Trump these days touting shale jobs and production output, mostly because the industry has entered a bust cycle.

Matt Gallagher, CEO of Parsley Energy, a top 20 producer in Texas, spoke recently with the Financial Times and said crude output of 12 or 13 million barrels per day is over:

“I don’t think I’ll see 13m [barrels a day] again in my lifetime.

“It is really dejecting, because drilling our first well in 2009 we saw the wave of energy independence at our fingertips for the US, and it was very rewarding . . . to be a part of it,” Gallagher,37, said.

Us Crude Oil Production

The shale bust of 2020 is an ominous sign of America’s energy dominance is over. Crude output will continue to wane this year and likely into next. The lack of shale profitability, mainly due to West Texas Intermediate (WTI) prices sub-$40 per barrel won’t be enough for highly indebted shale companies to survive.

We’ve pointed out the shale industry could be on the verge of destruction due to the sharp decline in demand and plummeting energy prices brought on by coronavirus pandemic. So far, bankruptcies in the shale patch are accelerating to levels not seen since the first half of 2016.

Another significant driver of lower production levels is a halving of rig counts due to collapsing price and demand; rigs dropped from 539 in mid-March to 258 last week.

“Tight oil production will decline by 50% by this time next year. As a result, US oil production will fall from to less than eight mmb/d by mid-2021,” we noted via Arthur Berman via OilPrice.com.

The combination of the Saudi-Russia oil price war and the virus pandemic has been nothing but disastrous for shale companies. These two factors forced Gallagher earlier this year to shut down wells and slash spending.

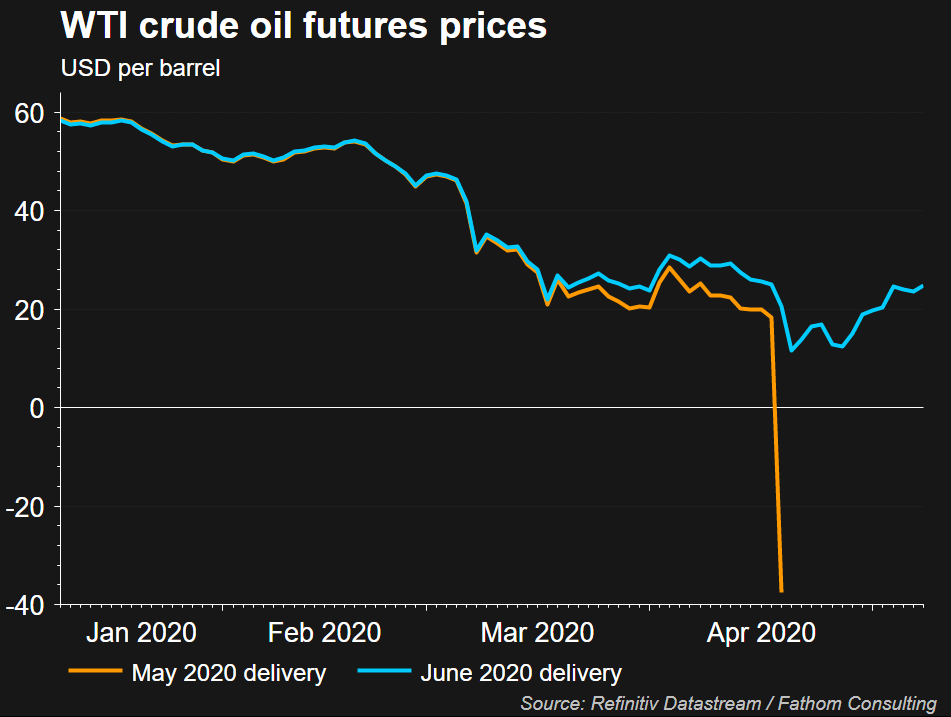

He said the recent oil-price crash was “hands down” the worst ever. In April, WTI prices dove below the zero mark for the first time in history due to oversupplied conditions triggered by virus-related lockdowns.

WTI May contracts dove into negative territory in April.

Gallagher said car and air travel demand has slumped – which could result in oil production stabilizing around 11 million barrels per day. He said producers would focus on maintaining output, not increasing it.

Gallagher concluded the interview by saying hundreds of thousands of jobs depend on the shale industry, adding that activity levels for the industry will be “dramatically lower for a long time.”

Slumping crude production is more bad news for the stock market…

Contrary to Larry Kudlow’s constant touting of a “V-shaped” recovery – this is more bad news that deep economic scarring from the virus pandemic will result in years of high unemployment and sub-par economic growth. And it now appears shale has lost its energy dominance in the world.

via ZeroHedge News https://ift.tt/3hp4b4n Tyler Durden

As businesses, agencies and organizations recalibrate to the reality that the V-shaped recovery was nothing but a brief fantasy, 6 million additional jobs lost may be a best-case scenario rather than the worst-case scenario.

It is somewhat less than reassuring that the “official” unemployment rate of around 12% is roughly half of the “real-world” unemployment rate. As always in the wonderful world of statistics, especially politically potent ones, it depends on what you measure, what you don’t measure / act as if it doesn’t exist, and how you measure what you do measure.

Everyone who digs beneath the headline numbers of employment / unemployment soon discovers a number of jarring anomalies in what the media presents as “factual statistics.”

The first is that the Bureau of Labor Statistics (BLS) doesn’t actually count the number of people who are employed / unemployed; they rely on a sampling survey of employers, which is more like an election poll than an actual measurement.

Secondly, they estimate the number of new businesses which are “born” and existing businesses that “die”, and then guesstimate the number of additional employees this real-time churn generates. This birth/death model is notoriously inaccurate, as it ignores little things like pandemics and is often magically revised to create or eliminate hundreds of thousands of presumed jobs.

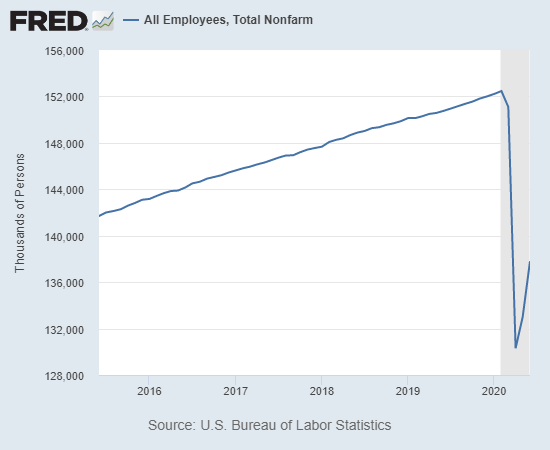

The BLS reported that the U.S. employed workforce stood at about 152 million in February. With 32 million claiming unemployment, that’s an unemployment rate of 21%. How do we arrive at a 12% unemployment rate? We ignore the 14.3 million contract / gig workers who are currently drawing emergency Federal unemployment via Pandemic Unemployment Assistance (PUA),and the 936,000 in the Pandemic Emergency Unemployment Compensation (PEUC) program.

But even the 21% real-world unemployment rate doesn’t reflect the full unemployment picture: previously full-time workers who have had their hours cut to part-time aren’t counted in unemployment statistics, even though their employment status has changed for the worse.

Then there are the millions of workers who were recalled to work as businesses re-opened whose employment is up in the air as the expected return-to-normal has failed to materialize.

An entire class of workers has been glossed over: small business owners who have closed their businesses. Those owners who incorporated and paid unemployment insurance on themselves as employees of the corporation qualify for unemployment, but many small business owners didn’t pay themselves as employees, and their status is uncertain.

Anecdotally, the number of small business owners who have decided to close in recent weeks appears to be significant, as the hoped-for V-shaped recovery failed to materialize even as states re-opened. This trend could gather momentum as hope decays into realistic assessment and funds borrowed from emergency federal programs (PPP) run out.

The number of employees who will be laid off again as a rising flood of small businesses throw in the towel could quickly become consequential.

Barring an immediate additional influsion of federal stimulus, local governments will also start laying off temp and contract workers as tax revenues continue their downward spiral.

As Corporate America’s revenues falter, the only ways to reduce costs are 1) dump leases on commercial space and 2) lay off employees and 3) slash spending to the bone. All of these end up triggering layoffs.

Could the number of unemployed rise to 38 million from 32 million, a 25% rate of unemployment? As businesses, agencies and organizations recalibrate to the reality that the V-shaped recovery was nothing but a brief fantasy, 6 million additional jobs lost may be a best-case scenario rather than a worst-case scenario.

{kind=link}