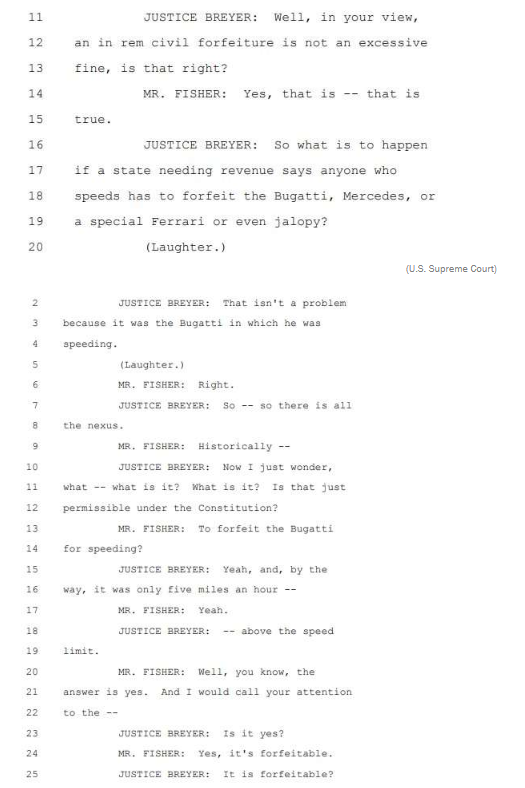

Despite losing in the United States Supreme Court, the state of Indiana is still arguing that there are virtually no eighth amendment limits on what it can seize using civil asset forfeiture, according to Reason.

In fact, Indiana Solicitor General Thomas Fisher argued in Indiana Supreme Court last week that it would be constitutional to seize any and every car that exceeded the speed limit. It was an argument that drew laughter from the U.S. Supreme Court last year.

Fisher said:

“This is the position that we already staked out in the Supreme Court when I was asked by Justice Breyer whether a Bugatti can be forfeited for going over five miles over the speed limit. Historically the answer to that question is yes, and we’re sticking with that position here.”

The issue has been brought to light as a result of the Indiana Supreme Court reconsidering a case where a 2015 seizure of Tyson Timbs’ $42,000 Land Rover, after he was convicted of a drug felony, was argued to have violated his eighth amendment protections against excessive fines and fees.

Tyson Timbs

In February, the United States Supreme Court reversed the Indiana Supreme Court’s ruling that Timbs “could not challenge the seizure on Eighth Amendment grounds because the excessive fines clause had not yet been applied, or ‘incorporated,’ to the states.”

It also brought to light the power of the practice, which allows authorities to seize property suspected of being connected to criminal activity. The Indiana Supreme Court will now have to figure out how to determine whether a civil forfeiture is excessive or not. The result could either check – or reinforce – the state government’s power.

Lawyers for the Institute for Justice, a libertarian-leaning public interest law firm, argued that the seizure of Timbs’ car, which was not purchased with drug proceeds and was worth four times the maximum fine for his crime, was a disproportional punishment.

The Institute for Justice had to petition the US Supreme Court to review the case after the Indiana Supreme Court ruled against Timbs. The state argued that the excessive fines clause did not apply to the practice of civil asset forfeiture which operates under the legal fiction that it is an action against the property itself, not the owner.

Both sides of the aisle in the U.S. Supreme Court have expressed skepticism about civil asset forfeiture in past rulings and they were not impressed by Fisher’s argument. A judge even forced counsel for the state of Indiana to admit it would be constitutional to then seize any car going over the speed limit.

According to Reason:

The state of Indiana, although forced to recognize that the Eighth Amendment applies to civil forfeiture, now insists that the test that should apply to determine whether the seizure was excessive is not the proportionality, but rather whether the government can prove a nexus between Timbs’ car and the illegal activity – a standard that would put virtually no check on the amount of property police could seize as long there was some connection to a crime.

Justice Loretta Rush pushed back on the argument:

“So where’s the limits? If the state decides you’re going over x miles per hour so we’re going to take your car, is there any limit to that government power?”

Fisher responded:

“No, look, I’ve gone out on a limb on the Bugatti, and I don’t think I’m going back.”

Institute for Justice lawyer Sam Gedge said:

“Indiana has resorted to an increasingly dangerous view of governmental power over the years it has been fighting to keep Timbs’ car. In the State’s view, it can constitutionally forfeit a Bugatti that goes five miles over the speed limit. And the State insists that it can take any property from any person who has ever struggled with drug addiction. That boundless view of governmental power cannot be squared with the Constitution.“

via ZeroHedge News https://ift.tt/30kUIT9 Tyler Durden

There are growing signs that the global economic slowdown is for real. As was the case in 1929, the combination of the peak of the credit cycle coupled with trade protectionism in the Smoot-Hawley Tariff Act are similar conditions to those of today and potentially pose a serious economic challenge to the post-Bretton Woods fiat currency system. Therefore, we must consider the consequences if monetary policy fails to contain the developing recession and it turns into a full-blown slump. Complacency over broken markets is no longer an option, with rising prices for gold and bitcoin signalling the prospect of a new round of currency debasement to avoid market distortions unwinding. This article shows why this outcome could undermine fiat currencies entirely and looks at the alternatives of bitcoin and gold in this context.

Introduction

Never in all recorded history have financial markets been so distorted everywhere. In our lifetimes we have seen the USSR and also China under Mao attempt to do without markets altogether and fail, having starved and slaughtered millions of their citizens in the process. The Romans started a long period of currency debasement, lasting from Nero to Diocletian, who wrote prices in stone (the origin of the phrase) in a vain attempt to control them. While the Roman Empire was the known world at the time, it was essentially restricted to the Mediterranean and Europe. Subsequently, there have been over fifty instances recorded of complete monetary collapse, the vast majority in the last hundred years, which have led to the breakdown of every society involved. And now we could be facing a global totality, the grand-daddy of them all.

We have become inured to cycles of credit expansion, driven by fractional reserve banking at least since the Bank Charter Act of 1844, which legalised fractional reserve banking. Extra impetus was given by central banks from the 1920s onwards. We have become so used to it that we now expect central banks to issue and control our money and only get really worried when we think they might lose control. In their efforts to satisfy the mandate they have assumed for themselves central banks intervene more and more with every credit cycle.

Our complacency extends to prices, especially regarding the exchange and valuation of capital assets. There are now about $13 trillion of bonds in issue with negative yields. We rarely think in any depth about this strangeness, but negative yields are never the consequence of market pricing free from monopolistic distortions. The ECB, the Bank of Japan and the Swiss National Bank all impose negative interest rates, as well as Sweden’s Riksbank and Denmark’s Nationalbank. The ECB commands the currency and finances of the largest economic area in the world and the BoJ the third largest national economy. In Denmark, mortgage lenders are even offering negative-yield mortgages: in other words, Danes are being paid to take out loans with negative interest rates. Ten-year government bonds issued by Germany, Japan, Sweden and even by France have negative yields. All Danish government bonds have negative yields.

Negative yields stand time-preference on its head. Time-preference refers to the fact that we prefer current possession to future possession, for obvious reasons. So, when we part with our money we always do so at a discount to expected repayment, which is reflected in a positive rate of interest. The idea that anyone parts with money to get less back at a future date is simply nuts.

It gets even more bizarre. The French government has debts roughly equal to France’s GDP and by any analysis is not a very good credit risk, but it is now being paid by lenders to borrow. Only forty per cent of her economy is the productive tax base for a spendthrift, business-emasculating government. An independent observer evaluating French government debt would be hard put to classify it as investment grade in the proper meaning of the term. But not according to bond markets, and not according to the rating agencies which today’s investors slavishly follow.

There are a number of explanations for this madness. Besides complacency and misplaced investor psychology, the most obvious distortion is regulation. Investors, particularly pension funds and insurance companies are forced by their regulators to invest nearly all their funds in regulated investments. Their compliance officers, who are effectively state-sponsored bureaucrats, control the investment decision process. Portfolio managers have become patsies, managing capital with little option but to comply.

Additionally, with their highly-geared balance sheets state-licenced banks complying with Basel II and III are also corralled into “riskless” assets, which according to the regulators are government debt. The rating agencies play along with the fiction. For example, Moody’s rates France as Aa2, high quality and subject to very low credit risk. This is for a country without its own currency to inflate to repay debt. Low enough for negative yields? Low enough to be paid to borrow?

In Japan, the country’s government debt to GDP ratio is now over 250%. The Bank of Japan maintains a target rate of minus 0.1%, and the 10-year government bond yield is minus 0.16%, making the yield curve negative even in negative territory. It doesn’t stop there, with the Bank of Japan having bought 5.6 trillion yen ($52bn) of equity ETFs last year. This takes its total equity investment to 29 trillion yen ($271bn), representing 5% of the Tokyo Stock Exchange’s First Section. Last year’s purchases absorbed all foreign selling of Japanese equities, so they were clearly aimed at rigging the equity market, rather than some sort of monetary manoeuvre.

It’s not only the Bank of Japan, but the National Bank of Switzerland has been at it as well. According to its Annual Report and Accounts, at end-2018 it held CHF156bn in equities worldwide ($159bn), being 21% of its foreign reserves. We can see the direction central bank reserve policy is now heading and should not be surprised to see equity purchases become a wide-spread means of rigging stockmarkets and expanding base money.

Sovereign wealth funds, which are government funds that owe their origin to monetary inflation through the foreign exchanges, have invested a cumulative total of nearly $2 trillion dollars in listed equities.[iii] While this is only 2.5% of total market capitalisation of listed securities world-wide, they are a significant element in marginal pricing, more so in some markets than others.

Between them, central banks and sovereign wealth funds that are buying equities in increasing quantities further the scope of quantitative easing. The precedent is now there. Economists in the central banking community now have a basis for drafting erudite neo-Keynesian papers on the subject, giving cover for policy makers to take even more radical steps to pursue their interventions.

By all these methods, state control of regulated public and private sector funds coupled with the expansion of bank credit has cheapened government borrowing, and it would appear that governments are now enabled to issue limitless quantities of zero or negative-yielding debt. So long as enough money and credit is fed into one end of the sausage machine, it emerges as costless finance from the other. Never mind the destruction wreaked on key private sector investors, such as pension funds, whose actuarial deficits are already in crisis: that is a problem for later. Never mind the destruction of insurance fund finances, where premiums are normally supplemented by healthy bond portfolio returns. Just blame the insurance companies for charging higher premiums.

This is now the key question: are we entering a new phase of low-inflation managed capitalism, or are we tipping into a mega-crisis, possibly systemically destructive?

If the latter, there’s a lot to go horribly wrong. The Bank for International Settlements, the central banks’ central bank, is certainly worried. Only this week, it released its annual economic report, in which it said, “monetary policy can no longer be the main engine for economic growth.” Clearly whistling to keep our spirits up, it calls for structural reforms to boost government spending on infrastructure. Translated, the BIS is saying little more can be achieved by easing monetary policy, so Presidents and Prime Ministers, it’s over to you. You can create savings by making government more efficient and you can spend more on infrastructure.

While the BIS washes it hands of the problem, history and reason tell us increased state involvement in economic outcomes will only make things worse. It is in the nature of government bureaucracy to be economically wasteful, because its primary purpose is not the efficient use of capital resources. And while the outcome, be it a new high-speed railway or a bridge to nowhere may be a visible result, it fails to account for the true cost to the economy of diverting economic resources from what is actually demanded.

Heed the message from the credit cycle

Bullish investors should note that we are already far down the path of our economic decline, which gives a fundamental falsity to financial valuations. Following the Lehman crisis, the expansion of money and credit fed into asset inflation, creating an illusion of improving business prospects. The suppression of interest rates was the come-on to businesses to invest in production. The government’s budget deficit created extra spending as a further encouragement. The government’s economists say it’s all down to reviving those animal spirits. But they have been encouraging businesses to chase a mirage, which as they progress towards it always seems that little bit further away, until it finally disappears altogether. Businesses that relied on the state’s mirage now find it is just an illusion.

For those of us struggling to preserve our savings the effect of monetary inflation on financial prices is the reality that matters. The purchasing power of the currency in which we measure our savings is a commonly neglected consideration, an issue of added importance at times of high monetary inflation. Unfortunately, it is an effect that cannot be measured, but it doesn’t stop statisticians from persuading us that they can. Even though they are accepted by financial analysts without any reservation, government statistics on price inflation have underplayed the progressive impoverishment of productive consumers by monetary debasement. Since this dishonourable manipulation of statistics was adopted, governments have been faced with a stark choice: either they confess to the deceit and protect the currency from further debasement, or like every Roman Emperor who followed Nero, continue to debauch the currency so long as there are suckers to believe in it.

The growing dishonesty of statistical manipulation over time is an additional factor to take into account when observing successive credit cycles. They are part of a policy of concealing the fact that they are getting worse, when the official line is otherwise: policy-makers claim to be improving their control over the excesses of the markets by supressing evidence to the contrary.

Credit cycles have been generally worsening, at least since the inflationary crisis of the 1970s, which followed the abandonment of the Bretton Woods Agreement in 1971. Central banks have debauched their currencies increasingly over successive credit cycles, building up to an inevitable apocalyptic crash. The approaching one could be our global totality, the grand-daddy of them all.

Those of us not wrapped up in the illusion of modern monetary theory and Keynesian and monetarist claptrap have always know it will happen one day. The collapse of the Bretton Woods Agreement was an event in a larger cycle of government intervention and failure. Von Mises knew it would happen, and he explained why in his The Theory of Money and Credit, first published in German over one hundred years ago. Ten years before it happened, he predicted the collapse of the mark and other European currencies in the early 1920s. Since then, we have proved that collectively we have learned little.

It’s like living on the slopes of a volcano, knowing it is certain to erupt one day. The optimists are betting that the growing mountain of negative-yielding debt is not the apocalypse’s calling-card.

Trade protection and the credit cycle

So far, I have described the worrying imbalances in financial markets, evidenced in this credit cycle by growing quantities of negative-yielding debt. But last year, an additional problem arose through American trade tariffs, which now combine with the top of the credit cycle.

I have written about this before, so will only summarise the main point here.[iv] In 1929, the Smoot-Hawley Tariff Act was legislated at the end of the 1920s credit expansion, and it was the combination of the two that changed the similarly benign conditions of the 1920s to those of today into the 1929 crash and the depression that followed. Undoubtedly, there were other factors that made the situation worse than it otherwise would have been, principally President Hoover’s disastrous attempts to intervene in the economy. Today, government intervention is far more pervasive, and has the potential to make things even worse.

It must not be assumed that today’s stock markets will fall by nine-tenths, as was the case between 1929-32. Through the medium of dollar, in those days prices were effectively measured in gold at the fixed rate of $20.67 to the ounce. Today, currencies are totally fiat, and the price of any financial asset will reflect changes in value from the money side as well as from the asset itself. However, stocks are still likely to be liquidated in a serious downturn. Added to this today is a potential ETF problem, where investors’ only attachment is to bullish stockmarkets and not individual investments. As soon as the public wake up to changed market conditions we can expect them to liquidate index-tracking ETFs.

By all appearances, in its early days the ending of a prolonged period of credit expansion is turning out for investors to be no worse than a normal downturn – nothing monetary policy can’t fix. It is certainly possible the can will be kicked down the road just one more time. If that fails, a second phase of investor psychology will anticipate a deepening of the global recession and a realisation that monetary policy is failing to stop it. Equity markets should then begin to fall in earnest. Property prices can be expected to follow, perhaps declining heavily given the leverage of mortgage debt. So far, so conventional.

If it happens, almost certainly there will be a financial abyss into which we will all stare. We have seen it before: in January 1975 in the UK, it was after the stockmarket had fallen 73% from its 1972 peak. There was a similar moment in America in 2002, when Alan Greenspan turned it round. And during the great financial crisis, there was another moment, still fresh in our minds. Always, the solution was for the establishment, comprising the government, its central bank, the commercial banks and the pension and insurance funds to act together behind the scenes to restore confidence. We can be sure that government coercion to achieve the same revival of confidence will be tried again if the situation arises.

If an attempt to fully restore confidence fails to do more than provide a short-term fix, government finances will deteriorate further, and monetary inflation will be tried in even greater quantities than we have seen heretofore. Flooded with fiat money, most economies will then experience rising price inflation that can no longer be camouflaged by government statistics. To protect the currencies and reflect the markets’ increasing time-preference, higher interest rates will then surely follow.

In such an environment, the world’s banking system will be under enormous strain, and the risk of systemic failure will escalate. While it is never too late to look for alternatives to deposits in the banking system, it is far better to seek them before a crisis can be seen on the horizon. In the event that global fiat-money finances do deteriorate into a systemic crisis, the majority of people will be caught by surprise, having relied on the state to regulate greedy bankers and crony capitalists of all stripes.

Unfortunately, complacency and ignorance are no defence in the courts of human experience. The two alternative stores of value, whereby money can be taken out of a bank without queueing for physical cash, are through the purchase of secure cryptocurrencies such as bitcoin and metallic money – gold and silver. Their prices are already rising, perhaps reflecting shortening odds of the cataclysmic events described herein taking place.

For this reason, the merits and limitations of both should hold our interest.

Bitcoin, King of the cryptos

The more prescient individuals amongst us will have already taken out some insurance against the inevitable calamity von Mises described over a hundred years ago. Traditionally, this has meant portfolio exposure to precious metals. But in the last few years, we have observed an interesting development. The decentralisation of information through the internet has undermined government control of the media, particularly with respect to money.

The growing numbers of millennials now seeking the truth about money is a new phenomenon. They seek alternatives to state-issued currency, and are the driving force behind cryptocurrencies. The invention of a digital rival, bitcoin, along with other cryptocurrencies has profound implications for the hitherto unquestioning public acceptance of fiat currency.

Keynes wrote that:

“There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces on the side of destruction and does it in a manner which not one man in a million is able to diagnose.” (The Economic Consequences of the Peace, 1919).

With the new millennials, the ignorance of the masses upon which currency-issuing governments depend is being unexpectedly eroded. Through their interest in cryptocurrencies they have learned about the drawbacks of fiat currencies, and while their unconditional support for bitcoin and the like may be challenged, they realise that governments debauch currencies at their expense. For this reason, cryptocurrencies, particularly bitcoin, are a significant threat to state currencies.

The consequence may be to speed up the collapse of fiat currencies. Faith in fiat currencies is already being tested, which can be deduced from the performance of bitcoin’s price. Furthermore, if commercial banks become systemically threatened, we can expect to see rapidly increasing amounts of fiat deposits being exchanged by millennials for diminishing quantities of bitcoin.

The mistake observers of bitcoin often make is to disqualify it as money because it is volatile. What matters is not its use as a medium for transactions, but its ability to store value wholly protected from government intervention by virtue of its distributed ledger. Through their continual debasement and their tightening control over the use of fiat currencies, governments have created and fuelled the demand for bitcoin. And when it comes to security, bitcoin and its blockchain has survived all attempts to break them. It is in various service providers that the weaknesses lie, not in bitcoin and its blockchain.

Though they have shown interest in the blockchain, financial institutions are only now beginning to take notice of bitcoin itself, and pressure is mounting for it to be accepted as an investment asset. Regulated bitcoin futures contracts are being traded on Comex, and when other asset classes yield inadequate returns, pressure for financial institutions to invest in bitcoin should continue to increase.

While no one can predict how bitcoin prices will actually evolve, it is already becoming clear that its story has much left to tell. Interestingly, bitcoin’s recent dramatic price move has come at a time when the risk of a deepening and global economic recession appears to be increasing. It is not yet tangible evidence that bitcoin could accelerate the transfer of value away from fiat money, thereby undermining it, but it is food for thought.

Gold, the only money that survives all

In all history, its rarity, desirability and chemical stability tell us that gold is the most secure form of money. It is only in the advanced economies in the West, where we have fallen for decades of government propaganda that gold no longer has a monetary role, that people have forgotten its proven qualities as the ultimate money.

It stands to reason that as the purchasing-power of state-issued currencies is increasingly threatened by over-issuance, the west’s collective amnesia will be replaced by a reassessment of gold as the proven protection from collapsing fiat currencies. Despite the excitement generated by secure cryptocurrencies such as bitcoin, gold remains the refuge of choice for those concerned about an emerging post-fiat world, a world where even the internet and mobile communications risk being disrupted, rendering cryptocurrencies temporarily useless as transaction money.

Ahead of a collapse in fiat currencies, the most powerful argument in favour of both bitcoin and gold is their ability to store value. This is not the same as their role as currency, which becomes more important afterwards, when bitcoin cannot compete with gold. The transfer of bitcoin ownership is restricted to a daily rate of about 500,000 and is already running close to this capacity. For this reason, it can never replace conventional forms of instant exchange, unlike a gold coin. Only gold (and additionally silver) will offer both the store of value and cash-transaction functions demanded in a post-fiat world. The physical supply of gold will become central to its price relationship with failing fiat currencies, so a proper assessment of the stock of gold available as currency in a post-fiat world is essential.

Gold as money can be regarded as being in two categories. There are the reserves, held by central banks, which will be required to back note issues and electronic money when the fiat-money component of reserves become worthless. Additionally, there are gold bars and coins distributed in public ownership. The two quantities appear to be similar, as the following analysis demonstrates.

Of a total above-ground stock of physical gold, which at Goldmoney we estimate to be about 176,000 tonnes, perhaps 60% is used for jewellery and industrial purposes, leaving 70,400 tonnes, of which 34,024 tonnes are recorded as official reserves. However, it is almost certainly the case that nations, such as China, hold gold which is undeclared, and at the same time, not all official reserves are bullion, but bullion swapped and leased so are double-counted. Let us simplistically assume that these two quantities cancel each other out. That leaves an estimated 36,376 tonnes owned by the public as bar and coin, which together with official reserves we can regard as the gold money supply.

Strictly speaking, it is a mistake to include jewellery in Asia (where the bulk of it is held) as part of gold’s money supply. While it can easily be encashed close to melt value, in practice it is not held for this purpose. The flow of gold into jewellery tends to be a one-way phenomenon, where it is more likely to be used as collateral at Asian pawnshops for the purpose of bridge financing and capital spending, with the intention of being redeemed for fiat cash. Therefore, except in the case of a post-apocalyptic economic catastrophe, gold jewellery is not part of gold’s monetary flow. Significantly higher gold prices may change this, but for now gold jewellery should be regarded as its owners see it: a dependable asset to be held and passed on to successive generations.

The reason for belabouring the point is analysts mistakenly use estimates of total above-ground stock as gold’s money supply. It confuses a store of value with money available for transactions, the same confusion that leads advocates of cryptocurrencies to regard bitcoin as a circulating currency. Bitcoin can only circulate within the constraints of a distributed ledger, so its theoretical status is more akin to a form of digital jewellery, hoarded and not intended to be spent.

We can now compare the value of gold that will circulate as currency with the total of cash and bank deposits in fiat currencies held round the world. Internet searches tell us the world’s fiat money totals about $80 trillion, while the quantity of monetary gold as redefined above at current prices is worth $3.2 trillion, a ratio of 25 times. And that’s before any further expansion of fiat money is issued in an effort to stem a developing credit crisis.

Conclusion

It is very likely the recent strength in both gold and bitcoin is linked to changing perceptions of risk to the global economy. It has become increasingly clear in recent weeks that the coincidence of the end of the expansionary phase of the credit cycle coinciding with trade protectionism has damaged global trade very severely, and the effects are now extending into domestic economies. This being the case, we can expect a renewed acceleration of monetary inflation. While supporting government finances through new bouts of quantitative easing, the wealth-transfer effect of monetary inflation will increasingly undermine the productive economy.

That is why gold and bitcoin prices could turn out to be an early warning of an acceleration in the rate at which fiat currencies will lose purchasing-power. If leading nations through their central banks fail to protect their currencies, then these two alternatives to fiat currencies will have only just started to rise.

via ZeroHedge News https://ift.tt/2YI0u16 Tyler Durden

On July 1, many – us included – wrote lengthy articles, pointing out that the longest US economic expansion in history is now a fact.

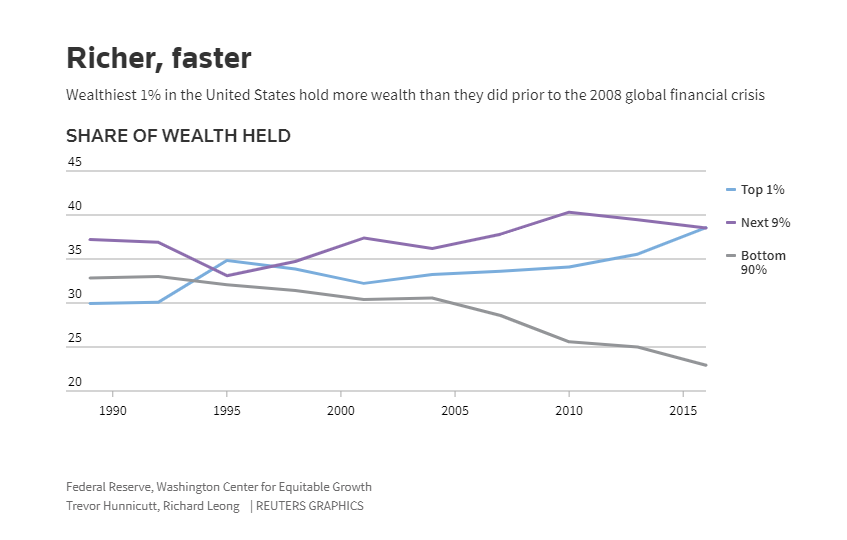

Sadly, when peeling back the layers of the centrally-planned onion, the reality is far less euphoric, and as Reuters writes today, this historic expansion – mostly of asset prices – achieved just one thing: it made the rich richer while crushing the middle class, with Reuters reporting that the number of billionaires in the United States has more than doubled in the last decade, from 267 in 2008 to 607 last year.

John Mathews, Head of Private Wealth Management and Ultra High Net Worth at UBS said: “The rich have gotten richer and they’ve gotten richer faster. The drive or the desire for consumption has just gone upscale.”

At the same time, the signs of struggle and stagnation for lower income levels have also been presenting themselves. The wealthiest 20% of Americans hold 88% of the country’s wealth, a share that has grown since before the crisis. On the other end of the spectrum, “the number of people receiving federal food stamps tops 39 million, below the peak in 2013 but still up 40% from 2008 even though the country’s population has only grown about 8%” as the middle class was crushed and as millions dropped out, and down, into the lower class.

Regardless, 10 years ago, this kind of growth wasn’t thought possible. The financial system was teetering on the brink of disaster and people feared that bank failures could permanently undermine capitalism.But now, it looks as though many of the signs of the wealth that proceeded the financial crisis are again presenting themselves.

The report laid out a couple of examples of the wealth effect:

The cost of a dinner at the French Laundry, the chic California restaurant, is up 35% to $325 per person, from $240 10 years ago, beating inflation by nearly 20%.

Undergraduate tuition at Ivy League mainstay Columbia University is a hair under $60,000 a year, up by half from $39,000 in the 2008 school year.

The U.S. stock market, measured by the S&P 500, has tripled in the last decade.

Hedge fund boss Ken Griffin set a record for a U.S. home sale when he bought a $238 million penthouse condominium on “Billionaires’ Row” just off New York City’s Central Park.

However, rents in places like New York have risen more than twice as fast as wages, which puts pressure on lower income residents. And the amount of people sleeping in New York’s shelters is 70% higher than it was 10 years ago, as the ranks of the homeless soar.

Carolyn Valli, CEO at Central Berkshire Habitat For Humanity, in Pittsfield, Massachusetts said: “Under-resourced areas are not getting any better; the housing opportunity for them is not getting any better. High healthcare costs and a lack of large employers mean fewer jobs in some areas. Food, utilities and housing costs, meanwhile, remain high. It doesn’t feel like a boom yet.”

The widening inequality gap continues to be a popular topic among Democratic presidential hopefuls as policymakers are starting to believe that the expansion could be on the precipice of slowing down. Many worry that as rates start to tick up and the US continues its trade war with China that a fragile lower income citizen could be put into an even more precarious financial situation.

But naturally, this didn’t stop Federal Reserve Chairman Jerome Powell from recently stating: “The benefits of this long recovery are now reaching these communities to a degree that has not been felt for many years. Many people who in the past struggled to stay in the workforce are now getting an opportunity to add new and better chapters to their life stories. All of this underscores how important it is to sustain this expansion.”

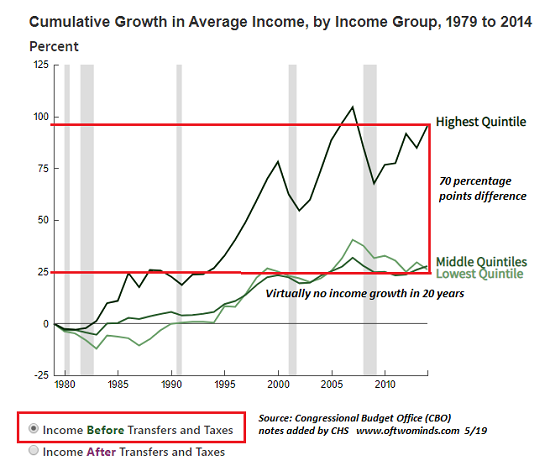

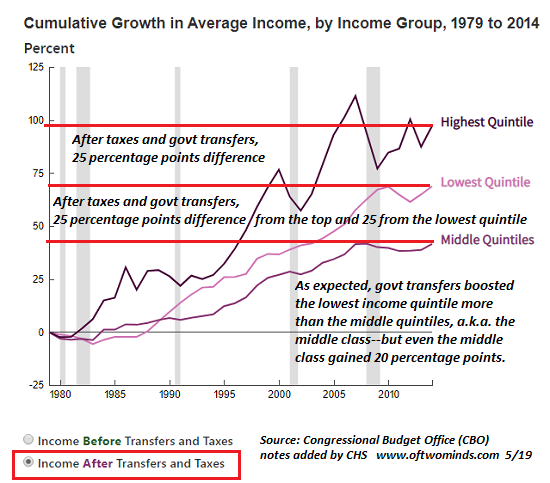

We’re guessing Powell didn’t read our recent article about income inequality and the decline of the middle class. It includes these two charts that are so simple, even a Fed chair could understand them.

via ZeroHedge News https://ift.tt/2XvpnQU Tyler Durden

While the media and other leftist elites ignore the millions of folks living in “flyover” states, they do so at their own peril; it was this silent majority that put President Trump in the White House. Each week, Liberty Nation gives voice to the hard-working heartlanders who are silent no more.

They stood for the flag, hats in hands over hearts, as the local high school band played a John Phillips Souza march on Independence Day. Bar-b-ques fired across the heartland as flyover folks spoke about the freedoms of America and the sacrifices that were made to achieve them, followed by community fireworks displays and children running with sparklers and tossing pop-its as the day drew to a close.

Independence Day in the heartland was celebrated. But it was also met with concern by those who believe an anti-American faction has invaded our government and is undermining the unprecedented gift the Founding Fathers bequeathed to this nation.

The list of grievances ranged from what flyover folks saw as outright lies from a New York congresswoman to the extreme error in judgment perpetrated once again by an American corporation caving to an angry and historically ignorant demographic.

She Speaks, She Lies?

Rep. Alexandria Ocasio-Cortez (D-NY) once again decided that facts were second to what she defines as a moral obligation. Living up to her remarks from earlier this year – “I think that there a lot of people more concerned with being precisely, factually and semantically correct than about being morally right.” – A-O-C felt “obligated” to accuse several members of the U.S. Border Patrol of lewd and lascivious and threatening behavior towards her as she sort of visited a detention center at the border. “Sort of visited,” as several witnesses claim she never set foot inside the Texas facility.

Officials and a group of Hispanic pastors tell a much more likely tale – that it was Ocasio-Cortez who launched a disrespectful tirade against federal employees and made up outrageous lies when facing the press. Flyover folks were not surprised and certainly not amused.

Alexandria Ocasio-Cortez

Amanda Lindquist wondered, “How would she know? She sat outside taking pictures of herself crying at a parking lot,” to which Paula Taylor observed, “She is such a bad actress.”

Nancy Couch Mackay from Michigan weighed in with, “So she can make up any bull she wants make accusations without proof and face no consequences for flat out rabble-rousing and slander?”

But others basically said, “bless her heart,” which translated to she’s brainless to begin with and should require our pity. JFE Hillen reminded Americans to be gentle: “Be kind to A-O-C. She recently discovered the use of her apartment’s garbage disposal. Learning to identify and properly use a toilet is a big step for her.” But Mark Russell was having none of Hillen’s advice, replying, “For whatever reason and without knowing much about her, I kind of liked her at first. I’m now rapidly realizing the woman is a box of rocks.”

Nike, Oh Nike

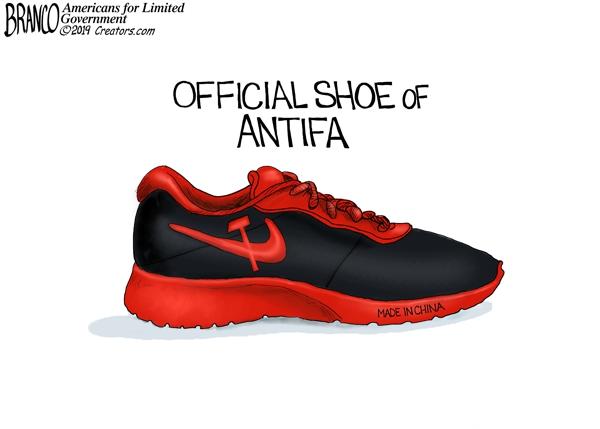

Back in the news – perhaps realizing it hasn’t ticked off any patriotic Americans of late – Nike caved to its whiny spokesman, the former midlevel football player, Colin Kaepernick, who bawled like a newborn calf over the Revolutionary War flag – a banner that distinguished rebels from followers of the tyrannical crown in England.

The flag was on a tennis shoe – and apparently, this had the wild-haired Kaepernick seeking a safe space.

Texan Kathleen Thornell Bowings threw in with, “I don’t buy Nike products….never have, never will. The flag symbol was used to stir up the pot of haters for America. I am thankful for those that founded this country, the men and women that have fought, and died, to give me the right to live in freedom from oppression. God Bless the USA!”

If you’re offended by a shoe celebrating the flag of the American Revolution, it’s a good indication that you may be better off living in a permanent safe space.

DuWayne Orth agreed with the good Congressman from Texas, Dan Crenshaw (R-TX), and added a few additional garden spots for consideration: “I think Kaepernick should move to Venezuela, Cuba, Iran, North Korea, Russia, or Afghanistan. Ya know, to get a better understanding of what oppression really is.”

James Holdren saw dollar signs and narcissism that led to this latest ploy by the show manufacturer. “It’s not the flag he just wants his name on the internet,” he opined. “It’s for the attention and nothing else. I hope Nike goes completely out of business.”

And Holdren may have gotten his wish as Ohioan Tom Beery reported that “NIKE died this week. Initial cause was reported as Colin Cancer.” Charlie Eastman brought it home: “People have no idea how much damage Obama did to America in 8 years of transforming our great nation.”

Perhaps we should view the divide in this nation as empathy finally leaving the electorate. It appears few are on the sidelines and all are readying for battle. Patriots, my readers, still exist – and they have a winnable platform.

via ZeroHedge News https://ift.tt/2JsyhVt Tyler Durden

Emergency responders are combing through rubble looking for possible trapped victims after a massive blast reduced a chunk of a large shopping center to rubble on Saturday at “The Fountains” shopping center in Plantation, just outside of Fort Lauderdale, Florida. It”s being reported that “multiple patients” are filling up local hospitals after what’s believed to have been a gas explosion, according to early reports.

“There was a huge flash of light … it lit up the whole sky,” one witness told a local ABC affiliate. “And it was loud … this surpassed fireworks … your ears were ringing.” The eyewitness added:

“It just looks like an apocalypse.”

Image source: WLPG

The cause of the blast is as yet unknown, but early reports strongly suggest a ruptured gas line may have been the cause of the blast. Local police and firefighter officials have told ABC that while initially unconfirmed, “ruptured gas lines were found in the rubble”.

Via ABC/WLPG: First responders at the scene of an explosion at The Fountains shopping mall in Plantation, Fla., July 6, 2019.

CNN later confirmed in a follow-up report that “a gas explosion shattered parts of a shopping mall in the South Florida city…”.

WATCH: Video shows windows blown out of an LA Fitness gym and wreckage scattered across the ground after explosion at South Florida shopping center.

A police statement said, “All stores and businesses in the area of the Fountains Plaza and the Plantation Marketplace plaza near LA Fitness will be shut down until further notice until Fire Personnel can determine that it is safe to return. Please do not come into this area if possible.”

Fire officials indicated that about to 15 to 20 people were injured, including two seriously, however, the casualty count is expected to rise as first responders comb the scene.

Image source: WLPG

Social media users documented the aftermath of the carnage as confusion gripped the area. Police quickly began evacuating the area while searching for survivors and injured among the rubble.

“The whole building blew up,” one man is heard saying in a social media video cited by CNN.

Some passersby at time of the blast were injured by flying debris, including on person at a Tesla charging station seen in some of the images of the blast’s aftermath.

#Update: Just in – Confirmed at least 20 people are injured, following a Massive gas explosion at The Fountains shopping center in #Plantation, west of Fort Lauderdale in Broward County. pic.twitter.com/JlO44EYHBB

U.S. natural gas prices have collapsed since the end of winter, even as inventory levels remain below average levels for this time of year.

Henry Hub prices spiked in the fourth quarter of 2018 due to record levels of demand, cold weather, and historically low inventories. But prices remained elevated, over $4/MMBtu, for only a brief period of time. Production continued to soar, so traders were not overly concerned about market tightness.

As peak winter demand season drew to a close in March, prices continued to ease, and prices have eroded steadily in the last few months. Prices dipped below $2.30/MMBtu recently, hovering in that range for the first time in roughly three years. As recently as December, prices were twice as high as they are now.

What’s going on? The main driver of the bearish market is production, which continues to ratchet higher, even as shale gas drillers are suffering from financial strain. Production from the Marcellus shale alone was up about 15 percent in May from the same period a year earlier.

Gas markets also go through seasonal swings, seeing a peak in demand in winter and to a lesser degree in summer, while consumption falls sharply in spring and fall. But swings in temperatures from year to year can lead to significant disruption. A cool start to the summer this year led to lower demand than otherwise would be the case, allowing inventories to build back up.

In the last week in June, U.S. natural gas storage levels stood at 2,390 billion cubic feet (Bcf), up 89 Bcf from a week earlier. Storage was still 152 Bcf below the five-year average but 249 Bcf higher than last year, which helps explain why prices recently fell off a cliff. Stocks have replenished, at least relative to last year.

The multi-year low for natural gas prices are likely to deal a further blow to the coal industry, already caught in a death spiral. At least three coal companies have filed for bankruptcy since May, potentially putting 2,000 mining jobs at risk. Coal has a hard time competing with natural gas prices this low.

But low gas prices is also bad news for the gas industry itself. Recently, a former executive at EQT, one of the country’s largest shale gas producers, said that fracking has been an “unmitigated disaster” for the industry, depressing prices and leading to consistent losses. “And at $2 even the mighty Marcellus does not make economic sense,” Steve Schlotterbeck, the former EQT executive said at an industry conference last month. “There will be a reckoning and the only questions is whether it happens in a controlled manner or whether it comes as an unexpected shock to the system.”

The gas rig count continues to decline, recently falling to 173 in the last week of June, down from over 200 at the start of the year.

Meanwhile, overseas gas markets are also suffering from oversupply and low prices. A wave of new LNG export terminals are coming online in 2019, and LNG prices have tumbled. In the all-important market in East Asia collapsed this year, with JKM prices falling below $5/MMBtu, the lowest level in years. Traders clearly do not see things improving much going forward. While front-month JKM prices are trading at $4.58/MMBtu right now, contracts for August 2023 are only trading at $5.93/MMBtu. Oversupply could stick around for years, if this outlook bears out.

In Europe, too, gas markets are oversupplied. Higher volumes of LNG are arriving on European shores at a time when Russia is hoping to defend market share. “As two of the world’s largest gas producers, Russia and the US are natural competitors in what seems to be a race to the bottom, not only in the lucrative Asian market but now also in Europe. Both countries have sent increasing amounts of gas to Europe despite the low price environment,” Carlos Torres-Diaz, head of gas markets research at Rystad Energy, said in a statement.

“Some US exporters are not covering their operational costs. Nevertheless, US exports to Europe during the first five months of 2019 increased by 6.9 Bcm versus the same period last year,” Torres-Diaz said.

via ZeroHedge News https://ift.tt/32aBJN1 Tyler Durden

Texas Democratic Rep. Veronica Escobar (D) has reportedly been sending staff members into the northern border town of Ciudad Juárez to track down migrants ejected from the United States under the “remain in mexico” policy, and coach them on how to exploit a legal loophole that would allow them back into the USA.

According to the Washington Examiner‘ Anna Giaritelli, the Texas Democrat’s office is working in conjunction with the local Catholic diocese – telling the migrants to pretend they cannot speak Spanish – as US law requires fluency in order to legally deport them.

The National Border Patrol Council’s El Paso chapter and several Customs and Border Protection personnel told the Washington Examiner aides to Rep. Veronica Escobar, who took over 2020 Democratic presidential candidate Beto O’Rourke’s district, and the local Catholic diocese have interviewed thousands of migrants in Juarez over the past few weeks to find cases where Department of Homeland Security officials may have wrongly returned people. –

…

Under the bilateral Migration Protection Protocols, or “Remain in Mexico” policy, anyone returned must be fluent in Spanish because they may have to reside in Mexico up to five years until a U.S. federal judge decides their asylum claim. A Democratic politician’s aides reescorting people back to the port are telling officers the Central American individual with them cannot speak Spanish despite their having communicated in it days earlier, CBP officials said. –Washington Examiner

According to the report, “Escobar’s team has sought interviews with 6,000 people who were returned last month.”

“What we believe is happening is Veronica Escobar’s office is going … to basically second-guess and obstruct work already done by the Border Patrol,” one senior union official told the Examiner, sharing evidence from concerned CBP managers as well as rank-and-file members.

“What we’re hearing from management is that they’re attempting to return people, and the story was changed in Mexico, where a person who understood Spanish before now doesn’t understand — where a person who didn’t have any health issues before now has health issues,” added the union rep.

“They went through and interviewed everybody, cherry-picked them, brought them back, and now are using them as tag lines. They’re going over there and manufacturing a lot of these issues.”

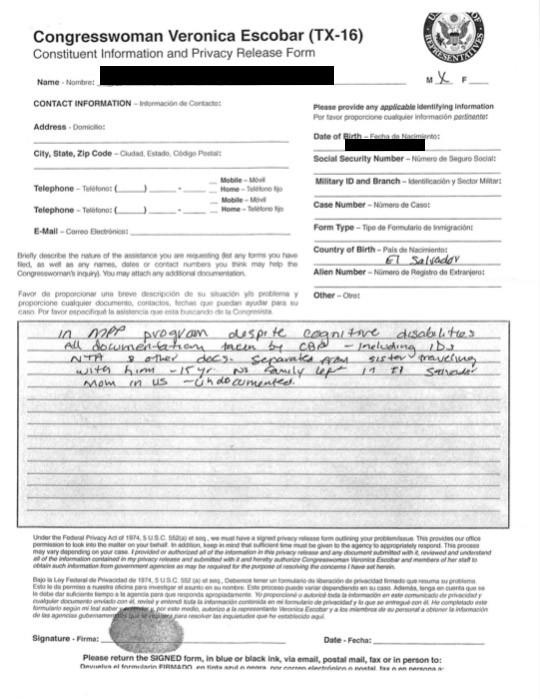

In one incident, an Escobar aide and diocese official walked a male migrant over the bridge in June and asked for him to be admitted into the U.S. because they had found he had “cognitive disabilities.” Officers took the boy and turned the case over to the Border Patrol, where an agent found a Constituent Information and Privacy Release Form with the U.S. House of Representatives seal on it inside the 17-year-old’s file. Two officials said the paper would have to have been put in his file while he was interviewed in Mexico and was not supposed to have been left there because it would reveal to the Border Patrol that a member of Congress or their staff was meeting with migrants in Mexico.

The boy has since returned to Mexico because the medical condition was not diagnosed by a medical professional but by an aide of the congresswoman, one official said Friday. –Washington Examiner

“Management saw that form and was like, ‘What is this?’ and reached out to our International Liaison Unit. And ILU said, ‘Yes, Veronica Escobar and several other politicians are in Mexico trying to defeat the MPP program,'” said the union rep.

The border officials who approached the Examiner on condition of anonymity all feel that the interviews might be used to make the case that the Border Patrol is wrongfully deporting or turning away large numbers of asylum-seekers.

“We had finally found a happy medium ‘cause we always get crapped on when it comes to immigration laws, and then they’re finding loopholes to bring them back,” said a second official.

Mark H. Metcalf, a former federal immigration judge during the George W. Bush administration, said the involvement of Escobar’s office was likely “more of a stunt than a genuine threat to the integrity of the process.“

“She’s trying to obviously say these people have been wrongly denied their claims and they’re waiting when they shouldn’t be,” said Metcalf.

However, he said a criminal case would exist if Escobar were found to be complicit in an effort to perpetrate a fraud, which would have to include knowingly injecting false statements during interviews, follow-up conversations, and documents presented to U.S. officials.

One Homeland Security official aware of the situation said that Democrats are “furious” that migrants aren’t allowed to “await their court dates in the US, where they have the opportunity to disappear and slip into the interior never to be seen again.”

“By opposing a system that assists migrants and speeds wait times, these individuals are exposing a cause that looks more like a cover story for their political motivations. Any efforts to subvert and obstruct federal law enforcement operations should receive a full review,” the official said in a text.

“Resources are being diverted into a foreign country in an attempt to reverse already-decided legal action, meaning these people were found inadmissible under a new program and they must remain in Mexico. They’re trying to subvert that.”

via ZeroHedge News https://ift.tt/2xISIYZ Tyler Durden

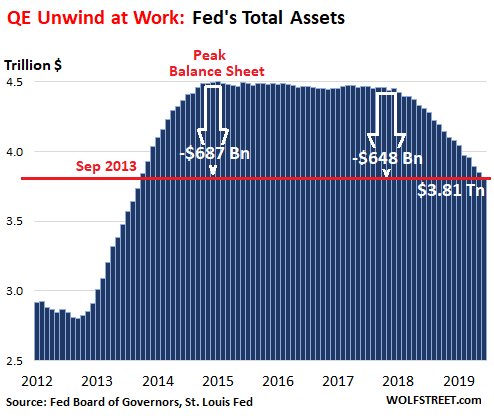

Where is the Fed’s “U-Turn” that Wall Street promised us?

In June, the Fed shed Treasury securities at the slower pace announced in its new plan for QT, but it dumped Mortgage Backed Securities (MBS) at the fastest rate since the QE unwind started, breaching its “up to” cap for the first time. And it is experimenting with the opposite of its QE-era “Operation Twist” – Operation Untwist?

Total assets at the Fed fell by $34 billion in June, as of the balance sheet for the week ended July 3, released Friday afternoon. This includes $15 billion in Treasury securities and a record $23 billion in MBS, for a total of $38 billion, less some other balance-sheet activities unrelated to the QE unwind. This trimmed its total assets to $3.813 trillion, the lowest since September 2013. Since the beginning of the “balance sheet normalization” era, the Fed has shed $648 billion. Since peak-QE in January 2015, it has shed $687 billion:

Treasury Runoff.

The Fed doesn’t sell its Treasury holdings outright. But when securities mature, the US Treasury Department pays them off, and the Fed then doesn’t reinvest this money in new securities. Instead, it destroys this money in the reverse manner in which it created it during QE. But the Fed has announced caps — the “up to” amounts. If the amount of Treasuries that mature in a given month exceed the cap, the Fed reinvests the overage in new Treasuries. Under the Fed’s new regime, the maximum amount of Treasury securities allowed to roll off when they mature was $15 billion in June. And that’s what happened.

In June, three issues matured, for a total of about $21 billion. The Treasury Department redeemed them and paid the Fed for them. The Fed reinvested $6 billion of this money into new Treasury securities but allowed $15 billion to roll off without replacement. So the balance of Treasuries dropped by $15 billion, to $2.095 trillion, the lowest since September 2013:

“Operation Untwist”

Over the past couple of months, the Fed began replacing longer-term Treasury notes with short-term Treasury bills. It’s the reverse of “Operation Twist,” which had been part of QE, layered between QE-2 and QE-3. During Operation Twist, it had replaced its short-term T-Bills with longer-term T-Notes and T-Bonds in order to force down the recalcitrantly high long-term yields.

Now it is starting to do the opposite, albeit in only small amounts. Short-term bills cropped up for the first time on its May-dated weekly balance sheets. In the current balance sheet, it lists $5 million, with the first batch maturing on July 9, the second batch in August. The Fed seems to be testing what it said would be implemented after September: Replacing long maturities with short-term bills to bring down the average maturity of its portfolio.

If Operation Twist worked to bring down long-term yields during QE – doubts remain – then “Operation Untwist” should do the opposite and put upward pressure on long-term yields.

Mortgage-Backed Securities

MBS securities differ from regular bonds: Holders receive pass-through principal payments as the underlying mortgages are either paid down through monthly mortgage payments or are paid off when the home is sold or the mortgage is refinanced. Any remaining principal is paid off at maturity.

About 95% of the residential MBS on the Fed’s balance sheet – they’re issued and guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae – mature in over 10 years. So the current runoff is almost exclusively due to pass-through principal payments.

These pass-through principal payments vary with movements in mortgage interest rates: Falling mortgage rates induce homeowners to refinance their mortgages, which means that their old mortgages are paid off, and the principal is passed through to the holders of MBS.

Mortgage rates had hit a multi-year high last November, and mortgage refi applications dropped to a decade-low in December. But mortgage rates have since skittered lower, and refi applications have surged, according to the Mortgage Bankers Association. And the flow of pass-through principal payments has surged too – and the Fed is taking advantage of it.

In June, the balance of MBS fell by $23 billion to $1.533 trillion. This was not only the biggest run-off since the QE unwind started but it also exceeded the $20 billion cap – another first! In May, the run-off had hit the cap of $20 billion for the first time, but didn’t exceed it:

The action on MBS confirms that the Fed is eager to get rid of them as soon as possible. Its new plan calls for getting rid of all of them, even if it has to sell them outright if pass-through principal payments slow down too much, as it said. Starting late this year, it will begin to replace MBS with Treasuries. Meanwhile, the Fed is making hay while the sun shines – given the surge in mortgage refis and pass-through principal payments and the prospect that when mortgage rates snap back, this flow of pass-through principal payments slows down.

Let me just throw this out there for us to kick around: The Fed has already accomplished more with its verbiage so far this year than it had in the past when it cut rates all the way down to zero and did trillions of dollars of QE. We’re already seeing the first results. Here’s why. Read… The Fed’s Stealth Stimulus Has Arrived

Some reports are already calling it the ‘smoking gun’ in the ongoing conflict between Washington and Beijing centered on Chinese telecom giant Huawei, and accusations that it’s tied closely to Chinese military and intelligence, as a way for Beijing to infiltrate and spy on western governments and US companies.

Now, a “massive trove” of newly leaked records of Huawei employees appear to show “far closer links” between the private company and military-backed cyber agencies than previously known, according to The Telegraph. This follows on the heels of the discovery of academic research documents also confirming close cooperation between Huawei employees and the People’s Liberation Army (PLA) uncovered by Bloomberg last month, as we previously reported. The new trove of employee CVs contains some 25,000 records analyzed by Fulbright University’s Christopher Balding and UK-based Henry Jackson Society researchers (which, it should be noted, is a hugely controversial neocon think tank).

Huawei has long been accused of working closely with military-backed cyber agencies. Image via Reuters

Yet in spite of the growing mountain of documented evidence, the company line has remained, “Huawei does not have any R&D collaboration or partnerships with the PLA-affiliated institutions,”as stated by Huawei spokesman Glenn Schloss less than two weeks ago. “Huawei only develops and produces communications products that conform to civil standards worldwide, and does not customize R&D products for the military,” he added, as cited in Bloomberg.

Huawei’s defense following that prior report was to say the joint research publications were “not authorized”— but the newest revelation places cooperation with the PLA even closer, per a new bombshell report:

According to the study, the employment files suggest that some Huawei staff have also worked as agents within China’s Ministry of State Security; worked on joint projects with the Chinese People’s Liberation Army (PLA); were educated at China’s leading military academy; and had been employed with a military unit linked to a cyber attack on US corporations.”

Analysts are calling it confirmation of a “systemized, structural relationship” between the PLA, Chinese intelligence, and Huawei.

The company has responded by pointing out it’s common to have an employee revolving door of sorts between the private and public sectors (as does Washington), and that personnel CVs will reflect this reality.

Source: Getty Image

However, many employees’ prior postings within China’s intelligence apparatus are shockingly high level and at the heart of the PLA’s cyber-spying operations. As Forbes summarizes of the findings:

One example given is for a current employee whose previous posting was with the National Information Security Engineering Centre, which Reuters has linked to the PLA’s Unit 61398—“the unit has been accused of being at the heart of China’s alleged cyber-war against Western commercial targets.”

Some employees have links to the Chinese Ministry of State Security (MSS), which the report points out “is the primary entity responsible for espionage and counter-intelligence. It should raise immediate concern that MSS assets are working on networking equipment as representative agents for Huawei.”

And further examples from the trove of documents are as follows:

Analysis of the CVs found 11 Huawei staff graduated from the PLA’s Information Engineering University, a military academy reputed to be China’s centre for “information warfare research”.

CVs are full of references to military backgrounds among Huawei employees:

Prof. Balding, in conjunction with the Henry Jackson Society, a London-based think-tank, concluded that about 100 Huawei staff had connections with the Chinese military or intelligence agencies and their “backgrounds indicated experience in matters of national security”.

In a number of instances employees at the managerial level maintain simultaneous roles in PLA operations and the private telecom giant:

The study claims that one Huawei project team leader refers on his CV to work on joint projects between the telecoms company and the Chinese Army’s National University of Defence Technology, one of China’s leading military academies and was put on a U.S. list, banning American firms from selling it technology in 2015, under Barack Obama’s presidency.

Another Huawei employee’s CV says she works both at the telecoms giant as a software engineer and also at the Radar Academy of the Chinese Army. The academy, says Prof. Balding, “matches closely her work for Huawei”.

…The study links another Huawei engineer, who has worked in Europe, to being a “representative” of the Ministry of State Security, China’s intelligence agency.

A HJS investigation has revealed, contrary to Huawei’s claims, its employees claim on their own CVs to be working on “MSS” projects and cooperating with the PLA. https://t.co/XjpBwRh6ql

And crucially, at least one telecoms engineer involved in Huawei’s controversial next generation 5G broadband roll out has a CV which heavily restricts information “due to the involvement of military secrets”:

A further CV reveals a senior Huawei engineer worked on “a database-driven surveillance system capable of accessing every citizen’s record and connecting China’s security organizations” — otherwise known as the “Great Firewall of China”.

One more CV shows a Huawei telecoms engineer involved in development of 5G “base stations” who says on his CV that he cannot comment on his previous employment “due to the involvement of military secrets”.

One of the chief researchers involved in analyzing the employment records said, “These CVs are a treasure trove”; however, in light of the report’s release Huawei maintains a nothing to see here stance, likening the findings to the parallel situation of former NSA contractors rotating between the public and private sectors in the US.

A Huawei spokesperson quoted in Forbes said “this information is not new and is not secret, being freely available on LinkedIn and other career web sites. It is also not unusual that Huawei, in common with other tech companies around the world, employs people who have come from public service and worked in government. We are far more competitive thanks to our colleagues’ previous experiences. We are proud of their backgrounds and we are open about them.”

Is this indeed the Huawei-PLA intelligence smoking gun, or just business as usual for a major tech giant in an industrialized, militarily powerful nation?

via ZeroHedge News https://ift.tt/2Nz08sd Tyler Durden

Despite all the grousing and griping about his “politicizing” of the Fourth of July and “militarizing” America’s birthday, President Donald Trump turned the tables on his antagonists, and pulled it off.

As master of ceremonies and keynote speaker at his “Salute to America” Independence Day event, Trump was a manifest success.

A president acting as president is almost always a more effective campaigner than a president acting as campaigner. And Trump, in what he said and did not say, played the president Thursday night.

The crowd on the Mall was huge and friendly, extending from the Lincoln Memorial to the Washington Monument. The TV coverage was excellent. Friday, virtually every major newspaper had front-page stories and photos.

Earlier, former Vice President Joe Biden had snidely asked, “What, I wonder, will Donald Trump say this evening when he speaks to the nation at an event designed more to stroke his ego than celebrate American ideals?”

Thursday evening, Joe got his answer.

Despite predictions he would use “Salute to America” for a rally speech, the president shelved partisan politics to recite and celebrate the good things Americans of all colors and creeds are doing, and the great things Americans have done since 1776.

“Together, we are part of one of the greatest stories ever told — the story of America,” said Trump. “It is the epic tale of a great nation whose people have risked everything for what they know is right and what they know is true.”

It was not a celebration of Trump but of America.

“What a great country!” declared the president. “(F)or Americans nothing is impossible.” Ours is “the most exceptional nation in the history of the world.”

The second half of Trump’s speech was given over to tributes to the five branches of the armed forces — Coast Guard, Air Force, Navy, Marines, Army — with each tribute ending in a display of air power.

The flexing of America’s military muscle had evoked early howls of protest. But the flyovers of F-22s and F-35s, the B-2 stealth bomber and the Ospreys, and the culmination of the aerobatics with the Navy’s Blue Angels, as the Marine Corps band played and all sang the “Battle Hymn of the Republic,” was exhilarating, even moving.

It was positive, uplifting, patriotic. And one imagines that not only Trump’s “deplorables” standing on the Mall loved it.

Still, one wonders: Where is all this negativity, this constant griping and grousing by the left, going to lead? Do these people think America will turn with hope to a party that reflexively recoils at patriotic displays?

Everywhere it seems the left is attacking America’s history and her flawed heroes. Monday, the Charlottesville City Council voted 4-1 to remove April 13, the birthday of Thomas Jefferson, as a paid holiday.

Why? Because our third president was a slave owner. The council’s public comment period featured demonstrators accusing the author of America’s Declaration of Independence with having been a racist and a rapist.

Last week, too, ex-NFL quarterback Colin Kaepernick urged his sponsor, Nike, to pull off the market its new Air Max 1 Quick Strike Fourth of July sneakers featuring Betsy’s Ross’s first American flag on the heel. Says Nike, Kaepernick told the company he finds the colonial flag offensive, as it was flown when slavery was still legal.

Just how far and fast the Democratic Party is moving left became clear last week with some startling findings of a new poll.

According to Gallup, while 76 percent of Republicans say they are “extremely proud” to be an American, only 22 percent of Democrats say the same, a sharp drop from last year. In 2013, the beginning of Obama’s second term, 56% of Democrats said they were “extremely proud” to be Americans.

Another jolting note: While huge majorities of Americans — 9 in 10 — are extremely proud of the U.S. military and America’s scientific achievements, more than two-thirds of all Americans now say that our political system no longer makes them proud.

This is especially true of Democrats. Only 25 percent, 1 in 4 Democrats, professes to be proud of our political system, our democracy.

A specter of anti-Americanism appears to be rising on the left.

Listening to the Democratic debates, and the depiction of the nation and its economy by the candidates, one would think we were living in the Paris of “Les Miserables” or the London of Charles Dickens.

Demography undeniably favors a millennial-dominant Democratic Party over the middle-aged and seniors party that is the GOP.

Yet how does a party, 3 of 4 of whose adherents profess no pride in its political system, persuade the nation to put it in charge of that system? How does a party, not one-fourth of whom are “extremely proud” to be an American, persuade a majority of Americans to entrust it with the leadership of their nation?

From liberals and progressives, we constantly hear griping, grousing and grievances. When do we hear the gratitude — for America?

via ZeroHedge News https://ift.tt/329DVUY Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}