In what will almost certainly be remembered as one of the most chaotic weeks for global markets in recent memory due to the unceasing flow of trade news, global stocks were back in risk-off mode Thursday after a seemingly offhanded remark by President Trump during a MAGA rally last night doused the sense of optimism that had prevailed earlier in the day.

But with the Chinese delegation having arrived in Washington, more reports published late Wednesday and early Thursday have offered new insights into why Beijing decided to play hardball, and how Washington is planning to show that it means business while stopping short of torpedoing any accumulated goodwill with new tariffs.

Though paperwork filed by the Trade Representative’s office on Wednesday suggests that tariffs will almost certainly rise on Friday, the administration has apparently come up with an important caveat that could allow negotiators more time: The new tariff rates won’t apply to goods already in transit, which would give negotiators up to a month to work out a deal before the new rates take effect, according to the FT.

The clarification offers US and Chinese negotiators a window of two to four weeks to reach a deal before the bulk of the pain from the higher tariffs hits US consumers and businesses, based on shipping times between the countries.

On Wednesday morning, Mr Trump noted on Twitter that Mr Liu was still coming to the US capital to “make a deal.”

The president’s latest tweets were posted just before the US equity markets were set to open after two days of losses driven by the flare-up in trade tensions with China. US stocks were volatile but trading slightly higher on Wednesday compared to earlier in the week.

Meanwhile, in a lengthy piece purporting to explain why Beijing decided to start playing ‘hardball’ so late into the talks (though, to be sure, other reports suggest that Beijing had taken a hard line almost from the start), WSJ claimed that President Xi and the senior leadership interpreted Trump’s attacks on Fed Chairman Jay Powell as a sign that Trump would be ready to compromise.

The reason? It was interpreted as evidence that Trump secretly believed the US economy was more fragile than the official data reflected. Meanwhile, the Chinese economy has stabilized, in part thanks to a massive stimulus program.

Beijing was further emboldened by Trump’s professions of ‘friendship’ with Xi, and his praise for Liu. Then, an April 30 Trump tweet praising Chinese economic policy cemented this view, according to WSJ’s sources.

An analyst quoted in the WSJ piece offers an apt summary: “Why would you be constantly asking the Fed to lower rates if your economy is not turning week?”

That’s a great question. We’re still waiting for an explanation on that one.

A spokesman for MOFCOM on Thursday rejected US accusations that Beijing had reneged on its promises, which is what allegedly prompted Trump’s tariff threats. Beijing has vowed to retaliate to any new tariffs out of Washington, but the takeaway from Thursday’s reports is that even if a deal doesn’t happen Friday (which it almost certainly won’t), the trade negotiations will remain an intense market focus for at least the next two weeks, until the new rates take effect.

At any rate, we imagine the WSJ report was at least a small consolation to Powell, who has now been partially vindicated for his slightly hawkish tilt during the post-FOMC press conference earlier this month.

via ZeroHedge News http://bit.ly/2VbFvRI Tyler Durden

There is nothing to worry about in trade negotiations. Apparently, all the flubber and fluster in global markets is due to a simple misunderstanding: The Chinese thought Trump asking the Fed to ease rates was a sign of US economic slowdown which encouraged them to row back on some of their earlier commitments. And, with Chinese numbers not quite as bad as the spooks thought they were, the US side had also overplayed its hand.

Silly. They will all be laughing about it tonight when Lie He arrives in Washington to smooth it all out. Imagine not understanding each other. The talks continue.

Or do they?

Lines have been drawn. The Chinese aren’t happy. The Americans are… well what are the Americans..? There seem to have been “communication issues” in the mixed messages Trump’s fractured administration has delivered. I read each word of Donald Trump’s tweets translated into $13 bln less on the stockmarket – and he was still blaming the Chinese at a rally last night while tweeting he’s willing to keep tariffs in place for longer than sign a bad deal. “China Broke The Deal” That’s hardly diplomatic, and didn’t he tell us a trade deal was the easiest thing in the world?

Although the Chinese arrive in Washington tonight, 10-25% tariffs will still be slapped on Chinese imports Friday morning with another $325mm to follow. Do the Chinese care? Probably not that much aside from it being a matter of face – Xi can’t be chums with a guy who has insulted China. Global supply chains being what they are, the hikes will be passed to straight to US consumers to pay – but with inflation so low, what’s to worry about.

Actually, the US might have quite a bit to worry about. If US consumers pay for the China tariffs – and they will – then weakening consumer sentiment is just one thing. Last thing the soar-away US market needs is a sharp-intake of air from retail, and a consumer spending clampdown reminding them just how weak commercial property and retail malls are.

And how do the Chinese respond to the new tariffs? By putting duties on US goods? I suspect Chinese consumers will prove more patriotic than their US counterparts – and who needs a reason to buy fewer US imports from cars to planes? (Hogs are another matter – we suspect the Chinese authorities are withholding just how badly African Swine Flu has compromised China’s main source of protein.)

I read Moody’s saying China retaliation could trigger unemployment and a 1.8% decline in US GDP. (With all things rating agency, discount these numbers dramatically..)

Yet the markets, deep down, still expect the US and China are going to reach a trade accommodation in the near future, and none of the bad things will happen.

What if we don’t get a deal, and the bad things start to happen..?

Under a simple No-deal scenario; The positive market start to 2019 will reverse as it was fuelled by trade optimism. US inflation increases, the Fed undoes its neutral stance and stands ready to address inflation and the market perceives this as profoundly negative. Stock market stalls, and bond yields rise catching duration extended investors out. Agri-voters get angry and lash out at Trump.

Maybe it gets more complex.

More than a few blogs have wondered about the US Right. They suggest part of the US power complex would rather push China than find a trade solution. Years of IP and US military secrets theft has infuriated the Pentagon. They know China’s massive Red Army is a paper tiger today – unable to stage more that demonstration against US forces. Imagine if they were thinking it’s a good time to face-up to China now, force them to stand down, and pin them back geopolitically across the globe?

That would need to happen before China can reform and create a military capable of the significant force projection needed to back its attempt to capture global infrastructure through the “Belt and Road” initiative?

Just thinking out loud, but if Trump is looking for a way to play the tough guy as the “easy” China trade negotiations stumble, maybe he’s listening to others? I wonder what the Generals and Admirals think? And what about the China Hawks? If they are telling him the US economy is in fine shape and positioned to withstand a trade escalation….

Who knows what goes on in Washington? Damn sure Trump doesn’t.

via ZeroHedge News http://bit.ly/309RNNS Tyler Durden

Florida lawmakers just voted to create a public registry of people caught paying or attempting to pay for sex.

After an initial defeat in the Florida House of Representatives, the registry—arguably the worst part of a new Florida crime bill capitalizing on human-trafficking propaganda—was revived and reinserted before the measure’s passage in the Florida Senate. The final version, approved last week, creates a database of convicted prostitution customers, targets strip clubs, and mandates that a slew of state workers and businesses jump through new hoops to accommodate a few politicians’ latest attempt to get their names in the press.

As the Florida Senate’s Committee on Community Affairs stated, the new registry “will collect and centralize information relating to those convicted of soliciting prostitution, regardless of whether the person subject to the solicitation is a victim of human trafficking or not.”

The Soliciting for Prostitution Public Database will list anyone who has been convicted of, or plead guilty, to “soliciting, inducing, enticing, or procuring another to commit prostitution, lewdness, or assignation.” The legislation specifies that the database should include a person’s name, photograph, address, and offense. Listed people who go five years without a subsequent offense could have their names removed.

“This isn’t creating a list of bad or dangerous clients; it’s just a list of clients who got caught by the police,” Kaytlin Bailey of Decriminalize Sex Work toldFilter. “It’s impossible to tell the good guys from the bad if you lump them all together. Men who pay for sex aren’t predators. Predators who pose as clients are. When you make potential clients scared of giving sex workers the information they need to screen, you make it impossible to tell the difference between men who are scared and men who are scary.”

The new measure also classifies strip clubs as “adult theaters”—then makes it a first-degree misdemeanor criminal offense for the operator of any adult theater to fail to keep proper records.

The law also creates wide new categories of workers and businesses that are required to make state-approved “anti-trafficking” curriculum part of employee training, continuing education hours, or occupational licensing schemes.

In Florida and elsewhere, this training has proven to be anti-prostitution and pro-surveillance propaganda disguised as tips for teaching bystanders how to prevent human trafficking. Officials get to collect fees for the training, or award funding for it to favored law enforcement and activist groups. Making sure businesses comply with training and awareness rules gives government officials a new reason to monitor them.

While it will certainly transfer private money to the state, give bureaucrats something to do, and provide the public with people to gawk at and judge, Florida’s “human trafficking” legislation does nothing for victims of actual sex trafficking.

from Latest – Reason.com http://bit.ly/2WzEGDt

via IFTTT

Florida lawmakers just voted to create a public registry of people caught paying or attempting to pay for sex.

After an initial defeat in the Florida House of Representatives, the registry—arguably the worst part of a new Florida crime bill capitalizing on human-trafficking propaganda—was revived and reinserted before the measure’s passage in the Florida Senate. The final version, approved last week, creates a database of convicted prostitution customers, targets strip clubs, and mandates that a slew of state workers and businesses jump through new hoops to accommodate a few politicians’ latest attempt to get their names in the press.

As the Florida Senate’s Committee on Community Affairs stated, the new registry “will collect and centralize information relating to those convicted of soliciting prostitution, regardless of whether the person subject to the solicitation is a victim of human trafficking or not.”

The Soliciting for Prostitution Public Database will list anyone who has been convicted of, or plead guilty, to “soliciting, inducing, enticing, or procuring another to commit prostitution, lewdness, or assignation.” The legislation specifies that the database should include a person’s name, photograph, address, and offense. Listed people who go five years without a subsequent offense could have their names removed.

“This isn’t creating a list of bad or dangerous clients; it’s just a list of clients who got caught by the police,” Kaytlin Bailey of Decriminalize Sex Work toldFilter. “It’s impossible to tell the good guys from the bad if you lump them all together. Men who pay for sex aren’t predators. Predators who pose as clients are. When you make potential clients scared of giving sex workers the information they need to screen, you make it impossible to tell the difference between men who are scared and men who are scary.”

The new measure also classifies strip clubs as “adult theaters”—then makes it a first-degree misdemeanor criminal offense for the operator of any adult theater to fail to keep proper records.

The law also creates wide new categories of workers and businesses that are required to make state-approved “anti-trafficking” curriculum part of employee training, continuing education hours, or occupational licensing schemes.

In Florida and elsewhere, this training has proven to be anti-prostitution and pro-surveillance propaganda disguised as tips for teaching bystanders how to prevent human trafficking. Officials get to collect fees for the training, or award funding for it to favored law enforcement and activist groups. Making sure businesses comply with training and awareness rules gives government officials a new reason to monitor them.

While it will certainly transfer private money to the state, give bureaucrats something to do, and provide the public with people to gawk at and judge, Florida’s “human trafficking” legislation does nothing for victims of actual sex trafficking.

from Latest – Reason.com http://bit.ly/2WzEGDt

via IFTTT

Four words from Donald Trump during his Panama City Beach rally on Wednesday night is all it took for the rug to be pulled from under markets: “China broke the deal” Trump said with Chinese Vice Premier Liu He on route to Washington for two days of talks, and then said another three to cement the sell-off: “They’ll be paying.”

And though Trump added that “it will all work out”, Beijing warned it will retaliate should the U.S. hike tariffs as advertised at 12:01am on Thursday against Friday. With traders already extra jumpy in a week in which the trade war tide reversed unexpectedly and furiously, that’s all it took to accelerate this week’s slide in risk, and world shares tumbled for a fourth day running on Thursday, the result a sea of red amid global markets…

… with S&P500 futures dropping again on Thursday, sliding as much as 0.8% as the deadline approached for America and China to raise reciprocal tariffs.

If talks indeed fail to reach a deal, Washington is set to raise tariffs on $200 billion of Chinese goods to 25% from 10% at 12:01 a.m. ET on Friday. Kazuhiko Fuji, senior fellow at RIETI, a Japanese government-affiliated think-tank, said the trade talks looked fragile.

“I would suspect the U.S. will just hand China an ultimatum. No wonder the U.S. yield curve is almost inverting again,” he said.

“Markets remain on edge ahead of the Chinese vice premier’s visit to Washington today,” Rabobank analyst Bas van Geffen said. “Doubt that this tariff increase can be avoided is growing,” he added as Goldman Sachs also put the chance of a hike at 60 percent.

“In the event of a complete breakdown in talks and higher tariffs, we would expect this to see U.S. stocks trade 10–15 percent below their highs and a fall of around 15–20 percent in the Chinese market,” Mark Haefele, global chief investment officer at Global Wealth Management at UBS, said.

With tariffs imminent barring a last minute miracle, the FT reported that US trade official said the additional tariffs on Chinese goods would apply to goods exported from Friday and will not include goods already in transit, which reports noted provides negotiators a window between 2-4 weeks before the full impact of higher tariffs.

As the flight from risk continued, Treasuries and the yen climbed with gold as investors sought havens, while the yuan fell to its weakest since January. European stock markets sank almost immediately after a torrid day for Asia. Europe’s Stoxx 600 hit session low shortly after the open, falling for the third time in four days, led lower by shares in cyclical sectors including automakers and miners, European tech stocks dropped as much as 1% dragged by a drop in semiconductor shares after Intel’s disappointing forecasts while banking stocks tumbled, with Banco BPM down 6.3% after disappointing quarterly results. The Stoxx 600 was down as much as 1.1%, its lowest level since March 29; the index has fallen 3.6% since hitting its peak in late April, on track to post its biggest weekly drop since December. There was broad based carnage in tech as well: wafer-maker Siltronic -3%, Infineon -2.6%, STMicro -2.6%, and AMS -1.6% all tumbled after Intel gave long-term forecasts for low, single-digit sales growth. Smaller European chip peer and Apple supplier Dialog Semiconductor gives up early gains to trade 0.3% lower after saying 2019 underlying revenue likely to decline this year.

Earlier in the session, Asian stocks fell for a fourth day, headed for their largest decline in six weeks led by technology and material firms; the rout was led by China, whose Shanghai Composite – which is often seen as the bellwether for how this trade war hits home – tumbled 1.5% while South Korea plunged 3%.

Most Asian markets were down, with Japan, South Korea and Hong Kong leading declines. The Topix gauge fell 1.4%, led by Toyota Motor Corp. and Honda Motor Co. The Shanghai Composite Index closed 1.5% lower, with Kweichow Moutai Co. and Ping An Insurance Group Co. among the biggest drags. The S&P BSE Sensex Index declined as much as 1%, as Reliance Industries Ltd. and HDFC Bank Ltd. contributed the most to losses.

Further hurting sentiment was the latest credit data out of China, where April money and credit growth decelerated from the rebound in March, with new CNY loans and total social financing below expectations. Overnight, the PBOC reported that new CNY loans were RMB 1020bn in April, below the RMB 1200bn expected, while Total social financing increased only RMB 1360bn in April, well below the RMB 1650bn consensus. According to the PBOC, TSF stock growth was 10.4% yoy in April, vs. 10.7% yoy in March. The implied month-on-month growth of adjusted TSF was 9.2% SA ann, lower than 11.5% in March.

In addition to trade headlines, traders will also be closely watching the pricing on ride-hailing firm Uber’s initial public offering, which is set to be the biggest of the year so far.

In the currency market, the Japanese yen surged to a three-month high of 109.64 yen as one-week yen volatility surged to its strongest level in four months, while China’s yuan fell half a percent to hit a four-month low of 6.838 and was headed for its worst four-day decline in a year as Australia’s currency falls on weak China credit growth data. A hawkish Norges Bank saw the krone climb against the euro even as faltering risk sentiment and depressed oil prices limited gains, after the central bank signaled a June rate hike. The pound was on track to wipe out last week’s advance against the euro as a Brexit deal resolution still proves elusive. Losses in sterling were limited as Prime Minister Theresa May earned a stay of execution from her Conservative Party.

In geopolitical news, following initial reports that North Korea had fired an unidentified projectile, further reports indicate this this was likely 2 short-range missiles. Prior to the further reports South Korea stated that it is unclear whether North Korea fired single or multiple projectiles.

In rates, Treasury 10-year notes jumped due to the escalation in risk-aversion, just hours after Wednesday’s auction saw the weakest demand for the benchmark bond in a decade. The yield spread between three-month U.S. government bonds and the 10-year notes shrank to 3 basis points, compared with about 15 basis points a few weeks ago. The spread first turned negative in late March, spooking investors, who read the development as portending a recession. The benchmark 10-year Treasury yield stood at 2.4529%, having touched its lowest level in five weeks of 2.426 percent on Wednesday before an especially poor 10Y auction sent the yield surging.

Commodity markets also felt the U.S.-China trade strains according to Reuters. Brent crude futures dropped 0.6 percent to $69.92 a barrel, while U.S. West Texas Intermediate crude also retreated 0.6 percent to $61.75 despite a surprise fall in U.S. crude stockpiles. London copper hit its lowest in nearly three months, going as low as $6,111 a tonne.

Expected data include PPIs, trade balance, jobless claims, and inventories. Canadian Natural Resources, Hydro One, Dropbox, and Yelp are among companies reporting earnings.

Market Snapshot

S&P 500 futures down 0.8% to 2,864.25

STOXX Europe 600 down 0.8% to 379.05

MXAP down 1.4% to 156.55

MXAPJ down 1.8% to 515.76

Nikkei down 0.9% to 21,402.13

Topix down 1.4% to 1,550.71

Hang Seng Index down 2.4% to 28,311.07

Shanghai Composite down 1.5% to 2,850.95

Sensex down 0.8% to 37,474.17

Australia S&P/ASX 200 up 0.4% to 6,295.33

Kospi down 3% to 2,102.01

German 10Y yield fell 1.5 bps to -0.059%

Euro down 0.07% to $1.1184

Italian 10Y yield fell 0.4 bps to 2.243%

Spanish 10Y yield fell 0.4 bps to 0.956%

Brent futures down 0.3% to $70.15/bbl

Gold spot up 0.3% to $1,285.02

U.S. Dollar Index little changed at 97.58

Top Overnight News

U.S. President Donald Trump declared China’s leaders “broke the deal” he was negotiating with them on trade, before adding that “it will work out.” Chinese state media warned that “fighting while talking” may become the new normal in trade relations with the U.S

China’s credit growth slowed more than expected in April after record expansion in the first quarter

North Korea fired at least one unidentified projectile Thursday, South Korean military officials said, in the country’s second test launch of weapons in less than a week

The Bank of Japan will quickly consider additional easing steps if risks such as protectionist moves by the world’s two largest economies wipe out upward price momentum in Japan, its Governor Haruhiko Kuroda said

U.K. Prime Minister won a reprieve from her Tory party after a key panel of lawmakers kept the rules on leadership challenges unchanged. May agreed to meet with the executive of the so-called 1922 Committee of Tory Members of Parliament next week to discuss her future

Theresa May earned a stay of execution from her Conservative Party after a key panel of lawmakers kept the rules on leadership challenges unchanged, as talks with the opposition Labour Party to find a compromise on Brexit gained new life

The U.S. Treasury on Wednesday saw the weakest demand for its benchmark 10-year note in a decade, illustrating the diminishing appetite among some investors to accept current yields

Trump issued an executive order on Wednesday prohibiting the purchase of Iranian iron, steel, aluminum and copper, ratcheting up tensions with the Islamic Republic less than a day after it declared it may begin enriching uranium again in two months

House price growth in the U.K. remained weak in April as the slump in southeast England and London depressed the market, the latest survey from the Royal Institution of Chartered Surveyors showed

Asian equity markets were mostly negative as US-China trade uncertainty kept global risk sentiment cautious ahead of trade talks in Washington and as the region also digested a heavy slate of corporate earnings, as well as mixed Chinese data. Nonetheless, ASX 200 (+0.4%) was the exception due to corporate updates. Nikkei 225 (-0.9%) was weighed by currency effects and with individual stocks driven by a plethora of earnings releases, while Hang Seng (-2.4%) and Shanghai Comp. (-1.5%) were the worst hit on trade concerns after the US issued a notice confirming that tariffs will be increased on Friday and with China’s Mofcom mulling counter measures. There was also some sabre rattling from US President Trump who alleged that China broke the deal in trade talks and warned to not backdown until China stops cheating US workers, otherwise the US will not do business with them. Furthermore, overnight data releases were mixed in which Chinese CPI printed inline and PPI topped forecasts, although lending data disappointed with both New Yuan Loans and Aggregate Financing below expectations. Finally, 10yr JGBs initially saw mild upside on the risk averse tone and with the BoJ present in the market focused in the belly. However, the gains were later pared amid mixed comments from BoJ Governor Kuroda who reiterated to continue with powerful monetary easing under YCC given that inflation is still below target, but noted that JGB purchases are slowing and suggested that even if BoJ bond purchases slow to JPY 30tln annually, it would not cause huge trouble.

Top Asian News

Bahrain Is Set to Receive $2.3 Billion From Allies in 2019

Singapore’s First 2019 Mainboard IPO Falls in Trading Debut

European bourses have succumbed to the risk aversion [Eurostoxx 50 -1.0%] seen in Asia and Wall Street, with the downbeat tone exacerbated by reports of further missiles tests in North Korea. Sectors are largely lower with the exception of defensive sectors such as Utilities (Unch) and Consumer Staples (+0.2%). A few themes are in play today; 1) a guidance cut by Intel yesterday has prompted a sell-off in European chip names with Infineon (-2.8%) and STMicroelectronics (-2.8%) shares plumbing the depths, albeit Dialog Semiconductor (+0.2%) is bucking the trend on the back of optimistic earnings. 2) Mining names bear the brunt of sentiment-subdued base metal prices coupled with ArcelorMittal’s (-3.9%) 33% drop in profits, thus Rio Tinto (-0.9%), Antofagasta (-1.3%) and Glencore (-1.8%) all weigh on the sector. 3) Against the backdrop of weaker auto earnings, Continental (-3.2%) also reported dismal numbers which dragged its peers Michelin (-0.9%) and Pirelli (-1.2%) lower in sympathy. Finally, Renault (-2.0%) shares declined amid press reports that Nissan could lower its 2022 guidance. Back to earnings, some analysis from JPM notes that thus far, 55% of the Stoxx 600 companies topped EPS estimates (vs. 76% in the S&P 500) whilst 58% of firms are beating on topline with sales growth at 1% Y/Y (vs. +5% Y/Y in the S&P 500), “This is consistent with our view that sales growth in Europe would underwhelm relative to the US, given the weaker macro momentum in the region” JPM says.

Top European News

Continental AG Sees China Auto Rebound Boosting Second Half

Norges Bank Says It Will ‘Most Likely’ Raise Rates in June

Airbus 320 Makes Emergency Landing in Sweden After Cabin Smoke

SocGen Introduces Crypto to $2 Trillion Market for Covered Bonds

In FX, demand for the Yen remains fervent and the Franc is also back in favour as tensions rise ahead of the US/China face-off in Washington, while geopolitical factors are also weighing on sentiment given the US-EU-Iran sanctions dispute and NK firing an unidentified projectile. Hence, Usd/Jpy has retreated a bit further from 110.00+ to fill/trip a few stops between 109.75-70 and test the top end of decent option expiry interest spanning 109.60-50, while Usd/Chf and Eur/Chf have pulled back from 1.0200+ and 1.1400 respectively.

USD – Notwithstanding the greater appeal for safer-havens noted above, the Dollar retains a firm underlying bid vs the other G10s and especially EMs that are suffering in their own right. Indeed, the DXY continues to find support below 97.500 and its 30 DMA (97.398) with the index currently hovering in a 97.702-517 range.

AUD – The major underperformer and most prone to the threat of a complete breakdown in US-China trade dialogue that would trigger an exchange of more aggressive tit-for-tat tariffs. Aud/Usd has recoiled from recent recovery highs towards this week’s multi-month low around 0.6963 and Aud/NZD has unwound more post-RBNZ spike gains to sub-1.0600 as Nzd/Usd holds more comfortably above 0.6550 and depths plunged in wake of Wednesday’s NZ rate cut. On that note, Governor Orr has reiterated that the policy outlook is now more neutral and it is too soon to assess if more easing is required ahead of testimony on the latest meeting and action to a parliamentary select committee.

NOK – Staying with the Central Bank theme, but in stark contrast to the RBNZ, Norway’s Norges Bank flagged a hike at next month’s meeting and the Nok shot up across the board in response. However, gains were rapidly eroded and reversed at one stage amidst the aforementioned risk-averse tone before the Norwegian Crown regained bullish momentum on the fact that rates are set to rise against the general global grain of steady to easier policy. Eur/Nok is back under 9.8000, albeit just within 9.7784-8393 trading parameters and eyeing hefty expiry interest (1.1 bn) at the strike.

EUR/GBP/CAD – All narrowly mixed vs the Greenback, but with a bearish bias below 1.1200, 1.3000 and only just over 1.3500 respectively. Eur/Usd has multi-bn expiries stretching from 1.1150 to 1.1200 and beyond to keep price movement contained along with the 30 DMA (1.1223) and interim chart support at 1.1155, while Cable has gleaned some traction around a Fib (1.2980) and ahead of the 200 DMA (1.2960), but needs to recapture the 100 DMA (1.3013) to revisit best levels of 1.3025. Back to the Loonie, Canadian trade data looms alongside house prices.

EM – More widespread losses vs the Usd, but once again the Try is underperforming and has been down to through 6.2450 with the Lira lamenting another decline in Turkish foreign reserves.

In commodities, Brent (-0.5%) and WTI (-0.4%) prices are choppy, with prices initially subdued amid the general risk sentiment as markets await US-China updates and the most recent geopolitical developments being reports that North Korea has fired an unidentified projectile at 16:30 local time, although it is still unknown whether it was a single or multiple projectiles. Despite the recent price action being sentiment-driven, the macro picture still stands, with Iranian/Venezuelan sanctions, Libyan tensions and OPEC-led cuts still on the table. Thus, Barclays revised their Q3 2019 Brent and WTI forecasts higher by USD 4/bbl amid expectations of tightening market conditions. In terms of US supply, ING highlights that refinery run rate remain at a season-low at 88.9% last week amid a heavier maintenance season alongside several unplanned outages. Meanwhile, gold (+0.3%) has been accumulating some risk premium in light of the aforementioned developments in the Korean peninsula whilst conversely, copper is pressured by the humdrum risk tone emanating from the seemingly escalating US-Sino tensions and geopolitical concerns. Finally, China State Planner stated that strict pollution related controls will be imposed on steel-making capacity in key pollution area whilst also raising domestic iron ore production. It’s worth noting that earlier in March, a level 1 smog alert was issued which requires steel mills to curb production by 40-70%. Although, it is worth assuming that iron ore production will be hiked to offset volatility in the base metal. China’s State Planner state they will impose strict controls on steel-making capacity in key pollution areas.

Looking at the day ahead, we will get the April PPI report where the market consensus is pegged at +0.2% mom for the core. Expect there to be focus on the health care and portfolio management services components of the report as a read-through for the core PCE deflator. Away from that we’ll also get the latest claims reading and March trade balance print, followed later by the final March wholesale inventories revisions. Away from that we’re due to hear from the ECB’s Hakkarainen while over at the Fed, Powell is scheduled to speak in the early afternoon, albeit only opening remarks with no Q&A to follow. The Fed’s Bostic and Evans also speak today.

US Event Calendar

8:30am: PPI Final Demand MoM, est. 0.3%, prior 0.6%; YoY, est. 2.3%, prior 2.2%

PPI Ex Food and Energy MoM, est. 0.2%, prior 0.3%, YoY, est. 2.5%, prior 2.4%

8:30am: Trade Balance, est. $50.1b deficit, prior $49.4b deficit

8:30am: Initial Jobless Claims, est. 220,000, prior 230,000; Continuing Claims, est. 1.67m, prior 1.67m

9:45am: Bloomberg May United States Economic Survey; Bloomberg Consumer Comfort, prior 60.4

10am: Wholesale Trade Sales MoM, est. 0.55%, prior 0.3%; Wholesale Inventories MoM, est. 0.0%, prior 0.0%

DB’s Jim Reid concludes the overnight wrap

As US/China trade and Brexit talks looked increasingly more vulnerable yesterday at least here in the UK we had the first glance of a new royal baby to distract us. I was disappointed he was named Archie rather than Divock after Liverpool’s Tuesday night heroics which have still yet to fully sink in. As it stands I have a one-way flight to Madrid booked and no final tickets. I also haven’t run the idea of a weekend away watching football by my wife yet. I thought I’d work on this in stages. Flight out first (only tick so far), ticket second, flight back third, accommodation next (but I could camp) and then ask permission. No point asking permission and firing a bullet if you can’t logistically do it. If Liverpool’s performance was astonishing one would have to say Spurs also coming back from 3-0 down in the tie at HT against Ajax last night and winning on away goals deep in injury time was also remarkable. My long-time work colleague Nick Burns is a Spurs season ticket holder and entitled to final tickets and as I reserved him an flight to the final yesterday just in case I will assume he’s reserved me a ticket this morning. This morning could be the defining moment in his 2019 appraisal.

Outside of the knowledge of the craziness of sport, the last 24-48 hours has taught us that markets have no greater insight as to whether this week’s trade developments are just hardball from Trump or the start of a very real threat to the global growth narrative. If it’s the latter then you can’t help but feel that markets look extremely complacent at this point. However if it’s just hardball negotiation en route to a deal then we’ll likely resume the rally. A big bid offer admittedly, but in the very short term the risks probably look greater than the rewards as it feels unlikely that either side can back down in the near term. Maybe over weeks but not over the next few days.

At the time of writing, China’s top trade negotiator Liu He is flying over to Washington DC for talks with Lighthizer and Mnuchin. Time is not on China’s side though with tariffs due to kick in in a little under 24 hours after the Office of the US Trade Representative yesterday signed off that tariffs on $200bn of China goods are to be raised on Friday morning at 12:01am ET.

In line with the back-and-forth newsflow, markets slipped between gains and losses before ending the US session slightly lower. Just four minutes before the Office of Trade statement in late morning US time, President Trump tweeted that China were “coming to the US to make a deal” which appeared to at least hold some hope of optimism in markets. A bigger boost came after White House spokeswoman Sarah Sanders said that the White House had received an “indication” that China is ready to make a deal. Within half an hour, however, a commerce department statement from China said that “The US intends to raise the tariff of 200 billion US dollars of Chinese exports to the United States from 10% to 25% on May 10. The escalation of trade friction is not in the interests of the people of the two countries and the people of the world. The Chinese side deeply regrets that if the US tariff measures are implemented, China will have to take necessary countermeasures.”

Overnight, while addressing a rally in Panama City Beach, Florida, President Trump has said that China’s leaders “broke the deal” he was negotiating with them on trade and added there’s “nothing wrong with taking in $100 billion a year” in tariffs on Chinese imports, in the absence of a trade deal. However, he also said, “they come in tomorrow and whatever happens, don’t worry about it. It will work out. It always does.” Elsewhere, the WSJ has reported that China’s Vice Premier Liu He is not carrying the title of President Xi’s “Special Envoy” while visiting the US for trade negotiations and this means that he cannot make any big concessions. China’s Global Times is also reporting this morning that China wont flinch in the face of a tough-talking US and is likening the trade talks to a “Banquet at Hongmen”, a Chinese reference to a historical event that took place in 206 BC at Hong Gate and implies a treacherous situation. So emotions and rhetoric are being raised in both sides. It should be worth watching China’s regular ministry of commerce briefing at 03:00 pm Beijing time (08:00 am London) to get further insight into the situation.

All nice and straightforward then. The end result to the conflicting headlines yesterday was a bit of volatility for the S&P 500 just before Europe went home, opening -0.37% lower before rallying to +0.47%, but ultimately closing -0.15% after a sharp late drop. That leaves May’s returns at a still pretty mild -2.24% though considering all that has gone on. The VIX touched an intraday high of 21.74 yesterday though – a level it hasn’t closed at since January 3 – before ending at 19.92, trading in a range of 3.5pts. That’s the third consecutive day with a range of over 3pts, the first such stretch since January 4. The NASDAQ fell -0.26% and the DOW traded flat (+0.01%), while in Europe the STOXX 600 finished +0.15% after spending the bulk of the session in the red.

Meanwhile, bond markets couldn’t quite make their minds up yesterday with 10y Treasury yields rising +2.7bps, +5.9bps off the morning low but 2bps lower again in Asia. The 3m10y curve steepened +1.9bps yesterday, taking it back to +5.8bps after flirting with another inversion over the last few sessions. The 2y10y is still hovering around 18.3bps and the reality is that this has been in a broad 10-20bp range ever since December. Bunds have been more of a beneficiary of the risk-off moves, hitting an intraday low of -0.065% yesterday before closing at -0.044% as risk rallied back into the European close. For reference, the recent low mark for Bunds was -0.095% on an intraday basis back at the end of March. BTPs have been caught up in the broader risk off move – with the recent budget headlines also not helping – though they retraced their +7.7bps intraday move yesterday to end the session flat. Elsewhere EM FX traded flat overall, with the Turkish lira again underperforming (-0.56%) as the government announced plans to re-hold the Istanbul elections. Balancing this was a +0.26% rally by the South African rand, as the country held national elections yesterday, with the results due this morning.

This morning in China we saw the release of April aggregate financing data which came in at CNY 1,360bn (vs. 1,650bn expected and 2,859.3bn last month) with new loans standing at CNY 1,020bn (vs. 1,200bn expected and 1,690bn last month). Weakness in China’s credit data along with the possibility of further escalations in the trade war is continuing to weigh on Asian markets with the Nikkei (-1.01%), Hang Seng (-1.95%), CSI (-1.90%), Shanghai Comp (-1.35%), Shenzhen Comp (-1.03%) and Kospi (-1.67%) all down over -1% alongside most Asian markets. China’s onshore yuan is down -0.39% to 6.8090, the weakest since January. Other EM Fx is also trading weak this morning with the exception of Turkish Lira which is up +0.37% while the Korean won is leading losses (-0.56%). G10 Fx is also weak with the exception of the Japanese yen which is up +0.14%. Elsewhere, futures on the S&P 500 are down -0.53% and crude oil prices (WTI and Brent both down -0.74%) are also weak. In terms of other data releases China’s April CPI came in line with consensus at +2.5% yoy while PPI stood at +0.9% yoy (vs. +0.6% yoy expected).

In other news, cross-party talks between the Conservatives and Labour continued yesterday but finding common ground remains elusive. In the meantime, the BBC has reported this morning that Labour Party’s Jeremy Corbyn is set to launch his European elections campaign later and will say that the party backs “the option of a public vote” if a “sensible” Brexit deal cannot be agreed and there is not a general election. Elsewhere Prime Minister May looks set to survive for at least another week as the 1922 committee failed to agree on any changes to Conservative party rules at this week’s meeting. The 1922 head Graham Brady said he expects May to hold a vote on the Withdrawal Agreement Bill next week, which could possibly still leave time to exit the European Union before the European Parliament elections but that is looking very very unlikely.

Back to the US and Fed Governor Brainard made some headlines yesterday by expressing interest in a form of yield curve control as a future policy option. She said “we might turn to targeting slightly longer-term interest rates — initially one-year interest rates, for example, and if more stimulus is needed, perhaps moving out the curve to two-year rates.” This would potentially allow the Fed to better signal how long it plans to keep rates low. Such tools could be needed in a future recession if short-term interest rates again approach zero.

Oil prices rose +1.101% before this morning’s fall as tensions between the US and Iran continued to intensify and the outlook for Iranian oil exports continues to darken. First, Iran announced that it is also withdrawing from the nuclear deal, following the US’s move exactly one year ago. While the Iranian government did not declare an intention to renege on all the deal’s elements, they did announce their plans to resume stockpiling low enriched uranium and heavy water, and signalled that they would resume construction of a closed reactor if Europe fails to compensate for the US’s unilateral sanctions. That comes after news that Europe’s mechanism to avoid US sanctions, which reportedly would have allowed Iran to export more oil, will actually only apply to food and humanitarian aid. Finally, the US administration followed up by adding new sanctions to Iran’s iron, steel, aluminium, and copper industries.

Before we wrap up, the data yesterday included a better than expected March industrial production print in Germany (+0.5% mom vs. -0.5% expected) albeit somewhat offset by downward revisions to February. In the UK the Halifax house price index rose +1.1% mom in April and more than expected. US mortgage applications rose +2.7% last week, the first rise since March.

Finally to the day ahead, where there are no data releases due in Europe this morning however in the US this afternoon we will get the April PPI report where the market consensus is pegged at +0.2% mom for the core. Expect there to be focus on the health care and portfolio management services components of the report as a read-through for the core PCE deflator. Away from that we’ll also get the latest claims reading and March trade balance print, followed later by the final March wholesale inventories revisions. Away from that we’re due to hear from the ECB’s Hakkarainen while over at the Fed, Powell is scheduled to speak in the early afternoon, albeit only opening remarks with no Q&A to follow. The Fed’s Bostic and Evans also speak today.

via ZeroHedge News http://bit.ly/2YdQn3e Tyler Durden

Say what you will about the ethics of plagiarists — at least they have an ear for what audiences want to hear.

When Joe Biden cratered in his first official run at the White House in 1987, it was because of a series of borrowed speech passages, hand gestures, and even biographical details (no, he didn’t derive from a family of coal miners, as he once claimed, nor was he “the first” in his clan to ever attend college; he lifted those details from a speech by U.K. Labor politician Neil Kinnock). The deceptions nonetheless revealed a political truth: Ronald Reagan had peeled off blue-collar voters from the Democratic Party, and it would take a relatable, regular-sounding Joe to lure them back.

Americans may tell themselves they seek candidates who lead, but in reality they’re more likely to reward politicians, like Biden, who follow where public tastes have already gone. You generally don’t serve in multiple tiers of elected office for his 47 years — longer than Pete Buttigieg, Beto O’Rourke and several other Democratic presidential candidates have been alive — by getting out ahead of voters’ comfort zones. You get there by being a weather vane.

Joe Biden is a political weather vane covered in rust. He’ll creak in the direction of the prevailing winds eventually, apologetically if need be, but don’t expect the man to point toward some bold new future. It’s both his main selling point and greatest weakness.

During the late 1980s and early ’90s, when the country was at the exhausted end of a three-decade rise in violent crime, Biden was right there putting his fingerprints all over what would become America’s mass incarceration machine. He co-sponsored the Anti-Drug Abuse Act, which included much tougher penalties for crack cocaine than for powder cocaine, and lamented that “6 out of every 10 criminals who are arrested on drug charges have their cases dropped.”

Now that even a law-and-order Republican president is pushing through criminal justice reform, Uncle Joe is characterizing his role in the crack/powder disparity as a “big mistake.”

Biden absolutely will follow, not lead, on legalizing marijuana, which two out of three Americans — and all 12 presidential candidates immediately behind him in national polls — now support. Even while serving in the White House with “Choom Gang” emeritus Barack Obama, the then-veep was still using old-timey prohibitionist language, calling pot a “gateway drug.”

Think of every time American public opinion over the past half-century swung toward a public-policy hysteria many would eventually regret, and you’ll see Joe there, Zelig-like, flashing his choppers. Iraq war? Check. The (as characterized by Vox’s Dara Lind) disastrous, forgotten 1996 law that created today’s immigration problem? Yep. Patriot Act? He’s been dining out on that one for years.

Those of us wary of government power shudder at the sight of politicians with a demonstrated eagerness to wield it when the masses get rowdy. And yet Biden’s finger-in-the-wind ideological pliability can have its uses, too, most famously in 2012, when he gingerly led his party to the conclusion on marriage equality its voting members had long since held. This, less than two decades after (of course!) voting for the notorious Defense of Marriage Act.

Biden’s current high standing in the polls is a sight to behold for those of us who remember his six feeble previous flirtations with the Oval Office. It suggests that, in a cycle in which Democrats are prioritizing electability more than in any recent election, it’s precisely Joe’s rust that makes him attractive.

With the exception of the vanishing never-Trump rump, just about every right-of-center political and policy grouping I’m aware of is gearing up for 18 months of trench warfare against incipient socialism. “If Trump doesn’t win,” the once-Trump-averse Glenn Beck recently warned, “we are officially at the end of the country as we know it.”

In a campaign that has already zoomed from Medicare-for-all to the Green New Deal to even slavery reparations with vertigo-inducing speed, who among the recognizable half of the Democratic field seems least likely to hoist the red banner? Rust is not, after all, a useful lubricant for revolution.

While Sen. Elizabeth Warren (D-Mass.) is out there unveiling giant (and costly!) new policy proposals every 48 hours or so, Biden just waves off any such commitments, saying he doesn’t “have the time to completely lay out all the details” of his plans.

In a political moment so weird that Donald Trump is president and Bernie Sanders damn near took over the Democratic Party, it may seem counterintuitive to bet on a politician who works so hard at coloring inside the lines. But two-party systems tend to resemble pendulums. After four years of comparative madness, maybe Americans are looking for a typical politician: unprincipled and pandering, sure, but at least predictable. And slow.

Tehran tried to call Washington’s bluff on Wednesday when it threatened to start stockpiling enriched uranium and heavy water again – which would constitute a violation of the JCPOA’s terms – unless the treaty’s signatories abide by their commitments to buy oil and offer other financial relief, something that American sanctions have rendered impossible.

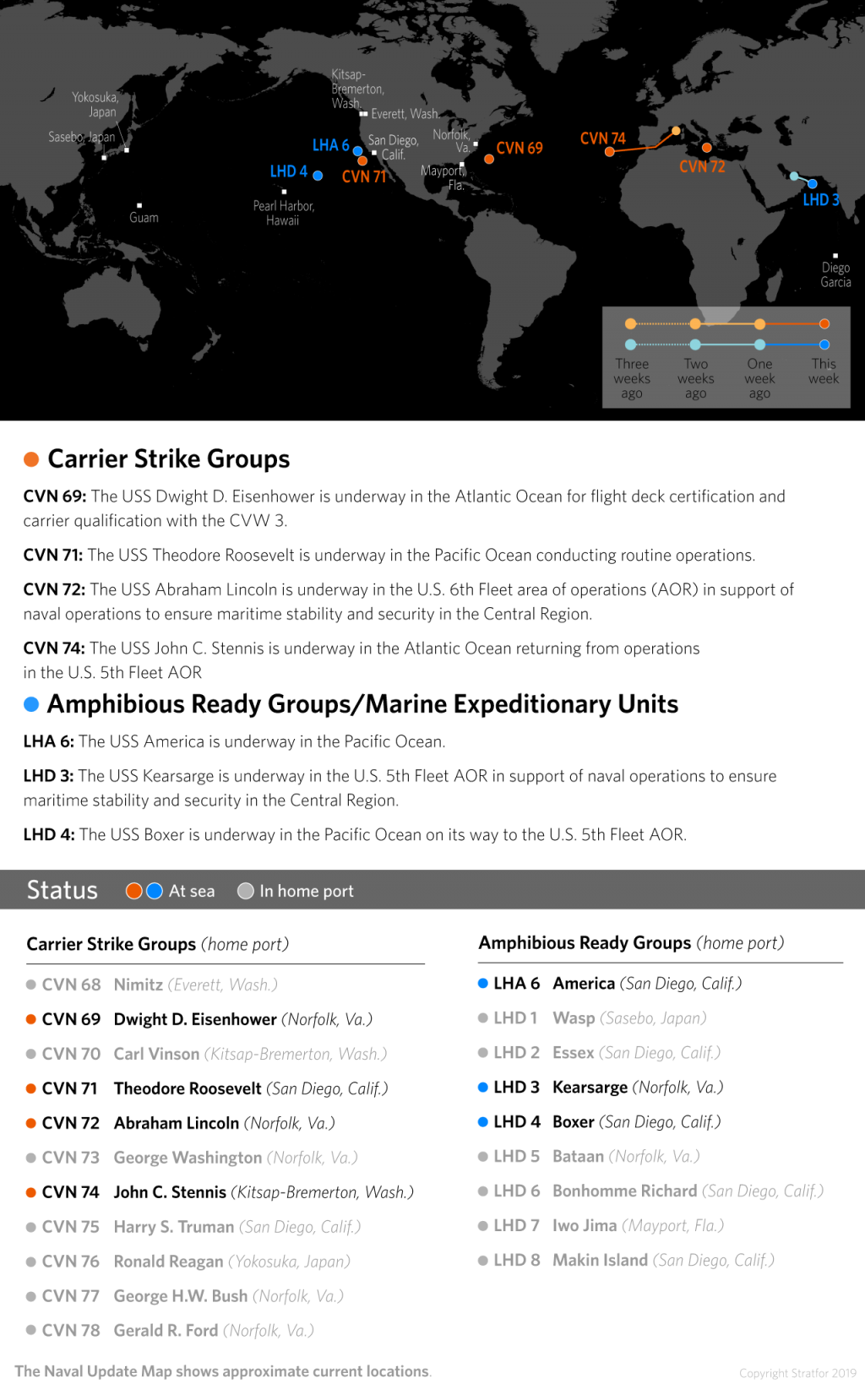

But in what appears to be an attempt to show Tehran that it’s not bluffing, Washington has committed to another threatening display of force. Reuters reports that the USS Abraham Lincoln, which had been dispatched to the Mediterranean last week amid worsening tensions with Iran, has passed through the Suez Canal, the first stop in what appears to be a journey into Iranian waters.

U.S. AIRCRAFT CARRIER ABRAHAM LINCOLN, SENT AS WARNING TO IRAN, PASSES THROUGH EGYPT’S SUEZ CANAL – CANAL AUTHORITY

The report cited the Canal Authority as its main source.

Last night, Trump issued a statement affirming that the relationship with Iran is “broken beyond repair” and placed new sanctions on Iran’s industrial metals sector.

Meanwhile, the Iranians have dismissed Washington’s dispatching of the aircraft carrier and several B-52 bombers to the region.

The Iranians have warned that they would retaliate if US forces get too close – possibly by blocking off the critical Strait of Hormuz (vital to the global oil trade) or responding with violence. If the aircraft carrier is indeed heading for the Persian Gulf, the situation could swiftly spiral out of control.

via ZeroHedge News http://bit.ly/2WyKNIa Tyler Durden

Say what you will about the ethics of plagiarists — at least they have an ear for what audiences want to hear.

When Joe Biden cratered in his first official run at the White House in 1987, it was because of a series of borrowed speech passages, hand gestures, and even biographical details (no, he didn’t derive from a family of coal miners, as he once claimed, nor was he “the first” in his clan to ever attend college; he lifted those details from a speech by U.K. Labor politician Neil Kinnock). The deceptions nonetheless revealed a political truth: Ronald Reagan had peeled off blue-collar voters from the Democratic Party, and it would take a relatable, regular-sounding Joe to lure them back.

Americans may tell themselves they seek candidates who lead, but in reality they’re more likely to reward politicians, like Biden, who follow where public tastes have already gone. You generally don’t serve in multiple tiers of elected office for his 47 years — longer than Pete Buttigieg, Beto O’Rourke and several other Democratic presidential candidates have been alive — by getting out ahead of voters’ comfort zones. You get there by being a weather vane.

Joe Biden is a political weather vane covered in rust. He’ll creak in the direction of the prevailing winds eventually, apologetically if need be, but don’t expect the man to point toward some bold new future. It’s both his main selling point and greatest weakness.

During the late 1980s and early ’90s, when the country was at the exhausted end of a three-decade rise in violent crime, Biden was right there putting his fingerprints all over what would become America’s mass incarceration machine. He co-sponsored the Anti-Drug Abuse Act, which included much tougher penalties for crack cocaine than for powder cocaine, and lamented that “6 out of every 10 criminals who are arrested on drug charges have their cases dropped.”

Now that even a law-and-order Republican president is pushing through criminal justice reform, Uncle Joe is characterizing his role in the crack/powder disparity as a “big mistake.”

Biden absolutely will follow, not lead, on legalizing marijuana, which two out of three Americans — and all 12 presidential candidates immediately behind him in national polls — now support. Even while serving in the White House with “Choom Gang” emeritus Barack Obama, the then-veep was still using old-timey prohibitionist language, calling pot a “gateway drug.”

Think of every time American public opinion over the past half-century swung toward a public-policy hysteria many would eventually regret, and you’ll see Joe there, Zelig-like, flashing his choppers. Iraq war? Check. The (as characterized by Vox’s Dara Lind) disastrous, forgotten 1996 law that created today’s immigration problem? Yep. Patriot Act? He’s been dining out on that one for years.

Those of us wary of government power shudder at the sight of politicians with a demonstrated eagerness to wield it when the masses get rowdy. And yet Biden’s finger-in-the-wind ideological pliability can have its uses, too, most famously in 2012, when he gingerly led his party to the conclusion on marriage equality its voting members had long since held. This, less than two decades after (of course!) voting for the notorious Defense of Marriage Act.

Biden’s current high standing in the polls is a sight to behold for those of us who remember his six feeble previous flirtations with the Oval Office. It suggests that, in a cycle in which Democrats are prioritizing electability more than in any recent election, it’s precisely Joe’s rust that makes him attractive.

With the exception of the vanishing never-Trump rump, just about every right-of-center political and policy grouping I’m aware of is gearing up for 18 months of trench warfare against incipient socialism. “If Trump doesn’t win,” the once-Trump-averse Glenn Beck recently warned, “we are officially at the end of the country as we know it.”

In a campaign that has already zoomed from Medicare-for-all to the Green New Deal to even slavery reparations with vertigo-inducing speed, who among the recognizable half of the Democratic field seems least likely to hoist the red banner? Rust is not, after all, a useful lubricant for revolution.

While Sen. Elizabeth Warren (D-Mass.) is out there unveiling giant (and costly!) new policy proposals every 48 hours or so, Biden just waves off any such commitments, saying he doesn’t “have the time to completely lay out all the details” of his plans.

In a political moment so weird that Donald Trump is president and Bernie Sanders damn near took over the Democratic Party, it may seem counterintuitive to bet on a politician who works so hard at coloring inside the lines. But two-party systems tend to resemble pendulums. After four years of comparative madness, maybe Americans are looking for a typical politician: unprincipled and pandering, sure, but at least predictable. And slow.

Has President Trump finally turned on John Bolton? It’s starting to look that way.

Shortly before President Trump tweeted about a meeting with Marco Rubio and Rick Scott where the “terrible abuses by Maduro” were discussed, the Washington Post published an anonymously sourced story claiming that Trump is growing frustrated with the situation in Venezuela, and is blaming aides like Bolton for misleading him about opposition leader Juan Guaido’s chances of success.

After a great rally in Panama City Beach, Florida – I am returning to Washington, D.C. with @SenRickScott and Senator @MarcoRubio, discussing the terrible abuses by Maduro. America stands with the GREAT PEOPLE of Venezuela for however long it takes! pic.twitter.com/KcBoNfEibv

According to WaPo, Trump has privately described Maduro as a “tough cookie”, and blamed aides for misleading him when they said the socialist strongman could be ousted during last week’s demonstrations. In recent days, Trump has expressed concern that Bolton is trying to get him “into a war.” We imagine a leaked plan for a US-backed coup prepared by SOUTHCOM hasn’t helped to assuage these concerns.

Though two WaPo sources insisted that Bolton’s job is ‘safe’ – for now at least – the fact that Trump has finally caught on to the drawbacks of Bolton’s neoconnishness, and now appears to understand that Bolton’s views are at odds with Trump’s “America First” platform, certainly doesn’t bode well for his prospects.

Earlier this week, Vice President Mike Pence revealed that the White House would lift sanctions on a general who had turned on Maduro, and offered the same level of amnesty to any military officials who would join him.

Still, the administration’s policy is officially unchanged. But the report at least shows that Trump is uneasy about what appears to be a slow march toward another American military intervention – and might be taking steps to stop it from happening.

via ZeroHedge News http://bit.ly/2DXOTCK Tyler Durden

We recently documented how Amazon has come under fire from its merchants for allegedly trying to undercut them on pricing and products. Now, the e-commerce giant is under scrutiny for a different reason: security. Amazon is now saying it was hit by an “extensive” fraud last year, revealing in court documents that hackers were able to transfer funds from merchant accounts over the course of six months, according to Bloomberg.

The “serious” online attack included hackers breaking into about 100 seller accounts and moving cash from loans or sales into their own bank accounts. The hack took place between May 2018 and October 2018, according to Amazon’s lawyers.

Amazon said it was still looking into the compromised accounts and that it believed hackers changed the details on its Seller Central platform to bank accounts in their name. Amazon believes that the accounts were compromised by phishing techniques that looked for login information. Amazon has reportedly concluded its investigation of the incident.

Lawyers for the online retailer asked a judge in London to approve searches of account statements at Barclays and Prepay, two banks that “have become innocently mixed up in the wrongdoing.” Amazon says that it needed the documents “to investigate the fraud, identify and pursue the wrongdoers, locate the whereabouts of misappropriated funds, bring the fraud to an end and deter future wrongdoing.”

The filing doesn’t denote how the suspected wrongdoers were able to add new bank account information to merchant accounts. Amazon has issued more than $1 billion in loans to merchants and one of the units named in the filing was Amazon Capital Services U.K., a division of the company responsible for making these loans.

The dollar amount stolen by the hackers has not been disclosed but the incident could mark the latest in a series of incidents that may deter merchants from using Amazon to sell goods. In an April report, we detailed how Amazon merchants were feeling more and more like they were on the wrong end of a lopsided deal with the company, which has been selling its own brand of “Basics” that often undercut its own merchants.

One vendor interviewed, Jason Boyce, has been wary of regulation as small business owner. Despite this, he was willing to consider proposed regulations by Senator Elizabeth Warren that would prevent Amazon from competing against its merchants. Boyce said: “If you’re going to have a marketplace, you shouldn’t be able to piggyback off the hard work and labor of your sellers to beat them.”

“Amazon crushes small companies by copying the goods they sell on the Amazon Marketplace and then selling its own branded version,” Senator Warren has previously said.

Boyce, a former Marine Corps officer, started selling his product – basketball hoops – online in 2002. In 2004, he got a call from Amazon who said that they “liked” his products and he began to list them on the site. But over the next few years, his experience on Amazon resulted in competitors entering in the market and pushing down prices. So, like a good businessman, he pivoted to other products, developing his own line of foosball tables, air hockey tables, bocce ball sets and exercise equipment.

Then, in 2009, Amazon started selling its own products, Amazon Basics. Among its offerings, Amazon started selling bocce ball sets that cost $15 less than Boyce’s, and giving them ideal page space to win the shopper looking for the lowest price.

“They’re pulling market share away from us and our competitors as well,” Boyce said. Now, it appears merchants are having their money pulled from them, too.

via ZeroHedge News http://bit.ly/2DWXzcc Tyler Durden