“Everything is awesome”

S&P 500 tops its Sept 21st record intraday highs…

Will earnings and macro catch up now?

via ZeroHedge News http://bit.ly/2GHcyYt Tyler Durden

another site

“Everything is awesome”

S&P 500 tops its Sept 21st record intraday highs…

Will earnings and macro catch up now?

via ZeroHedge News http://bit.ly/2GHcyYt Tyler Durden

Via Greg Hunter’s USAWatchdog.com,

President Trump says the Deep State tried and failed to remove him from office in a coup. Former CIA Officer and whistleblower Kevin Shipp says the attempted coup on Trump was a global conspiracy.

Shipp explains, “Yes, this is a coup. This is the most shocking violation of the Constitution and criminal activity in the history, not just of America, but of a western government…”

“Much of this rises to the level of treason. People need to understand how shocking this is. It was a clear conspiracy. There will be arrests and indictments without question. . . . This was a coup. It was a conspiracy. It was criminal activity. These people need to be indicted, charged and need to be put in prison, and if they’re not, then our Constitution is nothing more than a sham. This was a coup against a duly elected President, and people need to understand how serious this is.”

Shipp adds, “We have a not so covert civil war going on right now that has been brewing over 60 years…”

“We have the ‘Dark Left,’ and the DNC is fully involved with all their Congressmen and Senators. There is a Marxist movement within the DNC that is in control right now. You can match up the progressive goals with Marxist documents, and you can see they are one in the same. . . . ..

And the Second Amendment first of all. Second of all, they despise and are targeting Christianity because Christianity… underlines the Constitution and is mentioned in the Declaration of Independence. That’s their second target they have to destroy. Their third target is the founding principles of America.

That’s our culture. They have to destroy those three things if they are going to overturn our Constitution and turn this into a global Marxist government. That is not an understatement. . . . It’s not the same party of JFK. It’s now a Marxist party and an umbrella for every victim, twisted and perverted group that has nowhere else to go. This is a mortal blow to the Democrat Party when these things come out.”

Shipp predicts President Trump will declassify more than anyone can imagine. Shipp says,

“They have been using ‘classification’ as a way to cover up illegal activity. The CIA has, especially in the case of this coup, not just in this, but in other things they have done criminally. They have been withholding things from Congress using ‘classification’ for decades. Trump knows what those are, and he is going to demand that classification is removed so the American people can see it. I am going to be dancing on top of my house if and when that happens.”

Shipp predicts Trump will win re-election in 2020. Shipp says Trump won’t be voted in by just devout Republicans, but Democrats who are running from their party because of how extreme it has gotten. Shipp explains,

“Yes, they are running from the Democrat Party. Support for Trump has been increasing by the millions. A lot of these Democrats are being very, very quiet right now because they know what will happen to them if they come out in support of Trump. When 2020 comes, these Democrats are going to push that button and pull that lever for Trump, and it’s going to be more shocking than 2016.”

So, what’s the danger for “We the People”? Shipp says,

“The danger for ‘We the People’ is the Dark Left and Dark Left violence. As these indictments begin to come out, and as the players are called out, the violence on what I call the Dark Left, the violence is going to increase to the point where it’s going to be very, very bad. There are going to be beatings and probably shootings, and shooting at police. . . . There is going to be a lot of violence coming from the Left in the next year or two. This is one of the reasons you need to exercise your 2nd Amendment rights . . . because of what the Left is going to do with these findings and what is going to be the death knell for the Democrat Party and the death knell for taking over our Constitution and culture. They will exponentially bring up their violence, and Americans need to arm themselves and protect themselves against that.”

Join Greg Hunter as he goes One-on-One with CIA whistleblower Kevin Shipp, founder of the popular website ForTheLoveofFreedom.net.

To Donate to USAWatchdog.com Click Here

via ZeroHedge News http://bit.ly/2DDG1BI Tyler Durden

Kamala Harris wants to make absolutely sure that we know she’s an authoritarian. Fresh off announcing that as president she would override Congress to get her way on gun policy, the Democratic senator from California and 2020 presidential hopeful said she would use executive power to push for bans on state laws she opposes, too.

Speaking to a Service Employees International Union (SEIU) gathering on Saturday, Harris spoke of the need for “banning right-to-work laws” that nearly half of states have enacted and how, as president, she would use both her “bully pulpit” and “executive authority” to accomplish that.

Right-to-work laws are often framed by Democrats as anti-union or anti-worker policy. In fact, all they say is that employees can’t be told to join a union or pay union fees as a condition of employment. They’re still welcome to do so; they just have to make that choice for themselves.

In the topsy-turvy world of Harris and other Democrats, however, giving workers options is no good. If elite forces in Washington think workers would be better off joining unions, then they’re just going to override the will of individual employees and state governments across the country. Do as they say! Or else! For your own good.

Sure, some low-income workers might think their hard-earned dollars are better spent on securing immediate material well-being for them and their families. But Harris thinks their dollars would be better off with a massive and bloated international organization that can help her presidential campaign. I mean, have you seen SEIU’s massive mansion across the street from the White House? How could any group so swampy be wrong?

As The Wall Street Journal editorial board noted yesterday:

Right to work is a bugbear to union leaders because it crimps their finances for political spending, and Ms. Harris is eager to get the endorsement of the SEIU and other major unions. Her first big policy proposal, unveiled in March, would have the feds give teachers across the country an average pay raise of $13,500 a year. That payoff to the teachers unions would cost federal taxpayers some $315 billion over 10 years, not including what states would have to contribute to qualify for these Harris Grants.

The big story of the 2020 campaign so far is the Democratic Party’s lurch to the left, and Ms. Harris’s pitch against right to work is evidence that her goal is entrenching union power rather than assisting workers.

Several years ago, Reason ran a series of articles on whether libertarians should support right-to-work laws. Here’s Shikha Dalmia making that case that yes, “right to work laws are indeed libertarian.” Meanwhile, contributors Sheldon Richman and J.D. Tuccille make a libertarian case against right-to-work laws, arguing that they interfere with freedom of contract, here and here.

QUICK HITS

The state’s presence was minimal, and villagers sustained themselves through farming and remittances from relatives working in the Persian Gulf. Even in retrospect, nothing in those days indicated that my home province would become the main transit hub for jihadists moving from Syria into Iraq after the 2003 invasion, or the site of the Islamic State’s final battle as a caliphate.

Now Hassan struggles “to connect images from my past with the reality of today,” he writes in The Atlantic. Read the whole thing here.

from Latest – Reason.com http://bit.ly/2V3pBgT

via IFTTT

Kamala Harris wants to make absolutely sure that we know she’s an authoritarian. Fresh off announcing that as president she would override Congress to get her way on gun policy, the Democratic senator from California and 2020 presidential hopeful said she would use executive power to push for bans on state laws she opposes, too.

Speaking to a Service Employees International Union (SEIU) gathering on Saturday, Harris spoke of the need for “banning right-to-work laws” that nearly half of states have enacted and how, as president, she would use both her “bully pulpit” and “executive authority” to accomplish that.

Right-to-work laws are often framed by Democrats as anti-union or anti-worker policy. In fact, all they say is that employees can’t be told to join a union or pay union fees as a condition of employment. They’re still welcome to do so; they just have to make that choice for themselves.

In the topsy-turvy world of Harris and other Democrats, however, giving workers options is no good. If elite forces in Washington think workers would be better off joining unions, then they’re just going to override the will of individual employees and state governments across the country. Do as they say! Or else! For your own good.

Sure, some low-income workers might think their hard-earned dollars are better spent on securing immediate material well-being for them and their families. But Harris thinks their dollars would be better off with a massive and bloated international organization that can help her presidential campaign. I mean, have you seen SEIU’s massive mansion across the street from the White House? How could any group so swampy be wrong?

As The Wall Street Journal editorial board noted yesterday:

Right to work is a bugbear to union leaders because it crimps their finances for political spending, and Ms. Harris is eager to get the endorsement of the SEIU and other major unions. Her first big policy proposal, unveiled in March, would have the feds give teachers across the country an average pay raise of $13,500 a year. That payoff to the teachers unions would cost federal taxpayers some $315 billion over 10 years, not including what states would have to contribute to qualify for these Harris Grants.

The big story of the 2020 campaign so far is the Democratic Party’s lurch to the left, and Ms. Harris’s pitch against right to work is evidence that her goal is entrenching union power rather than assisting workers.

Several years ago, Reason ran a series of articles on whether libertarians should support right-to-work laws. Here’s Shikha Dalmia making that case that yes, “right to work laws are indeed libertarian.” Meanwhile, contributors Sheldon Richman and J.D. Tuccille make a libertarian case against right-to-work laws, arguing that they interfere with freedom of contract, here and here.

QUICK HITS

The state’s presence was minimal, and villagers sustained themselves through farming and remittances from relatives working in the Persian Gulf. Even in retrospect, nothing in those days indicated that my home province would become the main transit hub for jihadists moving from Syria into Iraq after the 2003 invasion, or the site of the Islamic State’s final battle as a caliphate.

Now Hassan struggles “to connect images from my past with the reality of today,” he writes in The Atlantic. Read the whole thing here.

from Latest – Reason.com http://bit.ly/2V3pBgT

via IFTTT

Following a couple of quiet weeks – if not in earnings which peaked last week when a third of the S&P reported – markets face what DB’s Craig Nicol calls a star-studded lineup of events this week, which should reignite a bit of newsflow into markets again, and perhaps even give volatility some of the old Night King treatment and rise from the dead.

We’ve got Fed and BoE meetings, a huge slew of data including payrolls, PMIs, US and European inflation and the latest growth data in Europe. If that wasn’t enough we’ve also got US-China trade talks resuming, and another packed week of earnings on both sides of the pond.

Going down the list, on Tuesday US Trade Representative Lighthizer and Treasury Secretary Mnuchin are due to travel to Beijing to continue with another round of trade talks. The latest suggestion was that both sides were working to reach a draft agreement for some time in May with talks next week covering “trade issues including intellectual property, forced technology transfer, non-tariff barriers, agriculture, services, purchases and enforcement”. Chinese Vice Premier Liu He is then expected to travel to the White House May 8th. So the intensity of these meetings should ramp up next week should both sides adhere to aiming for a draft agreement in the coming weeks.

The Fed takes center stage on Wednesday, and with policy expected to be kept on hold for the near term, the focus will instead be on the committee’s assessment of recent data, which will include today’s Q1 GDP print. The Fed may also announce a “surprise” IOER cut as a result of the persistence of the EFF above the ceiling of the interest rate corridor. The minutes to the March meeting suggested that uncertainty about the causes of muted inflation pressures remain a source of Fed unease. With inflation failing to hold at the Fed’s target level, officials’ views on inflation will be closely scrutinized.

Next week is also another busy one for earnings with 166 S&P 500 companies due to report. The notable ones include Google on Monday, Apple, ConocoPhillips, General Electric, General Motors, McDonalds and Pfizer on Tuesday, Kraft Heinz on Wednesday, and DowDupont on Thursday. As of last night we’ve had 218 companies report with 166 beating on earnings but just 116 on sales. It’s worth noting that we’re also due to get numbers from Merck, GlaxoSmithKline, BNP, Lloyds, Royal Dutch Shell and BP in Europe too.

The data highlight next week comes on Friday when we get the April employment report in the US. The market consensus is for a 181k payrolls reading which follows 196k last month. The unemployment rate is expected to hold at 3.8% while earnings are expected to show a solid +0.3% mom rise. That would push the annual rate up to +3.3% yoy and therefore just one-tenth below the February highs. Prior to that we’ll get to test the US inflation pulse with the March PCE data on Monday. The consensus is for a +0.1% core deflator reading however base effects are expected to lower the annual reading to +1.7% yoy.

As well as that we’ve also got the April PMIs around the world to look forward to next week. It will start with China on Tuesday when we get the official manufacturing, services and composite PMIs, then we’ll get Japan’s manufacturing PMI on Wednesday along with the UK and the US. The April ISM manufacturing for the US is also out on Wednesday where the consensus is for a modest decline from 55.3 to 55.0. We’ll then get the Caixin PMI in China on Thursday along with the final manufacturing PMIs for Europe. As a reminder the flash Euro Area reading improved 0.3pts to 47.8 albeit with Germany at 44.5 and sub-50 readings for France (49.6) and Italy (47.6).

In Europe we’ll also get the advance Q1 GDP reading for the Euro Area on Tuesday. The market consensus is for +0.3% qoq, a view shared by our European economists who also note that risks are tilted towards +0.4% based on recent hard data. However they also note that a positive GDP surprise has to be put in context given that it would likely be due to transitory factors and the underlying momentum of the economy is likely weaker. Also out on the same day are Q1 GDP readings for France, Italy and Spain.

As well as growth data we’ll also get the latest April CPI readings in Europe. The broad Euro Area reading is due Friday (+1.0% yoy for the core expected) and country level readings are due in France, Spain, Italy and Germany on Tuesday. Elsewhere, the BoE meeting on Thursday is not expected to produce any policy changes. However it will be the first opportunity to see how the BoE will approach the six-month Brexit extension, and markets will be on the watch to see if a rate hike for later this year is left on the table. It will also include the latest GDP and CPI forecasts.

Meanwhile, it’s another light week for central bank speakers however we do have the Fed’s Evans, Clarida, Williams and Bowman speaking on Friday. The former is speaker at a NABE forum in Stockholm while the latter three all speak at the Hoover Institute Policy Conference which will likely be closely followed. The BoE’s Carney and Ramsden are also due to speak on Monday and Tuesday respectively while the ECB’s Guindos is due to speak on Wednesday and Praet and Nowotny on Thursday. Finally, other things to keep an eye on include the conclusion of talks between Abe and Trump at the White House tomorrow, Merkel and Macron hosting a meeting of leaders from Serbia and Kosovo on Monday, Salvini and Orban meeting in Budapest on Monday to discuss a potential EU parliament alliance, the expiration of US waivers on purchases of Iranian oil on Thursday, and the EU’s Tusk speaking on Friday

Summary of key events in the week ahead:

And visually, courtesy of Amplify:

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the ISM manufacturing report on Wednesday and the employment report on Friday. In addition, the May FOMC statement will be released on Wednesday at 2:00 PM ET, followed by Chairman Powell’s press conference at 2:30 PM. There are several speaking engagements from Fed officials on Friday.

Monday, April 29

Tuesday, April 30

Wednesday, May 1

Thursday, May 2

Friday, May 3

Source: DB, Amplify, Goldman, BofA

via ZeroHedge News http://bit.ly/2IYGbY9 Tyler Durden

People attending the Coachella Music Festival this year are picking up much more than “good vibes” – they are also picking up herpes. According to the herpes tracking app “HerpAlert” there has been a massive outbreak of the sexually transmitted disease in California which is believed to be associated with the Coachella Music Festival.

HerpAlert is an app that allows users to self-report potential cases of the virus in return for access to doctors who can give them a full diagnosis and prescribe medicine. The app received at least 250 requests for medication per day during the Coachella music Festival, according to The Daily Wire. Most of these requests came from the area of the festival and surrounding towns were festival-goers stay during the event.

The spokesperson for the app told CBS that it typically receives no more than 12 cases per day from the same area. Use of the app costs a flat fee of $79.

“In all, 1,105 herpes cases were reported in the Coachella Valley area and in the nearby cities of Los Angeles and San Diego,” the New York Post reported. That number is a record for the App, blowing past the 60 inquiries received in L.A. during the Academy Awards back in February.

HerpAlert “patients fill out a series of questions about herpes symptoms for HerpAlert and provide a picture of a lesion or scar, which appears on the genitals or around the mouth. A physician then reviews the information, makes the diagnosis and can prescribe medication within hours,” the Orange County Register reported.

A HerpAlert spoksperson said people “came to the platform for a variety of reasons, including to get medication to treat and prevent flares, in addition to those who came to see if they had a new case of cold sores or herpes.”

Doctors in the area caution that although the app is showing increased number, in-person visits have not increased in the area. However, the anonymous nature of the app could make it a better tool for getting an accurate number on reports.

One doctor told Billboard:

“There were many coming to get medication to treat and prevent flares. We see it as people deciding to take proactive care of their health and the health of those they may interact with over the weekend. We do not have a number of diagnosed new cases, as sometimes we cannot determine via their history and photos, so we have to advise they see a provider in person.”

Coachella “is a perfect place for the herpes virus to pop up,” one public health official said. In addition to its 250,000 people routinely having sex with each other, participants also share things like makeup, cigarettes and drinks. Attendees also get more than the typical amount of sun exposure and less than the typical amount of sleep, making them more susceptible to illness.

via ZeroHedge News http://bit.ly/2ZKzZbW Tyler Durden

Authored by Charles Hugh Smith via OfTwoMinds blog,

No super-wealthy individual or household is going to pay billions in additional taxes when $10 to $20 million will purchase political adjustments.

The 2020 election cycle has begun, and a popular campaign promise is “free everything” paid for by new taxes on the super-wealthy. Who doesn’t like free stuff? Who will vote for whomever offers them free stuff? No wonder it’s a popular campaign promise.

As even the most self-absorbed American voter has a latent street-savvy awareness that nothing is truly free, the other popular campaign promise is to “tax the rich” to pay for the proposed “free” programs. Proposals to “Tax the rich” feed off the growing awareness that the financial wealth created since 2000 has largely flowed to the very top of the wealth-power pyramid, and so it’s payback time: tax those who have pocketed the lion’s share of income and wealth gains.

Fair enough, right? Even the super-rich publicly affirm that the super-wealthy should pay at least the same percentage of federal tax as their employees.

Public pronouncements are of course good PR, but the real issue is what will the super-wealthy do behind closed doors to protect their wealth from additional taxation. There are two issues here: one is that the wealthy already pay most of the federal income taxes, and the second is the compelling cost-benefit of funding political adjustments to the new taxes.

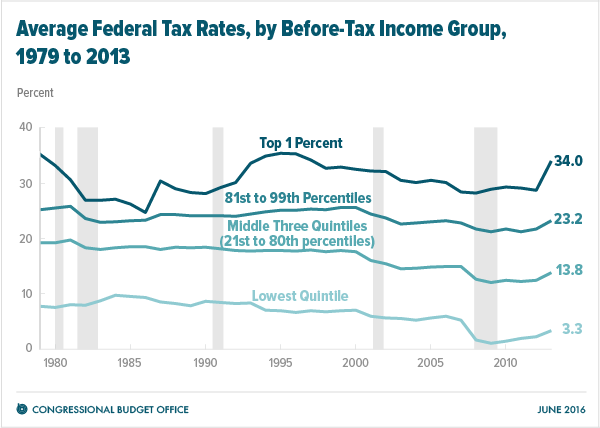

If one has a taste for facts, it turns out the U.S. federal tax system is highly progressive: the top 1% pay the highest tax rates (see CBO chart below) and about 37% of all federal income tax. The top 5% pay almost 60% of all federal income taxes. (Note Social Security payroll taxes are not income taxes; most wage earners pay more payroll taxes than they do income taxes.)

A good source for this sort of data is the Congressional Budget Office reports (scroll down to Distribution of Household Income and Federal Taxes).

The CBO data is noteworthy for including all income, not just wages: capital gains, business income and government transfers (Social Security, social welfare programs, etc.)

The new idea in current “tax the rich” proposals is to increase taxes on the super-wealthy: mega-millionaires and billionaires. Given the outsized gains secured by these mega-wealthy folks, it makes sense to nail them for the tax revenues needed to pay for more free stuff.

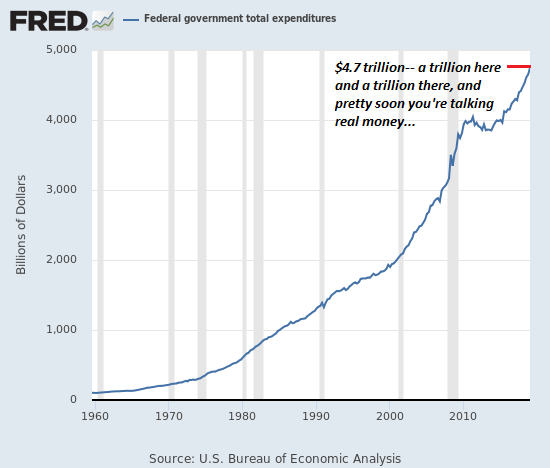

At this point let’s reacquaint ourselves with the enormous size of federal expenditures: roughly $4.75 trillion annually out of a GDP of about $20 trillion. State and local governments spend another $3.25 trillion, for total government expenditures of about $8 trillion.

Total personal income is around $10 trillion a year, with the top 1% (about 1.4 million people) getting about $2 trillion of this personal income. Out of this, they pay $538 billion in federal income tax. (Source: Summary of the Latest Federal Income Tax Data, 2018 Update)

According to this excellent overview of the top 1%, Never mind the 1 percent: Let’s talk about the 0.01 percent, the super-wealthy (top .01%) earn about 5% of all income, or about $500 billion.

So say some new tax law was actually able to capture 50% (half) of all this income: that would total $250 billion, a nice chunk of change but hardly enough to fund a trillion or two in additional “free” programs.

Since this income is already being taxed at a 34% rate according to the non-partisan CBO, jacking the rate from 34% to 50% is only 16% more, or an additional $80 billion in tax revenues. Look at the chart of current federal expenditures ($4.75 trillion) and then reckon the impact of an additional $80 billion. It’s a drop in the bucket, Baby.

Jacking the top tax rate to 70% on the super-wealthy would only raise a total of $180 billion, a nice boost but hardly enough to fund trillion dollar increases in federal spending.

This brings us to the second reality: it’s much cheaper to buy political adjustments to the new taxes via lobbying and campaign contributions than paying the extra $180 billion. A mere $10 million will buy a great deal of political adjustments, and $100 million will get pretty much whatever you need in the way of political adjustments.

The list of special dispensations and obscure tax code loopholes is endless: the wealth can be protected in a philanthro-capitalist family trust, or an overseas holding company, or taxed at a much lower rate for creating jobs in America (or equivalent political cover)– the ways to escape a 70% tax rate via political adjustments is truly infinite.

No super-wealthy individual or household is going to pay billions in additional taxes when a fraction of that will purchase political adjustments. From the point of view of the super-wealthy, 2/3 of whom are self-made via building businesses, they already pay enough taxes, and they have the wherewithal to get politicos to agree with them.

Here are the two little problems with “taxing the rich” to pay for trillions of dollars in new freebies:

1. Taxing the super-rich won’t really move the needle much when the federal government spends $4.7 trillion annually.

2. Trying to double the taxes they pay from 35% to 70% will only push them to increase their their spending on political adjustments that cost a fraction of the proposed taxes they will pay if they do nothing.

Tax Rates (CBO):

Federal Expenditures (current fiscal year):

* * *

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.

via ZeroHedge News http://bit.ly/2XQTCgP Tyler Durden

After lagged (govt shutdown) and mixed performances in the last two months, income and spending growth was expected to rebound notably in March (despite a weak signal from within the GDP data) and while income growth was lower than expected (+0.1% MoM vs +0.4% MoM exp), spending exploded…

Personal Spending rose 0.9% MoM (well above the 0.7% expected) and the biggest rise since August 2009…

On a year over year basis, spending has accelerated beyond income growth once again…

On the income side, wages unchanged from last month on an annual basis:

Private workers +4.4% Y/Y

Govt Workers +3.0% Y/Y

And as expected given the surge in spending, the savings rate collapsed from 7.3% to 6.5% – the lowest since November.

This is the biggest monthly drop in the savings rate since Jan 2013.

At the same time the Core PCE Deflator is at its lowest since 2017…

…allowing ‘goldilocks’ narratives to flourish ahead of this week’s FOMC.

via ZeroHedge News http://bit.ly/2PC4Z9A Tyler Durden

The United States has recorded a whopping 695 cases of measles in 22 states, its largest outbreak since public health officials in 2000 declared the disease “eradicated” apparently rather prematurely.

The outbreak has led to fines being imposed in major cities and the quarantine of over 1,000 as the outbreak spread across Los Angeles universities.In fact, according to the latest CDC numbers, the number of measles cases registered four months into 2019 has surpassed the count of cases from last decade. All new cases since the eradication declaration have come from foreign travelers.

On Monday, the CDC on Monday is due to release the latest updated figures on the number of cases recorded so far this year. Here are key facts about the outbreak:

Sources: U.S. CDC, World Health Organization, public health offices in New York State and City, Washington state, California and Michigan

via ZeroHedge News http://bit.ly/2UQM37P Tyler Durden

Ahead of Boeing CEO Dennis Muilenburg’s first showdown with shareholders since the March 10 crash of Ethiopian Airlines flight 302, the FAA has drawn attention to recent reports about dangerous hydraulic leakages involving the Boeing 787, otherwise known as the ‘Dreamliner’.

The regulator is imposing a new ‘flight directive’ on Dreamliners, meaning planes could be grounded if they don’t undergo additional rounds of inspections and records checks to make sure parts including the aileron and elevator power control units are still working properly.

Shares dumped as this news added to anxieties about a weekend report about Boeing’s failure to alert the FAA and Southwest, its biggest customer, that it had disabled an important safety feature on the 737 MAX 8.

Still, Boeing shares are – incredibly – still up 17% on the year.

via ZeroHedge News http://bit.ly/2J27CQD Tyler Durden