Whole Foods CEO Warns: ‘Capitalism Cannot Be Replaced With Disastrous Socialism’ Tyler Durden

Sun, 11/29/2020 – 23:00

Global leaders are using the virus pandemic to exert control over the world’s population under the guise of preventing the spread of COVID-19. The pandemic has provided elites with an opportunity to reset the global economy and abandon capitalism for socialism.

In the US, business leaders and politicians are fretting over a socialist system under a Biden presidency.

Whole Foods founder and CEO John Mackey recently spoke with America Enterprise Institute’s President Robert Doar about what socialism would mean for the country. Mackey called it a “failed system that “impoverishes everything,” according to Just The News.

While referring to the criticism of “trickle-down economics,” Mackey told Doar that socialism means “trickle up poverty.”

“We have to recognize that some of the progressive insights are important and they shouldn’t go away, but we can’t throw out capitalism and replace it with socialism, that will be a disaster,” he said. “Socialism has been tried 42 times in the last 100 years, and 42 failures, it doesn’t work, it’s the wrong way. We have to keep capitalism, I would argue, we need conscious capitalism.”

Mackey said one of the biggest problems plaguing the capitalism versus socialism debate is that businesses and corporations’ motivations are often misunderstood by the working-class.

“Until we get this corrected, capitalism is always going to be disdained and criticized and attacked,” he said. “It’ll be attacked for its motivations, because its motivations are seen as somehow impure. Yes, of course, business has to make money. If a business doesn’t make money, it will fail, but that doesn’t mean that its purpose is to make money.”

He said the business community must convey the benefits of capitalism to the livelihoods of Americans, otherwise, the implementation of socialism will mean a path to poverty for all.

“It needs to evolve, otherwise the socialists are going to take over — that’s how I see it, and that’s the path of poverty,” he said. “They talk about trickle down wealth, but socialism is trickle up poverty. It just impoverishes everything, that’s my fear, that the Marxists and socialists, the academic community is generally hostile to business. It always has been. This is not new.”

Mackey explained that the US’ university system is “anti-capitalist.” He said it starts with the lack of “business people” teaching in college business programs.

“Intellectuals teach, mostly intellectuals, who’ve never actually been in business at all, right? It’s very interesting,” he said. “And who don’t actually understand business, who don’t particularly understand entrepreneurship, and actually can oftentimes be hostile towards the very thing they’re teaching. So that’s a particular challenge.”

Watch Full Interview:

Despite Mackey’s strong dislike for socialism, Whole Foods has been described as a fairly liberal company. In the past, he has identified as a self-proclaimed libertarian.

And it wasn’t just Mackey last week with a warning about socialism – Republican Senator Tim Scott from South Caroline told Fox News that if Democrats win the two Senate seats in the Georgia runoffs in January, the left will transform America into a socialist state, adding that it would be ‘game over for our nation’.

“There’s no doubt when you think of the elections in Georgia, it’s not simply controlling the Senate, it’s controlling the legislative agenda for America,” said Scott.

An elitist attempt to push socialism could spell disaster for the country and mean more control over society.

via ZeroHedge News https://ift.tt/33oa0L5 Tyler Durden

Reasons why the 2020 presidential election is deeply puzzling

To say out-loud that you find the results of the 2020 presidential election odd is to invite derision. You must be a crank or a conspiracy theorist. Mark me down as a crank, then.

I am a pollster and I find this election to be deeply puzzling. I also think that the Trump campaign is still well within its rights to contest the tabulations. Something very strange happened in America’s democracy in the early hours of Wednesday November 4 and the days that followed. It’s reasonable for a lot of Americans to want to find out exactly what.

First, consider some facts.

President Trump received more votes than any previous incumbent seeking reelection. He got 11 million more votes than in 2016, the third largest rise in support ever for an incumbent. By way of comparison, President Obama was comfortably reelected in 2012 with 3.5 million fewer votes than he received in 2008.

Trump’s vote increased so much because, according to exit polls, he performed far better with many key demographic groups. Ninety-five percent of Republicans voted for him. He did extraordinarily well with rural male working-class whites.

He earned the highest share of all minority votes for a Republican since 1960. Trump grew his support among black voters by 50 percent over 2016. Nationally, Joe Biden’s black support fell well below 90 percent, the level below which Democratic presidential candidates usually lose.

Trump increased his share of the national Hispanic vote to 35 percent. With 60 percent or less of the national Hispanic vote, it is arithmetically impossible for a Democratic presidential candidate to win Florida, Arizona, Nevada, and New Mexico. Bellwether states swung further in Trump’s direction than in 2016. Florida, Ohio and Iowa each defied America’s media polls with huge wins for Trump. Since 1852, only Richard Nixon has lost the electoral college after winning this trio, and that 1960 defeat to John F. Kennedy is still the subject of great suspicion.

Midwestern states Michigan, Pennsylvania, and Wisconsin always swing in the same direction as Ohio and Iowa, their regional peers. Ohio likewise swings with Florida. Current tallies show that, outside of a few cities, the Rust Belt swung in Trump’s direction. Yet, Biden leads in Michigan, Pennsylvania, and Wisconsin because of an apparent avalanche of black votes in Detroit, Philadelphia, and Milwaukee. Biden’s ‘winning’ margin was derived almost entirely from such voters in these cities, as coincidentally his black vote spiked only in exactly the locations necessary to secure victory. He did not receive comparable levels of support among comparable demographic groups in comparable states, which is highly unusual for the presidential victor.

We are told that Biden won more votes nationally than any presidential candidate in history. But he won a record low of 17 percent of counties; he only won 524 counties, as opposed to the 873 counties Obama won in 2008. Yet, Biden somehow outdid Obama in total votes.

Victorious presidential candidates, especially challengers, usually have down-ballot coattails; Biden did not.

The Republicans held the Senate and enjoyed a ‘red wave’ in the House, where they gained a large number of seats while winning all 27 toss-up contests. Trump’s party did not lose a single state legislature and actually made gains at the state level.

Another anomaly is found in the comparison between the polls and non-polling metrics. The latter include: party registrations trends; the candidates’ respective primary votes; candidate enthusiasm; social media followings; broadcast and digital media ratings; online searches; the number of (especially small) donors; and the number of individuals betting on each candidate.

Despite poor recent performances, media and academic polls have an impressive 80 percent record predicting the winner during the modern era. But, when the polls err, non-polling metrics do not; the latter have a 100 percent record. Every non-polling metric forecast Trump’s reelection. For Trump to lose this election, the mainstream polls needed to be correct, which they were not. Furthermore, for Trump to lose, not only did one or more of these metrics have to be wrong for the first time ever, but every single one had to be wrong, and at the very same time; not an impossible outcome, but extremely unlikely nonetheless.

Atypical voting patterns married with misses by polling and non-polling metrics should give observers pause for thought. Adding to the mystery is a cascade of information about the bizarre manner in which so many ballots were accumulated and counted.

The following peculiarities also lack compelling explanations:

1. Late on election night, with Trump comfortably ahead, many swing states stopped counting ballots. In most cases, observers were removed from the counting facilities. Counting generally continued without the observers

2. Statistically abnormal vote counts were the new normal when counting resumed. They were unusually large in size (hundreds of thousands) and had an unusually high (90 percent and above) Biden-to-Trump ratio

3. Late arriving ballots were counted. In Pennsylvania, 23,000 absentee ballots have impossible postal return dates and another 86,000 have such extraordinary return dates they raise serious questions

4. The failure to match signatures on mail-in ballots. The destruction of mail in ballot envelopes, which must contain signatures

5. Historically low absentee ballot rejection rates despite the massive expansion of mail voting. Such is Biden’s narrow margin that, as political analyst Robert Barnes observes, ‘If the states simply imposed the same absentee ballot rejection rate as recent cycles, then Trump wins the election’

6. Missing votes. In Delaware County, Pennsylvania, 50,000 votes held on 47 USB cards are missing

7. Non-resident voters. Matt Braynard’s Voter Integrity Project estimates that 20,312 people who no longer met residency requirements cast ballots in Georgia. Biden’s margin is 12,670 votes

8. Serious ‘chain of custody’ breakdowns. Invalid residential addresses. Record numbers of dead people voting. Ballots in pristine condition without creases, that is, they had not been mailed in envelopes as required by law

9. Statistical anomalies. In Georgia, Biden overtook Trump with 89 percent of the votes counted. For the next 53 batches of votes counted, Biden led Trump by the same exact 50.05 to 49.95 percent margin in every single batch. It is particularly perplexing that all statistical anomalies and tabulation abnormalities were in Biden’s favor. Whether the cause was simple human error or nefarious activity, or a combination, clearly something peculiar happened.

If you think that only weirdos have legitimate concerns about these findings and claims, maybe the weirdness lies in you.

via ZeroHedge News https://ift.tt/3fUSjHZ Tyler Durden

Tesla Now Building Third Gen Superchargers In China Tyler Durden

Sun, 11/29/2020 – 22:00

In what appears to us to be a continuing push to eventually become a Chinese company, Tesla will soon be producing its third generation electric Superchargers in China, in addition to vehicles it already manufactures there.

The company said it’ll start producing the chargers in 2021, according to Reuters. It plans on investing $6.4 million in a new factory to help make its third generation of chargers, called the Supercharger V3.

It’s no surprise Musk is eager to expand in China, having called the country “smart” and “hard working” back in August of this year. The Tesla CEO – who has made himself billions off the back of U.S. government subsidies and the U.S. taxpayer – took to the “Daily Drive” podcast over the summer to make it clear exactly what country his allegiances lie with.

On the podcast, reported by CNBC, he called the people of China “smart” and “hard working” while at the same time calling U.S. citizens “entitled” and “complacent”. He specifically called out both New York and California, states whose taxpayers have literally funded Tesla’s business with massive tax breaks amounting to billions.

When asked about China as an EV strategy leader worldwide, Musk responded: “China rocks in my opinion. The energy in China is great. People there – there’s like a lot of smart, hard working people. And they’re really — they’re not entitled, they’re not complacent, whereas I see in the United States increasingly much more complacency and entitlement especially in places like the Bay Area, and L.A. and New York.”

He then compared the U.S. to losing sports teams: “When you’ve been winning for too long you sort of take things for granted. The United States, and especially like California and New York, you’ve been winning for too long. When you’ve been winning too long you take things for granted. So, just like some pro sports team they win a championship you know a bunch of times in a row, they get complacent and they start losing.”

Recall, Tesla secured $1.6 billion in loans from the Chinese government to help build its Shanghai factory, which helped the company resume normal operations post-Covid this year.

Musk – apparently completely devoid of any humility to the amount of money he has received from the U.S. taxpayer – defended his company by saying over the summer it hadn’t received as much government support from the Chinese government as most competitors: “They have been supportive. But it would be weird if they were more supportive to a non-Chinese company. They’re not.”

Tesla’s total government assistance in the U.S. has surpassed $4.9 billion, according to CNBC.

Recall, just weeks ago we also reported that Tesla’s Supercharger network in Australia now officially costed more than gas. The news came as a result of a “recent price increase” to use the Superchargers and – stop us if you’ve heard this one – “incorrect fuel figures on the Tesla website”.

This, of course, puts an end to Tesla’s years long claims that recharging its vehicles offered savings versus traditional internal combustion engine vehicles.

“According to Tesla the cost of charging a Tesla Model 3 is $7 per 100km compared with $12 for a rival petrol car,” WhichCar notes, before revealing the estimate uses “at least three incorrect figures”. The report disputes “how much electricity a Tesla Model 3 uses, the cost of electricity at a Tesla Supercharger and the price of petrol.”

It also notes Tesla’s increase for its Supercharger to 52 cents per kilowatt-hour. The article calculates this recharging “even the most efficient” Model 3 Standard Range would cost $9.78 per 100km using a Supercharger.

via ZeroHedge News https://ift.tt/36lA7UA Tyler Durden

I’ve always much enjoyed the work of Virginia Postrel (who, among many other things, was once the editor-in-chief of Reason), and I’m delighted to report that she’ll be guest-blogging this week about her new book, The Fabric of Civilization: How Textiles Made the World. From the publisher’s description:

The story of humanity is the story of textiles—as old as civilization itself. Since the first thread was spun, the need for textiles has driven technology, business, politics, and culture.

In The Fabric of Civilization, Virginia Postrel synthesizes groundbreaking research from archaeology, economics, and science to reveal a surprising history. From Minoans exporting wool colored with precious purple dye to Egypt, to Romans arrayed in costly Chinese silk, the cloth trade paved the crossroads of the ancient world. Textiles funded the Renaissance and the Mughal Empire; they gave us banks and bookkeeping, Michelangelo’s David and the Taj Mahal. The cloth business spread the alphabet and arithmetic, propelled chemical research, and taught people to think in binary code.

Assiduously researched and deftly narrated, The Fabric of Civilization tells the story of the world’s most influential commodity.

And just part of the suitably electic collection of blurbs:

“We are taken on a journey as epic, and varying, as the Silk Road itself… [The Fabric of Civilization is] like a swatch of a Florentine Renaissance brocade: carefully woven, the technique precise, the colors a mix of shade and shine and an accurate representation of the whole cloth.”

―New York Times

“From the Stone Age to Silicon Valley, textiles have played a central role in the history of the world. Virginia Postrel has an encyclopedic knowledge of the subject but she imparts it with a touch as light as Penelope’s at the loom. Ambitious, erudite, and absorbing, The Fabric of Civilization is both an education and a pleasure to read.”―Barry Strauss, author of Ten Caesars: Roman Emperors from Augustus to Constantine

“Virginia Postrel has created a fascinating history of textiles from their Palaeolithic beginnings to the present and future—from the earliest plant fibers plucked from weeds to synthetic fabrics with computer chips in the threads. And why, you say, should we examine mere cloth? Precisely because it fills more and more roles in our lives, yet we take it for granted…. Well researched and highly readable, the book is a veritable treat.”

―Elizabeth Wayland Barber, author of Women’s Work: The First 20,000 Years Women, Cloth, and Society in Early Times and Prehistoric Textiles

“A fascinating, surprising and beautifully written history of technology, economics, and culture, told through the thread of textiles, humanity’s most indispensable artefacts. I loved it.”

―Matt Ridley, author of How Innovation Works

“The story of technology is a story of human ingenuity, and nowhere is this more clear than in the story of textiles: the original technology, going beyond what we commonly think of as ‘tech.’ As with many technologies, we suffer an amnesia about them when we enjoy them in abundance, as Postrel observes; her book gives us back our memories about this technology that we use every day without even knowing it.”

―Marc Andreessen, co-founder, Netscape and Andreessen Horowitz

“Cleanly written and completely accessible, this book opens up an entirely new world of textiles, explaining the most ancient archeological fabrics and the latest polymer blends that cool the body—not warm it as textiles have done for thousands of years—with equal verve.”

―Valerie Hansen, author of The Year 1000: When Explorers Connected the World—and Globalization Began

“Postrel’s brilliant, learned, addictive book tells a story of human ingenuity…. Her deep story is of the liberty that permitted progress. Presently the descendants of slaves and serfs and textile workers got closets full of beauty, and fabric for the cold, a Great Enrichment since 1800 of three thousand percent.”

―Deirdre Nansen McCloskey, author of the Bourgeois Era trilogy

“Fascinating and wide-ranging… This is an engrossing and illuminating portrait of the essential role fabric has played in human history.”

―Publishers Weekly

I very much look forward to Virginia’s visit!

from Latest – Reason.com https://ift.tt/2JbJM7P

via IFTTT

If you are advocating for lockdowns, you are complicit in tearing families apart. You are complicit in inflicting untold suffering on millions of people around the world. You are complicit in casting the poorest and most vulnerable in our societies into even further grinding poverty. You are complicit in murder.

In 2006, a 15-year-old high school student from Albuquerque, New Mexico won third place in the Intel science and engineering fair for her project on slowing the spread of an infectious pathogen during a pandemic emergency. Using a computer simulation that she developed with the help of her father, she argued that in order to slow the spread of the disease, governments should implement school shutdowns, keep kids at home and enforce social distancing.

Incredibly, that third place high school science fair project can be tied directly to the lockdown policies being implemented by governments around the world today. You see, that father that she developed her computer simulation with was no average doting dad, but a senior researcher at Sandia National Laboratories who at that time was working on pandemic emergency response plans for the US Department of Homeland Security. His proposal to implement school shutdowns and, if need be, workplace shutdowns in the event of a pandemic emergency was developed at least in part in response to his daughter’s high school project.

Now those advocating for lockdowns have seen the destruction and death that those policies have wrought this year and we are living through that right now. Not only are people being deprived of their livelihoods and forced into grinding poverty as a direct result of these shutdowns, but now the undeniable truth is that if you are advocating for lockdowns, you are advocating for some portion of the population to be consigned to death.

This is no longer debatable. It is even openly admitted—although months too late by the World Health Organization.

DAVID NABARRO: I want to say it again: we in the World Health Organization do not advocate lockdowns as a primary means of control of this virus. [. . .] We may well have a doubling of world poverty by early next year. We may well have at least a doubling of child malnutrition because children are not getting meals at school and their parents and poor families are not able to afford it.

This is a terrible, ghastly global catastrophe, actually. And so we really do appeal to all world leaders: stop using lockdown as your primary control method. Develop better systems for doing it. Work together and learn from each other. But remember, lockdowns just have one consequence that you must never, ever belittle, and that is making poor people an awful lot poorer.

This is the point at which, no doubt, I’ll be expected to produce the data to back up the non-controversial observation that lockdowns kill, even though that data will do precisely nothing to penetrate the consciousness of those who have already decided that they occupy the moral high ground for advocating locking billions of people around the globe as prisoners inside their own homes. But persevere I will.

I’ll point, for example, to the letter signed by hundreds of doctors calling the lockdowns themselves a “mass casualty incident” and exhorting politicians to end the shutdowns.

I’ll point to the research that shows that thousands of people will die because of delays to cancer surgery treatments as a result of the medical shutdowns.

I’ll point to the research of the Well-Being Trust showing that 75,000 Americans are expected to die deaths of despair—including alcohol and drug misuse and suicide—this year alone as a result of the lockdowns.

I will point to the research of The Lancet showing that 265 million people are expected to be thrown into severe food insecurity as a result of these lockdowns.

I will even point to the research showing 125,000 children are expected to die from malnutrition as a result of these lockdowns.

But, as I say, none of these deaths will matter to those who have already decided that they are right and virtuous for advocating locking vast swathes of the human population inside their own homes to starve to death in the name of slowing the spread of a disease that even the epidemiologists who have been wrong about everything this year tell us will kill less than one percent of the infected.

Yes, slowing the spread, not stopping the spread. This was never about stopping a pandemic. Even the lockdown advocates never advocated that. But somehow that has been forgotten and “15 days to flatten the curve” has turned into a never-ending carte blanche for the biosecurity state to implement any number of draconian policies on its population, any number of policies on the checklist of the would-be dictator. Not only locking people inside their own homes, but constant surveillance of the population through the contact tracing and tracking apps that are increasingly being implemented around the globe, and, inevitably, the proposals for mandating the experimental vaccines which agents of the state will forcibly inject into people against their will.

This is not acceptable.

We cannot allow this to stand.

If we forsake this, our most basic right—the right to step foot outside of our own homes—then we forsake our humanity itself. An important part of what makes us human is being taken away from us in the name of stopping the spread of COVID-19.

But there is good news for those who have managed to retain their sanity in the time of insanity. We do not need a complicated plan in order to subvert this agenda. We do not need special deputization or to ask permission from the government. We do not need to join any particular political party or even any particular protest movement.

All we have to do is disobey these unlawful “orders.”

CASSIE ZERVOS: The persistent anti-lockdown protesters said they will not forget Melbourne’s strict 112 day measures as they took to the steps of Parliament. They carried signs saying “Don’t trust the government” and chanted for police to join them in their rally.

If you have managed to retain your sanity during this time of widespread insanity, I applaud you and wish to assure you that you are not alone. Many, many people all around the world are defying orders. They are protesting against these lockdowns. They are standing up. They are disobeying.

But of course the corporate controlled press don’t want you to know that disobedience is an option on the table and they will not report on this. But disobedience is an option.

Open your business. Leave your home. Do not ask for permission. Disobey.

To those who are still advocating for lockdowns, I encourage you to do so to the face of those parents who have lost their teenage children due to suicide as a direct result of the shutdowns and tell them that their child’s death doesn’t matter because it wasn’t listed as being due to COVID-19. Or do so to the face of the tens of thousands of others who have already lost loved ones as a direct result of these shutdown or the hundreds of thousands more who will die as long as these lockdowns endure.

If you are advocating for lockdowns, you are complicit in tearing families apart. You are complicit in inflicting untold suffering on millions of people around the world. You are complicit in casting the poorest and most vulnerable in our societies into even further grinding poverty. You are complicit in murder.

A line is being crossed right now. Which side of history are you on? Make your decision now and make it wisely, because your actions during these times will not be forgotten.

You have been warned.

via ZeroHedge News https://ift.tt/3mksUK5 Tyler Durden

I’ve always much enjoyed the work of Virginia Postrel (who, among many other things, was once the editor-in-chief of Reason), and I’m delighted to report that she’ll be guest-blogging this week about her new book, The Fabric of Civilization: How Textiles Made the World. From the publisher’s description:

The story of humanity is the story of textiles—as old as civilization itself. Since the first thread was spun, the need for textiles has driven technology, business, politics, and culture.

In The Fabric of Civilization, Virginia Postrel synthesizes groundbreaking research from archaeology, economics, and science to reveal a surprising history. From Minoans exporting wool colored with precious purple dye to Egypt, to Romans arrayed in costly Chinese silk, the cloth trade paved the crossroads of the ancient world. Textiles funded the Renaissance and the Mughal Empire; they gave us banks and bookkeeping, Michelangelo’s David and the Taj Mahal. The cloth business spread the alphabet and arithmetic, propelled chemical research, and taught people to think in binary code.

Assiduously researched and deftly narrated, The Fabric of Civilization tells the story of the world’s most influential commodity.

And just part of the suitably electic collection of blurbs:

“We are taken on a journey as epic, and varying, as the Silk Road itself… [The Fabric of Civilization is] like a swatch of a Florentine Renaissance brocade: carefully woven, the technique precise, the colors a mix of shade and shine and an accurate representation of the whole cloth.”

―New York Times

“From the Stone Age to Silicon Valley, textiles have played a central role in the history of the world. Virginia Postrel has an encyclopedic knowledge of the subject but she imparts it with a touch as light as Penelope’s at the loom. Ambitious, erudite, and absorbing, The Fabric of Civilization is both an education and a pleasure to read.”―Barry Strauss, author of Ten Caesars: Roman Emperors from Augustus to Constantine

“Virginia Postrel has created a fascinating history of textiles from their Palaeolithic beginnings to the present and future—from the earliest plant fibers plucked from weeds to synthetic fabrics with computer chips in the threads. And why, you say, should we examine mere cloth? Precisely because it fills more and more roles in our lives, yet we take it for granted…. Well researched and highly readable, the book is a veritable treat.”

―Elizabeth Wayland Barber, author of Women’s Work: The First 20,000 Years Women, Cloth, and Society in Early Times and Prehistoric Textiles

“A fascinating, surprising and beautifully written history of technology, economics, and culture, told through the thread of textiles, humanity’s most indispensable artefacts. I loved it.”

―Matt Ridley, author of How Innovation Works

“The story of technology is a story of human ingenuity, and nowhere is this more clear than in the story of textiles: the original technology, going beyond what we commonly think of as ‘tech.’ As with many technologies, we suffer an amnesia about them when we enjoy them in abundance, as Postrel observes; her book gives us back our memories about this technology that we use every day without even knowing it.”

―Marc Andreessen, co-founder, Netscape and Andreessen Horowitz

“Cleanly written and completely accessible, this book opens up an entirely new world of textiles, explaining the most ancient archeological fabrics and the latest polymer blends that cool the body—not warm it as textiles have done for thousands of years—with equal verve.”

―Valerie Hansen, author of The Year 1000: When Explorers Connected the World—and Globalization Began

“Postrel’s brilliant, learned, addictive book tells a story of human ingenuity…. Her deep story is of the liberty that permitted progress. Presently the descendants of slaves and serfs and textile workers got closets full of beauty, and fabric for the cold, a Great Enrichment since 1800 of three thousand percent.”

―Deirdre Nansen McCloskey, author of the Bourgeois Era trilogy

“Fascinating and wide-ranging… This is an engrossing and illuminating portrait of the essential role fabric has played in human history.”

―Publishers Weekly

I very much look forward to Virginia’s visit!

from Latest – Reason.com https://ift.tt/2JbJM7P

via IFTTT

China’s Xi Continues To Urge Troops Toward ‘War Readiness’ Over Taiwan Issue Tyler Durden

Sun, 11/29/2020 – 21:00

China’s President Xi Jinping has continued to tell his armed forces that they should prepare for potential war amid heightened hostilities with America, particularly over the Taiwan issue.

Speaking to a room full of People’s Liberation Army (PLA) leaders and officers at the Jingxi Hotel in Beijing this past week, Xi hailed the “new era” of a highly modernized fighting force which has transformed the PLA into a world-class fighting force.

The address to the Central Military Commission featured him ordering all officers and soldiers to focus on preparing for war “under real combat conditions,”according to quotes in state Xinhua News Agency.

PLA troops via AFP

He further stressed that the national soldiers must not “fear hardship and do not fear death” while committing further to deepening training.

“Military training is the regular and central task of the army. It is the basic way to generate and improve combat effectiveness. It is the most direct preparation for military battles,” said Xinhua, citing the chairman.

Over the past month Xi has toured various military bases while urging war preparations and readiness. This also comes as naval and air forces step up drills off China’s coast, particularly near the Taiwan Strait and in the South China Sea.

Western analysts and media have tended to interpret this latest jingoistic rhetoric as something more than just the usual military orders of ‘readiness’ common to all national militaries:

Earlier this month, China‘s state broadcaster released footage of the country’s soldiers launching multiple missiles to take down enemy targets during a live-fire drill.

China has been flexing its military muscles since tensions heightened between China and the United States over Taiwan.

Xi’s address to military officers last Wednesday, via CCTV

The outgoing Trump administration has vowed to keep up its pressure on Beijing, the latest actions which has included sanctioning PLA-linked China-based companies, even down to the final weeks leading to Biden’s inauguration on January 20.

The PLA consists of some two million active troops with a half million in reserve.

via ZeroHedge News https://ift.tt/3lgGrBj Tyler Durden

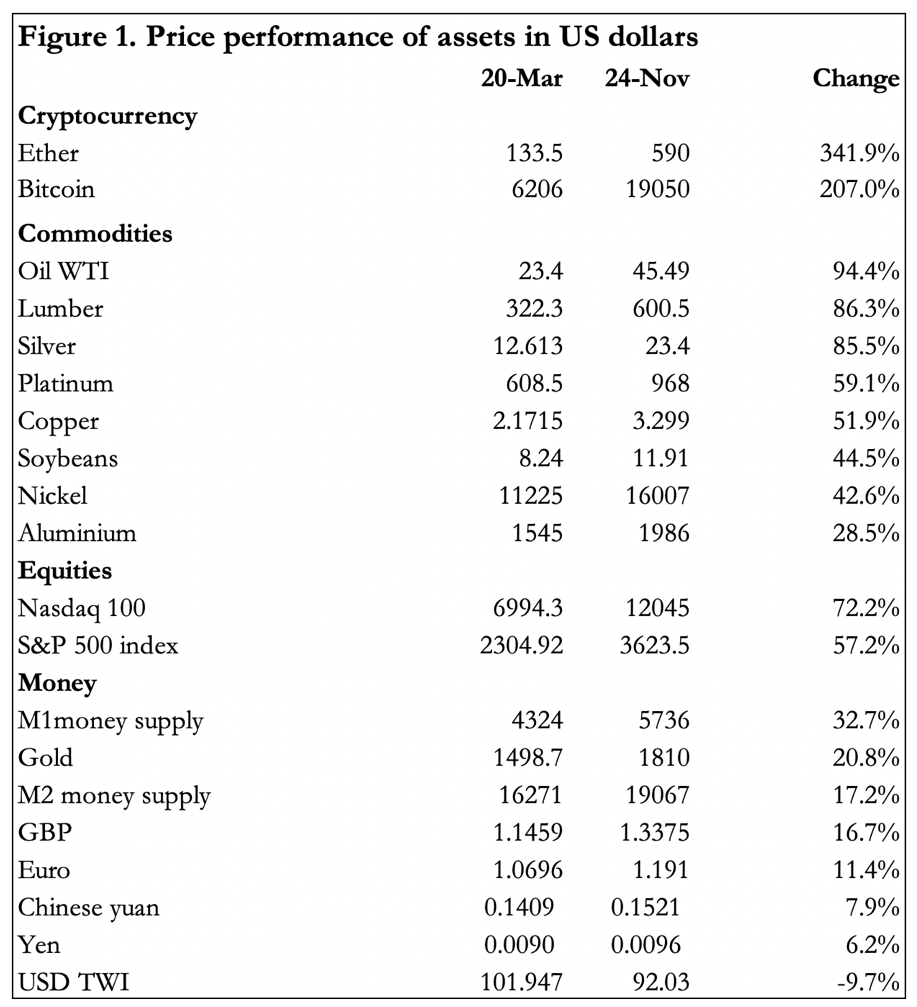

This article posits that fiat currencies are on the path to hyperinflation and looks at the evidence in the prices of financial assets and commodities. So far, gold has notably underperformed, which indicates that the early signals of hyperinflation are confined to the cryptocurrencies, whose participants broadly understand fiat debasement, to equities reflecting the desire not to maintain cash and deposit balances, and in international trade, where commodity prices of all stripes have risen in price.

Given that the early warnings of hyperinflation of money supply are here, the article then looks at the qualities required of a sound money to replace fiat currencies.

Introduction

Figure 1 shows how prices have moved from the Friday before the Fed’s announcement on 23 March that it would go all-in on its support for the US economy with unlimited quantitative easing. It amounted to a commitment to hyperinflate the money supply if needed. Before the Fed cut its funds rate to zero on 16 March nearly all these prices were falling.

Since late-March every category has seen increases in prices. Sector and specialist analysts will always claim that there are identifiable reasons why prices for an individual category or commodity have risen. But the fact is that with the exception of the dollar and the other fiat currencies listed in the table all prices have risen. This cannot happen without the dollar and these currencies losing purchasing power.

While being far from exhaustive in its representation, Figure 1 shows that on the back of existing and perhaps anticipated expansion of money supply, cryptocurrencies have seen the most substantial rises. Putting to one side the debate as to whether cryptocurrencies can be a replacement for fiat currencies, in the general population it is their followers who are most aware of fiat currency debasement. In a monetary inflation, the fact that a significant minority of economic actors understand what governments are doing to money early in the hyperinflationary process does not appear to have happened before. It invalidates the old saying that not one person in a million understands what is happening to their money.

More people are flocking to cryptocurrencies, and while they appear to be predominantly driven by the prospect of profit rather than seeking an insurance against the demise of their local currencies, we cannot doubt that most of them have learned the lessons about money that evaded their forebears.

That being the case, we can assume that far from being just a speculative bubble, the rise in prices for bitcoin, ether and other cryptocurrencies anticipates further falls in purchasing power for government currencies, yet to be reflected in the other categories.

The rise in commodity prices varies considerably, but at a time of global economic slump, they are all higher not just in dollars, but measured in the other currencies represented in the table, which can only be a reflection of monetary debasement. Equities have also been strong with the more volatile NASDAQ 100 outpacing the S&P 500 index. And as if to ram the point home commodities and equity prices fell heavily on deflationary fears before the Fed’s unending stimulus was announced in March, only recovering and rising subsequently. The divide between deflationary and inflationary expectations could not be more marked.

Not all items in Figure 1 turned higher precisely on 20—23 March. Gold bottomed at $1452 earlier on 16 March, the day when the Fed cut its funds rate to zero. It rallied before falling to test $1456 on 20 March before closing at $1498.7. Nevertheless, a rise of 20.8% puts it between the increase in M1 money supply and M2. The WTI Oil price went negative on 20 April due to delivery problems on Comex before recovering strongly to rise over 90% on balance from late-March.

In the currencies, only the euro and sterling rose more than the dollar’s trade weighted index fell. And priced in all these currencies, the other items in Figure 1 increased.

The relationship between money and prices

There is usually a time lag between an expansion of the money quantity and its effect on prices, depending on the route it takes to full circulation. The lack of any distinction between existing and new circulating currency conceals its existence. And while every economic actor knows that government money loses purchasing power over time, it is still regarded by transacting parties as having the objective value while variations in price are reflected entirely in the goods or services being exchanged.

If the distribution of new money is channelled through increased government spending targeted at one part of the total economy, then the price effect is initially confined to a few corporations and locations in the sectors concerned, before it spreads to the wider economy before being disseminated by employees, contractors and subsidiary businesses. Alternatively, if money is distributed widely by a representational helicopter, the price effect is more instantaneous because it is more immediately spent mainly on consumer goods.

Even if the additional distribution of new money is made obvious to a population, it fails to grasp the consequences for the dilution of the existing stock of money. Like most analysts in the commodity markets, they initially think that prices are simply rising, and they fail to consider monetary debasement as the cause.

While the simple mathematical relationship between the quantity of money and the effect over time on prices is widely understood, other effects are less so. Changing the amount of money in circulation fatally corrupts statistical comparisons, yet financial analysts appear unaware of the profound differences between today’s money and that of the past. Furthermore, in more normal times the expansion and contraction of bank credit is usually a far larger variation of total money than its expansion by a central bank to fund a government deficit.

But the most profound effect on a money’s purchasing power comes when foreign owners of it domestic users gradually realise that the debasement will continue and even accelerate. Since 23 March, when the Fed told the world it would inflate limitlessly, there were two important categories of actors who immediately understood the inflation message. The first was the cryptocurrency community, as discussed above, and the second was the Chinese government, which accelerated its purchase of commodities, including iron ore, copper and oil. Wheat, cooking oil, and soybeans have followed. Predictably, commentators have seen the ramping up of commodity stockpiles, but not the unseen winding down of dollars. That is the point the Chinese appear to have understood, confirmed by the timing of accelerated commodity purchases. And their currency has also risen by nearly 8% against a weakening dollar, a marked change in official exchange policy.

Hyperinflation of the dollar is here

It is now impossible to envisage the US Government and the Fed limiting further monetary expansions. Their Keynesian creed tells them that to do so would be disastrous for the economy. By relying on macroeconomic beliefs upon which they base their policy decisions they cannot come up with an answer that ultimately saves the currency and the economy. They do not appear to realise that by transferring wealth to a generally non-productive government sector, monetary inflation impoverishes the productive capacity of the economy.

It is against this background that having seen one enormous budget-busting stimulus package from the US Government, we shall shortly see another. Apart from the unconventional cryptocurrency sector and perhaps equity markets, there is little evidence that markets are discounting the inflationary effects of a second package yet — they are awaiting the shape of the next inflationary stimulus. The gold price, having risen by about a fifth since 20 March, is certainly not yet reflecting hyperinflation.

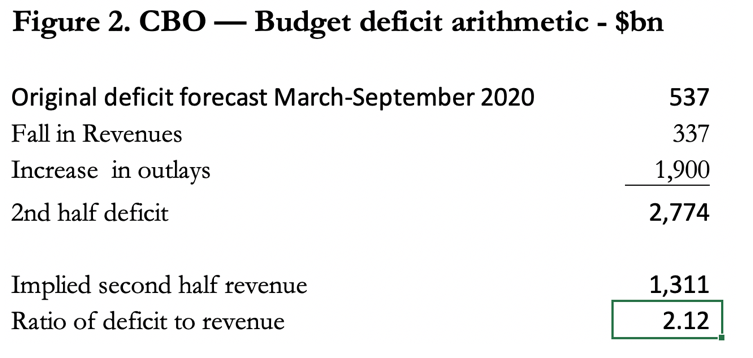

But it is worth looking at US Government finances since March, when the covid response commenced, leading to a fall in tax revenue and an increase in government spending. This is shown in Figure 2.

The numbers in the table reflect the US Government’s financing of federal expenditure following the Fed’s decision to implement limitless QE, and so covers the period of the first wave of coronavirus. From it, we can see that government spending rocketed to 2.12 times tax revenue. This is not so obvious in the annualised CBO figures, where the additional expenditure is spread over the whole fiscal year to September 2020. But with a second half deficit over twice government spending, government financing is roughly one-third by tax revenue and two-thirds by money printing. And this is not going to be a one-off event.

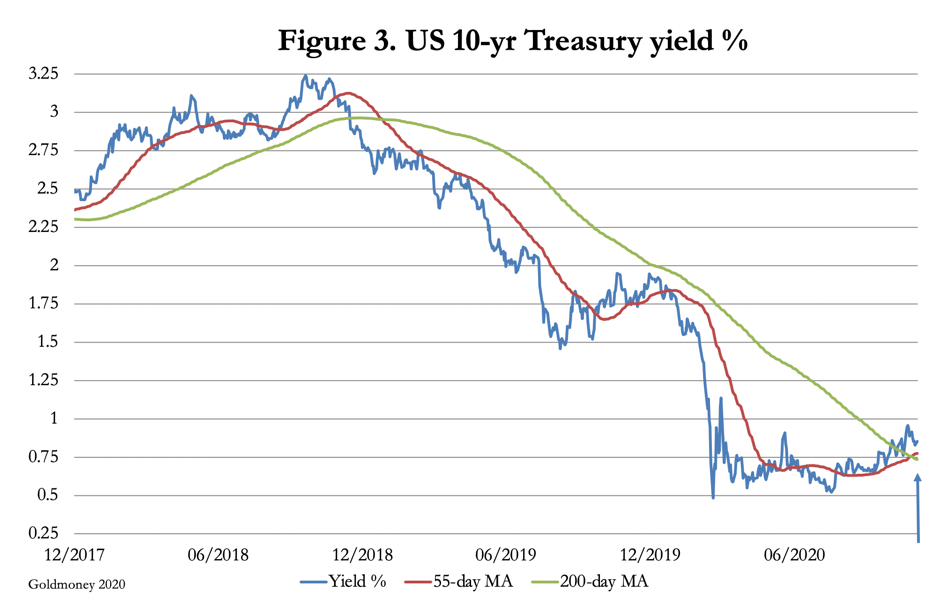

Along with the rest of the world, America has entered a second wave of infections, which will oblige the government to deploy a second similar, or even greater stimulus. The second covid wave is likely to lead to a further fall in tax revenues, as a result of bankruptcies from the initial coronavirus wave combining with the effects of the second. There is also a growing realisation that the economic problems from the virus alone will continue beyond the second wave. This fear is beginning to be reflected in the US Treasury bond market, with yields threatening to rise significantly, as illustrated in Figure 3.

The evidence from technical analysis strongly suggests the low point for the 10-year US Treasury bond yield has now passed and yields are set to rise significantly. That being the case, the Fed will find itself isolated as the only significant buyer as investors increasingly abandon Treasuries as a safe haven investment. And that is before we consider the position of foreign holders of US Treasuries and agency debt, with some of these key players having begun to reduce their holdings.

A further consideration concerning the purchasing power of the next tranche of monetary expansion will come into play. While it is yet to be reflected in consumer prices, with the dollar already diluted by over 30% of additional M1 money between March and September, for the government to obtain the same effect from debasing the currency the expansion of M1 money supply will have to increase by roughly 40% on the expanded base. An aphorism that states for every debasement, a larger one for the same effect will follow, applies. It is the other side of the transfer of wealth from the productive economy to the government which is consistently ignored by macroeconomists. And the more wealth is transferred from the productive private sector to a generally unproductive government, the less there is to transfer. And far from serving to stimulate the economy, these monetary transfers are impoverishing the economy and reducing the government’s tax base at an accelerating pace. The ratio of tax income to inflationary financing illustrated in Figure 2 then rapidly deteriorates from three of inflation to one of tax revenue.

The US Government’s dependency on inflationary financing is already a commitment with no palatable escape. Politicians are trapped by their earlier electoral promises. Assuming Biden is confirmed as the next US President, his left-leaning socialistic policies can only accelerate the debasement process.

As has been the case in many other advanced economies, the US financial system has predominantly supported zombie companies since the Lehman crisis. The increase in unproductive debt has been widely noted. A final collapse of the hampered economy simply cannot be avoided, only deferred. But assuming attempts will continue to be made to defer this outcome, the Fed and the Treasury between them will have to underwrite commercial bank loans and the bank credit extended to businesses that would otherwise collapse. Instead of an understanding of the consequences for hyperinflation of the money supply from covid-19 lockdowns, it will be the realisation that currency debasement must continue to prevent widespread bankruptcies of unproductive, labour intensive businesses that finally awakens the general public to the likely collapse of its government’s money.

The fallacy of the deflation argument

Keynesian economists who see global economic activity badly undermined by covid lockdowns will be confused by the tendency for prices of commodities to rise, because demand for them must be falling. They are almost certain to argue that price rises are probably a short-term aberration, and that lack of consumer demand and oversupply of products will begin to deflate prices. This is reflected in statements from leading central bankers. They envisage that without the support of increasing money supply, the failure of businesses in a deflationary environment will lead to the thirties-type deflation, which fed into multiple bank failures and record levels of unemployment. In other words, they believe there is a growing danger of a self-feeding deflationary slump.

The underlying mistake in the deflation argument was made long ago by dismissing Say’s law. Say’s law points out that we produce through the division of our labour in order to consume. Therefore, in approximate terms an increase in unemployment is matched by loss of production, so the supply and demand of consumer goods broadly remain in balance, but at a lower level of economic activity. The Keynesians only account for falling consumer demand without realising production also declines.

Instead of linking production and consumption through Say’s law, Keynesians imagine a decline in consumer demand due to rising unemployment releases unused production capacity. Understanding this error explains another phenomenon: in a contracting economy people will not increase their cash and deposit balances at a rate to match the expansion of the money supply. Being poorer from the wealth transfer to government through monetary inflation, people tend to reduce their money balances. This alters their money to goods preferences to the detriment of the money’s purchasing power, while more money from the central banks floods the markets.

The reason asset prices rise, followed by those of consumer goods, is a reflection of this desire not to increase money balances, and inevitably, then a tendency to begin reducing them takes hold. Today, this explains the rise in cryptocurrency and equity prices relative to fiat money, driven by the cohorts that are first to ditch a currency which is depreciating relative to their perceptions of financial security.

The Keynesians’ reference point was the appalling depression of the 1930s, which they blamed on gold. With gold, prices fell bankrupting farmers, other businesses and the banks. But farmers with their new tractors increased grain output around the world, the glut driving prices lower for nearly all foodstuffs. At the same time the banks ended a period of credit expansion, withdrawing loans from businesses, creating the usual cyclical slump. The difference from previous slumps was intervention, first by President Herbert Hoover and then by Franklin Roosevelt. It was the prototype Keynesian intervention that prolonged the slump, not the gold standard.

The misunderstanding of inflation-supporting economists and subsequent distortions of the historical truth about the depression have led the economic establishment to fully embrace inflationism, while condemning the deflation of prices as an evil. Again, this flies in the face of historical fact, because prices fell throughout the nineteenth century, improving the living standards of everyone and allowing the purchasing power of their savings to grow. Hard work and innovation were rewarded, while by permitting free markets the government let it all happen under a working gold standard.

One can only suppose that the unadmitted purpose of inflationism is not to improve the prospects for the ordinary individual but to enhance government revenue. That is certainly the outcome of macroeconomic beliefs which condemn deflation.

The case for gold as future money

Some of the reasons commonly put forward denying an inflation problem are notably fiat-centric. For example, a claim that the rise in cryptocurrencies and equity markets are speculative bubbles and not indicative of monetary instability. There is almost certainly truth in this, with a large element of investment always dedicated to trend-chasing rather than founded on reason. But those that take the view it is only speculation fail to get the signal, that what they might describe as unwarranted speculation is an early warning of the consequences of monetary inflation. These are the financial commentators who fail to realise that of any form of money, only sound money can truly reflect a sustainable objective value.

This brings us to metallic money, the gold and silver to which people have always defaulted when kings, emperors and governments fail to sustain their unbacked alternatives. In Figure 1 silver has been included in the commodity category, because with the gold/silver ratio at roughly 77 times it is not being priced for its monetary qualities. That may change. Until it does, we should consider the position of gold as the ultimate money while silver remains priced as an industrial metal, a situation that must nevertheless be kept under review. Furthermore, if governments are to stop the collapse of their currencies, that can only be done by mobilising central bank gold reserves to back them, or alternatively by linking their currencies to another which is fully convertible into gold at every holders’ option.

Apart from other significant hurdles, those who believe that cryptocurrencies will replace gold when fiat dies have the problem of explaining how bitcoin and other cryptocurrencies will be sanctioned as money by governments which have none in their monetary reserves. Instead, they are currently designing their own central bank digital currencies, through which, they hope, they can control economic activity and ultimately prices. If anything, in the face of technological innovation they are spurred on by a determination to keep control of all forms of currency for themselves.

The best hope for cryptocurrencies appears to be that fiat continues to exist and like the Argentine peso, never quite die. If and when they do elapse, or at least when the planners realise their battle is lost and that to prevent a complete monetary breakdown they must introduce proper backing for their currency, then states have the power and the means to ensure sound money is available within a matter of weeks. The only sound medium of exchange they can use is what they have to hand, and that is their gold reserves. Of course, if governments fail to back their currencies convincingly or rein in their spending — necessary to sustain gold backing credibly — cryptocurrencies might have a brief extension as stores of value.

Putting the cryptocurrency issue aside, the history of collapses in the purchasing power of fiat money allows us to rank stores of wealth. The best has always been gold, or other reputable currencies backed by gold and fully accepted by the public as gold substitutes. This time, there are none, so it must be physical gold. As noted above, the debauchment of fiat money impoverishes the private sector until there is no wealth left to be transferred by this means. In consequence, the purchasing power of gold rises to reflect its relative scarcity compared with the capital and consumer goods in the hands of distressed sellers who at the same time reject the government’s currency. Only then can we rank the capital goods relative to each other. Residential property and country estates which produce food come high on the list, as do equities of companies that manage to survive the currency collapse.

But these assets only rise measured in rapidly depreciating government currency. When the paper mark in Germany began its final collapse in 1923 a large house in a fashionable part of Berlin could be had for $100, at $20.67 to the ounce of gold, the equivalent of just under five ounces. Similarly, country estates could be had for ridiculously small amounts of gold-backed foreign currency.

The requirements for monetary flexibility

The argument promoted by bitcoin hodlers is that its future issuance is firmly capped at 21 million, and that with about 18.5 million already issued, of these many have been irretrievably lost. It is simply a supply argument, and if bitcoin replaces failing fiat the price will be sky-high.

This reasoning ignores the fact that a rigid quantity of money in circulation is an unworkable proposition. Prices of consumer items will lack the stability that sound money contributes to transactions. It would become impossible to do the business calculations required for capital investment, because assumptions about future values for both the repayment of debt and the eventual value of the business investment cannot be reasonably assessed. And we must remember that we are moving from a fiat world where through inflation value is transferred from saver to borrower. A significant value-transfer to the saver from the borrower, which would be the inevitable outcome of using bitcoin as the money, would therefore severely restrict entrepreneurial activity and hamper economic progress.

Gold is far more flexible, which is why it has always returned to be the peoples’ money when government money fails. In general terms, mine supply has always increase the level of above ground stocks at a rate similar to the world’s population growth, leading to long-term stability in the general level of prices. Furthermore, a large quantity of gold is not mobilised as money, but for other purposes, mainly jewellery. If the free market demand for monetary gold increases, scrap supply is there to augment gold used for monetary purposes, and if monetary demand diminishes relative to other uses, then scrap supply simply declines.

With gold, there is minimal transfer of value over time from savers to borrowers or vice-versa. The increase in purchasing power that gold-backed savings have enjoyed in the past has come not because of supply constraints of gold, but through competition and innovation of production methods and technology. This certainty always led to savings being protected and available for personal emergencies, retirement, and to pass on to families. And as well as funding personal and family welfare, therefore rendering state welfare provision virtually unnecessary, personal savings provided the monetary capital for businesses and entrepreneurs, who could reasonably calculate the profits from their investment, the money being sound.

Society under a gold standard enables its users to accumulate wealth, because its government, being generally unproductive by virtue of its bureaucracy and monopoly, would have to radically alter its expenditure commitments in order to discard inflationism. In the absence of this source of funding, the cost of government becomes fully exposed, and the tax burden cannot be increased sufficiently to replace it. With sound money, the state has no option but to cut its spending, and to reduce its interventionist roles.

Properly understood by the state authorities, the route to maximising their own power is to let free markets flourish with sound money. This was the wisdom of Britain’s leaders in the nineteenth century, which made this small nation the most powerful on earth. It was also understood by America’s Founding Fathers and America similarly became the most powerful nation after Britain’s decline.

But after decades of fiat money inflation, it is difficult for those steeped in macroeconomics to envisage a world where gold and fully backed gold substitutes are the only money. Much of the paraphernalia of risk management, derivatives and forward markets will no longer be needed and will disappear. Debt can only be taken out on the basis it is repaid when due, and assumptions that it can always be rolled over, or perhaps that the state will come to the rescue must be banished.

Other than the residual role of issuing gold substitutes, of maintaining gold reserves and overseeing the production and free circulation of gold coins, there will be no role for central banks and their planners. Stemming from the UK’s Bank Charter Act of 1844, the laws and regulations that permit the creation of unbacked bank credit should be revised either to make it a criminal offence in line with natural law, or to permit free banking with the removal of limited liability for the managers and shareholders. Only then can the expansion of unbacked money, the origin of which is credit expansion, be reined in. Crony capitalism, whereby an entity gains government support for its operations or to the disadvantage of its competitors, must also cease.

It must be admitted that politicians are unlike to benefit from a sudden Damascene conversion. The only thing that will be clear to them is the need to stabilise the currency, which they will probably have to fight against their own establishments to achieve. There will remain the considerable risk of political anarchy if wise leaders fail to take the public and their administrations with them, raising the prospect of Hayek’s Road to Serfdom.

All that is for the future — perhaps not so distant as we might think — for which cryptocurrencies and central bank digital currencies are not equipped. But today, while there is incontrovertible evidence that some economic actors are beginning to understand that hyperinflation of the money supply is taking hold, the modest performance of the gold price tells us that for the broader public this realisation is still in its early stages.

via ZeroHedge News https://ift.tt/3fOHvv9 Tyler Durden

House To Vote On Bill That Would Delist China-Based Companies If They Fail U.S. Audit Standards Tyler Durden

Sun, 11/29/2020 – 20:00

As we have already reported, U.S. lawmakers appear as though they are finally going to hold Chinese companies’ feet to the fire: they are going to require China based companies comply with audit oversight rules that U.S. companies must also abide by.

This voids a years long loophole that literally everyone on Wall Street knew about and led to numerous U.S. listed China based frauds totaling well into the billions of dollars.

On Wednesday, house leaders will hold another measure that would require shares to be removed from trading in the U.S. if the transition to an annual U.S. reviewed audit isn’t undertaken. The law would still give Chinese companies a generous three years to comply with new rules, the Wall Street Journal notes.

Beijing has been critical of the bill, as it will obviously allow them to commit far less fraud on U.S. capital markets. But the legislation has bipartisan support in the U.S. and could be signed by Trump – who is rumored to be looking at new crackdowns on China before leaving office – if it passes the House.

The Senate bill was sponsored by Sens. John Kennedy and Chris Van Hollen. Kennedy said: “The current policy that allows Chinese firms to flout the rules that American companies follow is toxic. I hope the House joins the Senate this week in unanimously passing this bill so it can start helping hardworking Americans.”

As we reported about 2 weeks ago, the proposal will be issued for public comment in December, and will address a problem that has plagued Chinese companies on U.S. capital markets for more than a decade: China hasn’t let the work of Chinese auditors be inspected.

This has been the key factor in a number of Chinese firms being halted and delisted from U.S. exchanges over the last decade, as short sellers like Citron Research and Muddy Waters Research have collectively worked, among others, to help expose innumerable frauds and misstatements from companies based in China. A movie, “The China Hustle“, was even made about the widespread fraud.

The PCAOB has been unable to get cooperation from China on a broad scale. The PCAOB has often had to sue Chinese audit firms and negotiate with Chinese regulators for more information. Now, new regulations could put the responsibility on the listing exchanges, like NASDAQ and NYSE, who choose to give credibility to China-based entities by accepting their listing fees and putting them on their well known exchanges.

In other words, it appears to us that U.S. exchanges seem to have no problem making people like Jack Ma into billionaires with U.S. capital, without even understanding the intricacies of the opaque businesses they choose to list.

The SEC is trying to get the plan in order before Chairman Jay Clayton leaves at the end of the year, as we noted earlier this month. The regulation could then be “tweaked” by an incoming Biden administration.

China has come up with the laughable excuse that it “is worried about auditors revealing strategic secrets held by domestic firms, some of which are majority-owned by the Chinese government”. In fact, the country signed into law this year a rule stating that its citizens can’t comply with overseas regulators without the government’s permission.

via ZeroHedge News https://ift.tt/33p5UCb Tyler Durden

Over the last several months we’ve gotten very used to communicating via video chat. Zoom, FaceTime, Google Hangouts, and the like have not only replaced most in-person business meetings, they’ve acted as a stand-in for gatherings between friends and reunions between relatives. Just a few short years ago, many of us would have found it strange to think we’d be spending so much time talking to people “face-to-face” while sitting right in our own homes.

Now there’s a new technology looming on the horizon that may one day replace video calls with an even stranger-to-contemplate, more futuristic tool: real-time, full-body holograms.

Picture this: you’re sitting in your living room having a cup of coffee when the phone-booth-size box in the corner dings, alerting you that you have an incoming call. You accept it, and within seconds your best friend (or your partner, your grandmother, your boss) appears in the box – in the form of millions of points of light engineered to look and sound exactly like the real person. And the real person is on the other end of the line, talking to you in real time as their holographic likeness moves around the box – you can see their gestures, body language, and facial expression just as if they were really there with you.

The closest approximation to this that you may have heard about was when a holographic version of the late Tupac Shakur performed at Coachella in 2012. The hologram was simultaneously highly detailed—the lines of Tupac’s washboard abs were clearly defined and visible—and somewhat blurry; after the opening “scene,” in which the hologram stood still, it was hard to see any of Tupac’s facial features.

The Tupac hologram was created by events tech company AV Concepts and Hollywood special effects studio Digital Domain, and reportedly cost at least $100,000. It seems holograms don’t come cheap; the afore-mentioned hologram box is currently going for $60,000.

The box is called an Epic HoloPortl, and it’s made by PORTL, a company whose founder was inspired by Tupac’s hologram; after seeing the 2012 performance, David Nussbaum quickly bought the patents for the technology that made it possible, and has been working on turning the tech into something useful, fun, and scalable ever since.

The Epic has high-resolution transparent LCD screens embedded into its interior walls. The person on the other end—the one appearing as a hologram, that is—just needs to have a camera and be standing against a white background. A camera on the Epic shows the sender the room and people he or she is being beamed to, essentially just like a Zoom call.

Last month PORTL raised $3 million in funding, led by Silicon Valley venture capitalist Tim Draper. Nussbaum says he’s sold a hundred Epics, has pre-orders “in excess of a thousand,” and dozens of the devices have already been delivered, with clients including malls, airports, and movie theaters (all places that aren’t very frequented today—but here’s hoping they’ll make a comeback when the pandemic subsides).

In fact, PORTL may not have gotten this funding if it weren’t for the pandemic; Nussbaum told TechCrunch that Draper pushed him to expand his vision for the company and its technology when the virus hit, likely anticipating that people will want new ways to communicate from a distance.

Few can afford to shell out $60k for a hologram booth, though (not to mention having space for a 7-foot-tall by 5-foot-wide by 2-foot-deep box), and Nussbaum knows it; his next project is to build a smaller, cheaper version of the Epic.

Even at a tenth of the current cost, the tech likely wouldn’t see widespread adoption by people wanting their own personal hologram portal at home. But there are many possible use cases beyond person-to-person communication.

Any venue or event that would typically hire famous people to appear in person—be they celebrities, academics, religious figures, or business leaders—could beam a hologram of those people in instead. The implications may be most significant for education and business; Nussbaum believes the CEOs of the not-too-distant future will conduct their meetings via hologram. “You can now make that very important personal emotional contact with people that you need to talk to without actually having to leave your office,” he said.

Whether this is true remains to be seen. Many of us have experienced Zoom fatigue over the course of the pandemic, becoming acutely aware that while it’s better than nothing, it’s also nothing like being in a room with someone in person; there’s only so much you can get from a face and voice on a screen.

Will a face and voice on a three-dimensional, life-sized hologram be better? Stay tuned to find out.

via ZeroHedge News https://ift.tt/3q5Uvky Tyler Durden

{kind=link}

{kind=link}