Biden Appointee Neera Tanden Spread the Conspiracy That Russian Hackers Changed Hillary’s 2016 Votes To Trump: Greenwald

Tyler Durden

Mon, 11/30/2020 – 09:45

Authored by Glenn Greenwald via greenwald.substack.com (emphasis ours)

The announcement that Joe Biden intends to nominate Neera Tanden as his Director of the Office of Management and Budget — a critical position overseeing U.S. economic and regulatory policy — triggered a wide range of mockery, indignation and disgust from both the left and the right. That should not be surprising: though a thoroughly mediocre and ordinary D.C. swamp creature from the perspective of both ideology and competence, Tanden’s uniquely unhinged, venomous, corrupt and pathologically dishonest conduct as a Clinton Family and DNC apparatchik and President of the corporatist-and-despot-funded Center for American Progress (CAP) has earned her a list of enemies far longer and more impressive than her accomplishments.

When news of her appointment broke, many of the journalists and activists she has spent years abusing, slandering, and lying about instantly stepped forward to compile just some of her worst political and behavioral lowlights. And some preliminary signs emerged that she might encounter difficulty in obtaining the Senate confirmation needed for her to assume this position. The Communications Director for GOP Senator John Cornyn of Texas announced that “Tanden stands zero chance of being confirmed” by the Senate.

Former Sanders campaign aide David Sirota hypothesized that “it is not a coincidence that they are putting Neera Tanden — the single biggest, most aggressive Bernie Sanders critic in the United States of America — specifically at OMB while Sanders is Senate Budget Committee ranking/chair.” Sirota’s statement suggests Biden’s nomination of Tanden was intended as yet more humiliation doled out to the Democratic-loyal Sanders left by cucking the Vermont Senator even further by forcing him to shepherd the confirmation of one of his most vicious and amoral attackers (who Sanders himself in 2019 vehemently denounced). But Sirota’s point also raises the prospect that Tanden’s nomination could even encounter trouble from that side of the aisle as well (given Sanders’ compliant and disciplined conduct over the last six months, it’s more likely we will see him roll out a literal red carpet for Tanden to walk on, gently toss red roses on it before she passes, and then serve her a glass of Chardonnay rather than meaningfully obstruct her confirmation).

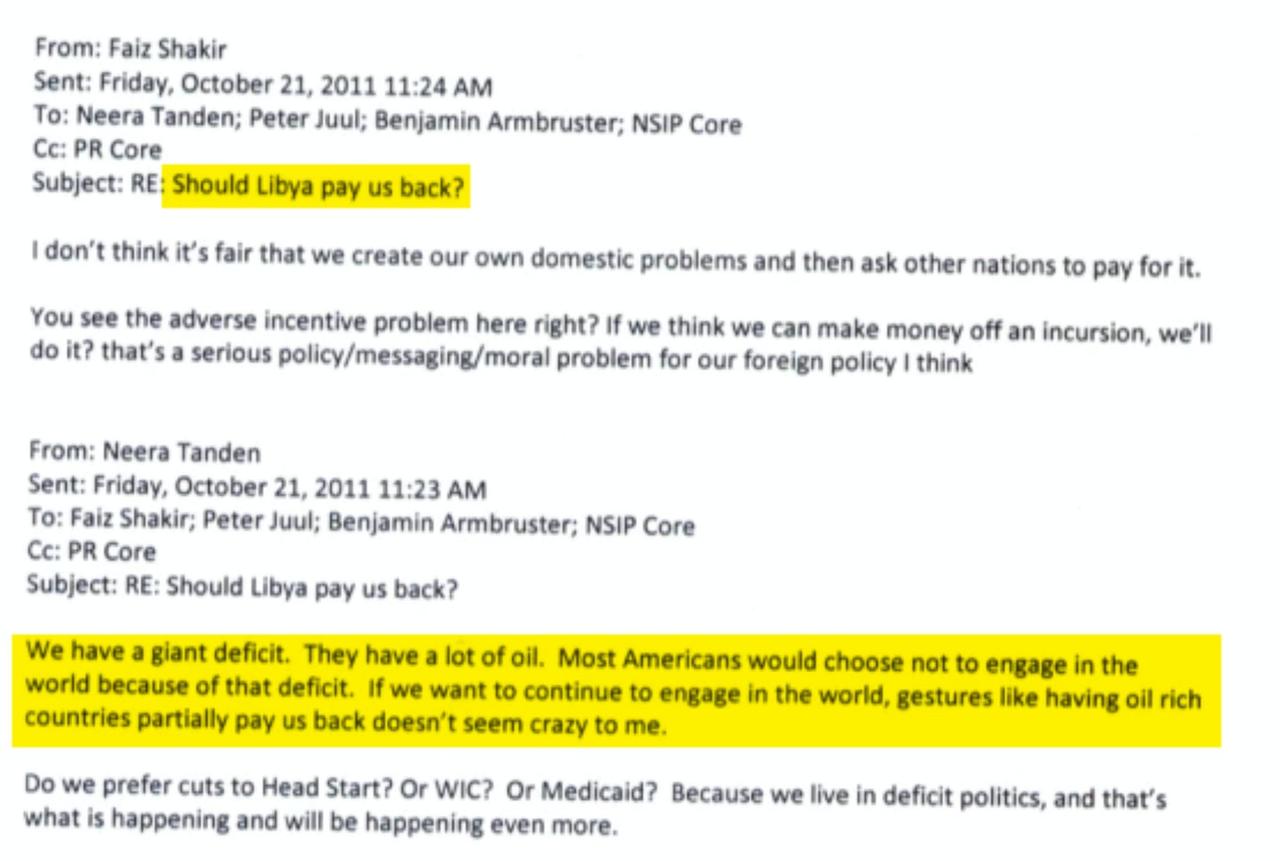

The list of sociopathic and even monstrous acts from Tanden is too long to list comprehensively. She punched one of her own employees, a reporter for CAP’s now-abolished blog ThinkProgress, after he had the temerity to ask Hillary Clinton in 2008 about her support for the Iraq War (Tanden claimed she “merely” had “pushed,” not punched, her undeferential reporter). In 2011, as the Obama administration was participating in the NATO bombing of Libya, Tanden suggested in internal CAP discussions that the U.S. steal Libya’s oil as a way of reducing the U.S. deficit (a story I was able to report only because Tanden had abused and alienated so many of her employees that they worked together to leak her incriminating emails to me).

During her tenure as CAP’s President, Tanden accepted millions of dollars from the regime of the United Arab Emirates, which built Dubai and Abu Dhabi using slave labor, along with massive donations from Facebook, Google, Microsoft, J.P. Morgan, the Walton Family and Michael Bloomberg, while hiding the identity of some of her think tank’s largest donors. A huge chapter on the NYPD’s abusive policies toward Muslims under Mayor Michael Bloomberg was removed from a CAP report after Boomberg donated more than $1 million to Tanden’s organization, and he continued to donate even more after that courteous gesture.

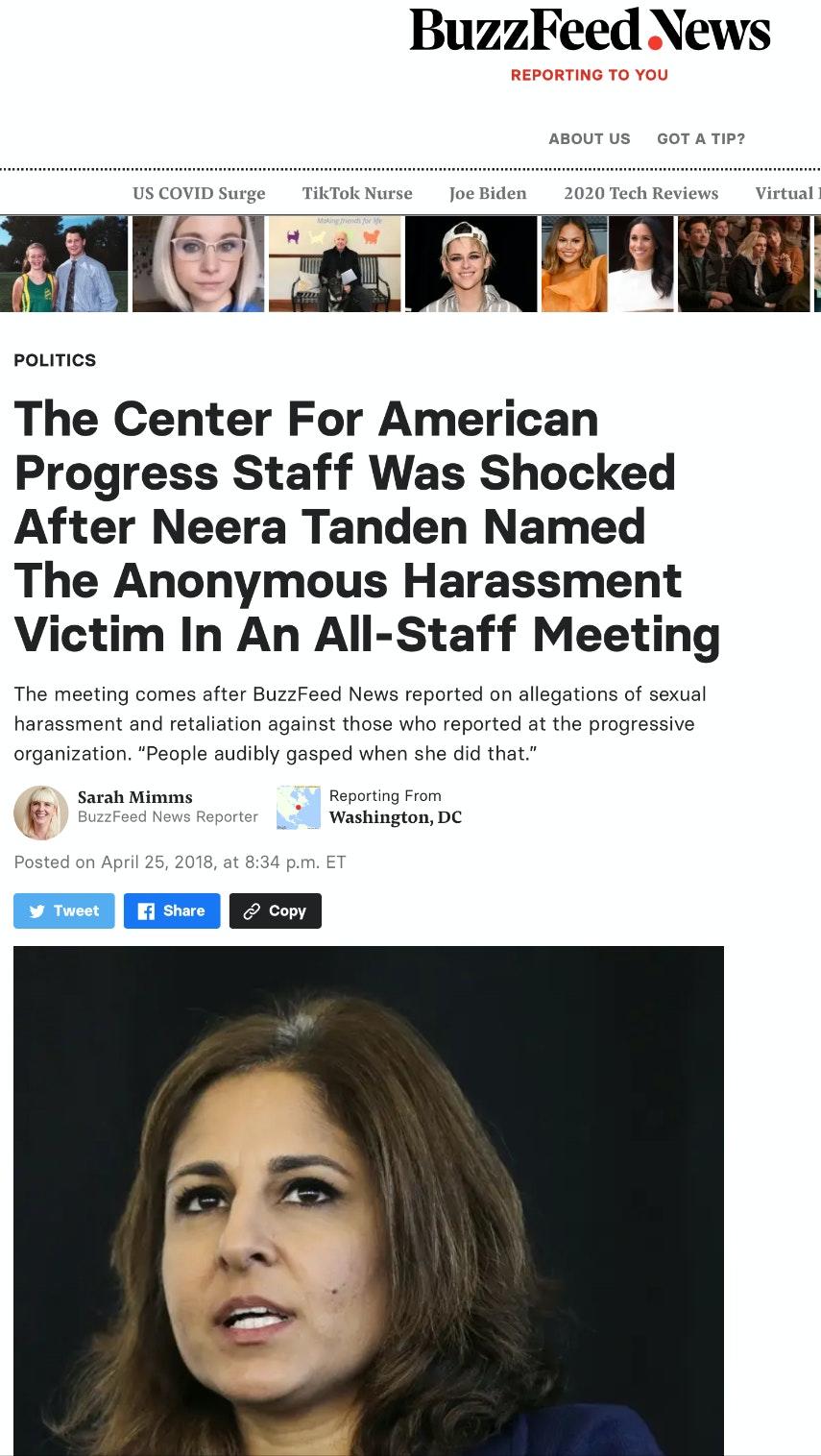

She ordered the supposedly independent journalists of the ThinkProgress blog, including Muslim writers, to stop writing critically about Israel after key CAP donors, including Barney Frank’s sister Ann Lewis and long-time Clinton advisor Howard Wolfson, complained. She and Wolfson plotted in 2016 how to weaponize female journalists and people of color against Hillary’s critics as well to use their identity to stigmatize and thus stop undesirable coverage from The New York Times. In 2018, she outed a CAP employee at a staff-wide meeting who had filed an anonymous complaint of sexual harassment and retaliation against one of Tanden’s male allies. Secure with her UAE-and-corporate-funded large salary, she has long urged cuts to Social Security. The list goes on and on.

One can reasonably view Biden’s choice of Tanden as a positive. She is no different in character or ideology than any of the faceless, more obscure DNC operatives who would occupy this position if she did not. But because of how well-known her sociopathy, militarism and corporatism are to many on the liberal-left, her face serves as an undeniable and unavoidable reminder of what the Biden administration and the Democratic Party really are. She illuminates the truth about their real aims.

But beyond things like wanting to steal Libya’s oil after bombing it into oblivion, outing sexual harassment complainants, and physically assaulting and censoring her own employees, there is one uniquely abominable feature of Neera Tanden. She is one of the most deranged conspiracy theorists in the United States, and has done more than almost any other Washington functionary to contaminate Democrats’ mental health, capacity to reason, and faith in the legitimacy of U.S. elections.

Tanden owes her entire career to the patronage of Hillary Clinton, and her devotion to Hillary approaches restraining-order levels of creepiness (here you can watch Tanden beam with adoration as then-Senator Hillary Clinton, on the Senate floor in 2004, explains her steadfast opposition to marriage equality for same-sex couples on the ground that “marriage is a sacred bond between a man and a woman” and “exists between a man and a woman going back into the mists of history” for the primary purpose of raising children — just a few short years before Democrats changed views on this, after which it instantly became the hallmark of an unreconstructed hateful bigot to say this).

Few people took Hillary’s 2016 loss to Donald Trump as hard as Tanden, or handled it as poorly. Indeed, she refused to believe it really happened, and encouraged others to similarly refuse to accept its reality.

In the weeks after Trump’s victory, Tanden joined numerous Democrats in encouraging electors of the Electoral College to ignore their states’ votes and refuse to elect Trump as President (many rationale were invoked for this: Tanden’s was a CAP article promoting #Resistance fanatic Richard Painter’s argument that Trump’s violations of the Emolument Clause precluded an Electoral College win). She insisted that Hillary lost because of Russia, claiming the “Russians did enough damage to affect more than 70k votes in 3 states.” And she was not only one of the first to push the Steele Dossier’s claim that Russia held blackmail power over Trump but also one of the last to do so — insisting in 2018 that “the dossier been mostly proven to be true” and claiming as late as 2019 that nothing in this discredited junk report had been disproven.

But what really distinguished Tanden when it came to unhinged and toxic behavior was her repeated (and obviously baseless) claims that Hillary only lost because Russian hackers invaded the U.S. voting system and clandestinely changed Hillary’s votes to Trump’s, costing the real winner — Hillary — her rightful place on the throne, behind the Resolute Desk.

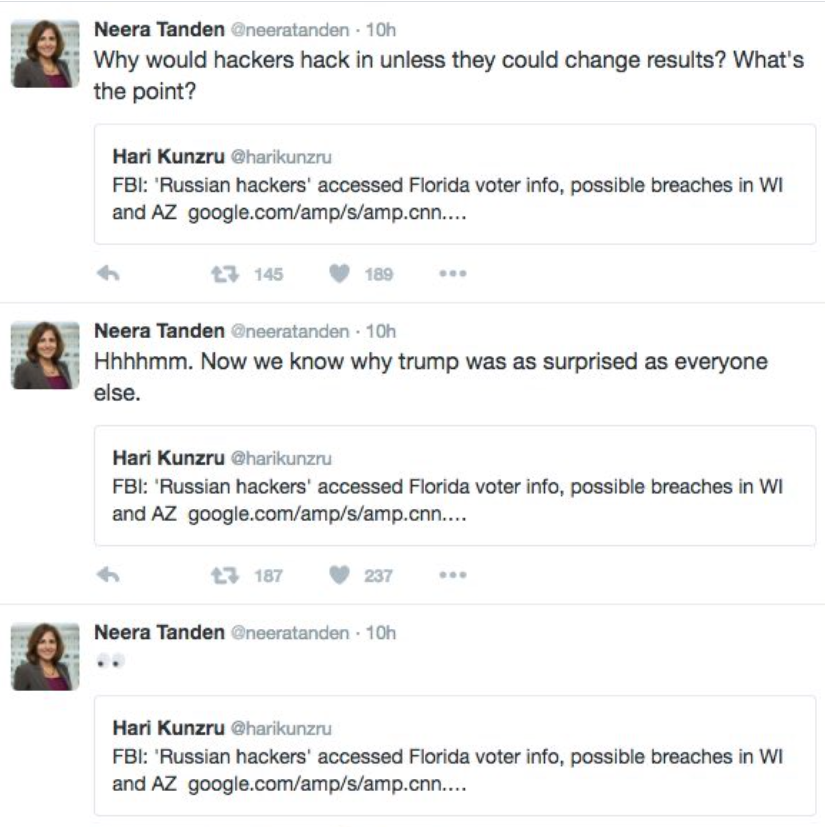

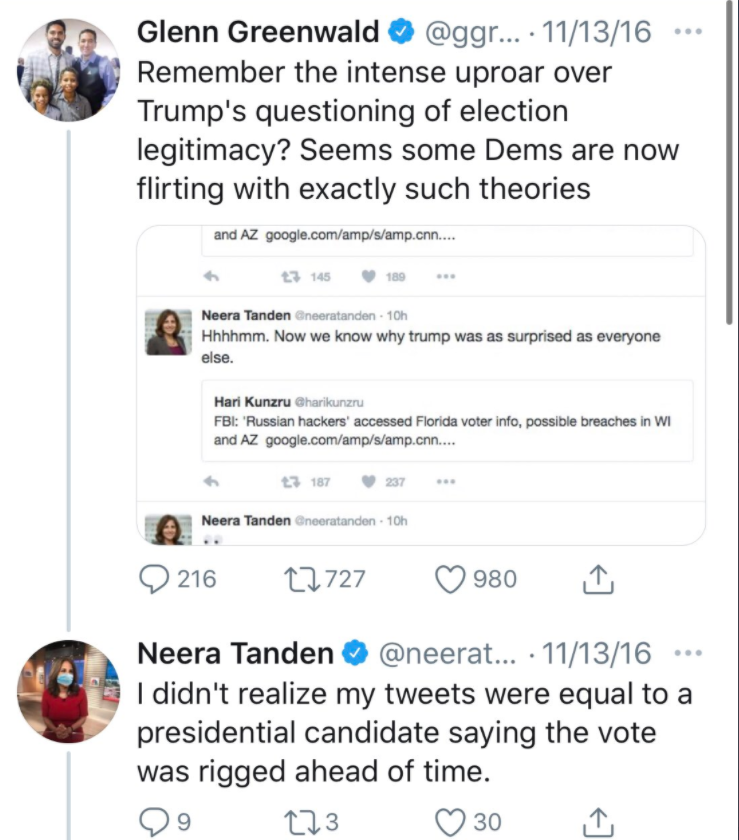

Four days after the 2016 election, Tanden began strongly implying, if not outright stating, that Russian hackers changed the vote totals, and that this is why “Trump was as surprised as everyone else” by his victory. When I highlighted her conspiratorial claims, she did not deny their obvious meaning, but rationalized them by insisting that her conspiracies were not as bad as Trump’s refusal, in advance of the election, to acknowledge the legitimacy of an election that had not yet taken place:

Tanden’s insistence that Russia changed the voting results through hacking did not once her traumatic shock in the weeks after Hillary’s loss dissipated (if it ever did). After The Intercept published an anonymous, evidence-free document in June, 2017, allegedly sent by NSA employee Reality Winner, which led that site to claim that “Russian military intelligence executed a cyberattack on at least one U.S. voting software supplier and sent spear-phishing emails to more than 100 local election officials,” Tanden returned to pushing this bizarre conspiracy theory, demanding that I “retract” my post-election criticism of her for peddling this Russia-changed-the-votes madness — as if this NSA document published by The Intercept proved vote-changing hacking by Russia.

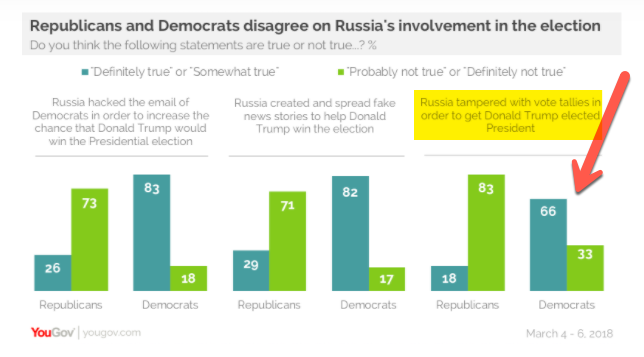

This conspiracy-mongering led by Tanden and other prominent liberal activists had a corrosive effect on the ability of Democrats to perceive basic reality, to put that mildly. A 2018 poll from Economist/YouGov — conducted more than a year after Trump’s inauguration — found that a large majority of Democrats (66%) believe that “Russia tampered with vote tallies in order to get Donald Trump elected President.”

Thereafter, Hillary herself took to calling Trump an “illegitimate” president, further fueling the destruction of confidence and faith among Democrats in the legitimacy of the vote totals and specifically the outcome of the 2016 presidential election.

Democratic leaders and their media allies love to patronizingly warn that conservative media outlets and their audiences are prone to spread and believe crazy conspiracy theories. They purport particular worry when such conspiracies are designed to undermine faith and trust in the U.S. electoral system itself.

Yet few have done more to destroy such confidence and faith than Neera Tanden, achieved by disseminating over the course of several years some of the most unhinged, evidence-free and deranged conspiracy theories in which she deliberately deceived Democratic partisans into believing that Moscow’s dastardly hackers invaded the sanctity of the U.S. voting system to change Hillary’s votes to Trump’s. And it worked: at least as of 2018, large majorities of Democrats believe that this utterly unproven but dangerous assertion is true.

If Joe Biden succeeds in empowering someone like Neera Tanden without extreme opposition from supposedly adversarial journalists, not only Democrats but also these media outlets will lose whatever lingering credibility they have to denounce conspiracy theories and to defend the legitimacy of U.S. elections. And they will deserve that fate. You can’t run around expecting people will take you seriously when you warn of the dangers of toxic, moronic conspiracy theories when you yourself embrace, elevate and promote the most prolific and reckless purveyors of them.

* * *

NOTE TO READERS: We are in the process attempting to expand the content we provide on this Substack platform, including featuring more writers and voices for podcasts, videos, articles and other content in conjunction with my own. I am grateful to those who have subscribed thus far and made our launch a success: further subscriptions will enable us to expand further and do ever more with our journalism here: SUBSCRIBE NOW

via ZeroHedge News https://ift.tt/39rRYva Tyler Durden

{kind=link}