Nikola signed a non-binding Memorandum of Understanding with General Motors for a global supply agreement related to the integration of GM’s Hydrotec fuel-cell system into Nikola’s commercial semi-trucks.

Notably, the MOU does not include the previously contemplated GM equity stake in Nikola or development of the Nikola Badger.

Full Nikola Press Release:

Nikola Corporation (NASDAQ: NKLA) today announced the signing of a non-binding Memorandum of Understanding (“MOU”) with General Motors for a global supply agreement related to the integration of GM’s Hydrotec fuel-cell system into Nikola’s commercial semi-trucks. This supersedes and replaces the transaction announced on September 8, 2020.

Under the terms of the MOU, Nikola and GM will work together to integrate GM’s Hydrotec fuel-cell technology into Nikola’s Class 7 and Class 8 zero-emission semi-trucks for the medium- and long-haul trucking sectors. As previously announced, Nikola expects to begin testing production-engineered prototypes of its hydrogen fuel-cell powered trucks by the end of 2021, with testing for the beta prototypes expected to begin in the first half of 2022. In addition, Nikola and GM will discuss the potential for the utilization of GM’s versatile Ultium battery system in Nikola’s Class 7 and Class 8 vehicles.

“We are excited to take this important step with GM, which provides an opportunity to leverage the resources, strengths and talent of both companies,” said Mark Russell, Chief Executive Officer of Nikola. “Heavy trucks remain our core business and we are 100% focused on hitting our development milestones to bring clean hydrogen and battery-electric commercial trucks to market. We believe fuel-cells will become increasingly important to the semi-truck market, as they are more efficient than gas or diesel and are lightweight compared to batteries for long hauls. By working with GM, we are reinforcing our companies’ shared commitment to a zero-emission future.”

The agreement between Nikola and GM is subject to negotiation and execution of definitive documentation acceptable to both parties. The MOU does not include the previously contemplated GM equity stake in Nikola or development of the Nikola Badger. As previously announced, the Nikola Badger program was dependent on an OEM partnership. Nikola will refund all previously submitted order deposits for the Nikola Badger.

The stock’s immediate reaction was impressive (up over 40%) but has quickly faded to just around 9%…

Finally, we note that today is lock-up expiration (Milton can sell 92 million shares) – interesting timing for a short-squeeze-enabling press release – given the huge short interest…

There’s no such thing as coincidence.

via ZeroHedge News https://ift.tt/2KOR3dX Tyler Durden

Trump Expands China Crackdown, Adds China’s Top Chipmaker And Oil Producer To Defense Blacklist Tyler Durden

Mon, 11/30/2020 – 08:10

In hopes of making a renormalization in relations with Beijing next to impossible for Joe Biden, the Trump administration is poised to add China’s top chipmaker SMIC and national offshore oil and gas producer CNOOC to a blacklist of alleged Chinese military companies, Reuters reported citing a document and sources, curbing their access to U.S. investors and escalating tensions with Beijing.

The latest crackdown comes after a report from Reuters earlier this month that the Department of Defense (DOD) was planning to designate four more Chinese companies as owned or controlled by the Chinese military, bringing the number of Chinese companies affected to 35. A recent executive order issued by President Donald Trump would prevent U.S. investors from buying securities of the listed firms starting late next year.

It was not immediately clear when the new tranche, would be published in the Federal Register. But the list comprises China Construction Technology Co Ltd and China International Engineering Consulting Corp, in addition to Semiconductor Manufacturing International Corp (SMIC) and China National Offshore Oil Corp (CNOOC), Reuters reported.

SMIC said it continued “to engage constructively and openly with the U.S. government” and that its products and services were solely for civilian and commercial use. “The Company has no relationship with the Chinese military and does not manufacture for any military end-users or end-uses.” Shares in SMIC closed 2.7% lower on Monday.

CNOOC’s listed unit CNOOC Ltd, whose shares fell by almost 14% after the Reuters report, said in a stock market statement that it had inquired with its parent and learnt that it had not received any formal notice from relevant U.S. authorities.

Later on Monday, Bernstein Research downgraded CNOOC Ltd’s stock to ‘market perform’ by applying a 30% discount to share price targets, citing sanction risks that range from a ban on U.S. funds owning CNOOC stock to prohibiting US companies from doing business with CNOOC.

China’s foreign ministry spokeswoman Hua Chunying said, in response to a question about Washington’s planned move, that China hoped the United States would not erect barriers and obstacles to cooperation and discriminate against Chinese companies.

The upcoming move is seen as seeking to cement Donald Trump’s tough-on-China legacy and to box incoming Democrat Biden into hardline positions on Beijing amid bipartisan anti-China sentiment in Congress. The list is also part of a broader effort by Washington to target what it sees as Beijing’s efforts to enlist corporations to harness emerging civilian technologies for military purposes.

Reuters reported last week that the Trump administration is close to declaring that 89 Chinese aerospace and other companies have military ties, restricting them from buying a range of U.S. goods and technology.

The list of “Communist Chinese Military Companies” was mandated by a 1999 law requiring the Pentagon to compile a catalog of companies “owned or controlled” by the People’s Liberation Army, but DOD only complied in 2020. Giants like Hikvision, China Telecom and China Mobile were added earlier this year.

via ZeroHedge News https://ift.tt/3o1aPkS Tyler Durden

I was flattered but also surprised when Eugene Volokh kindly invited me to contribute a week of guest posts, since my new book, The Fabric of Civilization: How Textiles Made the World, is not about the law. It examines the central role textiles have played in the history of innovation, from pre-history to the near future. Fortunately, Eugene and his fellow conspirators are as guided by intellectual curiosity as by legal reasoning, and mixing it up, he assured me, would make the blog “fun and eclectic.”

In this post, drawn from the book’s introduction, I start with an insight from the influential computer scientist Mark Weiser, writing in 1991. “The most profound technologies are those that disappear,” he wrote. “They weave themselves into the fabric of everyday life until they are indistinguishable from it.”

Do you see what he did there?

We hairless apes co-evolved with our cloth. From the moment we’re wrapped in a blanket at birth, we are surrounded by textiles. They cover our bodies, bedeck our beds, and carpet our floors. Textiles give us seatbelts and sofa cushions, tents and bath towels, bandages and duct tape. They are everywhere.

But, to reverse Arthur C. Clarke’s famous adage about magic, any sufficiently familiar technology is indistinguishable from nature. It seems intuitive, obvious—so woven into the fabric of our lives that we take it for granted. We no more imagine a world without cloth than one without sunlight or rain.

We drag out heirloom metaphors—”on tenterhooks,” “tow-headed,” “frazzled“—with no idea that we’re talking about fabric and fibers. We repeat threadbare clichés: “whole cloth,” “hanging by a thread,” “dyed in the wool.” We catch airline shuttles, weave through traffic, follow comment threads. We speak of lifespans and spinoffs and never wonder why drawing out fibers and twirling them into thread looms so large in our language. Surrounded by textiles, we’re largely oblivious to their existence, and to the knowledge and efforts embodied in every scrap of fabric.

Cloth-making is a creative act, analogous to other creative acts. It is a sign of mastery and refinement. “Can we expect, that a government will be well modelled by a people, who know not how to make a spinning-wheel, or to employ a loom to advantage?” wrote philosopher David Hume in 1742. The knowledge is all but universal. Rare is the people that does not spin or weave and rare, too, the society that does not engage in textile-related trade.

The global story of textiles illuminates the nature of civilization itself. I use this term not to imply moral superiority or the end state of an inevitable progression but in the more neutral sense suggested by Mordecai Kaplan’s definition: “the accumulation of knowledge, skills, tools, arts, literatures, laws, religions and philosophies which stands between man and external nature, and which serves as a bulwark against the hostility of forces that would otherwise destroy him.” This description captures two critical dimensions that together distinguish civilization from related concepts, such as culture.

First, civilization is cumulative. It exists in time, with today’s version built on previous ones. A civilization ceases to exist when that continuity is broken. Minoan civilization disappeared. Conversely, a civilization may evolve over a long stretch of time while the cultures that make it up pass away or change irrevocably. The Western Europe of 1980 was radically different in its social mores, religious practices, material culture, political organization, technological resources, and scientific understanding from the Christendom of 1480, yet we recognize both as Western civilization.

The story of textiles demonstrates this cumulative quality. It lets us trace the progress and interactions of practical techniques and scientific theory: the cultivation of plants and breeding of animals, the spread of mechanical innovations and measurement standards, the recording and replication of patterns, the manipulation of chemicals. We can watch knowledge spread from one place to another, sometimes in written form but more often through human contact or the exchange of goods, and see civilizations become intertwined.

Second, civilization is a survival technology. It comprises the many artifacts—designed or evolved, tangible or intangible—that stand between vulnerable human beings and natural threats and that invest the world with meaning. Providing protection and adornment, textiles are themselves among such artifacts. So, too, are the innovations they inspire, from better seeds to weaving patterns to new ways of recording information.

Along with the perils and discomforts of indifferent nature, civilization protects us from the dangers posed by other humans. Ideally, it allows us to live in harmony. Eighteenth-century thinkers used the term to refer to the intellectual and artistic refinement, sociability, and peaceful interactions of the commercial city. But rare is the civilization that exists without organized violence. At best, civilization encourages cooperation, curbing humanity’s violent urges; at worst, it unleashes them to conquer, pillage, and enslave. The history of textiles reveals both aspects.

Every scrap of cloth represents the solution to innumerable difficult problems. Many are technical or scientific: How do you breed sheep with thick, white fleeces? How do you maintain enough tension to spin fibers together without breaking them? How do you prevent dyes from fading? How do you construct a loom that can weave complex patterns?

Some of the trickiest, however, are social: How do you finance a crop of silkworms or cotton, a new spinning mill, or a long-distance caravan? How do you record weaving patterns so someone else can duplicate them? How do you pay for textile shipments without physically sending currency? What do you do when the law forbids the cloth you want to make or use?

In the posts that follow, I’ll concentrate on some of the institutions and practices—”social technologies”—that addressed these types of questions.

from Latest – Reason.com https://ift.tt/2VkFRrs

via IFTTT

In his first TV interview since the presidential election, Donald Trump spoke to Fox News host Maria Bartiromo on Sunday morning, reiterating his unsubstantiated claim that vote counting was “rigged” to ensure Joe Biden’s victory. Although Bartiromo began by inviting the president to “go through the facts” that support his allegations of systematic election fraud, he presented no real evidence, and Bartiromo did not press him to do so.

Instead Bartiriomo seemed to accept the president’s claims at face value. “This is disgusting!” she said. “And we cannot allow America’s election to be corrupted.”

Any mildly skeptical person would have seen several opportunities for follow-up questions. “This election was a fraud,” Trump said. “It was a rigged election.” How so? “We had glitches where they moved thousands of votes from my account to Biden’s account,” he asserted. “They’re not glitches. They’re theft. They’re fraud—absolute fraud.”

Trump was repeating a story about fraud-facilitating voting machines that has been repeatedly debunked. “To our collective knowledge,” a group of 59 computer scientists and election security experts said in an open letter published earlier this month, “no credible evidence has been put forth that supports a conclusion that the 2020 election outcome in any state has been altered through technical compromise.” Trump’s own Department of Homeland Security called the 2020 election “the most secure in American history,” saying, “There is no evidence that any voting system deleted or lost votes, changed votes, or was in any way compromised.”

In addition to claiming that voting machines were rigged, Trump said large numbers of fraudulent ballots mysteriously arrived at counting locations to save the day for Biden. “This election was over, and then they did dumps…big, massive dumps in Michigan, Pennsylvania, and all over,” he said. “If you take a look at just about every state that we’re talking about, every swing state that we’re talking about…they did these massive dumps of votes. And all of a sudden, I went from winning by a lot to losing by a little….They started just doing ballot after ballot very quickly and just checking the Biden name on top. ” This is another claim that the Trump campaign has failed to substantiate in court. “They backdated all these ballots that came in,” Trump said, referring to yet another accusation that did not pan out.

Trump also asserted that “there are a lot of dead people that so-called voted in this election.” Such cases, which typically involve people who mail absentee ballots on behalf of recently deceased spouses, are “exceedingly rare,” FactCheck.org found. More often, purported examples of dead voters turn out to be mistakes—confusing a father and son with similar names, for instance. Sometimes people who cast votes by mail die before Election Day. “Every once in a while, it turns out that someone votes in the name of someone who’s passed away,” Justin Levitt, a voting fraud expert at Loyola Law School, told FactCheck.org. “A handful of votes in a sea of millions. It’s not OK, but it doesn’t swing results.”

Trump expressed disappointment that the Department of Justice and the FBI had not taken his allegations more seriously, saying “maybe they’re involved.” If so, they would join a long list of alleged conspirators, including Democratic and Republican election officials, the Biden campaign, Dominion Voting Systems, George Soros, the Clinton Foundation, and the Venezuelan, Cuban, and Chinese governments, not to mention the Republican members of Congress, Trump-friendly news outlets, and Republican-nominated judges who have been skeptical of the president’s claims about election fraud.

Again and again, post-election lawsuits filed by the Trump campaign have failed to specifically allege the sort of massive fraud that could have changed the outcome. Trump complained that some of those lawsuits have been dismissed for lack of standing, meaning the campaign failed to show that it had suffered an “injury in fact” caused by the defendants that would be addressed by the remedy it sought. “They say you don’t have standing,” Trump told Bartiromo. “You mean as president of the United States, I don’t have standing. What kind of a court system is this?”

As U.S. District Judge Matthew Brann explained when he rejected the Trump campaign’s attempt to block certification of Pennsylvania’s election results, it’s the kind of court system that is empowered to act only when it is presented with “cases” or “controversies.” To satisfy that requirement, Brann noted, “a plaintiff must establish that they have standing,” which is “an ‘irreducible constitutional minimum,’ without which a federal court lacks jurisdiction to rule on the merits of an action.”

The Trump campaign, joined by two voters, challenged Pennsylvania’s policy regarding technical errors in absentee ballots. Some counties, following advice from Secretary of the Commonwealth Kathy Boockvar, gave voters a chance to “cure” those errors, while other counties did not. The campaign and the voters argued that the uneven application of that policy violated the 14th Amendment’s guarantee of equal protection.

Brann found that the two voters, whose ballots were rejected by counties that did not give them a chance to fix their mistakes, could not show that the injury they asserted—invalidation of their votes—was caused by the parties they sued: Boockvar and seven counties that allowed curing. Furthermore, the remedy they sought—preventing certification of millions of other people’s votes—would not have corrected the injury.

As for the Trump campaign, Brann said, the issue of standing “is particularly nebulous because neither in the [first amended complaint] nor in its briefing does the Trump Campaign clearly assert what its alleged injury is. Instead, the Court was required to embark on an extensive project of examining almost every case cited to by Plaintiffs to piece together the theory of standing as to this Plaintiff.”

Brann considered two possibilities: “associational standing” and “competitive standing.” He concluded that neither applied in this case.

Associational standing requires that an organization’s members “would otherwise have standing to sue in their own right.” Since the voters who joined the lawsuit did not have standing to sue Boockvar and the seven counties, Brann said, the campaign could not meet that prong of the test.

Competitive standing, according to case law from the 9th Circuit on which the Trump campaign relied, “is the notion that ‘a candidate or his political party has

standing to challenge the inclusion of an allegedly ineligible rival on the ballot, on

the theory that doing so hurts the candidate’s or party’s own chances of prevailing

in the election.'” That description did not apply to this case either.

Although Brann concluded that the plaintiffs did not have standing to sue, he considered their equal protection claims while deciding whether to dismiss the lawsuit. “Even if Plaintiffs had standing, they fail to state an equal-protection claim,” he said. “The general gist of their claims is that Secretary Boockvar, by failing to prohibit counties from implementing a notice-and-cure policy, and Defendant Counties, by adopting such a policy, have created a ‘standardless’ system and thus unconstitutionally discriminated against Individual Plaintiffs. Though Plaintiffs do not articulate why, they also assert that this has unconstitutionally discriminated against the Trump Campaign.”

The two voters’ equal protection claims ran into the same problem as their argument for standing: The defendants were not responsible for rejecting their ballots. “Because Defendants’ conduct ‘imposes no burden’ on Individual Plaintiffs’ right to vote, their equal-protection claim is subject to rational basis review,” Brann said. “Defendant Counties, by implementing a notice-and-cure procedure, have in fact lifted a burden on the right to vote, even if only for those who live in those counties. Expanding the right to vote for some residents of a state does not burden the rights of others.”

Brann concluded that Pennsylvania’s notice-and-cure policy easily satisfied the highly deferential rational basis test, because “it is perfectly rational for a state to provide counties discretion to notify voters that they may cure procedurally defective mail-in ballots.” Although “states may not discriminatorily sanction procedures that are likely to burden some persons’ right to vote more than others,” he said, “they need not expand the right to vote in perfect uniformity.”

Regarding the Trump campaign, Brann wrote, “they do not allege that Secretary Boockvar’s guidance differed from county to county, or that Secretary Boockvar told some counties to cure ballots and others not to. That some counties may have chosen to implement the guidance (or not), or to implement it differently, does not constitute an equal-protection violation.”

The campaign also complained that election officials in some counties kept poll watchers unreasonably far from the vote counting. But here, too, it failed to allege that the practice discriminated against Republicans. “Plaintiffs fail to plausibly plead that there was ‘uneven treatment’ of Trump and Biden watchers and representatives,” Brann said.

Contrary to Trump’s implication in the Fox News interview, then, Brann did consider the plausibility of the campaign’s equal protection claims, and he found them wanting. So did the U.S. Court of Appeals for the 3rd Circuit in a ruling it issued on Friday. “The Campaign cannot win this lawsuit,” the unanimous three-judge panel said in a scathing opinion written by a Trump appointee. “The Campaign’s claims have no merit.”

from Latest – Reason.com https://ift.tt/2HQP8o6

via IFTTT

In his first TV interview since the presidential election, Donald Trump spoke to Fox News host Maria Bartiromo on Sunday morning, reiterating his unsubstantiated claim that vote counting was “rigged” to ensure Joe Biden’s victory. Although Bartiromo began by inviting the president to “go through the facts” that support his allegations of systematic election fraud, he presented no real evidence, and Bartiromo did not press him to do so.

Instead Bartiriomo seemed to accept the president’s claims at face value. “This is disgusting!” she said. “And we cannot allow America’s election to be corrupted.”

Any mildly skeptical person would have seen several opportunities for follow-up questions. “This election was a fraud,” Trump said. “It was a rigged election.” How so? “We had glitches where they moved thousands of votes from my account to Biden’s account,” he asserted. “They’re not glitches. They’re theft. They’re fraud—absolute fraud.”

Trump was repeating a story about fraud-facilitating voting machines that has been repeatedly debunked. “To our collective knowledge,” a group of 59 computer scientists and election security experts said in an open letter published earlier this month, “no credible evidence has been put forth that supports a conclusion that the 2020 election outcome in any state has been altered through technical compromise.” Trump’s own Department of Homeland Security called the 2020 election “the most secure in American history,” saying, “There is no evidence that any voting system deleted or lost votes, changed votes, or was in any way compromised.”

In addition to claiming that voting machines were rigged, Trump said large numbers of fraudulent ballots mysteriously arrived at counting locations to save the day for Biden. “This election was over, and then they did dumps…big, massive dumps in Michigan, Pennsylvania, and all over,” he said. “If you take a look at just about every state that we’re talking about, every swing state that we’re talking about…they did these massive dumps of votes. And all of a sudden, I went from winning by a lot to losing by a little….They started just doing ballot after ballot very quickly and just checking the Biden name on top. ” This is another claim that the Trump campaign has failed to substantiate in court. “They backdated all these ballots that came in,” Trump said, referring to yet another accusation that did not pan out.

Trump also asserted that “there are a lot of dead people that so-called voted in this election.” Such cases, which typically involve people who mail absentee ballots on behalf of recently deceased spouses, are “exceedingly rare,” FactCheck.org found. More often, purported examples of dead voters turn out to be mistakes—confusing a father and son with similar names, for instance. Sometimes people who cast votes by mail die before Election Day. “Every once in a while, it turns out that someone votes in the name of someone who’s passed away,” Justin Levitt, a voting fraud expert at Loyola Law School, told FactCheck.org. “A handful of votes in a sea of millions. It’s not OK, but it doesn’t swing results.”

Trump expressed disappointment that the Department of Justice and the FBI had not taken his allegations more seriously, saying “maybe they’re involved.” If so, they would join a long list of alleged conspirators, including Democratic and Republican election officials, the Biden campaign, Dominion Voting Systems, George Soros, the Clinton Foundation, and the Venezuelan, Cuban, and Chinese governments, not to mention the Republican members of Congress, Trump-friendly news outlets, and Republican-nominated judges who have been skeptical of the president’s claims about election fraud.

Again and again, post-election lawsuits filed by the Trump campaign have failed to specifically allege the sort of massive fraud that could have changed the outcome. Trump complained that some of those lawsuits have been dismissed for lack of standing, meaning the campaign failed to show that it had suffered an “injury in fact” caused by the defendants that would be addressed by the remedy it sought. “They say you don’t have standing,” Trump told Bartiromo. “You mean as president of the United States, I don’t have standing. What kind of a court system is this?”

As U.S. District Judge Matthew Brann explained when he rejected the Trump campaign’s attempt to block certification of Pennsylvania’s election results, it’s the kind of court system that is empowered to act only when it is presented with “cases” or “controversies.” To satisfy that requirement, Brann noted, “a plaintiff must establish that they have standing,” which is “an ‘irreducible constitutional minimum,’ without which a federal court lacks jurisdiction to rule on the merits of an action.”

The Trump campaign, joined by two voters, challenged Pennsylvania’s policy regarding technical errors in absentee ballots. Some counties, following advice from Secretary of the Commonwealth Kathy Boockvar, gave voters a chance to “cure” those errors, while other counties did not. The campaign and the voters argued that the uneven application of that policy violated the 14th Amendment’s guarantee of equal protection.

Brann found that the two voters, whose ballots were rejected by counties that did not give them a chance to fix their mistakes, could not show that the injury they asserted—invalidation of their votes—was caused by the parties they sued: Boockvar and seven counties that allowed curing. Furthermore, the remedy they sought—preventing certification of millions of other people’s votes—would not have corrected the injury.

As for the Trump campaign, Brann said, the issue of standing “is particularly nebulous because neither in the [first amended complaint] nor in its briefing does the Trump Campaign clearly assert what its alleged injury is. Instead, the Court was required to embark on an extensive project of examining almost every case cited to by Plaintiffs to piece together the theory of standing as to this Plaintiff.”

Brann considered two possibilities: “associational standing” and “competitive standing.” He concluded that neither applied in this case.

Associational standing requires that an organization’s members “would otherwise have standing to sue in their own right.” Since the voters who joined the lawsuit did not have standing to sue Boockvar and the seven counties, Brann said, the campaign could not meet that prong of the test.

Competitive standing, according to case law from the 9th Circuit on which the Trump campaign relied, “is the notion that ‘a candidate or his political party has

standing to challenge the inclusion of an allegedly ineligible rival on the ballot, on

the theory that doing so hurts the candidate’s or party’s own chances of prevailing

in the election.'” That description did not apply to this case either.

Although Brann concluded that the plaintiffs did not have standing to sue, he considered their equal protection claims while deciding whether to dismiss the lawsuit. “Even if Plaintiffs had standing, they fail to state an equal-protection claim,” he said. “The general gist of their claims is that Secretary Boockvar, by failing to prohibit counties from implementing a notice-and-cure policy, and Defendant Counties, by adopting such a policy, have created a ‘standardless’ system and thus unconstitutionally discriminated against Individual Plaintiffs. Though Plaintiffs do not articulate why, they also assert that this has unconstitutionally discriminated against the Trump Campaign.”

The two voters’ equal protection claims ran into the same problem as their argument for standing: The defendants were not responsible for rejecting their ballots. “Because Defendants’ conduct ‘imposes no burden’ on Individual Plaintiffs’ right to vote, their equal-protection claim is subject to rational basis review,” Brann said. “Defendant Counties, by implementing a notice-and-cure procedure, have in fact lifted a burden on the right to vote, even if only for those who live in those counties. Expanding the right to vote for some residents of a state does not burden the rights of others.”

Brann concluded that Pennsylvania’s notice-and-cure policy easily satisfied the highly deferential rational basis test, because “it is perfectly rational for a state to provide counties discretion to notify voters that they may cure procedurally defective mail-in ballots.” Although “states may not discriminatorily sanction procedures that are likely to burden some persons’ right to vote more than others,” he said, “they need not expand the right to vote in perfect uniformity.”

Regarding the Trump campaign, Brann wrote, “they do not allege that Secretary Boockvar’s guidance differed from county to county, or that Secretary Boockvar told some counties to cure ballots and others not to. That some counties may have chosen to implement the guidance (or not), or to implement it differently, does not constitute an equal-protection violation.”

The campaign also complained that election officials in some counties kept poll watchers unreasonably far from the vote counting. But here, too, it failed to allege that the practice discriminated against Republicans. “Plaintiffs fail to plausibly plead that there was ‘uneven treatment’ of Trump and Biden watchers and representatives,” Brann said.

Contrary to Trump’s implication in the Fox News interview, then, Brann did consider the plausibility of the campaign’s equal protection claims, and he found them wanting. So did the U.S. Court of Appeals for the 3rd Circuit in a ruling it issued on Friday. “The Campaign cannot win this lawsuit,” the unanimous three-judge panel said in a scathing opinion written by a Trump appointee. “The Campaign’s claims have no merit.”

from Latest – Reason.com https://ift.tt/2HQP8o6

via IFTTT

Futures, Global Stocks Dip On Last Day Of Record Month For Markets Tyler Durden

Mon, 11/30/2020 – 07:55

US equity futures and world shares paused on Monday, dropping modestly on the back of weakness in oil and energy stocks even as they were set to finish a record-breaking month sparked by major progress toward a coronavirus vaccine and yet more free money from central banks.

Trading volumes were muted with European stocks holding steady, reversing an earlier loss while U.S. futures dropped as lows as 3,600 before rebounding. The MSCI World Index has soared 13% in November, the best performance on record. IHS Markit Ltd. jumped 16% in U.S. premarket trading. The research firm with more than 5,000 analysts, data scientists agreed to be bought by S&P Global Inc. for about $39 billion in stock.

Early downbeat sentiment was reversed by yet another case of “Medical Monday”, after Moderna became the latest company to apply for emergency COVID vaccine approval in the US and Europe after new analysis showed the vaccine was highly effective in preventing Covid-19, with no serious safety problems. The news came after a weekend, in which U.S. Surgeon General Jerome Adams said the federal government hopes to quickly review and approve requests from two drugmakers for emergency approval of their Covid-19 vaccines. The rapid pace to a vaccine has given investors the confidence to price in a return to normalcy and faster economic growth, helping lift shares of companies that were hardest hit by the pandemic.

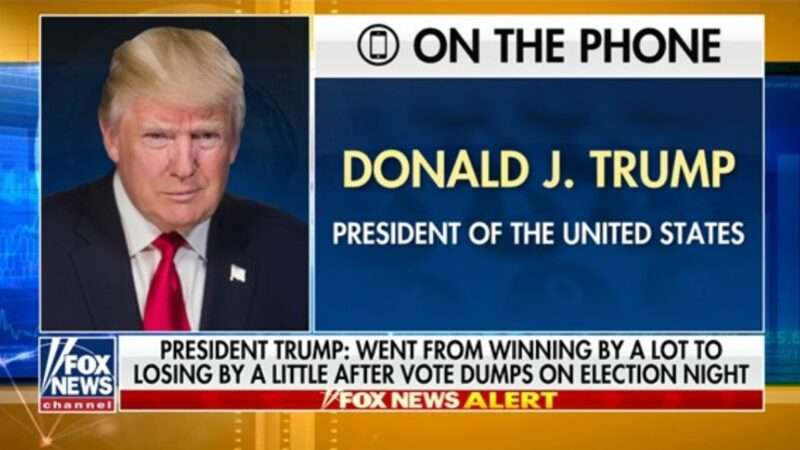

Sentiment also got a boost from the latest Chinese PMI data showed manufacturing and service activity handily beat forecasts in November, even as the country’s central bank surprised with a helping of cheap loans.

On Monday, the rotation in equities showed signs of a slight reversal. Futures on the tech-heavy Nasdaq 100 Index were little changed, while small-caps, banks and energy producers dropped, according to Bloomberg. The MSCI Asia Pacific Index sank 1.6%, the biggest loss in a month. The risk-on mood across markets has hurt demand for haven assets. Gold extended a retreat on Monday and is on course for its largest monthly decline in four years. The dollar is poised for a 2.7% drop in November.

“I suspect that investors have become cautious after big gains in the last few weeks that were driven by the vaccine news,” said Peter Rosenstreich, head of market strategy at Swissquote Bank. “It’s a big positive as it’s really provided an endgame for Covid-19.”

“Markets are overbought and at risk of a short term pause,” said Shane Oliver, head of investment strategy at AMP Capital. “However, we are now in a seasonally strong time of year and investors are yet to fully discount the potential for a very strong recovery next year in growth and profits as stimulus combines with vaccines.” Cyclical recovery shares including resources, industrials and financials were likely to be relative outperformers, he added.

Today’s drop in oil and energy names notwithstanding, November’s rush to value names benefited oil and industrial commodities while undermining safe-haven dollar and gold. “It has been a very, very strong month for markets, especially on the equity side but also on the fixed income side too,” said Rabobank’s Head of Macro Strategy Elwin de Groot. “And this market still remains very much supported by liquidity from the central banks,” De Groot added. With the ECB set to provide more stimulus next month “the market view seems to be, what can possibly go wrong?”

The positive developments on vaccines and swiftness with which they are likely to be rolled out had been key drivers.

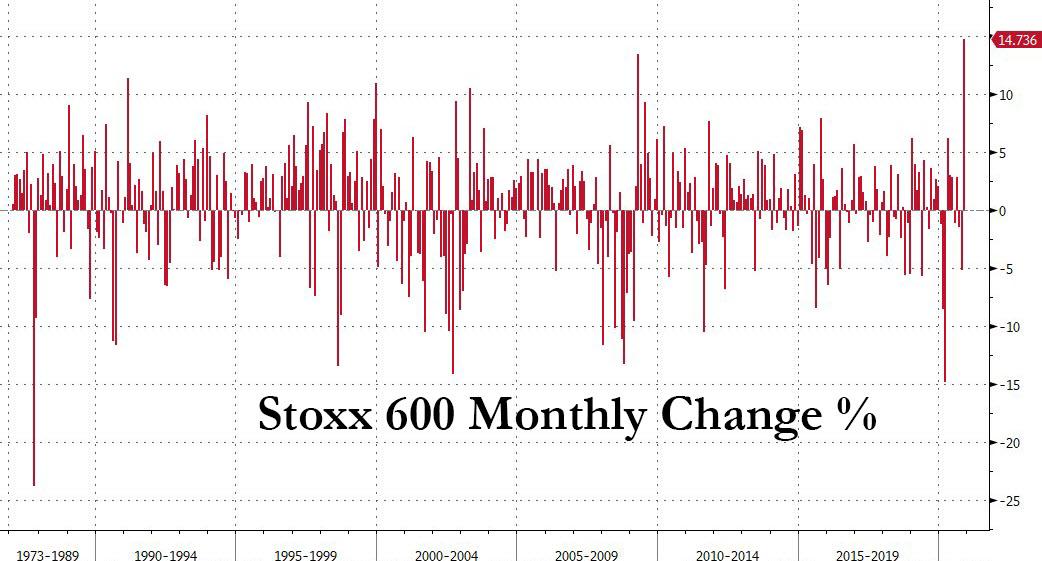

European bourses boasted their best month ever with France up 21% and Italy almost 26%. The MSCI measure of world stocks is up nearly 13% for November, while the S&P 500 has climbed 11% to all-time peaks. The Stoxx is also having its best month on record.

After initially dropping as much as -0.7%, European stocks were unchanged after Moderna said it plans to request clearance for its coronavirus vaccine in the U.S. and Europe. The Eurostoxx 50 reversed an initial 0.6% drop to trade in the green. DAX and FTSE 100 lead peers. Peripheral indexes remain in the red, with Spain’s IBEX underperforming. Retail, chemical and healthcare stocks lead gains with banks, while oil & gas and travel the weakest sectors following Sunday’s failure of OPEC+ to reach a preliminary deal on whether to extend output curbs. ABN Amro Bank NV fell as much as 6.5% in Amsterdam trading. The Dutch lender plans to cut about 2,800 jobs over four years as it retreats from large parts of its investment bank.

Earlier in the session, Asia closed November on a weak note with MSCI’s index of Asia-Pacific shares ex-Japan ending 1.5% lower on the day but was still up almost 10% for the month. The Topix lost 1.8%, with Toyota and Daiichi Sankyo contributing the most to the move. The Shanghai Composite Index retreated 0.5%, driven by China Merchants Bank and Kweichow Moutai. Chinese blue chips ended lower but up nearly 6% for the month. Trading volume for MSCI Asia Pacific Index members was 88% above the monthly average. Japan’s Nikkei 225 eased 0.8%, but was still 15% higher on the month for the largest rise since 1994.

Emerging-market stocks fell on the last day of November, their best month since March 2016, as investors weighed the failure of an OPEC+ ministers panel to reach a supply agreement and renewed coronavirus restrictions from Hong Kong to Europe. MSCI’s gauge tracking developing-nation equities headed for the biggest daily drop this month.

The surge in stocks has put competitive pressure on safe-haven bonds but much of that has been cushioned by expectations of more asset buying by central banks. Sweden’s Riksbank surprised last week by expanding its bond purchase program and the European Central Bank is likely to follow in December.

In rates, European fixed income markets were relatively quiet, ignoring comments from ECB’s Lagard; Bunds bear flatten, semi-core spreads tighten marginally to core. German 10-year Bund yield were down 1.1 basis points at -0.598%, its lowest since Nov. 9. The rest of the core market also fell by around 1 bp.

Treasury futures were near session lows in early U.S. trading as stock futures pare declines, despite expectations that a large month-end index duration extension at the end of the day will support the long end. Yields were higher across the curve led by 10- to 30-year sectors, 10-year by nearly 2bp at 0.857%, slightly lagging bunds and gilts; front-end yields are little changed. As a result, U.S. 10-year yields are ending the month almost exactly where they started at 0.84%, a solid performance given the exuberance in equities.

The U.S. dollar has not been as lucky: “The idea that a potential Treasury Secretary (Janet) Yellen and Fed chair Powell could work more closely to shape and coordinate super easy monetary policy and massive fiscal stimulus that could drive a rapid post pandemic recovery saw the dollar under pressure,” said Robert Rennie, head of financial market strategy at Westpac.

Against a basket of currencies, the dollar index was pinned at 91.771 having shed 2.4% for the month to lows last seen in mid-2018. The Bloomberg dollar index was headed for its biggest monthly decline since July, as G-10 peers tested multi-year highs against the greenback. The euro has caught a tailwind from the relative outperformance of European stocks and climbed 2.7% for the month to reach $1.1967. A break of the September peak at $1.2011 would open the way to a 2018 top at $1.2555.

Elsewhere, the pound rose the most in nearly a week on optimism a Brexit trade deal is close, though signs of caution showed up in the options market. GBP/USD rose as much as %0.4 to 1.3364 in its biggest move since Nov. 24. The U.K. and European Union are close to a breakthrough on fishing with an acceptance of a British proposal for a transition period on fishing rights after Jan. 1, the Telegraph reported. In Switzerland, the USD/CHF fell as much as 0.5% to 0.9019, its lowest since Nov. 9; The Swiss franc was initially supported as the nation’s voters rejected two proposals that had the potential to alter the corporate landscape of a country known for low taxes and light-touch regulation.

In commodities, one major casualty of the rush to risk has been gold, which was near a five-month trough at $1,771 an ounce having shed 5.6% in November, its largest monthly decline in four years.

Oil, in contrast, benefited nearly 30% from the prospect of a demand revival should the vaccines allow travel and transport to resume next year. Some profit-taking set in early on Monday ahead of an OPEC+ meeting to decide whether the producers’ group will extend large output cuts. Brent crude futures fell 52 cents to $47.66, while WTI dropped below $45 a barrel in New York on Monday. An informal meeting of OPEC+ ministers didn’t reach an agreement on whether to delay January’s oil-output increase. A full meeting of the cartel is planned for later today, where a deal is still seen as the most likely outcome.

As Bloomberg notes, looking at Monday’s calendar, OPEC holds a virtual full ministerial meeting to make a final decision on whether a production supply hike should proceed as scheduled in January. Further into the week, the Reserve Bank of Australia holds a policy meeting on Tuesday, while Fed Chairman Jerome Powell testifies before Congress on Tuesday and Wednesday. The U.S. jobs report on Friday is expected to show more Americans headed back to work in November, though at a slower pace than last month.

Market Snapshot

S&P 500 futures down 0.2% to 3,628

STOXX Europe 600 up 0.01% to 393.28

German 10Y yield rose 0.5 bps to -0.583%

Euro up 0.1% to $1.1977

Italian 10Y yield fell 0.7 bps to 0.483%

Spanish 10Y yield rose 0.6 bps to 0.064%

MXAP down 1.6% to 189.96

MXAPJ down 1.5% to 625.40

Nikkei down 0.8% to 26,433.62

Topix down 1.8% to 1,754.92

Hang Seng Index down 2.1% to 26,341.49

Shanghai Composite down 0.5% to 3,391.76

Sensex down 0.3% to 44,149.72

Australia S&P/ASX 200 down 1.3% to 6,517.81

Kospi down 1.6% to 2,591.34

Brent futures down 1.8% to $47.30/bbl

Gold spot down 0.6% to $1,777.30

U.S. Dollar Index down 0.2% to 91.64

Top Overnight News from Bloomberg

Boris Johnson’s officials believe a Brexit trade deal could be reached within days if both sides continue working in “good faith” to resolve what the U.K. sees as the last big obstacle in the talks — fishing rights

Boris Johnson is battling to convince his own Conservative Party colleagues to back plans to keep most of England under strict pandemic controls when the national lockdown ends this week

Germany can’t continue compensating businesses for lost sales beyond next month and more targeted measures will be needed instead, according to senior officials in Chancellor Angela Merkel’s government

China’s economic rebound is gathering pace toward the end of the year, with an official gauge of manufacturing rising faster than expected in November, fueled by exports

China unexpectedly added medium-term funding to the financial system on Monday, as the central bank sought to ease liquidity tightness in the final weeks of the year

The Bank of England is seeing old fault lines open up as officials lock horns on whether to take interest rates below zero for the first time. That’s what the math on the nine-member Monetary Policy Committee is starting to look like, as the so-called “internals” on the panel with full-time operational roles at the central bank show the greatest signs of resistance to the measure. The minority of part-time “external” officials tend to be more open to subzero policy

Quick look at global markets courtesy of NewsSquawk

Asian equity markets began the week mixed amid tentativeness heading into month-end and this week’s key risk events, with the region also digesting a slew of data including better than expected Chinese Manufacturing and Non-Manufacturing PMI data. ASX 200 (-1.3%) underperformed as gold miners led the broad retreat seen across sectors after the recent slump in the precious metal and with Treasury Wine Estates hampered again by China’s anti-dumping measures on Australian wine, while Nikkei 225 (-0.8%) was initially kept afloat after Industrial Production data topped estimates but later succumbed to the headwinds from a firmer currency. Hang Seng (-2.1%) and Shanghai Comp. (-0.5%) initially diverged with the mainland bourse outperforming after Chinese official Manufacturing PMI printed its highest reading in more than 3 years and amid PBoC efforts in which it injected funds through Reverse Repo operations and the Medium-term Lending Facility. Conversely, the mood in Hong Kong was subdued with CNOOC and other blue-chip oil peers pressured after reports US President Trump is to add CNOOC and chipmaker SMIC to the defense blacklist, while Alibaba was also among the laggards amid suggestions the Ant Financial IPO faces narrow chances of going through next year. Finally, 10yr JGBs were lacklustre and attempted a breakdown of the psychological 152.00 level with price action failing to take impetus from the bull-flattening last Friday in USTs and the BoJ presence in the market today, while the central bank also recently announced its bond purchase intentions for December whereby it maintained the value amounts but reduced the frequency of buying in 1-3yr and 3-5yr maturities to 5 times from 6 times a month.

Top Asian News

Suning.com Is Said to Mull E-Commerce Business Stake Sale

China Unexpectedly Injects $30 Billion Into Financial System

Meituan’s Sales Surge Alongside China’s Appetite for Takeout

H.K. Doctor Is Cleared in Massive Securities Fraud Probe

Major European bourses see a mixed performance (Euro Stoxx 50 Unch) after the region trimmed the modest losses seen at the cash open despite a lack of fresh fundamental catalysts, and with some suggesting month-end rotation for the earlier losses ahead of a number of key risk events for the week – including Brexit, OPEC and the US Labour Market reports. State-side futures also sees tepid trade in early European hours ahead of the US entrance from the long Thanksgiving weekend. Back to Europe, sectors kicked the week of with a defensive bias as Healthcare, Utilities and Staples initially performed better than the cyclicals, albeit thereafter, sectors re-calibrated to show more of a mixed picture, with no clear risk tone to be derived as things stand. Energy remains the straddler amid price action in the complex ahead of the OPEC confab, whilst Banks also retain their spot near the bottom amidst a lower yield environment, and as Brexit continues hang over UK financials heading into the crunch week. Further for the banking sector, HSBC (-2%) trades lower following reports the group is looking to exit retail banking in the US as part of a cost reduction plan, whilst ABN AMRO (-6.2%) sees more pronounced losses following its investor update whereby it sees some 15% workforce reduction by 2024. Elsewhere, on the M&A front – AA (-0.5%) trades modestly lower as its largest shareholder is set to oppose the takeover from Warburg Pincus and TowerBrook Capital Partners, with his stake just under the 25% needed to block the deal. Meanwhile, JD Sports (+6.3%) tops the FTSE 100 amid source reports that the group is less likely to make an offer for the Debenhams as its chairman is reportedly concerned that COVID restrictions have had a larger impact. Meanwhile, Siltronic (+9.1%) holds onto gains amid reports the Co. is said to be in talks to be bought by Taiwan’s GlobalWafers for EUR 3.75bln. Finally, state-side S&P Global Inc confirmed it is in advanced talks to acquire IHS Markit for a deal worth around USD 44bln.

Top European News

Swiss Reject Business Liability Plan, Ban on SNB Investments

Lloyds Names HSBC’s Nunn as CEO to Replace Horta- Osorio

ABN Amro to Cut About 2,800 Jobs as Investment Bank Shrinks

Poland Upset With EU But Not Enough to Follow U.K. Exit Path

In FX, the Dollar remains downbeat irrespective of any safe haven demand that might ordinarily be warranted as stocks waver on the last trading day of the month, with bank models flagging a relatively strong sell strong signal against G10 currencies, bar the Yen. Hence, the DXY is depressed below 92.000 and just off a new 2020 low within 91.762-630 parameters and technically weak unless it can regain momentum and reclaim losses through a Fib retracement level at 91.729. Ahead, Chicago PMI before pending home sales and Dallas Fed manufacturing and a speech from Barkin.

NZD/CHF/EUR/GBP – More independent traction for the Kiwi as it targets 0.7050 vs its US counterpart in wake of improvements in the NBNZ business outlook and own activity readings for November, while the Franc has taken on board a pick up in Swiss retail sales and KOF’s leading indicator slowing less than expected this month rather than mixed weekly sight deposits to maintain gains above 0.9050. Elsewhere, the Euro is making steady measured progress towards 1.2000 after eclipsing resistance at 1.1975, albeit with some assistance from reported Eur/Gbp RHS interest for month end as the cross tests 0.9000 and Cable continues to trade heavy on the 1.3300 handle amidst ongoing Brexit uncertainty and conflicting UK data (BoE consumer credit weak, mortgage lending sub-consensus, but approvals considerably higher than forecast).

CAD/AUD – The Loonie is holding up pretty well between 1.3000-1.2970 parameters given another downturn in oil prices and Aussie also close to 0.7400 following contrasting business inventory and company profits, with similarly divergent external impulses via strength in Chinese PMIs to temper some of the pain inflicted by Beijing’s steep anti-dumping tax on wine and a fresh diplomatic twitter spat.

JPY – A major laggard on the aforementioned lack of demand for portfolio purposes vs the Greenback, as the Yen pivots 104.00 and comfortably inside recent extremes after a raft of inconclusive Japanese data overnight.

SCANDI/EM – The Nok is also displaying a degree of resilience against the backdrop of weaker crude and Sek is consolidating off post-Riksbank lows, while the Cnh has firmed from PBoC midpoint fix levels for the Cny with more reverse repo and MLF liquidity to compound the robust official PMIs and the Try has drawn encouragement from a more pronounced than anticipated GDP rebound in Q3, narrower trade deficit and cheaper oil.

In commodities, WTI and Brent futures trade on the backfoot in the run-up to the decision-making OPEC/OPEC+ meetings over the next two days, for which a full Newsquawk preview can be found here, whilst the Newsquawk OPEC Twitter Dashboard can be accessed here. In terms of where we stand, Sunday’s impromptu meeting offered little in the way of a breakthrough, with the panel of OPEC+ ministers unable to reach an agreement on the extension of current cuts, but most participants are reportedly supporting a delay of hikes through Q1 2021. Market expectations are still leaning towards the second tranche (7.7mln BPD cuts) being extended through in the first three months of 2021, albeit with some sources suggesting an extension by 2-3 months, whilst the most recent sources suggested 3-4 months. Meanwhile, Russia is said to be advocating gradual monthly increases in output from January, according to sources. Nonetheless, futures contracts remain subdued awaiting concrete clarity, with the OPEC meeting set to commence at 13:00GMT/08:00EST and a drip-feed of to-and-fro sources likely. WTI Jan resides under USD 45/bbl (vs. high 45.42/bbl) whilst Brent Feb continues to lose ground sub-48.00/bbl (vs. high 48.04/bbl). Elsewhere, spot gold and silver trade lacklustre despite a lack of fundamental catalysts, but with month-end rotation to keep in mind – with the former struggling to gain ground after yielding the 1800/oz mark. Turning to base metals. Dalian iron ore and Shanghai copper futures extended on recent gains with traders pointing to upbeat economic data from China. LME copper meanwhile is catching tailwinds from the copper performance overnight coupled by somewhat of a recovery in stocks.

US Event Calendar

9:45am: MNI Chicago PMI, est. 59, prior 61.1

10am: Pending Home Sales MoM, est. 1.0%, prior -2.2%

10am: Pending Home Sales NSA YoY, prior 21.9%

10:30am: Dallas Fed Manf. Activity, est. 15.8, prior 19.8

DB’s Jim Reid concludes the overnight wrap

Welcome to what has become “Vaccine Monday” and also the last day of what will very likely be a record month for many equity markets. We’ll give full details tomorrow in our monthly performance review. Everyone will be waiting with baited breath though to see if there is a new vaccine efficacy release before the markets open today. It feels like the next developed world candidates are many weeks behind the three who have reported so far so we’re not expecting anything today but it wouldn’t surprise me if traders were very reluctant to go short, if that was their desire, before noon GMT / 7am NYT. Staying with vaccines, reports suggest that the U.K. will be the first country to approve the Pfizer/BioNTech vaccine, perhaps even early this week, with a view to starting inoculations as soon as next Monday. Meanwhile, the US Surgeon General Jerome Adams has said that Pfizer/ BioNTech is scheduled to submit an Emergency Use Authorization request for their vaccine on December 10 followed by Moderna on December 18 while Anthony Fauci said that vaccines would likely roll out from the middle to end of December.

Overnight we saw China’s November official PMIs with manufacturing printing at 52.1 (vs. 51.5 expected), the highest since September 2017, with services at 56.4 (vs 56.0 expected) bringing the composite reading to 55.7 (vs. 55.3 last month). This beat is leading to Chinese bourses outperforming this morning with the CSI (+0.96%), Shanghai Comp (+0.74%) and Shenzhen Comp (+0.52%) all making advances. Other indices in the region however have largely turned red after opening higher with the Nikkei (-0.61%), Hang Seng (-1.12%) and Kospi (-0.84%) all trading lower. Futures on the S&P 500 (-0.63%) have also turned lower and European ones are also pointing to a weaker open. Elsewhere, Reuters has reported that the Trump administration is adding SMIC and CNOOC Ltd. to a blacklist of “alleged Chinese military companies”.

In other weekend news an informal side OPEC+ meeting last night has seemingly failed to agree a plan to maintain production cuts through Q1. So lots at stake as we head into a two day meeting of the full group today and tomorrow. Crude oil prices are down c. -1.30% overnight. Our Oil strategist Michael Hsueh wrote a piece over the weekend (link here) suggesting that the current oil price factors in maintaining the production curbs and if we don’t get them we could see a -10% fall. So one to watch after a big bull run. Elsewhere, Bloomberg has reported overnight that S&P Global is in advanced talks to buy IHS Markit for about $44 bn and an announcement towards this could come as soon as today. If true, the tie-up would be this year’s second-biggest deal.

Now turning to the latest on the virus and the underlying message continues to remain same with new infections slowing in Europe but continuing to remain high in the US. In France, the positivity rate has now fallen to 11.1%, just over half of where it was in early November and the number of ICU patients are also on a continued decline. A similar pattern to the U.K. and Italy. Meanwhile in the US, Los Angeles and San Francisco imposed tighter restrictions but NYC schools will begin to reopen from December 7 despite the 3% positive test rate breach which had led to closures in the last couple of weeks. Across the other side of the world, South Korea has tightened social restrictions outside of the Seoul area which already had tighter restrictions in place. Hong Kong has said that it will suspend face-to-face classes at kindergartens, primary and secondary schools as cases are on a clear rising trajectory in the city.

Looking forward now and It’s a fairly busy week for data but how much markets will care is a moot point as everyone knows we’re on a short-term path to a double dip but that the short to medium term is a path covered in potential golden vaccine petals.

Data releases include the US jobs report (Friday) and the November PMIs (tomorrow and Thursday), while Fed Chair Powell and ECB President Lagarde will both be speaking through the week. Otherwise, attention will remain on the Brexit negotiations, with just a month remaining until the year-end deadline and less time given any deal has to be ratified across the continent.

Looking into more detail, the US jobs report for October on Friday sees consensus at +500k and a fall in the unemployment rate to 6.8% from 6.9%. Though this would be further progress from the situation in the spring, it would still be the slowest monthly jobs growth since the massive contractions in March and April, and leave the total nonfarm payrolls number over 9.5m beneath its pre-Covid peak back in February. Of some concern is the recent weekly initial jobless claims trend which have risen more than expected for the last couple of weeks. So it feels like a difficult month or so ahead for the US economy.

Meanwhile on the PMIs, the flash readings we’ve already had showed a noticeable deterioration in Europe as much of the continent headed into renewed lockdowns. It’ll be interesting to gauge what’s happening in the countries where there aren’t flash readings however, including a number of emerging markets. Also in focus will be the Euro Area’s flash CPI estimate for November tomorrow as for the previous 3 months it’s been in deflationary territory.

Elsewhere on Brexit I won’t say this is a crucial week as I’ve said this many times before and nothing much has happened. However it probably is now that face to face talks are back and that we’ll are running low on days to ratify a deal. In terms of the current state of play, it has been reported that the last big remaining obstacle in the talks is fishing rights with the UK Foreign Secretary Dominic Raab asking the EU to recognise that regaining control over British waters is a question of sovereignty for the UK. Meanwhile, on other key obstacles of competition rules and state aid, Raab said that he could see “a landing zone”. If fishing is truly now the only stumbling block this is very good news as the numbers here are minuscule compared to the cost of no deal. Sterling is up +0.21% to 1.3339 overnight.

Finally, there are a number of important central bank speakers this week, with Fed Chair Powell and Treasury Secretary Mnuchin appearing before the Senate Banking Committee tomorrow and the House Financial Services Committee on Wednesday. Meanwhile ECB President Lagarde will be speaking today at the European Policy Center Forum, before she appears at an Atlantic Council event tomorrow. The Fed will also be releasing their Beige Book on Wednesday.

To recap the week just gone, risk assets had yet another strong performance and global equity markets soared to all-time highs, with markets buoyed by further positive vaccine news and increasing signs that there’ll be a smooth transition of power in the United States. By the end of the week, the S&P 500 had advanced +2.27% (+0.24% Friday) to hit a new record, as did the MSCI World Index which rose +2.42% (+0.44% Friday) in its 4thconsecutive week higher. In Europe, the STOXX 600 was up +0.93% (+0.41% Friday) at its highest level since the pandemic, while the DAX rose +1.51% (+0.37% Friday) to move back into positive territory on a YTD basis. The moves higher for risk assets coincided with increasingly subdued volatility (at least by 2020 standards), with the VIX index falling -2.86pts last week (-0.41pts Friday) to 20.84pts, which is its lowest closing level since late February. Furthermore, Bloomberg’s index of US financial conditions eased to its most accommodative level since late February too.

Core sovereign bonds saw little movement last week, with yields on 10yr US Treasuries up just +1.3bps (-4.4bps Friday) to 0.84%. That said, there were some notable moves in southern Europe, with yields on 10yr Italian BTPs falling to an all-time low of 0.59%, as yields on 10yr Portuguese debt closed just shy of negative territory at 0.01%. That’s a far cry from the peak of the sovereign debt crisis earlier this decade when the Portuguese 10yr yield spent more than a year above 10% in 2011/12. Some milestones were also reached in FX, where the dollar index fell -0.65% (-0.22% Friday) to reach a 2-year low, while the Euro strengthened +0.89% (+0.42% Friday) to reach a 2-year high against the US Dollar of $1.196. Finally there were some strong performances in the commodities sphere, with Brent Crude oil prices up +7.16% (+0.79% Friday) as they moved higher for a 4th consecutive week, while the industrial bellwether of copper climbed +3.30% (+2.72% Friday) to reach a 6-year high.

Finally Bitcoin declined -8.5% over the week with c. -10% coming through on Thursday/Friday partly due to worries over the prospect of tighter crypto rules in the US.

via ZeroHedge News https://ift.tt/2HQ5ZHB Tyler Durden

Moderna Applies For Emergency COVID Vaccine Approval In US & Europe Tyler Durden

Mon, 11/30/2020 – 07:20

In a repeat of the last three Mondays, positive COVID vaccine news has delivered a jolt to stocks as Moderna has confirmed that it has applied for emergency approval. The company will ask regulators in the US (the FDA) and Europe, as the vaccine is set to become the second COVID-19 vaccine to go into service.

According to the company, in the 30,000-person trial, 196 subjects developed COVID-19 with symptoms after receiving either the vaccine or a placebo. Of those, 185 had taken a placebo, while only 11 had gotten the vaccine, indicating it protects against the disease.

If the FDA clears the shot, distribution could start within weeks. “I think this vaccine is going to be really a game changer for this pandemic,” said Moderna Chief Executive Stéphane Bancel said in an interview with WSJ. “We think it can really prevent severe disease.”

Minutes after the news broke, Bancel appeared on CNBC Monday morning to answer some questions. During the interview, he said the vaccine is “a premium product” intended for health-care workers, the elderly and others with “high risk”. The company is in discussions with Covax, the international program to deliver vaccines to the developing world, to supply some of its vaccines to the program.

Moderna shares surged on the results.

Bancel said that trials for minors – broken into two groups, teenagers and younger children – could start later this year and early next year.

via ZeroHedge News https://ift.tt/2JcVWxf Tyler Durden

S&P Global To Buy IHS Markit In $44BN Deal That Could Be 2020’s Biggest Tyler Durden

Mon, 11/30/2020 – 07:00

The quest to build a functional competitor to Bloomberg and its ubiquitous terminals continues Monday as IHS Markit and S&P Global confirmed reports about a buyout worth some $44 billion.

According to WSJ, S&P Global plans to buy its smaller rival to create “a powerful challenger to information powerhouses Bloomberg and Refinitiv,” assuming the deal goes ahead.

The move would mark the latest round of consolidation among large data providers: A year ago, the London Stock Exchange moved to acquire Refinitiv – formerly known as Reuters’ financial data business – for $27 billion a year ago. New York Stock Exchange owner Intercontinental Exchanges struck its largest deal ever after it agreed to buy US mortgage data provider Ellie Mae for $11 billion.

As the FT points out, the move would mark the latest round of consolidation among large data providers. New York Stock Exchange owner Intercontinental Exchanges struck its largest deal ever after it agreed to buy US mortgage data provider Ellie Mae for $11 billion. That followed the London Stock Exchange’s move to acquire Refinitiv for $27 billion a year ago.

The deal would bolster S&P Global’s data business as the company struggles to compete with Michael Bloomberg’s eponymous Bloomberg LP. IHS Markit, which was formed from the 2016 merger between IHS and Markit, would boost S&P Global’s data and analytics offerings, making it one of the biggest competitors for Bloomberg’s data business.

The industry has seen a wave of consolidation that in turn has made some regulators anxious. In particular anti-trust agents in Brussels have applied intense scrutiny to this deal and the deal between Refinitive and the London Stock Exchange. We suspect the tie up between IHS and S&P Global could face similar obstacles.

via ZeroHedge News https://ift.tt/3o8KHVk Tyler Durden

Airbnb, DoorDash Raise Share Price Targets As US IPO Market Booms Tyler Durden

Mon, 11/30/2020 – 06:24

As global equity markets are on track for their best monthly gains in more than decade, DoorDash and Airbnb are developing new strategies for launching their initial public offerings. As the American economy craters thanks to COVID-19, more than $140 billion has been raised in 383 IPOs, exceeding the previous full-year record high set during the peak of the dot-com boom in 1999, according to data from Dealogic stretching back to the mid-90s.

And just last week, the S&P 500 notched its 26th record close of the year, while the Dow vaulted above the 30,000 mark for the first time last week.

With such promising market conditions, why shouldn’t these companies try to squeeze a few billion dollars more out of their offerings.

Airbnb is planning to target a range of around $30 billion to $33 billion – using a fully diluted share count—when the home-rental startup kicks off its investor roadshow Tuesday, according to people familiar with the matter. That is greater than $30 billion people close to the offering had expected.

DoorDash, meanwhile, plans to target a range of around $25 billion to $28 billion on a fully diluted basis ahead of a roadshow expected to begin Monday. That is greater than the $25 billion people close to the offering had expected.

Typically, companies and their underwriters seek to set relatively conservative IPO ranges, but as WeWork demonstrated back in 2019, that strategy has been abandoned in favor of an aggressive cash grab. Both Airbnb and DoorDash are expected to list in mid-December, which could give markets a nice year-end boost, or perhaps catalyze a crash.

Both companies have successfully survived the pandemic; Airbnb is celebrated for its innovative moves to try and target users looking for longer-term stays in more suburban or even rural areas. A $33 billion valuation would be nearly 2x the $18 billion valuation kicked around during the worst of the pandemic, when market analysts feared the worst might not yet be over.

CEO Brian Chesky swiftly moved to borrow $2 billion while slashing the marketing spend, laying off a quarter of the company’s staff and putting many non-core projects on hold. Bookings at Airbnb rebounded by summer, though they’re still nowhere close to pre-pandemic levels.

DoorDash’s situation is a little different. While the company saw a surge in orders during the pandemic, it still heavily subsidizes each meal delivered with some of its remaining venture capital. In its prospectus, DoorDash warned that it might never be profitable.

via ZeroHedge News https://ift.tt/33tbVhu Tyler Durden

Airbnb, DoorDash Raise Share Price Targets As US IPO Market Booms Tyler Durden

Mon, 11/30/2020 – 06:24

As global equity markets are on track for their best monthly gains in more than decade, DoorDash and Airbnb are developing new strategies for launching their initial public offerings. As the American economy craters thanks to COVID-19, more than $140 billion has been raised in 383 IPOs, exceeding the previous full-year record high set during the peak of the dot-com boom in 1999, according to data from Dealogic stretching back to the mid-90s.

And just last week, the S&P 500 notched its 26th record close of the year, while the Dow vaulted above the 30,000 mark for the first time last week.

With such promising market conditions, why shouldn’t these companies try to squeeze a few billion dollars more out of their offerings.

Airbnb is planning to target a range of around $30 billion to $33 billion – using a fully diluted share count—when the home-rental startup kicks off its investor roadshow Tuesday, according to people familiar with the matter. That is greater than $30 billion people close to the offering had expected.

DoorDash, meanwhile, plans to target a range of around $25 billion to $28 billion on a fully diluted basis ahead of a roadshow expected to begin Monday. That is greater than the $25 billion people close to the offering had expected.

Typically, companies and their underwriters seek to set relatively conservative IPO ranges, but as WeWork demonstrated back in 2019, that strategy has been abandoned in favor of an aggressive cash grab. Both Airbnb and DoorDash are expected to list in mid-December, which could give markets a nice year-end boost, or perhaps catalyze a crash.

Both companies have successfully survived the pandemic; Airbnb is celebrated for its innovative moves to try and target users looking for longer-term stays in more suburban or even rural areas. A $33 billion valuation would be nearly 2x the $18 billion valuation kicked around during the worst of the pandemic, when market analysts feared the worst might not yet be over.

CEO Brian Chesky swiftly moved to borrow $2 billion while slashing the marketing spend, laying off a quarter of the company’s staff and putting many non-core projects on hold. Bookings at Airbnb rebounded by summer, though they’re still nowhere close to pre-pandemic levels.

DoorDash’s situation is a little different. While the company saw a surge in orders during the pandemic, it still heavily subsidizes each meal delivered with some of its remaining venture capital. In its prospectus, DoorDash warned that it might never be profitable.

via ZeroHedge News https://ift.tt/33tbVhu Tyler Durden