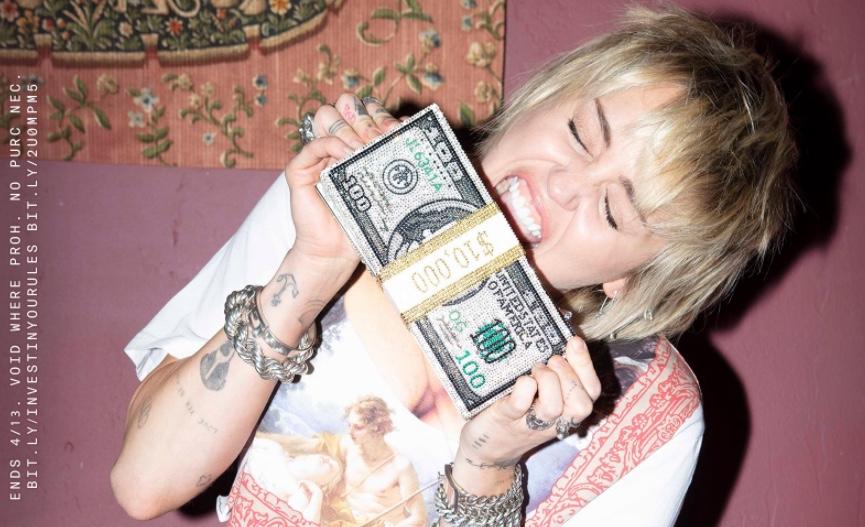

Sign Of The Top? Miley Cyrus Partners With Cashapp To Give Away $1MM In Shares

Investing conventional wisdom dictates that when your taxi driver or hairdresser starts talking stocks, it’s time to sell. But in the post-Trump era, it might be time to modify this just a little to include celebrities hawking stocks – or simply giving them away – on Instagram.

Yesterday, pop singer Miley Cyrus celebrated the 15th anniversary of the debut of her hit Disney television series Hannah Montana – which launched her to instant megastardom – by partnering with the Cash App to give away $1MM worth of stocks. To enter, fans can simply comment on her Twitter or Instagram pages. Cyrus followed up the announcement by sharing a link and urging followers to “learn more about stocks” – or “stonks”, as the kids are calling them.

For those who prefer Robinhood or another discount online brokerage to buy and sell stocks, the Cash App has gained notoriety for allowing customers to buy fractional shares of some of the hottest US-listed companies (like Tesla and Amazon) for as little as $5.

Nothing is more important than investing in yourself. I want to spread ownership to as many people as I can, so I’m teaming up with @CashApp to give out $1 MILLION in stocks. Share your $Cashtag & favorite company name for your chance to own📈#INVESTINYOU #partner #15YearsofMiley pic.twitter.com/mFvkDeNnFV

— Miley Ray Cyrus (@MileyCyrus) March 31, 2021

Learn more about stocks: https://t.co/SH0aKNl6yA #InvestInYou

— Miley Ray Cyrus (@MileyCyrus) March 31, 2021

Bloomberg reported that the promotion shows how stocks have gained “cultural cachet” and are now “cool”, ever since the pandemic helped inspire a retail trading boom that has impacted the structure of contemporary markets in a fundamental way.

It’s the latest illustration of how stocks are gaining pop-cultural cachet after long being relegated to the realm of boring financial instruments associated with Wall Street pros. It’s also a reflection of how Silicon Valley firms such as Square — its chief executive is Twitter co-founder Jack Dorsey — and brokerage app operator Robinhood are leveraging the power of social media to draw more customers.

For what it’s worth, Cashapp owner Square last month purchased $170MM in bitcoin, a reflection of Dorsey’s “belief in cryptocurrencies and the open Internet.”

Of course, while Bloomberg focused on the “stocks are now cool” angle, others took their analysis one step further.

sign of the taup? https://t.co/MIQYq8VwUQ

— jsadinolfi (@jsadinolfi) March 31, 2021

Meanwhile, Cyrus has begun retweeting the excited thank-yous from fans who received stocks during the giveaway. The tickers featured a smattering of popular stocks among retail traders, from Apple to Tesla to Airbnb.

thank you queen #15yearsofMiley #INVESTINYOU pic.twitter.com/FYlKxdIX3W

— em (@miIeystrilogy) March 31, 2021

Thank you so much! 📈#INVESTINYOU #partner #15YearsofMiley pic.twitter.com/ogRjSaFFxS

— Pika Saur (@pika_saur) March 31, 2021

Dude! @MileyCyrus and @CashApp really gave away stock!

Thank you Miley and Cash App! pic.twitter.com/FtmcaJ0dkU

— J (@JordonLCameron) March 31, 2021

Bloomberg reached out to one recipient who requested Tesla shares and asked him why he chose that company? His response: “Go big or go home (nevermind that the Biden administration is pushing to dole out billions of dollars in effective subsidies to EV makers like Tesla).

Why did he want Tesla? “Tesla and Elon are on the forefront of batteries and electric vehicles innovation, so I thought go big or go home,” he said. Alex Mendez, 18, also received $100 worth of Tesla stock, while Madison Bennett, 20, from Boston received $50 worth of it.

The giveaway will continue until April 13.

Tyler Durden

Thu, 04/01/2021 – 15:21

via ZeroHedge News https://ift.tt/3sI6TYR Tyler Durden