US stock index futures were flat on Thursday as investors assessed the impact of a surge in commodity prices on inflation and economic growth while eyeing news that a Ukraine delegation was headed to talks with Russia offering some hope of a ceasefire as the war in Ukraine enters its second week. Contracts on the Nasdaq 100 were down 0.2% by 7:15 a.m. in New York, after the underlying technology-heavy index rallied Wednesday to its highest level in two weeks. S&P 500 futures were flat and Dow futures declined 0.1%.

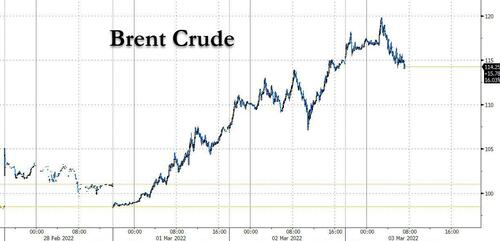

We’ll bring the commodity section up because today that’s where all the action is again: Commodities markets have been upended by the Ukraine crisis as big companies withdraw from Russia, lenders pull back from financing deals and the threat of new sanctions deters buyers. WTI soared to its strongest level since 2008 as the knock-on effect of sanctions starve the world of Russian oil supply, a hole that is over 5mm/d and which can’t reasonably be filled on short notice; Brent neared $120 at one point Thursday before dropping back to $115, while European natural gas whipsawed after rising to a fresh record.

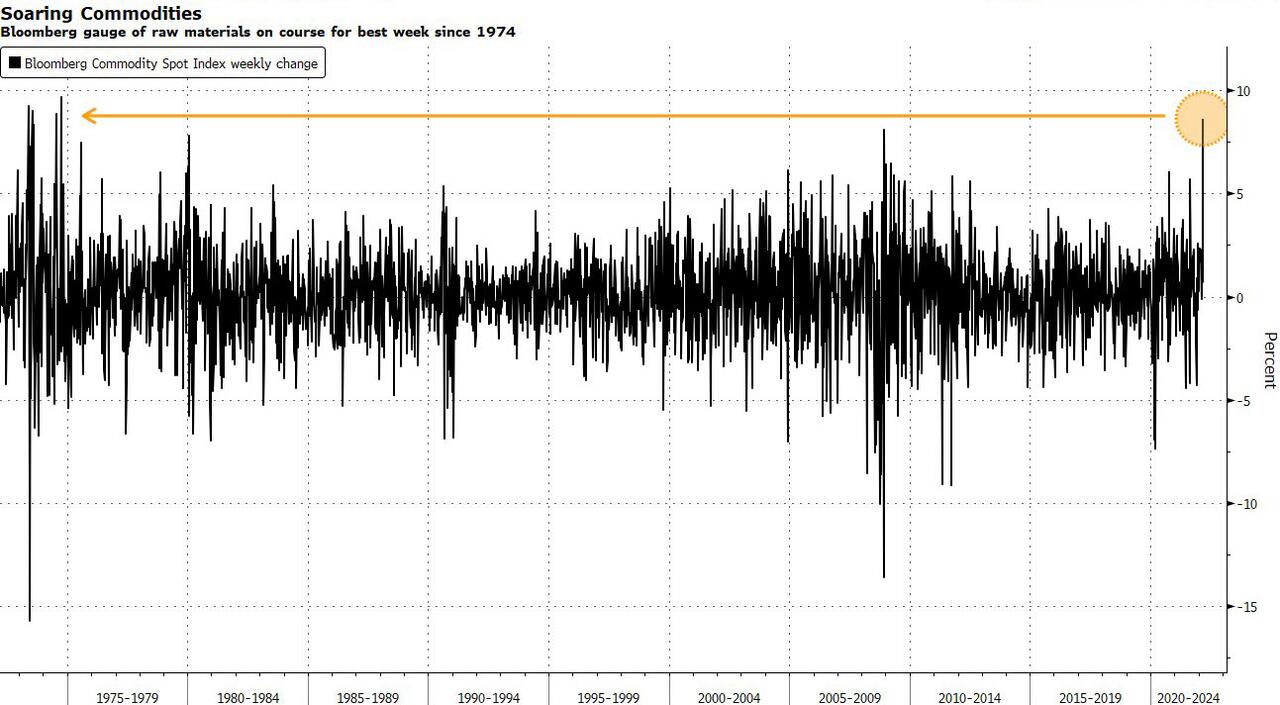

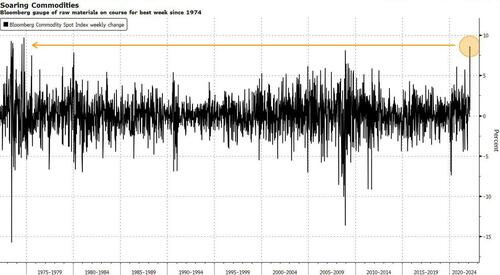

Wheat rocketed past $11 a bushel, zinc hit $4,000 a ton, the highest since 2007, and aluminum hit a new record. The meteoric rallies put the Bloomberg Commodity Spot Index on course for its best week since at least the 1960s. Spot gold rises roughly $3 to trade above $1,930/oz. Most base metals trade in the green; LME nickel outperforms peers. European gas futures pare gains.

Overall, the Bloomberg commodity spot index is having its best week since… the 1973 oil crisis.

Back to stocks, looking at the premarket, Snowflake shares slumped 22% after projecting that product sales growth would slow from its previous triple-digit-percentage pace in the fiscal year, although analysts including at Morgan Stanley remained positive on the software firm. Other notable premarket movers:

- Samsara (IOT US) jumps 15% in Wednesday’s postmarket session after the maker of GPS fleet-tracking devices and other technologies fourth quarter sales beat estimates and set guidance for fiscal 2023 ahead of consensus.

- Several analysts covering Veeva (VEEV US) cut their price targets after the software company forecast adjusted earnings per share for 1Q that missed the average analyst estimate. Shares fell 11% in postmarket trading.

- Anaplan (PLAN US) shares are up 6.6% in postmarket trading after forecasting revenue for the first quarter that topped the average analyst estimate.

- Pure Storage (PSTG US) gains 8.7% in premarket trading after forecasting 2023 revenue, adjusted operating income and adjusted operating margin that beat expectations.

- International Paper (IP US) shares rise 1.1% in premarket after the company tells investors during a presentation that it is “actively reassessing, with all of the stakeholders involved, our options for our investment in Ilim.”

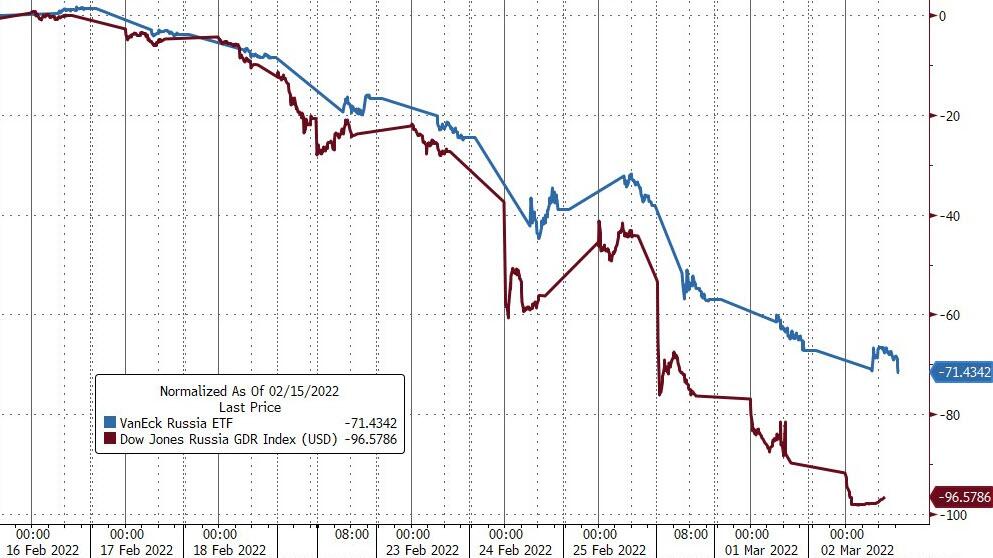

Russia’s ostracism continues: MSCI Inc. and FTSE Russell are cutting Russian equities from widely-tracked indexes, while the London Stock Exchange suspends dozens of Russian depositary receipts from trading, isolating the stocks from a large segment of the investment-fund industry. Russia’s credit rating was cut to junk by Moody’s Investors Service and Fitch Ratings amid doubts about its capability and willingness to service debt. The big question now facing Russian debt owners is whether they ever get their money back. A Russian telecommunications company will be the first test of whether Russian companies continue servicing their foreign-currency bonds. Here is the latest overnight news from Ukraine:

- Next round of Russia-Ukraine discussions could start at 12:00GMT today, according to Belta, citing a Russian Negotiator; with Foreign Minister Lavrov suggesting discussions are to start shortly while the Kremlin remarked that Ukraine is clearly not in a hurry for talks and President Putin’s aide Medinsky says they are still awaiting the arrival of the Ukrainian delegation.

- Most recently, Russian negotiating delegation says “We are waiting for the arrival of the Ukrainian delegation”, according to Sky News Arabia.

- Russian Deputy Foreign Minister believes that talks with Ukraine in Belarus can yield results, via Sky News Arabia.

- Russian Foreign Minister Lavrov says that President Putin and French President Macron are holding phone discussions at the moment. Reported at 10:00GMT/05:00EST

- US President Biden said Russia is responsible for the humanitarian crisis in Ukraine and for devastating human rights abuses.

- US State Department said Russia is engaged in a full assault on the truth regarding the war in Ukraine and that Russia is throttling Twitter, Facebook and Instagram platforms which Russians rely on for independent information.

- Canada imposed sanctions on a total of 10 individuals from Russian energy firms Rosneft and Gazprom.

- FTSE Russell said Russia will be deleted from all FTSE Russell equity indices effective from the open on March 7th, while as portfoliosJapan’s GPIF is looking into announcements by index companies on Russia will need to reflect index changes they track.

- Fitch downgraded Russia’s sovereign rating from BBB to B; Rating Watch Negative and Moody’s also cut .Russia’s sovereign rating from Baa3 to B3; Outlook Negative which put its at junk status

- Germany to deliver 2.7k additional anti-air missiles to Ukraine, via AFP citing gov’t sources.

- Ukraine’s Secretary of the National Security and Defense Council Danilov says that their intelligence is that Russia is set to impose martial law across Russia from March 4th, according to Ukrinform citing the Ukrainian official. Note, this is a report in Ukrainian press and we are yet to see reports on the subject from Russian vendors, as such, proceed with caution. Russian Kremlin subsequently pushed back on such reports.

- Ukraine has requested that the IAEA asks NATO to close the air above Ukrainian power plants to avoid acts of “nuclear terrorism”.

- US President Biden is to hold a call with the Quad leaders Thursday morning re. Ukraine, at 14:00GMT/09:00EST

Besides the chaos unleashed by the Ukraine war, global equity markets have been whipsawed this year as worries around a slowdown in economic growth were compounded by Russia’s invasion of Ukraine, fueling a surge across commodities from oil to grains.

Investors are now watching central banks to see if they are likely to stay the course on aggressively tightening monetary policy, and Fed Chair Jerome Powell managed to “appease risk-markets by ruling out a 50 basis-points hike in March, while simultaneously promising inflation vigilance at following meetings,” Citigroup Inc. strategists William O’Donnell and Edward Acton wrote in a note.

“It’s really time for investors to be prepared for more volatility, especially in the bond markets,” as the Fed has yet to commence balance-sheet reduction, Nancy Davis, chief investment officer at Quadratic Capital Management LLC, said on Bloomberg Television.

“It was quite unusual that Powell was so explicit,” said Stefan Koopman, an economist at Rabobank. “It remains to be seen if the FOMC will be less aggressive in its monetary policy tightening because of the war in Ukraine. It’s also worth emphasizing that this war won’t be settled anytime soon, even as markets derive some optimism on any news of new peace talks. This will continue to keep upwards pressure on (agri-)commodity prices, downward pressure on long-term safe haven yields and some continuously volatile equity markets.”

Bucking the trend in growing pessimism, Citigroup strategists upgraded U.S. stocks and the technology sector to overweight, saying growth trades should benefit from the recent sharp drop in real yields. Of course, this happens one day after Citi closed its oil short at a 11% loss in a month, so maybe this is just the right signal to pile on those shorts.

In Europe, the Stoxx 600 Index fell 0.6% with utilities and travel and leisure stocks among the biggest decliners while shares in firms with exposure to Russia tumbled.

Earlier in the session, Asian stocks advanced as comments by Federal Reserve Chair Jerome Powell gave investors some relief amid concerns over the Russia-Ukraine war. The MSCI Asia Pacific Index rose as much as 0.9%, lifted by financial and industrial shares. Japan and South Korea equities were among the best performers, getting boosts from electronics and auto makers. In his testimony to U.S. lawmakers, Powell backed a quarter-point rate increase later this month while vowing to combat inflation in light of global political risks. The modest increase helped ease investor fears of aggressive Fed policies to control the pace of price increases even as oil continued to surge due to the war. “Capital may be flowing back to risk assets for bargain-hunting opportunities after the severe selloff over the last few days,” said Margaret Yang, a strategist at DailyFX. “Still, geopolitical uncertainties may cap the extent of the rally until progress is made between Russia and Ukraine in negotiating a ceasefire agreement.” Asian equities were on track for their first weekly gain in three, as the region remained resilient given its relatively limited exposure to Russia. The Asian stock benchmark has declined less than 6% so far this year, compared with drops of about 8% in European and U.S. counterparts. Chinese stocks fluctuated after the Wall Street Journal reported that the nation is exploring an exit from its zero-tolerance approach to Covid-19. The Indonesia market was closed for a holiday.

Japanese equities climbed, following a rally in U.S. peers after Federal Reserve Chair Jerome Powell said the economy is expanding enough to withstand rate hikes while pledging to be judicious in removing stimulus. Banks and trading houses were the biggest boosts to the Topix, which rose 1.2%. Daikin and M3 Inc. were the largest contributors to a 0.7% rise in the Nikkei 225. The yen slightly extended its 0.5% overnight loss the dollar. “There is still concern about how high rates will go in the medium term,” said Shogo Maekawa, global market strategist at JP Morgan Asset Management. “But for now Powell maintained his outlook of a 0.25 percentage point hike so now we’re past the first point of uncertainty.”

In rates, Treasuries were relatively calm with yields richer by 2bp-3bp across the curve. Curve spreads are broadly within a basis point of Wednesday’s closing levels following extreme volatility in yields and spreads over past two sessions; 10-year yields around 1.86%, ~2bp lower on the day while gilts, bunds are cheaper by 9bp and 6bp in the sector. Gilts lead broad fixed-income selloff, while dollar rallies and stocks fall. Gilts lead a broad selloff in fixed income, bear-flattening with short end about 9bps cheaper. Traders move forward wagers on 125bps of BOE tightening to November from December previously. Bunds also bear-steepen but are ~5bp richer to gilts. IG dollar issuance slate includes CBA 5-part, Sumitomo Mitsui Trust 3Y/5Y and Honda 3Y/5Y/10Y; sixteen issuers priced $18b Wednesday across 28 tranches in busiest day in six months. Focal points of U.S. session include Fed Chair Powell’s second day of congressional testimony and a busy economic data slate. Three-month dollar Libor jumps more than 6bp, biggest increase since Feb. 11.

In FX, the Bloomberg Dollar Spot Index climbed 0.2% and the greenback was steady to higher against its Group-of-10 peers; Canadian and Australian dollars were the top performers as commodities powered higher. Treasuries inched up, led by the 2-year tenor. The euro slipped for a fourth day against the greenback, after falling to the lowest since May 2020 on Wednesday. Bunds fell as they caught up with Treasuries, and Italian bonds extended their slide and underperformance against euro-area peers after demand fell at a sale of Spanish debt. The pound weakened against the dollar but rose to its strongest level versus the euro since July 2016 as sterling proved relatively resilient to market shocks from the war in Ukraine. Gilts fell after money markets increased bets on Bank of England rate hikes after the most dovish member of the Monetary Policy Committee, Silvana Tenreyro, said she expects “upside surprises on inflation” on Wednesday. Aussie rose to the highest level since November against the greenback, and neared its 200-DMA, before paring gains. Aussie sovereign bonds extended losses made after Fed Chair Jerome Powell reaffirmed his support for a 25 basis- point rate hike this month. The yen weakened for a second day amid broad strength in the greenback. Japan’s 30-year bond pared an intraday loss after the sale of this tenor confirmed resilient demand. Ruble continues to underperform EMFX peers.

In commodities, the rally faded slightly after assets from gas to oil surged earlier as buyers rushed to stock up on materials due to fears of how the increasing economic isolation of Russia will impact trade. Oil pares some gains. Brent trades at $115 after rising as high as $119 a barrel. WTI falls back to $112 after soaring to the highest since 2008 as buyers shun Russian crude. Investors bet that oil will rise further. Spot gold rises roughly $3 to trade above $1,930/oz. Most base metals trade in the green; LME nickel outperforms peers. European gas futures pare gains.

Bitcoin has been erring lower throughout the session after an initial move higher fizzled out, though, Bitcoin remains towards the top-end of recent levels capped by the USD 45k mark.

Looking at day ahead now, and we’ll hear from Fed Chair Powell again, this time before the Senate Banking Committee. Other central bank speakers include the Fed’s Barkin and Williams, Bank of Canada Governor Macklem and the ECB’s de Cos. On top of that, we’ll also get the minutes from the ECB’s February meeting. On the data side, releases include the global services and composite PMIs for February, as well as the ISM services index for February from the US. Other releases include the Euro Area unemployment rate and PPI for January, while in the US we’ll get the weekly initial jobless claims and January’s factory orders. Finally, earnings releases include Broadcom and Costco.

Market Snapshot

- S&P 500 futures down 0.1% to 4,375.50

- STOXX Europe 600 down 0.3% to 444.91

- MXAP up 0.6% to 181.77

- MXAPJ up 0.4% to 595.82

- Nikkei up 0.7% to 26,577.27

- Topix up 1.2% to 1,881.80

- Hang Seng Index up 0.6% to 22,467.34

- Shanghai Composite little changed at 3,481.11

- Sensex down 0.8% to 55,035.74

- Australia S&P/ASX 200 up 0.5% to 7,151.40

- Kospi up 1.6% to 2,747.08

- German 10Y yield little changed at 0.05%

- Euro down 0.4% to $1.1077

- Brent Futures up 2.8% to $116.11/bbl

- Brent Futures up 2.8% to $116.12/bbl

- Gold spot down 0.1% to $1,926.29

- U.S. Dollar Index up 0.27% to 97.65

Top Overnight News from Bloomberg

- Russian forces pressed ahead with their offensive in Ukraine as the war entered its second week, firing missiles at Kyiv overnight and stepping up their campaign to take cities in the coastal south

- The sanctions the U.S. and Europe are slapping on Russia’s economy and the billionaires around President Vladimir Putin are unprecedented in scope. Some experts wonder if these powers have made clear what actually needs to happen to get those restrictions lifted

- Bank of Japan board member Junko Nakagawa says there is no need to make a significant change in monetary policy for now in response to events in Ukraine, though the situation warrants close attention

- Commodities are on course for their most stunning weekly surge in records that go back to when Nikita Khrushchev was in the Kremlin

- European natural gas rose to a fresh record near 200 euros a megawatt-hour. The European Commission wants at least 80% of gas storage facilities in the EU to be filled by Sept. 30, accelerating plans to reduce the bloc’s dependence on Russian gas, Der Spiegel reported, citing a draft paper on a new energy security strategy to be presented next week

- As traders try to navigate a global crude market upended by the invasion of Ukraine, an offer of a Russian Far East cargo that drew no bids suggested that spot differentials on the nation’s oil may weaken sharply

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mostly positive after the gains in the US where stocks and yields climbed amid peace talk hopes and hawkish central bank rhetoric, but with upside capped as the region digested a slowdown in Chinese Caixin Services PMI data. ASX 200 was underpinned by a commodity surge, spearheaded by the energy sector as Brent rose to its highest level since 2013. Nikkei 225 benefitted from a weak JPY but with gains capped as Tokyo and neighbours seek an extension of COVID measures. Hang Seng and Shanghai Comp were mixed with the mainland clouded after PBoC’s liquidity drain and soft PMI data

Top Asian News

- Asia Stocks Rise as Powell Comments Boost Investor Mood Amid War

- Indian Agrochemical Firm UPL Said to Draw Takeover Interest

- Developer Shares Gain on Regulator’s Remarks: Evergrande Update

- Hong Kong Reports 56,827 Covid Cases, 144 Deaths Thursday

European bourses, Euro Stoxx 50 -0.5%, are moving in-line with the generally cautious mood as we await the commencement of the Russia-Ukrainian negotiations, which are set for around 12:00GMT/07:00EST; though, we are yet to see the Ukrainian delegation arrive. Within sectors, the picture is mixed after initial relative underperformance in cyclical names. US futures are modestly softer, ES -0.2%, but have been fairly contained amid the geopolitical developments awaiting US data and Chair Powell’s second day of testimony

Top European News

- European Gas Hits Record Near 200 Euros With Sanctions in Focus

- U.K. Feb. Composite PMI 59.9 vs Flash Reading 60.2

- Traders Stockpiling Bonds Are Causing a Great Collateral Squeeze

- Russia’s Gas Giant Shunned by European Traders and Landlord

In FX, high stakes and anxiety levels in the FX space as Russia and Ukraine head for ceasefire fire talks from around 12:00GMT/ 07:00EST. DXY firm either side of 97.500 as yields rise again and risk aversion resurfaces. Aussie underpinned near 0.7300 and the 200 DMA as industrial metals remain strong. Franc rebounds following above forecast Swiss CPI in stark contrast to Lira after latest acceleration in headline and pipeline Turkish inflation; USD/CHFf sub-0.9200, EUR/CHF circa 1.0200 and Usd/Try above 14.000. Euro still lagging on conflict contagion and Rouble back down towards all time lows; EUR/USD under 1.1100 and Usd/Rub eyeing 119.00

In commodities, WTI & are off best levels, at USD 116.50/bbl and USD 119.84/bbl for WTI April and Brent May respectively,Brent but remain at elevated levels ahead of negotiations. Japan plans to hold a ministerial meeting on Friday to compile measures to respond to higher oil prices. Gazprom is shipping gas to Europe via Ukraine, in-line with requests; separately, the Yamal-Europe pipeline westbound gas flows to Germany from Poland have stopped, via Reuters citing Gascade data. Iran’s Energy Minister Owji says domestic oil production can hit maximum capacity in one/two months following a nuclear agreement being reached, via Reuters citing a Telegram channel. Spot / are supported but around familiar parameters while base metals experienced noted overnightgold silver upside, particularly nickel and zinc.

US Event Calendar

- 8:30am: U.S. Initial Jobless Claims, Feb. 26, est. 225k, prior 232k

- Continuing Claims, Feb. 19, est. 1420k, prior 1476k

- 9:45am: U.S. Markit US Services PMI, Feb. F, est. 56.7, prior 56.7

- 10am: U.S. Durable Goods Orders, Jan. F, est. 1.6%, prior 1.6%; -Less Transportation, Jan. F, est. 0.7%, prior 0.7%

- Cap Goods Orders Nondef Ex Air, Jan. F, no est., prior 0.9%

- Cap Goods Ship Nondef Ex Air, Jan. F, no est., prior 1.9%

- 10am: U.S. Factory Orders, Jan., est. 0.7%, prior -0.4%

Central bank speakers

- 10am: Fed Chair Powell Testifies Before Senate Panel

- 11:30am: Bank of Canada’s Macklem Gives Economic Progress Report

- 12pm: Fed’s Barkin Speaks on Economy

- 12:45pm: Bank of Canada’s Macklem to Hold Press Conference

- 3:30pm: Bank of Canada Speaks to Lawmakers at Committee Hearing

- 6pm: Fed’s Williams Takes Part in Discussion on the Economy

DB’s Jim Reid concludes the overnight wrap

We go to press this morning after another volatile 24 hours in markets, one that saw equities and sovereign bond markets retrace the prior day’s declines (completely so in the case of American assets), while energy prices and inflation breakevens have kept marching higher. Policymakers are facing an unenviable situation over the near-term; inflationary pressures are mounting while the broader outlook grows more uncertain by the day. The latest commodity price spike overnight has now taken Brent Crude oil above $118/bbl, and it’s only slightly retraced that since to $116.75/bbl. Bear in mind that before the US warning of an invasion in mid-February it was trading just above $90/bbl. That spike in oil prices has occured as data yesterday showed Euro Area inflation reached to its highest level since the formation of the single currency. And as our economists have already written, if this commodity shock persists then that’s going to have negative implications for European growth, raising the spectre of a significant slowdown ahead. Indeed yesterday we saw the 2s10s Treasury yield curve hit another low that hasn’t been matched since March 2020 despite the selloff in yields (more below), speaking to the worry that central banks will have to hike in to a deteriorating outlook. Likewise in Europe, after an historic rally the day before that saw 10yr bunds blow through z scores (see my CoTD from yesterday, link here) rates sold right back off yesterday. It’s thus timely that our European rates team will be hosting a call at noon London time today, which you can register for here.

This morning however, Asian markets have followed the rebound in the US and Europe, supported by the comments by Fed Chair Powell that have helped to reduce uncertainty about the Fed’s near-term intentions (more on which below). The Nikkei (+0.76%), Hang Seng (+0.63%) and the Kospi (+1.45%) are all trading higher this morning, with the latter’s advance coming as South Korea reported GDP grew by +1.2% in Q4 (vs. +1.1% expected). Mainland stocks in China have posted a more mixed performance however, with the Shanghai Composite (+0.10%) just about in positive territory whilst the CSI (-0.29%) has lost ground, which has occurred after China’s Caixin services PMI edged down to a 6-month low of 50.2 (vs. 50.7 expected), so just about in expansionary territory still. US equity futures are fairly steady this morning as well, with those on the S&P 500 up +0.11%.

In terms of the latest in Ukraine, there has been continued fighting in the country, although the prospect of talks today between Russia and Ukraine has offered a semblance of hope. Although the ruble strengthened slightly on news of the further peace talks, the broader financial situation hasn’t appeared to improve much for Russia, with Moody’s and Fitch downgrading their sovereign debt to junk status overnight, while MSCI reported it would remove Russia from its equity indices due to issues of market access. The Bank of Russia reported that equity indices would remain closed today, as they have all week so far.

For markets, one of the biggest ways the conflict has manifested itself is this massive spike in commodities, with yesterday bringing yet another round of broad-based increases that will only intensify the inflationary pressures already here. Brent crude ended the day up +7.58% at $112.93/bbl, which was its highest closing level since 2014 and took its YTD gains beyond +40%. Then overnight it surpassed that to reach its highest levels since 2013 and take its YTD gains above +50%. Meanwhile, WTI also saw a similar move higher, rising +6.95% to its highest level since 2013 at $110.60/bbl, and this morning it’s now above $114/bbl. Those increases follow President Biden’s indication that he’d be open to the imposition of sanctions on Russian oil and gas, saying that “nothing is off the table” when he was asked about the potential of the US banning Russian oil imports. Indeed, influential US Senators began drafting a bill that would ban US imports of Russian oil and gas products. When it came to natural gas, we saw some significant price increases there too, with futures in Europe up by a massive +36.05% to €165.54/MWh, which leaves them just shy of their pre-Christmas peak. This pressure could be seen across the board, with aluminium (+2.62%) at a record and wheat prices (+5.67%) reaching levels not seen since 2008, which just shows the extent to which the current conflict is affecting commodity markets right now.

Those commodity price rises came amidst further inflation records, with the Euro Area flash CPI print for February coming in at +5.8% (vs. +5.6% expected), which is its highest level since the formation of the single currency. Core CPI was also up to +2.7% (vs. +2.6% expected), another record since the Euro’s formation. The effects of all this were evident in market-based measures of inflation expectations, with the 10yr German breakeven up by a further +9.0bps to 2.28%, its highest level in a decade, and its Italian counterpart (+4.8bps) also hit a decade high of 2.08%. Interestingly, we heard from ECB Chief Economist Lane later in the European session, who said ahead of the ECB meeting next week, that “the schedule for the March staff projections exercise has been revised in order to take into account the implications of the Russian invasion of Ukraine”, which means that they’ll include the upside inflation release from yesterday as well. He struck a balanced note in his speech, acknowledging that an adverse supply shock means that “the horizon over which inflation returns to the target level could be lengthened in order to avoid pronounced falls in economic activity and employment”. But then he also said that “it is essential to avoid that a spell of temporarily-high inflation pressures – even if arising from a supply shock – becomes entrenched by permanently altering longer-term inflation expectations.”

Staying on that central bank theme, we had some significant headlines from Fed Chair Powell yesterday as he testified before the House Financial Services Committee. First, he said that “I am inclined to propose and support a 25 basis-point rate hike” at the March meeting, so steering away from the more hawkish possibility of a 50bp move that markets had already begun to price out. That said, he noted “we would be prepared to move more aggressively” if inflation remained high, so not ruling out moves larger than 25bps if justified. The Chair also remarked that policy may need to tighten above neutral, which he put as the policy rate between 2%-2.5%, as opposed to simply being less accommodative. Meanwhile on Ukraine, Powell said that the “implications for the US economy are highly uncertain, and we will be monitoring the situation closely.”

That confirmation of likely rate hikes ahead helped Treasury yields fully retrace the previous days’ decline, with the 10yr yield up +14.9bps to 1.88%. As mentioned at the top however, the more policy-sensitive 2yr yield (+17.1bps) saw a larger rise that saw +23.5bps of hikes priced back into money markets through 2022. The curve thus bear flattened, and the 2s10s curve fell to 35.9bps, after falling as low as 31.3bps intraday. The 2s10s curve has now flattened by more than 120bps since its peak at the end of Q1 last year. Those movements in Treasuries echoed what took place in Europe, where yields on 10yr bunds (+9.9bps) moved back into positive territory, and those on 10yr OATs (+11.9bps), gilts (+13.1bps) and BTPs (+15.3bps) all moved higher as well.

For equities, they managed to stage something of a recovery against this backdrop, with the S&P 500 (+1.86%) actually moving back into positive territory for the week. That was part of an incredibly broad-based advance that left 466 companies in the index in the green on the day, which is the second-highest so far this year. In Europe the advances weren’t quite as strong, with the STOXX 600 only up +0.90%, but indices across the continent moved higher including the DAX (+0.69%), the CAC 40 (+1.59%) and the FTSE 100 (+1.36%). When it came to Russian assets, stock trading was closed for a third consecutive day, although depositary receipts in London continued to decline yesterday, with those for Gazprom down -23.50%, whilst Sberbank fell another -78.43%.

Another central bank announcement yesterday came from the Bank of Canada, who became the latest to start hiking rates for the first time since the pandemic. They increased their target for the overnight rate by 25bps to 0.5%, and said in their statement that “the Governing Council expects interest rates will need to rise further.” In reference to the Ukrainian conflict, they said that the invasion was “putting further upward pressure on prices for both energy and food-related commodities”, which along with other factors meant that “inflation is now expected to be higher in the near term than projected in January.” This hawkish-leaning language meant that the Canadian dollar was the strongest performing G10 currency yesterday, gaining +0.88% against the US Dollar, and markets are fully pricing in another hike at their next meeting in April.

Aside from the Euro Area CPI release there wasn’t much in the way other data yesterday. However, we did get the ADP’s report of private payrolls from the US, which rose by +475k in February (vs. 375k expected). That comes ahead of tomorrow’s jobs report, where our US economists are anticipating growth of +300k in nonfarm payrolls.

To the day ahead now, and we’ll hear from Fed Chair Powell again before the Senate Banking Committee. Other central bank speakers include the Fed’s Barkin and Williams, Bank of Canada Governor Macklem and the ECB’s de Cos. On top of that, we’ll also get the minutes from the ECB’s February meeting. On the data side, releases include the global services and composite PMIs for February, as well as the ISM services index for February from the US. Other releases include the Euro Area unemployment rate and PPI for January, while in the US we’ll get the weekly initial jobless claims and January’s factory orders. Finally, earnings releases include Broadcom and Costco.