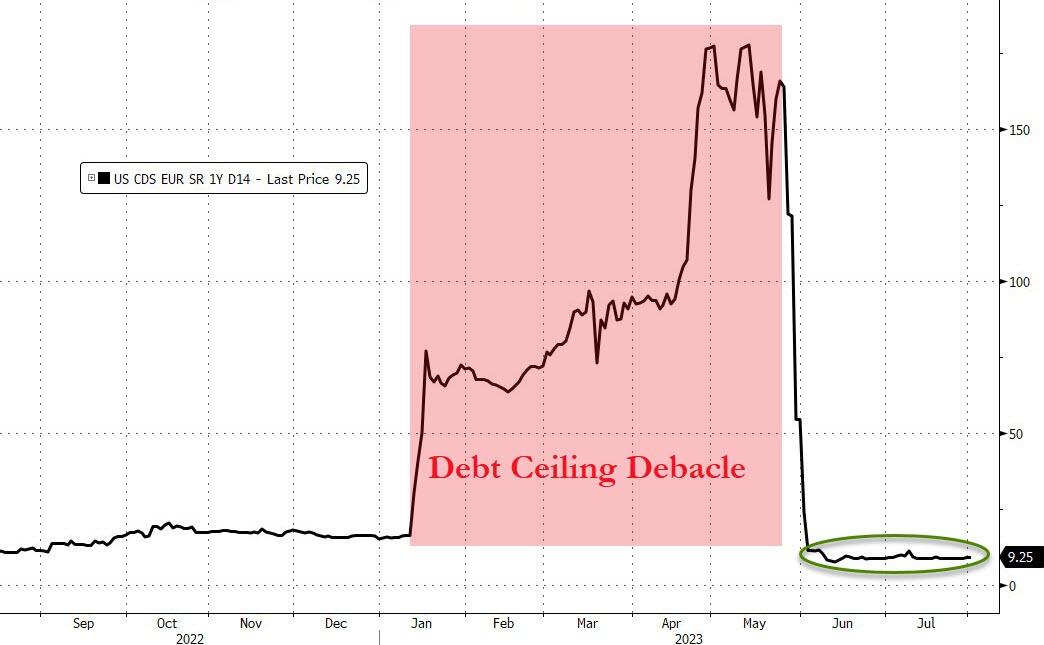

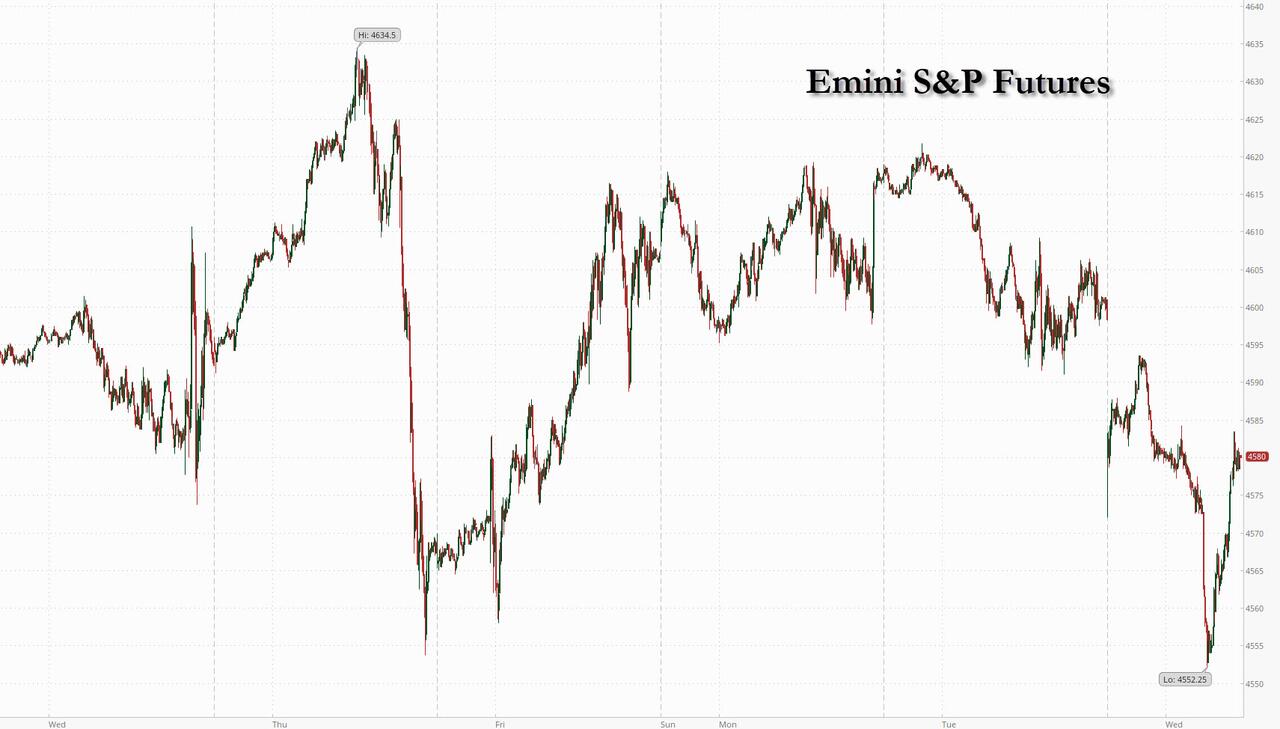

US futures slumped as part of a global risk-off tone (but were well off their lows, which were down as much as 1%), after the US was stripped of its AAA top-tier credit rating by Fitch (which joined S&P in doing so back in 2011), due to growing fiscal deficits and an “erosion of governance” even as Treasuries yields and the Dollar were steady. And in a complete coincidence, at the exact same time, Donald Trump was indicted for a record third time on federal charges over his efforts to overturn the 2020 presidential election, and has a court date set for Thursday.

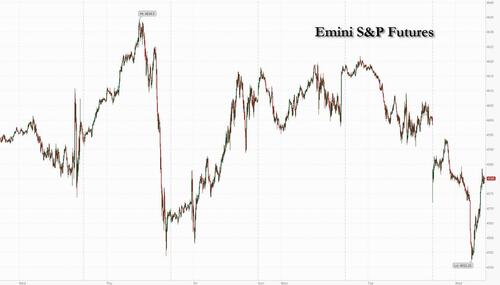

As of 7:45am, emini S&P futures were down 0.5%, while Nasdaq 100 futures slid 0.8%, signaling a pullback later Wednesday for a market that has surged 44% in 2023. Broad losses in Europe dragged all industry groups in the benchmark regional index into the red. Asian and European stocks slumped, while the Treasury curve steepened with two-year TSY yields falling 4bps to 4.86%; the Bloomberg Dollar Spot Index was barely changed, up 0.1%.

In premarket trading, AMD rose as much as 1.2% in premarket trading on Wednesday, after the chipmaker reported better-than-expected second-quarter results and said it was making further inroads in artificial-intelligence computing. Analysts noted that there are indications that the PC business was recovering and they were also optimistic about the company’s AI potential. Starbucks dropped as its quarterly sales fell short of analysts’ estimates, a sign that momentum may be slowing for the coffee giant amid higher prices and tighter pocketbooks. Pinterest slid after the social networking company failed to meet heightened expectations. Apple and Amazon.com are among companies scheduled to report this week, with investors on the lookout for clues on how high interest rates are affecting the economy. Here are some other notable premarket movers:

- Cardlytics shares jumped as much as 19% and are set to reach their highest level since last Sept., after the company, which makes software to analyze customer purchases, reported results that beat expectations, helping to ease worries over a tough backdrop for the advertising industry. JPMorgan raised its price target on the stock, positive on the progress seen with new products and initiatives.

- KeyCorp upgraded to neutral at JPMorgan, with analysts noting that the risks of a dividend cut at the financial services company had waned after US regulators gave it more time to comply with new capital rules. Shares fell as much as 1.8%, however, after Fitch’s downgrade of the US sovereign credit grade hit sentiment across risky assets.

- Lumen Technologies shares fall 8.4% in US premarket after the wireline telecommunications company posted what analysts saw as a mixed set of 2Q results with free cash flow weaker than expected.

- Oatly Group fell 2.0% after JPMorgan downgraded the oat-milk producer to neutral from overweight due to the “increasingly opaque” growth story.

- Pinterest shares fall as much as 5% in premarket trading on Wednesday, after the social networking company reported its second-quarter results and provided an outlook. Citi said the report failed to meet heightened expectations.

- Rover Group rises as much as 27% in premarket trading after the online pet care platform boosted its year revenue and adjusted Ebitda forecast. International growth remains solid, with strong lifetime value metrics and product improvements driving tailwinds for top and bottom-line results, says William Blair.

- SolarEdge Technologies shares slid as much as 14% in US premarket trading after the solar-equipment maker’s third-quarter revenue forecast disappointed as elevated levels of inventory among its customers weighed on demand. Other solar stocks fell in US premarket trading after the report.

- Starbucks shares fall 1.3% after the coffee- chain operator’s third-quarter comparable sales missed estimates. Overall, analysts were disappointed in the print, flagging lower-than-expected comparable sales in North America as well as the weaker-than-anticipated outlook for the metric in China.

- Virgin Galactic fell as much as 8.9% after the company’s revenue fell short of analysts’ expectations, even as the space-tourism company gears up for monthly commercial flights. Analysts note that while the firm will continue to burn cash, it does have enough on its balance sheet to fund near-term investments.

There was disagreement over the consequences of the Fitch downgrade: some said it serves up an extra dose of jeopardy for equity investors already concerned over the risks of recession and whether this year’s run-up in stocks is sustainable; others looked at the complete lack of reaction in Treasuries and claims it is a complete non-event, and that it will be forgotten by the market in a few hours. And indeed, Treasuries were steady, in keeping with Janet Yellen’s assertion that they remain “the world’s preeminent safe and liquid asset” for now.

“One can have the feeling that the market is looking for excuses to take some profits,” said Alexandre Baradez, chief market analyst at IG Markets in Paris. “But rather than the Fitch downgrade, I suspect that what’s currently being priced is the growing risk of an economic slowdown. The downward trend started to emerge yesterday on the back of disappointing Chinese and US data, which suggests it’s not really about the rating downgrade, but rather the risk of a slowdown.”

Indeed, the consequences of the latest downgrade seem positively tame by comparison: the last time the US sovereign credit rating was downgraded, the S&P plunged 6.7% with all stocks in the red for the first time since at least 1996, and briefly dropped into a bear market (the benchmark eventually erased those losses five trading days later and is up 282% since). Also, yields tumbled, gold exploded and the SNB was forced to devalue the franc.

European stocks also slumped with the Stoxx 600 down 1.3% and on course for its largest fall in almost four-weeks. Ferrari slumped more than 4% after the Italian supercar maker issued disappointing guidance. Siemens Healthineers AG fell after the German medical technology company missed estimates. Hugo Boss AG dropped after the fashion retailer’s margin fell short of expectations and inventories rose. Here are the biggest European movers:

- BAE Systems shares rose as much as 6.6% after the defense and aerospace company upgraded its 2023 guidance and approved a further buyback of as much as £1.5 billion

- Taylor Wimpey shares rose as much as 4.7% after the residential housing developer’s results for the first-half exceeded expectations. Analysts said that the company raising the bottom end of its guidance range for UK completions for the year was a positive sign in a tough market

- Melexis shares rise as much as 6.5% after the chipmaker raised margin guidance and boosted revenue outlook to top end of its prior range, a sign that strong demand for automotive chips continues to benefit the Belgian company

- Virgin Money gains as much as 3.3%, outperforming a broader market decline, after the UK lender announced a share buyback. It also reported steady net interest margins

- ConvaTec shares gain as much as 7.8%, the biggest intraday gain since November 2022, after the wound care and ostomy products provider reported first-half revenue that beat estimates and boosted its full-year organic revenue forecast. Citi said it was particularly impressed by growth in wound care as well as the strong gross margin

- Iveco shares advance as much as 5.5%, the most since mid-March, after the truckmaker delivered another boost to full-year guidance that analysts say will prompt a significant increase in consensus expectations

- Siemens Healthineers falls as much as 8%, the most since May, after the German medical technology firm’s Varian unit weighed on its latest quarterly earnings, with margins a particular concern, analysts say

- JDE Peet’s falls as much as 4.4%, after the Dutch coffee company cut its adjusted Ebit guidance on uncertainty over the transition from international brands to local brands in Russia

- Hugo Boss shares declined as much as 5% at the open on Wednesday but then pared losses to 0.7% by 9:36 am in Frankfurt. While the German fashion group raised its guidance for 2023 and second-quarter earnings beat most expectations

- Schaeffler drops as much as 5.2% as Citi writes that the German automotive and industrial supplier’s second- quarter results were overshadowed by “concerning” organic growth underperformance in auto-tech

- Man Group shares drop as much as 3.7%, adding to Tuesday’s 5.5% decline, following results which reflected a lower-margin long-only shift from clients. The recent stock price weakness is an “over-reaction,” according to UBS

- Auto1 shares fall as much as 14%, the most since January, after the used-car trading platform reported second-quarter revenue and units sold below estimates

Earlier in the session, Asian stocks posted the biggest decline in more than four months as technology names dropped. Japanese stocks slumped the most this year as gains in the yen dented the outlook for corporate profit; the Nikkei 225 underperformed and dipped below the 33,000 level as the focus shifted to corporate earnings and despite comments from BoJ’s Deputy Governor Uchida who stuck to a dovish tone.

The MSCI Asia Pacific Index fell 1.5%, with all sectors and major markets in the red. Benchmarks dropped more than 1% in Japan, South Korea and Taiwan, and about 2% in Hong Kong, as investors booked profits on chip and electric-vehicle stocks that have surged on artificial intelligence and net-zero emissions trades. “It’s buyers’ fatigue,” said Derek Tay, head of investments at Kamet Capital Partners. US stock futures declined after Fitch stripped the US of its top-tier credit grade, though few market participants saw that as having a major impact on Asian equities. Some investors rather appeared to be taking bets off the table ahead of US employment data later this week, which may influence the Federal Reserve’s next policy decision. “We’ve had an extraordinary run in risk markets and we are starting to get some steepening in the yield curve,” said Matthew Haupt, portfolio manager at Wilson Asset Management in Sydney. “We might get some squeeze on that big rate-cut trade,” he added. The MSCI Asian benchmark earlier this week flirted with its highest close since last April after a rally fueled by hopes for Chinese efforts to boost its economic recovery and a peak-out in US interest rates. The gauge is still up about 6% since the start of June. Australia’s ASX 200 declined with utilities, real estate and financials leading the broad-based retreat and with weaker AIG Manufacturing and Construction data adding to the glum mood.

In FX, the Bloomberg dollar index erased losses as investors bought into the dip that followed Fitch Ratings’ US sovereign credit-rating downgrade. Leveraged short covering of the yen and Australian dollar was short-lived with the latter breaching support below 0.6600 as an Asia Pacific equity gauge headed for the biggest decline in almost a month. New Zealand’s dollar was sold for the greenback and Aussie as a jump in the nation’s jobless rate fueled bets that rates had peaked.

In rates, the front-end of the Treasury curve led gains, extending Tuesday’s steepening move and leaving 2-year notes richer by around 4bp in early US trading. Longer Treasuries broadly shrugged off the US downgrade news. US 10-year yields are little changed on the day, sitting around 4.02% and offering muted reaction to the Fitch downgrade; bunds outperform by around 4bp in the sector while gilts trade slightly cheaper. Front-end gains on the day steepen 2s10s, 5s30s spreads by 3.8bp and 3bp, with both remaining near session highs. For the first time since November 2020, the quarterly unveiling of auction amounts is expected to feature across-the- board increases to the Treasury’s seven main offerings of notes and bonds. German two-year yields fall 6bps to a two-week low of 3.01%. Dollar IG issuance slate empty so far; Tuesday session was inactive for new deals, while August volume projection is around $85 billion. A focus of the day is the quarterly refunding announcement at 8:30am New York time.

“US Treasuries are the world’s largest and most liquid sovereign bond market,” said Alvin Tan, head of Asia FX strategy at RBC Capital Markets in Singapore. “It’s unthinkable large global bond investors will decide to entirely exclude US Treasuries from their holdings. If they do, what USD-denominated bonds will they hold?”

In commodities, oil extended its rally with Brent crude up 0.8%, after API pointed to a huge, in fact a record 15 million drawdown in US inventories, adding to signals the market is tightening. Spot gold adds 0.3%. Bitcoin gains 0.9%

After a data heavy day yesterday, we have only the US July ADP report as the major data release to look forward to today. But watch out for the refunding announcement. Key company earnings include semiconductor firm Qualcomm, as well as Teva, Shopify, PayPal, Occidental Petroleum, Equinix, Kraft Heinz, DoorDash, Albemarle, MGM Resorts, Zillow, and Etsy.

Market Snapshot

- S&P 500 futures down 1.0% to 4,554.25

- MXAP down 1.7% to 167.30

- MXAPJ down 2.1% to 528.37

- Nikkei down 2.3% to 32,707.69

- Topix down 1.5% to 2,301.76

- Hang Seng Index down 2.5% to 19,517.38

- Shanghai Composite down 0.9% to 3,261.69

- Sensex down 1.4% to 65,517.16

- Australia S&P/ASX 200 down 1.3% to 7,354.60

- Kospi down 1.9% to 2,616.47

- STOXX Europe 600 down 1.8% to 458.96

- German 10Y yield little changed at 2.52%

- Euro little changed at $1.0986

- Brent Futures up 0.4% to $85.25/bbl

- Gold spot up 0.4% to $1,951.76

- U.S. Dollar Index down 0.16% to 102.14

Top Overnight News

- BOJ deputy governor pushes back on speculation the central bank is planning an early exit from a policy of extreme accommodation (the recent YCC tweak was aimed at making it more sustainable). RTRS

- South Korea’s CPI undershoots the Street (+2.3% vs. the Street +2.4% and down from +2.7% in June) and falls to a 25-month low. RTRS

- SoftBank’s Arm is targeting an IPO at a valuation of between $60 billion and $70 billion as soon as September, people familiar said. Arm execs may still be gunning for $80 billion, but the odds of achieving that are uncertain. BBG

- China will curb the amount of time kids can spend on their smartphones, dealing a potential blow to Tencent, ByteDance and other social media leaders. Minors will be banned from accessing the internet from 10:00 pm to 6:00 am and mobile usage will be cut to two hours for those aged 16 to 18. BBG

- Binance, the world’s largest crypto exchange, was supposed to leave China behind when the country made cryptocurrency trading illegal in 2021. Almost two years later, users traded $90 billion of cryptocurrency-related assets in China in a single month, according to internal figures viewed by The Wall Street Journal and current and former employees. The transactions made China Binance’s biggest market by far, accounting for 20% of volume worldwide, excluding trades made by a subset of very large traders. WSJ

- Fitch cut the US credit rating from AAA to AA (it warned back in May that a downgrade was possible). Fitch’s move follows a similar cut by S&P about 12 years ago. Moody’s continues to rate the US AAA. Fitch says its downgrade “reflects the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance relative to ‘AA’ and ‘AAA’ rated peers over the last two decades that has manifested in repeated debt limit standoffs and last-minute resolutions”. Fitch

- The major entertainment studios and thousands of striking writers have agreed to meet to restart talks after a three-month standoff, according to the writers guild. NYT

- US prosecutors have charged Donald Trump in connection with his attempts to overturn the results of the 2020 election, the second federal indictment brought against the former president in as many months. Trump was charged with four criminal counts including conspiracy to defraud the US, to obstruct an official proceeding and to threaten individual rights, according to an indictment filed in federal court in Washington on Tuesday. FT

- US crude stockpiles saw a jumbo drawdown last week as inventories plunged 15.4 million barrels, the API is said to have reported. That would be the biggest in data going back to 1982 if confirmed by the EIA. BBG

- Foreign buying of U.S. homes fell for a sixth straight year, sinking to the lowest level on record, though some signs of turnaround are starting to emerge. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded lower following the mostly negative lead from Wall St where sentiment was dampened by higher yields and weak data, while participants also digested Fitch’s credit rating downgrade for the US from AAA to AA+. ASX 200 declined with utilities, real estate and financials leading the broad-based retreat and with weaker AIG Manufacturing and Construction data adding to the glum mood. Nikkei 225 underperformed and dipped below the 33,000 level as the focus shifted to corporate earnings and despite comments from BoJ’s Deputy Governor Uchida who stuck to a dovish tone. Hang Seng and Shanghai Comp conformed to the risk aversion albeit with the downside in the mainland initially cushioned by further policy support and jawboning by Chinese agencies.

Top Asian News

- China’s Finance Ministry said it cut value-added tax for small taxpayers, according to Reuters.

- China’s cyberspace regulator drafts guidelines to strengthen the limit around minors’ use of apps, smart terminals and app stores, according to Reuters.

- China said reports that it obstructed G20 discussions in reducing fossil fuels use are inconsistent with facts, while China regrets a failure to reach an agreement and blames geopolitical issues brought up by other countries, according to Reuters.

- BoJ Deputy Governor Uchida said at present, the risk of losing the chance to hit the price target with a premature shift from easy policy is bigger than the risk of being too late in tightening and Japan is now at a phase where it is important to patiently maintain easy policy. Furthermore, Uchida said last week’s decision was a pre-emptive step at continuing monetary easing without disruptions and the BoJ must fine-tune YCC at times and make the policy more flexible. Adds, depending on the speed of the moves, BoJ will step in before the 10yr yield hits 1%.

- BoJ minutes from the June 15th-16th meeting noted members agreed BoJ must maintain current monetary easing to stably and sustainably achieve the price target, while many members said it was appropriate to sustain monetary easing to support changes seen in corporate wages and price-setting behaviour. Furthermore, a few members said a premature policy shift could mean the BoJ will lose the opportunity to achieve the price target.

- Australian Trade Minister says they are hopeful that in the next few days, there will be a positive decision from China re. barley tariffs, if not will restart the WTO process.

European bourses are in the red, Euro Stoxx 50 -1.4%, as sentiment continues to deteriorate from a downbeat Wall St./APAC handover. Sectors are similarly in the red with earnings dominating stock specifics while the Energy sector is the relative outperformer, but still lower, given benchmark action. Stateside, futures are lower as the risk-off trade continues with sizeable attention on Fitch’s action, ES -0.8%; ADP and Quarterly Refunding dominate the calendar ahead intersected by numerous earnings.

Top European News

- The Times’ Shadow MPC voted 8-1 in favour of a 25bps rate hike this month. All members agreed that the Bank should not provide financial markets with guidance about the future path of interest rates due to economic uncertainty.

- ECB’s de Guindos says “Policymakers should focus on preserving bank resilience to strengthen macroprudential stability at a time of economic uncertainty. This would ensure that sufficient capital buffers are available should widespread losses arise”. Overall, the stress test confirms European banks could withstand a severe economic downturn.

FX

- The broader Dollar and index are firmer in the European morning, propped up by the risk aversion seen across the market after Fitch downgraded US, upside levels include the 100 DMA (102.35), yesterday’s high (102.43), then the 50 DMA (102.45).

- The JPY is the current G10 outperformer following three consecutive sessions of losses in the aftermath of the BoJ’s decision last Friday, with potential tailwinds seen from the broader risk-off sentiment across markets.

- Antipodeans are once again the marked laggards amid the broader risk tone, hangover from the RBA hold, and overall bearish Kiwi jobs data overnight, while EUR and GBP are resilient to the Dollar’s strength despite a lack of headlines, data, and broader risk aversion.

- PBoC set USD/CNY mid-point at 7.1368 vs exp. 7.1664 (prev. 7.1283)

Fixed Income

- EGBs are firmer and currently benefiting from traditional haven allure as the broader risk tone continues to deteriorate despite an absence of fresh catalysts.

- Gilts are the sole core benchmark in the red as we near Thursday’s BoE announcement where another 25bp hike is expected though there is around a 35% chance of 50bp priced and 75bp of total tightening implied by February 2023.

- USTs are faring relatively well and giving up some of the marked concession which was built in on Tuesday’s session both before and after the afternoon’s data docket, concession which comes ahead of today’s quarterly refunding announcement; Though, we are above Tuesday’s 110.26+ low by circa. 10 ticks as it stands.

Commodities

- WTI and Brent futures are off best levels but remain modestly firmer intraday, with the downside from risk aversion (after US’ rating downgrade by Fitch) cushioned by the mammoth drawdown in Private Inventories yesterday.

- Over to metals, the risk-off picture is clear. Spot gold and silver are firmer amid heaven flow and despite the stronger Dollar as the former initially battled overnight resistance at USD 1,950/oz but meanders around the level in European hours.

- Base metals are softer across the board as risk aversion and the Greenback hit the industrial metals, 3M LME copper declined from a USD 8,669/t high but maintains status above USD 8,500/t.

- Operations suspended at Ukraine’s Izmail port on Danube, according to Reuters citing sources.

- US Energy Inventory Data (bbls): Crude -15.4mln (exp. -1.4mln), Gasoline -1.7mln (exp. -1.3mln), Distillate -0.5mln (exp. +0.1mln), Cushing -1.8mln

- US Energy Department spokesperson announced the US pulled its offer to buy 6mln bbls of oil for the SPR due to market conditions, while a Bloomberg reporter noted that the Biden administration delayed the replenishment of the SPR after deciding the offers it received were too expensive.

- OPEC+ is unlikely to tweak its current output policy when it meets on Friday, according to multiple OPEC sources cited by Reuters.

- UK Government suspends anti-dumping duty on hot-rolled flat iron, non-alloy or other alloy steel with goods originating in Iran or Russia in some cases.

Geopolitics

- Explosions were reported in Ukraine’s capital of Kyiv and anti-aircraft units were in operation, according to Reuters citing Mayor Klitschko and military officials.

- Russian drones reportedly attacked port and grain storage facilities in Ukraine’s Odesa region which set some of them on fire, according to the regional governor.

- Poland’s Defence Ministry said it is deploying additional troops along the border with Belarus after 2 helicopters violated airspace, according to BNO News.

- Taiwan’s Presidential Office said Vice President Lai will transit in New York and San Francisco, while it noted reports that VP Lai is planning to transit through Washington DC are false. Furthermore, it stated the transit arrangement is based on comfort and safety and should not be an excuse for conflict.

- US and Mongolia reportedly prepare to sign an “open skies” deal which would grant airlines from both countries the right to operate in each other’s countries, according to Reuters sources.

- Russian Kremlin says a call between President Putin and Turkish President Erdogan is taking place now.

- Russia’s Defence Ministry says Russian forces start navy drills in the Baltic sea, according to Ria.

Crypto

- Binance Japan launched crypto services with 34 virtual currencies, according to Nikkei.

- Binance CEO Zhao attempted to shut down the crypto exchange’s US offshoot earlier this year to protect the much larger global exchange amid mounting regulatory scrutiny, according to sources cited by The Information.

US Event Calendar

- 07:00: July MBA Mortgage Applications, prior -1.8%

- 08:15: July ADP Employment Change, est. 190,000, prior 497,000

DB’s Jim Reid concludes the overnight wrap

Just when you thought it was safe to unwind into your holidays, after Europe went to bed last last night, Fitch Ratings downgraded the US from AAA to AA+ in a surprise move reminiscent of S&P’s back in August 2011. The rating agency had initially put the US on ratings watch back in May during the debt ceiling fight. In a corresponding statement, Fitch cited that tax cuts and new spending initiatives coincided with multiple economic shocks to rapidly grow the government’s debt burden. The rating reflects the political brinkmanship reflected in the debt ceiling fights, but also takes into account the forecast debt-to-GDP ratio which Fitch estimates will reach 118% by 2025, with the median AAA rated ratio being 39%. See our rates strategists’ immediate reaction to the decision here with one of the takeaways being that it should continue to help reprice term premium going forward. Obviously S&P being the first to downgrade 12 years ago was far bigger news and has allowed investors to adjust for the most important bond market in the world not being a pure AAA anymore but it’s still a big decision. Treasury yields sold off aggressively yesterday before the announcement due to concerns about the upcoming funding announcement as we’ll see below but have been a bit confused since the announcement as they initially rallied on a global risk-off move and then sold off to be c.1bps higher in Asia.

S&P 500 (-0.46%) and NASDAQ 100 (-0.56%) futures are lower as a result with Asian markets weak. The Hang Seng (-1.97%) is emerging as the biggest underperformer followed by the Nikkei (-1.84%), the KOSPI (-1.40%), the Shanghai Composite (-0.84%) and the CSI (-0.70%).

The downgrade follows an interesting story that has been bubbling under the surface around the US deficit and what that means for issuance and yields. 10yr Treasuries rose +6.4bps yesterday, before the Fitch news, to the highest level since the first half of July and 2s10s steepened +3.9bps in what seemed to be a delayed reaction, in thin markets, to Monday’s surprise announcement from the Treasury of a larger than expected borrowing estimate for the rest of the year. 30yr yields rose +8.2bps to 4.092% and are now at their highest levels since November. Today sees the subsequent refunding announcement at 8:30am EST where we’ll know more about the issuance pattern in the next few months. See our rates strategists’ preview here where they say their expectations have been boosted by Treasury borrowing over the next 5 months that is $500bn more than they originally expected.

I did a CoTD last Monday on the US deficit as it has unexpectedly surged this year. The piece (link here) references US economist Brett Ryan’s piece explaining that most of the deficit increase should be temporary due to delays in tax receipts. Much of California got an extension in filing their tax receipts until October 16th because of severe winter storms. So until we see that we wont really know whether the fiscal impulse has indeed turned notably positive or if, as is our current expectation, its just a timing issue. I am however getting more clients ask me if the US is increasing fiscal spending by stealth. At the moment I don’t think this is the case over and above our forecast from the start of the year, which is for a deficit not that different to last year, albeit still large. A big one to watch.

In terms of data, the lead stories yesterday were the ISM and JOLTS data for July and June respectively, which didn’t dent the soft-landing narrative for the US economy but still hinted at only a gradual reduction in labour market tightness.

The headline ISM manufacturing result did slip in July, with the ISM manufacturing index disappointing at 46.4 (vs 46.9 expected). However, there were encouraging snippets of inflation-related data, including the ISM prices paid which rose less than expected to 42.6 (vs 44.0 expected). Resilience in new orders were likewise evident, rising from 45.6 in June to 47.3, although remaining in contractionary territory. The employment component fell from 48.1 in June to 44.4 though, pushing the index further into contractionary territory.

Additionally, the slight downside surprise in the JOLTS job opening at +9582k (vs +9600k expected) similarly spoke of a more tepid labour market after falling to its lowest level since April 2021. Job openings are still historically high though. Lastly, the quits rate dropped down two-tenths to 2.4%, after a shock increase to 2.6% in the May release. The closely followed private quits rate also fell two tenths to 2.7% again reversing a surprise increase the month before. Another suite of labour market data is due today, with the release of ADP private-sector jobs for July ahead of payrolls on Friday.

However, with a lot of data between now and November, and Fedspeak emphasising data dependency, markets didn’t move much at the front end after the numbers with the long end buffeted instead by the supply outlook. Investors are pricing a nearly 1 in 5 chance of a 25bp rate hike at either of the next two Fed meetings. Yesterday, the balance shifted slightly to put slightly more weight on November, with the expected terminal rate at the end of the meeting expected to be 5.414%.

Across the Atlantic, the German labour market also remained tight, with the July unemployment rate falling to 5.6% from 5.7% in June (vs 5.7% expected), and unemployment claims decreasing -4k (vs +20k expected). The overall Eurozone unemployment rate fell from 6.5% to 6.4% (vs 6.5 expected). The better-than-expected results spoke to a still robust labour market, and with the ECB now data dependent, European overnight index swaps priced in nearly a 62% chance of another 25bps hike by year-end, up slightly from the previous session. Against this backdrop, 10yr bunds sold off, as yields rose +6.5bps. Over the channel in the UK, gilts underperformed, as 10yr yields rose +9.0bps ahead of the BoE meeting on Thursday notwithstanding weak economic data including the UK Lloyds business barometer, which fell from 37 to 31. Basically it was a day of rising western global bond yields.

Turning our attention away from fixed income to equities, the S&P 500 broke its two-day streak of gains to finish down -0.27% following mixed company earnings and possibly the weaker ISM. At the industry level, autos (-1.9%), telecoms (-1.4%), utilities (-1.3%) and consumer discretionary (-1.0%) all lagged. The latter was impacted by Uber (-5.68%) missing on Q2 revenue expectations. On the flipside, capital goods outperformed, up +0.6% following strong Q2 earnings by lead American construction company Caterpillar (+8.85%). The NASDAQ underperformed, falling back -0.43%. After the US close semiconductor producer AMD (up +2.7% in after-market trading) beat earnings expectations and described the PC chip market as having mostly recovered with customers having worked through excess inventory. The company expects to hit their initial full year guidance on surging AI demand. In Europe, the STOXX 600 earlier slipped, down -0.89%, after negative Q2 updates and cautious forward outlooks from top European firms such as BMW (-5.39%), DHL Group (-4.87%) and Daimler (-2.40%).

In terms of other notable data releases, we had the Dallas Fed Services Activity, which posted at -4.2, an increase from -8.2 in June. The final US manufacturing PMI result for July was unchanged from the flash result, at 49.0, increasing from 46.3 prior. Finally, the final euro area PMI manufacturing result for July was unchanged at 42.7.

Early morning data today showed that South Korea’s consumer price growth slowed for the sixth consecutive month, rising +2.3% y/y in July (v/s +2.4% expected) on the back of lower oil prices. It followed a +2.7% increase in June, and marks the lowest advance since June 2021.

After a data heavy day yesterday, we have only the US July ADP report as the major data release to look forward to today. But watch out for the refunding announcement. Key company earnings include semiconductor firm Qualcomm, as well as Teva, Shopify, PayPal, Occidental Petroleum, Equinix, Kraft Heinz, DoorDash, Albemarle, MGM Resorts, Zillow, and Etsy.