US stocks were set to snap a six-day rally on Tuesday as traders reassessed expectations of Fed interest-rate policy after hawkish comments Monday by Minneapolis Fed President Neel Kashkari dampened hopes of speedy interest rate cuts from the US central bank. Kashkari is back today for round two; Indeed, traders appear to be awaiting more from Fed officials on the rate path outlook following Kashkari’s comments, with Fed Chair Jerome Powell also set to speak later in the week, but first we have to get through today’s calendar:

- 07:30: Kashkari

- 08:00: Goolsbee

- 09:15: Barr

- 09:50: Schmid

- 10:00: Waller

- 12:00: Williams

- 13:25: Logan

As of 7:50am, S&P 500 futures are down 0.3% to 4372 with Nasdaq futures dropping by the same amount, while Europe’s Stoxx 600 index posted a similar loss.

Commodities ex-base metals/natgas are weaker while WTI slides under $80 for the first time in 2 months despite a war raging in the middle east. Today’s Macro data is primarily focused on consumer credit, the 7 Fed speakers, and the 3Y auction at 1pm. MegaCap Tech names are weaker premarket; here are some of the most notable premarket movers:

- Alteryx shares rise 17% after the software company reported better-than-expected results, providing relief following last quarter’s disappointing revenue forecast. Analysts said that the firm’s execution improved, showing some resilience against a tough backdrop and prompting some price target hikes.

- Coherus Bio shares tumble 18% as the biotech company cut its net product revenue and combined R&D and SG&A expenses forecast for the full year.

- DigitalOcean Holdings shares gain 8.2% as Goldman Sachs double-upgrades its rating on the cloud computing firm to buy, saying in note that cyclical risks appear to be priced in.

- Hims & Hers Health shares jump 7.0% after reporting third-quarter revenue that beat estimates and boosting its adjusted Ebitda guidance for the full year ahead of expectations. Analysts saw the results as strong, highlighting the execution of management.

- RingCentral shares rise 9.7% after the communications software provider narrowed its software subscription revenue guidance for the full year and reported what analysts said was a strong set of results, boosting hopes of further growth.

- TransMedics Group shares climb 37% after the organ transplant company boosted its sales forecast for the full year. The health-care firm also reported third-quarter revenue that exceeded the average analyst estimates.

- TripAdvisor shares jump 11% after the online travel company reported third-quarter adjusted earnings per share and revenue that came ahead of estimates. Analysts said the results were better than expected, highlighting the performance of TripAdvisor Core and Viator.

- Ventyx Biosciences shares drop 73%, set for a record fall, after the biotech said it’s terminating its Phase 2 trial of VTX958 in plaque psoriasis and psoriatic arthritis as efficacy results did not meet the internal target to support further development. The update prompted a downgrade from Wells Fargo, with the broker saying that its thesis on the stock is “busted.”

- Vimeo shares rise as much as 14% in premarket trading after the video software company reported better-than-expected 3Q revenue and boosted its adjusted Ebitda guidance for the full year

- Clover Health shares fall as much as 19% in premarket trading on Tuesday after reporting third quarter revenue that missed the average analyst estimate.

Kashkari, speaking in an interview on Fox News on Monday, said it’s too soon to declare victory over inflation. He added that while there have been three months of promising data on inflation, it isn’t enough.

“The Kashkari comment has injected a sense of reality back into the market, which had got carried away thinking that policy easing was just around the corner,” said Stuart Cole, head macro economist at brokerage Equiti Capital.

Meanwhile, bond markets rallied, led by the UK, as Bank of England Chief Economist Huw Pill hinted rate cuts may be on the table by the middle of 2024 and German industrial output figures suggested that recession isn’t far off. Two-year gilt yields fell 10 basis points to 4.6% and the rate on 10-year Treasuries slid five basis points to 4.59%.

European stocks are lower, with the Stoxx 600 falling 0.2%. Among individual stock movers, oil producers dragged down European equity benchmarks, with Shell Plc and BP Plc sliding more than 1%. UBS gained as much as 5%, most in two months, as the Swiss bank’s third-quarter results were “messy” yet better than expected as expenses were lower, according to analysts. Here are some of the other notable European movers:

- Engie shares gain as much as 2.4% after the French utility company raised its full-year guidance and reaffirmed its dividend policy. Morgan Stanley sees 7% upside to current consensus estimates for 2023 net income

- Associated British Foods shares rise as much as 7%, reaching the highest since July 2021, after reporting full-year adjusted operating profit that beat estimates and announcing an additional £500 million buyback

- NatWest Group rises as much as 2.3% and is among the biggest gainers on the Stoxx 600 banks index on Tuesday after BNP Paribas Exane double-upgrades its rating on the UK lender to outperform from underperform

- Nexi shares jump as much as 4.4% on Tuesday after newspaper MF reported the Canada Pension Plan and Francisco Partners are among firms that may be interested in the payments company. It didn’t say where it obtained the information

- Watches of Switzerland shares jump as much as 15%, the biggest intraday gain since Sept. 25, after the luxury watch retailer reported second-quarter results that analysts said showed resilience in a tough macroeconomic environment

- Poste Italiane shares gain as much as 2.3%, the most intraday since Oct. 10, after the company boosted its full-year Ebit guidance and released what Morgan Stanley called a strong set of third-quarter results

- Daimler Truck shares fall as much as 4.8% to their lowest intraday since June after the German commercial vehicle maker’s third-quarter Ebit showed the impact of supply-chain bottlenecks and missed estimates, says Citi

- Demant shares drop as much as 8.7%, the most in a year and dragging peer GN Store Nord lower, after the Danish hearing-aid maker reported third-quarter sales that missed expectations and narrowed its organic revenue forecast for the year

- RS Group shares fall as much as 19% after a tough first half as weakness in electronics weighs on the industrial and electronic products distributor sales, according to analysts

- OCI slumps as much as 5.8% after the Dutch fertilizer maker’s third-quarter results saw a big miss on adjusted Ebitda. There could be double-digit downgrades to full-year Ebitda numbers, Morgan Stanley says

- The Restaurant Group shares fall as much as 3.3% after Wheel Topco, the owner of Pizza Express, said it won’t make an offer for the owner of Wagamama due to “market conditions”

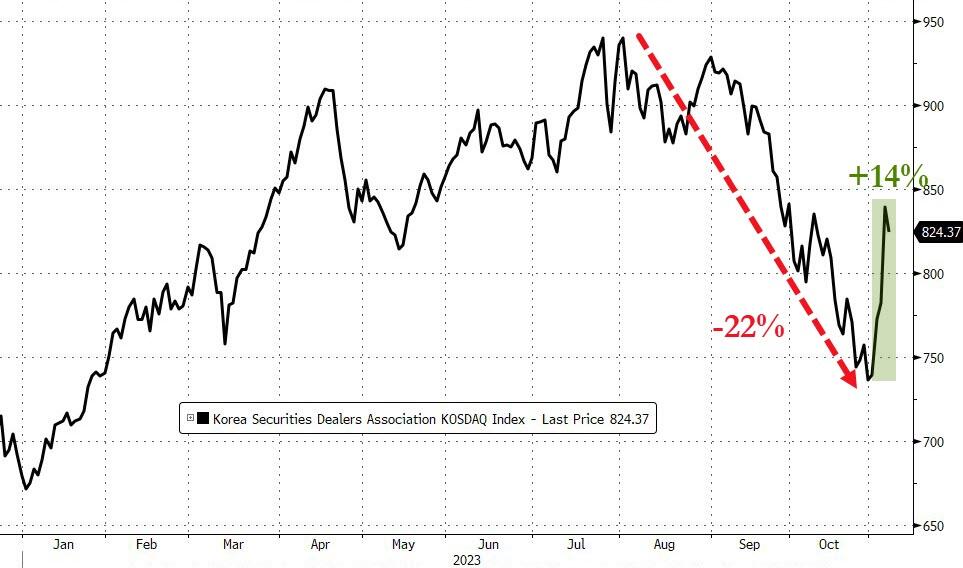

Earlier in the session, Asian equities declined, halting their best four-day advance since November 2022, with Chinese and Korean stocks leading the selloff in the region: South Korea’s Kospi Index lost 2.3% after Monday’s rally that was triggered by a short-selling ban, while Australia resumed policy tightening and raised its inflation forecast, a sign that central banks are not necessarily done hiking interest rates.

The MSCI Asia Pacific Index fell as much as 1.3%, its biggest drop since Oct. 26, with POSCO, Alibaba and AIA Group among the top laggards. Korean stocks were headed for their worst day in more than a year on profit-taking after a ban on short-selling triggered their biggest rally since March 2020 on Monday. Chinese shares also declined after data showed that exports unexpectedly deepened in October, underscoring the country’s fragile economic recovery. A gauge of technology stocks in Hong Kong fell the most in a week.

- Hang Seng and Shanghai Comp opened lower amid the broader market mood. Muted price action was seen after the narrower-than-expected October Chinese Trade Balance, although imports saw surprise growth, while China Vanke’s shares firmed after state shareholders showed signs of providing liquidity support.

- Australia’s ASX 200 saw its downside led by Financials, Energy, and Materials, although the index clambered off worst levels following the RBA’s dovish hike.

- Japan’s Nikkei 225 fell back under 32,500 as the index conforms to the losses across the region.

- Indian stocks ended a three-day rally to end flat amid declines in Asia and European markets. The S&P BSE Sensex settled at 64,942.40, erasing an intraday loss off 0.5%. The NSE Nifty 50 Index also ended flat at 19,406.70. The MSCI Asia Pacific Index slid as much as 1.4%, ending a four-day winning run that was the longest since October 12.

Asian equities started November with gains after three successive months of decline over hopes that the higher-for-longer interest rates narrative may be fading. Still, sentiment has slightly soured amid fresh doubts over the Fed’s policy path and as Australia resumed its interest rate hikes after stronger than expected inflation data. “Following the stellar rallies across the region yesterday, indexes are giving back some of their gains, with a recovery in bond yields and a firmer US dollar to start the week,” said Jun Rong Yeap, market analyst at IG Asia Pte.

In FX the Bloomberg Dollar Spot Index is up 0.2%. The Aussie is the weakest of the G-10 currencies, falling 1% versus the greenback after the RBA signaled a higher hurdle to further policy tightening.

In rates, Treasuries rose along with the dollar, ahead of a flurry of Fed speakers later on Tuesday and following wider gains across European rates. 10Y TSY are trading at 4.625% down 2bps from yesterday’s close. Gilts in particular underwent a sharp bull-steepening after Bank of England chief economist Huw Pill said there will be a “sharp further fall” in inflation for October and hinted that interest rates could be cut by the middle of next year. Adding to the upward pressure on UK bonds, market research firm Kantar reported UK grocery price inflation slowed to single digits for the first time in 16 months. UK two-year yields fall 10bps to 4.62%.

The US session includes at least seven Fed officials scheduled to speak and $48b 3-year note sale at 1pm New York time. US are yields richer by less than 2bp across the curve with gains led by belly, steepening 5s30s spread by around 1bp on the day; gilts lead gains across core European rates with 2-year sector richer by 10bp on the day into early US session, while in 10-year sector gilts outperform Treasuries by 4.5bp.

In commodities, West Texas Intermediate crude dropped below $80 a barrel for the first time in more than two months. WTI fell 2% to trade near $79.20. Spot gold falls 0.5%.

Looking to the day ahead now, data releases include German industrial production, Euro Area PPI, and the US trade balance for September. From central banks, we’ll hear from the Fed’s Barr, Schmid, Waller, Williams and Logan, along with the ECB’s Nagel. Finally in the political sphere, the King’s speech is taking place in the UK, where the government outlines its legislative agenda for the next parliamentary session. In the US, there are also 2 gubernatorial elections taking place today in Kentucky and Mississippi.

Market Snapshot

- S&P 500 futures down 0.3% to 4,373.00

- MXAP down 1.3% to 157.64

- MXAPJ down 1.2% to 493.63

- Nikkei down 1.3% to 32,271.82

- Topix down 1.2% to 2,332.91

- Hang Seng Index down 1.6% to 17,670.16

- Shanghai Composite little changed at 3,057.27

- Sensex little changed at 64,907.46

- Australia S&P/ASX 200 down 0.3% to 6,977.07

- Kospi down 2.3% to 2,443.96

- STOXX Europe 600 down 0.2% to 442.82

- German 10Y yield little changed at 2.71%

- Euro down 0.2% to $1.0694

- Brent Futures down 2.1% to $83.38/bbl

- Gold spot down 0.5% to $1,967.78

- U.S. Dollar Index up 0.29% to 105.52

Top Overnight News

- RBA hiked rates by 25bp to 4.35% (market expectations were close to 50/50 about whether they would move at this meeting) although the accompanying language evolved in a dovish fashion. RTRS

- China’s exports fall short of expectations in Oct, coming in -6.4% Y/Y (vs. the Street estimate of -3.5%), although imports were a bit better (+3% vs. the Street -5%). RTRS

- Tumbling pork prices could push China back into deflation this week, as the largest listed hog farmers flood the domestic market and complicate Beijing’s efforts to bolster confidence in the world’s second-largest economy. FT

- China steps in to provide support to stressed developer Vanke, with Shenzhen Metro, a state-owned enterprise, vowing to provide full support to the company. WSJ

- German industrial production for Sept comes in cooler than anticipated (-1.4% M/M vs. the Street’s -0.1% forecast). BBG

- The BOE might wait until the middle of next year before cutting interest rates from their current 15-year high, the BoE’s Chief Economist Huw Pill said on Monday. Pill said pricing in financial markets – that currently points to a first rate cut to Bank Rate in August 2024 – “doesn’t seem totally unreasonable, at least to me.” RTRS

- UBS shares climbed as stronger-than-expected client inflows and progress in cost savings overshadowed its first quarterly loss in six years. Sergio Ermotti said Credit Suisse has stabilized though remains structurally unprofitable, while demand for UBS debt is strong. BBG

- The UN reported the reopening of the crossing between Gaza and Egypt. Benjamin Netanyahu said he sees his country having security control over Gaza for an “indefinite period.” BBG

- James Gorman signaled he plans to step down as Morgan Stanley’s chairman by the end of 2024 as he prepares to vacate his CEO post this year. He pushed back on the notion of entering politics, saying, “I don’t like sharks.” BBG

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were softer across the board following the prior day’s gains and the choppy/mixed lead from Wall Street. South Korea’s KOSPI is the notable underperformer – slumping over 2.8% – after surging yesterday on the back of the stock short-selling ban. ASX 200 saw its downside led by Financials, Energy, and Materials, although the index clambered off worst levels following the RBA’s dovish hike. Nikkei 225 fell back under 32,500 as the index conforms to the losses across the region. Hang Seng and Shanghai Comp opened lower amid the broader market mood. Muted price action was seen after the narrower-than-expected October Chinese Trade Balance, although imports saw surprise growth, while China Vanke’s shares firmed after state shareholders showed signs of providing liquidity support.

Top Asian News

- RBA hikes its Cash Rate by 25bps as expected to 4.35% from 4.10%, and tweaked its forward guidance to say “Whether further tightening of monetary policy is required…will depend upon the data” (prev. “Some further tightening of monetary policy may be required”). The RBA also noted inflation in Australia has passed its peak but is still too high and is proving more persistent than expected a few months ago.

- China’s Commerce Ministry has issued new rules to strengthen management of rare earth exports, effective Oct 31 2023 to Oct 31, 2025; issued new rules to strengthen import management of crude oil, iron ore, copper concentrate, potash, according to Reuters.

- PBoC Deputy Governor said he is not too worried about the Chinese economy, and added the overall debt level of the Chinese government is in the mid to lower range by international standards, according to Reuters.

- PBoC injected CNY 353bln via 7-day reverse repos with the rate at 1.80% for a CNY 259bln net daily drain.

- Japan ruling ally Kometo tax chief says should not pre-decide to limit income tax cuts to just a year, according to Reuters.

- South Korean Vice Finance Minister says FX authorities will continue to monitor currency markets as done now even after rule changes in licenses, according to Reuters.

- IMF upgrades China’s GDP Growth forecasts: 2023 5.4% (prev. 5%), 2024 4.6% (prev. 4.2%); follows strong Q3 and growth policies.

European bourses are in the red, Euro Stoxx 50 -0.2%, but have been fairly contained throughout the morning with specific catalysts light and the tone thus far largely emanating from APAC pressure. Sectors are mixed with outperformance in Retail names post-AB Foods while Banks derive support from UBS despite yield pressure; in M&A Telefonica’s offer to purchase the remainder of Telefonica Deutschland has led to gains of circa. 40% for the German telecom name. Stateside, futures are in the red printing broad-based losses in a continuation of Monday’s/APAC risk tone, ES -0.2%, docket today features notable data incl. Manheim and numerous Fed speakers before a handful of earnings.

Top European News

- ECB’s de Guindos says low growth or economic standstill is expected to carry on into Q4 for the Eurozone.

- Telefonica Seeks 28% in German Unit for About €2 Billion

- UBS Seeks to Get Rid of $5 Billion in Rich Clients’ Assets

- Sunak Aims to Trap Labour With Election-Geared King’s Speech

- Aldi and Lidl Are Now Just as Middle Class as Other UK Grocers

FX

- Aussie retreats as risk aversion and less hawkish RBA guidance outweigh the widely anticipated 25bp hike, AUD/USD closer to 0.6400 than 0.6500, AUD/NZD cross sub-1.0850 from just under 1.0900.

- Buck maintains recovery momentum almost across the board as DXY climbs to 105.63 from a 105.25 low awaiting US trade data and a slew of Fed speakers.

- Euro losing grip of 1.0700 handle, Pound probes 1.2300 and Yen back below 150.00 all over again.

- Loonie undermined by a slide in oil ahead of Canadian trade with USD/CAD closer towards the top of 1.3755-1.3691 range.

- PBoC set USD/CNY mid-point at 7.1776 vs exp. 7.2854 (prev. 7.1780)

- BCB Minutes: It was decided to maintain the recent communication, which already includes the appropriate conditionality in an uncertain environment; rate cuts of 50bps are appropriate to keep the necessary contractionary monetary policy for the disinflationary process.

Fixed Income

- Debt futures resurgent after further retracement and curves revert to a flatter trajectory ahead of US refunding.

- Bunds bounce from 129.35 to 130.20 and Gilts from 94.47 to 95.42 in the wake of solid demand for 2034 UK issuance.

- T-note back on 108-00 handle within 107-19+/108-03+ range.

Commodities

- Crude benchmarks remain under pressure after slipping during APAC trade in-fitting with the broader risk tone and have been unable to stage any form of recovery this morning, despite equity performance being much more contained in comparison.

- WTI Dec’23 and Brent Jan’23 lose the USD 80/bbl and USD 84/bbl handles respectively, an action which pushes the benchmarks to multi-month lows with support seen around USD 78/bbl mark in WTI from late-August.

- Metals feature marked pressure in spot gold with the stronger USD offsetting any potential haven demand that may typically have been expected from the current tone, a tone which is weighing on base metal peers.

- US DoE announced a supplemental solicitation for up to 3mln barrels of oil for delivery in January 2024 for US Strategic Reserve.

- OPEC Secretary General says oil demand continues to rise significantly; Oil demand to grow more than 2mln BPD in 2024.

Geopolitics

- Israeli PM Netanyahu says Israel is open to “short pauses” in Gaza, but ruled out a ceasefire, according to Bloomberg.

- The Biden administration is reportedly planning a USD 320mln transfer of precision bombs for Israel, according to WSJ.

- Russian Defence Ministry says Russia destroyed 17 Ukraine-launched drones over Russian territory, according to RIA.

US Event Calendar

- 08:30: Sept. Trade Balance, est. -$59.8b, prior -$58.3b

- 15:00: Sept. Consumer Credit, est. $9.5b, prior -$15.6b

Central Banks

- 07:30: Fed’s Kashkari Speaks on Bloomberg Television

- 08:00: Fed’s Goolsbee Speaks on CNBC

- 09:15: Fed’s Barr Speaks on Financial Technology

- 09:50: Fed’s Schmid Speaks at Dallas/Kansas City Energy Conference

- 10:00: Fed’s Waller Speaks at St. Louis Fed Conference

- 12:00: Fed’s Williams Moderates Discussion in New York

- 13:25: Fed’s Logan Participates in Moderated Discussion

DB’s Jim Reid concludes the overnight wrap

Just when you thought it was safe to go back into the water and hoover up every bond in sight, yesterday saw yields do yet another 180 degree turn, something we’ve been used to seeing in recent weeks, even if last three days of last week was one way traffic. 2yr US yields led the way (+9.6bps). T he S&P 500 managed to eke out a narrow gain (+0.18%) but US small caps (Russell 2000 -1.29%) suffered again with higher rates.

Diving in, the bond selloff perhaps came as investors began to wonder if last week’s narrative about rate cuts was overdone. For instance, market pricing for the Fed now implies a 16% chance of another rate hike, up from 11% on Friday. Moreover, the rate priced in by the December 2024 meeting was up +12.4bps to 4.47%. So there was a clear, albeit partial unwinding of last week’s moves. After the market close, we heard from Minneapolis Fed Kashkari, one of the more hawkish FOMC voices, who said that “we need to let the data keep coming to us to see if we really have got the inflation genie back in the bottle”. So some pushback against declaring victory over inflation.

For markets, this is hardly the first time we’ve seen expectations of a dovish pivot, and Henry pointed out yesterday (link here) that this is at least the 7th time this cycle where markets have reacted notably in response to dovish speculation. Clearly rates aren’t going to keep going up forever, but on the previous 6 occasions we saw hopes for near-term rate cuts dashed every time. Note that we’ve still got above-target inflation in every G7 country. With that in mind, next week’s US CPI release will be an important factor on that front, and our US economists expect core CPI to remain at +0.3% for a third consecutive month .

In the latter half of the US session, we got the latest Senior Loan Officer Opinion Survey (SLOOS) from the Fed, which looks at bank lending standards and has traditionally been a strong leading indicator for the economy more broadly. This showed some improvement in banks’ willingness to lend compared to the previous quarter’s lows, with the net balance of banks reporting tighter lending standards falling from 50.8 to 33.9 for commercial & industrial loans and from 71.7 to 64.9 for CRE loans. However, more banks reported tightening standards for mortgages, up from 13.8 to 16.0. So the general SLOOS improvement is welcome but most measures are still at levels usually associated with recessions. Can the SLOOS improve quickly enough over the next 2-3 quarters before the current tight lending standards cause an accident or a serious growth slowdown. We likely have a race against time.

In terms of the actual moves for bonds, 10yr Treasury yields ended the day up +7.1bps to 4.64%. Real yields drove the increase, with the 10yr real yield up +5.2bps to 2.23%, following its biggest weekly decline of 2023 so far last week. The sell-off was stronger at the front-end, with 2yr yields up +9.6bps to 4.94%. $24bn worth of corporate bond deals getting priced on Monday may have added upward pressure on yields. It’s worth highlighting that although the QRA was more positive last week, supply and QT is a regular part of life now and today kicks off a 3-day Treasury auction schedule with 3yr notes today, 10yr tomorrow and 30yr bonds on Thursday. So markets will still have to price these to sell over the coming months.

Meanwhile in Europe, the rises in yields were also significant, with those on 10yr bunds (+9.3bps), OATs (+10.2bps) and BTPs (+13.3bps) all moving higher. Indeed, for BTPs it was the joint largest daily rise in yields since July 6. However the front end rise was more contained with German, French and Italian 2yr yields up +3.9 bps, +3.2bps and +9.1bps respectively .

The bond moves were an obvious headwind to equities, but the S&P 500 (+0.18%) still managed to build on last week’s advance, with a 6th consecutive gain for the first time since June. However, this advance was a narrow one with only 31% of the S&P constituents up on the day. The biggest driver were tech mega caps, with the Magnificent Seven index up +0.87%, and the NASDAQ (+0.30%) rising for a 7th consecutive session for the first time since January. On the other hand, small-caps put in a very weak performance, with the Russell 2000 (-1.29%) losing ground after recording its strongest week since February 2021. As with bonds, the picture was a bit weaker in Europe, with losses for the STOXX 600 (-0.16%), the DAX (-0.35%) and the CAC 40 (-0.48%).

Asian equity markets have turned negative this morning following the softer markets yesterday. As I check my screens, the KOSPI (-3.07%) is sliding hard after posting its best session yesterday (+6.43%) since late March 2020 following the renewed ban on short selling over the weekend. Elsewhere, the Hang Seng (-1.50%), the Nikkei (-1.12%), the CSI (-0.68%) and the Shanghai Composite (-0.35%) are also retreating. Meanwhile, the S&P/ASX 200 (-0.15%) is also trading lower after the RBA increased its key interest rate by 25bps as expected (more on this below). S&P 500 (-0.21%) and NASDAQ 100 (-0.15%) futures are ticking lower. Treasury yields have fallen 0 to -1.5bps across the curve, led by the front end.

The latest trade data from China showed that exports declined for a 6th consecutive month, dropping -6.4% y/y, worse than Bloomberg’s estimate of a -3.5% drop and against a -6.2% drop in September. Imports surprisingly rebounded +3.0% y/y in October (v/s -5.0% expected) after a revised -6.3% drop the previous month. The resulting trade surplus amounted to $56.53 billion (v/s $82.0 billion expected).

Elsewhere, the RBA lifted its cash rate for the first time in five months (+25bps) to a 12-year high of 4.35% citing a slower-than-expected decline in inflation while still indicating that inflation would return to its target range of 2% to 3% in a reasonable timeframe. The Aussie dollar (-0.79%) dropped against the US dollar in response to the rate hike as the central bank’s statement failed to confirm the possibility of another hike in this cycle. Policy sensitive 3yr government bond yields fell -3.1 bps to 4.24% before slightly recovering, standing at 4.25% as I type.

Looking at yesterday’s data, there wasn’t too much but we did get some of the final PMI readings from Europe, where the main headlines were in line with the flash prints from a couple of weeks ago. For instance, the final Euro Area composite PMI was exactly in line with the flash reading at 47.8, and in Germany it was revised by only -0.1pts to 45.8. One source of concern was Italy, where the composite PMI fell -2.0pts to 47.0, its lowest in 12 months. Otherwise, the latest reading on German factory orders for September showed a +0.2% expansion (vs. -1.5% expected), but with this upside offset by a major downward revision to the previous month (+1.9% vs +3.9% previously). This still leaves German factory orders down -4.3% year-on-year.

To the day ahead now, and data releases include German industrial production, Euro Area PPI, and the US trade balance for September. From central banks, we’ll hear from the Fed’s Barr, Schmid, Waller, Williams and Logan, along with the ECB’s Nagel. Finally in the political sphere, the King’s speech is taking place in the UK, where the government outlines its legislative agenda for the next parliamentary session. In the US, there are also 2 gubernatorial elections taking place today in Kentucky and Mississippi.