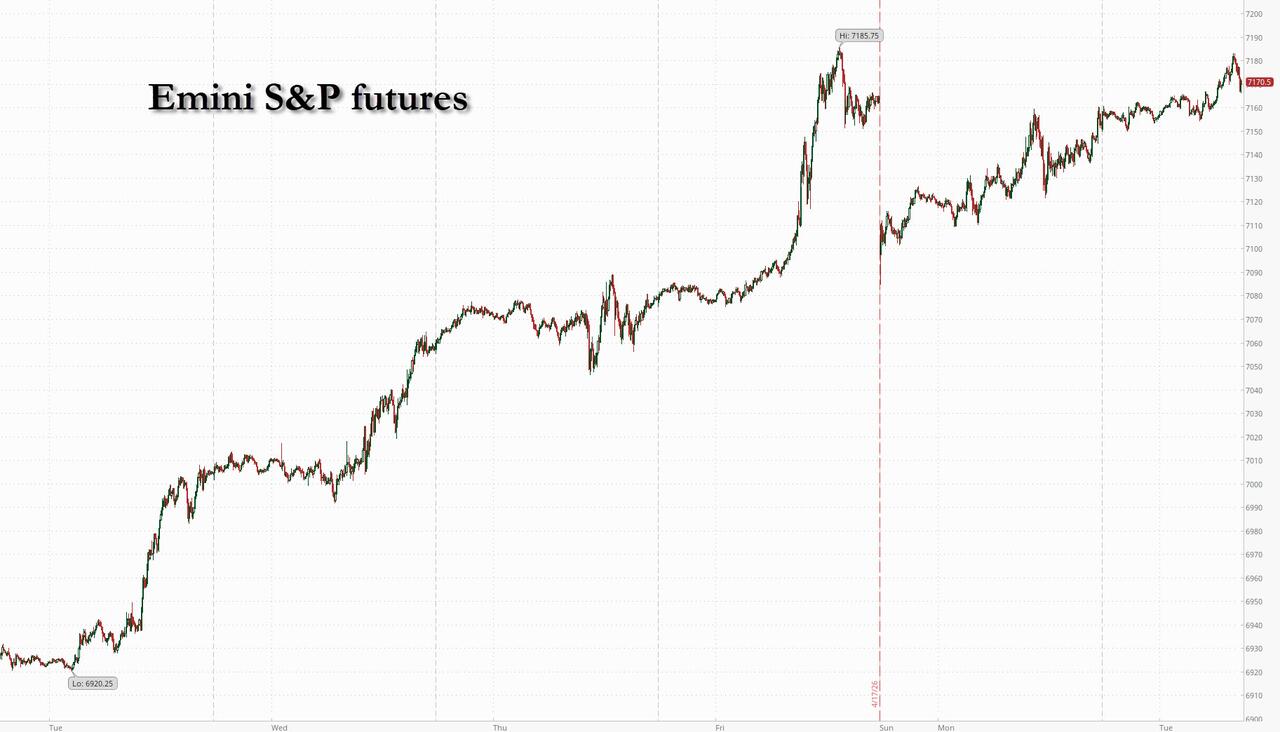

The optimism that helped list the S&P on 11 of the prior 12 days, and the Nasdaq on 13 consecutive days until Monday’s modest pullback, is back – because one can apparently draw the same exact event for 3 weeks now – and sending US equity futures higher again on signs that Iran will attend talks with the US, while the US president said it’s “highly unlikely” that he’d extend the truce. As of 8:00am, S&P 500 futures rose 0.4%, rebounding from Monday’s decline, and supposed by solid earnings, the AI narrative and positioning even as the situation in the Middle East remains unresolved. Nasdaq 100 futures rose 0.5% with most Mag 7 names higher: AMZN +2.8%, META +0.6%, AAPL -0.4%. Apple announced its new CEO after yesterday’s close (hardware chief John Ternus will become the CEO effective September 1st); AMZN announced it will invest another $25bn in Anthropic with Anthropic committing to spending more than $100bn over the next 10yr on AWS. 10Y yields added 1bps to 4.26%. Commodities are mostly lower: Copper -0.5%, Silver -1.0%, WTI crude was flat at $87.60 per barrel, reversing a modest loss. Retail sales and Warsh’s confirmation hearing will be in focus later.

In premarket trading, Mag 7 stocks are mostly higher after the iPhone maker said hardware chief John Ternus will be its next CEO, with current leader Tim Cook moving to the role of executive chairman. AMZN rises 3% after the cloud-computing and e-commerce giant said it is investing an additional $5 billion in Anthropic and may inject $20 billion more over time (META +0.5%, Tesla (TSLA) +0.7%, Microsoft (MSFT) +0.3%, Alphabet (GOOGL) +0.4%, Nvidia (NVDA) +0.2%).

- 3M Co. (MMM) slips 2% after the maker of Post-it notes, protective equipment and auto maintenance products reported adjusted organic growth that missed estimates.

- Amazon suppliers rise on Amazon’s investment in Anthropic. Marvell Technology (MRVL) +2%, Credo Technology (CRDO) +5% and Astera Labs (ALAB) +8%.

- Alaska Air (ALK) slips 1.2% after the carrier announced it will be suspending full-year guidance due to higher fuel costs. The company also expects a higher adjusted loss-per-share in the second quarter than what Wall Street is estimating.

- Avis Budget (CAR) rises 7% and is set to extend its short squeeze for a fourth consecutive session.

- Tractor Supply (TSCO) falls 5% after the retailer reported comparable sales for the first quarter that missed the average analyst estimate.

- UnitedHealth (UNH) climbs 7% after reporting first quarter profit that blew past Wall Street expectations. The company also boosted its outlook for the year, a sign of the health conglomerate’s progress toward rebuilding credibility with investors after a collapse a year ago.

In corporate news, Apple CEO Tim Cook will hand the reins to hardware boss John Ternus later this year. Ternus will face challenges even as he maintains Apple’s device empire — needing to take chances, enter new product categories and find the company’s footing in AI. Elsewhere in tech, Amazon is investing an additional $5 billion in Anthropic and may inject $20 billion more over time, a deal that strengthens ties in in an increasingly competitive AI race. The deal was struck at a valuation of $350 billion, not including the new funding, Anthropic said.

Sentiment rose overnight even though Trump signaled that a ceasefire extension is unlikely, while Iran hasn’t confirmed who, if anyone, will travel to the Pakistani capital for peace talks. Strategists continue to look outside of geopolitics, with JPMorgan’s Dubravko Lakos-Bujas raising his year-end S&P 500 price target to 7,600 on the back of strong tech and AI earnings. But for Kristina Hooper, chief market strategist at Man Group, the market is showing signs of “irrational exuberance 2.0,” with the strength of the recent equity rally defying logic and largely based on the belief in a “POTUS Put.”

The US is waiting to see if Iran will take part in a second round of ceasefire talks before the truce expires on Wednesday. President Donald Trump said his vice president, JD Vance, was ready to leave for negotiations in Pakistan. Tehran has yet to confirm its attendance.

Speaking to Bloomberg News in a phone interview on Monday, Trump said he would not be “rushed into making a bad deal” and that the US naval blockade on Iranian ports would stay in place until an agreement is reached. Additionally, the president said a ceasefire extension beyond late Wednesday was unlikely.

“Traders will understandably be focused on events in Pakistan, with talks expected to resume ahead of tomorrow’s deadline,” said Joshua Mahony, chief market analyst at Scope Markets.

Solid early earnings are also helping. The Citi US earnings revisions index has moved back into positive territory after two negative weekly prints. Of the 49 S&P 500 companies to have reported so far, 80% have beaten analysts’ forecasts, while 12% have missed.

The Federal Reserve’s future is also on the minds of traders, as Kevin Warsh for his confirmation hearing. Warsh is Trump’s pick to replace the central bank’s current chair, Jerome Powell. It could be one of the most contentious such hearings in many decades. Warsh, in prepared remarks, vowed to protect the Fed’s independence if he were confirmed to the role.

“We think that the appointment of Kevin Warsh is unlikely to significantly adjust the balance of the Federal Open Market Committee – or, in any case, not to the extent that it would lead to any non-key rate cuts that are not justified by the US economic situation and the institution’s mandate,” CIC economists including Adrien Régnier-Laurent wrote in a note.

Earnings season rolled on, with UnitedHealth Group Inc. jumping 7.4% during premarket trading after the health insurer boosted its profit forecast. General Electric Co. gained 1.3% after the jet-engine manufacturer’s first-quarter profit came ahead of Wall Street’s expectations.

Europe’s The Stoxx 600 is higher by 0.3% with IT near the top of the leaderboard. Insurance and utilities outperformed, while food and beverage names fell, led by Royal Unibrew which said its partnership deal with PepsiCo in several nations will expire at the end of 2028. Here are some of the biggest movers on Tuesday:

- British Land shares rise as much as 3.7% as the commercial property group upgrades earnings guidance.

- BF shares rise as much as 12% to a record high after the Italian agriculture services company received a voluntary takeover offer from Arum and Dompè Holding at a significant premium to Monday’s close.

- THG shares rise as much as 9.8% after the online retailer said it delivered its best 1Q revenue growth since 2021, as both the Beauty and Nutrition arms reported positive topline momentum.

- J D Wetherspoon gains as much as 5.9% as Peel Hunt upgrades to add from hold following recent share-price weakness, noting the pub operator has been trading at an EV/Ebitda close to all-time lows.

- Beiersdorf falls as much as 3.6% after the German personal care products group and Nivea owner reported first-quarter earnings which fell short of expectations.

- AB Foods shares drop as much as 7.1%, the most since January, after the company downgraded expectations for its Sugar business and said its clothing arm Primark experienced softer trading in April as the Middle East conflict hit consumer confidence.

- Royal Unibrew shares plunge as much as 23% after the Danish brewer said its partnership with PepsiCo in Denmark, Finland and the Baltic states will end when the current license agreements expire at the end of 2028.

- Crest Nicholson shares tumble as much as 45% to a record low as the UK homebuilder cuts full-year earnings guidance due to economic uncertainty and softening land sales that have caused it to prioritize cash preservation.

- Fagerhult falls as much as 20% after the Swedish lights and lighting systems manufacturer said first-quarter earnings would be weaker than it expected due to “continued general market uncertainty, largely related to the geopolitical unrest in the Middle East.”

- Barco drops as much as 10% as the consumer electronics firm warned that its full-year guidance is in doubt if current macro‑economic conditions and geopolitical tensions persist.

- Retail Estates shares decline as much as 5.2% after being downgraded at KBC Securities following its move to enter the French market. Analysts said it makes strategic sense, but warn that financing the expansion will erode earnings per share growth.

- Avanza shares fall as much as 7.8% after the Swedish retail trading platform reported first-quarter results that analysts viewed as disappointing.

Earlier in the session, Asian stocks advanced, as optimism over a potential resumption of negotiations ahead of a looming Middle East ceasefire deadline lifted sentiment. The MSCI Asia Pacific Index rose as much as 0.9% to the highest in seven weeks. Technology megacaps including TSMC and SK Hynix were among the top contributors to the gauge’s gains. South Korea’s Kospi index climbed to a record, powered by chipmakers as the artificial intelligence trade regained momentum. Fresh signals that Iran and the US are continuing to work on a deal to end the war buoyed risk-on sentiment across Asia even though President Donald Trump said he’s unlikely to extend the two-week ceasefire with Iran. Investors are also starting to refocus on fundamentals, reverting to familiar themes such as AI-related trades. The MSCI Asia Pacific Index has lagged the S&P 500 gauge since the war began given the higher exposure of Asian economies to oil imports from the Middle East. Still, the gap has narrowed as markets price in a de-escalation of the conflict. The Asian benchmark has risen 13% so far this year, versus 3.9% jump in its US peer.

In FX, the Bloomberg Dollar index is higher by 0.2% with the greenback higher versus all major peers with the exception of Kiwi dollar, which has been boosted by firmer inflation data.

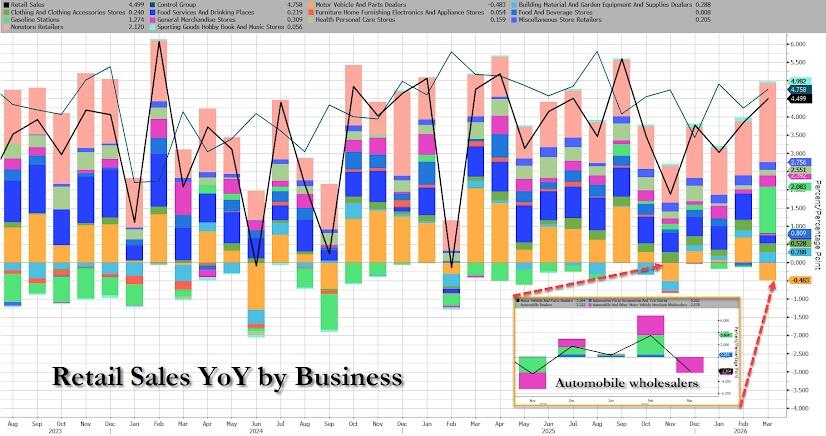

In rates, bonds edged lower into the early US session led by the front-end of the curve where 2-year yields are up almost 2bp on the day but price action has been muted with oil futures edging lower. Treasuries see subtle bear flattening move with long-end yields broadly unchanged on the day and front-end cheaper by around 2bp, tightening 2s10s and 5s30s spreads by 1bp and 1.2bp on the day. US 10-year yields trade around 4.26% with bunds outperforming by 1bp on the sector, gilts trading broadly in line. UK gilts reversed a brief wobble after a top UK official said he felt pressure from the government to approve Peter Mandelson’s appointment. Session focus includes Kevin Warsh scheduled to appear before the Senate Banking Committee, while data includes March retail sales.

In commodities, brent crude futures are down around 0.8% and back below $95/bbl despite US President Trump’s threat to not extend the current truce with Iran. Precious metals are on the backfoot with spot gold and silver down 0.8% and 0.9% respectively.

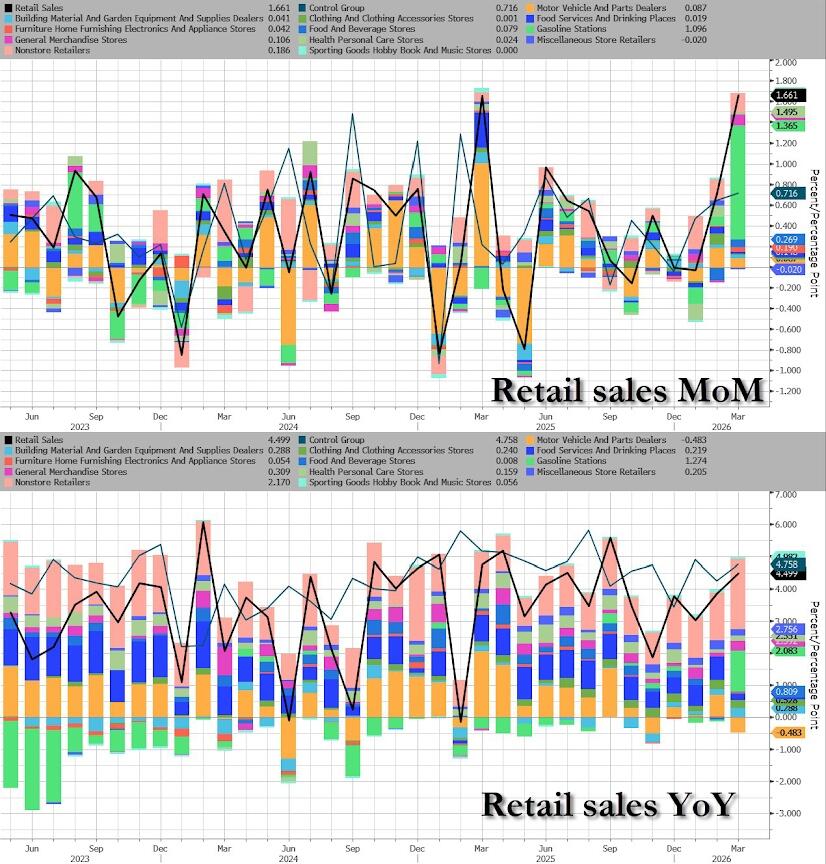

Today’s US economic data calendar slate includes weekly ADP employment change (8:15am), April Philadelphia Fed non-manufacturing activity, March retail sales (8:30am), February business inventories, March pending home sales (10am)

Market Snapshot

- S&P 500 mini +0.2%

- Nasdaq 100 mini +0.3%

- Russell 2000 mini +0.1%

- Stoxx Europe 600 +0.3%

- DAX +0.6%

- CAC 40 +0.2%

- 10-year Treasury yield little changed at 4.25%

- VIX +0.2 points at 19.08

- Bloomberg Dollar Index +0.2% at 1194.04

- euro -0.2% at $1.1759

- WTI crude -1.8% at $88.04/barrel

Top Overnight News

- Iran has yet to confirm its participation in new peace talks, underscoring uncertainty around the negotiations. Donald Trump said he’s “highly unlikely” to extend the truce and JD Vance is expected to travel to Islamabad as soon as tonight. BBG

- In private, Iranian officials say they’re preparing to resume peace talks with the US. In public, however, they are far more wary, even pugnacious at times as they blame the White House for putting diplomacy at risk. NYT

- The United States has expressed confidence that peace talks with Iran will go ahead in Pakistan and a senior Iranian official said Tehran was considering joining, but significant uncertainty remained on Tuesday as the end of a ceasefire loomed. RTRS

- Kevin Warsh heads to Capitol Hill for his Fed chair confirmation hearing, where he’ll face scrutiny from lawmakers. In prepared remarks, he pledged to protect the central bank’s independence and steer clear of “distractions” in policymaking. BBG

- China’s alumina imports surged to a two-year high in March as Middle East disruptions rerouted cargoes, boosting aluminum output and margins. Copper production rose to a record 1.33 million tons. BBG

- Indonesian stocks slid after MSCI extended the review period to June as it assesses the impact of recent regulatory reforms. BBG

- UK businesses stepped up job cuts in March. The number of employees on payrolls fell by 11,000 — the biggest drop since November — in a sign that the Iran war is causing caution in the labor market. BBG

- One of the US’s top insurance regulators has warned that a “transformation” in the sector has pushed insurers into riskier private investments that are “less appropriate” for retirees. FT

- Amazon will invest another $5 billion in Anthropic at a $350 billion valuation, and may inject $20 billion more over time. The startup plans to spend over $100 billion on Amazon’s cloud and chips over the next decade. BBG

Iran War Latest

- No Iranian delegation, primary or secondary, have travelled to Islamabad and that reported about the departure of such officials and claims about meeting times were inaccurate, IRIB reported. The earlier reports by Al Jazeera, citing a Pakistani diplomatic source, suggested that the Iranian preliminary delegation and US delegation are present in Islamabad.

- “A Pakistani official source told Al Arabiya: The US and Iranian delegations will arrive in Islamabad today at the same time”; “The second round of negotiations will be held as scheduled”. “We currently have no information about extending the ceasefire between America and Iran”.

- US VP Vance is to travel to Pakistan on Tuesday for Iran talks, according to sources cited by Axios.

- US-Iran negotiations may begin Wednesday morning in Islamabad, while US is said to believe that there is a split within the Iranian negotiating team, according to Al Arabiya citing CNN network sources.

- Pakistan media sources note expectations US and Iran will reach an agreement by Wednesday, according to Al Arabiya.

- Iranian official tells Washington Post that they have largely agreed on the broad outlines of the agreement, according to Al Arabiya.

- Pakistan asked the US and Iran to extend the truce for two more weeks, while Pakistani media sources say PM Sharif may announce a ceasefire extension on Tuesday, according to Al Arabiya.

- Journalist Elster writes “Pakistani source told Reuters that Trump may attend talks with Iran in person or remotely if an agreement is reached”.

- White House Press Secretary Leavitt said US has never been so close to making a good deal with Iran, adds Trump still has options if there is no deal with Iran.

- Iranian oil tanker entered Iran’s territorial waters, despite the US blockade, with an escort from the Iranian navy, Al-Mayadeen reported.

- Iran’s Judiciary head said it is “very possible” that negotiations will not lead to a result, in that scenario Iran will act again and there will be a response to the US’ interception of a Iranian ship.

- Iran’s Foreign Ministry condemned the seizure of Iranian cargo ship Touska by US forces and called for the “immediate release of the Iranian vessel, its sailors, crew and their families”, according to CNN.

- Iranian Parliament Speaker Ghalibaf said by applying the blockade and violating the ceasefire, Trump wants to turn this negotiation table into a table of surrender or to justify a renewed war. We do not accept negotiations under the shadow of threats, and in the last two weeks, we have prepared to face new cards on the battlefield.

- Israel-Lebanon ceasefire violated, ISNA reported, citing sources.

- Israeli army reportedly withdrew part of its forces south of Lebanon following the start of the ceasefire, according to sources cited by Haaretz.

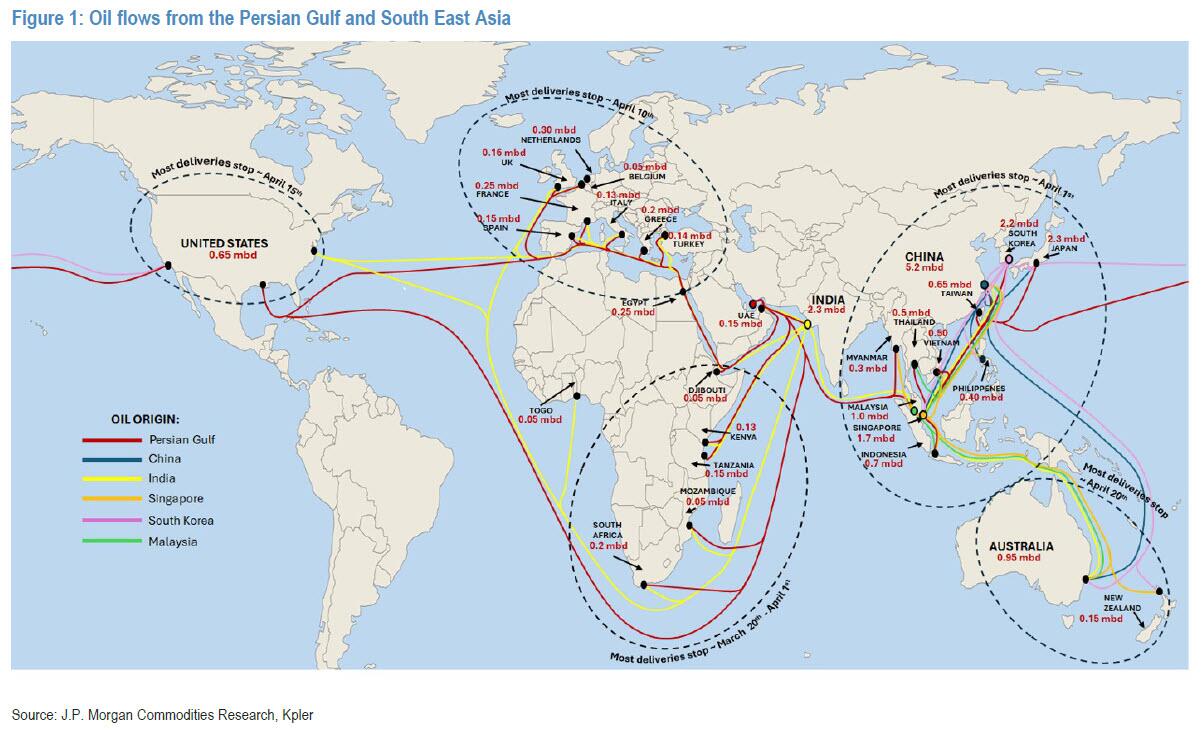

- UN agency is reportedly preparing evacuation plan from Strait of Hormuz for hundreds of ships, Bloomberg reported.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mixed with the region cautious amid uncertainty regarding US-Iran talks ahead of the ceasefire expiry, as there were numerous conflicting reports on when they will occur and if Iran will take part. Nonetheless, the latest relevant headlines provide some optimism, with sources stating that the US and Iran are expected to reach an agreement by Wednesday and that Pakistan’s PM is to ask for a two-week ceasefire extension, while there remains no official confirmation from Tehran about attending talks. ASX 200 trades subdued with the index dragged lower by weakness in health care, energy, mining and financials, while a quarterly production update from Rio Tinto failed to meaningfully inspire. Nikkei 225 rallied to back above the 59,000 level with upside facilitated by tech strength and expectations for the BoJ to refrain from hiking rates at next week’s meeting. Hang Seng and Shanghai Comp were contained amid earnings releases and the mixed performance in the tech sector, while markets failed to benefit from the NDRC head’s pledge that officials will help actively increase effective domestic demand and will further enhance supply chain resilience.

Top Asian News

- New Zealand Inflation Rate QoQ (Q1) Q/Q 0.9% vs. Exp. 0.8% (Prev. 0.6%).

- New Zealand Inflation Rate YoY (Q1) Y/Y 3.1% vs. Exp. 2.9% (Prev. 3.1%, Low. 2.8%, High. 3.1%)

- New Zealand RBNZ Sectoral Factor Model Inflation Index YY (Q1) 2.7% (Prev. 2.8%).

- Taiwan Export Orders (Mar) Y/Y 65.9% vs exp. 44.1% (prev. 23.8%).

European bourses (STOXX 600 +0.2%) are modestly rebounding from Monday’s losses, however the CAC 40 and SMI are failing to bounce. The DAX 40 is the outperformer, with most of the index in the green but cautiously awaiting SAP earnings on Thursday. European sectors are broadly gaining. Technology and Utilities top the pile while Food, Beverage & Tobacco lags as AB Foods weighs on the sector. Despite reaffirming its FY outlook, failure to show revenue growth and the announcement of the demerger of Primark from the food business have hit the Co.’s shares.

Top European News

- Former UK Foreign Ministry Official Olly Robbins said the Cabinet Office suggested Peter Mandelson not be vetted at all; Foreign Office overruled it.

- Former UK Foreign Ministry Official Olly Robbins said there was a “dismissive attitude” from Number Ten towards Mandelson’s vetting as they wanted to get him out to Washington as quickly as possible. Foreign Office was under constant pressure from the PM’s office to get Peter Mandelson cleared to become US ambassador.

- French PM Lecornu has asked ministers to reduce spending by an extra EUR 4bln, AFP reported.

Trade/Tariffs

- USTR Greer tells Mexican firms that auto and steel tariffs will not go down to zero, Reuters reports citing sources.

- USTR Greer met with Mexico’s President Sheinbaum on Monday ahead of North America trade pact review.

- US Trade Representative said US and Mexico are to launch USMCA talks on the week of May 25th and they are to be held in Mexico City.

- US Interior Secretary Bergum said Chinese solar panels are a national security issue.

FX

- Despite elements of risk in other assets, FX displays a risk-off bias today, with all G10 currencies bar NZD lower against the greenback.

- DXY trades higher by 0.2%. Though there is no clear driver, the index bounced off a session low of 98.10, continuing a rebound from Monday’s 98.00. This upside came around news that an Iranian delegation had not departed for Islamabad, contrasting earlier reporting. Technicals also likely at play here, around this news, USD/JPY surpassed the 159.00 mark, crude bounced, but hit resistance at USD 95.00/bbl – explaining why the haven USD and energy benchmarks are not in tandem this morning.

- GBP is weaker against the Buck and EUR, participants are focusing on domestic political updates, geopolitics and a hawkish Labour force survey this morning. On politics, former UK Foreign Ministry Official Robbins essentially denied the PM’s claims of due process in relation to Mandelson’s appointment. This leaves the PM in a somewhat weaker position – and as such, we saw a c. 15pip move in EUR/GBP, which has since paired. The data set for Feb, saw hotter-than-expected wage metrics and a much lower-than-expected unemployment rate. The series will be welcomed by policymakers on Threadneedle/Downing Street, signalling each were in a comfortable position pre-Middle East war & energy shock. ING writes “the details reveal the drop in the jobless rate is pretty much solely down to a rise in “economic inactivity” – that is, people neither in work nor actively seeking it.” MUFG post-data wrote “We are currently forecasting only one rate hike from the BoE.” GBP/USD saw an initial kneejerk higher, which since reversed amid the ongoing Robbins hearing.

- NZD leads the G10 space after the latest inflation data spurred bets for rate hikes. Q1 metrics revealed that inflation surprisingly remained elevated above the RBNZ’s 1-3% target. Markets are back to pricing in 81bps of tightening by year-end, similar to levels seen post-Bremen comments, though more hawkish than Monday.

Central Banks

- BoJ is reportedly set to stay on hold in April but keep a hawkish stance, Bloomberg reports citing sources. This adds to further reports from the Nikkei that the BoJ is to hold rates steady in April and to make a decision in June after assessing the situation in the Middle East.

- BoJ Financial System Report: Japan’s financial system has been maintaining stability on the whole; Japanese banks have sufficient capital bases and stable funding bases to withstand various stress situations.

- ECB’s de Guindos said high market valuations, private credit and fiscal policy are among the financial stability risks; monetary policy must be prudent, should keep a cool head.

- CNB Vice-Governor Zamrazilova tells Czech radio that inflation this year can be expected to be just under 3%.

- BoK’s new Governor Shin said to seek inflation stability and financial stability through cautious and flexible monetary policy operations.

Fixed Income

- Global fixed benchmarks are mixed, with US and UK paper in the red, whilst Bunds remain afloat. Ultimately, focus has been on the volatile geopolitical environment, with attention on developments surrounding US-Iran second round talks. Initially, there were reports via a Pakistani source which suggested that the US-Iran delegation teams had arrived in Islamabad, however, Iranian State TV pushed back on these claims calling them “baseless” – they said that Iran “has not yet sent a delegation”. Markets will await how this unfolds, ahead of the expiration of the US-Iran ceasefire on Wednesday.

- USTs are lower by around 3 ticks and currently within a 111-17 to 111-22+ range. Ultimately moving at the whim of energy price fluctuations, with a recent bout of pressure in the benchmark after the Iranian side pushed back on reports that a delegation had arrived in Pakistan. Geopols aside, US March retail sales are the main focus (exp. 1.4% M/M, prev. 0.6%), alongside the weekly ADP employment change and the Atlanta Fed GDPNow update. Elsewhere, Fed’s Waller is on the docket, though will not touch on monetary policy given the Bank is on blackout; Kevin Warsh’s senate hearing is also due. From a yield perspective, the curve is a touch steeper this morning; the 2yr currently resides around 3.73%. A positive outcome from the second round of talks could see the 2yr breach back below the 3.70% and approach near-term lows at 3.67%.

- Bunds are firmer this morning by around 15 ticks, and currently trade towards the mid-point of a 125.90 to 126.17 range. German paper appears to be benefiting from lower energy prices. On the yield front, the curve is lower across the horizon, but with the long-end underperforming. It seems to be the view of bond traders that the Middle East situation has only near-term implications, with 10yr yield action fairly sideways in the past week or so. On the data front, German ZEW deteriorated from the prior, and beneath the consensus. Not all too surprising given this data encapsulates more of the Iran war. No move in Bunds were seen on the data.

- Gilts are currently trading with losses of around 10 ticks, and hold within a 87.83 to 88.42 range. In recent days, domestic politics has taken a bit of attention away from the Middle East situation. The latest update came from the Former UK Foreign Ministry Official Olly Robbins, who said that the Cabinet Office suggested that Mandelson should not be vetted at all, and this was overruled by the Foreign Office. A comment which does not play in favour of PM Starmer, who has managed to shrug off some of the recent pressure he has faced. A little bit of downside was seen in Gilts at the time, but Robbins’ comments came in close proximity to geopolitical updates, which weighed on the broader complex. On the data front, UK unemployment rate fell to 4.9% (exp. 5.2%, prev. 5.2%); which would be welcomed at the BoE.

Commodities

- Crude futures are softer thus far but have clambered off worst levels over US-Iran uncertainty. More recently, reports out of Iran suggest that no delegation has been sent to Islamabad yet, which contradicts earlier reports by Al Jazeera, citing a Pakistani source, that both the Iranian and US teams are present in Islamabad. Both WTI and Brent briefly topped above USD 87/bbl and USD 95/bbl, respectively, before falling back.

- Other updates include the expectation that US VP Vance arrives in Islamabad on Tuesday for the talks, while President Trump stated that the US blockade will remain in place until a deal is reached.

- Spot gold continues to trade within its ascending channel but has slipped back below the USD 4800/oz handle (current range: USD 4773-4833/oz). The modest upside seen in the dollar, thus far, is weighing on the yellow metal, with the 50-SMA at 4891 also providing a ceiling for the metal. Elsewhere, 3M LME Copper oscillates in a tight USD 13.2k-13.3k/t range amid the mixed risk appetite as markets look to potential US-Iran talks.

- Russia is to pause Kazakhstan’s oil exports to Germany through the Druzhba pipeline starting May 1st, Reuters reports citing industry sources.

- Gunvor Head of Research Lasserre said oil markets are “one month away from tank bottoms”.

- China to lower retail Gasoline and Diesel prices by 555 and 530 CNY/t from April 22nd.

- Kuwait’s force majeure on oil shipments is to have a limited impact on South Korea, according to an official cited by Reuters.

- White House signs memo related to coal supply chains; Trump signs determination related to defence production act on domestic petroleum production.

Geopolitics: Ukraine

- Russia’s Kremlin, on the potential resumption of flows via Druzhba, said Russia is technically ready but there was “blackmail from Kyiv”.

- EU’s Kallas said they are to make decisions on Ukraine’s EUR 90bln loan on Wednesday.

- Explosion heard in Ukraine’s Zaporizhzhia.

- Japan is to permit its companies to export lethal weaponry for the first time, in a landmark break with its pacifist stance, according to FT.

US Event Calendar

- 8:30 am: United States Mar Retail Sales Advance MoM, est. 1.4%, prior 0.6%

- 8:30 am: United States Mar Retail Sales Ex Auto MoM, est. 1.4%, prior 0.5%

- 10:00 am: United States Mar Pending Home Sales MoM, est. 0.5%, prior 1.8%

- 10:00 am: United States Fed Chair Nominee Warsh Testifies in Confirmation Hearing

- 2:30 pm: United States Fed’s Waller Speaks on Fed Operations

DB’s Jim Reid concludes the overnight wrap

In terms of latest on Iran, all eyes are on whether and in what form expected talks in Islamabad take place over the next day or so ahead of the expiration of the earlier two-week ceasefire. Trump said yesterday that this would expire on “Wednesday evening Washington time” and warned that it was “highly unlikely” that he’d extend the ceasefire. Various reporting suggests that Vice President Vance is expected depart to Islamabad today, and we also saw reporting by the New York Times and others that Iran is also sending a team to Islamabad for negotiations. With a spokesman for Iran’s foreign ministry earlier saying that Tehran had no plans to attend the negotiations, this has given a more positive light on the talks going ahead, though it remains unclear who would lead the Iranian delegation.

While the Strait of Hormuz remained shut, the prospects for imminent talks have seen market sentiment edge higher overnight after a subdued session on Monday. Brent crude prices are -0.62% lower at $94.89/bbl after a +5.64% rise yesterday. S&P 500 (+0.17%) and NASDAQ 100 (+0.25%) futures are so far recovering most of yesterday’s losses, declines that got less severe as the day progressed with the S&P 500 only dipping -0.24% in the end. The probability of traffic returning to normal in the Strait of Hormuz by the end of May, according to Polymarket, stands at 69% this morning from 63% this time yesterday.

The NASDAQ (-0.26%) did end a 13-day winning run, the longest streak since 1992 and only bettered on four occasions in the index’s 55-year history. The Philadelphia Semiconductor index did achieve a 14th consecutive gain though. US Treasuries also slipped back modestly, with the 2yr yield (+1.5bps) up to 3.72%, and the 10yr yield (+0.2bps) up to 4.25%. And with doubts creeping back in, the VIX (+1.39pts) saw its biggest daily jump in 3 weeks, though at 18.87pts it still closed below its level on February 27, before the Iran strikes began.

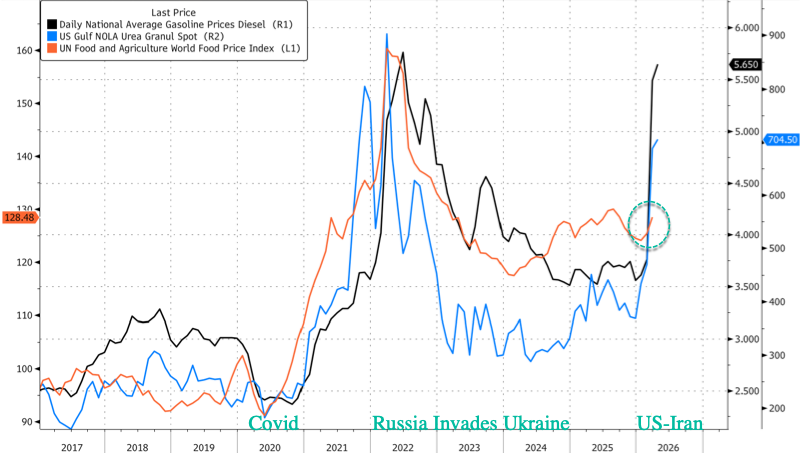

The hangover from the weekend’s negative news led to a fresh rise in oil prices, particularly given warnings from Trump that he wouldn’t open the Strait of Hormuz until a deal was signed. So Brent crude was up +5.64% to $95.48/bbl by the close, and there was a clear move higher across the futures curve too, with 6-month Brent futures (+3.16%) back up to $81.97/bbl. And in turn, those moves filtered into inflation pricing, with the 1yr US inflation swap (+2.6bps) up to 3.13%, whilst the Euro inflation swap (+9.1bps) moved up to 3.06%.

This morning, Asian equity markets are rallying, with the KOSPI (+2.31%) again leading the way, driven by optimism surrounding AI-related chip manufacturers. Japanese stocks are also being supported by technology shares, as evidenced by the Nikkei (+1.29%) which is trading significantly higher. On the other hand, Chinese stocks are more mixed with the Hang Seng (+0.13%) slightly higher but the CSI (-0.35%) and the Shanghai Composite (-0.24%) lower.

As much as the Middle East is the main focus for markets, especially as we near the end of the ceasefire, today there’ll also be attention on Kevin Warsh’s nomination hearing (10am ET) to become the next Chair of the Federal Reserve. He’s appearing at the Senate Banking Committee, so investors will get an opportunity to hear his views on policy and a whole array of Fed-related issues. For more information, our US economists published a note on Friday (link here) where they outline 5 things to watch. They think the critical questions will be how forcefully Warsh argues for near-term rate cuts, particularly given the recent upside risks to inflation from the Iran war, as well as views on Fed independence. In prepared remarks that were reported yesterday, Warsh says that “monetary policy independence is essential” but also noting that “Fed independence is largely up to the Fed” and that “Fed independence is placed at greatest risk when it strays into fiscal and social policies where it has neither authority nor expertise.” So focusing on the importance of Fed independence but also suggesting that the central bank needs to earn it.

Whilst the focus will be on Warsh, another point to look out for will be Republican Senator Thom Tillis, who’s said he’ll block any Fed appointments until the Department of Justice probe into Chair Powell is over. He sits on the Senate Banking Committee, but the Republicans only have a 13-11 majority, meaning if Tillis votes against then he could hold up Warsh’s nomination if the Democrats joined him. Powell’s current term as Chair concludes in mid-May, but he has a separate seat on the Board of Governors that lasts until January 2028, and at the most recent press conference, Powell said he’d serve as Chair pro tempore until his successor was confirmed. For reference, that’s what happened between Powell’s first and second terms as Powell awaited Senate confirmation, but that was when Powell himself had been re-nominated by President Biden, whereas Trump has suggested that “I’ll have to fire him” if Powell didn’t leave the Fed.

Earlier in Europe, markets underperformed their US counterparts, reflecting the continent’s greater exposure to higher energy prices. So the STOXX 600 (-0.82%) fell back, alongside declines for the DAX (-1.15%), the CAC 40 (-1.12%) and the FTSE 100 (-0.55%). That followed mounting speculation that the ECB would still need to hike rates this year if the oil shock were more prolonged, with the amount of hikes priced by December up +7.2bps on the day to 45bps. So sovereign bonds also lost ground across the continent, with yields on 10yr bunds (+2.1bps), OATs (+3.4bps) and BTPs (+4.4bps) all rising.

Here in the UK, 10yr gilts (+7.1bps) underperformed as question marks around Keir Starmer’s position as PM continued to swirl. The latest issues follow last week’s revelation that Peter Mandelson was appointed as US ambassador despite failing security vetting. That’s set to remain in the headlines today as well, because we’ll hear from Oliver Robbins, who was the most senior civil servant in the Foreign Office, who’s appearing before the Foreign Affairs Committee of MPs at 9am London time. Robbins was sacked for not informing Starmer that Mandelson hadn’t passed the vetting, so his version of events will be in focus today.

Finally, there wasn’t much data yesterday, but Canada’s inflation print was softer than expected, with headline CPI only up to +2.4% in March (vs. +2.6% expected). Moreover, the two core inflation measures tracked by the Bank of Canada were either in line or slightly beneath consensus. So that eased concern about imminent rate hikes, and Canada’s 10yr government bond yield fell -1.0bps on the day, outperforming its counterparts in the US and Europe.

Looking at the day ahead, one of the main highlights will be the US Senate Banking Committee, which is holding a nomination hearing for Kevin Warsh to become Chair of the Federal Reserve. Other central banks speakers include ECB Vice President de Guindos, and the ECB’s Nagel and Kocher. And data releases include US retail sales for March, the German ZEW survey for April and UK unemployment for February.