Authored by Lance Roberts via RealInvestmentAdvice.com,

My…my…how quickly we forget.

Yesterday, as the markets rocketed higher, my email lit up with questions surrounding the discussion from this last weekend’s newsletter.

“I have questioned over the last couple of weeks exactly how much volatility the Fed would allow before stepping into the fray to keep the markets stable.

We now know it is roughly a 10% decline.

Specifically were the comments about QE being ‘useful to have in the toolkit for those times when the short-term interest rate tool may not be available,’ adding that the Fed is ‘quite likely’ to require large-scale asset purchases again because real rates will remain low due to slow productivity and labor-force growth. They also added that ‘if LSAPs are indeed not effective, then the Fed may need to take other measures.’ (Zerohedge has the complete article.)

In other words, despite the rhetoric to the contrary, the Fed isn’t going away…….ever!”

The deluge of emails revolved around much of the same premise.

“If the the Fed isn’t going away, then why would there ever be another bear market?”

It is certainly an interesting question, particularly as the Fed continues to trot out officials to make market supporting statements such as Fed Vice Chairman Quarles who stated on Monday:

“It might seem reasonable to assume that faster growth would lead to firmer inflation. However, I think a lot remains to be seen.”

Or even Mario Draghi, Chairman of the ECB, who said:

“In the presence of an economic situation that is improving constantly, we need the right blend of measures. Uncertainties continue to prevail.”

So, despite economies that are supposedly improving, Central Banks continue into their tenth year of “emergency measures.” As Michael Lebowitz recently stated:

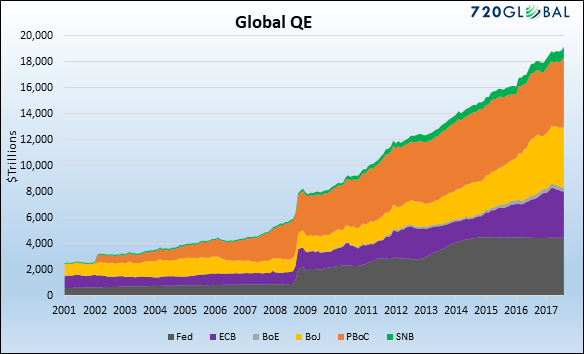

“Global central banks’ post-financial crisis monetary policies have collectively been more aggressive than anything witnessed in modern financial history. Over the last ten years, the six largest central banks have printed unprecedented amounts of money to purchase approximately $14 trillion of financial assets as shown below. Before the financial crisis of 2008, the only central bank printing money of any consequence was the Peoples Bank of China (PBoC).”

With that, I certainly understand the reasoning that if indeed “Central Banks” are now committed to monetary interventions going forward, the financial markets have been effectively “fire-proofed against bear markets.”

But such a belief is extremely dangerous.

It is also the same “belief” every major bubble was built upon throughout history and driven by the same underlying foundations.

Which created the bubble in “THE” asset class of choice at that time…

Which created the bubble…

Which always ended badly for investors.

Every. Single. Time.

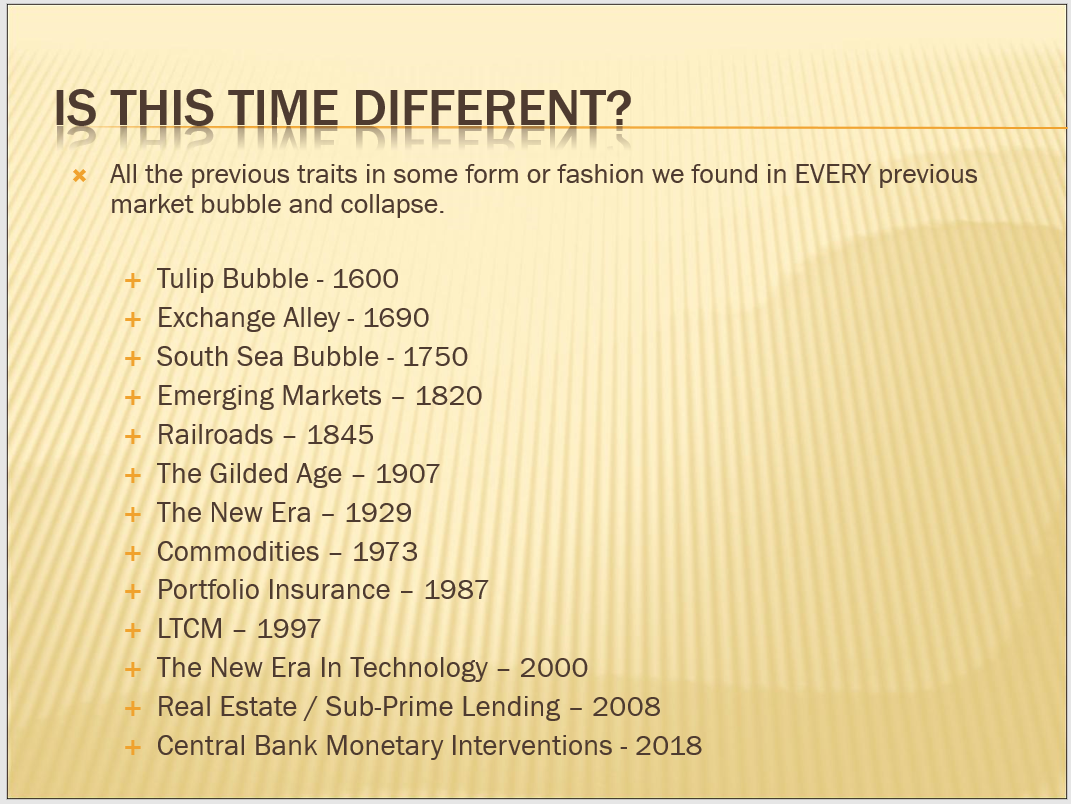

Is “this time different?”

No, and it will end just the same as every previous liquidity driven bubble throughout history.

Of this, there is absolute certainty.

There are only TWO questions that must be answered:

-

What will cause it, and;

-

When will it happen?

What Will Cause The Next Crash

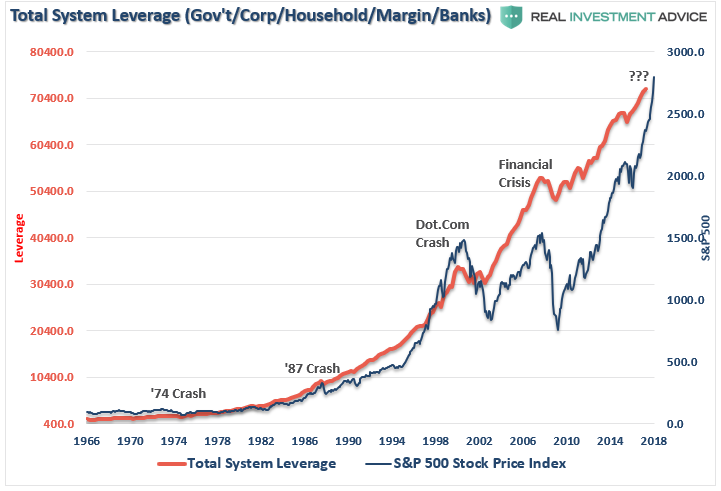

No one knows for certain what will cause the next financial crisis. However, in my opinion, the most likely culprit will be a credit-related event caused by the Fed’s misguided policy of hiking interest rates, and tightening monetary policy, when the financial system is more heavily levered than at any other point in human history.

The illusion of liquidity has a dangerous side effect. The process of the previous two debt-deleveraging cycles led to rather sharp market reversions as margin calls, and the subsequent unwinding of margin debt fueled a liquidation cycle in financial assets. The resultant loss of the “wealth effect” weighed on consumption pushing the economy into recession which then impacted corporate and household debt leading to defaults, write-offs, and bankruptcies.

With the push lower in interest rates, the assumed “riskiness” of piling on leverage was removed. However, while the cost of sustaining higher debt levels is lower, the consequences of excess leverage in the system remains the same.

You will notice in the chart above, that even relatively small deleveraging processes had significant negative impacts on the economy and the financial markets. With total system leverage spiking to levels never before witnessed in history, it is quite likely the next event that leads to a reversion in debt will be just as damaging to the financial and economic systems.

Since interest rates affect “payments,” increases in rates negatively impact consumption, housing, and investment which ultimately deters economic growth.

It will ultimately be the level of interest rates which triggers some “credit event” that starts the “next bear market”

It has happened every time in history.

Importantly, as prices decline it will trigger margin calls which will induce more indiscriminate selling. The forced redemption cycle will force investors to dump positions to meet margin calls at a time when the lack of buyers will create a vacuum causing rapid price declines.

When Will It Happen

Honestly, no one knows for sure. However, history can give us some guide.

“In the past six decades, the average length of time from the first tightening to the end of the business cycle is 44 months; the median is 35 months; and the lag from the initial rate hike to the end of the bull equity market is 38 months for the average, 40 months for the media.” – David Rosenberg

Averages and medians are great for general analysis but obfuscate the variables of individual cycles. To be sure the last three business cycles (80’s, 90’s and 2000) were extremely long and supported by a massive shift in financial engineering and a credit leveraging cycle. The post-Depression recovery, and WWII, drove the long economic expansion in the 40’s, and the “space race” supported the 60’s.

Currently, employment, economic and wage growth remain weak with 1-in-4 Americans on Government subsidies and the majority living paycheck-to-paycheck. This is why Central Banks, globally, have continued aggressively monetizing debt in order to keep growth from stalling out. With the Fed now hiking rates, and reducing market liquidity, the risk of a policy mistake has risen markedly.

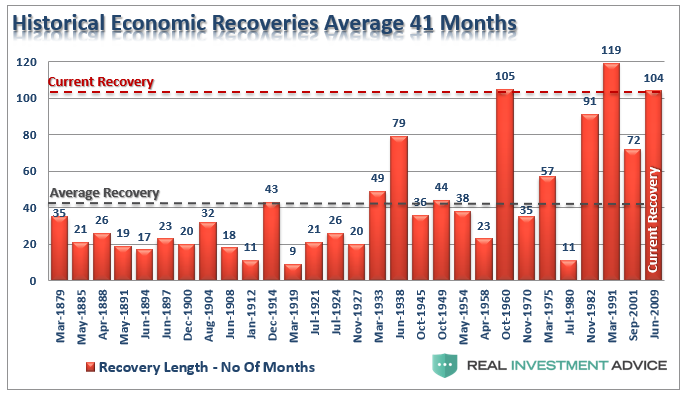

If David is correct, given the Fed began their current rate hiking campaign in December 2015, the next recession would occur 38-months later or February 2019. Such a span would make the current economic expansion the second longest in history based on the weakest economic growth rates.

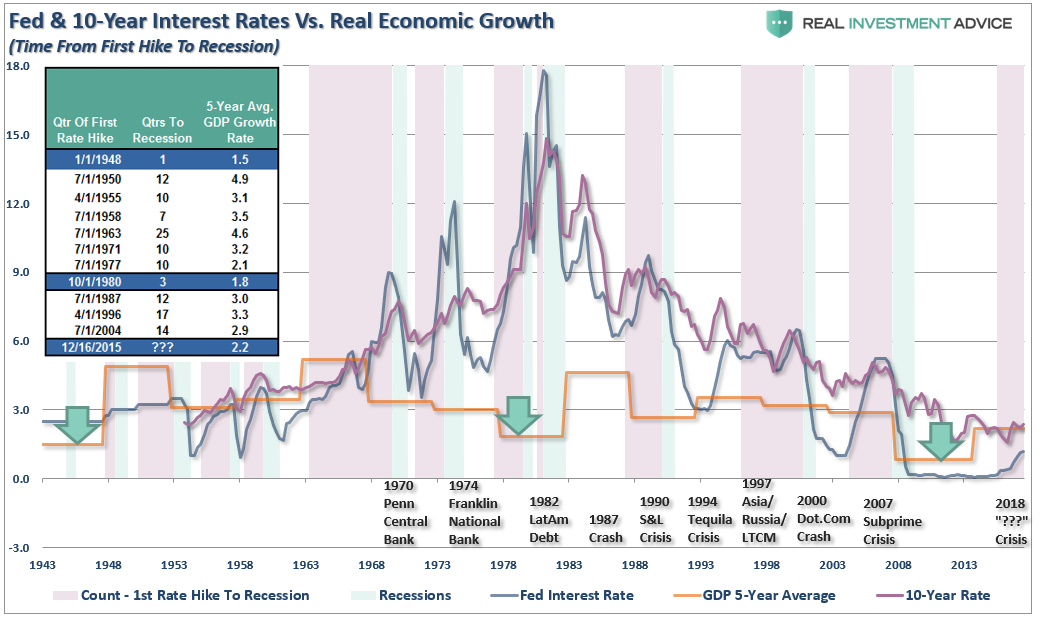

The chart and table below compares real, inflation-adjusted, GDP to Federal Reserve interest rate levels. The vertical purple bars denote the quarter of the first rate hike to the beginning of the next rate decrease, or onset of a recession.

If you look at the underlying data, which dates back to 1943, and calculate both the average and median for the entire span, you find:

- The average number of quarters from the first rate hike to the next recession is 11, or 33 months.

- The average 5-year real economic growth rate was 3.08%

- The median number of quarters from the first rate hike to the next recession is 10, or 30 months.

- The median 5-year real economic growth rate was 3.10%

The importance of this reflects the point made previously, the Federal Reserve lifts interest rates to slow economic growth and quell inflationary pressures. Yet, economic growth and inflation are running well below historical norms and system-wide leverage has surged to new records as individuals and corporations have feasted on debt in a low-rate environment.

That is now changing as the Fed hikes interest rates. Notice in the chart above, that recessions occur when the Fed starts hiking interest rates and the Fed rate approaches the 10-year Treasury rate. In every instance, a recession or “crisis” occurred.

Crisis, Recession & Bear Markets

If historical averages hold, and since major bear markets in equities coincide with recessions, then the current bull market in equities has about one year left to run. While the markets, due to momentum, may ignore the effect of “monetary tightening” in the short-term, the longer-term has been a different story.

As shown in the table below, the bulk of losses in markets are tied to economic recessions. However, there are also other events such as the Crash of 1987, the Asian Contagion, Long-Term Capital Management, and others that led to sharp corrections in the market as well.

The point is that in the short-term the economy, and the markets (due to momentum), can SEEM TO DEFY the laws of gravity as interest rates begin to rise. However, as rates continue to rise they ultimately act as a “brake” on economic activity.

While rising interest rates may not “initially” impact asset prices, it is a far different story to suggest that they won’t. In fact, there have been absolutely ZERO times in history that the Federal Reserve has begun an interest rate hiking campaign that has not eventually led to a negative outcome.

What the majority of analysts fail to address is the “full-cycle” effect from rate hikes. While equities may initially provide a haven from rising interest rates during the first half of the rate cycle, they have been a destructive place to be during the second-half.

It is clear from the analysis that “bad things” have tended to follow the Federal Reserve’s first interest rate increase. While the markets, and economy, may seem to perform okay during the initial phase of the rate hiking campaign, the eventual negative impact will push most individuals to “panic sell” near the next lows. Emotional mistakes are 50% of the cause as to why investors consistently underperform the markets over a 20-year cycle.

The exact “what” and “when” of the next “bear market” is unknown. It has always been some unanticipated event that triggers the “reversion to the mean.”

It will be obvious in “hindsight.”

While the media will loudly protest that “no one could have seen it coming,” there are plenty of clues if you only choose to look.

The Fed has not put an “end” to bear markets.

In fact, they have likely only succeeded in ensuring the next bear market will be larger than the last.

For now, the bullish trend is still in place and should be “consciously” honored. However, while it may seem that nothing can stop the markets rise, or seemingly the Fed will never let it fall, it is crucial to remember that it is “only like this, until it is like that.”

For those “asleep at the wheel,” there will be a heavy price to pay when the taillights turn red.

via Zero Hedge http://ift.tt/2HSLu8A Tyler Durden