Authored by John Coumarianos via RealInvestmentAdvice.com,

In this past weekend’s Real Investment Advice Newsletter, I wrote about financial advisor Larry Swedroe’s excellent article on the “Four Horsemen of the Retirement Apocalypse:”

- low stock returns,

- low bond yields.

- increased longevity; and,

- higher healthcare expenses.

In his article, Swedroe mentions that high yield (junk) bonds won’t save investors, who haven’t historically been rewarded well for taking on their risk. Swedroe also says high yield bonds correlate well with stocks, which means they don’t provide much diversification. Swedroe writes from the point of view of modern portfolio theory, which looks for ways to increase volatility-adjusted returns in a portfolio. In this post, I’ll treat junk bonds a little differently, showing why now is a terrible time to own them. My analysis doesn’t completely contradict Swedroe’s though; it supports his thesis that stocks and junk bonds are highly correlated.

Unlike Swedroe, I don’t dislike junk bonds per se. These loans to decidedly less-than-blue-chip companies are just like any other asset class.

They can be priced to deliver good returns, as they were in early 2009, or not.

Right now, they’re not.

Everyone looks at junk bonds initially by observing the starting yield or yield-to-maturity. Right now, the iShares High Yield Corporate Bond ETF (HYG) is yielding 5.53%. That can look attractive to some investors. After all, where else can you get over 5%?

Other people look at the spread to the 10-Year U.S. Treasury. 5.53% is around 2.7 percentage points more than the 2.8% yield of the 10-year U.S. Treasury. That might look find to some too. Of course, a little bit of research shows that spread is lower than the historical average of around 5.7 percentage points.

Still, investors seeking higher yield may be undisturbed by a historically low spread. Some people need the extra yield pick-up over Treasuries, however small it might be by historical standards, and that’s enough for them to make the investment.

Yield Isn’t Total Return

There’s one extra bit of analysis, however, that should make investors think again about owning junk bonds – a loss-adjusted spread. The problem high yield investors often fail to consider is that junk bonds default. And that means the yield spread over Treasuries isn’t an accurate representation of what high yield investors will make in total return over Treasuries. It’s easy to forget about defaults and total return because defaults don’t occur regularly. They tend to happen all at once, giving junk bonds a kind of cycle and encouraging complacency among yield-starved investors during calm parts of the cycle.

Default rates for junk average about 4.2% annually, according to research from Standard & Poor’s. And investors have typically recovered 41% (or lost a total of 59%) of those defaults, according to this Moody’s study from 1981 through 2008. That results in an annual loss rate for an entire portfolio of around 2.5%. So the iShares fund’s 5.53% yield isn’t quite what it seems to be. In fact, if we subtract 2.5 from 5.53, the result is 3.03, meaning investors in junk bonds are likely to make only 20 basis points more than the 2.8% they could capture in a 10-Year U.S Treasury currently.

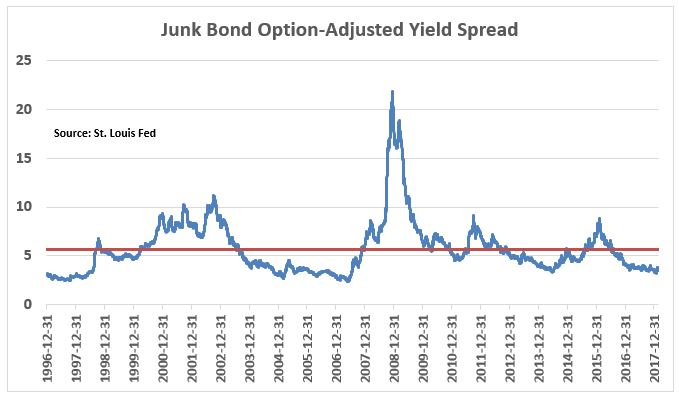

Now, a more careful analysis should consider an “option-adjusted” spread, which accounts for the fact that issuers can call bonds prior to maturity and lenders or bondholders can sell bonds back to the issuer at prearranged dates. This adjustment usually adds something to the spread, making higher yielding bonds slightly more attractive. So we took the options adjusted spread data, and adjusted it for an annual loss rate of 2.5 percentage points. Remarkably, there have been times such as immediately before the financial crisis when investors weren’t making anything on an options-adjusted basis above Treasuries to own junk bonds. Now at least it’s around 1 percentage point.

Still, even with the option adjustment, one percentage point over Treasuries is still very little, especially considering that the option-adjusted spread we used compares a junk bond index with Treasuries. In other words, the 0.50% expense ratio of most junk bond ETFs isn’t factored into the equation. At a 0.50% or so yield pickup over Treasuries, investors just aren’t making enough from junk bonds to justify owning them. Also, advisors pushing junk bonds on yield-hungry clients aren’t doing much due diligence. The mark of a good advisor is one who can say “No” to a client and bear the risk that the client will go to another advisor doing less due diligence.

via Zero Hedge http://ift.tt/2GTZ36d Tyler Durden