Monday’s selloff, which spared the US cash market which was closed for MLK day, has stretched for a second day, with US traders walking in to a sea of red in Asian and European markets, while S&P futures are down over 20 points following a pessimistic economic assessment by the IMF, renewed trade concerns after the US submitted a formal request to extradite the Huawei CFO from China and “very poor” results from UBS.

“The appetite for risk is exceptionally low,” Ajay Kapur, head of Asia-Pacific and global emerging market strategy at Bank of America Merrill Lynch, told Bloomberg Television. “Most of the time, when you buy when sentiment is this depressed, you tend to make money,” unless there’s a recession, he said. “If you’re confident there will be no recession in the next year or so, I think this is a good indicator.”

Europe’s Stoxx 600 Index pared an early drop after Swiss banking giant UBS reported disappointing results and $13 billion in outflows, compounding what had been a catastrophic 2018 for Europe’s banking sector which lost nearly 30 percent of its value over the year, and sending UBS stock sliding while setting up a pessimistic tone for the continent’s banks which are set to begin reporting Q4 earnings.

After stocks rallied to the strongest start of the year since 1938, investors now find their conviction tested anew as a familiar litany of concerns weigh on sentiment. Adding to the sense of gloom, on Monday in its World Economic Outlook report, the IMF downgraded the global economy for the second time in three months when it predicted the global economy would grow at 3.5% in 2019 and 3.6% in 2020, down 0.2 and 0.1 percentage point respectively from last October’s forecasts.

In the latest confirmation that Europe’s economy is on the verge of a recession, today’s German ZEW Current Situation report printed at 27.6, a huge miss to the 43.0 exp. and the lowest in 4 years.

The downgrades heavily reflected weakness in Europe though, with Germany hurt by new car emission rules, Italy under market pressure due to Rome’s recent budget standoff with the European Union and Brexit worries aplenty too. As a result, European stocks struggled to stay positive as U.S. futures pointed to a sharply lower open after Monday’s holiday.

“We have seen a little bit of a pull back, but whether it’s the IMF growth downgrade or China related is neither here nor there,” said CMC Markets’ senior analyst Michael Hewson. “We are at the top end of the range for this year and given the global uncertainty investors are probably taking the view that it is probably wise to take a bit of profit off the table.”

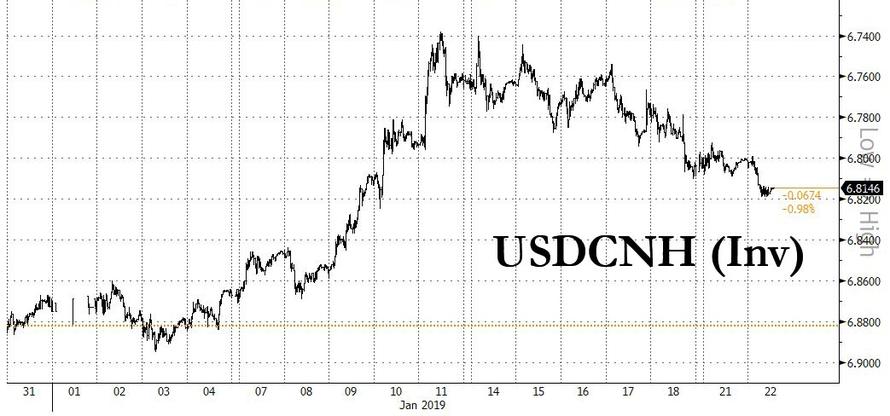

Earlier in the session, shares declined across Asia, with losses led by Chinese shares, as the Shanghai Composite slumped 1.2%, while Japan’s Nikkei skidded 0.5 percent, Hong Kong’s Hang Seng index closed down 0.8 percent and Sydney faltered 0.5 percent. Without any direction offered from American markets that were shut Monday for a holiday, the focus turned to comments from Chinese President Xi Jinping stressing the need to maintain political stability and news that the U.S. will move forward with a formal request to extradite Huawei CFO from Canada, sending Chinese equities and the yuan lower. The Offshore yuan weakened 0.20% to 6.8145 per dollar, the weakest level since Jan. 10

In another sign of risk aversion, the Australian dollar, often used as a liquid proxy for China investments, eased 0.3 percent to $0.7134, putting it on track for a third straight session of losses. The same worries had also sent copper, used in electrical wires and vehicles, drifting lower in the metals markets.

In FX markets, the dollar climbed for a sixth day, holding at a near three-week high as investors sought the relative safety of the U.S. currency. That knocked the euro and most emerging market currencies, many of which have had a decent start to the year. Sterling was slightly higher at $1.29 after data showed British workers’ pay growth hit a new 10-year high and employment had grown by much more than expected in the three months to the end of November. There was demand too for the safe-haven yen with the Japanese currency last buying at 109.41 per dollar. The euro was near the floor of its recent trading range at $1.1358. Against a basket of currencies, the dollar was barely changed at 96.393.

Otherwise traders were still waiting to see whether UK Prime Minister Theresa May can push her Brexit plans through the country’s bitterly divided parliament. May had offered tweaks on Monday by seeking further concessions from the European Union on a backup plan to avoid a hard border between the British-administered province of Northern Ireland and the Irish Republic. But she had also refused to rule out leaving the EU at the end of March without any deal.

In bonds, Bunds traded a round-trip back to unchanged on the day, cash 10s stalling around 0.23% early in the session before rebounding. UST yields are ~2bp lower across the curve, with 10s grinding lower after Monday’s market closure as curves flatten. Peripheral bonds tighten slightly to core. The 20Y Gilt auction was well received, bouncing off session lows are robust auction metrics.

In commodities, the global growth worries pulled oil prices lower with Brent down 55 cents at $62.19 and U.S. crude futures off 39 cents at $53.41. Euro zone government bond yields also fell. Most 10-year yields were down two basis points on the day with Germany’s at 0.225 percent compared to Friday’s one-month high close to 0.28 percent. The European Central Bank holds its first meeting of the year on Thursday.

Expected data include existing homes sales. J&J, Prologis, Travelers and IBM are among companies reporting earnings.

Top Overnight News

- U.K. Prime Minister Theresa May’s Brexit Plan B turns out to be a re-run of her Plan A — seeking EU concessions on the deal she’s already negotiated with Brussels. But even if she succeeds, it’s not at all clear she could get the modified terms through Parliament

- The U.K.’s main opposition party is backing a plan that could open the door to a second EU referendum, bringing the possibility of stopping Brexit a step closer

- At a meeting of euro-zone finance ministers on Monday, the Irish central-bank governor Philip Lane became the first nominee to replace Peter Praet on the ECB’s Executive Board in June. That puts him in prime position to take on Praet’s powerful role of overseeing economic projections and writing monetary-policy recommendations

- CME Group Inc. will move its FX forwards and swaps venue, which has trading volumes of about $15b a day, from London to Amsterdam, while Cboe Global Markets Inc. will shift most European equities trading to its market in the Dutch capital after Brexit

- Confidence across the energy industry is now where it was in 2010, when Brent soared to $95 a barrel, according to a survey by Det Norske Veritas, incorporating the views of 791 senior oil and gas industry professionals between October and November

- German Jan. ZEW Current Situation 27.6 vs 43.0 est; Expectations -15.0 vs -18.5 est

- China CSRC Vice Chair doesn’t see China significantly cutting U.S. bond holdings

- Trump says China should stop “playing around,” do “real” trade deal

- U.S. to proceed in seeking Huawei CFO extradition, Globe says

- China’s Xi warns of ’serious dangers’ to stability as risks mount

Market Snapshot

- S&P 500 futures down 0.7% to 2,654.00

- Lebanon’s Debt Urgency Prompts Moody’s Downgrade on Default Risk

- Chinese Stocks Decline as Investors’ Outlook on Economy Darkens

- Saudi Arabian Energy Minister Al-Falih Set to Cancel Davos Trip

- Philippines Central Bank Governor Takes Indefinite Medical Leave

- STOXX Europe 600 up 0.02% to 356.42

- German 10Y yield unchanged at 0.255%

- Euro down 0.02% to $1.1363

- Brent Futures down 1.3% to $61.93/bbl

- Italian 10Y yield rose 2.8 bps to 2.4%

- Spanish 10Y yield fell 1.4 bps to 1.352%

- Brent futures down 1.5% to $61.81/bbl

- Gold spot up 0.3% to $1,284.41

- U.S. Dollar Index little changed at 96.35

Asian equity markets were negative as the region lacked impetus following the non-existent lead from the US due to Martin Luther King Jr. Day and as the slowest growth in China in nearly 3 decades continued to reverberate across risk sentiment. ASX 200 (-0.5%) was led lower by underperformance in its largest weighted financials sector and with miners dampened following softer output numbers by BHP, while Nikkei 225 (-0.5%) was also pressured with losses later exacerbated by currency flows. Hang Seng (-0.7%) and Shanghai Comp. (-1.2%) conformed to the downbeat tone in the aftermath of the recent Chinese growth figures which some expect to further deteriorate this year and after the PBoC refrained from open market operations for a 2nd consecutive day which resulted to a net daily drain of CNY 80bln, while there were also reports the US is to proceed with the formal extradition of Huawei’s CFO. Finally, 10yr JGBs were underpinned amid the uninspiring risk tone in the region and as yields also declined in the super long-end in which the 40yr yield drop to its lowest since 2016.

Top Asian News

- Lebanon’s Debt Urgency Prompts Moody’s Downgrade on Default Risk

- Chinese Stocks Decline as Investors’ Outlook on Economy Darkens

- Saudi Arabian Energy Minister Al-Falih Set to Cancel Davos Trip

- Philippines Central Bank Governor Takes Indefinite Medical Leave

Major European equities extended losses [Euro Stoxx 50 -0.6%] after briefly pairing back opening losses as the risk sentiment continued to deteriorate. The European banking sector is underperforming, with the sector weighed on by UBS (-4.3%) following poor results; with this dragging other banking names down in sympathy such as Credit Suisse (-1.0%) and Deutsche Bank (-3.6%). Deutsche Bank also impacted by reports that they, alongside another bank, have been accused of fraud with a EUR 11bln lawsuit filed against them. Other notable movers include IG Group (-6.7%) who are at the bottom of the Stoxx 600 after stating that their HY net revenue and profit are down by 6% and 18% respectively. At the other end of the Stoxx 600 are Hugo Boss (+5.0%) who reported a beat on their Q4 sales.

Top European News

- Deutsche Bank Sued for $12 Billion by Sabet Over Lost Lawsuit

- U.K. Wages Grow at Fastest Pace Since 2008 in Tight Labor Market

- Italy’s Populists Make France Nemesis Ahead of European Vote

- Thiam Says Things Looking Up After ‘Difficult’ Fourth Quarter

- Auchan May Pay Up for Bond as French Unrest Adds to Challenges

In FX, the DXY is relatively flat on the day but choppy within a 96.300-480 range following an uneventful Asia-Pac session. The buck experienced a bout of Dollar demand in earlier European trade which coincided with comments from the Chinese Foreign Ministry regarding the extradition of Huawei’s Executive Meng wherein China strongly opposed the decision by the US and stated they will retaliate in accord with US lawmakers’ decisions. This saw the DXY push higher to intraday highs and levels just shy of 96.500 before a tweet by China’s Global Times Editor stating that China will not yield to an unequal deal from the US sent the index lower to around the middle of today’s range. On the States-side data front, today sees a scarce calendar with the release of existing home sales scheduled.

- GBP – Mixed trade as the Pound benefits from the pullback in the buck alongside optimistic jobs data in which headline average earnings beat expectations while the ILO unemployment rate ticked lower. Cable showed some strength in the run-up to the release and as the numbers provided further impetus for the Sterling, GBP/USD extended gains and breached its 100 DMA to the upside at 1.2891 to reclaim 1.2900 and print session highs of 1.2930. On the Brexit front, in yesterday’s statement PM May said she will to head back to the EU for dialogue, while The Telegraph reported that her chief Brexit negotiator is privately doubtful on her ability to renegotiate the Irish backstop. Furthermore, she dismissed the idea of extending Article 50 with reports emerging by BBC’s Assistant Political Editor Smith stating that Ministers will have to sit through the February recess and weekends to achieve in deal in by the Brexit date, which markets could perceive as a positive as it potentially gives them more time to achieve an appropriate deal. Meanwhile, Tory lawmaker Rudd warned that the Premier could face a dozen resignations if Tory MPs get no vote on plans to stop a no-deal Brexit, though analysts at JPM see the likelihood of a no-deal at 5%.

- EUR – Little changed against the Dollar as the single currency fails to benefit from the receding buck as gains are capped by the Sterling-induced decline in EUR/GBP following the aforementioned UK jobs data and Brexit developments, while the release of mixed ZEW number did little to move the single currency. EUR/USD remains flat around 1.1360 while EUR/GBP resides close to session lows under 0.8800 with no notable option expiries today.

- JPY – A positive day for the Yen amid overnight strength from the risk-averse tone and as the BoJ began their 2-day policy meeting (full preview available on the Research Suite). USD/JPY hovers under 109.50 (vs. low of 109.34) with the pair’s 50 and 200 DMAs poised to form a death-cross.

In commodities, Brent (-1.9%) and WTI (-1.8%) extended losses as the complex is impacted by the negative risk tone and US absence from market yesterday. The energy complex saw another leg lower after Saudi Energy Minister Al Falih has reportedly cancelled his trip to Davos; Al Falih was due to speak on Wednesday on the New Energy Equation but more importantly, the Energy Minister was due to hold talks on the recent OPEC+ production cuts with the Russian Eenergy Minister. Elsewhere, the Canadian province of Alberta is expected to announce a CAD 2bln oil sector investment plan. Separately, as yesterday was a US holiday API weekly data will be released tomorrow. Gold (+0.3%) is in the green, trading towards the top end of the sessions range as markets continue to be impacted by the negative risk tone and a receding dollar. Elsewhere, China’s top steel-making city of Tangshan has issued a level 2 smog alert; to be effective until January 25th. BHP, the world’s biggest miner, reported a 9% fall in iron ore production, as well as highlighting USD 600mln impact due to iron and copper operations disruptions.

Looking at the day ahead, the lone release is December existing home sales which is expected to show a small decrease (-1.5% mom) during the month. Elsewhere the annual Davos shindig kicks off today while the earnings highlights include Johnson & Johnson and IBM in the US, and UBS in Europe.

US Event Calendar

- 10am: Existing Home Sales, est. 5.24m, prior 5.32m; MoM, est. -1.5%, prior 1.9%

DB’s Jim Reid concludes the overnight wrap

Well we hope you survived Blue Monday yesterday, supposedly the most depressing day of the year. The guy who decided upon this used the following equation to denote it where W = weather, D = debt, d = monthly salary, T = time since Christmas, Q = time since failing our New Year’s resolutions, M = low motivational levels, Na = the feeling of a need to take action. If there are any quants out there that would like to tighten up this equation then feel free. For it to work for me I may need to add days since I was last injury free and days since our builder last increased the price of our renovations. These would be T-0 and T-1 respectively.

((W + (D – d)) x T^Q) / (M x Na)

To be fair Blue Monday was very quiet with the US on holidays. The latest Brexit developments were the focal point but in truth nothing much happened on that front. In her House of Commons speech yesterday, May ruled out a second referendum, which was largely as expected, and reiterated the greater role for parliament on the future relationship, as well as making assurances over EU worker rights. May specifically said that she will be “more flexible, open and inclusive in the future” as to how the government engages Parliament showing a slight move to embrace wider views. However in essence this is Plan A, but with hope that the Tories and DUP can coalesce around a better solution for the Irish problem and then persuade Brussels (and of course the Irish) to accept it. So not a huge amount of new news. What will be important now is what amendments get tabled ahead of Tuesday’s vote and whether or not they get a majority when voted on. That may give us a guide as to what Parliament can agree on and what is a non-starter. I can’t help feeling that if Parliament takes over this process it might actually give the two main parties a way of saving face. At the moment it’s difficult for either to back down for various reasons (splits within their parties) but if Parliament chooses the path for them and takes over it may allow for blame to shift.

The latest news in today’s Times suggests that the government divisions remain. Cabinet minister Amber Rudd has apparently warned No 10 that it could face 25-40 resignations from the government if Tory MPs are banned from voting for a plan that helps stop a no-deal Brexit. This is based on an amendment drafted by Labour’s Yvette Cooper and the Tory backbenchers Sir Oliver Letwin and Nick Boles. Ms Rudd is trying to persuade the PM to allow a free vote to allow a consensus to form. This perhaps fits with my view that Parliament taking over might be the best way of saving face and getting a deal. It’s worth noting that overnight opposition leader Corbyn has proposed the amendment of a second referendum.

May’s comments did at least help to lift Sterling marginally as it touched an intraday high of $1.291 before it settled down to trade broadly flat overnight at $1.288. Gilts were actually stronger through much of yesterday and ultimately finished -2.9bps lower in yield while the FTSE 100 and FTSE 250 finished a rather tepid +0.03% and -0.01% respectively. Overnight, sentiment more broadly in Asia is weaker with the majority of bourses in the red as we go to print. That’s the case for the Nikkei (-0.56%), Hang Seng (-1.01%), Shanghai Comp (-0.73%) and Kospi (-0.58%). Futures on the S&P 500 are also down -0.72% with the US market set to reopen today following yesterday’s holiday while EM FX is also struggling. Comments from China’s Xi (more below) appears to be playing a part while Bloomberg is also reporting that the US is to proceed in seeking the extradition of Huawaei’s CFO from Canada.

That US holiday meant it was predictably quiet for markets in Europe yesterday with equity bourses limping to small losses for the most part during a low volume session. That was the case for the STOXX 600 which ended -0.19% and so brought to an end a four-day winning run. Banks (-0.46%) – hot on the heels of four straight weekly gains – struggled as did utilities (-1.08%). The DAX (-0.62%), CAC (-0.17%), IBEX (-0.17%) and FTSE MIB (-0.35%) also closed lower while in contrast it was a slightly stronger day for cash credit – albeit modestly so – with IG and HY spreads both 1bp tighter. Bond markets were similarly unexciting. Bunds closed -0.7bps lower in yield while the periphery was 1bp to 3bps higher. Elsewhere WTI oil touched the highest level in two months intraday yesterday before fading overnight to trade down -0.69% versus Friday’s close.

While there might have been an element of the lull before the storm in markets yesterday with a packed rest of the week calendar ahead of us, if you did have to point the finger then the ever so slight risk-off tone could be attributed to comments made by China President Xi Jinping at a seminar of provincial leaders and ministers in Beijing. He said that “the (Communist) Party is facing long-term and complex tests in terms of maintaining long-term rule, reform and opening-up, a market-driven economy, and within the external environment”. The President also said that “the party is facing sharp and serious dangers of a slackness in spirit, lack of ability, distance from the people, and being passive and corrupt”. To counter all this Xi signalled that China will maintain economic operations “within a reasonable range”. This all appeared largely consistent with previous comments but adds to the slew of slowdown concerns coming from China now. On that note, post yesterday’s data, our Chinese economists reiterated their forecasts for GDP growth to fall to as low as 5.9% in Q2 before rebounding post policy loosening in March. See their report here.

Elsewhere, the IMF’s latest global growth forecasts were released yesterday. The Fund now expects 2019 growth to be 3.5% which compares to the 3.7% forecast made in October. That would also mark the slowest rate of growth in three years while the 2020 forecast now is for 3.6%, a small downward revision of one-tenth. At a regional level the forecast for emerging markets was revised down two-tenths this year to 4.5% while advanced economies are expected to grow 2.0% (one-tenth downward revision). The US is expected to grow 2.5% and 1.8% this year and next (both unrevised) which is broadly in line with the consensus on Bloomberg.

Finally, as for the day ahead, it’s a busy morning for data here in the UK with November and December employment stats due out (no change in the 4.1% unemployment rate or 3.3% yoy average weekly earnings prints expected) and December public sector net borrowing data. Also due out is the January ZEW survey in Germany. This afternoon in the US the lone release is December existing home sales which is expected to show a small decrease (-1.5% mom) during the month. Elsewhere the annual Davos shindig kicks off today while the earnings highlights include Johnson & Johnson and IBM in the US, and UBS in Europe.

via RSS http://bit.ly/2DsXZaN Tyler Durden