Authored by Sven Henrich via NorthmanTrader.com,

Will dovish central bankers trump fundamentals? Do fundamentals actually matter? Answers to these questions will decide the direction of the larger price range in 2019.

What have we learned over the past 5 weeks since that Christmas low? Everybody and their mother wants to sweet talk these markets. From the Mnuchin emergency liquidity calls with bankers over Christmas, to the China record liquidity injections, to the FOMC parading sudden flexibility on their balance sheet and a halt in rate hikes, to daily smooth talking about a China deal (think Kudlow, Trump, etc) whenever needed.

So what if $INTC missed last night? Or that Germany’s IFO and sentiment data coming out today was brutal or that the German government is reducing GDP growth down to 1% for 2019? Or that China growth keeps faltering? Or that the longest government shutdown in history keeps shaving off points off of Q1 GDP? Yet markets keep rising.

What’s the message? That fundamentals don’t matter, or even earnings.

Only liquidity…

No wonder everybody is in denial about the deteriorating macro picture. Because the Fed’s got the market’s back so the thinking goes. Again.

Indeed today the WSJ published an article about the Fed considering stopping QT altogether further juicing futures. In 2018 they were on auto pilot. The market dropped 20% and then Powell announced he was going to “flexible’ on the balance sheet on January 4th. And now they’re considering stopping it altogether. It took only 6 weeks from President Trump’s twitter demand for the Fed stop the “50Bs” to the Fed now openly considering it.

And so the track record remains the same. When markets wobble central bankers react. See central bankers (and the ECB also made this very clear yesterday, as did the SNB today) will not stop being dovish. They will do whatever it takes to keep sentiment up or to improve it. The notion of central banks returning to a normalized policy has been shelved a long time ago. They can’t and they won’t.

Investors have indeed gotten the message:

“The ticket to outperformance this year is as simple as betting the Federal Reserve will temper its tightening plan & do the bull market’s bidding, according to investors that help oversee a combined $1.4 trillion” The Fed is “at the mercy of the markets…That’s why we have re-instigated a risk position” across stocks in the U.S. and emerging markets.”

Well, there you have it ladies and gentlemen. The bull case in a nut shell. Dovish central banks capitulating on promises to reduce their balance sheets and/or to raise rates.

Add $1.3 trillion in the form of buybacks and dividends in 2019 and perhaps a China deal and the bull market is off to the races.

That’s the theory.

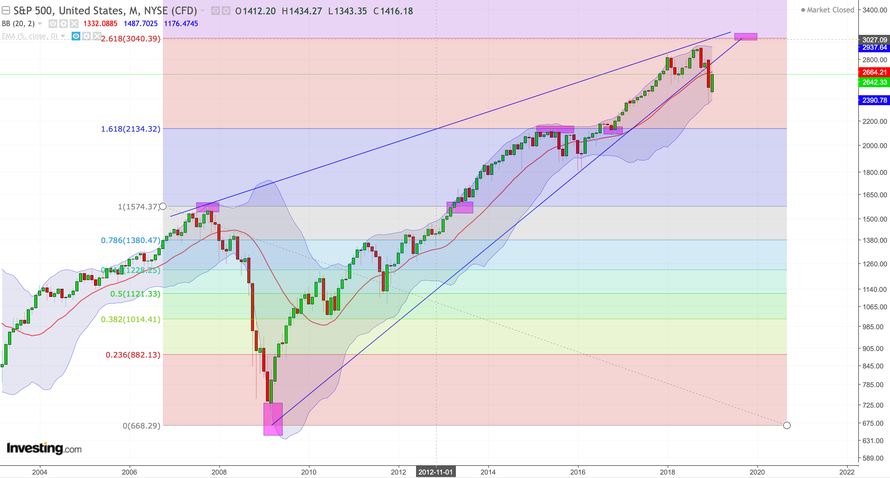

And even on the chart front one could make a very bullish case. Let me show you.

Consider this potential inverse on the $ES:

It seems incredulous to think we’ll see an inverse out of this steep V without so much of a basic .236 fib retrace of the original rally since the December lows, but there it is. But it is an unconfirmed pattern.

Ironically the theoretical technical target of this pattern? 3033. Not kidding, which bring us right back to the big 2.618 fib I’ve been discussing since January of 2018.

The broken trend line wouldn’t even matter, markets could keep hugging the underside of that trend line all the way into September 2019 and just relentlessly crawl higher. After all we’ve seen that movie before.

Does this confirm the bull case? Not at this point. Last weekend I outlined the technical trigger as to when markets would successfully signal a bullish confirmation. They haven’t done so yet.

Remember there is a reason for all this sweet talking and liquidity injections: Fundamentals are deteriorating and the journey of 2019 is on this road of discovery: Will fundamentals outweigh policy intervention? In the past policy intervention has succeeded as plenty of new liquidity was coming into the system. Now, other than China and ongoing Japan action, less new liquidity is coming in and the FOMC is still taking it out at least until they confirm they stop and, even if they stop, they are not adding. And neither is the ECB. Yet.

Also: The deterioration in fundamentals may be exacerbated by trade tensions, but they are not the root cause of them and that may ultimately be the mistake bulls are making here no matter all the efforts to jawbone markets higher. But we’ll see, this will be a multi-month long process, and we’re just at the beginning of it.

For now the empire has struck back, whether it’s enough remains to be seen.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News http://bit.ly/2FP2qPn Tyler Durden